Malted Barley Flour Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

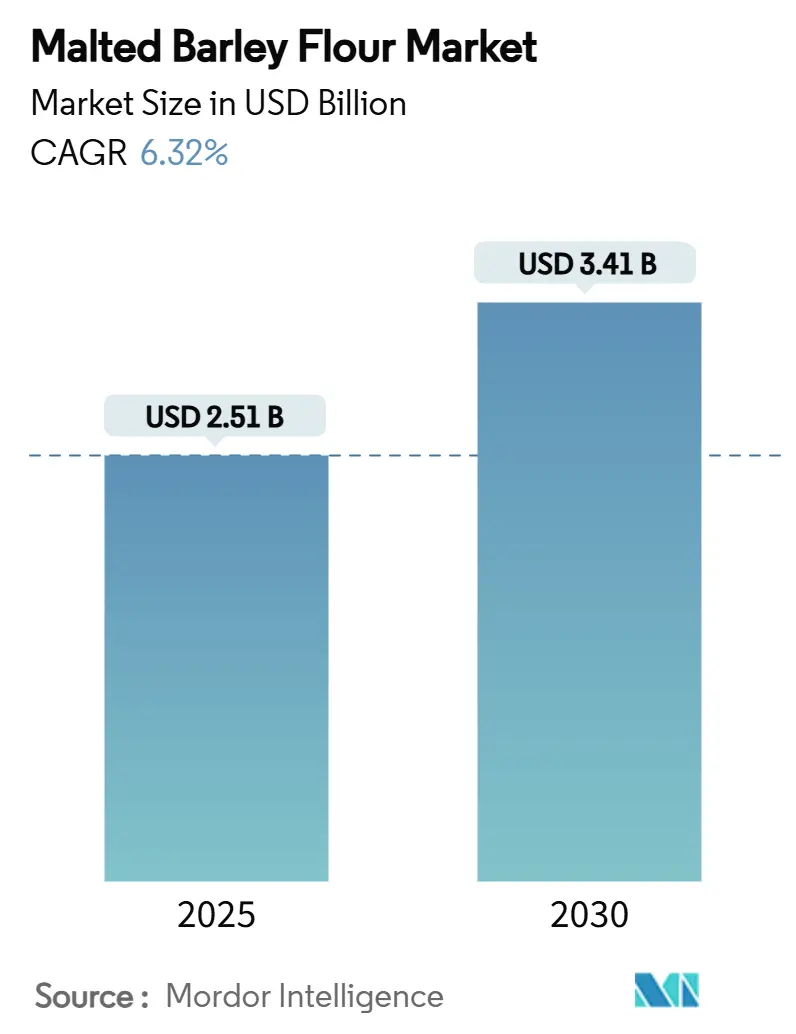

| Market Size (2025) | USD 2.51 Billion |

| Market Size (2030) | USD 3.41 Billion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

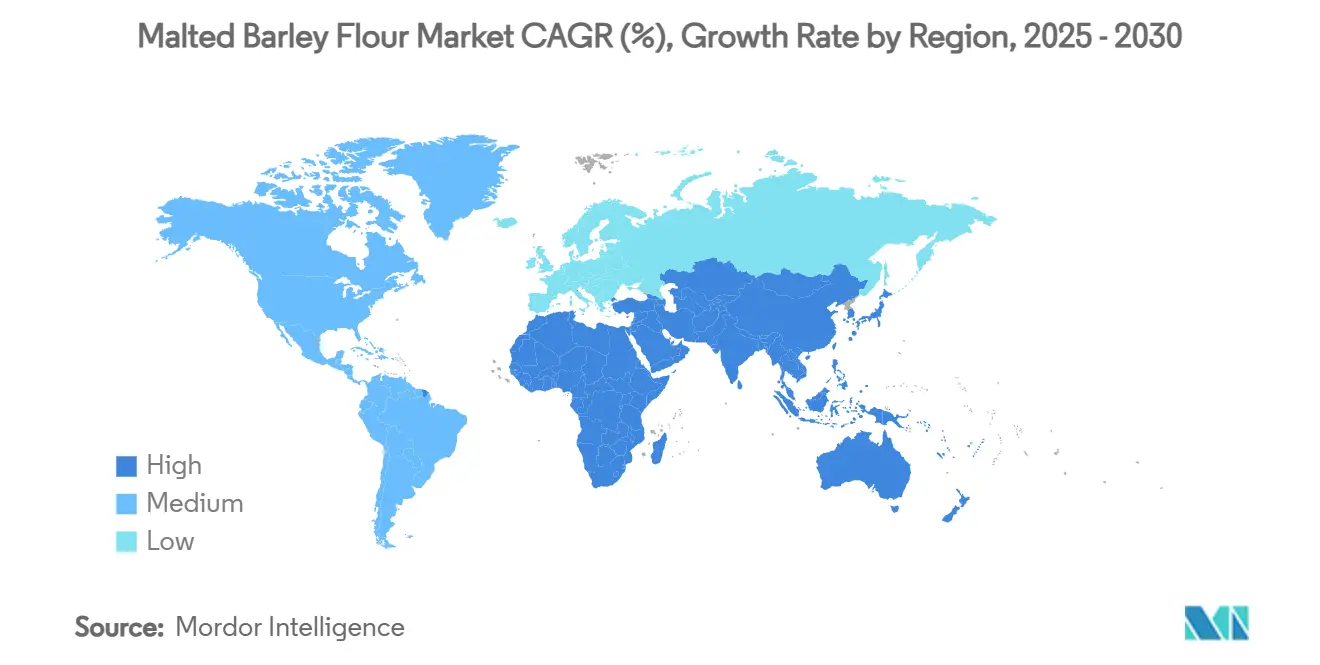

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malted Barley Flour Market Analysis by Mordor Intelligence

The malted barley flour market size is valued at USD 2.51 billion in 2025 and is projected to reach USD 3.41 billion by 2030, advancing at a 6.32% CAGR over the forecast period. As demand surges for clean-label baking aids and the shift to plant-based nutrition accelerates, the unique α- and β-amylase activity profile of malted barley flour drives steady volume gains. Craft brewers, premium bakeries, and formulators of functional foods are increasingly turning to malted barley flour[1]Source: Code of Federal Regulations, "§ 184.1443a", www.ecfr.gov. This ingredient not only enhances dough rheology and sugar conversion but also enables manufacturers to eliminate synthetic conditioners from their ingredient lists, aligning with the growing consumer preference for natural and minimally processed products. Additionally, malted barley flour contributes to improved texture, flavor, and shelf life in baked goods, further boosting its appeal across various applications. Leading suppliers, shielded from climate-related supply shocks, benefit from vertical integration spanning maltings and grain origination, which ensures a stable supply chain and reduces dependency on external sources. This integration also allows suppliers to maintain control over quality and consistency, which are critical in meeting industrial-scale demands[2]Source: United States Department of Agriculture,"Crop Production 2024 Summary", downloads.usda.library.cornell.edu. Meanwhile, technological innovations like controlled kilning and plasma seed treatment ensure consistent enzyme performance on an industrial scale, allowing manufacturers to maintain product quality and meet the rising demand for high-performance, clean-label ingredients. These advancements also support the development of customized solutions tailored to specific end-use applications, further enhancing the versatility and market potential of malted barley flour.

Key Report Takeaways

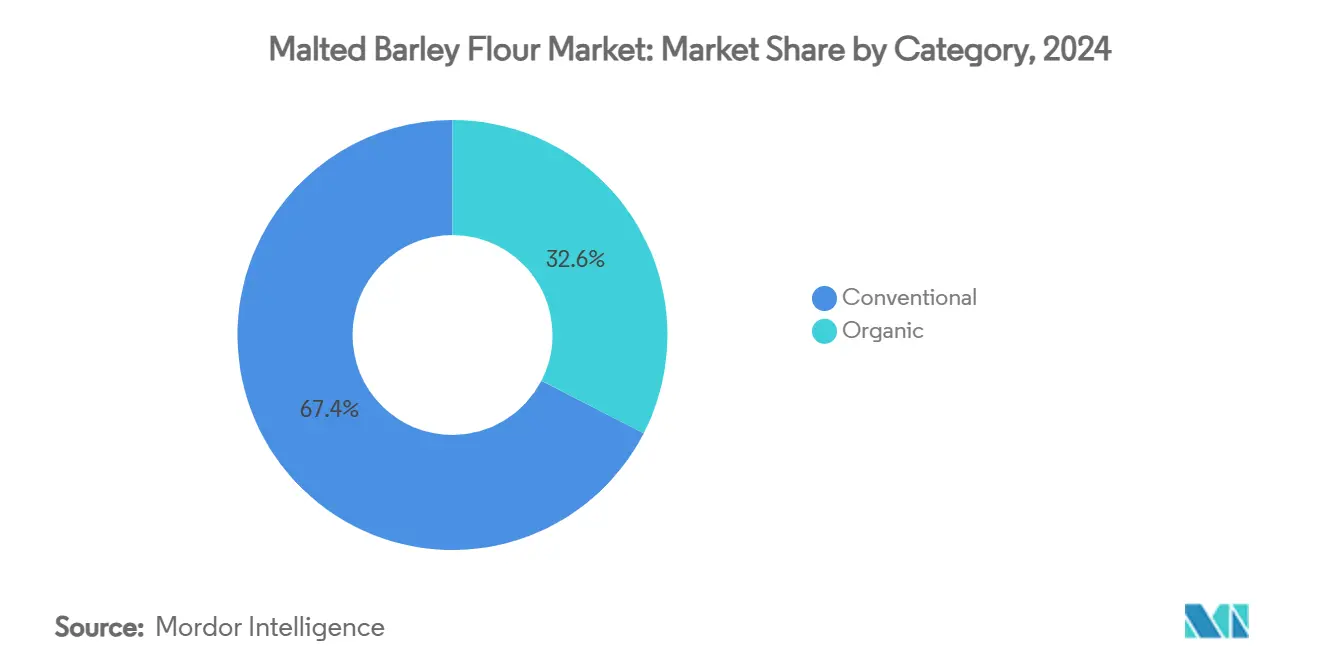

- By category, conventional grade captured 67.44% of the malted barley flour market share in 2024, while the organic segment is forecast to expand at a 7.55% CAGR to 2030.

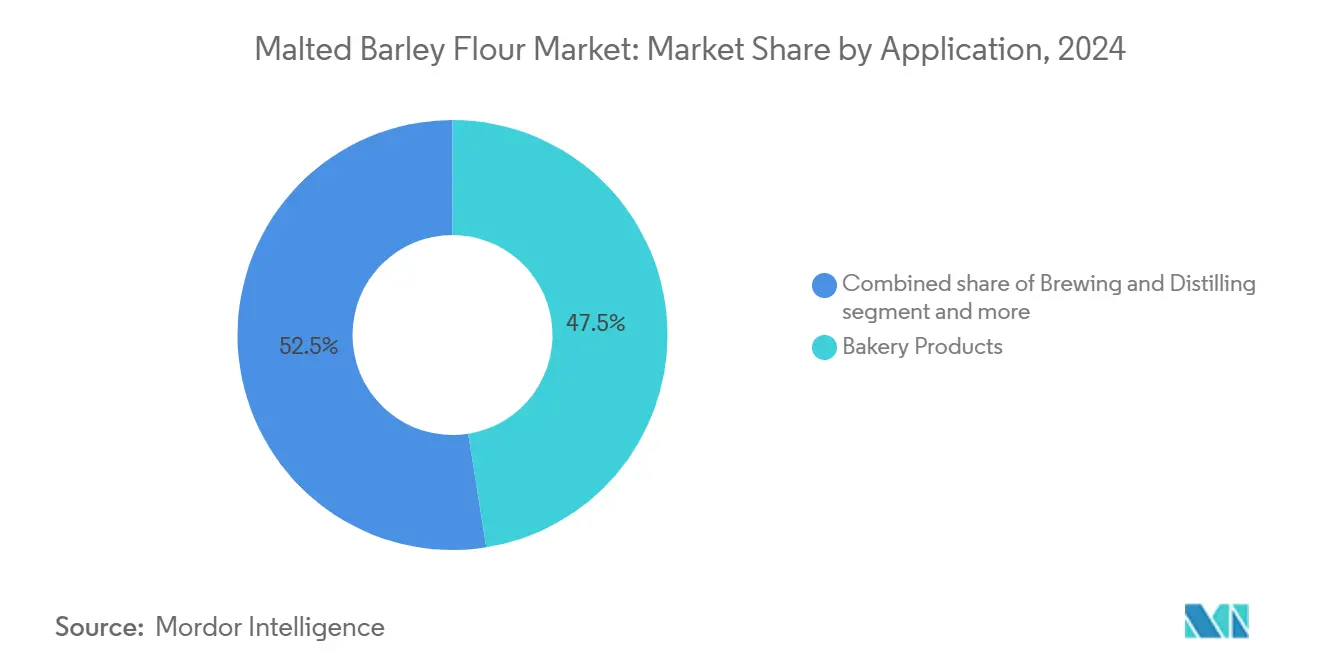

- By application, bakery products led with 47.52% revenue share in 2024; nutritional and snack foods are advancing at an 8.01% CAGR through 2030.

- By geography, North America held a 32.72% share of the malted barley flour market in 2024, whereas the Asia-Pacific region records the highest projected CAGR at 6.73% between 2025 and 2030.

Global Malted Barley Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label natural enzymes in bakery | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Growing craft-beer and micro-brewery sector utilisation | +0.9% | North America, Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of gluten-reduced bakery offerings | +0.8% | Global, particularly strong in developed markets | Medium term (2-4 years) |

| Technological advances in diastatic-activity optimisation | +0.7% | Global, led by advanced manufacturing regions | Long term (≥ 4 years) |

| Surge in plant-based nutrition bars and meal replacements | +0.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Government subsidies for domestic barley processing | +0.4% | United States, Canada, European Union member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label natural enzymes in bakery

Industrial bakers are increasingly opting for malted barley flour over synthetic dough conditioners. The enzymes in malted barley not only enhance loaf volume but also soften the crumb, all without adding chemical names to ingredient panels. This shift aligns with the growing consumer preference for clean-label products, which prioritize natural and recognizable ingredients. Controlled trials indicate that substituting 5% of wheat flour with malted barley flour preserves texture while reducing the need for artificial improvers. This advantage appeals to premium bakery shoppers, who are often willing to pay a premium for such products due to their perceived health and quality benefits. The Generally Recognized As Safe (GRAS) status of malted barley flour streamlines regulatory compliance for cautious food manufacturers, reducing potential risks and simplifying product approvals. Additionally, transparency campaigns on social media amplify the demand for easily recognizable ingredients, as consumers increasingly scrutinize product labels and ingredient lists. As a result, the trend towards clean-label reformulation stands as a significant growth driver for the malted barley flour market, offering opportunities for manufacturers to cater to evolving consumer demands while maintaining compliance and product quality.

Growing craft-beer and micro-brewery sector utilization

Valuing authenticity, local sourcing, and flavor differentiation, the craft-beer segment increasingly favors malted barley flour over enzyme extracts or refined sugars[3]Source: United States GRAINS Council, "Craft Beer Industry Grows Demand For Barley In Mexico", grains.org. Malted barley flour offers unique taste, texture, and nutritional benefits, aligning with the craft-beer industry's emphasis on quality, innovation, and sustainability. Microbreweries are now incorporating malted barley flour into their taproom menus, offering items like pretzels, pizza dough, and spent-grain snacks. This strategy not only enhances their offerings but also expands the market for malted barley flour by creating a cross-category appeal that attracts diverse consumer groups, including those seeking artisanal and locally sourced products. Furthermore, with emerging craft hubs in Mexico and certain Asian regions, demand is surging beyond the traditional brewing geographies. These regions are fostering a growing interest in craft beer, driven by changing consumer preferences and increasing disposable incomes, which, in turn, is broadening the reach for suppliers and creating new opportunities for market expansion.

Expansion of gluten-reduced bakery offerings

Processors can now approach gluten-free thresholds without sacrificing malty flavor and fermentation performance, thanks to ultra-low-gluten barley varieties like CSIRO’s Kebari (with less than 5 ppm gluten). This innovation not only fills the performance void between wheat substitutes and entirely gluten-free products but also paves the way for premium pricing and fresh product narratives. By leveraging these barley varieties, manufacturers can cater to a growing segment of health-conscious consumers seeking gluten-reduced options without compromising on taste or quality. Additionally, these varieties offer opportunities for product differentiation in a competitive market, enabling brands to position themselves as pioneers in gluten-reduced offerings. While markets like the United States provide regulatory clarity on “gluten-reduced” claims, emphasizing the need for consumer education remains paramount to ensure widespread adoption, build trust, and enhance consumer awareness of the benefits and limitations of these products.

Technological advances in diastatic-activity optimisation

Maltsters now harness smart kilning, moisture-controlled germination, and cold atmospheric plasma to fine-tune diastatic power for specific end uses. These advanced techniques allow for precise control over the malting process, enabling manufacturers to achieve desired enzymatic activity levels tailored to various applications. This innovation reduces formulation trials, minimizes production inefficiencies, and ensures consistent quality on bakery lines, meeting the high standards of the food industry. By optimizing these processes, maltsters can cater to the growing demand for high-performance ingredients in bakery and other food production sectors. Meanwhile, microwave-assisted hydrolysis is being employed to extract high-value nutraceuticals from malt residues. This process not only enhances the utilization of by-products but also contributes to improved profitability by creating additional revenue streams. The extracted nutraceuticals, which include bioactive compounds, are increasingly sought after in the health and wellness market, further expanding the potential applications of malt residues. Furthermore, this approach aligns with the sustainability metrics that are increasingly becoming a key purchasing criterion for major food conglomerates, as they prioritize environmentally responsible practices, resource optimization, and waste reduction to meet consumer and regulatory expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-induced volatility in barley yields and prices | -1.4% | Global; notably North America and Australia | Short term (≤ 2 years) |

| Competition from rice and sorghum malt alternatives | -0.8% | Asia-Pacific and Africa: global spillover | Medium term (2-4 years) |

| Stringent mycotoxin compliance costs | -0.6% | Global; highest in regulated markets | Long term (≥ 4 years) |

| Low consumer awareness in emerging economies | -0.5% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-induced volatility in barley yields and prices

Over the last fifty years, rising temperatures and atmospheric drying have led to a 13% decline in barley yields, reducing grain weight and impacting overall production efficiency. In 2024, U.S. barley output plummeted by 23%, totaling just 144 million bushels, which has significantly increased the cost pressures on maltsters due to inflation in raw material prices. This decline in production has also strained the supply chain, creating challenges for both growers and processors. Although an emergency program worth USD 10 billion provides some relief to growers by mitigating immediate financial losses, it does not fully address the long-term issues caused by climate change. Processors, on the other hand, continue to face challenges with unpredictable procurement windows, which disrupt supply chain stability and increase operational risks. To navigate these challenges, they are either diversifying their sourcing origins to reduce dependency on specific regions or investing in breeding programs aimed at developing stress-tolerant barley varieties. These efforts are critical to ensuring long-term sustainability in production and maintaining a steady supply of raw materials for the malt industry.

Competition from rice and sorghum malt alternatives

Rice malt, with yields per acre that double those of barley, offers a gluten-free appeal that resonates with allergy-conscious consumers, despite facing conversion costs that are roughly 20% steeper. This makes rice malt an attractive option for manufacturers targeting the growing demand for gluten-free products, especially as consumer preferences continue to shift toward healthier and allergen-free alternatives. Furthermore, rice malt's higher yield potential can contribute to improved production efficiency, making it a viable choice for regions with limited agricultural resources. Additionally, while sorghum malting currently grapples with double-digit kiln losses, there's potential for targeted breeding to mitigate these setbacks. Such advancements could significantly enhance sorghum's competitiveness, posing a threat to barley's dominance, particularly in agro-climatic zones that aren't ideally suited for temperate cereals. The shift could also diversify the supply chain, offering alternatives to barley in regions with challenging growing conditions, thereby reducing dependency on a single crop and improving resilience in the malt market. Moreover, the development of improved sorghum varieties could open up new opportunities for its adoption in the malt industry, further intensifying competition with barley.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Dominance Amid Organic Acceleration

In 2024, conventional grade dominated the malted barley flour market, capturing 67.44% of its value. This stronghold is attributed to well-established grower-processor networks and cost efficiencies, primarily serving high-demand bakery and brewing clients. While conventional suppliers grapple with margin pressures due to weather-induced input inflation, their scale efficiencies and long-standing certifications bolster steady contract renewals. This entrenched position ensures predictable sourcing and reliable contract fulfillment, solidifying their role as the segment's backbone. Yet, in response to climate risks and evolving market dynamics, these suppliers are diversifying their product lines. By incorporating organic offerings, they're not only hedging against potential downturns but also tapping into lucrative, higher-margin opportunities.

On the other hand, the organic segment, albeit starting from a modest base, is set to outpace others with a projected 7.55% CAGR through 2030. This growth is driven by discerning premium shoppers and retailers with a keen focus on sustainability. The three-year transition period for crops curtails swift supply expansion, helping maintain premium pricing for certified organic grains. Retail data highlights a surge in sales for organic products, like baguettes and granolas made with malted barley flour, underscoring the segment's momentum. To capitalize on this, mid-sized millers are upgrading plants for dedicated organic runs, ensuring segregation and traceability. However, this shift demands a heftier capital investment and extended inventory cycles. Consequently, while organic's rapid ascent complements conventional's steady dominance, together they are broadening the market landscape without undermining core segments.

By Application: Bakery Leadership with Nutrition Segment Momentum

In 2024, bakery formats, encompassing bread, rolls, and pizza dough, dominated the malted barley flour market, capturing 47.52% of the revenue share. By incorporating malted barley flour at typical rates of 2-5%, bakers achieve a consistent crumb texture and a golden crust. This practice not only underscores the bakery's pivotal role in the market but also highlights its stability amidst shifting consumer preferences. Supermarkets, increasingly adopting malted barley flour in their private-label loaves, leverage it as an economical colorant and flavor enhancer, further cementing its baseline consumption. The bakery segment's long-standing integration of malted barley flour ensures consistent volume year after year, anchoring the ingredient's significance in traditional food manufacturing.

On the other hand, nutritional and snack foods are emerging as the fastest-growing application, with projections indicating an 8.01% CAGR through 2030. Producers of protein bars and meal replacement shakes are turning to malted barley flour for its mild sweetness and prebiotic fiber content. This allows them to cut down on added sugars while upholding clean labels. As this segment capitalizes on the functional advantages of malted barley flour, it aligns with the surging consumer demand for healthier, more natural products. While brewing and distilling remain traditional avenues, they grapple with maturation in established markets. Yet, they're buoyed by the rise of microbreweries in Southeast Asia, which are delving into specialty malts. Moreover, sectors like confectionery and dairy are experimenting with malted barley flour as a substitute for synthetic colorants and flavorings, exploring niche opportunities. The cross-pollination of technical know-how between bakery and nutrition product developers is further propelling the adoption of malted barley flour across a spectrum of retail categories.

Geography Analysis

In 2024, North America held a dominant 32.72% share of the malted barley flour market. This stronghold is attributed to the tight connections between the barley belts of Montana, Idaho, and the Canadian Prairie, and the strategic placement of high-capacity malting plants close to bakers and craft brewers. The FDA's GRAS classification, coupled with clear allergen labeling rules, empowers formulators to expand their bakery offerings. Meanwhile, barley insurance and federal acreage subsidies provide growers with a buffer against unpredictable weather. However, a notable 144 million-bushel dip in 2024's output highlights the region's vulnerability to drought and heat, leading to a strategic shift in imports from countries like France and Argentina.

Europe, with its rich brewing tradition and a burgeoning artisan-bakery scene, continues to see stable malt usage, even as beer consumption per capita levels off. The EU's Farm-to-Fork initiatives boost the demand for organic and low-carbon materials. This trend benefits processors who can prove their barley is sourced from regenerative acres, enabling them to lock in long-term supply contracts. While Eastern European grain corridors offer alternative hedging options, they grapple with logistical challenges during peak export times.

The Asia-Pacific region is set for the most robust growth, with projections indicating a 6.73% CAGR for the malted barley flour market through 2030. As disposable incomes rise, Western-style bakery chains flourish in China, India, and Indonesia. Simultaneously, urban millennials are being introduced to craft beer culture, thanks to the trend of experiential dining. However, local bakers face challenges with imported malt prices, which are susceptible to currency fluctuations. This volatility underscores the importance of regional malting investments, like Malteurop's successful model in Mexico, now being mirrored in Vietnam. Furthermore, public-private partnerships are playing a crucial role, sponsoring food-handling training and ingredient literacy campaigns to tap into the region's untapped demand.

Competitive Landscape

The malted barley flour industry sees a moderate concentration. Top maltsters, from contracted barley acres to finished flour, ensure enzyme consistency and wield price leverage through vertical integration. Innovation is the new frontier. Cold atmospheric plasma not only reduces soak time but also diminishes mycotoxins, leading to higher yields and savings on compliance costs. Meanwhile, microwave-assisted hydrolysis produces beta-glucan-rich extracts, enhancing revenue from additives and boosting plant sustainability ratings

At its Ha'il operations, Almarai is investing in integrated processing facilities designed to significantly enhance its poultry processing capabilities. This initiative reflects the company's commitment to expanding its operational efficiency and production capacity. By adopting advanced processing technologies, Almarai aims to cater to the increasing consumer demand for high-quality poultry products while reinforcing its competitive position in the poultry market. Additionally, this investment underscores Almarai's long-term strategy to strengthen its supply chain, ensure consistent product quality, and support sustainable growth in the poultry sector.

Procurement teams at global bakeries are now prioritizing Scope 3 emissions, compelling suppliers to provide life-cycle analyses and transition to renewable-energy kilns. Suppliers lacking a credible decarbonization strategy face delisting threats, squeezing competitive margins. In a notable shift, regional cooperatives in Latin America and Africa are launching domestic malting projects, aiming to reduce import dependencies and hinting at a potential fragmentation away from the traditional Western supply dominance.

Malted Barley Flour Industry Leaders

-

Ardent Mills, LLC

-

Richardson International Limited

-

VIVESCIA

-

Briess Malt & Ingredients Co.

-

Muntons Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vertical Malt unveiled plans for a new dedicated mill, targeting an annual production of 4,000 tons of malted barley flour, with aspirations to scale up to 30,000 tons. This facility aims to cater to both industrial mills and small-scale farmers through toll milling, enhancing the flexibility and variety of malted barley flour products. Furthermore, this expansion paves the way for in-house malting and the creation of other value-added barley products.

- August 2024: Ardent Mills bolstered its foothold in the market by enhancing its Colorado mill. This expansion supports the production of barley flour across the market, allowing the company to meet growing demand and improve its supply chain capabilities.

- March 2023: Miller Milling Company, a key player in the market, ramped up its operations by increasing its flour production capacity to 34,000 cwts per day. This strategic move has enabled the company to better serve its customers and expand its presence in the competitive market.

Global Malted Barley Flour Market Report Scope

| Organic |

| Conventional |

| Bakery Products |

| Brewing and Distilling |

| Nutritional and Snack Foods |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| Category | Organic | |

| Conventional | ||

| By Application | Bakery Products | |

| Brewing and Distilling | ||

| Nutritional and Snack Foods | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the malted barley flour market in 2025?

It stands at USD 2.51 billion and is forecast to grow to USD 3.41 billion by 2030.

Which region exhibits the fastest growth for malted barley flour?

Asia-Pacific posts the highest CAGR at 6.73% through 2030, driven by urban bakery expansion.

Why is the organic malted barley flour segment gaining momentum?

Premium pricing, sustainability regulations, and consumer health perceptions push its 7.55% CAGR.

Which technological advances support product consistency?

Controlled kilning, cold atmospheric plasma, and microwave-assisted hydrolysis optimize diastatic power and reduce contaminants.

Page last updated on: