Micro-Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

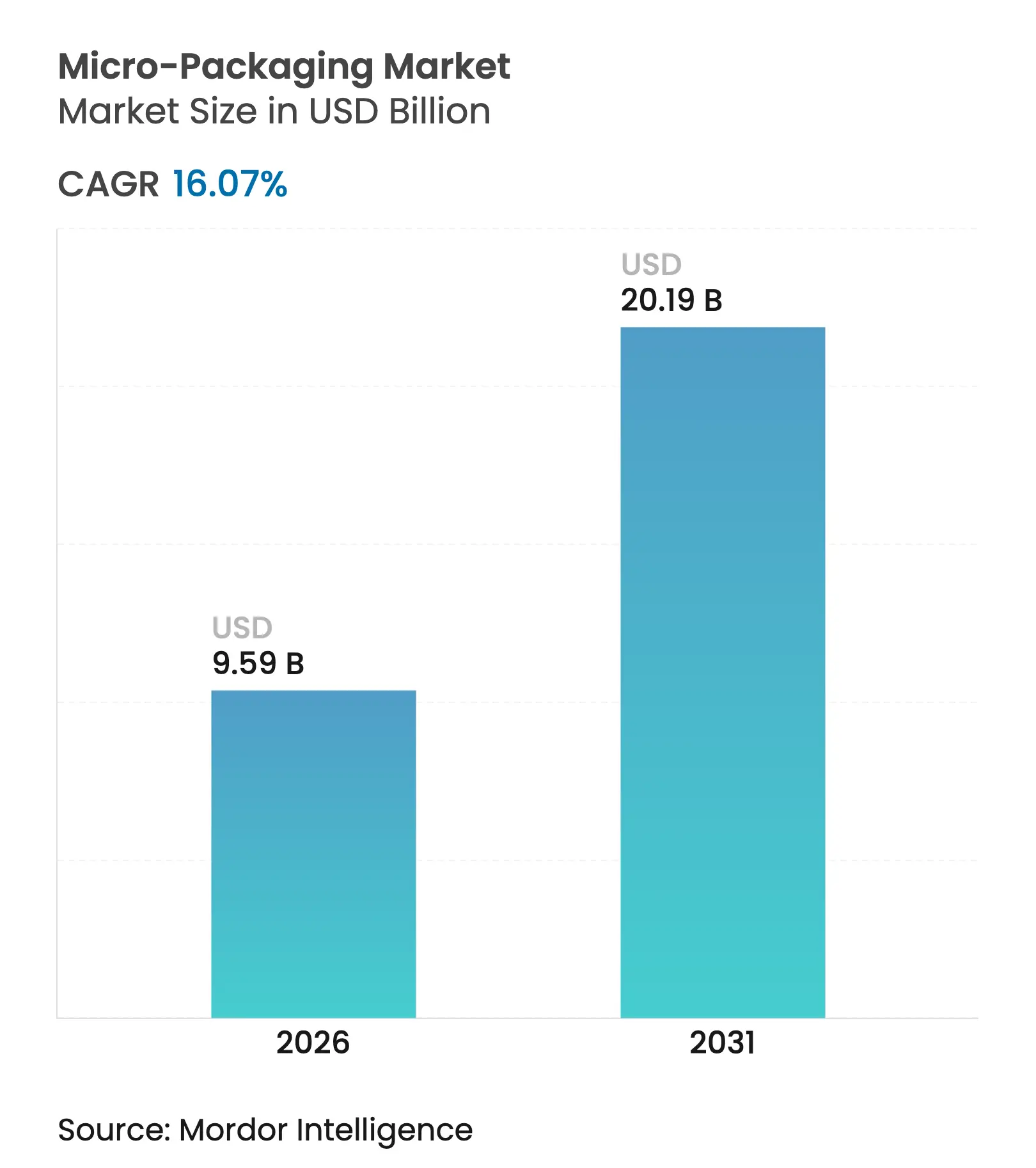

| Market Size (2026) | USD 9.59 Billion |

| Market Size (2031) | USD 20.19 Billion |

| Growth Rate (2026 - 2031) | 16.07 % CAGR |

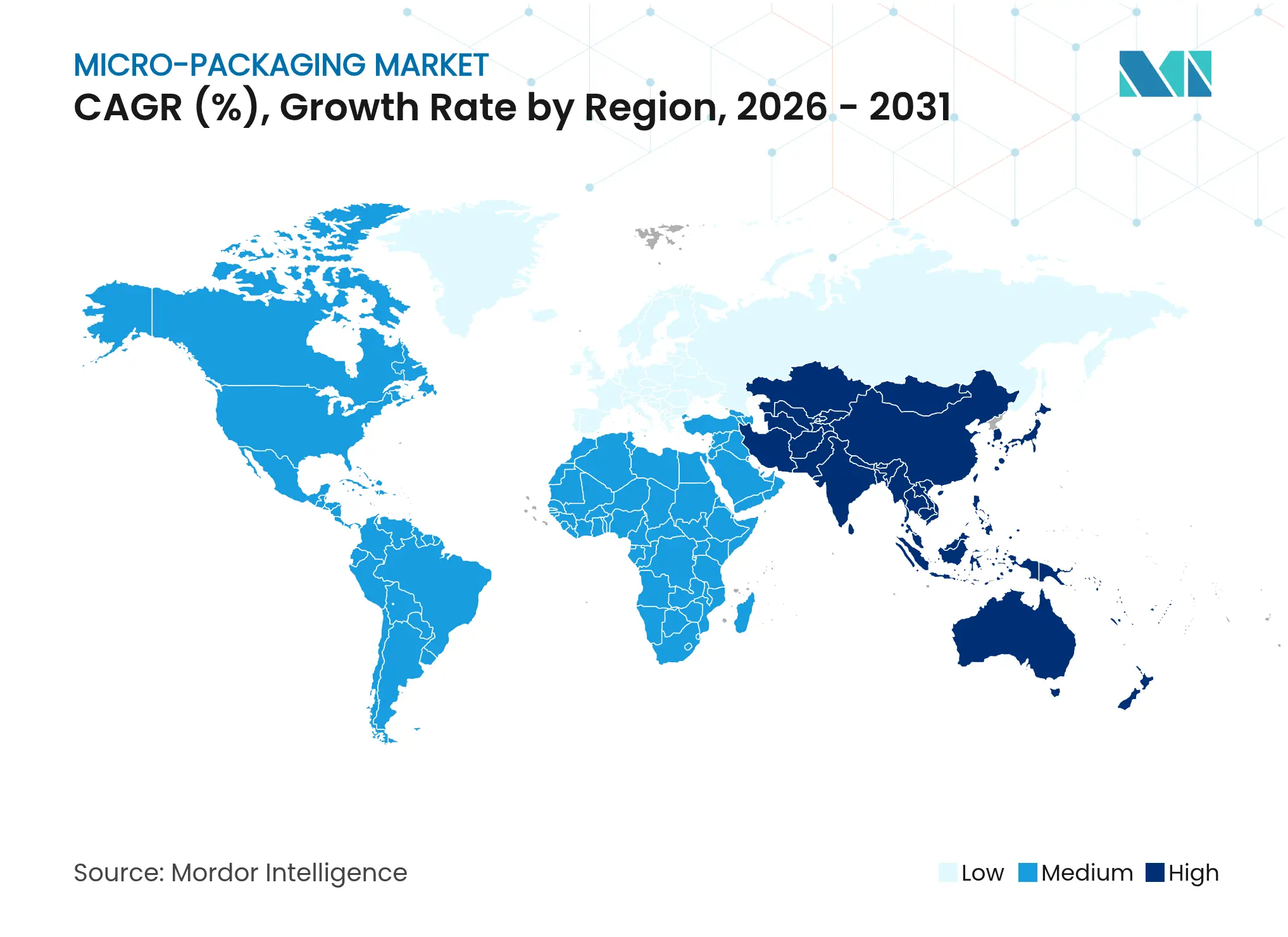

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

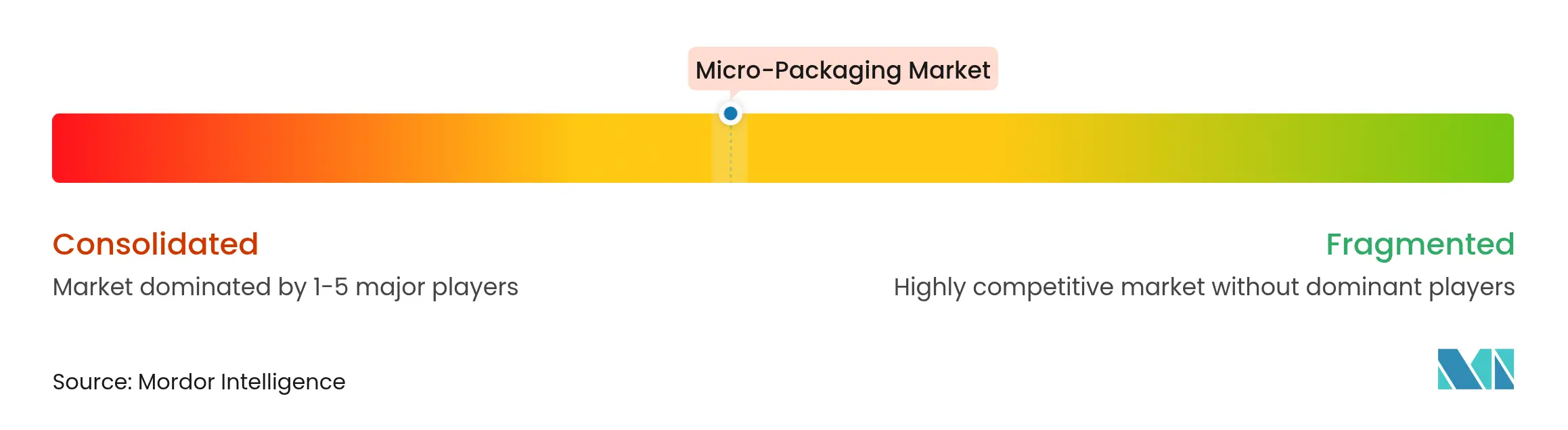

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Micro-Packaging Market Analysis by Mordor Intelligence

micro-packaging market size in 2026 is estimated at USD 9.59 billion, growing from 2025 value of USD 8.26 billion with 2031 projections showing USD 20.19 billion, growing at 16.07% CAGR over 2026-2031. Robust growth reflects converging forces: precision manufacturing, rising demand for miniaturized dose formats in biologics, and smart-label functionality that supports supply-chain transparency. Regulatory momentum—including the European Union’s requirement for 100% recyclable packs by 2030—continues to reshape material choices, rewarding first movers in biopolymer and high-barrier thin-film design. North America retains leadership, buoyed by strict FDA rules and semiconductor grade-packaging needs; Asia-Pacific, however, delivers the fastest expansion as Chinese and Indian manufacturing ecosystems scale high-accuracy forming lines. Consolidation accelerates: large packaging converters pursue multi-billion-dollar mergers to secure integrated capabilities, while capital-intensive precision equipment becomes a barrier for new entrants.

Key Report Takeaways

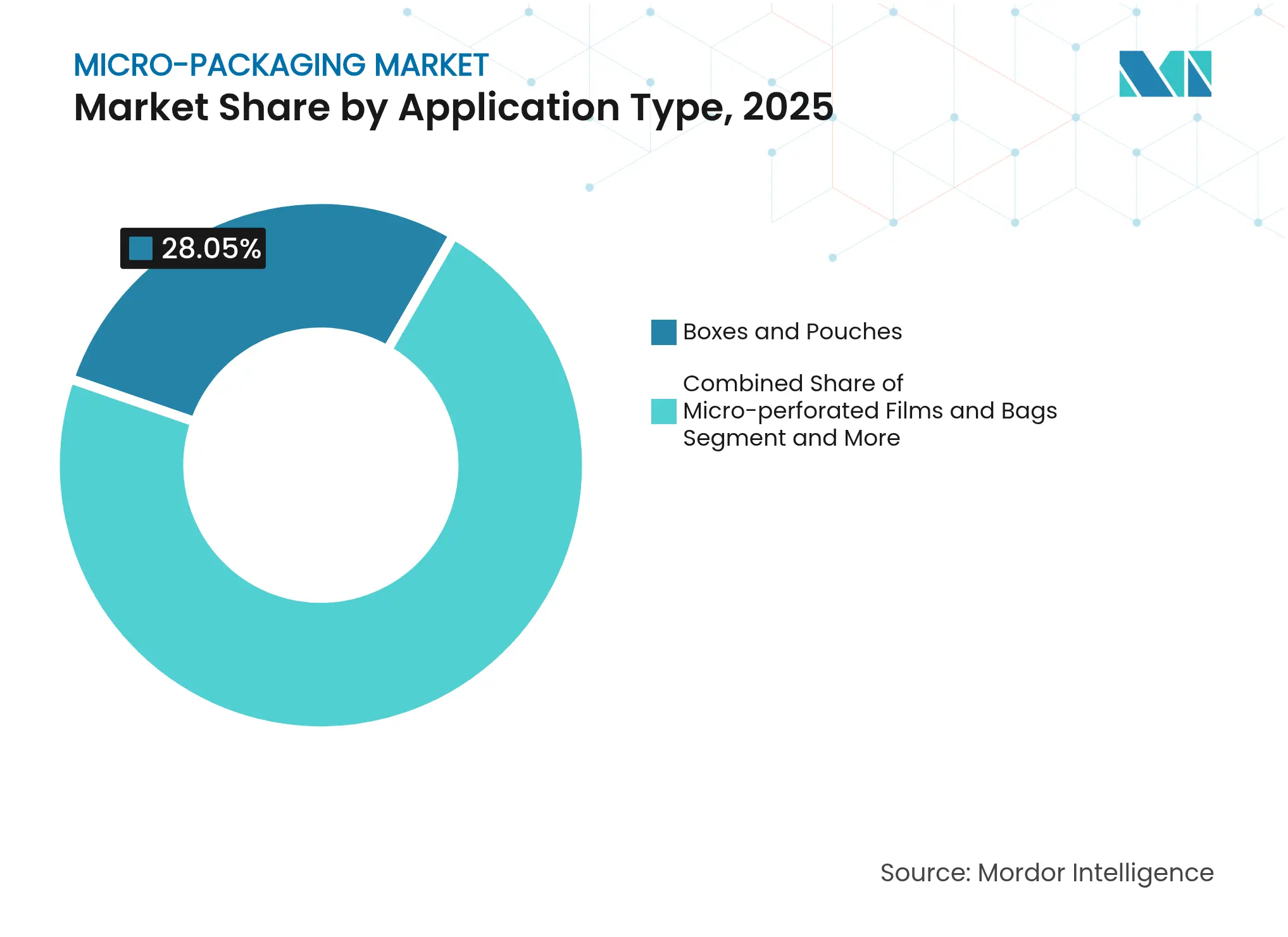

- By application type, boxes and pouches led with 28.05% of micro-packaging market share in 2025, whereas vials record the highest 19.78% CAGR through 2031.

- By end-user, food and beverage held 35.38% revenue share in 2025; pharmaceutical-biotech is expected to expand at a 20.98% CAGR to 2031.

- By material, plastics and polymers commanded 55.10% share of the micro-packaging market size in 2025, yet biopolymers and edible films rise at a 23.74% CAGR.

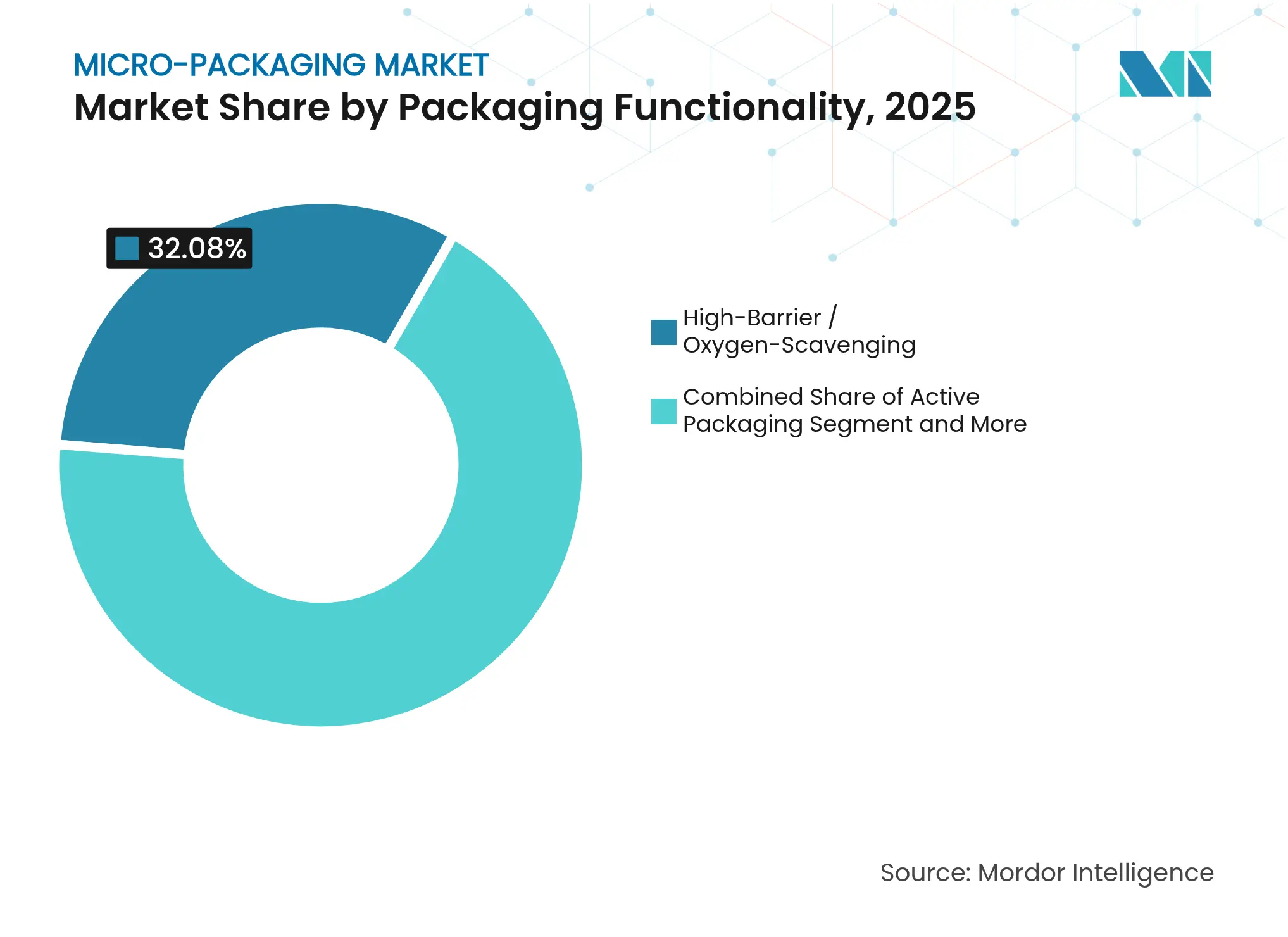

- By functionality, high-barrier formats captured 32.08% share in 2025; intelligent smart-packaging functionality grows fastest at 21.85% CAGR.

- By format, flexible solutions secured 55.78% of the micro-packaging market size in 2025 and are advancing at an 17.75% CAGR.

- By gepgraphy, North America captured 39.05% share in 2025; Asia-Pacific grows fastest at 18.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Micro-Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Demand

for micro-perforated food packaging for perishable products

Demand

for micro-perforated food packaging for perishable products

| +2.5% | Global, with concentration in North America and EU | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+2.5%

|

Geographic Relevance

:

Global,

with concentration in North America and EU

|

Impact Timeline

:

Medium

term (2-4 years)

|

Expansion

of novel drug-delivery formats and biologics pipelines

Expansion

of novel drug-delivery formats and biologics pipelines

| +1.8% | North America and EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) | |||

Shift

to single-dose adherence packs in outpatient care

Shift

to single-dose adherence packs in outpatient care

| +2.1% | Global, with early gains in developed markets | Medium term (2-4 years) | |||

Sustainability

push toward recyclable micro-structures

Sustainability

push toward recyclable micro-structures

| +1.9% | EU leading, North America following, Asia-Pacific emerging | Long term (≥ 4 years) | |||

IoT/sensor-embedded

smart micro-packages

IoT/sensor-embedded

smart micro-packages

| +1.2% | North America and EU advanced markets | Long term (≥ 4 years) | |||

Fulfillment-ready

sample size packs for e-commerce

Fulfillment-ready

sample size packs for e-commerce

| +1.5% | Global, with concentration in urban markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Demand for Micro-Perforated Food Packaging for Perishable Products

Laser micro-perforation now enables precise oxygen and humidity control that extends produce shelf life while cutting retail waste by up to 30%.[1]Packaging Insights, “Retailers turn to micro-perforated films to curb food waste,” packaginginsights.com Retail adoption rises alongside consumers’ sustainability focus, as 62% now prioritize eco-friendly packs versus two years earlier. Perforated films increasingly pair with IoT sensors that track in-pack atmosphere, allowing dynamic shelf-life adjustment across multi-node supply chains. Equipment suppliers scale high-speed lasers able to drill micron-scale holes without compromising mechanical strength, thereby widening fresh-food e-commerce possibilities. Cost savings on shrinkage and improved brand credentials make micro-perforated solutions a stable growth driver for the micro-packaging market.

Expansion of Novel Drug-Delivery Formats and Biologics Pipelines

Biologics account for a growing share of FDA approvals, and pre-sterilized micro-dose vials ensure cold-chain integrity. Stevanato Group reported EUR 1.104 billion revenue in 2024, with high-value solutions—including micro-packaging—contributing 38%, underscoring demand for micron-tolerance glass forming.[2]Stevanato Group, “Stevanato Group Reports Record Revenue of €1,104 Million for Fiscal Year 2024,” stevanatogroup.comUnit-dose containers minimize waste of expensive biologics and align with personalized medicine regimens. Pharmaceutical firms invest in camera-guided forming lines that monitor wall thickness under 50 µm, reducing breakage. Regulatory bodies increasingly require packaging that mitigates dosing errors, propelling smart vials embedded with NFC tags for verification and track-and-trace compliance.

Shift to Single-Dose Adherence Packs in Outpatient Care

Global non-adherence costs surpass USD 100 billion annually, spurring hospitals and pharmacies to adopt blister or wallet packs presenting one clear dose per intake. WestRock’s Dosepak reduced patient errors by 40% through intuitive labeling and tamper evidence. QR-enabled packs connect patients to mobile reminders and instructional videos, promoting chronic-disease management outside clinical settings. Pharmacy automation systems now assemble personalized adherence packs at 1,000 prescriptions per hour, reinforcing economies of scale. Demand scales further as aging populations shift healthcare delivery to the home setting, cementing adherence formats as a mainstay of the micro-packaging market.

Sustainability Push Toward Recyclable Micro-Structures

The EU’s Packaging and Packaging Waste Regulation compels 100% recyclability by 2030. Brands pre-empt mandates with circular designs such as Accredo’s sugarcane pouch, sequestering 43 g CO₂ per unit. Minimum recycled-content thresholds—30% recycled PET for food packs by 2030—heighten demand for closed-loop feedstocks. Companies integrating design-for-recycling with proprietary reprocessing hubs enjoy lower Extended Producer Responsibility fees. Circular models can cut lifecycle emissions by 80% versus linear systems, translating to measurable Scope 3 reductions coveted by multinationals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Nanoparticle

leaching concerns

Nanoparticle

leaching concerns

| -0.8% | Global, with stricter enforcement in EU and North America | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global,

with stricter enforcement in EU and North America

|

Impact Timeline

:

Medium

term (2-4 years)

|

High

capital cost of precision micro-perforation and forming equipment

High

capital cost of precision micro-perforation and forming equipment

| -1.2% | Global, with higher barriers in emerging markets | Short term (≤ 2 years) | |||

Emerging

micro-plastic and PFAS legislation

Emerging

micro-plastic and PFAS legislation

| -0.9% | EU leading, North America following, Asia-Pacific emerging | Long term (≥ 4 years) | |||

Supply

volatility in high-barrier polymers and coatings

Supply

volatility in high-barrier polymers and coatings

| -0.7% | Global, with concentration in petrochemical-dependent regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Nanoparticle Leaching Concerns

Regulators intensify migration testing of nano-scale additives used for oxygen and UV barriers, extending launch timelines by up to a year in pharma applications. The FDA now requests exhaustive particle-size distribution profiles and accelerated-aging studies, with protocols costing USD 50,000-100,000 per formulation. European authorities demand similar datasets, prompting brands to consider non-nano alternatives such as silicon oxide coatings. [3]U.S. FDA, “Guidance for Industry: Safety of Nanomaterials in Food Packaging,” fda.gov Advocacy groups amplify health debates, pressuring retailers to delist packs lacking transparency. Firms investing early in alternative barrier chemistries gain reputational edge and avoid requalification expenses.

High Capital Cost of Precision Micro-Perforation and Forming Equipment

Next-generation laser arrays able to drill 200,000 holes per minute exceed USD 5 million per line, plus clean-room upgrades and operator training. Lead times for critical optics now stretch to 18-24 months, curtailing agile capacity additions. Smaller converters struggle to access financing, fuelling consolidation as larger groups acquire niche specialists to secure throughput. Leasing models exist but seldom cover the most advanced equipment, keeping the entry bar high and sustaining an oligopolistic supply base within key segments of the micro-packaging industry.

Segment Analysis

By Application Type: Precision Vials Secure Biologics Quality

In 2025, boxes and pouches captured 28.05% of micro-packaging market share, serving omnichannel retail and lightweight e-commerce shipping. Stable demand for multi-layer pouches with oxygen scavengers sustains volumes, while customization drives short-run box production for subscription services. Vials, however, post a 19.78% CAGR through 2031, reflecting the surge in monoclonal antibodies and mRNA therapies. Stevanato Group’s new Latina plant expands pre-sterilized vial capacity and demonstrates capital commitment to ultra-clean, low-silicon glass lines. Integrated fill-finish vendors choose vial formats enabling in-line lyophilization, reducing freeze-dry cycle loss. With global biologics facilities upscaling, vials underpin the most dynamic avenue for the micro-packaging market.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Pharma–Biotech Accelerates Beyond Food Staples

Food and beverage retained 35.38% of revenue in 2025, driven by fresh-produce innovations and on-the-go snack formats that favor breathable films and re-closeable pouches. Supply-chain pressures to curb waste align with micro-perforated solutions that deliver longer shelf life without preservatives. Pharmaceutical-biotech applications deliver a 20.98% CAGR, outpacing every other user group as complex biologics demand sterile, low-particulate packs. The micro-packaging market size for pharma injection formats is forecast to grow steadily as unit-dose adherence mandates expand hospital-to-home dispensing.

By Packaging Material: Biopolymers Propel Circularity

High-barrier features remain the largest slice at 32.08%, protecting oxygen-sensitive foods and moisture-critical APIs. Aluminum-oxide nanolaminates on 12-µm PET films now achieve transmission rates below 0.01 cc/m²/day while maintaining recyclability. Intelligent and smart formats expand at 21.85% CAGR, integrating NFC or BLE sensors that verify provenance and log temperature excursions. Avery Dennison’s Saga Card enables carton-level cold-chain visibility without bulky dataloggers. As regulatory bodies tighten traceability, smart layers continue to propel digital convergence within the micro-packaging industry.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Format: Flexible Platforms Lead Material Efficiency

Flexible solutions held 55.78% of micro-packaging market share in 2025; multi-layer stand-up pouches replace rigid jars, trimming material mass by up to 70%. Amcor’s Perflex shrink bag achieves a 22% lower carbon footprint compared with traditional films, validating eco-advantage claims. Flexible formats are forecast at an 17.75% CAGR, underpinned by their compatibility with high-speed digital printing and suitability for omnichannel fulfillment. Lightweight, cube-optimized designs boost truckload efficiency by 30%, meeting retailer emissions targets and further embedding flexibles in the micro-packaging market.

Geography Analysis

North America occupied 39.05% of the micro-packaging market in 2025. Strict FDA guidelines for container-closure integrity and FSMA requirements for track-and-trace assure sustained demand for precision forming and data-rich labels. Semiconductor fabs adopt ultra-clean dry-pack films to protect sub-10 nm wafers, fostering joint R&D between material suppliers and chipmakers. California’s PFAS law (AB 347) compels packagers to reformulate by 2029, forecasting USD 3 billion in compliance outlays for wastewater upgrades. The United States also witnesses vertical integration as converters purchase sensor startups to offer end-to-end smart-pack solutions.

Asia-Pacific grows fastest at an 18.62% CAGR through 2031, driven by Chinese subsidies for advanced semiconductor packaging lines and India’s pharmaceuticals push aligned to global supply diversification. TSMC’s panel-level fan-out roadmap intensifies requirements for ultra-thin, debris-free carrier tapes. Indian contract-development organizations add isolator-based vial lines, favoring Western regulators’ expectations for sterile micro-packaging. Southeast Asian nations court direct investment with tax incentives for bio-material facilities, constructing a regional hub for sugarcane-based resin production.

Europe maintains influence through regulatory leadership. The Packaging and Packaging Waste Regulation in force from February 2025 anchors the continent’s status as a testbed for recyclable micro-structures. Germany houses precision machinery clusters supplying laser-perforation assets to global converters, while Italy’s container-glass expertise supports high-value biologics fill-finish operations. Energy-price swings remain a cost headwind, but coordinated policy encourages heat-recovery retrofits that stabilize OPEX. Brands leveraging circular models demonstrate emission reductions up to 80%, reinforcing Europe’s export of sustainability standards that increasingly shape the global micro-packaging market.

Competitive Landscape

Market Concentration

The micro-packaging market shows moderate fragmented as top converters pursue scale and technology breadth. Amcor’s USD 8.43 billion merger with Berry Global creates a powerhouse with global extrusion, printing, and smart-label assets. Sonoco’s USD 3.9 billion Eviosys acquisition strengthens metal and rigid-paper combinational offerings, allowing cross-selling of micro-perforated lids to multinational food clients.

Competitive advantage gravitates toward firms mastering micron-level tolerances and integrated digital ecosystems. Stevanato Group invests in vision-guided glass forming, controlling dimensional variance within 20 µm for high-value injectables. Ball Corporation partners with Meadow to adapt aluminum aerosol can lines for refillable personal-care cartridges launching in 2025. These moves highlight a trend toward platform innovation where material science, automation, and IoT coalesce.

New entrants target niche white spaces. Start-ups commercialize plant-protein coating technologies that deliver comparable oxygen barriers to EVOH while fully compostable. Sensor specialists supply printable antennas compatible with standard flexo lines, enabling mass-scale smart integration without capital overhaul. Established incumbents hedge disruptive risk through venture investments and joint development agreements, maintaining a dynamic yet increasingly technology-oriented competitive landscape for the micro-packaging market.

Micro-Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stevanato Group reported EUR 1.104 million revenue with micro-packaging accounting for 38%, highlighting biologics demand.

- January 2025: Ball Corporation invested in Meadow to offer fully recyclable aluminum cartridges for home and personal-care lines.

- December 2024: Mintel launched ‘Mintel Spark’ AI concept generator to accelerate CPG pack ideation.

Table of Contents for Micro-Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Demand for micro-perforated food packaging for perishable products

- 4.2.2Expansion of novel drug-delivery formats and biologics pipelines

- 4.2.3Shift to single-dose adherence packs in outpatient care

- 4.2.4Sustainability push toward recyclable micro-structures

- 4.2.5IoT / sensor-embedded smart micro-packages

- 4.2.6Fulfilment-ready "sample size" packs for e-commerce

- 4.3Market Restraints

- 4.3.1Nanoparticle leaching concerns

- 4.3.2High capital cost of precision micro-perforation and forming equipment

- 4.3.3Emerging micro-plastic and PFAS legislation

- 4.3.4Supply volatility in high-barrier polymers and coatings

- 4.4Supply-Chain Analysis

- 4.5Technological Outlook

- 4.6Regulatory Landscape

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Application Type

- 5.1.1Vials

- 5.1.2Micro-perforated Films and Bags

- 5.1.3Boxes and Pouches

- 5.1.4Trays

- 5.1.5Blister Packs

- 5.1.6Other Application Types

- 5.2By End-User

- 5.2.1Food and Beverage

- 5.2.2Pharmaceutical and Biotech

- 5.2.3Personal Care and Household

- 5.2.4Electronics and Semiconductors

- 5.2.5Other End-Users

- 5.3By Packaging Material

- 5.3.1Plastics and Polymers (PET, PP, EVOH, etc.)

- 5.3.2Paper and Paperboard

- 5.3.3Metals and Foils (Al, Tinplate)

- 5.3.4Glass

- 5.3.5Biopolymers / Edible Films

- 5.3.6Other Packaging Materials

- 5.4By Packaging Functionality

- 5.4.1High-Barrier / Oxygen-Scavenging

- 5.4.2Active Packaging (antimicrobial, moisture control)

- 5.4.3Intelligent / Smart (sensor-embedded, RFID)

- 5.4.4Controlled-Release / Adherence

- 5.4.5Edible / Compostable

- 5.5By Packaging Format

- 5.5.1Flexible

- 5.5.2Rigid

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Russia

- 5.6.2.7Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2India

- 5.6.3.3Japan

- 5.6.3.4South Korea

- 5.6.3.5Australia and New Zealand

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1Middle East

- 5.6.4.1.1United Arab Emirates

- 5.6.4.1.2Saudi Arabia

- 5.6.4.1.3Turkey

- 5.6.4.1.4Rest of Middle East

- 5.6.4.2Africa

- 5.6.4.2.1South Africa

- 5.6.4.2.2Nigeria

- 5.6.4.2.3Egypt

- 5.6.4.2.4Rest of Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Amcor plc

- 6.4.2Sonoco Products Co.

- 6.4.3Gerresheimer AG

- 6.4.4Uflex Ltd.

- 6.4.5Huhtamaki Oyj

- 6.4.6Thermo Fisher Scientific

- 6.4.7Stevanato Group S.p.A.

- 6.4.8Constantia Flexibles

- 6.4.9KM Packaging Services Ltd.

- 6.4.10A-ROO Company

- 6.4.11Ultraperf Technologies Inc.

- 6.4.12Bolloré SE

- 6.4.13Mondi plc

- 6.4.14Sonoco Alloyd

- 6.4.15Chengde Technology Co., Ltd.

- 6.4.16TCL Packaging

- 6.4.17Bemis (now part of Amcor)

- 6.4.18Schott AG

- 6.4.19AptarGroup Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Micro-Packaging Market Report Scope

Micro-packaging makes use of nanomaterials for prospective advantages such as enhanced antimicrobial effects, bio-availability, targeted deliverance of bioactive composites, thus increasing the demand for the micro packaging market in the end-user such as food, pharma, cosmetics, etc.