Anti-Counterfeit Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

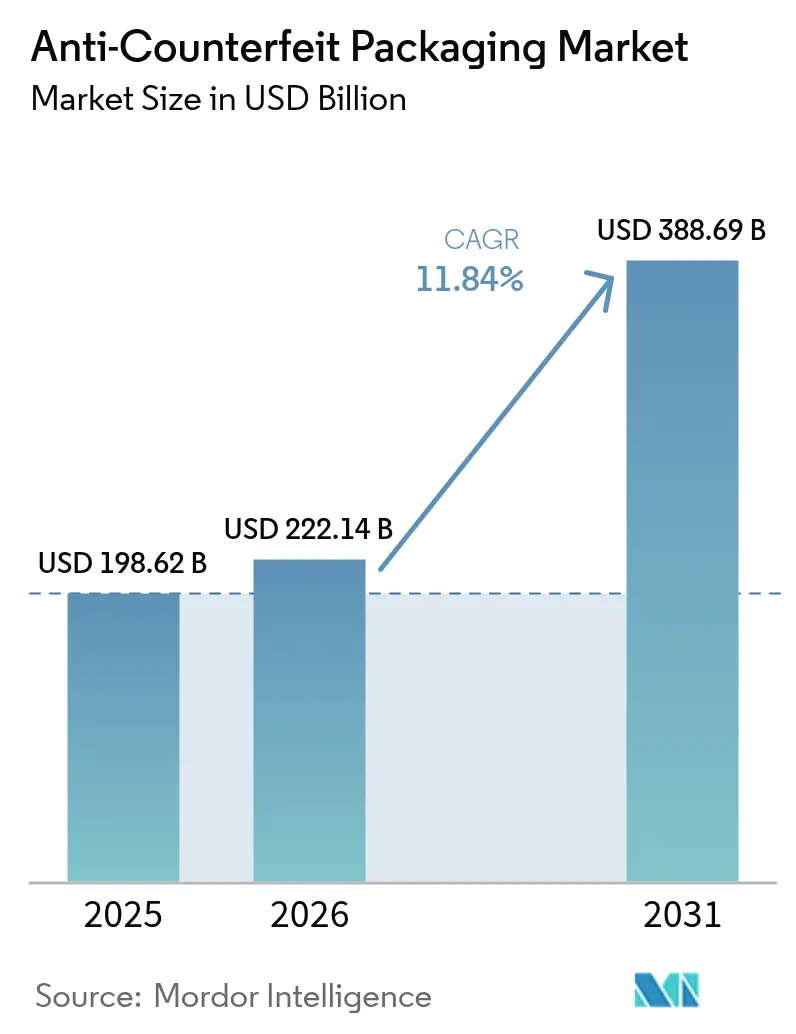

| Market Size (2026) | USD 222.14 Billion |

| Market Size (2031) | USD 388.69 Billion |

| Growth Rate (2026 - 2031) | 11.84% CAGR |

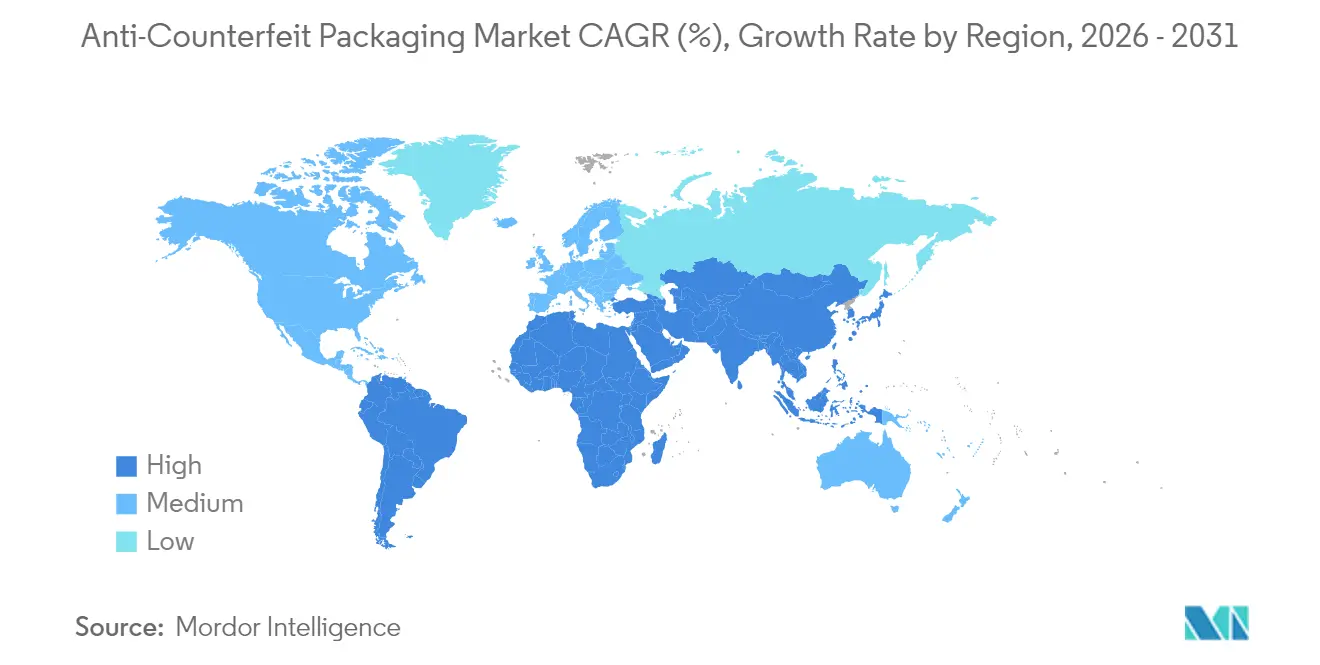

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Counterfeit Packaging Market Analysis by Mordor Intelligence

Anti-Counterfeit Packaging market size in 2026 is estimated at USD 222.14 billion, growing from 2025 value of USD 198.62 billion with 2031 projections showing USD 388.69 billion, growing at 11.84% CAGR over 2026-2031. Rising counterfeit sophistication, the spread of generative-AI printing, and a wave of tighter global traceability laws continue to enlarge the addressable opportunity for security technologies. Pharmaceutical serialization deadlines in the United States and the European Union anchor a sizable base of recurring demand, while new food, electronics, and luxury-goods mandates open fresh growth lanes. Brand owners increasingly look beyond visible holograms to multi-layered solutions that blend covert nano-pigment inks, mobile-readable digital watermarks, and blockchain provenance, ensuring that packages defend themselves throughout e-commerce fulfilment and reverse logistics. Large converters face material-cost inflation yet keep investing in embedded RFID and invisible watermarking because operating data show counterfeit incursions erode brand equity faster than packaging outlays rise. Venture investment stays healthy thanks to evidence that connected packs can double consumer-engagement time, turning security spend into a marketing asset.

Key Report Takeaways

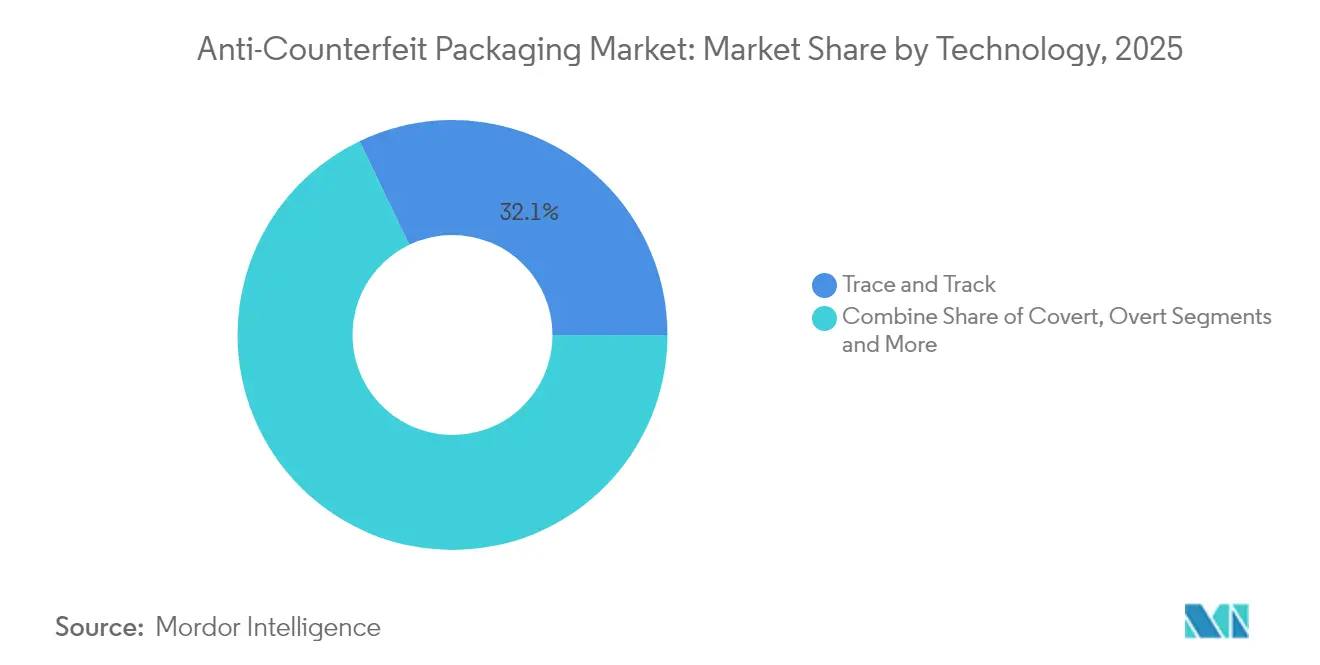

- By technology, Trace and Track systems held 32.12% of Anti-Counterfeit Packaging market share in 2025; Forensic Markers post the highest forecast CAGR at 15.1% to 2031.

- By usage feature, Serialization Codes captured 35.95% share in 2025, while RFID/NFC Tags are set to expand at 16.28% CAGR through 2031.

- By packaging component, Labels and Tags commanded 32.84% revenue in 2025; Security Inks and Coatings grow the fastest at 14.62% CAGR to 2031.

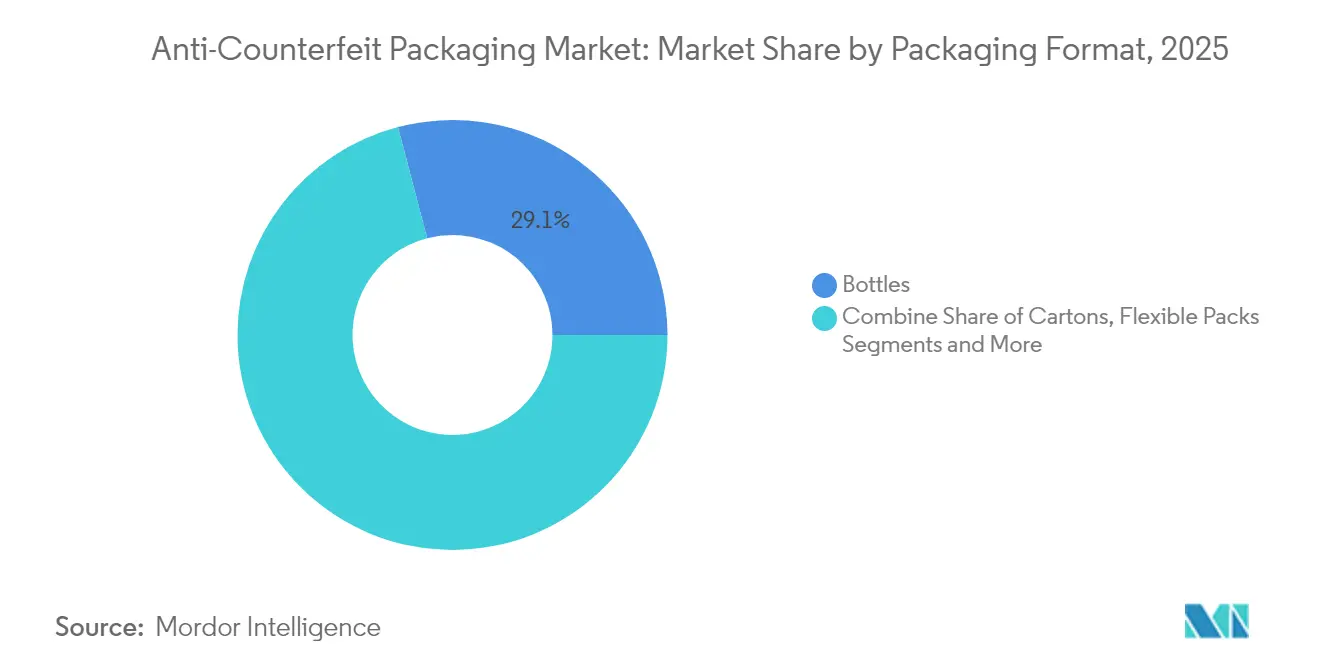

- By packaging format, Bottles led with 29.08% share in 2025, whereas Flexible Packs pace the field at 16.28% CAGR, driven by e-commerce fulfilment needs.

- By end-user sector, Healthcare and Pharmaceuticals retained 30.02% share in 2025; Consumer Electronics records the fastest 15.05% CAGR owing to premium-device counterfeiting.

- By geography, North America dominated with 38.64% share in 2025, while Asia-Pacific accelerates at 15.72% CAGR, spurred by China’s stricter labeling code.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Counterfeit Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce-driven serialization demand | +2.8% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Proliferation of national track-and-trace mandates | +3.2% | North America & EU primary, APAC emerging | Medium term (2-4 years) |

| Expansion of QR/NFC-enabled connected packaging | +2.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Nano-pigment security inks enabling low-cost authentication | +1.9% | Global manufacturing hubs, Asia-Pacific focus | Long term (≥ 4 years) |

| Blockchain-based provenance pilots maturing into roll-outs | +1.5% | North America & EU leading, selective APAC adoption | Long term (≥ 4 years) |

| AI image-forensics integrated into consumer apps | +1.2% | Global, technology-forward markets first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid e-commerce-driven serialization demand

Surging online sales shorten distribution chains and remove physical inspection points, forcing brands to embed unit-level digital identifiers that travel with every parcel. RFID pilots between Avery Dennison and US grocery chains show scan rates above 99% accuracy, confirming that serialized data flow improves both inventory turns and counterfeit detection. [1]Avery Dennison, “Avery Dennison Expands RFID Adoption in Grocery Retail Industry,” averydennison.comCloud dashboards now fit into fulfilment apps, so retailers block suspected fakes before last-mile dispatch, preserving shopper trust. The trend shifts cap-ex priority toward print-on-demand coders and away from decorative embellishments, raising the strategic value of software-ready converters in the Anti-Counterfeit Packaging market.

Proliferation of national track-and-trace mandates

After the United States enforced DSCSA unit-level traceability in late-2024, pharmaceutical exporters equipped plants worldwide with EPCIS-ready coding platforms to avoid dual inventories. The European Union’s FMD introduced parallel serialization and tamper-evident rules, prompting a template that Brazil, Saudi Arabia, and Thailand study for rollout. When regulations converge, vendors in the Anti-Counterfeit Packaging market win multi-country service contracts and amortize R&D faster, reinforcing scale advantages.

Expansion of QR/NFC-enabled connected packaging

Regulators in India now oblige top-selling medicines to carry QR codes that point to cloud repositories, while consumer-goods majors embed NFC chips so users tap phones to unlock loyalty perks. Digimarc’s watermark trials with Procter & Gamble cut counterfeit detection times by 60%, proving that invisible codes withstand image compression on social feeds. Brands thus repurpose security spend into digital-marketing infrastructure, expanding solution budgets inside the Anti-Counterfeit Packaging market.

Nano-pigment security inks enabling low-cost authentication

Flexographic formulations doped with TiO₂ and ZnO nanoparticles create spectral signatures that only FTIR readers detect, adding hidden layers at marginal ink cost. [2]MDPI, “Fine-Tuning Flexographic Ink's Surface Properties and Providing Anti-Counterfeit Potential via the Addition of TiO₂ and ZnO Nanoparticles,” mdpi.com DuPont’s drupa 2024 launch of low-viscosity Artistri inks shows large chemical incumbents aligning with printer OEMs to mainstream nano-pigment capability. [3]DuPont, “DuPont to Showcase New Innovative Artistri® Digital Printing Inks at drupa 2024,” dupont.comAs volumes scale, unit economics favor mass brands that long skipped advanced features, broadening the Anti-Counterfeit Packaging market addressable base.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for full-line serialization retro-fits | -2.1% | Global manufacturing centers, particularly Asia-Pacific | Short term (≤ 2 years) |

| Inter-operability gaps between global coding standards | -1.8% | Multi-regional supply chains, cross-border trade routes | Medium term (2-4 years) |

| Data-privacy and cybersecurity liabilities in cloud TandT | -1.4% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Counterfeiters' rapid adoption of generative printing | -1.2% | Global, with concentration in manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex for full-line serialization retro-fits

Legacy fillers and cartoners often lack space for vision cameras and reject stations, so firms must buy new turnkey lines rather than bolt-on modules. Although TraceLink’s no-code OPUS platform eases integration of data layers, hardware outlays still average USD 1 million per bottle line. Small generics players and contract packers in India and Vietnam defer upgrades, shrinking their accessible share of the Anti-Counterfeit Packaging market until financing improves.

Inter-operability gaps between global coding standards

GS1 EPCIS schemas exist, yet transport layers and reporting file specs differ by regulator, forcing exporters to keep multiple middleware stacks. TraceLink secured all 16 GS1 US conformance trustmarks only after extensive custom parsing routines. Duplicate efforts increase IT cost per SKU and slow pilot cycles, diluting ROI for some adopters in the Anti-Counterfeit Packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Regulatory mandates keep Trace and Track in command

In 2025, Trace and Track solutions captured 32.12% of the Anti-Counterfeit Packaging market, equal to an Anti-Counterfeit Packaging market size of roughly USD 63.8 billion, while Forensic Markers are projected to post a brisk 15.1% CAGR to 2031. Serialization hardware, vision inspection, and cloud vaults form a compliance backbone that pharmaceutical lines cannot sidestep. As counterfeiters mimic overt holograms with AI-guided presses, brands pivot to covert DNA inks and forensic taggants that require lab-grade readers, pushing solution diversity within the Anti-Counterfeit Packaging market.

Generative-AI printing tools now replicate guilloché patterns and kinetic micro-text with startling fidelity, cutting the deterrent value of purely visible marks. Research at MIT on terahertz-wave ID tags opens hope for tamper-proof physical-fingerprint systems that link packages to a unique spectral signature. Vendors selling hybrid traceability plus forensic stacks, therefore, command higher margins and lengthier service contracts.

By Usage Feature: Serialization Codes maintain dominance while RFID/NFC scales fast

Serialization Codes owned 35.95% of Anti-Counterfeit Packaging market share in 2025, supplying the backbone for DSCSA and FMD compliance; RFID/NFC, at a 16.28% CAGR, outpaces all other features as smartphone adoption universalizes contactless reading. Pack-level GS1 Digital Link formats now bind EPC codes to web-resolvable URLs, so consumers verify goods inside shopping apps.

Holographic seals still appear on spirits and luxury cosmetics because visual flair complements brand aesthetics. Yet digital watermarks, embedded invisibly in artwork, allow zero-ink alterations during line changeovers. Digimarc’s integration of such marks into the C2PA 2.1 standard shows how packaging and online imagery share one verification protocol. This convergence increases subscription revenue pools inside the Anti-Counterfeit Packaging market.

By Packaging Component: Labels and Tags keep the lead as inks race ahead

Labels and Tags represented 32.84% of total spend in 2025, yet Security Inks and Coatings will likely outrun them through a 14.62% CAGR as converters blend nano-pigments straight into flexo units. Embedding authentication within the print layer prevents label swapping and lowers changeover downtime.

Simultaneously, converters promote linerless facestock to curb waste, aligning security with sustainability. Films and pouches seize flexible-pack growth, adding metallized layers that double as light barriers and covert optical filters. Hologram suppliers fight commoditization by experimenting with volume Bragg gratings that sparkle at lower microns, defending a premium niche of the Anti-Counterfeit Packaging market.

By Packaging Format: Flexible Packs pace growth while bottles stay foundational

Bottles, notably in oral solids and beverages, accounted for 29.08% of 2025 revenue. Still, flexible packs chart a 16.28% CAGR as e-commerce shippers prefer lightweight, durable sachets that survive last-mile drops. QR-enabled pouches now carry freshness data and expiry alarms, enhancing value.

Cartons keep relevance because large printable panels host overt and covert layers in one pass. Blister packs stay indispensable where unit-dose accountability matters, though slower growth suggests saturation. Overall, line versatility guides capital flows, with packers weighing SKU complexity against the ROI every Anti-Counterfeit Packaging market upgrade promises.

By End-User Industry: Electronics outlook brightens as drugs anchor volume

Healthcare and Pharmaceuticals controlled 30.02% of spending in 2025, a pillar that ensures baseline orders for mandatory serial numbers and tamper-evident rings. The segment’s recurring maintenance fees give suppliers steady cash, lowering portfolio risk.

Consumer Electronics projects a 15.05% CAGR thanks to high-margin gadgets that face organized counterfeit rings. NFC-enabled boxes allow instant warranty activation, turning packages into service gateways. Food and beverage brands climb the adoption curve too, as origin labeling rules stiffen in China and the EU. Each new vertical widens the Anti-Counterfeit Packaging market and spreads fixed platform costs over more SKUs.

Geography Analysis

North America retained 38.64% revenue in 2025, buoyed by full DSCSA enforcement and a dense network of CMOs that need turnkey coding, inspection, and data-exchange stacks. Canada’s Plastics Pact also nudges converters to blend security and recyclability, favoring fiber-based packs that carry invisible watermark tracers enabling automated sortation. Mexico, intertwined with US supply chains, ramps anti-counterfeit adoption in medical devices and tequila exports to safeguard market access.

Asia-Pacific registers the swiftest 15.72% CAGR, driven by China’s new pre-packaged labeling law, India’s QR-code drug lists, and Japan’s Positive List for food-contact resins. Contract manufacturers across Guangdong and Ho Chi Minh City deploy low-cost inkjet coders and blockchain pilots to satisfy multinational audits. Flexible-pack printers in Indonesia install nano-pigment stations after early ROI studies show counterfeit returns fall by half within one year, proving the Anti-Counterfeit Packaging market’s potential beyond legacy pharma hubs.

Europe holds a mature but sizable share, with FMD and the upcoming Packaging and Packaging Waste Regulation intertwining sustainability and security. Brands explore fibre-based barrier packs paired with Digimarc watermarks so automated sorters read signals through dirt and glare. Russia’s PET bans and the EU’s BPA prohibition push resin switchovers, which in turn invite fresh security print trials. The Middle East and Africa remain nascent, yet luxury auto-parts suppliers in the Gulf invest in 2D code vaults to reassure global buyers, hinting at a wider Anti-Counterfeit Packaging market take-off once regional customs unions finalize common coding laws.

Competitive Landscape

The Anti-Counterfeit Packaging market stays moderately fragmented. Conglomerates such as Avery Dennison, 3M, and CCL Industries exploit scale to offer bundled RFID, labels, and cloud dashboards. Their global service networks reassure multinationals that serialization lines stay compliant across continents. Niche leaders like SICPA, AlpVision, and Digimarc capture premium segments with proprietary taggants, spectral fingerprinting, or digital watermark IP that counterfeiters find hard to crack.

Strategic moves center on capability convergence. Crane NXT’s USD 270 million purchase of OpSec Security merged micro-optics with banknote know-how, forming a cradle-to-grave brand-protection suite. 3M’s entry into the semiconductor consortium refines conductive adhesives that could double as covert circuitry on labels, expanding cross-selling routes [3M press release, Feb 2025]. Material inflation raises switching costs, so converters differentiate on total-cost analytics, showing clients how RFID inlays reduce write-offs that dwarf per-label price hikes.

Patent landscapes evolve quickly. Meta’s optical-modulation filings hint at next-gen holographic layers with dynamic imagery whose charge-carrier pattern shifts under polarized light. Start-ups test AI image-forensics that let customs officers confirm authenticity using smartphone cameras. Competitive intensity therefore hinges on software ecosystems as much as print chemistry, nudging traditional ink makers to partner with SaaS traceability portals and thus stay relevant within the Anti-Counterfeit Packaging market.

Anti-Counterfeit Packaging Industry Leaders

Avery Dennison Corporation

CCL Industries Inc.

3M Company

Zebra Technologies Corporation

E.I. Du Pont De Nemours and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Crane NXT completed its purchase of OpSec Security to build an integrated authentication platform.

- February 2025: 3M joined the US-JOINT semiconductor packaging consortium to advance materials for AI compute.

- January 2025: Honeywell supplied technology to Vioneo’s USD 1.6 billion Antwerp plant producing fossil-free virgin plastics.

- January 2025: DS Smith launched TailorTemp, a recyclable fiber-based cold-chain pack for pharmaceuticals.

Global Anti-Counterfeit Packaging Market Report Scope

Anti-counterfeiting packaging is incorporated to prevent imitation and confirm the goods' safety. Companies take these measurements to help them minimize losses due to counterfeiting in terms of revenue and loyalty. The counterfeiting industry is flourishing, and it is not only the consumer goods market that is affected. There has been an increase in counterfeit prescription drugs, car parts, and technologies (such as cell phone batteries), which are flooding the market in the future.

The anti-counterfeit packaging market is segmented by technology (trace and track, tamper-evident, covert, overt, and forensic markers), end-user (food and beverages, healthcare and pharmaceuticals, industrial and automotive, consumer electronics), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, Rest of Europe], Asia-Pacific [China, Japan, India, Australia, Rest of Asia Pacific], Latin America [Brazil, Argentina, Rest of Latin America], Middle East and Africa [South Africa, United Arab Emirates, Rest of the Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Trace and Track |

| Tamper-Evident |

| Covert |

| Overt |

| Forensic Markers |

| Serialization Codes |

| RFID / NFC Tags |

| Holographic Seals |

| Digital Watermarks |

| Labels and Tags |

| Security Inks and Coatings |

| Films and Pouches |

| Holograms |

| Other Packaging Component |

| Blister Packs |

| Bottles |

| Cartons |

| Flexible Packs |

| Other Packaging Format |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Industrial and Automotive |

| Consumer Electronics |

| Other End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Trace and Track | ||

| Tamper-Evident | |||

| Covert | |||

| Overt | |||

| Forensic Markers | |||

| By Usage Feature | Serialization Codes | ||

| RFID / NFC Tags | |||

| Holographic Seals | |||

| Digital Watermarks | |||

| By Packaging Component | Labels and Tags | ||

| Security Inks and Coatings | |||

| Films and Pouches | |||

| Holograms | |||

| Other Packaging Component | |||

| By Packaging Format | Blister Packs | ||

| Bottles | |||

| Cartons | |||

| Flexible Packs | |||

| Other Packaging Format | |||

| By End-User Industry | Food and Beverage | ||

| Healthcare and Pharmaceuticals | |||

| Industrial and Automotive | |||

| Consumer Electronics | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current Anti-Counterfeit Packaging market size?

The Anti-Counterfeit Packaging market size reached USD 222.14 billion in 2026 and is forecast to hit USD 388.69 billion by 2031 at a 11.84% CAGR.

Which technology leads the Anti-Counterfeit Packaging market?

Trace and Track serialization systems lead, holding 32.12% share in 2025, due to mandatory compliance in pharmaceuticals and fast-moving consumer goods.

Which region grows the fastest in Anti-Counterfeit Packaging?

Asia-Pacific posts the highest 15.72% CAGR to 2031, propelled by China’s new labeling laws and India’s QR-code drug mandates.

How are brands integrating digital features into packs?

Companies blend QR codes, NFC tags, and digital watermarks with cloud platforms, letting consumers verify authenticity through smartphones while brands collect engagement data.

What restrains wider Anti-Counterfeit Packaging adoption?

High capital outlays for retrofitting serialization hardware and inconsistent coding standards across countries slow smaller manufacturers’ implementation pace.

Who are key players in the Anti-Counterfeit Packaging industry?

Major suppliers include Avery Dennison, 3M, CCL Industries, SICPA, AlpVision, and Digimarc, each leveraging unique combinations of labels, RFID, inks, or digital watermarks to protect products.

Page last updated on: