Retort Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.13 Billion |

| Market Size (2031) | USD 8.14 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

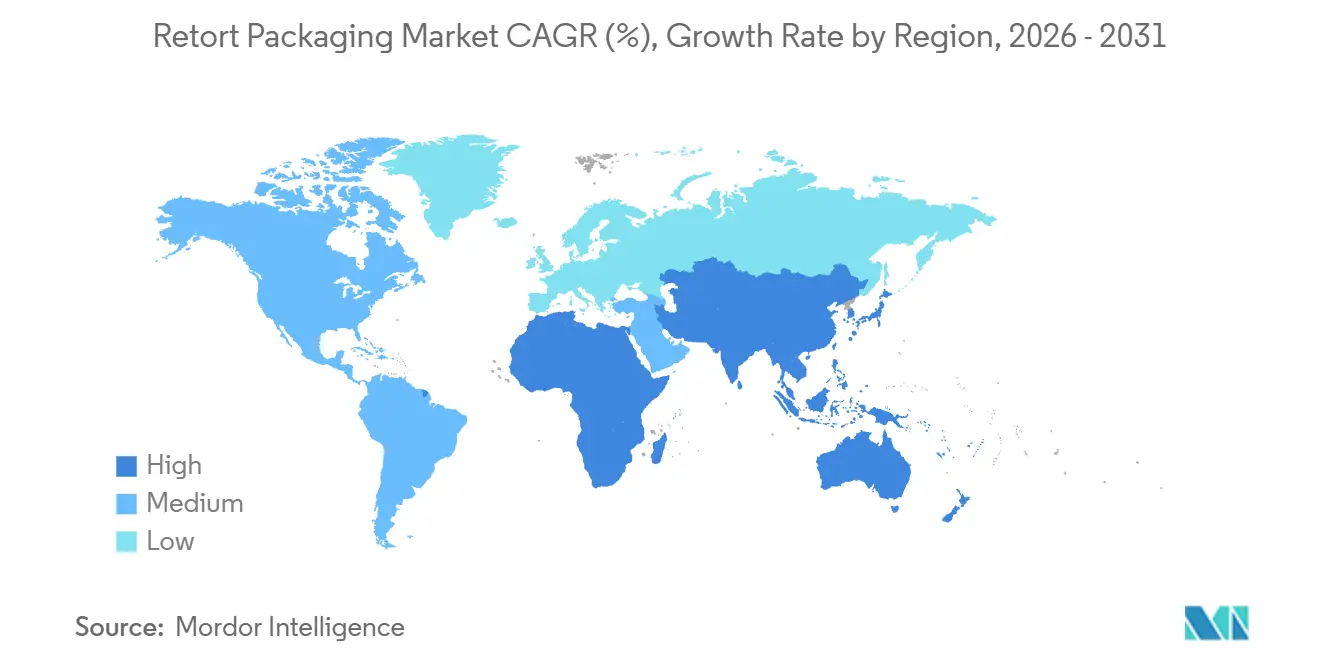

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

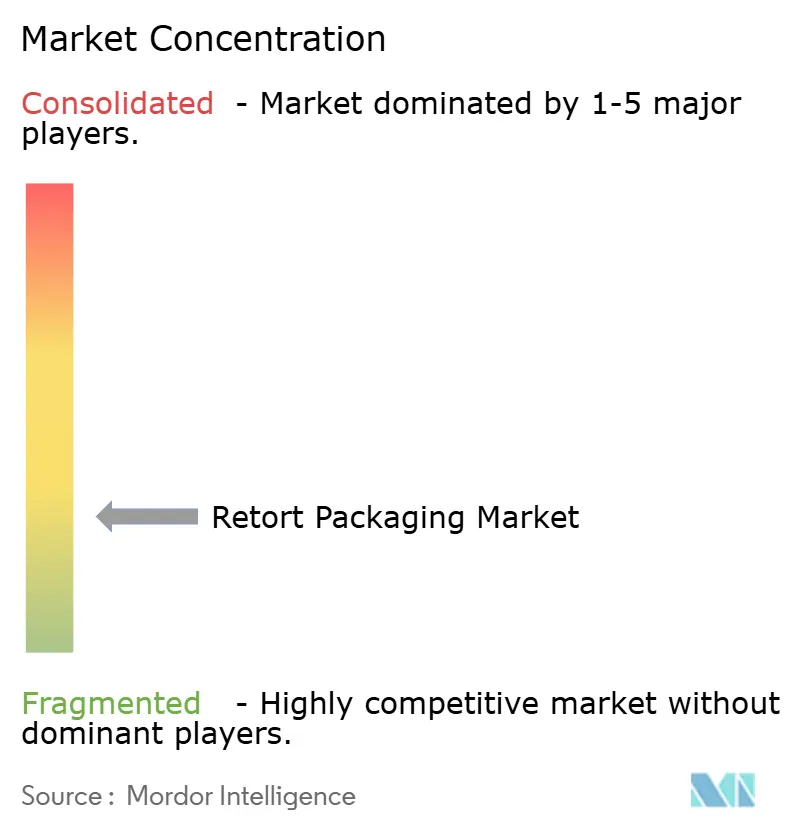

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Retort Packaging Market Analysis by Mordor Intelligence

The retort packaging market size is expected to grow from USD 5.85 billion in 2025 to USD 6.13 billion in 2026 and is forecast to reach USD 8.14 billion by 2031 at a 5.82% CAGR over 2026-2031. Urban migration in Asia-Pacific, regulatory pressure for recycle-ready mono-material laminates in Europe and North America, and premiumization trends in pet food are reshaping adoption patterns. Quick-service restaurants and last-mile e-commerce networks favor lightweight formats that reduce freight costs, while food processors in the Middle East and Africa are installing AI-enabled autoclaves that shorten cycle times and support halal-certified batch production. Backward integration by major converters is strengthening raw-material security, and patent activity in laser-scored easy-peel lids signals ongoing functional upgrades that enhance consumer convenience.

Key Report Takeaways

- By product type, pouches led with 54.32% of the Retort packaging market share in 2025, while trays are forecast to post the fastest 6.12% CAGR to 2031.

- By material, plastic held 58.82% of 2025 revenue, whereas paperboard is advancing at a 6.65% CAGR through 2031.

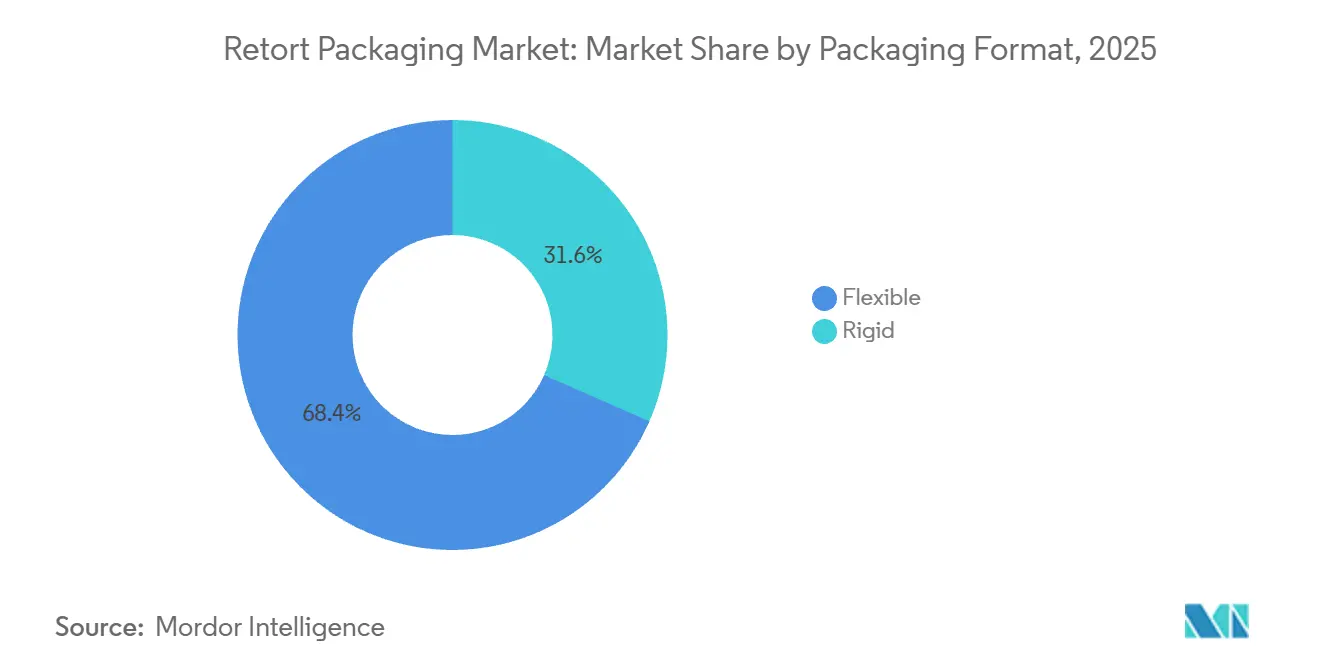

- By packaging format, flexible solutions commanded 68.43% of the Retort packaging market share in 2025, and rigid containers are expanding at a 6.48% CAGR driven by pharmaceutical demand.

- By end-user, food accounted for 56.31% of 2025 sales and is projected to grow at a 6.56% CAGR to 2031.

- By geography, Asia-Pacific generated 40.23% of 2025 revenue, while the Middle East and Africa is the fastest-growing region with a 7.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retort Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Lightweight and Compact Packaging | +1.2% | Global, with concentration in North America and Asia-Pacific e-commerce corridors | Medium term (2-4 years) |

| Rapid Adoption of Shelf-Stable Ready-to-Eat Meals | +1.5% | Asia-Pacific core, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Surge in E-Commerce Driving Lightweight Parcel Formats | +1.0% | Global, led by North America and Europe urban centers | Short term (≤ 2 years) |

| Regulatory Push for Recycle-Ready Mono-Material Laminates | +0.9% | Europe and North America, early adoption in Australia | Long term (≥ 4 years) |

| Growth of Pet Food in Retort-Compatible Formats | +0.8% | North America and Europe premium segments, expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Retort Process Optimization Reducing Downtime | +0.4% | North America and Europe manufacturing hubs, pilot deployments in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweight and Compact Packaging

Retort pouches weigh 85% less than equivalent metal cans, cutting pallet cube by 40% and driving logistics savings for cross-border shipments.[1]U.S. Securities and Exchange Commission, "Amazon.com Inc. Annual Report 2025," sec.gov Amazon waived dimensional-weight surcharges in 2025 for parcels under 200 grams, nudging suppliers toward flexible retort formats, and Indian defense agencies broadened pouch specifications to improve helicopter payload efficiency, accelerating orders across institutional channels. The preference spreads fastest in high-density Asian cities where elevators, public transit, and limited kitchen storage reward compact packs. Brand owners also benefit from lower warehouse rents, as lightweight inventory enables tiered racking systems.

Rapid Adoption of Shelf-Stable Ready-to-Eat Meals

In 2025, China recorded a 28% year-on-year jump in retort-processed ready meals, fueled by same-day e-commerce delivery of hot pots and braised dishes that bypass cold chains.[2]Government of China - Ministry of Agriculture, "Ready-to-Eat Meal Market Growth Report 2025," moa.gov.cn Japan's convenience chains introduced 18-month ambient curry and rice bowls, trimming store-level waste by 35% through centralized production. Middle Eastern hospitality groups adopted retort trays for airline catering and banquet operations where halal certification and extended hold times justify a 15% to 20% premium over frozen meals. Tier-2 and tier-3 cities in India, Indonesia, and Vietnam face persistent cold-chain gaps, making ambient-stable formats structurally advantageous. This driver reinforces Asia-Pacific dominance while opening opportunities in African markets where refrigeration infrastructure is even weaker.

Surge in E-Commerce Driving Lightweight Parcel Formats

Online grocery penetration reached 12% in North America and 9% in Europe by the end of 2025, and flexible retort pouches passed 1.5-meter drop tests without rupture. Walmart's direct-to-consumer meal kits, launched mid-2025, specified retort pouches for protein components to eliminate the need for cold packs and extend delivery windows to 72 hours. The European Union introduced carbon-intensity fees on parcels exceeding 500 grams, pushing brands to migrate from metal cans to lighter pouches that qualify for lower-tier shipping rates. This driver is most pronounced in North America and Europe, where e-commerce infrastructure is mature, but urban platforms in China and Brazil are beginning to favor retail formats as online grocery scales.

Regulatory Push for Recycle-Ready Mono-Material Laminates

France, Germany, and the Netherlands levy EUR 0.50 to EUR 1.20 per kilogram (USD 0.56 to USD 1.35 per kilogram) on non-recyclable multilayer packaging, compelling converters to develop mono-material retort structures.[3]European Commission, "Packaging and Packaging Waste Directive," ec.europa.eu Germany's amended packaging law mandates a 65% mechanical-recycling rate by 2028, a threshold that traditional aluminum-foil laminates cannot meet. Dow Chemical and BASF launched polypropylene-based barrier resins in 2025 that enable all-PP retort pouches to survive 121°C sterilization cycles while remaining compatible with existing recycling streams. Australia's APCO added retort packaging to its 2025 sustainable-packaging targets, requiring brands to transition 50% of volume to recyclable formats by 2027. This regulatory driver focuses on Europe and North America, with a long-term impact horizon as recycling infrastructure scales and resin costs decline with volume adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital for Retort Sterilization Lines | -0.7% | Global, most acute in South America and Africa where financing costs are elevated | Medium term (2-4 years) |

| Limited Recycling Infrastructure for Multilayer Films | -0.5% | Global, with infrastructure gaps most severe in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Supply Risk of High-Barrier Nylon and Aluminum Foil | -0.4% | Global, with Europe experiencing acute shortages in 2025 | Short term (≤ 2 years) |

| Consumer Perception of Flexible Packs as Less Premium | -0.3% | North America and Europe premium food segments, less pronounced in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital for Retort Sterilization Lines

A rotary retort autoclave capable of processing 10,000 pouches per hour requires an investment of USD 800,000 to USD 1.2 million, with ancillary filling, sealing, and quality-inspection equipment adding another USD 500,000 to USD 700,000. Small and mid-sized food processors in Brazil, South Africa, and Southeast Asia face financing challenges, as commercial lending rates for capital equipment ranged from 9% to 14% in 2025, pushing payback periods beyond 5 years. Amcor's 2025 annual report noted that customer hesitation to commit to retort lines delayed USD 45 million in expected equipment sales, particularly among regional dairy and vegetable processors evaluating format migration from metal cans. Leasing models and tolling arrangements are emerging as partial solutions, with contract manufacturers in India and Thailand offering retort processing services at USD 0.08 to USD 0.12 per pouch, enabling brands to test acceptance before committing capital. This restraint is most binding in emerging markets where access to low-cost capital is constrained, and it is likely to persist until modular, lower-capacity retort systems priced under USD 300,000 reach commercial scale.

Limited Recycling Infrastructure for Multilayer Films

Conventional retort laminates combine polyester, aluminum foil, and polyethylene in structures that mechanical recycling facilities cannot separate, leading to landfill disposal or incineration in regions lacking chemical-recycling capacity. The European Union processed only 8% of flexible packaging through mechanical recycling in 2025, with the remainder either incinerated for energy recovery or exported to Southeast Asia, where informal waste sectors face mounting import restrictions. Japan's Ministry of the Environment reported that retort pouches accounted for 3.2% of municipal solid waste by weight in 2025 but represented 11% of non-recyclable flexible-packaging volume due to aluminum-foil content. Brands face reputational risk as consumer awareness of packaging waste intensifies, with 34% of European shoppers in a 2025 survey stating they would switch brands to avoid non-recyclable flexible packaging. Investment in chemical-recycling plants capable of handling multilayer films is accelerating, with Eastman Chemical announcing a USD 1 billion polyester-renewal facility in France scheduled for completion in 2027, but the infrastructure gap will constrain growth in sustainability-conscious markets until at least 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Trays Gain Ground in Delivery Channels

Pouches held 54.32% of 2025 revenue, anchored by their cost efficiency and compatibility with high-speed filling lines, but trays are expanding at a 6.12% CAGR through 2031, the fastest rate among product formats. Quick-service restaurant chains and meal-kit providers are adopting single-serve retort trays that double as microwave-safe serving vessels, eliminating the need for consumers to transfer contents and reducing post-meal cleanup. Nestlé's 2025 investor presentation highlighted that its retort tray portfolio for the Stouffer's brand grew 19% year-on-year, driven by direct-to-consumer e-commerce orders where presentation quality influences repeat purchase rates. Cartons occupy a niche position, primarily in aseptic beverage applications where retort processing competes with ultra-high-temperature treatment, and this segment is growing modestly as dairy-alternative brands seek ambient-stable formats for oat and almond milk.

Other product types, including retort bottles and jars, serve pharmaceutical and specialty-food applications where glass-like clarity and tamper-evidence justify higher unit costs. The tray segment's outperformance reflects a broader shift toward formats that enhance convenience and perceived quality, particularly in markets where consumers associate flexible pouches with economy-tier offerings. Regulatory compliance is shaping product-type selection, as the U.S. Food and Drug Administration's 2025 guidance on low-acid canned foods now explicitly includes retort trays and pouches, requiring process-authority validation for each container geometry. This has standardized sterilization protocols and reduced the perceived risk of adopting non-traditional formats. European food-safety authorities are harmonizing retort-process approval across member states, with EFSA publishing unified thermal-process guidelines in early 2025 that treat pouches, trays, and cartons equivalently, removing a historical bias toward metal cans. Asia-Pacific markets are seeing innovation in stand-up retort pouches with reinforced gussets that enable vertical display on retail shelves, a format that combines the cost advantages of flexible packaging with the shelf presence of rigid containers. Japan's retort-pouch market grew 11% in 2025, with stand-up formats accounting for 62% of new product launches, signaling a maturation of consumer acceptance.

By Material: Paperboard Emerges as Sustainability Play

Plastic materials commanded 58.82% of 2025 revenue, with polypropylene and polyethylene dominating due to their heat-seal reliability and barrier-coating compatibility, yet paperboard is the fastest-growing material at a 6.65% CAGR through 2031. Brands targeting sustainability-conscious consumers are piloting fiber-based retort trays coated with water-based barrier layers that withstand 121°C sterilization while remaining recyclable in existing paper streams. Huhtamäki launched a paperboard retort tray in Europe in late 2025 that achieved a 72% fiber content by weight, meeting the threshold for paper-recycling classification under EU guidelines, and early adopters include organic soup and baby-food brands willing to absorb a 25% to 30% packaging-cost premium. Aluminum foil remains essential for high-barrier applications requiring oxygen transmission rates below 0.5 cubic centimeters per square meter per day, particularly for retort pouches containing fatty or oxygen-sensitive foods, but supply constraints in 2025 pushed lead times to 16 weeks and prices to EUR 3,200 per metric ton (USD 3,600 per metric ton), prompting converters to explore metallized-film alternatives.

Polypropylene's share within the plastic segment is rising as resin suppliers introduce clarified grades that offer transparency comparable to polyethylene terephthalate while maintaining the higher heat-deflection temperature required for retort processing. Dow's Retain polymer, commercialized in 2025, enables all-polypropylene retort pouches that eliminate the polyester layer traditionally needed for structural integrity, simplifying end-of-life recycling. Polyethylene is favored for cost-sensitive applications and remains the sealant layer in most multilayer structures, but its lower melting point limits use in retort processes exceeding 125°C, a constraint that matters for ultra-high-barrier applications in pharmaceutical packaging. Other plastics, including polyamide (nylon) and ethylene vinyl alcohol, serve as barrier layers in multilayer laminates, and their pricing volatility; nylon 6 resin surged 18% in early 2025 due to tight adipic-acid supply, is pushing converters to reduce gauge thickness through advanced coextrusion techniques. The material landscape is fragmenting as brands balance cost, sustainability, and performance, with no single material positioned to dominate across all applications.

By Packaging Format: Rigid Gains in Pharma and Premium Food

Flexible formats captured 68.43% of 2025 revenue, benefiting from lower material costs and transportation efficiency, but rigid retort containers are growing at a 6.48% CAGR through 2031, driven by pharmaceutical and premium-food applications. Injectable-drug manufacturers are adopting rigid retort vials and bottles for sterile formulations that require terminal sterilization, a process that ensures microbial lethality without relying on aseptic filling. The U.S. Pharmacopeia's revised chapter on container-closure integrity, published in 2025, specifies leak-detection methods for rigid retort containers that pharmaceutical companies cite as more straightforward to validate than flexible formats. Premium pet-food brands are also migrating to rigid retort trays with peel-away lids, positioning the format as comparable to refrigerated fresh pet food while offering ambient shelf life. This segment grew 23% in North America in 2025.

Flexible retort packaging's dominance rests on its 60% to 70% lower material cost per unit volume compared to rigid alternatives, a gap that matters most in price-sensitive food categories such as canned beans, soups, and sauces. However, consumer research conducted by Tetra Pak in 2025 found that 41% of European shoppers perceive flexible pouches as lower quality than rigid containers, a perception gap that limits premiumization opportunities and constrains willingness to pay. Brands are responding with hybrid formats, such as flexible pouches inserted into rigid paperboard sleeves that provide structural support and print real estate for brand storytelling. Compliance with food-contact regulations is driving format choices, as the European Union's Regulation (EC) No. 1935/2004 requires migration testing for all materials in contact with food during retort processing, and rigid containers' simpler material structures reduce the testing burden compared to multilayer flexible laminates. Asia-Pacific markets show less format polarization, with flexible and rigid retort packaging coexisting across price tiers, reflecting diverse consumer preferences and retail channel structures.

By End-User Industry: Food Segment Leads, Pharma Accelerates

The food end-user segment accounted for 56.31% of 2025 demand and is forecast to grow at a 6.56% CAGR through 2031, the fastest rate among end-user categories, as plant-based protein manufacturers and ethnic-cuisine brands adopt retort processing to extend ambient shelf life. Beyond Meat's 2025 product pipeline includes retort pouches for plant-based chili and curry formulations that eliminate the need for frozen distribution, a format shift that could unlock convenience-store and vending-machine channels where refrigeration is unavailable. Beverage applications, primarily shelf-stable coffee drinks and nutritional shakes, are growing steadily but face competition from aseptic carton formats that offer similar shelf life with lower packaging costs. Pet food commanded an estimated 18% of the 2025 retort packaging market volume, with premium wet-food brands adopting single-serve pouches and trays that emphasize ingredient visibility and portion control, trends that resonate with pet owners treating animals as family members.

Pharmaceutical applications represent a smaller but high-value segment, where retort sterilization is gaining traction for large-volume parenterals and ophthalmic solutions that require terminal sterilization to meet regulatory standards. The World Health Organization's 2025 guidelines on heat-stable vaccines recommend retort processing for lyophilized formulations distributed in regions lacking cold-chain infrastructure, a specification that could expand addressable markets for rigid retort vials in Africa and South Asia. Other end-user industries, including industrial lubricants and specialty chemicals, use retort packaging for products requiring hermetic seals and long-term stability, but these applications are niche and unlikely to drive aggregate retort packaging market growth. The food segment's outperformance reflects its scale and the alignment of retort packaging's value proposition, ambient stability, lightweight transport, and extended shelf life, with the operational and sustainability priorities of food manufacturers navigating volatile energy costs and tightening carbon-footprint regulations.

Geography Analysis

Asia-Pacific held 40.23% of global retort packaging market revenue in 2025, a position underpinned by China's ready-to-eat meal sector, Japan's convenience-retail infrastructure, and India's expanding military and institutional catering contracts. China's retort-pouch consumption grew 26% year-on-year in 2025, driven by e-commerce platforms such as JD.com and Alibaba's Tmall offering ambient-stable hot pots, braised meats, and rice bowls with an 18-month shelf life, a format that enables centralized production and nationwide distribution without cold-chain investment. Japan's Ministry of Economy, Trade, and Industry reported that retort packaging accounted for 34% of convenience-store meal volume in 2025, with Seven-Eleven and FamilyMart expanding retort curry and pasta offerings that require only microwave reheating. India's Defence Food Research Laboratory awarded contracts worth INR 2.4 billion (USD 29 million) in 2025 for retort pouches supplying border troops, specifying 24-month ambient shelf life and resistance to altitude and temperature extremes. South Korea's retort-tray market is growing as meal-kit delivery services adopt formats that combine cooking and serving functions, reducing packaging waste and enhancing user convenience.

Middle East and Africa is expanding at a 7.21% CAGR through 2031, the fastest regional growth rate, fueled by Saudi Arabia's food-security investments and the United Arab Emirates' role as a logistics hub for African exports. Saudi Arabia's Vision 2030 framework mandates that 50% of processed-food consumption be locally produced by 2030, and retort packaging's ambient stability makes it the preferred format for stockpiling strategic food reserves in a climate where summer temperatures exceed 45°C. The UAE's Jebel Ali Free Zone hosts retort-packaging converters supplying East African markets, where cold-chain gaps and electricity unreliability make ambient-stable formats essential for humanitarian aid and commercial food distribution. South Africa's retort packaging market consumption grew 14% in 2025, driven by ready-meal brands targeting urban consumers and mining companies provisioning remote work camps. Egypt's government launched a food-security initiative in 2025 that includes subsidies for retort-processing equipment, aiming to reduce post-harvest losses in tomato and vegetable canning. Regulatory harmonization is lagging, with each Gulf Cooperation Council member state maintaining distinct food-contact material approvals, a fragmentation that raises compliance costs for converters serving the region.

North America and Europe are investing in closed-loop recycling systems for retort packaging, with Germany's DIN CERTCO certifying the first mechanically recyclable mono-polypropylene retort pouch in late 2025, a milestone that validates the technical feasibility of sustainable retort formats. The United States retort packaging market grew 7% in 2025, with military meal-ready-to-eat contracts and pet-food applications offsetting slower growth in traditional canned-soup categories where consumer preferences are shifting toward fresh and refrigerated options. Canada's retort-pouch adoption is concentrated in outdoor-recreation and emergency-preparedness segments, where lightweight and long shelf life justify premium pricing. Europe's retort packaging market growth is constrained by mature food-retail markets and consumer skepticism toward flexible formats, but plant-based protein brands are driving incremental demand as they seek ambient-stable formats for export to markets lacking refrigeration infrastructure. South America's trajectory depends on Brazil's agricultural processors, which are piloting retort pouches for tomato paste, black beans, and palm hearts, targeting both domestic e-commerce and export to North America and Europe where Brazilian specialty foods command premium shelf space.

Regulatory Landscape

Retort packaging sits at the intersection of food-contact safety requirements and packaging waste rules, with compliance pressure increasingly concentrated in Europe and North America. In the European Union, plastics used in retort structures continue to be evaluated against the EU plastics food-contact framework (including migration testing under the applicable EU rules for food contact materials), while broader packaging obligations are tightening under the Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40). The PPWR adds constraints on substances and affects how recyclability claims are made, which can shift design choices for retort laminates and coatings.

Recent EU food-contact updates also raise the bar for legacy structures used in high-temperature processing. Regulation (EU) 2026/250 (published February 2026) corrected technical elements tied to the EU BPA restrictions and set a July 20, 2026, deadline for placing certain non-compliant single-use food contact articles on the market. In the United States, retort-packed low-acid foods require scheduled process validation by a Process Authority under 21 CFR Part 113, reinforcing container-geometry-specific validation for pouches and trays and increasing the focus on documented heat-process control across packaging suppliers and food processors.

Value Chain Analysis

The retort packaging value chain begins with upstream inputs including polymer resins (PP, PET, PA, EVOH), aluminum foil, adhesives, primers, and barrier coatings, then moves through film extrusion and coating, printing/lamination, and slitting into pouch or tray converting. Food, pet food, and pharmaceutical packers then handle filling and sealing, followed by thermal sterilization in retort autoclaves. In distribution, ambient logistics and just-in-time replenishment matter most for large processors, and for e-commerce-driven meal formats that rely on shelf-stable product.

Key bottlenecks appear at the material-performance interface under heat and moisture, including adhesion failures, metallized surface corrosion, and polypropylene shrinkage that can weaken barrier performance after retort. As recyclability requirements drive structure changes, equipment and materials co-development is becoming more visible; for example, BOBST, Brueckner, and Mitsui Chemicals highlighted a collaboration around K 2025 to align mono-material, recyclable retort solutions with metallization and heat-resistant primer chemistry. Quality assurance and compliance checkpoints (migration testing, seal integrity, and scheduled process validation for low-acid foods) further gate supplier qualification and tend to favor converters with validated formulations and process-control capabilities.

Competitive Landscape

The retort packaging industry is fragmented, with players including Amcor, Sealed Air, Mondi, Sonoco, Constantia Flexibles, and Others. Competitive intensity is rising as Tier-1 players integrate backward into barrier-film extrusion to secure a supply of high-barrier nylon and aluminum foil, a vertical-integration strategy that Amcor pursued with its 2025 acquisition of a European film-coating line for USD 87 million. Patent activity is concentrating on laser-scored easy-peel retort lids and mono-material laminate structures, with Sealed Air filing 14 patents in 2025 related to polypropylene-based barrier coatings that enable recyclable retort pouches to survive 121°C sterilization cycles. White-space opportunities exist in pharmaceutical retort packaging, where stringent validation requirements and low volumes deter generalist converters, and in emerging markets where mid-sized food processors lack access to turnkey retort lines priced below USD 500,000.

Emerging disruptors include Southeast Asian machinery OEMs offering rotary retort autoclaves at 30% discounts to Western equipment, enabling regional food processors in Vietnam and Indonesia to enter the retort packaging market without prohibitive capital outlays. Technology is differentiating competitors, with AI-enabled process-control systems that adjust retort temperature and pressure in real time based on pouch-thickness variation, reducing over-processing and preserving sensory quality.

Mondi's 2025 sustainability report highlighted its closed-loop water system for retort-line cleaning, which cut water consumption by 40% and positioned the company favorably with food brands facing Scope 3 emissions-reduction targets. Compliance with ISO 15378 for pharmaceutical packaging and BRC Global Standard for Packaging Materials is becoming table stakes, and converters lacking these certifications are losing bids to qualified competitors even when pricing is competitive.

Retort Packaging Industry Leaders

-

Tetra Pak Group

-

Huhtamäki Oyj

-

Proampac LLC

-

Amcor plc

-

Constantia Flexibles Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is emerging around redesigning retort packaging toward recycle-ready mono-material and fiber-forward structures that can still maintain barrier performance at sterilization conditions. Mondi introduced a DIN CERTCO-certified mono-polypropylene retort pouch in November 2025. Huhtamaki has also been progressing mono-material polypropylene retort concepts such as Blueloop PP Retort in 2026, which creates space for converters to validate all-PP barrier layers, inks, and sealants for 121 degrees C processes while maintaining compatibility with mechanical recycling streams. Material roadmaps are also extending higher-temperature capability, with 2026 activity around mono-PP retortable film concepts aimed at elevated sterilization resistance.

A second opportunity area involves expanding beyond classic pouches into alternative retort-compatible rigid and carton formats that target canned-food replacement, premium presentation, and lightweighting. In June 2026, Tetra Pak and seafood producer Jealsa unveiled an industry-first carton packaging for shelf-stable tuna using Tetra Recart, after an initial launch in Sweden, and the step reflects willingness by brands to trial non-can ambient formats for protein categories. On supply and capacity, Amcor announced a USD 120 million investment in January 2026 to expand retort-pouch production capacity in Pune, India, signaling active localization to support ready-meal and pet-food corridors and creating room for regional processors seeking shorter lead times and validated structures.

Recent Industry Developments

- July 2026: Tetra Pak introduced its Tetra Recart carton solution for shelf-stable tuna to Southeast Asia. The move broadens the addressable market for retort-compatible cartons in a protein category traditionally dominated by metal cans, creating a new competitive reference point for lightweight, ambient-stable packaging.

- January 2026: Amcor plc announced a USD 120 million investment to expand retort-pouch production capacity in Pune, India, adding high-speed lines and targeting food and pet-food customers serving domestic demand and export corridors. The expansion strengthens regional supply resilience for Asia-Pacific customers and raises the competitive intensity for local and regional converters on lead time and scale.

- October 2025: Sonoco Products Company partnered with a Thai food processor to install a turnkey retort line for ready-to-eat curry and rice products targeting export to Japan and South Korea. The project links packaging supply with validated processing capability, enabling faster commercialization of retort formats for export markets that require consistent quality and compliance documentation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the retort packaging market covers packaging formats and materials that can safely withstand retort heat and pressure for shelf-stable products, and it is sized in value terms across flexible and rigid packs used by end users.

Scope exclusions: It excludes non-retort packaging used only for chilled or frozen distribution, and it also excludes retort processing equipment and services.

Segmentation Overview

-

By Product Type

- Pouches

- Cartons

- Trays

- Other Product Types

-

By Material

-

Plastic

- Polypropylene

- Polyethylene

- Other Plastics

- Aluminum Foil

- Paperboard

-

Plastic

-

By Packaging Format

- Flexible

- Rigid

-

By End-User Industry

- Food

- Beverage

- Pet Food

- Pharmaceutical

- Other End-User Industries

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the initial demand picture and to set practical boundaries for what qualifies as retort-capable packaging, since not every high-barrier pack is used in retort. We reviewed public sources such as the US Census Bureau, UN Comtrade, the World Bank, and FAO food supply and trade indicators to understand packaged food output, trade flows, and consumption direction by region.

To keep assumptions grounded, we also used sources such as the US FDA and European Commission pages related to food contact and packaging compliance, along with peer-reviewed packaging journals, to understand how material choices and regulatory expectations affect adoption. On top of that, we used company annual reports, investor presentations, association websites, and credible press to cross-check capacity additions, format shifts (pouches versus trays), and pricing discussions. Where needed, paid subscriptions were used only for company financials and intelligence, patent landscaping, and shipment-level trade checks, and then the insights were rechecked against public signals. These desk research sources are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was completed through expert interviews and structured surveys with packaging converters, raw material participants, brand owners, and downstream buyers in food, beverage, pet food, and pharmaceuticals. Coverage was balanced across APAC, EMEA, and the Americas so that regional demand patterns, retort line usage, and format preferences could be validated, and then fed back into the final assumptions where desk research was thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 40% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 17% | Managers: 55% | Americas: 26% |

Market-Sizing & Forecasting

Sizing started with a top-down build where packaged food and adjacent retort-ready categories were reconstructed by region, and then filtered through retort penetration assumptions that were validated in calls. Because the same product can be packed in cans, cartons, trays, or pouches, the demand pool was shaped using indicators such as ready-to-eat and shelf-stable meal output, pet food wet category momentum, retortable pack conversion trends, and material mix shifts between plastic, aluminum foil structures, and paperboard.

Once the demand pool was set, price and value were formed using a practical ASP logic by format and material (using ranges gathered from interviews, then normalized to a common currency timing). To keep the totals realistic, we corroborated the result with selective bottom-up approximations, including sampled supplier revenue roll-ups, channel checks on retort pouch and tray usage, and volume to value conversions where suitable data existed. When gaps appeared in smaller regions or niche end uses, ratios from similar markets were applied and then re-tested with follow-up expert inputs.

Forecasting used scenario analysis supported by a light multivariate regression where feasible, using drivers such as packaged food growth, urbanization linked convenience demand, and the pace of format substitution into flexible retort packs. The forward view was then adjusted to reflect expected shifts in sustainable structures and compliance changes that influence material choices, while keeping assumptions traceable and repeatable.

Data Validation & Update Cycle

Results were triangulated across multiple checks so that one weak data point did not move the full market. Model outputs were compared with independent signals like packaged food production direction, trade movement for relevant materials, and announced capacity or investment themes, and then any large variances were investigated before sign-off.

A multi-step review was followed, where assumptions and formulas were peer-checked, followed by a final consistency check across regions and end-use demand logic. When interview feedback showed a meaningful mismatch on adoption rates or pricing movement, respondents were re-contacted and the inputs were corrected, and then the totals were re-run. Reports refresh annually, with interim updates for material events, and before delivery we do a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Retort Packaging Market Size Measured Against Other Published Estimates

Published market sizes for retort packaging can vary even when they sound like they cover the same topic, because the cut of products, years, and value logic are not always aligned. Differences typically show up when one estimate mixes in adjacent packaging that is not used in retort processing, or when pricing is assumed using a single blended ASP that misses format-level spread.

The table points to a wide range mainly because scope and year choices differ, and because some publishers lean on longer-range growth cases that are not rechecked against near-term demand signals. The market also shifts with pouch adoption, foil replacement efforts, and regional packaged food growth, so if a model does not refresh penetration and pricing assumptions frequently, the gap becomes larger quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.13 B (2026) | |

| Industry Publisher A | USD 4.80 B (2025) | Uses an earlier base year and a broader product list that appears to include metal cans alongside retort packs, and it can also blend prices across formats without separating pouch, tray, and carton value differences. |

| Industry Publisher B | USD 4.34 B (2024) | Anchors sizing to a 2024 base with a slower growth track, and the estimate is more sensitive to high-level packaged food trends without clearly revalidating retort penetration by end use and region. |

The spread is understandable once the year and scope are lined up, since 2024 to 2026 alone can move totals meaningfully in a growing packaging category. The table also shows that, in Mordor Intelligence's model, only retort-capable packaging formats are counted under defined end uses, and value is built with format and material level pricing checks, which helps keep the number tied to a realistic demand pool and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the retort packaging market in 2031?

The market is expected to reach USD 8.14 billion by 2031, rising from USD 6.13 billion in 2026 at a 5.82% CAGR.

Which product format shows the fastest growth?

Retort trays lead with a 6.12% CAGR through 2031 as quick-service restaurants and meal-kit firms favor single-serve, microwave-safe formats.

Why is paperboard gaining momentum for retort applications?

Paperboard retort trays, expanding at a 6.65% CAGR, help brands meet Extended Producer Responsibility goals by offering fiber-based, recyclable solutions.

Which region is the fastest growing for retort packaging?

The Middle East and Africa market is expanding at a 7.21% CAGR, buoyed by Saudi Arabia’s Vision 2030 food-security drive and UAE logistics hubs.

What capital barrier limits new entrants?

A full retort line can cost USD 1.3 million - 1.9 million, and emerging-market lending rates near 10%–14% extend payback periods beyond 5 years.

How are recyclability challenges being addressed?

Converters are commercializing mono-material polypropylene pouches that survive 121 °C sterilization and are certified as mechanically recyclable.

Page last updated on: