Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

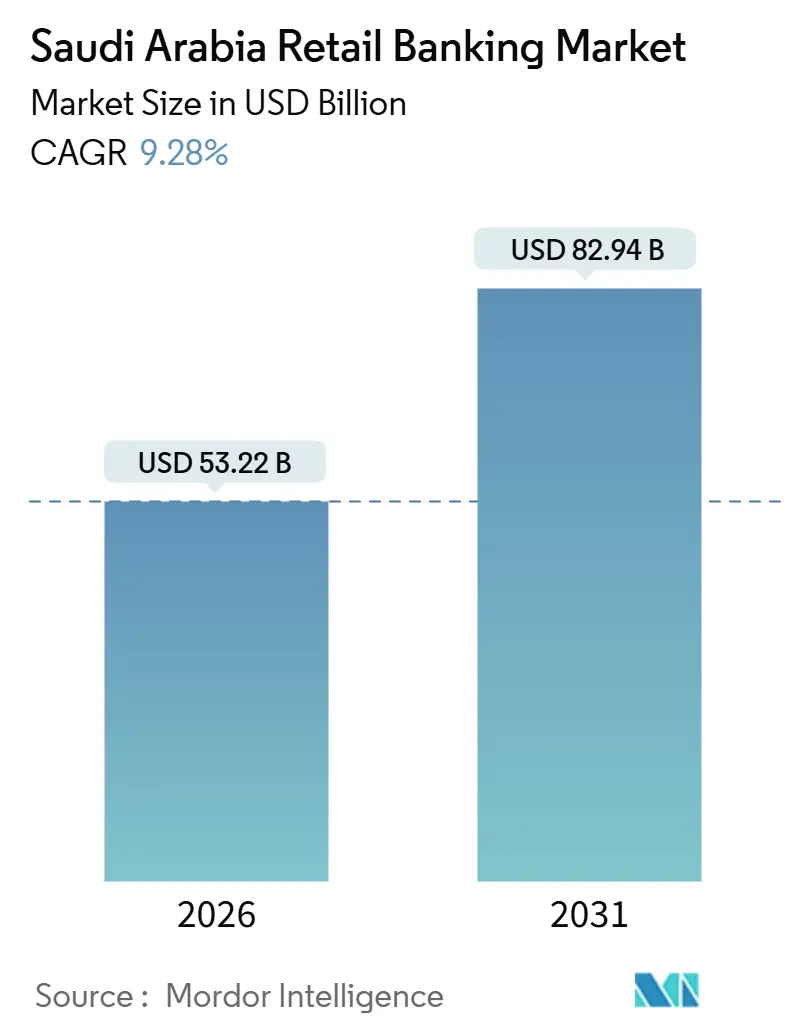

| Market Size (2026) | USD 53.22 Billion |

| Market Size (2031) | USD 82.94 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Retail Banking Market Analysis by Mordor Intelligence

The Saudi Arabia retail banking market size stands at USD 53.22 billion in 2026 and is forecasted to reach USD 82.94 billion by 2031, advancing at a 9.28% CAGR. Growth is shaped by Vision 2030-linked housing finance programs, systemwide adoption of Sharia-compliant product standards, and the deployment of SAMA’s real-time payments infrastructure, SARIE, which lifted electronic payments to 79% of retail transactions in 2024. Product momentum is rotating toward cards supported by near-universal contactless acceptance and issuer-led loyalty features. Household leverage continued to expand within prudential limits, as consumer loan balances reached SAR 476 billion (USD 126.84 billion) in Q3 FY2025 and real-estate loans to individuals reached SAR 726.2 billion (USD 193.50 billion), supported by salary-assignment frameworks that stabilized asset quality[2]Ministry of Finance, “Budget Statement FY2026,” Ministry of Finance, mof.gov.sa .

Key Report Takeaways

- By product, transactional accounts led with 38.26% of the Saudi Arabian retail banking market share in 2025, while credit cards are projected to expand at a 12.68% CAGR through 2031.

- By channel, online banking accounted for 58.77% of the Saudi Arabian retail banking market share in 2025, and it is projected to record the highest growth at a 14.74% CAGR through 2031.

- By customer age group, the 29–44 years segment held 40.52% of the Saudi Arabian retail banking market share in 2025, while the 18–28 years cohort is projected to grow at a 13.43% CAGR through 2031.

- By bank type, national banks retained 81.89% of the Saudi Arabian retail banking market share in 2025, while Neobanks & others are projected to grow at 18.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Retail Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030-Led Mortgage Subsidy Programs Accelerating Home-Financing Demand | +2.1% | National, with early gains in Riyadh, Jeddah, and Eastern Province | Medium term (2–4 years) |

| SAMA's Instant Payment System (SARIE) Boosting Non-Cash Retail Transactions | +1.9% | National, spill-over to GCC via cross-border payment pilots | Short term (≤ 2 years) |

| Mandatory Ijara & Murabaha Compliance Catalysing Islamic Lending Penetration | +1.4% | National, concentrated in Sharia-compliant retail segments | Medium term (2–4 years) |

| Fintech-Licence Regime Enabling Digital-Only Challenger Banks | +1.8% | National, with higher adoption in urban centres (Riyadh, Jeddah, Dammam) | Short term (≤ 2 years) |

| Rapid Youth & Expat Workforce Growth Expanding Addressable Mass-Market Deposits | +1.3% | National, with an outsized impact in Riyadh, Eastern Province | Long term (≥ 4 years) |

| Government Salary-Assignment Scheme Stabilising Personal-Loan Asset-Quality | +0.9% | National, benefiting public-sector-focused lenders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030-Led Mortgage Subsidy Programs Accelerating Home-Financing Demand

Saudi Arabia’s housing agenda remains central to retail-credit formation, with progress toward the 70% homeownership target supporting steady loan origination pipelines while also creating periodic demand swings during policy recalibrations. Lenders continue to adapt to subsidy scope adjustments by tightening underwriting on unsubsidized exposures and refining risk-based pricing for mid-income segments to safeguard portfolio yields under evolving program parameters. Non-bank mortgage specialists have complemented bank balance sheets by securitizing Islamic home-finance receivables, which recycle capital and accelerate loan supply without straining deposit-funded capacity, including issuances in 2025 that signalled investor appetite for asset-backed structures. Product innovation now intersects with sustainability mandates, as evidenced by a USD 1 billion green sukuk in 2024 structured to support clean-energy housing, which attracted both ESG-focused institutions and retail participants. Regulatory standard-setting in Islamic finance, especially the anticipated Sharia Standard 62 on asset-backed sukuk, is poised to nudge funding costs higher by 20–30 basis points but could deepen secondary-market liquidity and diversify the investor base. Digital execution continues to compress cycle times, with leading incumbents reporting sharp growth in online mortgage origination throughput during 2025, a pattern that aligns with consumers’ preference for app-based pre-approvals and lighter-branch engagement.

SAMA's Instant Payment System (SARIE) Boosting Non-Cash Retail Transactions

The share of electronic payments in retail transactions reached 79% in 2024, reflecting mass adoption of real-time rails and pervasive mobile usage that shifted routine payments from cash to instant account-to-account movements. Card acceptance also remains extensive, with domestic debit activity scaling to billions of annual point-of-sale transactions and nationwide contactless infrastructure across millions of terminals that reinforce the digital-first habit for both consumers and merchants. Cross-border architecture is evolving in parallel, as SAMA joined the BIS mBridge multi-CBDC initiative in 2024 to trial near-instant cross-border settlements with key Asian and GCC hubs, which positions the riyal as a credible settlement currency for regional trade corridors. Digital wallet penetration is deep among residents, and large ecosystem operators continue to scale, enabling banks and fintechs to embed payment initiation and value-added services that accelerate checkout and reduce friction at the point of interaction. SAMA’s E-Wallet Rules, issued in November 2024, formalized segregation of customer funds and established minimum capital requirements of SAR 10 million (USD 2.7 million), which raised operating standards and reduced regulatory uncertainty for scaled players. The combined effect is a payment landscape where instant transfers, best-in-class acceptance, and clarified licensing catalyse more digital origination across the Saudi Arabian retail banking market.

Fintech-Licence Regime Enabling Digital-Only Challenger Banks

SAMA’s licensing agenda has expanded the roster of regulated digital operators across buy-now-pay-later, wallets, crowdfunding, and digital-only banks, which has lowered barriers to product experimentation and pushed incumbents to accelerate their own digital roadmaps. New digital banks launched operations during 2024 and 2025 with machine-learning underwriting, instant account opening, and app-first experiences that resonated with younger and digitally savvy customers. Minimum capital requirements for full-scope digital bank licenses are set at SAR 2.5 billion, which ensures entrants are adequately capitalized and capable of meeting prudential obligations as they scale lending and payments. Wallet ecosystems from large telecom-backed platforms also provide powerful distribution and embedded-finance rails that new banks can leverage to reach users with high-frequency payment use cases and seamless onboarding. The combination of regulatory clarity, minimum capital thresholds, and deep consumer familiarity with digital payments is expanding the digital share of origination across the Saudi Arabian retail banking market. As operators mature, partnerships with incumbents for Banking-as-a-Service and open-banking connectivity continue to unlock new use cases for instant financing and embedded transactions at the point of sale.

Rapid Youth & Expat Workforce Growth Expanding Addressable Mass-Market Deposits

A youthful population structure and sustained job creation under Vision 2030 projects are expanding the base of salaried customers, which supports steady inflows into transactional accounts and payroll-linked lending across major metro centres. At the same time, adoption of mobile banking continues to rise, with a large majority of retail customers now using mobile apps to manage accounts and credit products, which shifts servicing and origination to online channels. Digital banks launched in 2024 and 2025 are targeting this segment with instant onboarding, fee-free transactional accounts, and micro-savings features that fit the needs of first-time bankers and early-career professionals. Payroll flows tied to Vision 2030 contractor and supplier ecosystems also create a pipeline of new-to-bank customers in cities like Riyadh, Jeddah, and Dammam, where large-scale infrastructure and services projects are underway. The structural tilt toward mobile-first behaviour and program-driven employment is increasing deposit growth potential and digital sales conversion in the Saudi Arabian retail banking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cooling Mortgage Growth Post-Subsidy Phase-Out Pressuring Retail Loan Yields | -0.8% | National, with a sharper impact in lower-income provinces (Northern Borders, Jazan) | Short term (≤ 2 years) |

| Tight Liquidity & Rising Time-Deposit Costs Compressing Net-Interest-Margins | -1.1% | National, acute in banks with loan-to-deposit ratios above 115% | Medium term (2–4 years) |

| Limited Retail Credit Bureau Depth Hindering Risk-Based Pricing for New-to-Bank | -0.4% | National, most severe in rural areas with thin financial histories | Long term (≥ 4 years) |

| Sharia Standard 62 Transition Risk for Variable-Rate Islamic Products | -0.3% | National, concentrated among Islamic banks and hybrid lenders | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Tight Liquidity & Rising Time-Deposit Costs Compressing Net-Interest-Margins

The sector’s loan-to-deposit ratio reached 111.3% in April 2025, up 672 basis points year over year, which signalled persistent funding tightness and drove banks to pay up for time deposits to support loan growth. Funding-cost pressure flowed through to net interest margins at mid-tier lenders during 2024 results, and similar patterns persisted into 2025 as the deposit mix shifted toward term products that carry higher coupon costs. International assessments of Saudi Arabia’s macro-financial conditions flagged a decline in liquid assets to short-term liabilities and the reversal of net foreign assets in 2024, which constrained the latitude for broad-based liquidity injections without exchange-rate ramifications. Banks responded by fortifying capital through Tier 2 issuances during Q3 2025, which helped maintain capital adequacy at healthy levels while providing room to continue lending into priority segments. Even so, competition for deposits is expected to remain elevated, which will keep margin management central to earnings resilience across the Saudi Arabian retail banking market.

Sharia Standard 62 Transition Risk for Variable-Rate Islamic Products

AAOIFI’s Sharia Standard 62, poised for final approval, would require sukuk structures to meet strict asset-transfer criteria that emphasize true sale, which differs from widely used asset-based models. This could complicate the use of public infrastructure assets in sukuk pools and may necessitate portfolio restructuring across sovereign and quasi-sovereign issuers, which might reduce near-term issuance capacity. Variable-rate Islamic mortgages and corporate Murabaha facilities would need alignment with asset-backed cash-flow certainty under the standard, which could prompt a shift toward fixed-rate structures and duration risk management on bank balance sheets. Funding costs may rise by 20–30 basis points during the transition as markets internalize structural changes and documentation updates, though deeper global investor participation could offset some cost pressures over time. Banks are preparing governance and structuring playbooks under existing Sharia governance rules to ensure consistent interpretation and reduce fragmentation across the Saudi Arabian retail banking market as the standard is finalized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Credit Cards Lead Growth as Transactional Accounts Dominate Share

Transactional accounts held the largest share at 38.26% in 2025, which confirms their role as salary and payments anchors for retail customers across major cities and growth corridors. Credit card portfolios are projected to deliver the strongest growth at a 12.68% CAGR through 2031, supported by widespread contactless acceptance and issuer investment in rewards ecosystems that lift usage and retention. Debit cards continue to see near-universal tap-to-pay usage at the point of sale, reflecting a mature acceptance infrastructure with millions of active terminals nationwide. The steady expansion of consumer finance and real-estate lending, alongside stable repayment under salary-linked frameworks, reinforces multi-product relationships that underpin low attrition rates for customers with broader product stacks. These dynamics keep payments, deposits, and lending tightly integrated in the Saudi Arabian retail banking market as banks balance volume growth with risk and margin control.

Credit card expansion is also benefiting from instant decisioning embedded in mobile journeys, which shortens application-to-activation timelines and lifts first-month usage, especially among digital-first cohorts. Consumer loan balances reached SAR 476 billion (USD 126.84 billion) in Q3 FY2025, and individual real-estate loans climbed to SAR 726.2 billion (USD 193.50 billion), providing a broad base for cross-sell into cards, instalment plans, and protection products. Debit transactions remained overwhelmingly contactless during 2024, which continues to acculturate customers to digital payments and drives spend to issuers that deliver the smoothest tap-to-pay experience. Product innovation in Islamic formats is steady across mortgages and personal finance, backed by governance standards that ensure consistency and comparability for customers across providers. These product-level shifts collectively support the long-run expansion of the Saudi Arabian retail banking market and set the stage for deeper engagement across payments, deposits, and credit.

By Channel: Online Banking Captures Majority Share and Fastest Growth

Online banking accounted for 58.77% of value in 2025 and is projected to grow at a 14.74% CAGR through 2031, confirming that digital is the primary revenue engine for consumer finance in the country. The share of electronic payments reached 79% of retail transactions in 2024, which reinforced online account primacy for transactions and servicing. Leading incumbents reported strong growth in digital personal-finance sales during 2025, while branch footprints were re-optimized toward SME and advisory centres rather than transaction processing. Millions of POS terminals and domestic-card transaction volumes also underpin digital readiness among merchants, which helps shift high-frequency spend and service interactions away from cash and branches. These shifts sustain higher digital origination in the Saudi Arabian retail banking market and compress time-to-yes across lending and card issuance.

Offline channels continue to serve wealth, complex mortgage underwriting, and corporate treasury needs where face-to-face interactions and extensive documentation remain valuable, yet even these areas are incorporating video advice and digital signatures to streamline journeys. Branch networks were modestly reduced in 2025 as institutions reallocated space to specialized centres, which indicates a pivot from transactional density to relationship depth. Digital-only banks launched with channel-exclusive strategies during 2024 and 2025, using instant onboarding and in-app servicing to draw in first-time bankers and digital natives. Open-banking rules that introduced payment initiation alongside account information services enable merchants and fintechs to integrate instant funds movement directly into checkout and bill-pay flows, which reinforces digital-first behaviour. As these capabilities mature, the Saudi Arabian retail banking market will see further gains in digital share, while branches deepen their focus on advice and complex sales.

By Customer Age Group: Millennials Dominate While Gen Z Posts Fastest Growth

The 29–44 years segment held 40.52% share in 2025, reflecting peak earning years and a higher likelihood of owning multiple products across deposits, cards, and home finance. The 18–28 years cohort is projected to post the fastest growth at a 13.43% CAGR through 2031 as digital origination expands, mobile adoption deepens, and instant decisioning becomes the norm in entry-level credit. Digital banks have targeted younger customers with zero-fee transactional accounts and rapid approvals that align with their expectations for app-first service and transparent pricing. Incumbents also reported significant increases in digital financing volumes in 2025, a signal that product penetration among younger cohorts is rising within incumbent ecosystems as well. These trends reinforce generational convergence toward mobile channels and embedded finance within the Saudi Arabian retail banking market.

Older cohorts continue to value branch-based interactions for complex needs, yet their usage of mobile apps and remote servicing is rising as banks streamline digital journeys and expand support channels. The result is a multi-generational customer base that is more comfortable executing standard transactions online, placing offline teams in roles that emphasize advice, onboarding for complex products, and relationship management. Digital-only entrants strengthened their appeal to early-career customers through simple bill-pay, micro-savings, and credit features that bundle smoothly into daily mobile behaviours. Incumbents are responding with faster decision-making and simplified pricing, which narrows the perceived experience gap and raises retention as their mobile capabilities mature. These moves should keep customer-level growth balanced across age groups in the Saudi Arabian retail banking market through the forecast window.

By Bank Type: National Banks Retain Dominance as Neobanks Disrupt at a significant CAGR

National banks held 81.89% share in 2025, reflecting deep deposit franchises, strong capital adequacy, and multi-product ecosystems that span payments, lending, and wealth. Neobanks & others are projected to grow at 18.29% CAGR through 2031 as they scale app-first models, automate underwriting, and bring new users into the formal financial system through straightforward onboarding. Leading incumbents supplemented organic growth with Tier 2 issuances during 2025 to support lending capacity and maintain strong capital buffers, which signals durable competitiveness amid rising digital rivalry. Minimum capital set by SAMA for new digital-bank licenses at SAR 2.5 billion also raises the bar for entrants and favours well-capitalized players that can scale prudently under the prudential regime. These structural pillars ensure incumbents remain central in the Saudi Arabian retail banking market even as challengers add competitive intensity.

New market entries by foreign institutions in late 2025 widened service offerings in trade finance and wealth, while domestic institutions deepened specialization in SME and corporate advice centres across major cities. Non-bank lenders extended mortgage capacity via securitization programs during 2025, which increased competitive pressure for customer acquisition across home finance and related cross-sell products. Large Sharia-compliant banks maintained leading loan books in 2024, supported by strong demand for Islamic products under updated governance standards. Challenger banks are differentiating through user experience and speed, but face the same prudential capital and liquidity standards, which encourage disciplined scaling and partnerships with incumbents for certain services. This interplay is likely to keep the Saudi Arabian retail banking market competitive and innovative through 2031.

Geography Analysis

Retail banking activity is concentrated in the Central, Western, and Eastern regions, where population density, government employment, and private-sector investment produce strong deposit flows and loan origination pipelines. Incumbents optimized their branch networks in 2025 by trimming low-traffic locations and expanding specialized centres for SMEs and advisory services in key urban areas, which supports higher-margin engagement. Digital tooling and centralized cloud platforms allow both banks and fintechs to serve remote regions without full-service branches, which reduces geographic disparities in access to mobile-first services. Payment acceptance is widespread, and domestic debit processing at scale supports both urban and non-urban commerce as customers migrate to electronic transactions. These channel shifts and servicing models strengthen inclusive coverage across the Saudi Arabian retail banking market.

Riyadh continues to draw outsized project investment under Vision 2030, which channels payroll flows, SME banking needs, and supplier finance into the capital region. Banks responded by opening new SME and advisory centres in 2025 and by scaling digital channels to absorb routine transactions, which improves both cost-to-serve and customer satisfaction. The Western region exhibits healthy diversification in services and tourism-linked activity that sustains retail demand for deposits, cards, and consumer finance products. The Eastern Province benefits from energy-sector employment and cross-border flows, and participation in the BIS mBridge project sets the foundation for faster regional settlements that could benefit local corridors. These pockets of momentum reinforce national growth in the Saudi Arabian retail banking market as projects and ecosystems scale.

Branch density remains lower in certain northern and southern provinces, but mobile banking and wallet adoption mitigate access constraints as digital onboarding and e-KYC propagate. Payments and open-banking rules enable licensed operators to provision services nationally without full physical presence, which reduces disparities between urban centres and rural districts. The FY 2026 borrowing plan and continued investment in infrastructure projects channel payroll, contractor payments, and account openings into regions where project workforces are concentrated. As digital penetration deepens, region-specific product mixes are likely to converge, with advisory-heavy services concentrated in flagship locations and routine transactions fully digital across the Saudi Arabian retail banking market. This structure supports steady national growth even as regional composition evolves under Vision 2030.

Competitive Landscape

Market structure remains moderately consolidated, with large national banks sustaining leadership through deposit franchises, capital strength, and broad product portfolios, while digital-only entrants add intensity through experience-led differentiation. Leading banks tapped Tier 2 capital in Q3 2025 to maintain robust capital adequacy and fund growth, and non-bank lenders executed securitization programs to scale originations without drawing heavily on deposits. BNPL platforms secured sizable facilities to expand merchant coverage and consumer adoption, which increases competition with incumbent card issuers in instalment financing[3]Tamara, “USD 2.4 Billion Asset-Backed Financing Facility,” Tamara, tamara.co. Sharia governance standards introduced in 2024 raised compliance requirements for all providers of Islamic products, which boosted confidence and comparability across offerings. The result is a dynamic Saudi Arabia retail banking market that blends strong incumbents, capital-market funding, and digital-led challengers.

Incumbents also rebalanced physical networks toward SME and advisory hubs in 2025 while leaning into mobile-first origination for consumer finance and cards, which shortens cycle times and lifts conversion. Foreign entrants opened operations in 2025 to address trade finance and wealth niches, which broadens specialization and adds competitive options for corporate and affluent clients. Regulatory momentum on open banking and payments continues to encourage partnerships between banks and fintechs, which accelerates embedded finance use cases in merchant checkout and SME financial operations. Liquidity conditions in 2025 required disciplined pricing of time deposits and careful margin management, which heightened the importance of fee-light digital distribution for cost efficiency. These strategic choices point to continued emphasis on speed, convenience, and ecosystem connectivity across the Saudi Arabian retail banking market.

Selective M&A-style consolidation in fintech infrastructure and partnerships in corporate payments gained momentum during late 2025, which is likely to influence treasury and expense-management solutions for SMEs. Banks and fintechs expanded Banking-as-a-Service arrangements to monetize core-processing and cash-management capabilities under the prevailing regulatory frameworks. Digital-only banks continued to leverage strong wallet ecosystems to broaden product uptake, while incumbents invested in faster decisioning and simplified digital journeys that improved parity in user experience. With sustained capital adequacy and greater capital-market access, incumbents remain well positioned to invest through the cycle and defend share against agile entrants in the Saudi Arabia retail banking market. The interplay of funding strength, regulatory clarity, and digital innovation should keep competitive intensity elevated through the forecast horizon.

Saudi Arabia Retail Banking Industry Leaders

Saudi National Bank

Al Rajhi Bank

Riyad Bank

Alinma Bank

Saudi Awwal Bank (SAB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SAMA licensed Tabby Finance for buy-now-pay-later services, Darb Pay for e-wallet operations, and Madd Balas for debt-based crowdfunding, raising the fintech-company count and signalling the regulator's commitment to fostering financial-services competition.

- November 2025: Union Bancaire Privée opened a Riyadh office targeting ultra-high-net-worth wealth management, signalling foreign confidence in the Kingdom’s financial-services trajectory.

- October 2025: The National Bank of Egypt launched its first Saudi Arabia branch in October 2025, focusing on corporate and trade-finance services to support Egyptian-Saudi bilateral commerce.

- September 2025: EZ Bank received SAMA approval for a digital-banking license with SAR 2.5 billion in capital on September 30, 2025, becoming a new neobank authorized to compete with incumbents.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia retail banking market as all fee- and interest-based products and services offered by licensed banks directly to individual residents and expatriates, including transactional and savings accounts, personal and auto loans, mortgages, debit and credit cards, and basic wealth products.

Scope exclusion: commercial and wholesale banking activities that target corporates or public entities fall outside this analysis.

Segmentation Overview

- By Product

- Transactional Accounts

- Savings Accounts

- Debit Cards

- Credit Cards

- Loans

- Other Products

- By Channel

- Online Banking

- Offline Banking

- By Customer Age Group

- 18-28 Years

- 29-44 Years

- 45-59 Years

- 60 Years and Above

- By Bank Type

- National Banks

- Regional Banks

- Neobanks & Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with branch managers, digital-bank executives, consumer-finance officers, and fintech regulators across Riyadh, Jeddah, Dammam, and Abha. Insights on average ticket sizes, mobile-app adoption, and subsidy tapering helped us stress-test growth assumptions and reconcile discrepancies spotted in desk data.

Desk Research

We began by mining publicly available sources such as Saudi Central Bank (SAMA) statistical bulletins, Ministry of Finance budget releases, General Authority for Statistics household surveys, and Vision 2030 dashboards, which give granular data on deposits, loan books, digital-payment volumes, and demographic shifts. Trade bodies like the Union of Arab Banks and Shariah Standards publications supplied regulatory milestones and Islamic-product adoption metrics.

To refine competitive benchmarks, our analysts tapped paid repositories, D&B Hoovers for bank financials and Dow Jones Factiva for newsflow around branch closures, fintech licenses, and SARIE transaction counts. These inputs anchor trend lines before we layer in proprietary estimates. The sources listed illustrate the mix; many additional documents were reviewed to validate facts and fill gaps.

Market-Sizing & Forecasting

We apply a top-down construct that rebuilds retail revenue pools from SAMA deposit and lending tables, card-spend statistics, and fee schedules, which are then cross-checked with bottom-up snapshots such as sampled average selling price multiplied by active card base or mortgage drawdowns by lender tier. Key variables like household formation, real-wage growth, e-payment penetration, mortgage subsidy cadence, and neobank customer migration feed a multivariate regression that projects values to 2030. Where branch-level roll-ups under-report, we interpolate using Vision 2030 targets or past elasticity between GDP per capita and retail credit. This is where Mordor Intelligence differentiates, ensuring every leap is traceable.

Data Validation & Update Cycle

Before sign-off, outputs pass a two-analyst variance check against alternative data such as ATM cash withdrawals and mobile-wallet KPIs; anomalies trigger re-contact of earlier respondents. Models refresh annually, with interim tweaks when policy or macro shocks exceed predefined thresholds.

Why Our Saudi Arabia Retail Banking Baseline Inspires Confidence

Published estimates seldom align because firms pick different service baskets, convert currencies at varied dates, and refresh on uneven cadences.

Key gap drivers here include whether Islamic profit-sharing accounts are blended with conventional deposits, the treatment of fee income from brokerage apps, and if expatriate remittance products are rolled into retail totals. Mordor's base year (2025) squarely captures these elements using the latest SAMA series and verified bank disclosures, while some peers extrapolate older or partial datasets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 48.7 B (2025) | Mordor Intelligence | - |

| USD 185.6 B (2024) | Global Consultancy A | Includes corporate deposits and treasury gains, inflating base |

| USD 19.4 B (2024) | Regional Consultancy B | Omits Islamic profit-sharing accounts and digital-wallet float |

| USD 19.98 B (2024) | Trade Journal C | Uses pre-merger bank data and fixed 3-year refresh cycle |

Taken together, the comparison shows that when scope discipline, up-to-date inputs, and transparent cross-checks converge, as in Mordor's framework, decision-makers receive a balanced, reproducible baseline they can rely on.

Key Questions Answered in the Report

What is the size and growth outlook for the Saudi Arabian retail banking market?

The Saudi Arabia retail banking market size is USD 53.22 billion in 2026 and is forecasted to reach USD 82.94 billion by 2031 at a 9.28% CAGR.

Which product categories are leading, and which are growing fastest in Saudi Arabia's retail banking?

Transactional accounts lead by share at 38.26% in 2025, while credit cards are the fastest-growing product with a projected 12.68% CAGR through 2031.

How are digital channels shaping performance in the Saudi Arabian retail banking market?

Online banking holds 58.77% of value in 2025 and is projected to grow at a 14.74% CAGR, supported by 79% electronic-payment penetration and rising mobile usage.

Which customer segments are most important for growth?

The 29-44 years segment holds 40.52% share in 2025, while the 18-28 years cohort is the fastest growing with a 13.43% CAGR, driven by digital-first origination.

What are the key regulatory and payment infrastructure drivers?

SAMA's open banking and SARIE instant payments are enabling real-time fund movement and embedded finance, while Sharia governance standards raise consistency for Islamic products.

How is liquidity affecting bank performance in 2025?

The loan-to-deposit ratio reached 111.3% in April 2025, increasing reliance on time deposits and pushing banks to manage net interest margin pressure while reinforcing capital buffers.

Page last updated on: