Malted Wheat Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

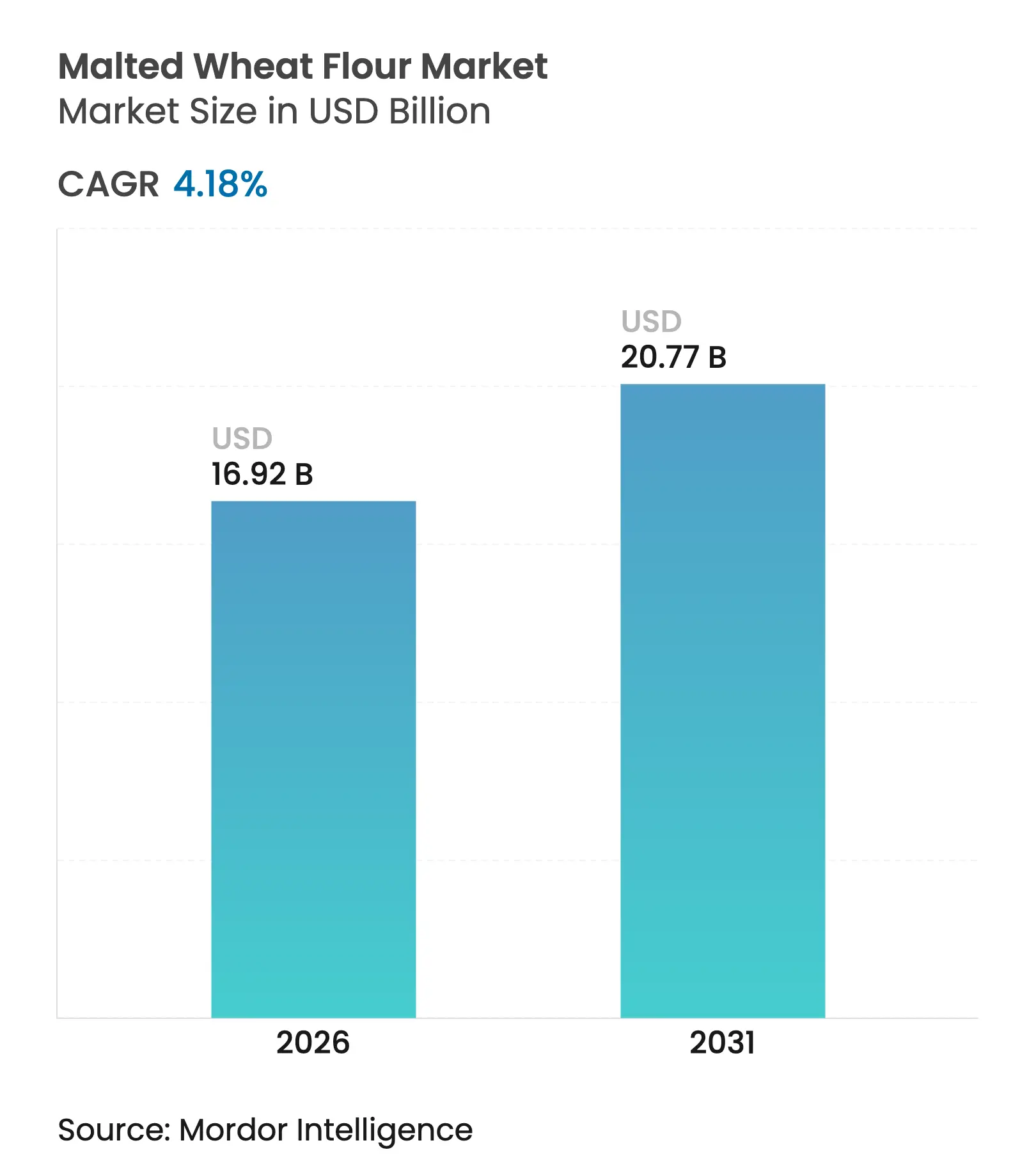

| Market Size (2026) | USD 16.92 Billion |

| Market Size (2031) | USD 20.77 Billion |

| Growth Rate (2026 - 2031) | 4.18 % CAGR |

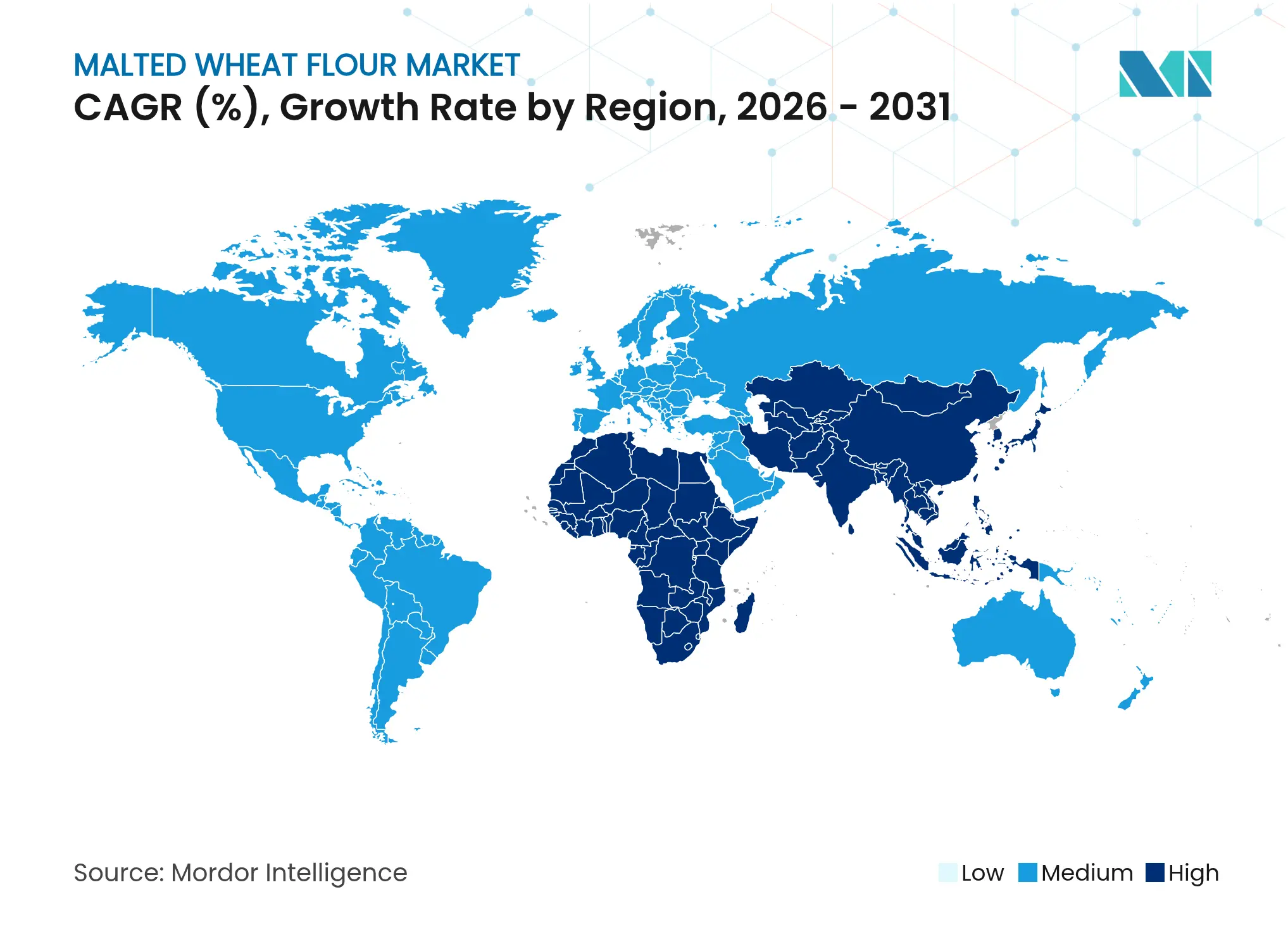

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Malted Wheat Flour Market Analysis by Mordor Intelligence

The global malted wheat flour market size was valued at USD 16.24 billion in 2025 and estimated to grow from USD 16.92 billion in 2026 to reach USD 20.77 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). The market growth is driven by increased adoption of clean-label formulations, growth in premium and artisanal bakeries, and broader applications in both alcoholic and non-alcoholic beverages. The FDA's 21 CFR 137.105 regulation ensures the ingredient complies with standard flour requirements while supporting natural enzyme solution demand [1]U.S. Food and Drug Administration, “Cereal Flours and Related Products—Standards of Identity,” ecfr.gov. While Europe dominates consumption, the Asia-Pacific region shows the highest growth rate due to increased distilling investments and local supply expansion. The USDA's projected decrease in wheat prices for 2025/26 benefits processor margins, despite varying farming costs due to fertilizer price fluctuations [2]USDA Economic Research Service, “Wheat Outlook,” ers.usda.gov.

Key Report Takeaways

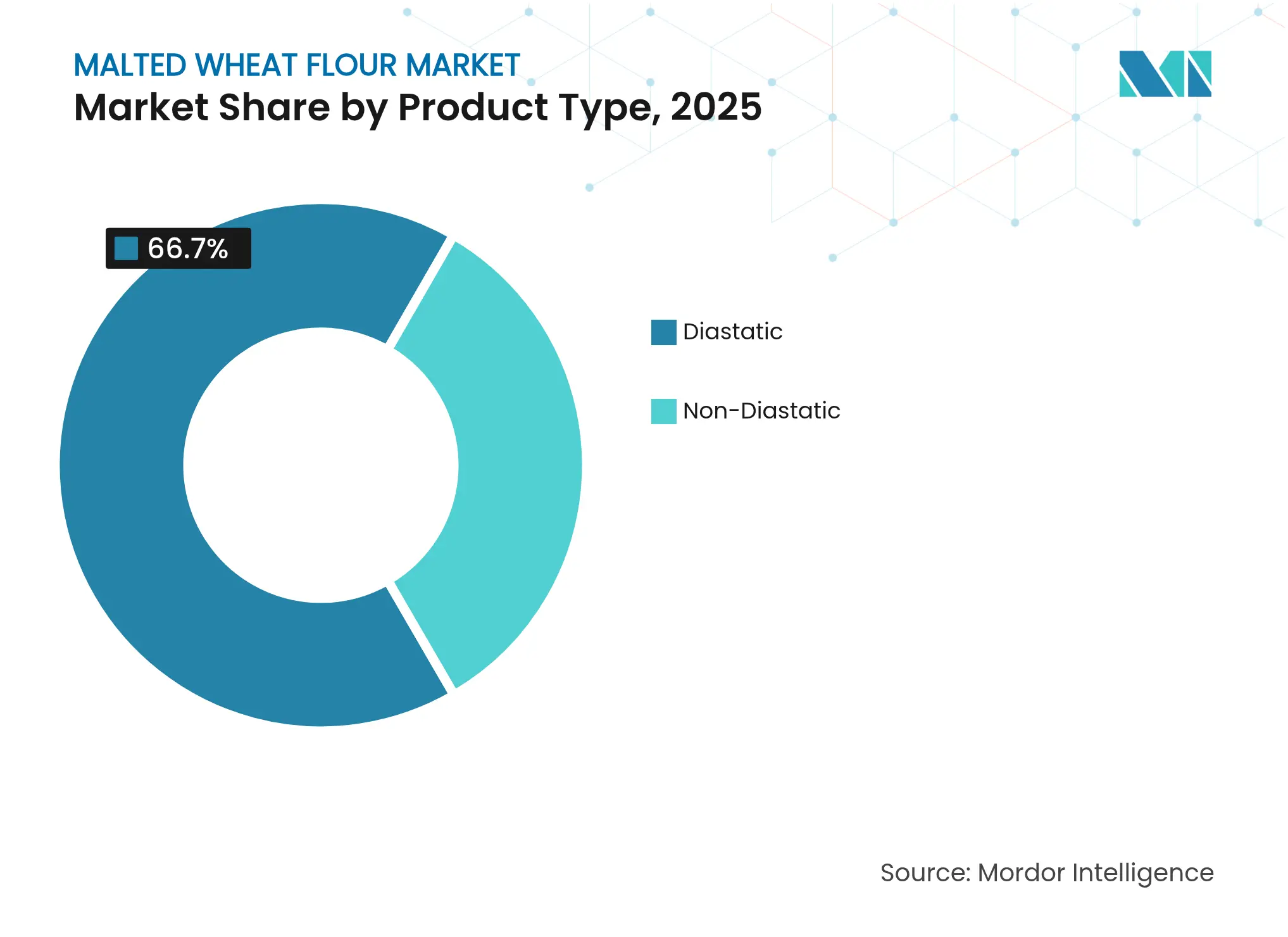

- By product type, diastatic variants led with 66.70% 2025 malted wheat flour market share and are forecast to grow at a 3.78% CAGR to 2031, while non-diastatic products post the fastest 6.01% CAGR in the segment.

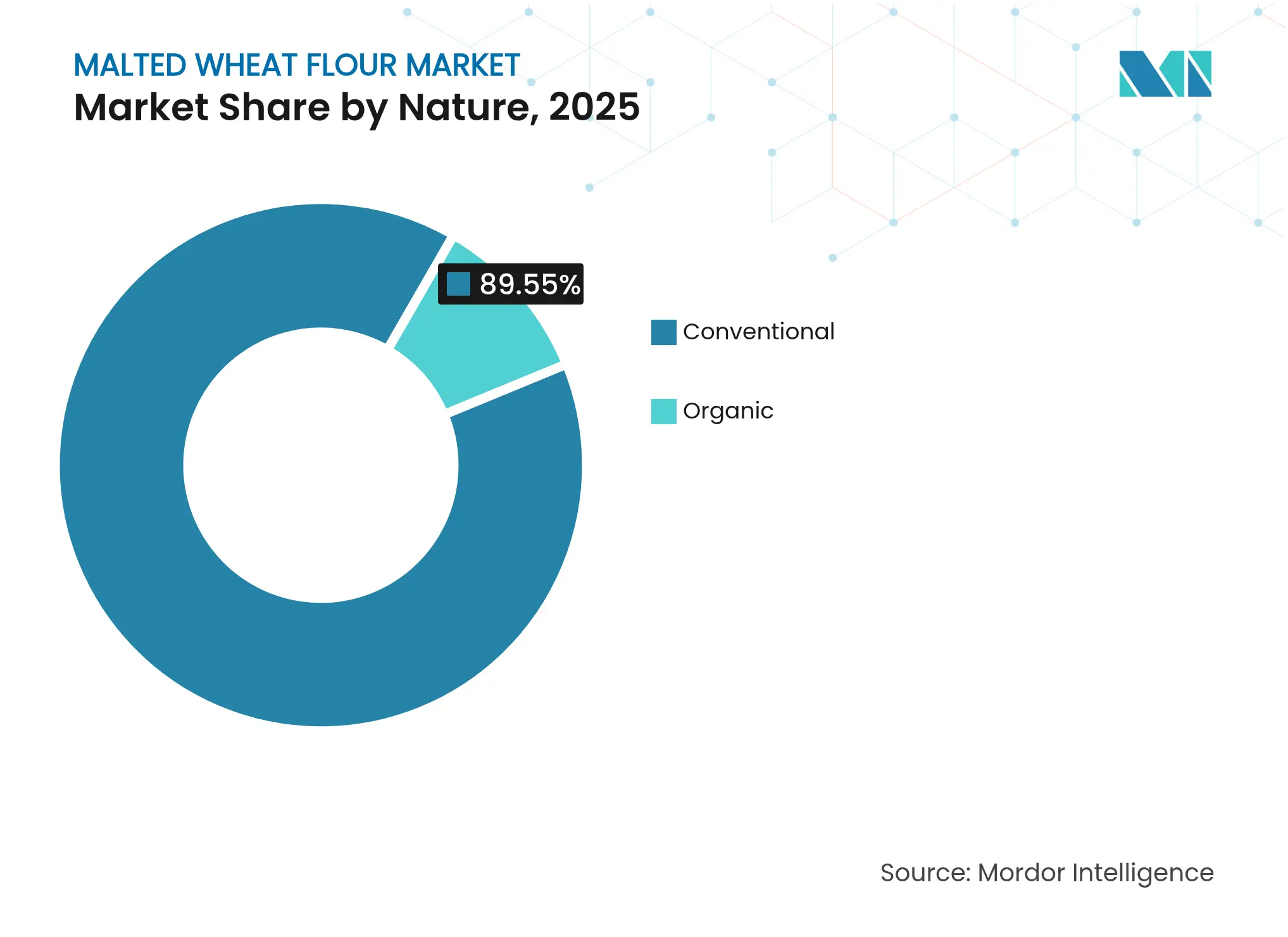

- By nature, conventional products dominated with an 89.55% 2025 share, but organic offerings record the highest 7.02% CAGR through 2031 in North America.

- By application, bakery and confectionery captured 65.90% of the 2025 malted wheat flour market size and will expand at 3.62% CAGR, whereas beverages chart the quickest 6.55% CAGR, most notably in Asia-Pacific.

- By geography, Europe retained 31.40% of the 2025 malted wheat flour market size, yet Asia-Pacific advances at a 6.63% CAGR on the back of large-scale malt distilling projects in India.

- Company concentration is moderate; the top five maltsters hold a combined 55-60% share of global capacity, led by Soufflet-United Malt, Boortmalt, and Malteurop.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Malted Wheat Flour Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Clean-label and naturally processed ingredients Clean-label and naturally processed ingredients | +1.2% | North America, EU strongest | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:North America, EU strongest | Impact Timeline:Medium term (2-4 years) |

Premium and artisanal bakery expansion Premium and artisanal bakery expansion | +0.8% | North America, Europe, APAC cities | Long term (≥ 4 years) | |||

Nutritionally rich, fiber-enhanced flour demand Nutritionally rich, fiber-enhanced flour demand | +0.7% | Developed markets | Medium term (2-4 years) | |||

Ready-to-eat and frozen food flavor & texture enhancement Ready-to-eat and frozen food flavor & texture enhancement | +0.6% | North America, Europe | Short term (≤ 2 years) | |||

Malt-based nutritional beverages in developing regions Malt-based nutritional beverages in developing regions | +0.5% | APAC core, MEA and Latin America | Long term (≥ 4 years) | |||

Brewing and distilling functional advantages Brewing and distilling functional advantages | +0.4% | Established brewing hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Clean-Label and Naturally Processed Ingredients

The growing consumer preference for natural ingredients has led food manufacturers to replace chemical enzymes with malted wheat flour. Its Generally Recognized As Safe (GRAS) status and exemption from additional labeling requirements make it an effective clean-label processing aid. Research indicates that germination increases resistant starch and antioxidant content while maintaining proper dough handling properties, benefiting various clean-label snacks and breads. Bakery companies are now incorporating malt-derived sweeteners instead of refined sugars in their products to improve nutritional value and meet consumer demands [3]Escuela Superior Politécnica del Litoral, “Effect of Germination on Wheat Flour Antioxidants,” espol.edu.ec.

Growth in Premium and Artisanal Bakery Segments Using Specialty Flours

The demand for specialty malted flours is increasing due to artisanal bakeries seeking distinctive flavors and improved fermentation properties. British maltsters are reintroducing traditional barley varieties to create unique flavor profiles for craft brewing and artisanal baking. Consumers are willing to pay premium prices for authentic, locally-sourced ingredients with clear origins. The growth of artisanal bakeries is supported by urbanization and rising disposable incomes in emerging markets, where Western-style bakery products are becoming more popular. Weyermann's range of more than 90 specialty malt varieties indicates strong market demand for diverse products that allow bakers to develop unique flavor characteristics.

Rising Consumer Interest in Nutritionally Rich and Fiber-Enhanced Flour Alternatives

The growing consumer focus on health and nutrition has increased the demand for malted wheat flour due to its enhanced protein digestibility and mineral bioavailability. Malted wheat flour helps address micronutrient deficiencies through improved iron and zinc absorption compared to regular flour. During the malting process, enzymes break down phytic acid and antinutrients, which increases the availability of essential minerals and B-vitamins. This nutritional profile aligns with current dietary preferences for plant-based proteins and functional foods, creating opportunities in health-focused retail segments. The breakfast cereal category demonstrates this trend, with protein-enriched formulations containing malted ingredients showing double-digit growth.

Expanding Application in Ready-to-Eat and Frozen Food Products for Enhanced Flavor and Texture

Frozen food manufacturers use malted wheat flour to improve texture retention and flavor development during storage, addressing quality degradation that affects product shelf life. The ingredient's enzyme activity enhances Maillard reactions during reheating, improving color and flavor in frozen bakery products. Malt extract serves multiple functions beyond brewing, including moisture retention and texture enhancement in breakfast cereals and snacks. In ready-to-eat products, malted wheat flour helps maintain crispness and prevent staling, particularly in products requiring extended distribution. Cereal manufacturers are expanding their products from breakfast items to all-day snacks, necessitating ingredients that preserve texture across different consumption occasions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Higher cost compared to conventional wheat flour Higher cost compared to conventional wheat flour | -0.9% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Global, particularly price-sensitive emerging markets | Impact Timeline:Short term (≤ 2 years) |

Limited consumer awareness of malted wheat flour and its benefits Limited consumer awareness of malted wheat flour and its benefits | -0.6% | Developing regions, rural markets | Medium term (2-4 years) | |||

Inapplicability in gluten-free product formulations due to gluten content Inapplicability in gluten-free product formulations due to gluten content | -0.4% | Global, concentrated in health-conscious segments | Long term (≥ 4 years) | |||

Competition from enzyme additives and other flour types Competition from enzyme additives and other flour types | -0.3% | Industrial applications, cost-sensitive segments | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Higher Cost Compared to Conventional Wheat Flour

The malted wheat flour market faces pricing challenges due to a 15-25% premium over conventional flour alternatives. This price differential limits adoption among cost-sensitive food manufacturers, especially in emerging markets with high price elasticity. The malting process requires additional energy, labor, and time compared to standard flour milling, resulting in inherent cost disadvantages that restrict market penetration in price-competitive segments. In 2024, malting barley supply constraints, caused by declining beer sales and contract uncertainties, increase input costs for specialty flour producers. The USDA projects lower wheat prices for 2025/26, which may improve margins for processors who secure long-term supply contracts. While cost remains a significant barrier, it creates opportunities for manufacturers to develop premium market segments where functional benefits support higher pricing.

Limited Consumer Awareness of Malted Wheat Flour and Its Benefits

The lack of consumer understanding about malted wheat flour's functional and nutritional benefits restricts market growth, especially in regions where traditional flour usage dominates food preparation. Malted wheat flour has not achieved the same consumer recognition as other alternative flours like almond or coconut, despite its enhanced enzymatic properties and nutritional value. Its primary use as a processing aid rather than a direct flour substitute creates challenges in marketing and consumer communication. While educational programs targeting food service professionals and home bakers could increase awareness and adoption, market penetration faces significant barriers in developing regions where traditional cooking methods and ingredient preferences are well-established. These markets require long-term marketing investments and culturally adapted approaches to achieve substantial market presence.

Segment Analysis

By Product Type: Diastatic Dominance Faces Non-Diastatic Innovation

Diastatic malted wheat flour accounts for 66.70% of global volume in 2025, driven by its consistent enzyme activity that optimizes fermentation in industrial bread production. Industrial craft bakers prefer it for reducing proof times and increasing loaf volume without artificial additives. Studies show that incorporating 0.5-2% diastatic malt increases gas retention by 18-22% during dough development, resulting in softer crumb texture after baking.

Non-diastatic varieties are growing at a 6.01% CAGR through 2031, primarily due to increased demand in confectionery coatings and frozen products where enzyme activity could cause excessive fermentation. Manufacturers offer toasted, caramel, and chocolate malt varieties that enhance flavors in premium cookies, energy bars, and craft spirits. These specialty products command prices 30-40% higher than conventional flour blends, compensating for lower production volumes.

Note: Segment shares of all individual segments available upon report purchase

By Application: Bakery Dominance Pressured by Beverage Innovation

The bakery and confectionery segment accounted for 65.90% of total malted wheat flour consumption in 2025. This dominance stems from its widespread use as a fermentation improver in both industrial and artisanal bread production. The natural amylase activity in malted wheat flour extends product shelf life, while its applications in clean-label cakes and laminated pastries reinforce its market position.

The beverages segment is experiencing the highest growth rate at 6.55% CAGR. This growth is primarily due to increased demand for non-alcoholic beers and malt-based functional drinks in Asia. Equipment manufacturers now provide modular brewhouses designed for wheat malt spirit production, benefiting regional craft distillers. The segment's expansion also includes plant-based nutritional shakes that utilize malt's natural sweetness and B-vitamin properties.

By Nature: Conventional Leadership Challenged by Organic Acceleration

Conventional malt production accounts for 89.55% of the 2025 supply, supported by established infrastructure and economies of scale. Major multinational maltsters utilize integrated global sourcing networks to maintain stable costs and ensure consistent supply throughout the year. This reliability appeals to manufacturers in the bread, snack, and beer industries.

The organic malt segment, while representing a smaller share, is growing at a 7.02% CAGR, supported by increased U.S. organic wheat production and facility transitions like Bay State Milling's Platteville plant. Consumer interest in transparent supply chains and health benefits drives acceptance of 35-40% price premiums. Companies securing certified organic farmland and establishing traceable supply chains can achieve higher profit margins.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe held 31.40% of the global malted wheat flour market in 2025, maintaining its position as the largest regional market. Germany, Belgium, and the UK's established brewing industries provide consistent demand. However, climate-related yield variations in barley and wheat have increased supply risks, prompting manufacturers to expand sourcing options and implement forward contracts. The region continues to see infrastructure development, as evidenced by Malteries Soufflet's acquisition of UK specialty malt facilities, which enhances premium production capacity and implements energy-efficient kilning processes.

The Asia-Pacific region demonstrates the highest growth rate at 6.63% CAGR through 2031. The expansion of India's whisky industry serves as a primary growth driver, with Pernod Ricard's INR 1,785 crore Nagpur distillery expected to increase wheat malt consumption. INTERMALT's Vietnam facility supports the expanding craft beer market. China and Indonesia's growing middle-class population increases premium bread consumption, while regional bakeries incorporate malted wheat flour for product differentiation.

North America exhibits consistent growth, driven by the expansion of artisanal bakeries and brewers' preference for local wheat malts to reduce transportation emissions. USDA organic transition initiatives help address certification constraints and support domestic organic supply. The Middle East and Africa regions, while emerging, demonstrate development potential through new facilities in Ethiopia and South Africa, indicating progress toward regional production independence.

Competitive Landscape

Market Concentration

The Malted Wheat Flour Market is moderately consolidated. ADM (Archer Daniels Midland) and Malteurop lead the global malted wheat flour market, together holding a significant share and influencing the competitive dynamics. Muntons plc and Ireks GmbH have a notable presence, primarily affecting specialized or regional segments.

Additionally, the scale of operations allows these major producers to secure multi-year contracts with global brewers and bakery conglomerates, offering stability in raw material prices and extensive logistics networks. Regional companies like Weyermann, Crisp Malt, and Simpsons maintain their market position through specialty malt portfolios, flexible production volumes, and close customer relationships. Recent strategic developments include Crisp Malt's bulk-silo expansion in 2024 to support craft distillers and Weyermann's introduction of heirloom wheat malt products for premium bakeries.

Technology investments create competitive differentiation in the market. Major producers implement CO₂ recovery systems, low-energy germination chambers, and digital twin monitoring to reduce operational costs and meet sustainability requirements. Additionally, research and development in enzyme modulation optimizes diastatic performance for specific flour combinations, enabling joint development initiatives with multinational bakery companies seeking clean-label products.

Malted Wheat Flour Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Soufflet Malt and Heineken formed a partnership where Soufflet Malt will invest EUR 100 million (USD 108.51 million) to construct a malting facility in South Africa to supply malt to Heineken.

- January 2025: Viking Malt has joined the Sustain-a-bite EU project, a collaborative initiative focused on addressing critical challenges in food production and consumption systems. The project specifically targets resource efficiency and environmental sustainability in the food supply chain.

- November 2024: Simpsons Malt Limited received recognition for its supply chain sustainability practices through the Farm Sustainability Assessment (FSA), a globally recognized framework for supply chain collaboration.

Table of Contents for Malted Wheat Flour Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand for clean-label and naturally processed ingredients

- 4.2.2Growth in premium and artisanal bakery segments using specialty flours

- 4.2.3Rising consumer interest in nutritionally rich and fiber-enhanced flour alternatives

- 4.2.4Expanding application in ready-to-eat and frozen food products for enhanced flavor and texture

- 4.2.5Increasing penetration of malt-based nutritional beverages in developing regions

- 4.2.6Functional advantages of malted wheat flour in brewing and distilling industries

- 4.3Market Restraints

- 4.3.1Higher cost compared to conventional wheat flour

- 4.3.2Limited consumer awareness of malted wheat flour and its benefits

- 4.3.3Inapplicability in gluten-free product formulations due to gluten content

- 4.3.4Competition from enzyme additives and other flour types

- 4.4Supply-Chain Analysis

- 4.5Regulatory and Technological Outlook

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Diastatic

- 5.1.2Non-Diastatic

- 5.2By Nature

- 5.2.1Conventional

- 5.2.2Organic

- 5.3By Application

- 5.3.1Bakery and Confectionery Products

- 5.3.2Beverages

- 5.3.3Snacks and Cereals

- 5.3.4Others

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2Europe

- 5.4.2.1Spain

- 5.4.2.2United Kingdom

- 5.4.2.3Germany

- 5.4.2.4France

- 5.4.2.5Italy

- 5.4.2.6Russia

- 5.4.2.7Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1Saudi Arabia

- 5.4.5.2United Arab Emirates

- 5.4.5.3South Africa

- 5.4.5.4Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1ADM (Archer Daniels Midland)

- 6.4.2Crisp Malt

- 6.4.3Ireks GmbH

- 6.4.4Muntons plc

- 6.4.5Malteurop

- 6.4.6Great Western Malting Co.

- 6.4.7Axéréal

- 6.4.8Viking Malt

- 6.4.9Malteries Soufflet

- 6.4.10Simpsons Malt Ltd.

- 6.4.11Barmalt

- 6.4.12Weyermann Specialty Malts

- 6.4.13Briess Malt and Ingredients

- 6.4.14Dingemans Malt

- 6.4.15PMV Maltings Pvt. Ltd.

- 6.4.16Imperial Malts Ltd.

- 6.4.17Castle Group

- 6.4.18Mahalaxmi Malt Products Private Limited

- 6.4.19Central Milling

- 6.4.20Malt Products Corporation

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Malted Wheat Flour Market Report Scope

The global malted wheat flour market is segmented by application and geography. By application, the market is segmented into beverages and food; and by geography into North America, Europe, Asia-Pacific, South America and Middle East and Africa.