Wheat And Rice Flour Substitute-Resistant Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

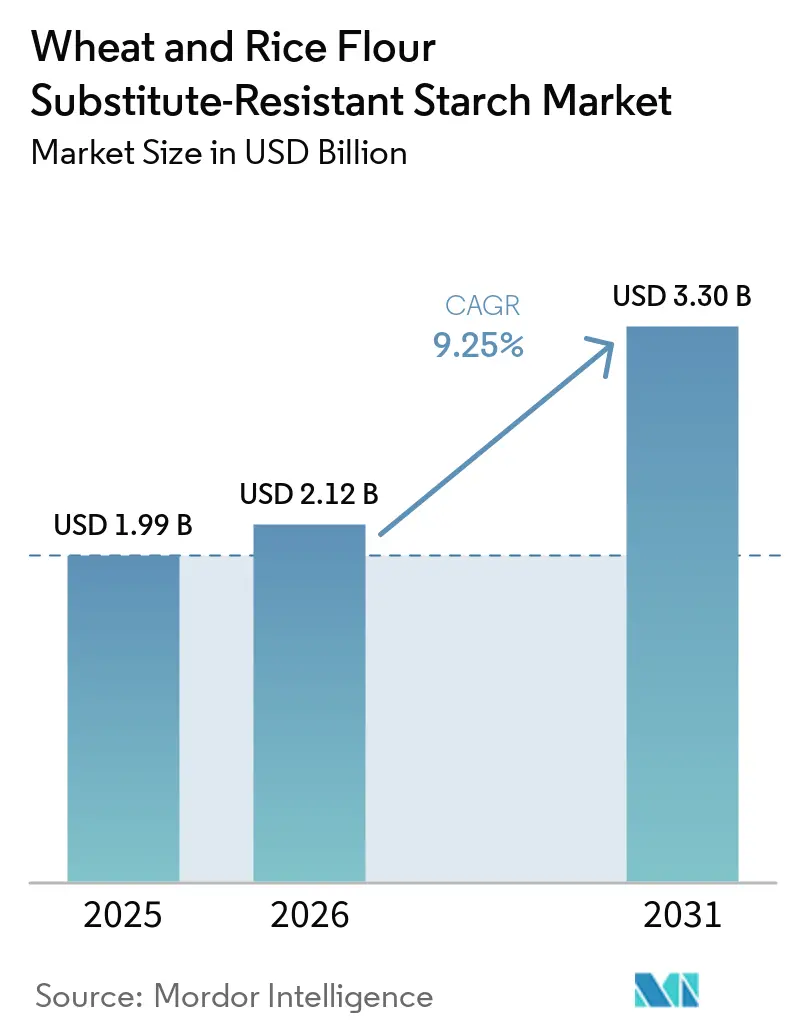

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 3.30 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wheat And Rice Flour Substitute-Resistant Starch Market Analysis by Mordor Intelligence

The Wheat and Rice Flour Substitute-Resistant Starch market was valued at USD 1.99 billion in 2025 and reached USD 2.12 billion in 2026, and is projected to climb to USD 3.3 billion by 2031, registering a 9.25% CAGR over 2026-2031. Steady growth stems from clean-label reformulation pressures, mounting regulatory support for metabolic health claims, and growing clinical validation of prebiotic benefits. Large Consumer Packaged Goods (CPG) companies are shifting their fiber strategies toward ingredients that deliver functional benefits without texture penalties, positioning resistant starch as a practical alternative to bran or inulin. In North America, the United States Food and Drug Administration’s (FDA) qualified health claim for high-amylose maize resistant starch is accelerating mainstream adoption, while Asia-Pacific governments are mandating higher dietary-fiber intake, creating tailwinds for suppliers able to scale regional production. Meanwhile, volatile crop yields for cassava and potato keep cost premiums elevated, reinforcing the need for diversified sourcing and technological advances that preserve flavor and structure at higher inclusion levels.

Key Report Takeaways

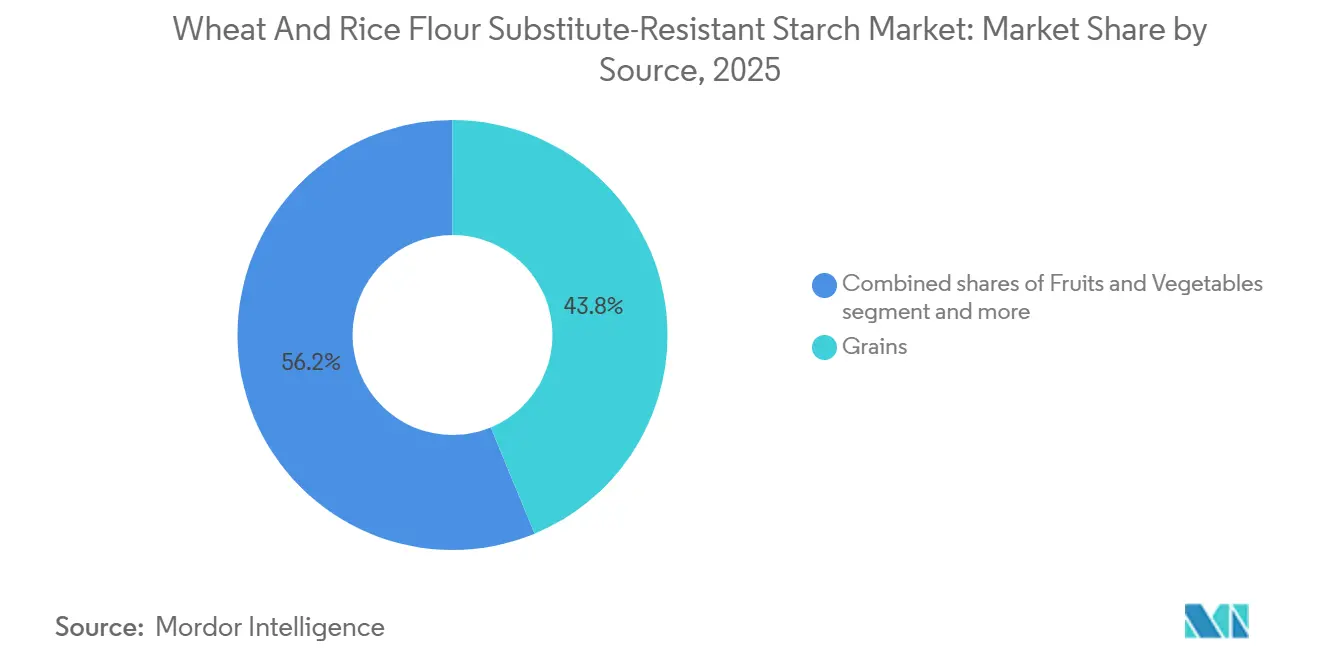

- By source, grains led with 43.76% of the resistant starch market share in 2025, while fruits and vegetables are forecast to advance at a 9.15% CAGR through 2031.

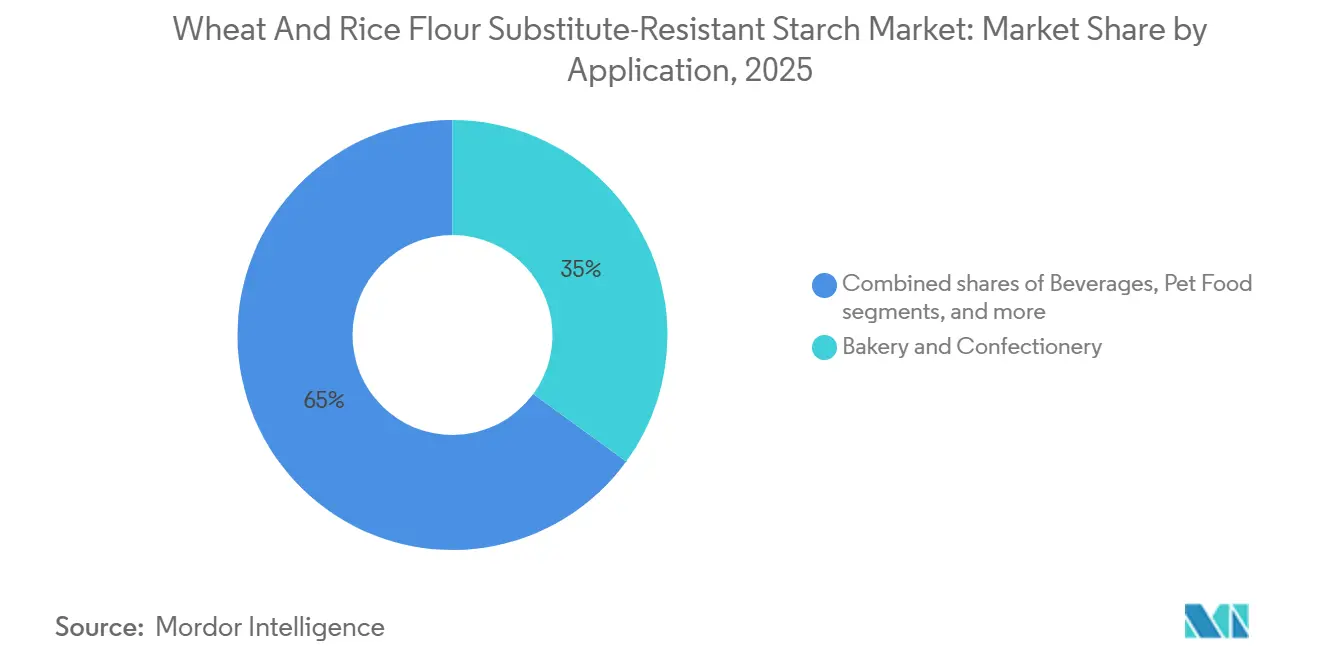

- By application, bakery and confectionery captured 35.02% share of the resistant starch market size in 2025, and beverages are projected to expand at a 10.05% CAGR from 2026 to 2031.

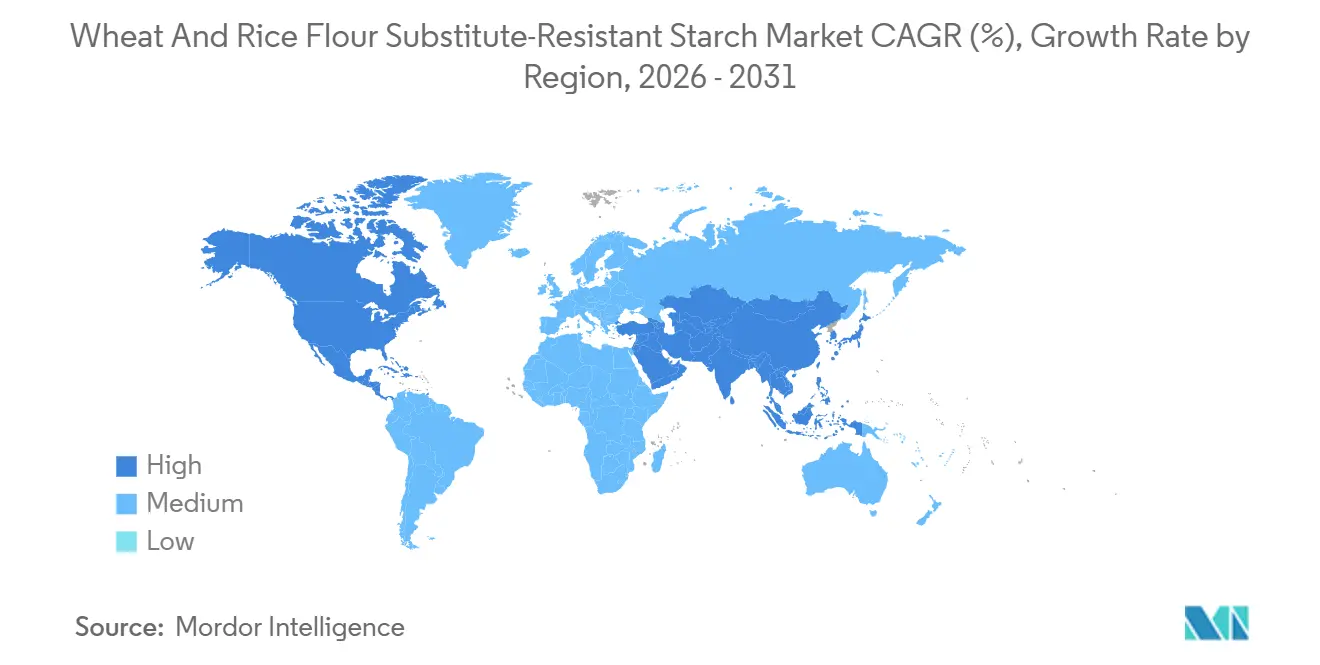

- By geography, North America held 32.98% of the resistant starch market share in 2025, whereas Asia-Pacific is poised for the fastest expansion at an 11.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wheat And Rice Flour Substitute-Resistant Starch Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for low-glycemic, high-fiber staple replacements | +2.1% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Clean-label reformulation push from bakery and snack giants | +1.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expanding clinical evidence for gut-microbiome benefits | +1.5% | Global, particularly North America and Europe where prebiotic awareness is highest | Long term (≥ 4 years) |

| Government fiber-enrichment mandates in Asia-Pacific | +2.3% | Asia-Pacific core (China, Japan, South Korea), spill-over to Southeast Asia | Medium term (2-4 years) |

| Surge in gluten-free diets and diagnosed coeliac disease | +0.9% | North America, Europe, Australia | Short term (≤ 2 years) |

| Carbon-footprint labeling favoring resistant starch over refined flour | +0.6% | North America, EU (pending regulatory adoption) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for low-glycemic, high-fiber staple replacements

Escalating global type 2 diabetes prevalence has reframed fiber fortification as a metabolic imperative. The United States Food and Drug Administration’s (FDA)-qualified health claim granted in 2025 allows manufacturers to link high-amylose maize resistant starch to reduced diabetes risk on mainstream pantry items, turbo-charging commercial uptake. Milling innovators such as Bay State Milling parlayed the evidence into an American Heart Association Heart-Check certification for its HealthSense flour, demonstrating that intrinsic resistant starch can displace commodity white flour without sensory compromise. Brands now communicate glycemic moderation, weight-management, and “good source of fiber” messages in the same breath, crystallizing resistant starch as a strategic ingredient for staple reformulation. Adding to the momentum, the European Food Safety Authority[1]Source: Code of Federal Regulations, "Food Starch Modified", ecfr.govhas greenlit health claims for foods boasting at least 14% resistant starch content, offering a regulatory nod that could hasten commercial uptake across a spectrum of food categories.

Clean-label reformulation push from bakery and snack giants

Ingredient statements with recognizable plant sources rank high in shopper surveys, driving food manufacturers to substitute traditional texturizers with fibers that mirror refined-starch functionality. Unlike bran, inulin, or polydextrose, resistant starch provides body, viscosity, and moisture retention yet labels cleanly as “maize fiber,” “potato starch,” or “wheat starch”. Tate & Lyle’s PROMITOR soluble corn fiber withstands heat and pH variation at doses up to 40 g/day without gastrointestinal distress, enabling high-fiber claims in muffins, cookies, and cereal clusters that historically failed sensory panels when fortified with inulin. Limagrain’s LifyWheat raises the fiber content of tortillas from 1.4 g/100 g to over 6 g/100 g and improves Nutri-Score from C to B, illustrating how reformulators can unlock front-of-pack nutrition upgrades without process overhauls. Additionally, Ingredion Incorporated reported a 29% rise in adjusted operating income for Q3 2024, driven by strong sales in their Texture and Healthful Solutions segment, highlighting how ingredient suppliers are leveraging this reformulation trend.

Expanding clinical evidence for gut-microbiome benefits

Peer-reviewed research continues to validate the prebiotic benefits of resistant starch, strengthening its position in the global market and supporting associated health claims. Recent randomized controlled trials have demonstrated that consuming resistant starch type 3 significantly enhances gut health. This is achieved by increasing beneficial bacteria such as Bifidobacterium and Prevotella, as well as improving bowel movement frequency and stool consistency. Additionally, research has shown strong evidence for its role in managing type 2 diabetes. Resistant starch not only supports improved glycemic control but also helps protect kidney function, addressing critical health concerns in aging populations, as reported in the Journal of Diabetes Investigation. This robust evidence enables food companies to pursue health claim approvals, justify premium pricing, and build consumer trust through scientifically validated claims. Moreover, the fermentation of resistant starch produces short-chain fatty acids, which play a crucial role in reducing inflammation and regulating metabolic functions, providing food manufacturers with credible, science-based narratives to support their products.

Government fiber-enrichment mandates in Asia-Pacific

China's dual policy initiatives, the National Whole Grain Action Plan (2024-2035) and the Food and Nutrition Development Guideline (2025-2030), mandate dramatic increases in whole-grain and dietary fiber consumption to address a national fiber intake shortfall of approximately two-thirds below recommended levels (current average intake one-third of the 25-30 grams per day target). Officials cite evidence that consuming 50 grams of whole grains daily can reduce Type 2 diabetes risk by 25% and cardiovascular mortality by 20%, framing fiber enrichment as a public health imperative to combat "hidden hunger" (vitamin B1 intake at half the recommended levels). Japan's National Institutes of. These mandates are expected to drive institutional procurement of fiber-enriched ingredients and incentivize product development by domestic and multinational food manufacturers operating in the Asia-Pacific. The Organisation for Economic Co-operation and Development (OECD)[2]Source: OECD, "Regulatory governance of large-scale food fortification: A measurement framework", oecd.org underscores this trend, highlighting the cost-effectiveness of fortifying staple foods like flour and rice in its framework for the regulatory governance of large-scale food fortification. This lends policy support to strategies promoting the integration of resistant starch.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost versus conventional starch and flour | -1.4% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Raw-material supply fluctuations (corn, potato, banana) | -1.1% | Global, with acute exposure in Southeast Asia (cassava) and Europe (potato) | Medium term (2-4 years) |

| Consumer preference for traditional flours | -0.7% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Taste and texture challenges at high inclusion rates | -0.9% | Global, particularly in cost-sensitive bakery and pasta segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher cost versus conventional starch and flour

Resistant starch is priced 15-30% higher than commodity starches due to factors such as the use of specialized crop varieties, enzymatic modification, extrusion processes, and lower production volumes. As of April 2026, spot prices indicate Polish potato starch at EUR 0.85/kg, while resistant potato derivatives range between EUR 1.20 and 1.42/kg. While high-income consumers are willing to pay a premium for products with clinically supported claims, such as improved gut health or reduced glycemic response, adoption in emerging markets largely depends on government fortification mandates. These mandates can help offset the impact of higher end-product prices by subsidizing costs or incentivizing manufacturers to incorporate resistant starch into staple foods. These factors drive up production costs, which manufacturers must either absorb or transfer to consumers. Small and medium food manufacturers, unable to leverage procurement scale for better pricing, are disproportionately affected by these cost differences. This dynamic creates barriers to market entry, favoring large multinational food companies.

Raw-material supply fluctuations

Cassava requires processing within 24 hours of harvest, making its starch yields highly susceptible to disruptions caused by tropical storms, disease outbreaks, or transportation issues. These disruptions can lead to significant supply shortages and increased costs for tapioca-derived resistant starch. Additionally, European potato harvests have faced challenges due to recurring droughts in France and Germany, which have reduced overall yields. Supply chain restrictions in Belarus have further compounded the issue by redirecting resources to Russia, creating additional pressure on potato-based starch suppliers. To address these challenges, companies often rely on strategies such as multi-origin sourcing, contract farming, and diversifying their supplier base. However, despite these efforts, crop variability and unpredictable weather patterns remain persistent risks, making it difficult for suppliers to secure stable, long-term contracts and maintain consistent pricing. The concentration of production in a few countries increases the risk of supply disruptions. Export restrictions and changes in trade policies can result in sudden constraints on availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Grains Retain Pole Position while Fruits and Vegetables Accelerate

Grains delivered 43.76% of the resistant starch market share in 2025, anchored by high-amylose maize RS2 (Resistant Starch 2) and emerging high-amylose wheat platforms. Ingredion’s HI-MAIZE underpins the only Food and Drug Administration (FDA)-qualified diabetes-risk claim, giving grain-derived fibers a regulatory edge. High-amylose wheat flour products such as HealthSense, LifyWheat, and Amuleia let bakers swap 1:1 for white flour, boosting intrinsic fiber without retooling plants or recipes. Tubers and roots fill gluten-free or allergen-avoidance niches, but price volatility often undercuts volume growth.

Fruits and vegetables, led by upcycled potato and green-banana sources, are on track for a 9.15% CAGR over 2026-2031. Solnul potato starch, certified upcycled and FODMAP (Fermentable Oligosaccharides, Disaccharides, Monosaccharides and Polyols) friendly, hit the European market in 2026 through Lehvoss Nutrition, aligning gut-health efficacy with sustainability marketing. Meal-replacement innovators add green-banana flour for RS2 content that supports GLP-1 stimulation, catering to satiety-conscious consumers. Legume-based prototypes remain in early-stage piloting, yet present future dual protein-fiber advantages. from processing traits and nutritional benefits to patterns of consumer acceptance.

By Application: Bakery Commands Revenue, Beverages Lead Growth

The bakery and confectionery segment accounted for 35.02% of the resistant starch market size in 2025. Products such as tortillas, breads, and cookies increasingly utilize high-amylose flours and modified starches to enhance fiber content with minimal impact on texture. For instance, Crespel & Deiters’ Lory Starch Elara enables a 20% flour replacement in buns and muffins, achieving “high fiber” standards without causing water-holding issues. This innovation allows manufacturers to meet consumer demand for healthier baked goods without compromising on quality or taste.

Beverages represent the fastest-growing application of resistant starch, with a projected CAGR of 10.05% through 2031. Shake brands like Supergut incorporate 15 g of resistant starch with protein to promote GLP-1 release and extend satiety for up to six hours, addressing the growing demand for functional beverages that support weight management and metabolic health. Tate & Lyle’s heat-stable PROMITOR allows ready-to-drink coffees and nutrition beverages to claim “good source of fiber” benefits without issues such as grittiness or viscosity changes, ensuring a smooth and enjoyable consumer experience.

Geography Analysis

North America accounted for 32.98% of the resistant starch market share in 2025, anchored by regulatory enablers and established health-claim infrastructure. The Food and Drug Administration's (FDA) June 2025 approval of a qualified health claim linking high-amylose maize resistant starch to reduced Type 2 diabetes risk unlocked differentiated labeling for conventional foods. Ingredion's HI-MAIZE, the subject of the Food and Drug Administration (FDA) petition supported by eight clinical trials, exemplifies how proprietary health claims can create competitive moats in commodity-adjacent ingredient markets. Bay State Milling's HealthSense high-fiber wheat flour achieved American Heart Association Heart-Check certification in 2025, becoming the first refined flour to meet American Heart Association heart-healthy standards and demonstrating resistant starch's capacity to bridge clinical nutrition and mainstream palatability. Consumer fiber awareness is elevated, 64% of Americans intentionally try to consume more fiber (2025 International Food Information Council, Food & Health Survey), yet only 5% meet recommended intake, creating a structural demand gap that resistant starch is positioned to fill through reformulation of everyday staples[3]Source: IFIC: "IFIC Spotlight Survey: Americans’ Perceptions Of Fiber & Whole Grains", ific.org.

Asia-Pacific is forecast to grow fastest at 11.35% CAGR during 2026-2031, propelled by government fiber-enrichment mandates and rising middle-class demand for functional foods. China's National Whole Grain Action Plan (2024-2035) aims to elevate whole grains' share of grain consumption from under 1% to a significant portion by 2035, with policy measures including public education, national standards development, and manufacturer competitiveness support, officials cite evidence that 50 grams of whole grains daily can reduce Type 2 diabetes risk by 25% and cardiovascular mortality by 20%. China's Food and Nutrition Development Guideline (2025-2030) sets per-capita annual consumption targets including 14 kilograms of legumes, 270 kilograms of vegetables, and 130 kilograms of fruit, with daily fiber targets of 25-30 grams, current average intake is one-third of recommended levels.

Europe exhibits moderate growth driven by clean-label trends, Nutri-Score optimization, and prebiotic awareness. Tate & Lyle invested EUR 25 Million (USD 27 Million) to expand PROMITOR soluble fiber production at its Boleráz, Slovakia facility, with first-phase production commencing mid-2024 to serve European and global customers. European fiber intake averages approximately 4 grams per day of resistant starch versus a recommended 20 grams per day, creating a structural consumption gap that ingredient suppliers are targeting through education and product innovation. South America and Middle East and Africa remain smaller markets with growth constrained by lower fiber awareness and price sensitivity, though institutional demand from government nutrition programs may catalyze adoption in select countries.

Competitive Landscape

The wheat and rice flour substitute resistant starch market exhibits moderate-to-high concentration, with established ingredient multinationals (Ingredion Inc., Tate & Lyle PLC, Cargill Incorporated, and others) defending share through capacity expansions, proprietary health claims, and vertical integration into high-amylose crop sourcing. Ingredion's June 2025 Food and Drug Administration (FDA)-qualified health claim for HI-MAIZE resistant starch and Type 2 diabetes risk reduction exemplifies how clinical investment can create a regulatory moat. The claim required submission of eight academic clinical trials and positions Ingredion as the sole supplier able to communicate this specific health benefit on conventional food packaging. Tate & Lyle's EUR 25 Million (USD 27 Million) Slovakia expansion for PROMITOR soluble fiber production (mid-2024 startup) and its 2020 acquisition of 85% stake in Chaodee Modified Starch (Thailand) signal strategic prioritization of specialty fibers and tapioca-based texturants to capture Asia-Pacific growth.

Smaller innovators are disrupting through high-amylose wheat platforms and upcycled sourcing. Arista Cereals' patented high-amylose wheat varieties (>50 patents, >20 years of research and development with Limagrain and CSIRO) deliver up to 10 times the fiber of conventional wheat via intrinsic resistant starch elevation, commercialized through regional milling partners (Bay State Milling, Limagrain Ingredients, Nisshin Flour Milling, Allied Pinnacle) that bypass incumbent starch suppliers' distribution channels Arista Cereals. MSP Starch Products' Solnul resistant potato starch, Upcycled Certified, FODMAP Friendly, gluten-free, glyphosate residue-free, Non-GMO Project Verified secured exclusive European distribution through LEHVOSS Nutrition in April 2026, positioning upcycled sourcing as a differentiated sustainability claim.

Technology deployment focuses on enzymatic modification, extrusion, and fermentation to improve resistant starch functionality and reduce sensory trade-offs at high inclusion rates, a 2025 review identified extrusion and heat/pressure processing as methods to alter dietary fiber molecular structure and increase resistance to digestion, though cost and scalability remain barriers to commercialization. Regulatory alignment with Food and Drug Administration (FDA) dietary fiber definitions and European Food Safety Authority (EFSA) health claim substantiation (such as European Food Safety Authority's (EFSA) 2011 authorization linking resistant starch to reduced postprandial glycemic response) is critical for market access and label differentiation.

Wheat And Rice Flour Substitute-Resistant Starch Industry Leaders

-

Ingredion Inc.

-

Tate & Lyle PLC

-

Cargill Inc.

-

MGP Ingredients

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: MSP Starch Products entered into an exclusive distribution agreement with Lehvoss Nutrition for Solnul resistant potato starch. The partnership aims to expand the availability of this ingredient, which is known for its gut-health benefits, in Germany and the United States. The product will primarily target applications in gut-health powders and meal replacements, catering to the growing demand for functional food products in these regions.

- July 2025: Brenntag Specialties expanded its distribution agreement with Royal Avebe to the United States, extending prior collaboration in Turkey, Benelux, Poland, United Kingdom, Ireland, Nordics, and Baltics. Brenntag will supply United States food and nutrition customers with Avebe's full specialty range of potato-based starches, functional proteins, and fibers.

- April 2025: BENEO inaugurated a EUR 50 million pulse-processing plant in Obrigheim, Germany, focusing on locally grown faba beans for high-quality food and feed ingredients. The facility operates on renewable energy with zero-waste approaches, addressing rising demand for plant-based proteins and sustainable ingredient sourcing.

Global Wheat And Rice Flour Substitute-Resistant Starch Market Report Scope

The Wheat and Rice Flour Substitute-Resistant Starch market encompasses resistant starch ingredients sourced from wheat, rice, and alternative materials. These ingredients are utilized as substitutes in food, beverage, nutraceutical, and industrial applications, driven by increasing demand for gluten-free, high-fiber, and low-glycemic products. The wheat and rice flour substitute-resistant starch market report is segmented by source, application, and geography. By source, the market is segmented into grains, fruits and vegetables, legumes and pulses, fruits and vegetables and novel bio-engineered sources. By application, the market is segmented into bakery and confectionery, cereals and snacks, pasta and noodles, beverages, dietary supplements, pet food, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market forecasts are provided in terms of value (USD).

| Grains |

| Tubers and Roots |

| Fruits and Vegetables |

| Legumes and Pulses |

| Novel Bio-engineered Sources |

| Bakery and Confectionery |

| Cereals and Snacks |

| Pasta and Noodles |

| Beverages |

| Dietary Supplements |

| Pet Food |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Source | Grains | |

| Tubers and Roots | ||

| Fruits and Vegetables | ||

| Legumes and Pulses | ||

| Novel Bio-engineered Sources | ||

| By Application | Bakery and Confectionery | |

| Cereals and Snacks | ||

| Pasta and Noodles | ||

| Beverages | ||

| Dietary Supplements | ||

| Pet Food | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the present size and projected growth of the resistant starch market?

The resistant starch market size was USD 2.12 billion in 2026 and is forecast to reach USD 3.3 billion by 2031, reflecting a 9.25% CAGR according to Mordor Intelligence.

Which application is expanding most quickly?

Beverages are projected to post the highest CAGR at 10.05% through 2031, led by functional shakes rich in resistant starch that support GLP-1-mediated satiety.

How do recent FDA actions influence category growth?

The agency’s June 2025 qualified health claim linking high-amylose maize resistant starch to lower type 2 diabetes risk permits on-pack messaging, accelerating mainstream reformulation in bread, pasta and cereal.

Which region is expected to deliver the fastest gains?

Asia-Pacific should record an 11.35% CAGR to 2031 as China and Japan implement dietary-fiber mandates that favor soluble resistant starch in mainstream products.

Page last updated on: