Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.14 Billion |

| Market Size (2031) | USD 12.43 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protective Packaging Market Analysis by Mordor Intelligence

The protective packaging market size is expected to grow from USD 9.73 billion in 2025 to USD 10.14 billion in 2026 and is forecast to reach USD 12.43 billion by 2031 at 4.17% CAGR over 2026-2031. Rising e-commerce volumes, intensifying sustainability regulations, and the search for premium unboxing experiences are recasting protective solutions from a back-end expense into a brand value lever. Demand patterns now reward lightweight materials that curb dimensional-weight fees, and regulatory certainty is prompting rapid shifts toward paper and fiber alternatives that can demonstrate recyclability. Accelerating mergers aim to unlock scale economies in sustainable technology, while automation platforms help converters contain labor and waste costs. Asia-Pacific remains the strategic fulcrum, supplying both manufacturing density and the world’s fastest e-commerce growth, yet Europe wields outsized regulatory influence that shapes global investment roadmaps.

Key Report Takeaways

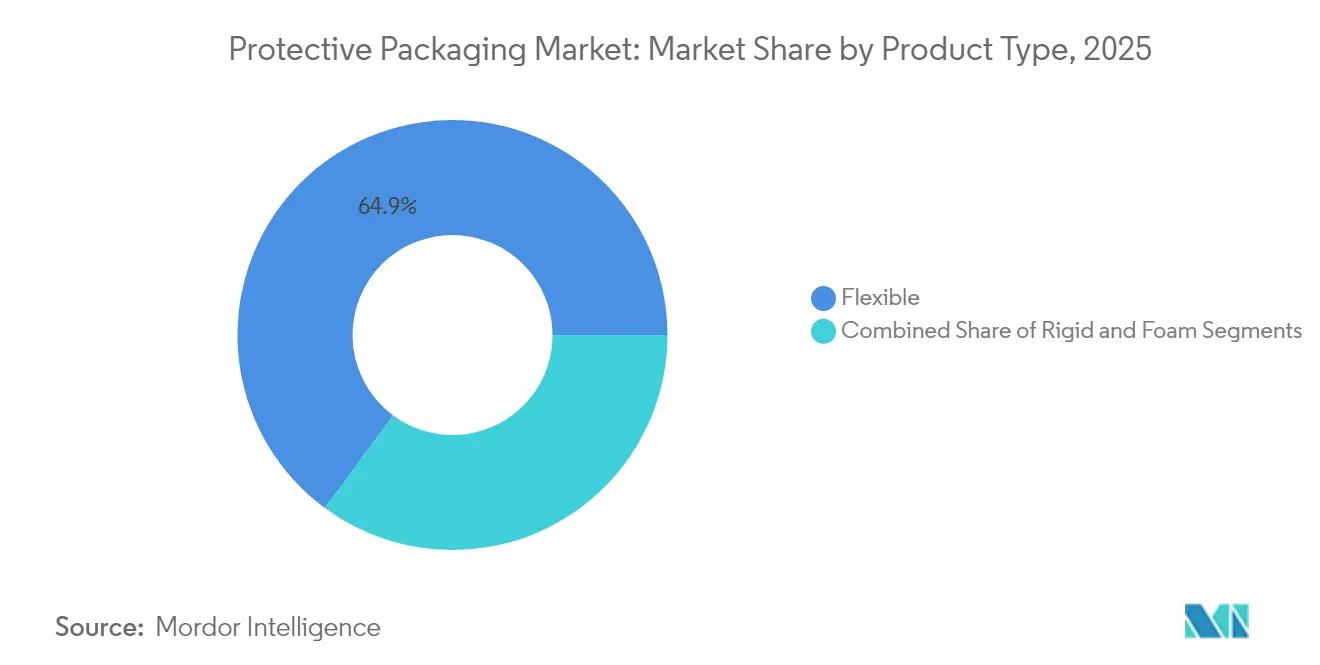

- By product type, flexible formats held 64.88% of protective packaging market share in 2025, whereas foam solutions are set to expand at a 6.52% CAGR to 2031.

- By material, plastics captured 57.70% share of the protective packaging market size in 2025, yet foam polymers are poised for 7.06% CAGR through 2031 .

- By end-user industry, consumer electronics accounted for 8.02% CAGR, the fastest within the protective packaging market to 2031.

- By geography, Asia-Pacific commanded 40.05% revenue share in 2025 and is advancing at a 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protective Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging e-commerce shipping volumes | +1.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Regulatory push for product safety and damage reduction | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Growing consumer electronics demand | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Preference for lightweight flexible protective formats | +0.5% | Global | Short term (≤ 2 years) |

| Adoption of on-demand packaging automation | +0.4% | North America & EU | Medium term (2-4 years) |

| Expansion of cold-chain biologics and vaccines | +0.6% | Global, led by North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging E-commerce Shipping Volumes

Exponential parcel growth is redefining protective packaging market logistics, compelling brands to shrink cube sizes and pivot toward fiber formats that meet carrier dimensional weight thresholds. HP’s redesign of its All-in-One PC packaging eliminated 98% of expanded polyethylene, reduced volume by up to 67%, and raised pallet density for the 27-inch model, trimming freight spend and carbon load. Logitech completed a portfolio-wide switch to paper in 2025, removing 660 tons of plastic and 6,000 tons of CO₂ each year, while 61% of surveyed buyers favored recyclable packs . Brands thus regard the protective packaging market not only as a cost line but as a retention lever in a doorstep economy.

Regulatory Push for Product Safety and Damage Reduction

New statutes go beyond recyclability to treat packaging as intrinsic to consumer safety. Europe’s General Product Safety Regulation obliges manufacturers to validate that pack integrity prevents contamination or tampering.[1]European Commission, “Regulation – EU 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu Thermo Fisher’s carton with built-in tamper evidence withstands -80 °C, discards glue, and scales across vial sizes. In the United States, serialization laws link tracking codes with cushioning layers, catalyzing smart-label demand. Compliance timetables push producers to confirm protective packaging market readiness years ahead of enforcement.

Growing Consumer Electronics Demand

Device miniaturization and premium branding lift tolerance for high-spec foams that guard against static and shock. Google’s plastic-free blueprint offers a 70-page manual that guides OEMs toward fiber cushions while retaining mechanical strength, proving that sustainable switches need not erode customer satisfaction. AI-assisted design now tailors cushioning density to component geometry, trimming weight without sacrificing drop resistance. This synergy of precision and sustainability keeps electronics the fastest-growing slice of the protective packaging market.

Preference for Lightweight Flexible Protective Formats

Suppliers leverage mono-material films and post-consumer resin grades that cut greenhouse gas footprints by over 40% versus virgin equivalents. Sealed Air’s on-demand inflatables store flat, freeing 80% of warehouse space and inflating seconds before dispatch. Origami-inspired boards from VTT raise compressive strength through Miura folds, foreshadowing fiber substitutes for expanded polystyrene. Flexible performance therefore underpins cost, space, and brand narratives in the protective packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental rules on plastics and EPS | -0.9% | EU leading, expanding globally | Long term (≥ 4 years) |

| Raw-material price volatility | -0.6% | Global, acute in North America | Short term (≤ 2 years) |

| Space constraints at urban last-mile hubs | -0.4% | Urban centers globally | Medium term (2-4 years) |

| Product redesign minimizing protective-packaging need | -0.3% | Global, technology-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Rules on Plastics and EPS

Europe mandates reusable targets climbing to 15% by 2040 and bans certain PFAS, triggering immediate material substitutions and extended-producer fees that squeeze converters’ margins. The United Kingdom’s October 2025 EPR rollout shifts full disposal costs onto brands, while California restricts the recycling symbol unless curbside acceptance is documented. These moves inflate compliance costs and lengthen payback periods for foam installations, dragging on the protective packaging market growth curve.

Raw-material Price Volatility

Corrugated price spikes in 2024 forced converters to balance inventory with cash flow. Fiber costs rose amid energy shocks, while specialized cold-chain foams fetched premiums tied to petrochemical swings. Sealed Air reorganized verticals to hedge with fiber products that feature steadier pricing. Volatility complicates long-term contracts and can delay capital spending across the protective packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Leadership Amid Foam Specialization

Flexible formats generated 64.88% of 2025 sales within the protective packaging market, reflecting their ability to serve high-volume parcels with minimal cube and lower freight spend. Foam categories, though smaller, are accelerating at 6.52% CAGR toward 2031 as electronics and biologics rely on custom molds with electrostatic discharge yields. The protective packaging market size for foam is projected to widen in tandem with cold-chain expansion, positioning foam makers for premium pricing aligned with higher barrier performance.

Sealed Air’s KORRVU suspension format illustrates how paper and corrugate can mimic foam resilience, offering curbside recyclability and shipping flat to cut inbound freight. Rigid corrugated, meanwhile, remains relevant for large white-goods and machinery where stacking strength matters. The product mix signals a divide: flexibles satisfy cost-down mandates in e-commerce, whereas technical foams win where precision cushioning and thermal insulation command a price premium.

By Materials: Sustainable Transition Accelerates

Plastics still supplied 57.70% of 2025 tonnage, yet foam polymers log the quickest 7.06% CAGR, tracking growth in high-value electronics and life sciences. Barley-based bioplastics and recycled polyethylene films are scaling pilot lines, proving viability for mass adoption. Protective packaging market share for biocomposites remains modest but expands as food and pharma buyers seek compostable or bio-based seals.

Paper and board converters upgrade barrier coatings so that fiber wraps repel moisture and grease. Virginia Tech’s low-pressure cellulose treatment strengthens paper while preserving transparency, unlocking shelf-ready appeal for perishables. Producers bundle such advances with carbon footprint disclosures, translating material innovation into procurement gains within the protective packaging market.

By Function: Cushioning Innovation Drives Growth

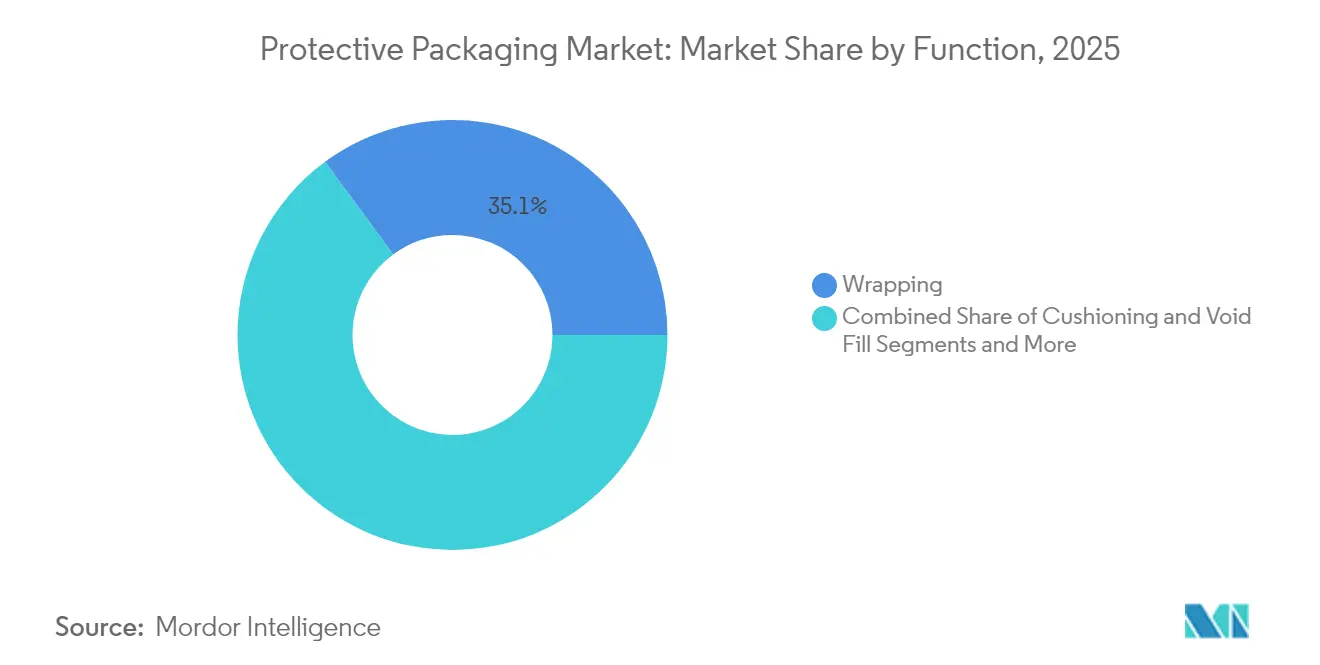

Cushioning applications outpace others with a 7.55% CAGR thanks to rising device fragility and the need for pristine unboxing. Wrapping kept 35.10% share in 2025 because it remains the first defensive layer against scuffs. Insulation lines enjoy momentum from biologics, where phase-change packets maintain 2-8 °C for up to 36 hours in DS Smith’s TailorTemp pack that trims emissions 40% relative to EPS.

Robotic void-fill systems feed on repeatable pillow dimensions compatible with automated pick arms, integrating standard SKUs that smooth warehouse throughput. As retailers commit to net-zero lanes, functions converge: one module delivers cushioning, thermal regulation, and QR-enabled provenance data, raising average selling prices across the protective packaging market.

By End-user Industry: Electronics Acceleration Through Innovation

Consumer electronics is the fastest-expanding customer set, growing 8.02% annually as SKUs multiply and buyers link packaging quality with brand equity.Logitech’s paper switch demonstrates how high-density foam can be swapped for folded board without bumping defect rates, winning consumer approval while meeting retailer recycling audits.

Food and beverage sustains volume with 28.20% 2025 share, yet regulatory pushes to strip superfluous wraps challenge margin recovery. Pharmaceutical payloads climb with global vaccine programs, demanding containers that sustain sub-zero lanes and readable barcodes after frost cycles. Automotive and industrial sectors rely on returnable dunnage trays that recirculate in just-in-time loops, a niche that shields them from one-way plastic bans yet still subjects them to recycled-content thresholds within the protective packaging market.

Geography Analysis

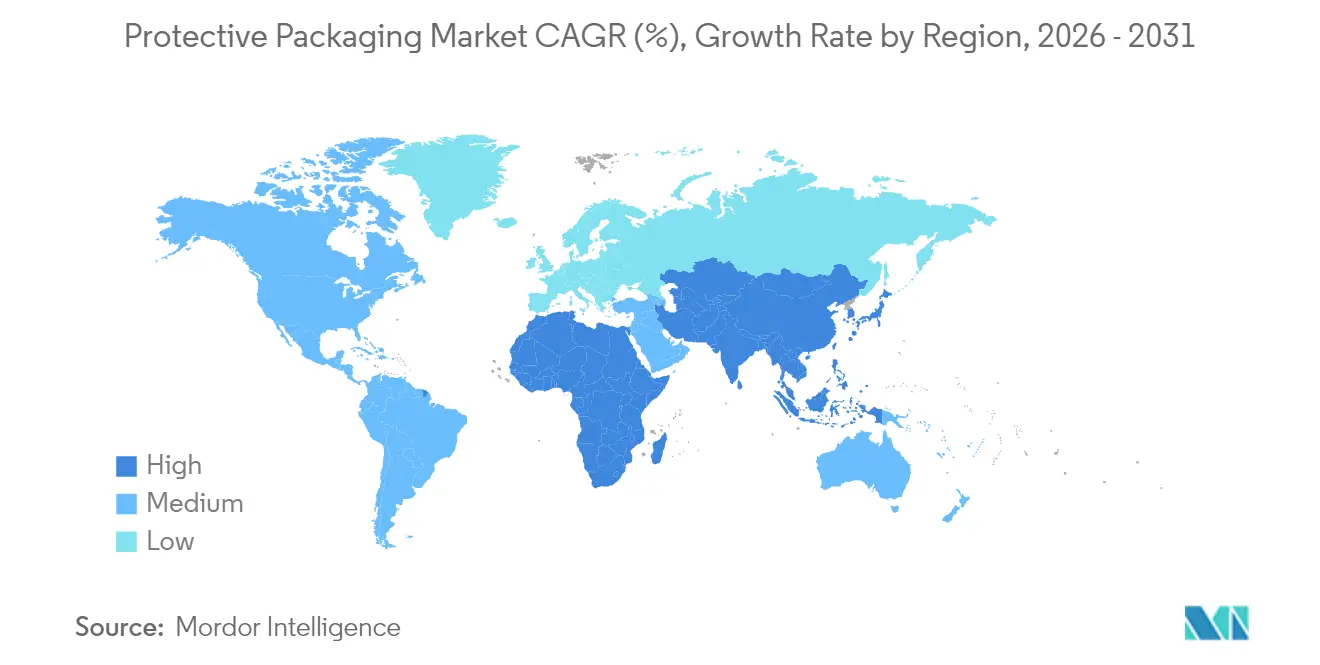

Asia-Pacific controlled 40.05% revenue in 2025 and is set for 7.41% CAGR, underpinned by dense manufacturing, rapid mobile penetration, and supportive yet tightening policy. China funnels half of global plastic output, offering localized resin access that favors converters, while Japan advances foamed paper research that can satisfy premium electronics exporters. Countries pilot government subsidies for automated packing lines, ensuring the protective packaging market keeps pace with cross-border e-commerce surges.

North America follows through premiumization. United States brands like HP and Amazon test zero-plastic pilots that later migrate worldwide, positioning the region as a trend bellwether. State-level Extended Producer Responsibility rules, beginning with California SB 343, compel recyclability declarations by 2026, rewarding early adopters in the protective packaging market. Canada promotes closed-loop paper recycling, whereas Mexico leverages near-shoring to grow appliance and electronics exports, widening demand for in-plant cushioning.

Europe leads rulemaking. The Packaging and Packaging Waste Regulation locks in recyclability and reuse quotas that benchmark global sourcing policies. Germany’s deposit systems and the UK’s plastic tax accelerate fiber uptake. Market entrants must navigate complex eco-modulation fees that vary by polymer, so multinationals cluster R&D hubs in the region to future-proof formulations. Compliance mastery therefore becomes a commercial edge across the protective packaging market.

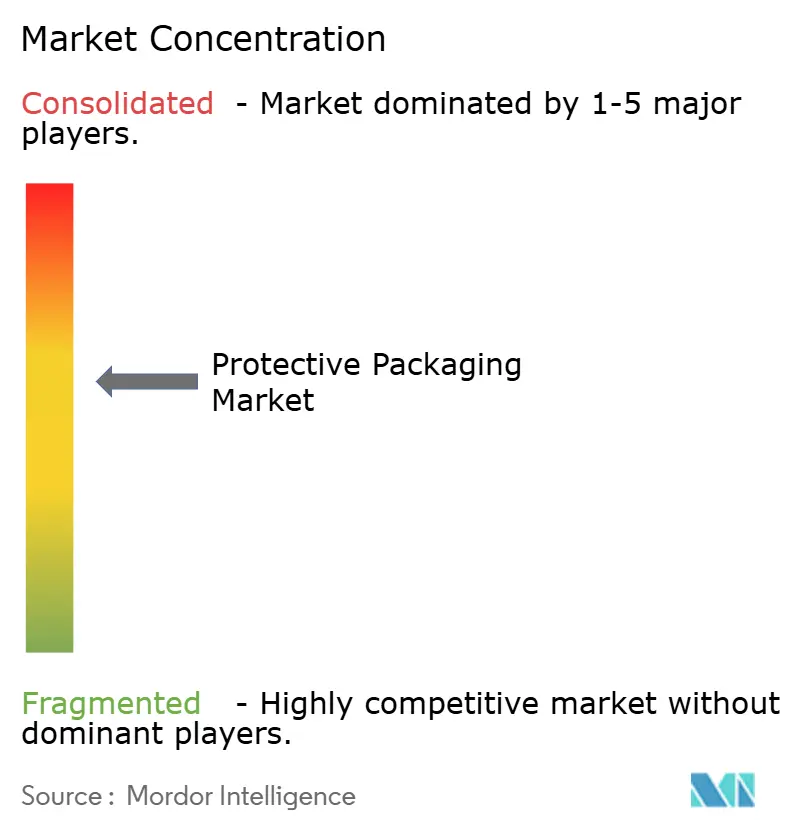

Competitive Landscape

The protective packaging market remains moderately concentrated. Smurfit Westrock emerged in 2025 by merging Smurfit Kappa with WestRock, creating USD 34 billion in adjusted revenue across 40 countries and more than 500 converting sites. International Paper’s USD 7.2 billion integration of DS Smith broadens European corrugated reach and projects USD 514 million in synergies. Consolidators pursue vertical integration that spans paper mills, design labs, and automation equipment to deliver turnkey sustainable solutions.

Sealed Air generated USD 5.5 billion in 2023 sales, spotlighting BUBBLE WRAP and auto-bagging systems that inflate material only when required, lowering warehouse footprints. Its CTO2Grow initiative seeks USD 160 million annual savings through digitized operations, underlining a pivot toward efficiency and recycled content. Mondi sustains leadership as Europe’s top virgin containerboard supplier and global kraft paper leader, with capital discipline funding Duino’s recycled containerboard line that opened in May 2025 for USD 220 million.[3]Mondi Group, “Mondi Starts Up New Containerboard Machine,” mondigroup.com

White-space opportunities cluster around cold chain, electrostatic discharge, and tamper evident formats where customers accept premiums for risk mitigation. Smaller innovators, often spin-offs from university labs, partner with majors to scale foam alternatives like barley plastic or Miura-fold boards, enriching the protective packaging industry pipeline and sharpening competitive intensity.

Protective Packaging Industry Leaders

Intertape Polymer Group Inc.

Sealed Air Corporation

Sonoco Products Company

Smurfit Westrock

Mondi Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mondi Group began commercial runs at its Duino, Italy recycled containerboard machine after a USD 220 million investment.

- April 2025: Novolex closed a USD 6.7 billion merger with Pactiv Evergreen, adding 250 brands and 39,000 SKUs to its roster.

- April 2025: Logitech finished its global switch to paper packaging, subtracting 660 tons of plastic each year.

- April 2025: DHL confirmed EUR 2 billion investment through 2030 to expand GDP-certified pharma hubs and cold chain capacity.

Global Protective Packaging Market Report Scope

Protective packaging supplies are items created to shield and safeguard a product from possible damage or destruction during shipping or storage. In terms of materials, protective packaging can be manufactured from anything, including but not limited to cardboard, plastic, and metal.

The protective packaging market is segmented by product type (rigid (corrugated paperboard protectors, molded pulp, insulated shipping containers, and other rigid product types), flexible (protective mailers, bubble wraps, air pillows/air bags, paper fill, and other flexible product types), and foam (molded foam, foam in place (FIP), loose fill, foam rolls/sheets, and other foam types)), end-user industry (food and beverage, industrial, pharmaceutical, consumer electronics, beauty, home care, and other end-user industries), and geography (North America (United States and Canada), Europe (United Kingdom, France, Germany, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, and New Zealand, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, Mexico, and Rest of Latin America), Middle East and Africa (Saudi Arabia, South Africa, United Arab Emirates, Egypt, and Rest of the Middle East and Africa). The market sizes and forecasts are provided in value (USD) for all the above segments.

By Product Type

| Rigid | Corrugated Paperboard Protectors |

| Molded Pulp | |

| Insulated Shipping Containers | |

| Other Rigid Types | |

| Flexible | Protective Mailers |

| Bubble Wrap | |

| Air Pillows / Air Bags | |

| Paper Fill | |

| Other Flexible Types (Foil Pouches, Stretch and Shrink Films) | |

| Foam | Molded Foam |

| Foam-in-Place (FIP) | |

| Loose Fill | |

| Foam Rolls / Sheets | |

| Other Foam Types (Corner Blocks etc.) |

By Materials

| Paper and Paperboard | |

| Plastics | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Foam Polymers | Expanded Polystyrene (EPS) |

| Expanded Polyethylene (EPE) | |

| Expanded Polypropylene (EPP) | |

| Biodegradable and Compostable | Molded Fiber |

| Starch-based | |

| Polylactic Acid (PLA) | |

| Other Materials |

By Function

| Cushioning |

| Blocking and Bracing |

| Void Fill |

| Insulation and Temperature Control |

| Wrapping |

| Dunnage and Others |

By End-user Industry

| Food and Beverage |

| Industrial Goods |

| Pharmaceuticals and Life Sciences |

| Consumer Electronics |

| Beauty and Home Care |

| Automotive and Aerospace |

| E-commerce and Retail Fulfilment |

| Other End-user Industry |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| By Product Type | Rigid | Corrugated Paperboard Protectors | |

| Molded Pulp | |||

| Insulated Shipping Containers | |||

| Other Rigid Types | |||

| Flexible | Protective Mailers | ||

| Bubble Wrap | |||

| Air Pillows / Air Bags | |||

| Paper Fill | |||

| Other Flexible Types (Foil Pouches, Stretch and Shrink Films) | |||

| Foam | Molded Foam | ||

| Foam-in-Place (FIP) | |||

| Loose Fill | |||

| Foam Rolls / Sheets | |||

| Other Foam Types (Corner Blocks etc.) | |||

| By Materials | Paper and Paperboard | ||

| Plastics | Polyethylene (PE) | ||

| Polypropylene (PP) | |||

| Polyethylene Terephthalate (PET) | |||

| Foam Polymers | Expanded Polystyrene (EPS) | ||

| Expanded Polyethylene (EPE) | |||

| Expanded Polypropylene (EPP) | |||

| Biodegradable and Compostable | Molded Fiber | ||

| Starch-based | |||

| Polylactic Acid (PLA) | |||

| Other Materials | |||

| By Function | Cushioning | ||

| Blocking and Bracing | |||

| Void Fill | |||

| Insulation and Temperature Control | |||

| Wrapping | |||

| Dunnage and Others | |||

| By End-user Industry | Food and Beverage | ||

| Industrial Goods | |||

| Pharmaceuticals and Life Sciences | |||

| Consumer Electronics | |||

| Beauty and Home Care | |||

| Automotive and Aerospace | |||

| E-commerce and Retail Fulfilment | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current protective packaging market size?

The protective packaging market size stood at USD 10.14 billion in 2026 and is forecast to reach USD 12.43 billion by 2031.

Which region leads the protective packaging market growth?

Asia-Pacific leads with 40.05% revenue share and a 7.41% CAGR through 2031, supported by manufacturing scale and e-commerce expansion.

Which product segment is growing fastest?

Foam solutions show the highest momentum at a 6.52% CAGR as electronics and biologics require precision cushioning.

How are regulations influencing material choices?

EU and North American rules mandate recyclability and recycled content, accelerating shifts from expanded polystyrene to fiber and post-consumer resin films.

Why are mergers increasing in the protective packaging industry?

Consolidation helps firms spread sustainability compliance costs, secure recycled feedstock, and build automation platforms that lower unit economics.

What role does automation play in this market?

On-demand packing systems and AI-driven design reduce material use and labor, improving margins while meeting sustainability targets.

Page last updated on: