Highly Visible Packaging Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

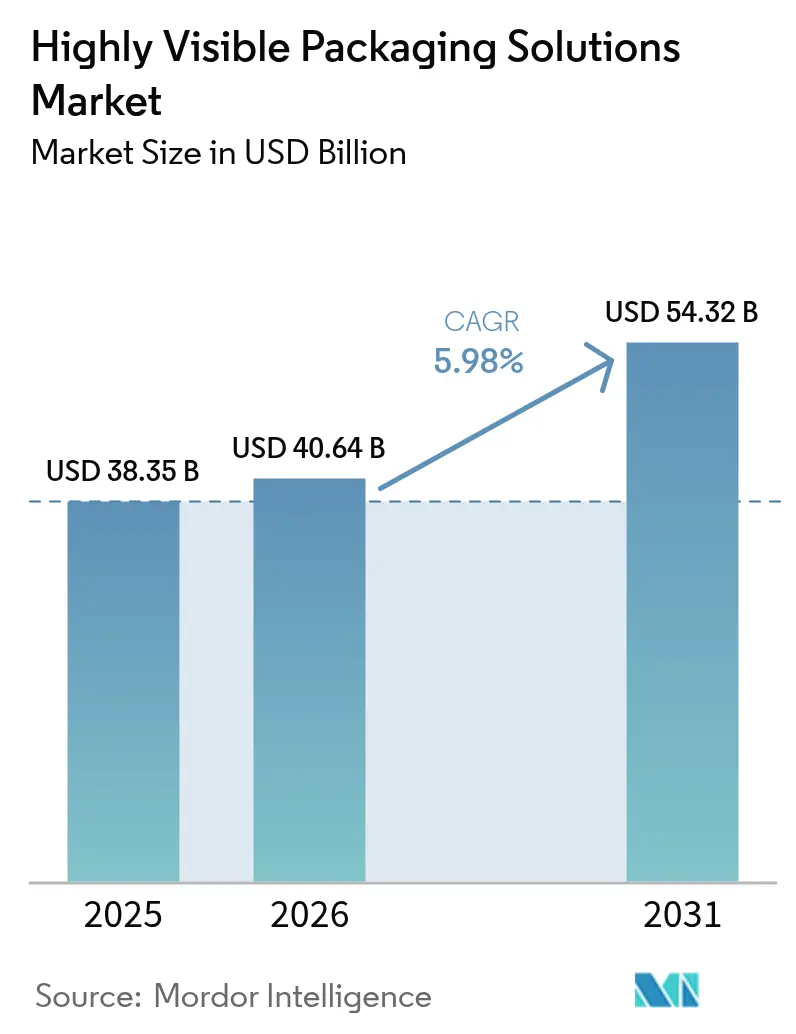

| Market Size (2026) | USD 40.64 Billion |

| Market Size (2031) | USD 54.32 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Highly Visible Packaging Solutions Market Analysis by Mordor Intelligence

Highly visible packaging solutions market size in 2026 is estimated at USD 40.64 billion, growing from 2025 value of USD 38.35 billion with 2031 projections showing USD 54.32 billion, growing at 5.98% CAGR over 2026-2031. Transparency now signals trust in categories where counterfeiting, recalls, and stricter oversight impose tangible costs on brand owners. Blister packs retained momentum on the strength of pharmaceutical unit-dose compliance, while windowed formats gained traction as direct-to-consumer subscriptions favored tamper-evident packaging without compromising the unboxing effect. Plastic substrates still dominate, yet bioplastic uptake is accelerating because the European Union Packaging and Packaging Waste Regulation penalizes non-recyclable formats placed on the market after 2030.[1]European Commission, “Packaging and Packaging Waste Regulation,” ec.europa.euFood and beverage brands sought visibility for fresh produce and transparency for ready-to-eat meals, whereas the healthcare sector adopted senior-friendly, child-resistant blisters to comply with 2024 guidance updates.[2]U.S. Food and Drug Administration, “Drug Supply Chain Security Act,” fda.gov Thermoforming stayed the workhorse technology, but 3D forming and over-molding progressed as brands demanded complex shapes that preserve shelf visibility.

Key Report Takeaways

- By type, blister packs accounted for 28.05% of 2025 revenue, while windowed packaging is forecast to expand at a 7.12% CAGR to 2031.

- By material, plastic substrates held 61.85% of 2025 revenue; bioplastics are advancing at a 6.41% CAGR.

- By transparency level, fully transparent formats captured 54.20% of 2025 shipments and are poised to rise at a 6.49% CAGR.

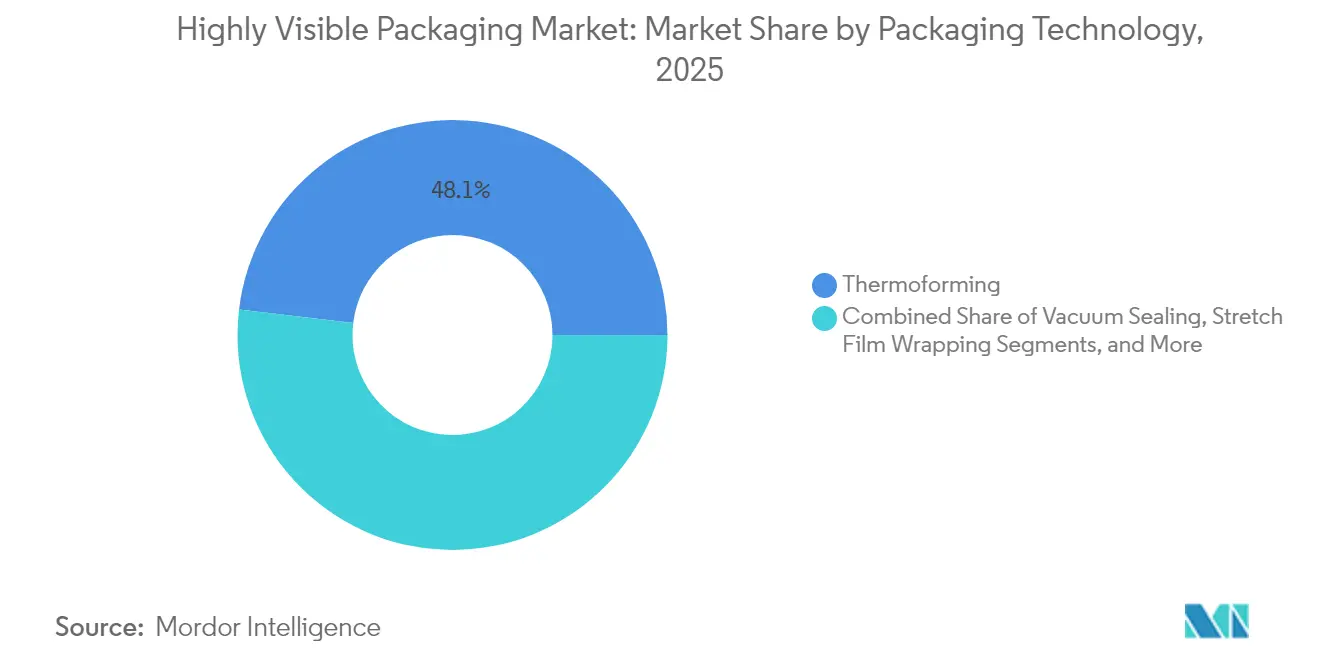

- By technology, thermoforming accounted for 48.10% of the 2025 output, whereas 3D forming and overmolding are projected to grow at a 7.40% CAGR.

- By end-user, food and beverage applications drove 37.80% of 2025 demand, yet healthcare is projected to post a 6.15% CAGR.

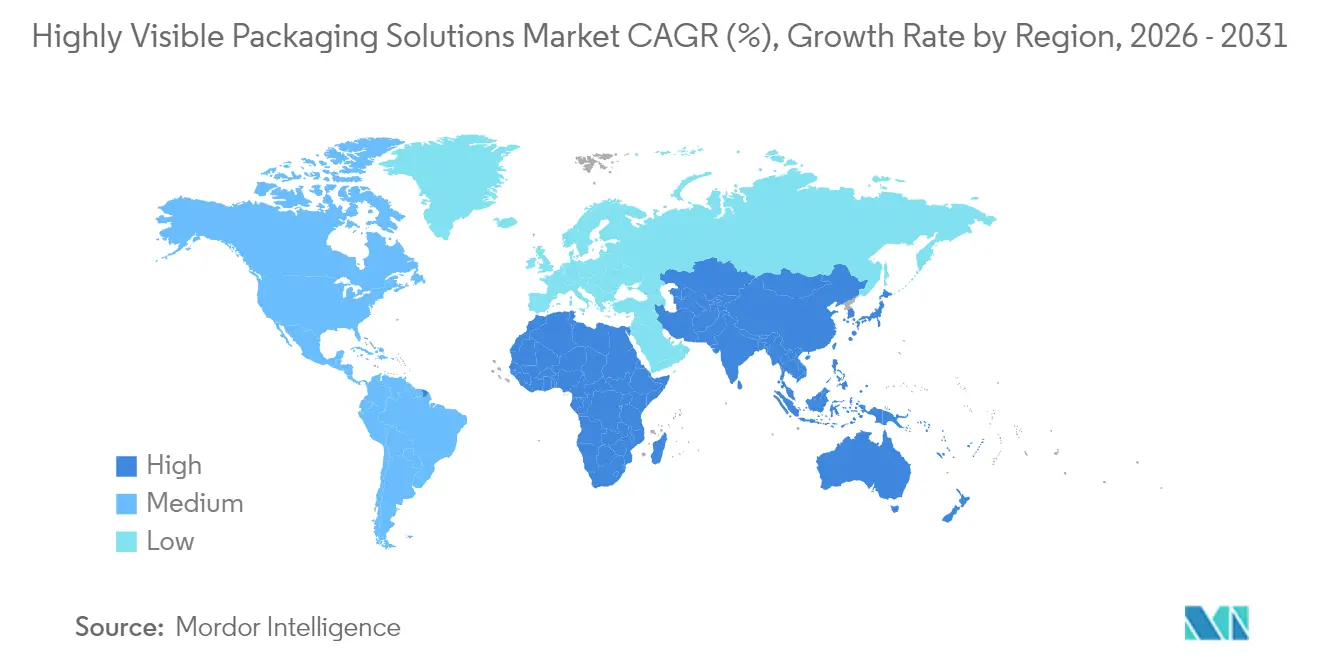

- By geography, North America generated 39.95% of the 2025 revenue, and the Asia-Pacific region is expected to log a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Highly Visible Packaging Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Tamper-Evident and Theft-Deterrent Packaging | +1.2% | Global with focus on North America and Europe | Short term (≤ 2 years) |

| Intensifying Retail Shelf Competition for Brand Differentiation | +0.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Stringent Product Labelling and Transparency Regulations | +1.4% | Europe, North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Integration of Smart QR Codes Enabling Augmented Reality Experiences | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Adoption in Direct-to-Consumer Subscription Services | +0.6% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Circular Economy Reverse Logistics Optimizing Inspection Speed | +0.5% | Europe, North America, pilot Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Tamper-Evident and Theft-Deterrent Packaging

Retail shrinkage reached USD 112 billion in 2024, and chains responded by implementing formats that clearly reveal interference at a glance.[3]National Retail Federation, “Retail Security and Loss Prevention Survey 2024,” nrf.com Pharmaceutical blisters now use holographic seals that fracture upon access, satisfying full Drug Supply Chain Security Act compliance as of November 2024. Electronics retailers adopted clamshells with ultrasonic welds that delaminate during forced entry, resulting in an 18% reduction in warranty fraud in pilots across Best Buy and Target. Fresh-produce trays with peel-back films changed color when compromised, trimming spoilage claims by 22% in Walmart trials. The driver also serves as a legal shield, enabling brands to demonstrate diligence during recall litigation.

Intensifying Retail Shelf Competition for Brand Differentiation

A 2024 Nielsen study found that windowed or transparent packs increased conversion by 14% compared to opaque versions in 12,000 North American stores. Subscription services, such as HelloFresh, adopted clear pouches, which reduced customer support calls by 27% year-over-year. Confectionery brands switched from foil to transparent flow wrap, resulting in a 9% increase in impulse purchases in Mondelez pilot markets. Pet-food pouches with die-cut windows allow shoppers to gauge kibble size, driving 11% volume growth at Mars Petcare. Amazon now rewards recyclable transparent packaging with higher search rank, reinforcing the shelf-visibility imperative.

Stringent Product Labelling and Transparency Regulations

The European Union PPWR will ban non-recyclable multilayer laminates from 2030, pushing converters toward mono-material transparent solutions. California SB 54 imposes steep fees on single-use plastic producers, redirecting budgets toward recyclable clear packs.[4]California Department of Resources Recycling and Recovery, “Senate Bill 54 Implementation,” calrecycle.ca.govThe U.S. Nutrition Facts redesign favors high-contrast, see-through labeling that transparent films are designed to support natively. China’s GB 7718-2024 requires bilingual labels, which windowed packs accommodate at a lower cost than full-surface printing. Regulations coalesce around verifiable packaging, making transparency a compliance requirement rather than an aesthetic choice.

Integration of Smart QR Codes Enabling Augmented Reality Experiences

Nestlé logged 3.2 million scans from QR-enabled transparent pouches within six months of rollout, lifting repeat purchases by 19%. L'Oréal embedded near-field tags in clear jars that improved conversion by 16% in European pilots. Drug makers added QR links for dosage reminders to blisters, aligning with Risk Evaluation and Mitigation Strategies mandates. Coca-Cola attached QR codes to shrink sleeves that unlocked loyalty points, resulting in an 8% volume growth in its premium water range. Brands now earmark up to 12% of packaging budgets for such digital features, spurring demand for converters that can print variable codes without clouding transparency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Material and Production Costs | -0.8% | Global with emphasis on Europe and North America | Short term (≤ 2 years) |

| Environmental Concerns About Single-Use Plastics and Waste | -0.6% | Europe, North America, urban Asia-Pacific | Medium term (2-4 years) |

| Retailer-Driven Shelf-Ready Standards Limiting Custom Shapes | -0.4% | North America, Europe | Medium term (2-4 years) |

| Counterfeiting Risks in Advanced Transparent Films | -0.3% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material and Production Costs

Polyethylene terephthalate resin averaged USD 1,220 per metric ton in 2024, up 14% from 2023, due to crude volatility and Asian cracker outages. Bioplastic premiums reached 60% above those of conventional resins, limiting adoption to premium categories. Tooling for complex clamshells can top USD 150,000, straining converters that serve short-run brands. Energy costs for vacuum sealing increased by 22% in the European Union, narrowing margins by 180 basis points. Recycled polyethylene terephthalate trades at a USD 200 premium because of collection gaps, adding further cost pressure.

Environmental Concerns About Single-Use Plastics and Waste

Single-use packaging accounted for 36% of global plastic waste in 2024, prompting increased pressure from activists and tighter regulations. The Single-Use Plastics Directive is expected to expand its scope to rigid polyethylene terephthalate clamshells that lack a recycling pathway. Microplastic contamination exceeded five particles per gram in seafood samples, amplifying consumer concern. Extended producer responsibility fees now reach USD 0.15 per kilogram on non-recyclable transparent packs in some jurisdictions, boosting converter costs by up to 18%. Two thirds of consumers surveyed in 2024 preferred paper-based windows over all-plastic alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Blister Dominance Masks Windowed Packaging Subscription Surge

Blister packs held a 28.05% share of the highly visible packaging solutions market in 2025, reflecting their entrenched role in drug compliance and electronic display. Windowed formats are predicted to rise at a 7.12% CAGR as subscription services favor lightweight pouches that provide tamper-evident security while still delighting consumers during unboxing. Clamshells remain the go-to choice for high-value electronics, thanks to their drop resistance and visibility, which cut return rates by 13% in Apple trials. Shrink wrap persists in bulk shipment scenarios where unit cost overrides shelf appeal, while clear plastic tubs prolong produce freshness by as many as five days, saving 19% in berry spoilage for Driscoll’s.

Across premium pet food, organic snacks, and nutraceuticals, die-cut windows enable brands to showcase texture without compromising barrier performance. Revised U.S. toy-packaging guidelines now accept windowed boxes that meet ASTM F963 sight criteria, creating a USD 2.8 billion opportunity previously closed to opaque cartons. Converters capable of sub-0.5 millimeter laser precision are set to command higher prices in categories that live or die by shelf aesthetics.

By Material: Bioplastic Momentum Confronts Food-Contact Certification Gaps

Conventional plastics accounted for 61.85% of 2025 revenue, primarily due to the clarity, barrier strength, and established recycling streams of polyethylene terephthalate. Yet bioplastics are advancing at a 6.41% CAGR as brand commitments and pending European regulation push toward compostable or low-carbon options. Polylactic acid won U.S. food-contact authorization for ambient applications in March 2024, unlocking bakery and confectionery channels worth USD 4.1 billion. Polyhydroxyalkanoate resins that biodegrade in marine environments entered pilot output at Danimer Scientific’s Kentucky complex.

Paper and paperboard window packs secured 18.30% of shipments in 2025 due to consumer sustainability perceptions and retailer mandates for lightweight, recyclable formats. Glass remained a niche option at 5.90%, appealing to premium cosmetics that value purity cues. Metal packs with clear over-caps took 4.10%, serving aerosol personal care where full visibility is less critical. Cellulose-acetate windows closely match the clarity of polyethylene terephthalate while composting within 90 days; however, delays in obtaining EN 13432 certification push the large-scale rollout to late 2025.

By Transparency Level: Fully Transparent Formats Navigate Counterfeiting Trade-Offs

Fully transparent packs delivered 54.20% of 2025 shipments and are projected to grow at a 6.49% CAGR as retailers prioritize rapid stock checks and theft deterrence. Windowed packs balance barrier performance with selective display, holding a 31.10% share, while opaque packs with cut-outs fill the remaining 14.70%, where light-sensitive or proprietary contents require shielding.

Counterfeiters exploit clear films that lack covert security traits, producing fake premium items at 20% of the genuine cost. Cosmetic houses embed near-field tags in jars, reducing counterfeit incidents by 34% in Asia, while drug makers laser-etch serial numbers linked to blockchain, thereby fulfilling verification requirements under the Drug Supply Chain Security Act. Suppliers that merge authentication with optical clarity stand to win in high-margin segments such as luxury skincare and biologics.

By Packaging Technology: 3D Forming Disrupts Thermoforming Commodity Lock

Thermoforming generated 48.10% of the 2025 volume, as its lower capital threshold and compatibility with polyethylene terephthalate favor mass production. Vacuum sealing accounted for 25.70% in fresh protein categories, where modified-atmosphere packaging extends shelf life. Stretch film supplied 17.60% for pallet stability, relying on transparency to verify loads without removal.

3D forming and over-molding are advancing at a 7.40% CAGR, creating complex geometries that integrate protective ribs inside clear housings. Automotive suppliers utilize them for instrument-cluster covers, valued at USD 1.9 billion, while medical-device firms roll out transparent housings that meet ISO 13485 clean-room standards. In-mold labeling within 3D-formed pieces eliminates secondary printing steps and enhances tamper evidence.

By End-User Industry: Healthcare Compliance Fuels Blister Innovation

Food and beverage represented 37.80% of 2025 demand as produce and ready-meal brands leveraged clarity to cut spoilage claims. Healthcare is slated for a 6.15% CAGR as blisters evolve to include senior-friendly push-through zones that still prevent access to children under 5 years. Manufacturing segments accounted for 14.20% with transparent bins enabling just-in-time audits on factory floors.

Agriculture utilized clear propagation trays to enhance seedling survival in controlled-environment farms, resulting in a 11% reduction in losses. Electronics claimed 11.80% through anti-static clamshells for semiconductors that must remain visible during customs checks. Toys, hardware, and stationery filled the balance as brands tied visibility to loss prevention and consumer reassurance.

Geography Analysis

North America generated 39.95% of 2025 revenue, driven by established blister-pack infrastructure and Amazon’s frustration-free certification, which prioritizes transparent and recyclable packs in search results. Full DSCSA enforcement in November 2024 is expected to increase demand for unit-dose blisters that provide both visual inspection and digital serialization. Canada’s extended producer responsibility fees of USD 0.12 per kilogram on non-recyclable plastics accelerated the adoption of mono-material clear clamshells. Mexico’s nearshore ecosystem scaled output for U.S. brand owners, expanding cross-border shipments by 19% in 2024.

The Asia-Pacific region is projected to record a 7.55% CAGR through 2031, driven by China’s cold-chain upgrade and India’s surge in contract manufacturing, which require tamper-evident, transparent formats. China’s GB 7718-2024 rule mandates bilingual labels, a requirement that windowed packs can meet cost-effectively. India, which supplies 40% of the global generics market, is transitioning from opaque foil to transparent blisters that align with export standards, resulting in a 27% increase in polyethylene terephthalate film imports in 2024. Japan’s aging demographic increased demand for larger, tactile blister apertures, with a 14% growth in 2024. Australia and New Zealand replicated European extended producer responsibility, stimulating demand for certified recyclable clear packs.

Europe contributed 28.40% of 2025 revenue as PPWR drives recyclable mono-material adoption. Germany’s VerpackG imposes fees up to USD 0.15 per kilogram on non-recyclables, steering converters toward clear polyethylene terephthalate and cellulose windows. The United Kingdom plastic packaging tax of GBP 200 per metric ton on sub-30% recycled content spurred demand for post-consumer recycled polyethylene terephthalate. France prohibited single-use plastic produce packs under 1.5 kilograms, encouraging paper-based windows. South America, the Middle East, and Africa together held 12.05%, supported by Brazil’s pharmaceutical demand, UAE food service, and South African electronics retail.

Regulatory Landscape

Regulatory pressure is tightening around recyclability, recycled content, and chemical safety for food-contact and healthcare-adjacent visible packaging. In the European Union, the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, entered into force on 11 February 2025 and applies from 12 August 2026, raising the compliance bar for labeling, sustainability requirements, and extended producer responsibility for packaging placed on the EU market.

In the United States, FDA oversight of food-contact materials is becoming more data-intensive, which affects transparent films, coated paperboard windows, and barrier layers used in visible packs. FDA actions highlighted in 2025-2026 include PFAS-related Food Contact Notifications being deemed no longer effective (January 2025) and a finalized systematic process for post-market assessment of food chemicals (May 2026), increasing the need for documentation and faster reformulation pathways when substances are deprioritized.

Value Chain Analysis

The value chain covers resin and specialty-material suppliers (PET, PE, rPET, bioplastics, coated paper or paperboard window materials), film and sheet extrusion, converting (thermoforming, 3D forming and over-molding, vacuum sealing, and stretch wrapping), and printing and variable data used for QR and serialization. Downstream pack-out for end users in food and beverage, healthcare, and consumer goods follows after material qualification and compliance testing, which act as a gating step for food-contact structures and healthcare blisters that need optical clarity while also meeting barrier and tamper-evidence requirements.

Recent collaborations show how suppliers are tightening linkages across materials and converting to address circularity and performance demands. In June 2026, Amcor collaborated with Kelpi to evaluate seaweed-based coating technology aimed at improving barrier performance and recyclability in fiber-based packaging, reinforcing the role of specialty coatings and paper-based windows in visible formats. Channel partners and retailers also shape specifications through shelf-ready constraints and reuse pilots, including refill models, which influence pack design, material choices, and reverse-logistics handling requirements.

Competitive Landscape

The highly visible packaging solutions market shows moderate concentration. The top five suppliers, Amcor, Mondi, Sealed Air, Sonoco, and Pactiv Evergreen, control about 35% of global capacity. Multinationals channel investment toward post-consumer recycled polyethylene terephthalate extrusion and bioplastic compounding to comply with extended producer responsibility, while regional converters woo direct-to-consumer brands through low minimums and rapid prototyping. Compostable windowed pouches for organic snacks and 3D-formed transparent housings for diagnostic devices remain niche markets where large incumbents lack the agility to serve accounts with annual revenues under USD 5 million.

Emerging players, such as Footprint and Notpla, scale molded-fiber and seaweed-based solutions that biodegrade in six weeks, commanding price premiums of 10% or more from sustainability-focused brands. Technology moats deepen as Amcor patents laser-etched variable QR codes printed at 200 meters per minute without clouding transparency, a technique smaller firms cannot match without USD 3 million in capital. ISO 15378 certification and REACH compliance lift entry barriers, favoring suppliers with strong regulatory teams

Highly Visible Packaging Solutions Industry Leaders

Amcor Plc

Mondi Plc

Sonoco Products Company

Rohrer Corporation

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is emerging at the intersection of high-visibility packaging and regulatory-driven redesign toward mono-material, recyclable structures, especially for windowed formats where barrier and clarity need to coexist. EU PPWR implementation from 12 August 2026 is a clear catalyst for converters to commercialize transparent or windowed solutions that meet recyclability and labeling requirements without relying on hard-to-recycle multilayer laminates. Evidence of active commercialization includes Amcor and De Ceuster Meststoffen NV (DCM) introducing a recycle-ready, mono-material polyethylene fertilizer packaging film in Europe with 35% post-consumer recycled content (March 2026), turning regulatory pressure into procurement-ready SKUs.

Another opportunity is the shift of visible packs toward paper-based or fiber-based structures with functional coatings, targeting recyclability perceptions and retailer requirements while preserving shelf visibility. Amcor and Alter Eco launched recyclable, paper-based chocolate-bar packaging with up to 61% lower packaging weight (February 2026), showing that premium brands are funding material shifts where visibility, shelf differentiation, and sustainability claims can be combined. In parallel, reuse and refill programs support niche demand for durable, high-clarity containers and labels that can withstand multiple cycles; Amcor participation in the Refill Coalition container project with Ocado Retail in the UK (May 2026) indicates ongoing retailer-led pilots that pull through packaging designs optimized for repeated handling and fast visual inspection.

Recent Industry Developments

- June 2026: Pacific Avenue Capital Partners completed the acquisition of ESE World from Amcor, transferring a waste and recycling container systems business into a new ownership structure. The transaction sharpened Amcor's portfolio focus while keeping attention on circularity infrastructure that supports the collection and handling of packaging materials in the broader ecosystem.

- May 2026: Closure Systems International acquired two of Amcor's North American beverage closure compression molding facilities in Erie and Hattiesburg. The deal reshapes capacity ownership in closures that pair with highly visible bottles and containers, while enabling Amcor to rebalance its manufacturing footprint and capital allocation.

- October 2024: Bayer launched PET-based, one-material blister packaging for the Aleve brand in the Netherlands in partnership with Liveo Research, eliminating PVC and reducing carbon footprint by 38%. The rollout showed how healthcare-adjacent packs can maintain high visibility while shifting to mono-material structures aligned with recyclability goals.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the highly visible packaging solutions market covers packaging formats and technologies that are intentionally designed to make the packed product easier to see and identify at purchase or use. The market is measured in revenue terms across major regions.

Scope exclusions: The sizing excludes secondary packaging that does not materially change on-shelf or on-pack visibility, along with in-house printing services that are not sold as part of a packaging solution.

Segmentation Overview

- By Type

- Clamshell Packaging

- Blister Pack

- Shrink Wrap

- Windowed Packaging

- Plastic Container Packaging

- Other Types

- By Material

- Plastic

- Paper and Paperboard

- Glass

- Metal

- Bioplastic

- By Transparency Level

- Fully Transparent

- Windowed

- Opaque with Cut-Outs

- By Packaging Technology

- Thermoforming

- Vacuum Sealing

- Stretch Film Wrapping

- 3D Forming and Over-Moulding

- By End-User Industry

- Food and Beverage

- Healthcare

- Manufacturing

- Agriculture

- Electronics and Appliances

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first layer of the model by mapping packaging demand signals and the supply footprint by region. We relied on public sources, such as UN Comtrade trade statistics, U.S. Census Bureau manufacturing data, Eurostat, the World Bank, and patent databases, to understand packaging output direction, resin and paper usage context, and technology adoption patterns.

We also reviewed company annual reports, investor presentations, sustainability disclosures, packaging association publications, and reputed business press to ground assumptions around material mixes, end-user activity, and pricing pressure. Where available, paid subscription access for company financials and a paid patent database were used to speed up cross-checks for revenue exposure and technology intensity. The sources listed here are illustrative only, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with packaging converters, material suppliers, brand owners, and distribution-side participants, so desk findings could be adjusted where on-the-ground realities differed. Coverage was kept global across demand-heavy regions, and discussions focused on what buyers actually specify for visibility features, material choices, and technology routes. This input helped us firm up shares and assumptions used in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 15% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing started with a top-down build where packaging demand was reconstructed by combining end-use packaging activity with the penetration of visibility-led formats, and then translating that demand into value using region-appropriate price bands. To make this practical, we used market fingerprints such as food and beverage packaged volumes, healthcare unit-dose and blister usage intensity, retail display and shelf-ready adoption, material share shifts (plastic versus paper and emerging bioplastic), and technology mix cues such as thermoforming and vacuum sealing.

Results were then corroborated with selective bottom-up approximations, including sampled supplier revenue splits, packaging line capacity discussions, and ASP times volume checks for major format families. This helped adjust totals where a top-down ratio looked stretched. Gaps that show up in smaller countries or niche end uses were handled through proxying from comparable markets and then re-tested with primary inputs. For forecasting, scenario analysis was used around key drivers like regulation-led material change, price pass-through behavior, and visibility feature adoption, and then the final trajectory was smoothed using time-series logic where the underlying demand indicators were stable.

Data Validation & Update Cycle

Validation was done through multiple checks, starting with internal consistency tests across type, material, and end-user splits so totals reconciled cleanly. We compared outputs against independent signals like packaging production direction, trade movement, and supplier commentary, and any large variance triggered a revisit of penetration or pricing assumptions.

Before sign-off, the model and written logic were reviewed in steps by different analysts, and outliers were challenged until a clear explanation was documented. Reports are refreshed annually, and interim adjustments are made when material events occur, such as major regulation changes, sharp resin price swings, or step changes in end-user demand. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Global Highly Visible Packaging Solutions Market Market Size Compared Against Other Published Estimates

Published market sizes for highly visible packaging solutions often do not match because the underlying scope is not the same, and the assumptions behind visibility, technology inclusion, and pricing are handled differently. Differences also show up when one estimate uses a shorter forecast window or a different base year, which can shift the stated current value even when the growth story appears similar.

The biggest gap drivers here are usually whether the count includes only packaging that improves product visibility at the point of sale, or if adjacent packaging and broader printing and labeling spend is also pulled in. Another frequent difference comes from how price is treated across materials and formats, since blister and clamshell structures can follow different resin cost pass-through timing than paperboard windows, and currency conversion timing can further widen the spread.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 40.64 B (2026) | |

| Industry Publisher A | USD 40.60 B (2026) | Uses a similar packaging-format view for 2026, but the forecast path extends to 2033 and visibility definitions are discussed at a higher level, which can leave technology and end-user weighting less transparent. |

| Market Publisher B | USD 32.60 B (2025) | Starts from a lower base year value and applies a longer forecast horizon to 2035 with a different growth profile, and the scope can be broader on printing and branding elements, which changes what gets counted as visibility-led packaging. |

The table shows that the spread is mainly explained by year selection and by what is treated as a visibility-driven packaging solution versus adjacent packaging spend. When visibility is counted only when it is delivered through specific formats, materials, and enabling technologies, and when pricing is rechecked by region with interview feedback, the resulting 2026 value stays more traceable to real packaging demand signals, which is the approach used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the highly visible packaging solutions market?

The highly visible packaging solutions market reached USD 40.64 billion in 2026.

How fast is the market expected to grow?

The market is forecast to post a 5.98% CAGR between 2026 and 2031.

Which packaging type leads in revenue?

Blister packs commanded 28.05% of 2025 revenue.

Which material is gaining traction for sustainability?

Bioplastics such as polylactic acid and polyhydroxyalkanoate are advancing at a 6.41% CAGR over 2026-2031.

Which region will grow the quickest through 2031?

Asia-Pacific is projected to expand at a 7.55% CAGR through 2031.

What technology is disrupting traditional thermoforming?

3D forming and over-molding are rising at a 7.40% CAGR over 2026-2031, enabling intricate clear shapes.

Page last updated on: