Self Heating Food Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 65.85 Billion |

| Market Size (2031) | USD 81.56 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

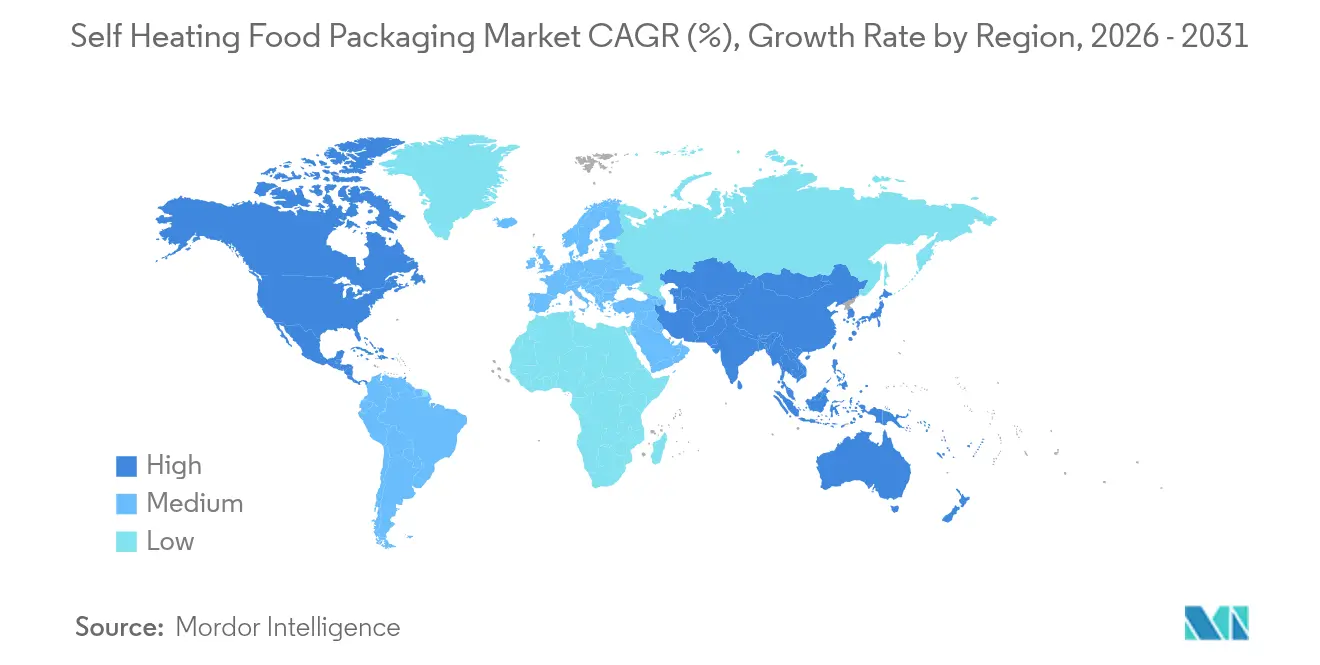

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self Heating Food Packaging Market Analysis by Mordor Intelligence

The self heating food packaging market size was valued at USD 63.09 billion in 2025 and estimated to grow from USD 65.85 billion in 2026 to reach USD 81.56 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031). The current growth trajectory reflects the diffusion of military-grade heater technology into mainstream convenience formats, sharper regulatory clarity around calcium-oxide micro-capsules, and stronger retail visibility for flexible packs. North American demand holds steady thanks to recurring defense orders, while Asia-Pacific accelerates on the back of urban lifestyles and e-commerce-driven meal-kit adoption. Continuous advances in exothermic chemistry, notably safer encapsulated gel packs, lower the barrier for civilian uptake, and direct-to-consumer brands exploit social commerce to command premium pricing. Intensifying patent filings around aluminum-silica cartridges signal sustained R&D investment as manufacturers seek both heat-rate control and end-of-life recyclability, positioning the self heating food packaging market for stable medium-term expansion.

Key Report Takeaways

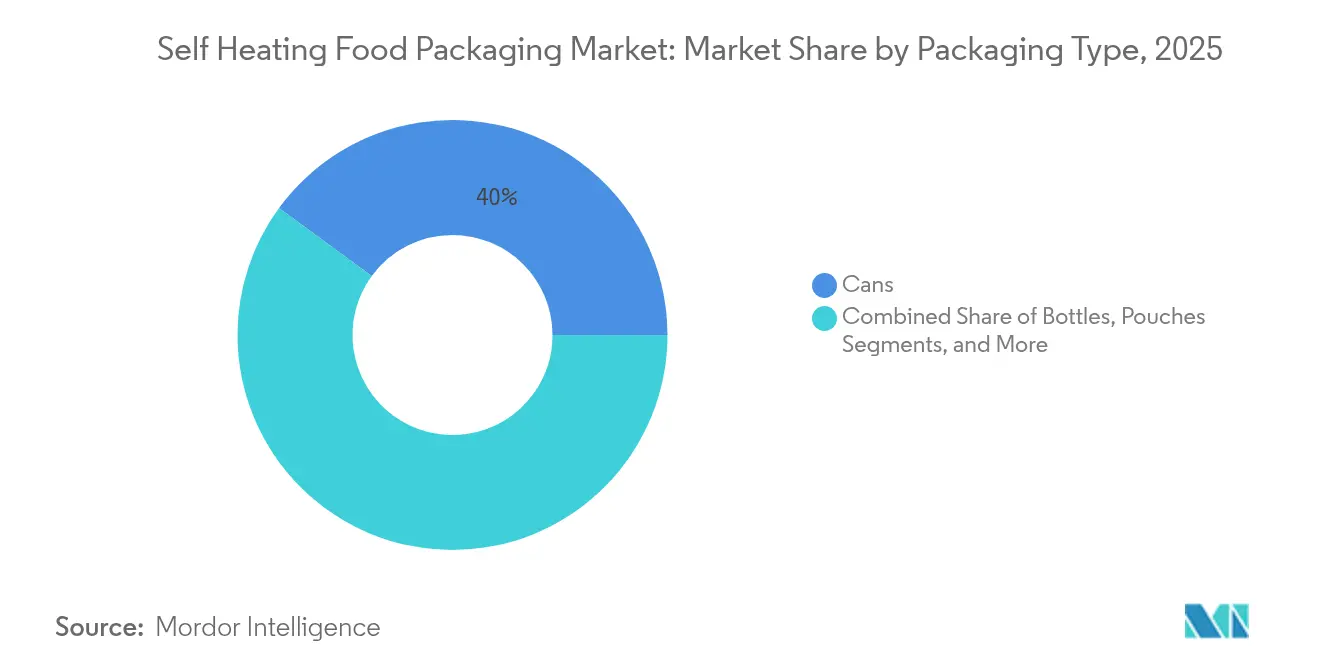

- By packaging type, cans led with 39.95% of self heating food packaging market share in 2025; pouches are forecast to expand at a 7.17% CAGR to 2031.

- By end-user vertical, food commanded 69.74% share of the self heating food packaging market size in 2025, while beverages record the highest projected CAGR at 6.21% through 2031.

- By heating chemistry, quicklime-water systems captured 28.11% of the self heating food packaging market share in 2025; encapsulated gel packs are projected to grow at an 8.31% CAGR to 2031.

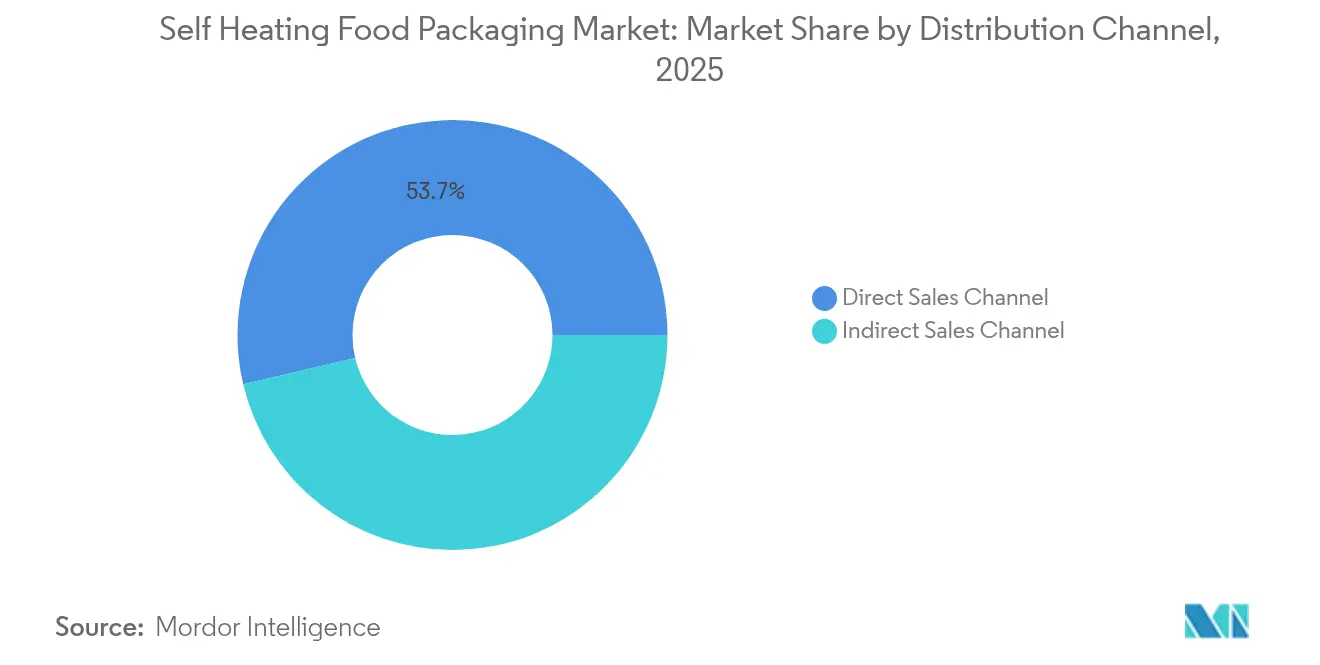

- By distribution channel, direct sales held 53.68% share of the self heating food packaging market size in 2025, whereas indirect channels are advancing at an 8.62% CAGR through 2031.

- By geography, North America accounted for 35.05% revenue share in 2025; Asia-Pacific is set to register the fastest 7.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self Heating Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for wholesome on-the-go meals | +0.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Military, disaster-relief and field-service rationing demand uptick | +0.6% | North America and Europe, expanding to MEA | Short term (≤ 2 years) |

| Product premiumisation of ready-to-drink coffee and tea cans | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Advancements in calcium-oxide micro-capsule heater safety | +0.4% | Global | Long term (≥ 4 years) |

| Integration of smart sensors for temperature-verified delivery | +0.3% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Surge in outdoor recreation and e-commerce meal-kit adoption | +0.7% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Wholesome On-the-Go Meals

Urban consumers favour balanced, ready-to-heat meals that remove the microwave altogether, and the self heating food packaging market turns this need into a premium feature rather than a novelty. China’s prepared-food revenue topping CNY 500 billion in 2024 underlines the commercial scale of convenience-centric diets. HeaterMeals shows the practicality of iron-magnesium-salt heaters that raise food temperature by 100 °F in 10 minutes, marrying speed with portion control Homefront Emergency. Brands routinely price self-heating SKUs 40-60% above ambient retort pouches, yet online grocery platforms register healthy repeat purchase rates as consumers trade up for time savings. The trend unlocks cross-category extensions, from rice bowls to functional soups, anchoring volume growth in the self heating food packaging market.

Military, Disaster-Relief and Field-Service Rationing Demand Uptick

Defense agencies remain the technology incubator for flameless heater packs. The U.S. Army demonstrated 60-second meal warm-up kits at its 2024 Culinary Industry Day, reinforcing performance standards for commercial suppliers. [1]U.S. Army, “Army holds first culinary industry day to generate ideas, feedback,” army.mil Luxfer Magtech expects utility gas and rescue (UGRE) heater sales to double in 2025 as procurement cycles widen beyond NATO arenas. Humanitarian organisations value the ability to distribute shelf-stable hot meals in climate emergencies, broadening contract opportunities. Energy crews working in remote fields add another customer cohort, cementing baseline demand that cushions cyclical swings in the self heating food packaging market.

Product Premiumization of Ready-to-Drink Coffee and Tea Cans

Single-serve hot beverage cans exploit sensory appeal to cut through a saturated refreshment aisle. The 42 Degrees Company elevates calcium-oxide heaters to deliver a 42 °C lift inside three minutes, merging indulgence with grab-and-go convenience.[2]The 42 Degrees Company, “Our Self Heating Technology,” the42degreescompany.comCoffee and tea labels have leveraged vending machines and commuter kiosks to drive trial, capturing 50-80% price gaps over non-heated equivalents. Beverage makers also pair heating with QR-code freshness tracking, reinforcing brand perception around quality and safety. As premiumisation remains price-inflexible, this channel supplies high-margin growth pockets for the self heating food packaging market

Advancements in Calcium-Oxide Micro-Capsule Heater Safety

Micro-encapsulation moderates exothermic rate, reducing burn incidents and satisfying insurer guidelines. The FDA’s GRAS recognition for calcium oxide in food contact clears the regulatory bottleneck for broader retail roll-outs.[3]U.S. Food and Drug Administration, “Finding of No Significant Impact for Food Contact Notification No. 1926,” fda.gov New patents integrate auto-shutdown films that interrupt the reaction once a setpoint is reached, preserving meal texture and consumer confidence Coffey et al.. R&D focus now shifts to recycling spent reactants into cement additives, aligning heater systems with emerging circular-packaging policies. These advances collectively widen the eligible user base, reinforcing long-term resilience of the self heating food packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety and burn-injury concerns over exothermic heaters | -0.9% | Global, particularly in consumer markets | Short term (≤ 2 years) |

| High unit cost versus retort and microwaveable packs | -0.7% | Global, with emphasis on price-sensitive markets | Medium term (2-4 years) |

| Patchy regulatory approvals for chemical heating agents | -0.5% | Europe and Asia-Pacific core, limited impact in North America | Medium term (2-4 years) |

| End-of-life disposal issues of spent heater residues | -0.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety and Burn-Injury Concerns Over Exothermic Heaters

Retailers weigh liability exposure when stocking self-heating SKUs, and negative press around misuse can slow shelf authorisations. Henkel’s guidance on hot-melt adhesive safety illustrates industry-wide emphasis on thermal PPE and consumer instructions. The FDA continues to evaluate migration risk under environmental assessments, and each favourable finding eases regulatory hesitation. Brands invest in pictorial operating guides and temperature-indicator labels to mitigate misuse. While incidents remain statistically rare, perception keeps insurance premiums elevated, adding friction to the self heating food packaging market.

High Unit Cost Versus Retort and Microwaveable Packs

Self-heating formats carry extra bill-of-materials from reactant sachets, heat-resistant liners and gas-release vents. Specialized calcium and magnesium alloy suppliers have limited capacity, which constrains bulk price negotiations Food Manufacturing. Fragmented regional demand restricts economies of scale, though rising Asia-Pacific volumes signal relief prospects. Consumers show varied willingness to absorb the premium; younger urban segments accept the trade-off, but large family buyers often default to cheaper retort pouches. Manufacturers therefore target workplace vending and outdoor recreation first, delaying mass grocery penetration and capping near-term upside in the self heating food packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Pouches Drive Innovation

Cans claimed 39.95% of self heating food packaging market share in 2025 on the strength of proven metal-can logistics and fill-seal lines, yet pouches outpace all rivals at a 7.17% CAGR to 2031 as brands migrate to lightweight flexible substrates. This shift compresses freight costs and appeals to hikers, campers and military units burdened by load weight. Rigid bottles sustain niche relevance for premium beverages that rely on tactile cues, while hybrid laminate trays test the waters in institutional catering.

Advances in aluminum-silica heater cartridges allow safe exothermic reactions inside laminated films, expanding pouch viability and smoothing the thermal gradient across the food mass. Heat-resistant polyolefins keep seal integrity despite the internal reaction, and some suppliers pilot compostable outer wraps that do not compromise barrier performance. Together, these innovations keep pouches at the forefront of unit-growth within the self heating food packaging market.

By End-user Vertical: Beverage Segment Accelerates

Food applications dominated the self heating food packaging market size with a 69.74% revenue share in 2025, underwritten by ready-to-eat meals for defense, emergency and outdoor leisure. Beverage lines grow faster, registering a 6.21% CAGR through 2031 as premium canned coffee and functional teas harness heat-on-demand to differentiate on taste and aroma. Soups blur category boundaries, offering both hydration and satiety in a single SKU.

Consumer polls show higher perceived value in beverage formats because flavour release is immediate and easily sensed. Coffee roasters add nitrogen flushing to maintain aroma during storage, then rely on fast-acting heaters to unlock aromatics at the point of use. The segment’s agility in vending networks fuels trial, positioning beverages as the headline growth engine inside the self heating food packaging market.

By Heating Chemistry: Gel Packs Emerge as Safer Alternative

Quicklime-water systems retained 28.11% self heating food packaging market share in 2025 thanks to decades of military validation, yet encapsulated gel packs top growth charts at an 8.31% CAGR to 2031 as consumer brands prioritise burn avoidance and reaction control. Magnesium-iron alloy blends stay relevant for high-heat applications, while phase-change salt compounds inch forward for extended warming cycles.

Gel-based heaters immobilise reactants within a polymer matrix, reducing leakage risk and enabling shaped heater pads that conform to non-cylindrical packs. The technology also shortens end-use training since actuation merely involves pressing a marked area rather than adding water. These traits broaden retail acceptance and reinforce the innovation narrative driving the self heating food packaging market.

By Distribution Channel: Indirect Sales Gain Momentum

Direct institutional contracts generated 53.68% of self heating food packaging market size in 2025 because military, disaster-relief and industrial buyers require customised rations and compliant documentation. Indirect channels grow 8.62% annually as supermarkets, convenience stores and e-commerce platforms normalise the format.

Online storefronts maintain higher margin capture while educating consumers with video tutorials. In physical retail, end-cap demonstrations have proven effective at overcoming first-use hesitation. As household familiarity builds, indirect distribution is on course to outstrip direct sales in absolute volume, realigning go-to-market strategies across the self heating food packaging market.

Geography Analysis

North America contributed 35.05% of global revenue in 2025 and remains the technology bellwether. U.S. defense budgets allocate multiyear funds for next-generation ration heaters, sustaining large production runs that underpin supplier economics. Civilian uptake benefits from a mature outdoor recreation culture and frequent climatic disruptions that strengthen emergency meal preparedness. Canadian relief agencies place standing orders for shelf-stable hot meals, while Mexico’s rising middle class adds incremental urban convenience demand. The regulatory climate is favourable, with the FDA’s clear stance on calcium-oxide contact uses accelerating brand plans.

Asia-Pacific registers the fastest 7.05% CAGR to 2031. China’s food sector revenue passing CNY 5.5 trillion in 2024 unlocks scale for mass-market self-heating bowls. Japan’s vending-machine density and ageing population encourage hot bento formats, evidenced by Kamakura Foods’ local subsidiary in Osaka. South Korea’s early-adopter consumers embrace app-connected heaters, and India sees pilot projects in rail catering. Regional regulators are streamlining chemical-heater approvals, though China and Australia enforce strict residue-disposal norms, nudging innovators toward recyclable reactants that sustain market momentum.

Europe delivers steady growth anchored in sustainability leadership. Germany’s engineering clusters refine heater cartridges for recyclability, while the United Kingdom’s RPS 112 lays groundwork for plastic reuse in heated packs. France and Italy position self-heating cuisine as an artisanal extension of their culinary heritage, targeting tourists and premium retailers. EU Regulation 2022/1616 on recycled plastics in food contact pushes material innovation toward high-heat PET blends. Although Europe’s caution on chemical heaters moderates uptake, the region’s focus on circular models and premiumisation keeps value share intact within the self heating food packaging market.

Competitive Landscape

The self heating food packaging market shows moderate fragmentation, with packaging multinationals, defence-oriented heater specialists and agile start-ups competing on safety, speed and sustainability. Crown Holdings leverages its extensive can-making network and posted USD 3.074 billion Q3 2024 segment sales, boosted by North American food-can demand. Luxfer Magtech anchors defence business with proprietary UGRE heaters and forecasts doubled 2025 sales on wider NATO procurement.

Emerging entrants differentiate through user-centric design. The 42 Degrees Company integrates one-hand activation and vent-less pressure control, striking distribution deals with humanitarian agencies. HeatGenie’s patent estate covers auto-shutdown alloys, which it licenses to beverage brands seeking premium positioning. Vertical integration trends continue as can-makers acquire heater IP, while chemistry firms partner with film suppliers to co-develop recyclable reactant housings. Patent analytics highlight clustering around aluminum-silica cartridges and micro-encapsulated gels, signalling next-generation heat management. Competitive intensity thus pivots on intellectual property strength, supply reliability, and compliance track-record rather than pure production scale, sustaining healthy rivalry within the self heating food packaging market.

Self Heating Food Packaging Industry Leaders

Luxfer Magtech Inc.

Tempra Technology Inc.

HeatGen LLC

The 42 Degrees Company SL

Crown Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Three High debuts GOEMON-460 bottom heater at FOODTECH TAIPEI 2025, offering energy-efficient can warming solutions.

- May 2025: Wada FoodTech wins FVD Award for its Gen6 hot-chain platform that dispenses hot dim-sum bento within nine seconds Wada FoodTech.

- May 2025: Perstorp launches Akestra™ polyester enabling 90% rPET in heat-resistant trays, cutting greenhouse emissions by 70% Perstorp.

- April 2025: Graphic Packaging unveils PaperSeal™ Cook Tray for oven- and microwave-ready meals Graphic Packaging.

Global Self Heating Food Packaging Market Report Scope

Self-heating or self-warming food packaging is designed to heat food or beverages within the container, eliminating the need for external heating sources. These packages achieve this by triggering an exothermic chemical reaction that releases heat, which is ideal for warming up dishes like meats and noodles and ensuring beverages like coffee are served piping hot. This innovative packaging is beneficial when traditional heating methods are unavailable, such as during outdoor activities, military operations, or emergencies. The convenience and efficiency of self-heating packaging make it a valuable solution for on-the-go consumption, enhancing the overall consumer experience by providing hot meals and drinks anytime, anywhere.

The self-heating food packaging market is segmented by packaging type (cans, bottles, and pouches), end-user vertical [food (ready-to-eat food, confectionary, and baby food) and beverages (soups and tea and coffee)], and geography (North America, Europe, Asia, Latin America, and the Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Cans |

| Bottles |

| Pouches |

| Other Packaging Type |

| Food | Ready-to-Eat Meals |

| Confectionery | |

| Baby Food | |

| Other Food | |

| Beverage | Soups |

| Tea and Coffee | |

| Other Beverage |

| Quicklime (CaO) - Water Reaction |

| Magnesium-Iron Alloy + Saline |

| Aluminum-Silica Solid-State Cartridge |

| Phase-Change Salt Compounds |

| Encapsulated Exothermic Gel Packs |

| Direct Sales Channel |

| Indirect Sales Channel |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Type | Cans | ||

| Bottles | |||

| Pouches | |||

| Other Packaging Type | |||

| By End-user Vertical | Food | Ready-to-Eat Meals | |

| Confectionery | |||

| Baby Food | |||

| Other Food | |||

| Beverage | Soups | ||

| Tea and Coffee | |||

| Other Beverage | |||

| By Heating Chemistry / Mechanism | Quicklime (CaO) - Water Reaction | ||

| Magnesium-Iron Alloy + Saline | |||

| Aluminum-Silica Solid-State Cartridge | |||

| Phase-Change Salt Compounds | |||

| Encapsulated Exothermic Gel Packs | |||

| By Distribution Channel | Direct Sales Channel | ||

| Indirect Sales Channel | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the self heating food packaging market?

The self heating food packaging market size stands at USD 65.85 billion in 2026 and is projected to reach USD 81.56 billion by 2031.

Which region leads the self heating food packaging market?

North America leads with 35.05% revenue share due to sustained defense procurement and robust emergency-preparedness demand.

Which packaging type is growing the fastest?

Flexible pouches post the highest 7.17% CAGR because of weight savings and advances in heat-resistant films.

What chemistry type is gaining ground over traditional quicklime heaters?

Encapsulated exothermic gel packs are expanding at an 8.31% CAGR by offering superior safety and controlled heat release.

Page last updated on: