North America Secondary Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

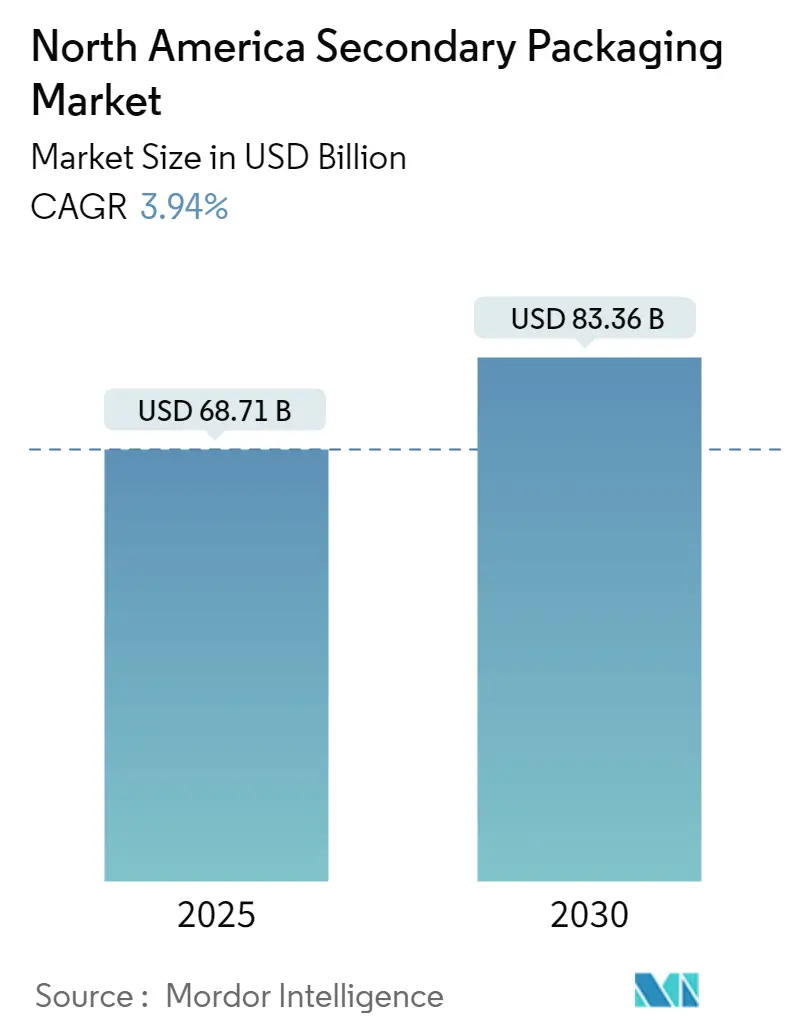

| Market Size (2025) | USD 68.71 Billion |

| Market Size (2030) | USD 83.36 Billion |

| Growth Rate (2025 - 2030) | 3.94% CAGR |

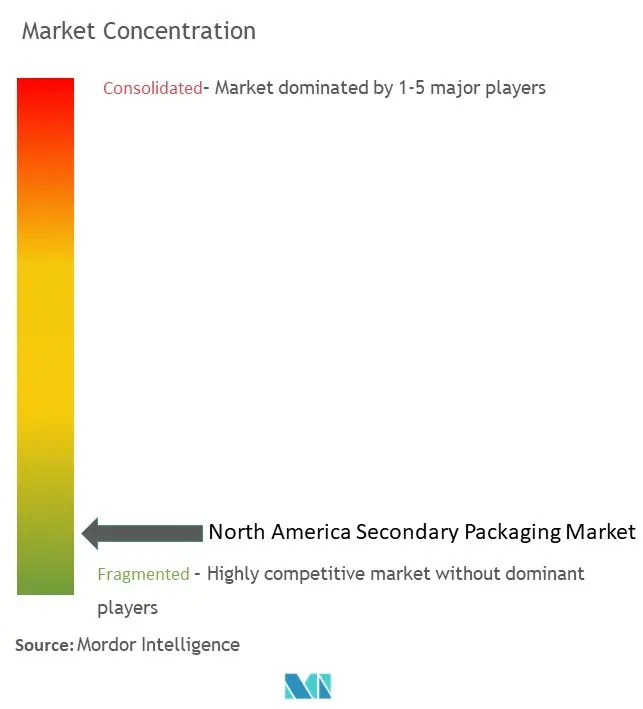

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Secondary Packaging Market Analysis by Mordor Intelligence

The North America Secondary Packaging Market size is worth USD 68.71 Billion in 2025, growing at an 3.94% CAGR and is forecast to hit USD 83.36 Billion by 2030.

The North American secondary packaging landscape is experiencing significant transformation driven by the rapid evolution of e-commerce and digital commerce channels. The surge in online retail has fundamentally altered packaging requirements, with UPS commanding approximately 37% of the courier market share in 2022, highlighting the growing importance of robust secondary packaging solutions for e-commerce deliveries. This shift has prompted packaging manufacturers to develop more specialized solutions that can withstand multiple handling points while maintaining product integrity throughout the supply chain. The integration of digital technologies and automation in packaging processes has become increasingly prevalent, with manufacturers investing in smart secondary packaging solutions that offer enhanced tracking and monitoring capabilities.

Environmental sustainability has emerged as a cornerstone of packaging innovation in North America, with a strong emphasis on recyclable and biodegradable materials. Major industry players are actively developing eco-friendly alternatives to traditional packaging materials, as evidenced by Cascades' introduction of a new recyclable closed basket for the produce industry in January 2023. This innovation serves as an alternative to hard-to-recycle food packaging and adheres to circular economy principles. In March 2023, MBOLD announced that 18 companies and organizations joined its circular economy initiative to build a sustainable ecosystem for flexible film in the Upper Midwest, demonstrating the industry's collective commitment to reducing plastic waste and greenhouse gas emissions.

The agricultural and food sectors continue to be significant drivers of secondary packaging demand, with the United States agricultural exports reaching USD 196.4 billion in 2022. This substantial trade volume has spurred innovations in protective packaging solutions that ensure product freshness and integrity during transportation. The industry has witnessed a notable shift toward sustainable materials that maintain the same level of protection while reducing environmental impact. Manufacturers are increasingly focusing on developing packaging solutions that optimize space utilization and reduce material usage without compromising protection capabilities.

Technological advancement and material innovation remain at the forefront of industry development, as exemplified by the March 2023 collaboration between Amcor and Nfinite Nanotechnology Inc. to test nanocoating technology for improving both recyclable and biodegradable packaging. According to International Paper, US corrugated packaging shipments are projected to reach 560 billion square feet (BSF) by 2026, indicating strong future growth potential. This growth is supported by continuous improvements in material science, manufacturing processes, and design capabilities that enable the development of lighter, stronger, and more sustainable industrial packaging solutions. The industry is witnessing increased investment in research and development activities focused on creating next-generation packaging materials that meet both performance and sustainability requirements.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on secondary packaging market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Secondary Packaging Market Trends and Insights

Increased Demand in the FMCG Industries

The fast-moving consumer goods (FMCG) sector is experiencing significant transformation driven by changing consumer behaviors and retail channels, creating increased demand for secondary packaging solutions. According to recent data, grocery store sales in North America witnessed substantial growth, reaching USD 848.37 billion in 2022, highlighting the expanding FMCG market that requires efficient packaging for distribution solutions. The rising adoption of e-commerce platforms has fundamentally changed how FMCG products are packaged and delivered, with companies focusing on developing packaging ready for retail solutions that can withstand the rigors of the digital supply chain while maintaining product integrity. This shift is evidenced by the dramatic rise in e-commerce sales, with Canadian mobile commerce alone generating over USD 28 billion in 2021, expected to reach USD 57 billion by 2025.

The industry is witnessing a notable shift towards sustainable secondary packaging solutions, driven by both consumer preferences and regulatory requirements. Major retailers and FMCG manufacturers are increasingly adopting recyclable and biodegradable packaging for protection materials, with companies like Sealed Air committing to create 100% recyclable or reused packaging by 2025, with approximately 50% of their solutions already incorporating recycled materials. The export value of consumer goods from Canada, reaching CAD 78.75 billion in 2021, further emphasizes the critical need for robust packaging for transit solutions that can protect products throughout the international supply chain while meeting sustainability requirements. This trend is reinforced by the growing implementation of environmentally friendly packaging materials across the FMCG sector, particularly in food and household care products, where secondary packaging plays a crucial role in product protection and brand presentation.

Increased Demand for Security and Tracking Solutions

The escalating concerns over product security and authenticity have propelled the demand for advanced tracking and security solutions in secondary packaging across North America. According to recent statistics, North America recorded the highest number of pharmaceutical counterfeiting incidents globally, with 2,442 cases in 2021, emphasizing the critical need for secure packaging for transport solutions. The implementation of sophisticated anti-counterfeiting technologies, including barcodes, holograms, sealing tapes, and RFID devices, has become increasingly prevalent, particularly in the electronics and pharmaceutical sectors. This trend is further exemplified by Walmart's expansion of its RFID mandate program to more products and departments in 2022, significantly impacting manufacturers, distributors, and vendors across the supply chain.

The rising incidents of package theft have also intensified the focus on security features in secondary packaging. Recent data indicates that states like Alaska and Delaware reported package theft rates of 0.29% and 0.27%, respectively, in 2022, with stolen packages valued at up to USD 80 per incident. This has led to increased integration of smart packaging for display solutions that enable real-time tracking and monitoring of products throughout the supply chain. The electronics packaging sector has particularly embraced these security measures, implementing both overt and covert technologies to protect product integrity. The industry's response includes the development of innovative security features that not only prevent counterfeiting but also enable end-to-end visibility in the supply chain, ensuring product authenticity from manufacturer to consumer while meeting the growing demands of e-commerce and retail channels.

Segment Analysis: By Product Type

Folding Cartons Segment in North America Secondary Packaging Market

The carton packaging segment has established itself as the dominant force in the North American secondary packaging market, commanding approximately 31% market share in 2024. This segment's leadership position is driven by its widespread adoption across various industries, particularly in food and beverage packaging applications. The segment's growth is propelled by increasing demand for eco-friendly packaging materials, as folding cartons are made from recyclable and biodegradable materials like paperboard. The segment is also experiencing the fastest growth trajectory, projected to expand at around 5% through 2024-2029, driven by technological advancements in digital printing, growing e-commerce activities, and increasing consumer preference for sustainable packaging solutions. Manufacturers are increasingly focusing on developing innovative carton packaging designs that offer enhanced protection while maintaining aesthetic appeal, further solidifying this segment's market leadership.

Remaining Segments in North America Secondary Packaging Market by Product Type

The other significant segments in the North American secondary packaging market include corrugated packaging, wraps and films, plastic crates, and other product types. Corrugated packaging represents the second-largest segment, widely used in e-commerce and retail applications due to its durability and cost-effectiveness. The wraps and films segment plays a crucial role in providing protective packaging solutions, particularly in the food and beverage industry, offering superior barrier properties and product visibility. Plastic crates serve specific niches in the market, particularly in agriculture and beverage industries, where reusability and durability are paramount. The other product types segment, including trays and mailers, caters to specialized packaging needs across various industries, contributing to the market's diversity and comprehensive packaging solutions.

Segment Analysis: By End-User Industry

Food Segment in North America Secondary Packaging Market

The food segment maintains its dominant position in the North American secondary packaging market, commanding approximately 24% market share in 2024. This leadership position is driven by the increasing demand for protective packaging solutions in the food industry, particularly for processed foods, ready-to-eat meals, and fresh produce. The segment's growth is further supported by stringent food safety regulations requiring robust secondary packaging solutions to maintain product integrity throughout the supply chain. The rise of e-commerce food delivery services and meal kit businesses has significantly contributed to the segment's market share, as these services require specialized secondary packaging solutions for safe transportation and handling. Additionally, the increasing focus on sustainable packaging solutions in the food industry has led to greater adoption of recyclable and biodegradable secondary packaging materials, particularly in carton packaging and corrugated packaging.

Consumer Electronics Segment in North America Secondary Packaging Market

The consumer electronics segment is emerging as the fastest-growing segment in the North American secondary packaging market, with a projected growth rate of approximately 5% from 2024 to 2029. This accelerated growth is primarily driven by the expanding e-commerce sector and the increasing complexity of electronic product protection requirements. The segment's growth is further fueled by technological advancements in packaging solutions, including enhanced protective features and smart packaging innovations. The rising demand for sustainable packaging solutions in the electronics industry has led to the development of eco-friendly alternatives to traditional packaging materials. Additionally, the increasing focus on user experience and unboxing experiences has driven innovation in secondary packaging design for consumer electronics products, leading to more sophisticated and premium packaging solutions that offer both protection and brand enhancement opportunities.

Remaining Segments in End-User Industry

The beverage, healthcare, personal care & household care, and other end-user segments continue to play vital roles in shaping the North American secondary packaging market. The beverage segment maintains strong demand for secondary packaging solutions, particularly in the areas of multipack packaging and transit packaging. The healthcare segment emphasizes tamper-evident and security features in secondary packaging, while the personal care & household care segment focuses on brand differentiation and sustainability. The other end-user industries segment encompasses various sectors including automotive, industrial goods, and agriculture, each contributing unique requirements and innovations to the secondary packaging market. These segments collectively drive innovation in areas such as material science, design optimization, and sustainable packaging solutions, while maintaining their specific requirements for protection, transportation, and brand presentation.

North America Secondary Packaging Market Geography Segment Analysis

Secondary Packaging Market in United States

The United States dominates the North American secondary packaging market, commanding approximately 89% of the total market share in 2024. The country's leadership position is driven by its vast population base and substantial customer demand across various end-user industries. The robust e-commerce sector, particularly the significant presence of major players like Amazon and Walmart, has been instrumental in driving demand for commercial packaging and logistics packaging solutions. The country's well-established food and beverage industry, coupled with stringent packaging regulations, continues to shape the market landscape. The increasing focus on sustainable packaging solutions, particularly in response to growing environmental concerns, has led to significant innovations in recyclable and biodegradable packaging materials. The United States has also witnessed substantial investments in advanced packaging technologies, with many manufacturers incorporating smart packaging solutions and tracking capabilities to enhance supply chain efficiency.

Secondary Packaging Market in Canada

Canada represents a dynamic growth market in the North American secondary packaging industry, projected to expand at a rate of approximately 5% during the forecast period 2024-2029. The country's packaging industry is experiencing significant transformation driven by evolving consumer preferences and stringent environmental regulations. Canada's strong commitment to sustainability has fostered innovation in eco-friendly packaging solutions, particularly in the development of recyclable paperboard packaging. The country's developing e-commerce market has been generating substantial demand for industrial packaging and logistics packaging products, notably from players in the transportation and logistics sectors. The nation's robust food and beverage sector, coupled with increasing export activities, continues to drive demand for various secondary packaging solutions. Canadian manufacturers are increasingly focusing on technological advancements, particularly in areas such as smart packaging and tracking solutions, to meet the evolving needs of various end-user industries. The market is further strengthened by the presence of several key packaging manufacturers who are expanding their production capabilities and introducing innovative solutions.

Secondary Packaging Market in Other Countries

The North American secondary packaging market analysis primarily focuses on the United States and Canada, as these two countries represent the entirety of the regional market. The market dynamics in these countries are closely interlinked due to their geographical proximity, shared trade agreements, and similar consumer preferences. Both nations demonstrate strong commitment to sustainable packaging solutions and technological advancement in the packaging industry. The regulatory frameworks in both countries continue to evolve, particularly concerning environmental sustainability and packaging waste management. The integration of advanced technologies, such as smart packaging solutions and tracking capabilities, is observed across both markets, albeit at different adoption rates. Future market developments in both countries are expected to be shaped by ongoing trends in e-commerce growth, sustainability initiatives, and technological advancements in the packaging industry.

Competitive Landscape

Top Companies in North America Secondary Packaging Market

The North American secondary packaging market is led by major players, including International Paper Company, Amcor PLC, WestRock Company, Berry Global Group, Smurfit Kappa Group, and Packaging Corporation of America. These companies are driving innovation through sustainable secondary packaging solutions, with a strong focus on recyclable materials and eco-friendly alternatives to traditional packaging. Operational excellence is being achieved through vertical integration strategies, allowing companies to maintain control over their supply chains and respond quickly to market demands. Strategic initiatives include significant investments in research and development, particularly in areas such as corrugated packaging technology and smart packaging solutions. Market leaders are expanding their geographical presence through strategic acquisitions and partnerships while simultaneously modernizing existing facilities to enhance production capabilities and meet evolving customer needs. The industry is witnessing a shift towards digitalization and automation in manufacturing processes, with companies investing in advanced technologies to improve efficiency and reduce operational costs.

Consolidated Market with Strong Regional Players

The secondary packaging market in North America exhibits a relatively consolidated structure, dominated by large multinational corporations with extensive manufacturing networks and established distribution channels. These major players leverage their economies of scale, technological capabilities, and strong customer relationships to maintain their market positions. The market also features several regional specialists who have carved out niches in specific packaging segments or geographical areas, competing effectively through specialized product offerings and local market knowledge. The industry has witnessed significant merger and acquisition activity, with larger players acquiring smaller companies to expand their product portfolios, enhance technological capabilities, and strengthen their market presence.

The competitive landscape is characterized by a mix of vertically integrated companies that control multiple stages of the value chain and specialized manufacturers focusing on specific packaging solutions. Market consolidation continues to be a prominent trend, driven by the need for operational efficiency and expanded geographical reach. Companies are increasingly pursuing strategic partnerships and joint ventures to access new technologies, enter new markets, and strengthen their competitive positions. The market also sees regular collaboration between packaging manufacturers and end-users to develop customized solutions, particularly in the food and beverage, healthcare, and e-commerce sectors.

Innovation and Sustainability Drive Future Success

Success in the North American secondary packaging market increasingly depends on companies' ability to innovate while maintaining environmental responsibility. Market incumbents are focusing on developing sustainable packaging solutions, investing in research and development to create recyclable and biodegradable materials, and implementing circular economy principles in their operations. Companies are also strengthening their market position by expanding their digital capabilities, offering smart packaging solutions, and developing value-added services such as package design and logistics packaging optimization. The ability to provide end-to-end packaging solutions, maintain cost competitiveness, and adapt to changing regulatory requirements is becoming crucial for maintaining market share.

For contenders looking to gain ground, differentiation through specialized product offerings and superior customer service is essential. Companies are investing in niche markets and developing innovative solutions for specific industry segments, particularly in areas with high growth potential such as e-commerce and healthcare packaging. The market presents moderate substitution risks, primarily from alternative packaging materials and formats, driving companies to continuously innovate and improve their product offerings. Regulatory compliance, particularly regarding environmental standards and sustainability requirements, is becoming increasingly important for both established players and new entrants. Success also depends on building strong relationships with end-users, understanding their specific needs, and providing customized solutions that address their packaging challenges.

North America Secondary Packaging Industry Leaders

Amcor PLC

International Paper Company

Reynolds Packaging

Westrock Company

Smurfit Kappa Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: Ara Partners announced the acquisition of Genera Energy Inc., a non-wood agricultural pulp and molded fiber products company. The firm also committed additional funding to support the significant expansion of its sustainable pulp and packaging business.

- February 2023: Mill Rock Packaging Partners LLC acquired Keystone Paper & Box Company. This leading specialty packaging company manufactures custom folding cartons for consumer and healthcare end markets.

- January 2023: Cascades, a packaging firm based in North America, disclosed releasing a new closed basket for the produce industry made of recyclable and recycled corrugated cardboard. This new product is the most recent addition to Cascades' collection of environment-friendly packaging and serves as an alternative to food packaging that is challenging to recycle. This product was created utilizing acknowledged eco-design principles. It adheres to a circular economy philosophy. Cascades are helping its clients lessen their environmental impact by incorporating recycled corrugated cardboard in its design and satiating consumer desire for more environment-friendly packaging.

North America Secondary Packaging Market Report Scope

Secondary packaging includes outer material that protects food, drinks, and consumer goods throughout transit. Secondary packaging is the exterior packaging of the primary packaging that groups a package and further protects a product.

The North American secondary packaging market is segmented by product type (corrugated boxes, folding cartons, plastic crates, wraps and films, and other product types), by end-user industry (food, beverage, healthcare, consumer electronics, personal care, household care and end-user industries), by country (United States and Canada). The report offers market forecasts and size in value (USD) for all the above segments.

| Corrugated Boxes |

| Folding Cartons |

| Plastic Crates |

| Wraps and Films |

| Other Product Types |

| Food |

| Beverage |

| Healthcare |

| Consumer Electronics |

| Personal Care and Household Care |

| Other End-user Industries |

| United States |

| Canada |

| By Product Type | Corrugated Boxes |

| Folding Cartons | |

| Plastic Crates | |

| Wraps and Films | |

| Other Product Types | |

| By End-user Industry | Food |

| Beverage | |

| Healthcare | |

| Consumer Electronics | |

| Personal Care and Household Care | |

| Other End-user Industries | |

| By Country | United States |

| Canada |

Key Questions Answered in the Report

How big is the North America Secondary Packaging Market?

The North America Secondary Packaging Market size is worth USD 68.71 billion in 2025, growing at an 3.94% CAGR and is forecast to hit USD 83.36 billion by 2030.

What is the current North America Secondary Packaging Market size?

In 2025, the North America Secondary Packaging Market size is expected to reach USD 68.71 billion.

What years does this North America Secondary Packaging Market cover, and what was the market size in 2024?

In 2024, the North America Secondary Packaging Market size was estimated at USD 66.00 billion. The report covers the North America Secondary Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the North America Secondary Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: