Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

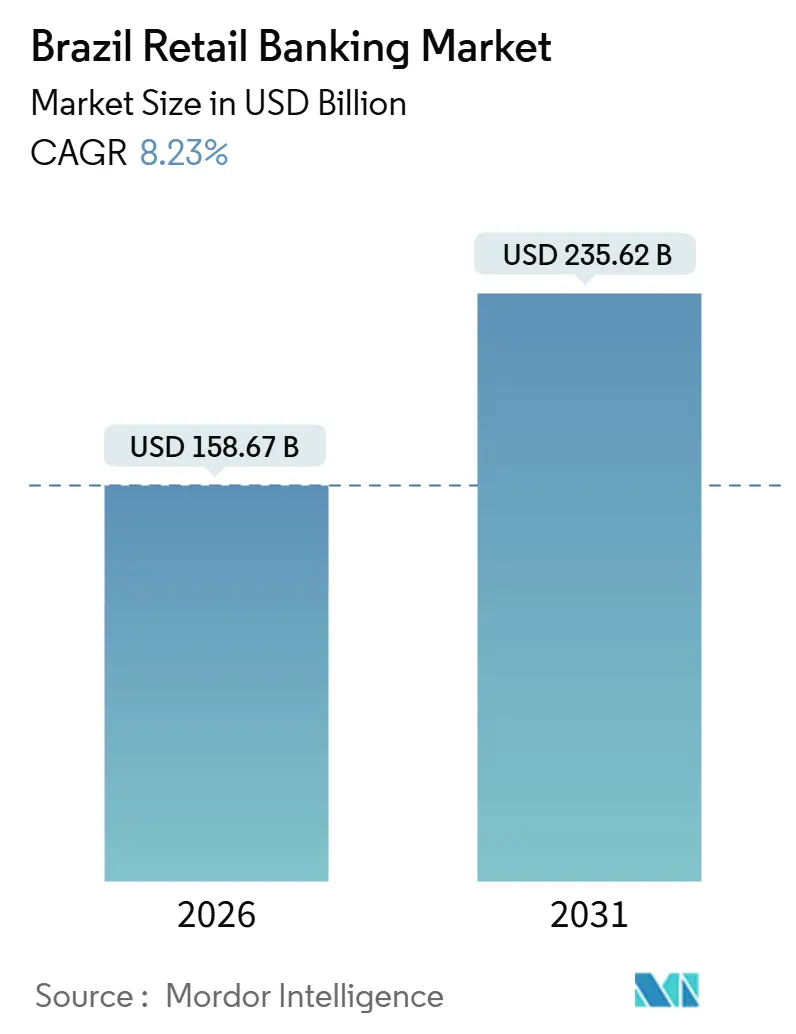

| Market Size (2026) | USD 158.67 Billion |

| Market Size (2031) | USD 235.62 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

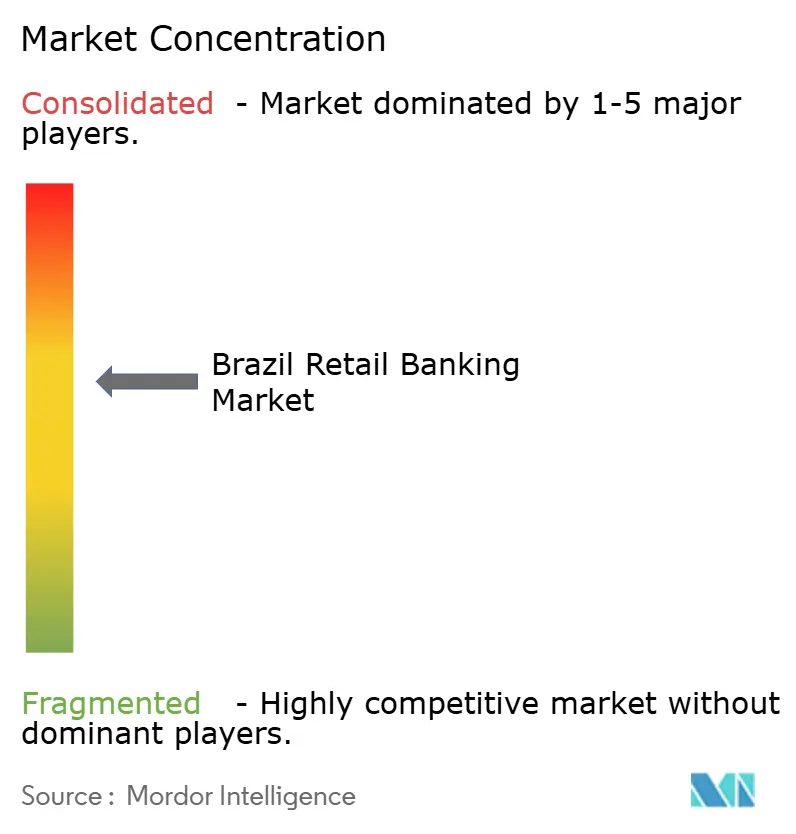

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Retail Banking Market Analysis by Mordor Intelligence

The Brazil retail banking market size is USD 158.67 billion in 2026 and is forecast to reach USD 235.62 billion by 2031 at an 8.23% CAGR. Adoption of instant payments at a national scale, mandatory open-finance data sharing, and digital-only entrants reshape origination, cross-sell, and funding economics in the Brazil retail banking market. Open Finance logged tens of millions of authorized consents and billions of weekly data requests, enabling lenders to refine underwriting and lower friction in onboarding and refinance journeys across the Brazil retail banking market. National banks still anchor scale in the Brazil retail banking market, while neobanks leverage lower cost-to-serve and data-driven risk models that supported a 19.1% ROE for digital banks by mid-2024, signalling a durable shift in competitive dynamics.

Key Report Takeaways

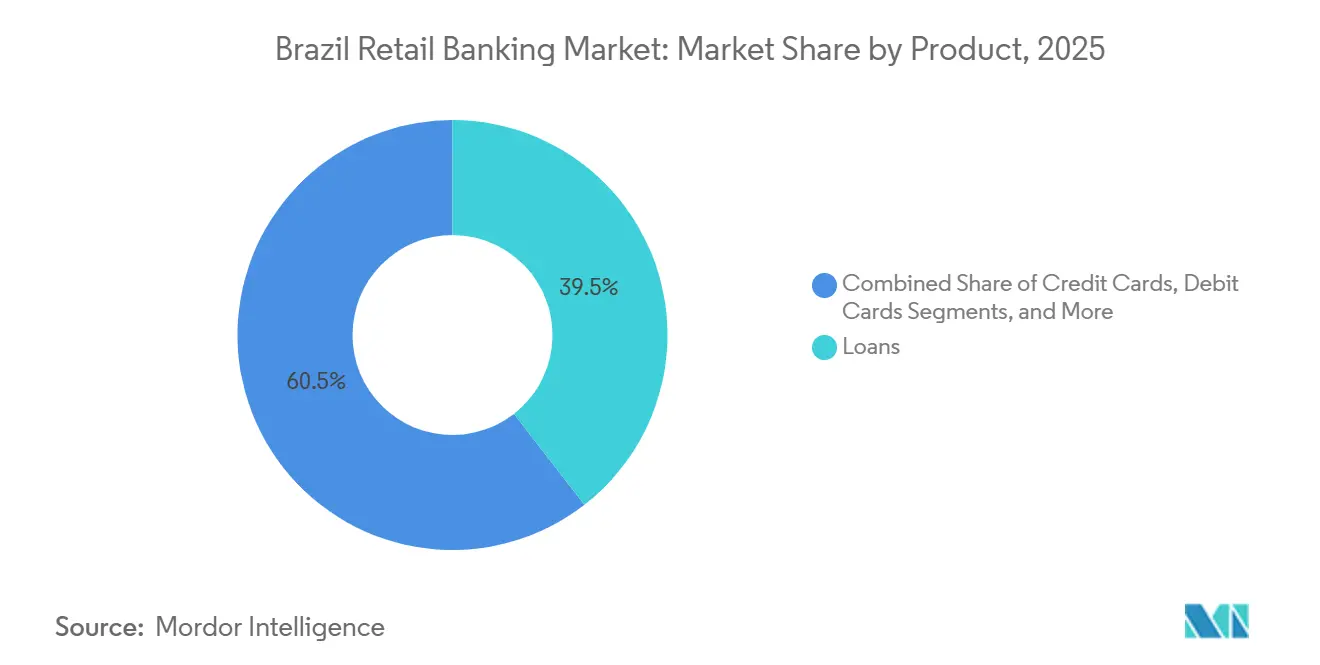

- By product, loans held 39.48% of the Brazil retail banking market share in 2025; credit cards are forecasted to grow at a 12.21% CAGR through 2031.

- By channel, offline banking accounted for 56.52% of the transaction value of the Brazil retail banking market share in 2025, while online banking is projected to record a 14.19% CAGR through 2031.

- By customer age group, the 29–44 cohort held 42.61% of customer accounts of the Brazil retail banking market share in 2025, while the 18–28 segment is set to expand at a 13.43% CAGR through 2031.

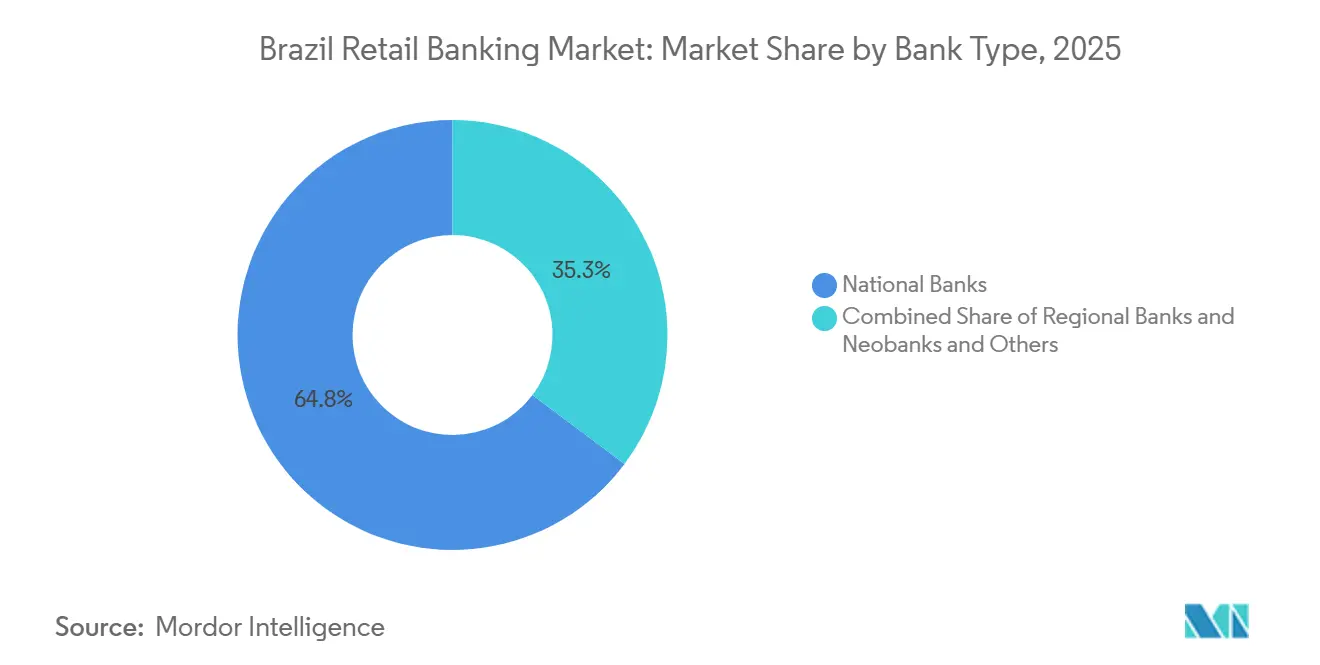

- By bank type, national banks commanded 64.75% of the Brazil retail banking market share in 2025, while neobanks and others are projected to post a 15.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Retail Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pix Instant-Payment Adoption Accelerating Account Growth | +2.8% | National, strongest in Southeast, Northeast, South | Medium term (2-4 years) |

| Open Finance Regulations Fuelling Product Innovation and Competition | +1.9% | National, with the strongest uptake in major urban centres | Medium term (2-4 years) |

| Rise of Digital-Only Challenger Banks Driving Financial Inclusion | +2.1% | National, strong in underbanked regions and among the 18–28 cohort | Long term (≥ 4 years) |

| Government Social-Transfer Programs Boosting Deposit Volumes | +0.9% | National, concentrated in lower-income brackets | Short term (≤ 2 years) |

| Smartphone Penetration Enabling Mobile-First Banking Onboarding | +1.3% | National, strongest in metropolitan areas | Medium term (2-4 years) |

| Interest-Rate Volatility Preserving High Retail Lending Spreads | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pix Instant-Payment Adoption Accelerating Account Growth

PIX, Brazil's instant payment system, covers 90% of the population, positively impacting financial inclusion, the informal economy, and small and medium-sized enterprises (SMEs). Person-to-business flows overtook person-to-person transfers in late 2025, indicating deeper merchant adoption that aligns with lower acceptance costs than card interchange, which improves working capital for small sellers across the Brazil retail banking market. Real-time settlement reduced cash-cycle frictions for large buyers and their supplier networks, with documented case studies showing that payment windows shrank from minutes to seconds for agricultural producers, which supports liquidity and reinvestment decisions. The central bank’s governance of Pix added dispute-resolution tooling and ongoing fraud-prevention enhancements, which underpin trust and support expansion into recurring-billing and point-of-sale use cases in the Brazil retail banking market. As Pix penetrates subscription and invoice use cases, the merchant and consumer activity pools increase the addressable base for cross-sell into checking, cards, and small-ticket credit across the Brazil retail banking market.

Open Finance Regulations Fueling Product Innovation and Competition

Open finance scaled under reciprocity rules that require data sharing by all regulated institutions, with tens of millions of customer consents and billions of weekly API calls recorded as the framework matured through 2025. The architecture supports payment initiation over consented rails and credit-decisioning that integrates payroll, transaction, and portfolio histories from multiple institutions, which reduces information asymmetry and speeds time to decision in the Brazil retail banking market. The central bank’s 2025–2026 roadmap includes credit-portability services with public availability staged for early 2026, which enables frictionless lender switching and intensifies price competition across unsecured and payroll-deducted credit. Investment-data aggregation continues to expand, allowing clients to consolidate views of accounts across brokers and banks, which strengthens cross-sell moves by wealth platforms and universal banks.

Rise of Digital-Only Challenger Banks Driving Financial Inclusion

Digital banks’ ROE rose to 19.1% by mid-2024 as operational leverage improved and provisioning expenses trended lower than those of traditional institutions, validating scalable unit economics for mobile-first players in the Brazil retail banking market. Nubank reported 123 million customers across Brazil, Mexico, and Colombia, and record quarterly revenue of USD 3.7 billion in Q2 2025, while activity rates remained above 83%, which points to durable engagement in core products and add-ons [1]Banco Central do Brasil, “Monetary Policy Report – June 2025,” Banco Central do Brasil, bcb.gov.br. Inter closed Q3 2025 with 41 million total customers and 24 million active accounts, growing its credit portfolio at triple the market pace through private payroll offerings and CX improvements that contained NPL ratios despite macro headwinds [2]OECD, “Brazil: OECD Economic Outlook, Volume 2025 Issue 1,” OECD, oecd.org. Instant-payment access also expanded participation, with multilateral research noting that Pix enabled tens of millions of first-time account-to-account transfers, which broadened the funnel for digital onboarding and basic financial services across the Brazil retail banking market. Regulatory parity on KYC, AML, and authentication, enforced by the central bank, aligns challenger compliance standards with incumbents and sustains confidence in continued scale-up.

Interest-Rate Volatility Preserving High Retail Lending Spreads

Central bank communications in 2025 emphasized a significantly contractionary stance for a prolonged period to ensure convergence of inflation toward the target, which sustained higher retail lending spreads and cautious credit supply in the Brazil retail banking market. Non-earmarked household credit costs rose faster than policy rates over the year as banks incorporated rising delinquency risks into pricing across credit cards and overdrafts [3]BrazilCham, “Inter&Co Reports Record 3Q25 Results, Driven by 30% Credit Expansion and 39% Net Income Growth,” Brazilian-American Chamber of Commerce, brazilcham.com. External funding conditions tightened as frontier-market bond yields climbed toward double digits on average since April 2025, which raised wholesale costs for institutions accessing international markets. The central bank’s forecasts pointed to slower real credit growth in 2025 and 2026 compared with 2024, aligning with tighter financial conditions and higher risk premia in the Brazil retail banking market. Capital and leverage rules under Basel III continued to constrain balance-sheet growth, which encouraged a tilt toward higher-spread retail products relative to lower-margin corporate facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Credit-Delinquency Among Low-Income Borrowers | -1.2% | National, concentrated in lower-income brackets and rural portfolios | Short term (≤ 2 years) |

| Net-Interest-Margin Compression From Selic Rate Cuts | -0.8% | National | Medium term (2-4 years) |

| High Market Concentration Hindering New-Entrant Scale-Up | -0.5% | National | Long term (≥ 4 years) |

| Rising Cyber-Fraud and Compliance Costs | -0.6% | National, with an elevated impact on payment institutions and BaaS providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Net-Interest-Margin Compression From Selic Rate Cuts

A leading digital bank’s reported NIM moved lower in Q1 2025 as funding costs rose faster than asset repricing, and its risk-adjusted NIM also declined due to higher credit-loss allowances in a changing mix. Central bank projections pointed to slower nominal and real credit growth in 2025 and 2026 than in 2024, which set a backdrop of tighter spreads and cautious originations in the Brazil retail banking market. Non-earmarked household credit granting moderated in late 2024 and shifted toward emergency modalities like revolving cards and overdrafts, which shortened average tenors and concentrated refinancing risk. Real estate lending slowed as the cost of operations rose with policy tightening, which weighed on mortgage affordability and volumes. Macro forecasts indicated decelerating GDP growth into 2026 with inflation above target, reinforcing a restrictive policy stance that will keep liability costs elevated against asset yields in the Brazil retail banking market [4]Nu Holdings, “Nubank Applies for U.S. National Bank Charter,” Nu Holdings, international.nubank.com.br.

Rising Cyber-Fraud and Compliance Costs

Technology and risk-control investments lifted non-interest expenses at leading banks in 2025 as institutions hardened systems and modernized infrastructure for digital channels in the Brazil retail banking market. Supervisors expanded the Risk and Control Assessment model to capture aggressive practices, high indebtedness, and incentive-related conduct risks, with the next cycle broadening the scope to additional entrants from January 2026. Climate-risk management requirements advanced through 2025, with system exposure to drought and water stress cited frequently, and more institutions reporting tangible impacts than a year earlier, which adds to disclosure and risk-modelling workloads. The central bank’s 2025–2026 agenda prioritized continued enhancements of open finance, payments security, and supervisory tooling, reinforcing a tighter compliance perimeter for both incumbents and fintechs in the Brazil retail banking market. The accumulation of cybersecurity spend and regulatory reporting tasks raises fixed costs of participation, which is more challenging for mid-sized players that lack diversified revenue bases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Secured Lending Anchors Portfolios While Unsecured Cards Race Ahead

Loans captured 39.48% of the Brazil retail banking market share in 2025, as secured facilities and payroll assignment supported lower loss severity and predictable repayment flows. Credit cards, while smaller in base, are forecast to expand at a 12.21% CAGR through 2031 as instalment plans and revolving balances scale within digital channels in the Brazil retail banking market. Rising consumer use of real-time transfers funded checking balances that serve as liquidity pools for everyday payments and bill pay, broadening cross-sell into short-duration credit. Debit remains widely held and supports a pathway to contactless and mobile wallets, which reduces cash dependence as merchant acceptance densifies. Product bundling that ties payments, deposits, and savings into app-based experiences further improves engagement and monetization paths while maintaining lean distribution costs in the Brazil retail banking market.

Policy shifts reshaped the mix in 2025. Legislation expanded payroll-deducted eligibility and added collateral paths, which unlocked millions of originations at lower average rates than non-payroll personal loans and widened access in underserved segments in the Brazil retail banking industry. Vehicle financing grew, but standards loosened, including higher LTVs and older vehicles, which increases residual-value sensitivity in a cyclical downturn. Real estate lending slowed as financing costs rose, which weighed on affordability and new originations even as housing programs continued to support lower-income households. Rural credit delinquency rose to a time-series high in mid-2025 due to climate events and commodity volatility, highlighting exposure concentration risks in specific sub-portfolios. Across unsecured lines, credit-card debt service remained elevated and reflected persistent use of higher-cost revolving modalities that are sensitive to macro conditions in the Brazil retail banking market.

By Channel: Digital Rails Gain Share as Branches Shrink

Offline banking retained 56.52% of market value in 2025, while online banking is set to grow at a 14.19% CAGR through 2031 as smartphones and instant payments reduce the need for in-person interactions across the Brazil retail banking market. Real-time transactions scaled to billions monthly and accounted for over a quarter of retail payments by late 2025, a trend reinforced by lower merchant acceptance costs and seamless point-of-sale experiences. Weekly login rates and mobile engagement sustained the case for branch-light models as consumers adopted wallet features, bill pay, and QR or contactless payments at checkout. API traffic rose sharply and now supports account aggregation, payment initiation, and automated refinance journeys, which blur the lines between bank and non-bank channels in the Brazil retail banking market. Digital wallets and contactless methods advanced in 2025, further accelerating tap-to-pay adoption and reducing cash withdrawals through Pix Saque functionality.

Incumbents and challengers both optimized distributions. The central bank highlighted continued branch rationalization as a lever to lower cost to serve, which was reflected in improved efficiency at scale for leading banks in 2025. A major incumbent reported a second-quarter efficiency ratio in Brazil of 36.9% alongside rising technology investments, indicating cost discipline even as digital spending continues. Open finance will add credit portability in 2026, which will intensify competition as borrowers compare offers in-app and authorize bank switching with standardized data sharing. As alternative payments reduce fee pools linked to card acquiring and legacy services, institutions continue to reprice bundles and shift toward modular offerings that can be embedded into partner platforms in the Brazil retail banking market. The Brazil retail banking market size benefits from greater channel optionality, yet cost curves continue to favour digital-first distribution at scale.

By Customer Age Group: Millennials Dominate Balances, Gen Z Drives Growth

The 29–44 cohort held 42.61% of customer accounts in 2025, reflecting peak earning years and greater uptake of mortgages and credit cards in the Brazil retail banking market. The 18–28 segment is projected to grow faster at a 13.43% CAGR through 2031 as digital onboarding, open finance, and social-benefit deposits create early relationships that expand over time. Activity data show that consumers aged 20 to 39 drive a majority of transactions on instant-payment rails, which supports mobile-first acquisition strategies and cross-sell penetration across deposit, card, and instalment lines. A leading neobank’s youth-focused products gained industry recognition in 2025 for financial empowerment and literacy, indicating the importance of tailored experiences for younger users in the Brazil retail banking market. For older cohorts, payroll-deducted loans and pension-linked income dynamics anchor stable repayment profiles and deposit balances, which remain a core pillar even as digital channel usage rises.

Credit expansion patterns vary by income and age. Credit is accelerated for lower-income households that frequently use emergency modalities like overdrafts and revolving cards, which carry higher risk and are more sensitive to rate cycles. The central bank noted that emergency credit remained high into late 2025, which signals budget stress risks that can impact younger and lower-income borrowers in the Brazil retail banking market. A digital incumbent added more than a million active clients in Q3 2025, expanding its active base while maintaining stable NPLs through product and risk controls aligned with private payroll offerings. Privacy-by-design and consent-management standards under open finance, monitored by supervisors, support age-appropriate offers and responsible marketing across the Brazil retail banking market. Overall, demographic momentum remains a constructive tailwind as mobile engagement rises, and life-stage events trigger multi-product adoption.

By Bank Type: Incumbents Hold Assets, Neobanks Seize Growth

National banks held 64.75% of the Brazil retail banking market in 2025 and continued to post strong profitability at scale, with a top-5 cohort delivering aggregate quarterly profits above BRL 29 billion. Neobanks and other digital-first entrants are projected to grow at a 15.87% CAGR through 2031, supported by low-cost distribution, data-driven underwriting, and lighter physical infrastructure in the Brazil retail banking market. Digital banks’ ROE reached 19.1% by mid-2024, above the system average, reflecting maturing monetization models and improved cost control. A leading universal bank reported BRL 11.5 billion in recurring net income in Q2 2025 with improved efficiency, while a top digital player posted USD 3.7 billion in Q2 2025 revenue with sustained user activity. Regional lenders and cooperatives maintain niche strength in agricultural and SME credit, though climate and commodity cycles tested risk outcomes in 2025.

Strategic vectors continue to diverge. Incumbents rationalize branches, invest in technology, and refine product mixes toward secured and fee-based offerings under tighter capital and liquidity management in the Brazil retail banking industry. Challengers prioritize customer growth, AI-enhanced underwriting, and embedded finance through partnerships, while scaling international footprints where local regulatory approvals are advancing. Supervisory focus on conduct, climate risk, and operational resilience expands compliance workloads across the board, which raises fixed costs and favours players with robust governance. The balance of market power remains with large incumbents, yet the growth vector continues to favour digital-first models in the Brazil retail banking market. The Brazil retail banking market size is expected to benefit from both the scale of incumbents and the innovation pace of challengers as open finance deepens.

Geography Analysis

Regional usage of instant payments highlights asymmetries that inform distribution choices. The Southeast accounted for 42.8% of Pix transactions in 2025, reflecting the region’s concentration of financial headquarters, merchant density, and high-income urban clusters in the Brazil retail banking market. São Paulo alone generated 23.8% of Pix transactions, while Rio de Janeiro posted 8.8% and Minas Gerais 8.3%, mirroring their roles in commerce, energy, services, and mining. The Northeast contributed 26.6% of Pix activity, driven by mobile adoption among younger demographics and broad acceptance by small merchants, which reduced reliance on cash. The South captured 12.3% of Pix usage, with Paraná at 5.0% supported by manufacturing and export flows, a profile that informs banks’ treasury and SME propositions in the Brazil retail banking market. The North and Central-West posted smaller shares but showed steady growth linked to logistics corridors, agribusiness, and federal payroll concentrations that feed deposits and payment volumes.

Risk and growth conditions diverged by state in 2025. The central bank documented climate events that escalated rural delinquencies to a series high, with southern states facing acute stress that spilled over to banks with concentrated agribusiness exposures in the Brazil retail banking market. Biometric authentication for specific payroll-deducted loans initially reduced daily origination volumes but recovered as mobile processes were tuned, with faster normalization in metropolitan areas with stronger network infrastructure. Open finance infrastructure is on track to expand credit portability in 2026 nationwide, which will intensify competition in peri-urban and rural geographies that previously favoured lenders with proprietary customer data. Government export and ecommerce reports indicated rising adoption of digital and contactless methods by merchants of all sizes, which helps level the playing field for distribution beyond the major capitals. These patterns indicate that regional opportunity sets are widening even as risk drivers remain uneven across the Brazil retail banking market.

Capital-market access and policy support remain uneven across regions. External wholesale funding for EMDEs stayed costly into late 2025, which requires regional and mid-tier banks to build local deposit franchises or alternative funding channels when scaling outside the Southeast and South. Supervisory priorities on open finance, consumer protection, and operational resilience apply uniformly nationwide and support interoperability of products and experiences across geographies in the Brazil retail banking market. As Pix penetration deepens in the Northeast and North, and as open finance portability normalizes switching, banks will intensify localized offers for SMEs and households in growth corridors. Over the forecast period, the Brazil retail banking market size benefits from the broader geographic diffusion of real-time payments and data-driven credit, even as climate and commodity exposures continue to shape regional credit outcomes. These dynamics reinforce the need for region-specific risk models and omnichannel strategies calibrated to local infrastructure and customer behaviour.

Competitive Landscape

The Brazil retail banking market shows moderate concentration with sustained profitability among the largest incumbents and fast growth among digital-first challengers. The top five banks reported aggregate quarterly profits above BRL 29 billion in Q3 2025, underscoring durable earnings that fund technology and risk investments at scale. Itaú Unibanco posted BRL 11.5 billion in recurring net income in Q2 2025, supported by stronger service revenue, lower delinquency, and improved efficiency in Brazil operations, while the loan book reached BRL 1.4 trillion. On the challenger side, Nubank delivered record Q2 2025 revenue of USD 3.7 billion with high activity rates, while advancing regulatory applications that support expansion of deposit and lending capabilities beyond Brazil. These profiles frame the Brazil retail banking market where scale and speed can coexist under uniform supervisory standards.

Strategic moves in 2025 emphasized productivity and selective expansion. Incumbents continued branch rationalization and deepened technology spend to support digital channels, which improved efficiency ratios even as infrastructure investment remained high. Digital players focused on AI-driven underwriting, customer experience improvements, and payroll-linked credit features to expand portfolios while managing NPLs in a risk-aware manner. Supervisors expanded conduct and climate-risk reporting frameworks, which raised compliance workloads and favoured players with strong governance in the Brazil retail banking market. The result is a competitive field that rewards cost leadership, disciplined risk, and rapid product iteration.

The outlook balances earnings resilience with continued disruption. Open finance credit portability will intensify competition for balances and compress switching frictions, which challenges legacy pricing power but unlocks share gains for teams with superior onboarding and servicing journeys in the Brazil retail banking market. External wholesale conditions will likely remain a constraint for mid-tiers, steering strategies toward deposit-led growth and partnership-driven embedded finance. Macro policy remains restrictive to secure inflation convergence, which supports retail spreads but weighs on origination volumes and keeps credit discipline at the forefront. Over time, the combination of instant-payments scale and data-sharing under open finance sustains a wide innovation surface while elevating operational and compliance standards across the Brazil retail banking market.

Brazil Retail Banking Industry Leaders

Caixa Economica Federal

Banco do Brasil

Itau Unibanco Holding

Banco Bradesco

Santander Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nubank, a Brazilian digital financial services platform, plans to secure a full banking license in Brazil by 2026. This initiative, driven by Joint Resolution No. 17, aims to enhance its lending capacity, capital flexibility, and brand credibility. Valued at USD 85 billion, Nubank ensures uninterrupted services for its 110 million customers during compliance transitions.

- December 2025: Banco XP, in partnership with Wise and Visa, introduced the XP Global Account. This offering includes a multi-currency digital wallet and international debit card, targeting investor clients. It aims to enhance cross-border liquidity and global asset management, reflecting Banco XP's strategic move to diversify its product portfolio beyond traditional brokerage services.

- November 2025: Nubank acquired the Dex Labs team, renowned for its AI-powered data platform. This move strengthens Nubank’s AI capabilities, advancing its global financial services strategy. The Dex Labs team, led by its founders, joins Nubank on December 2, focusing on AI initiatives to enhance customer personalization, risk management, scalability, and operational efficiency.

- April 2025: Fiserv, Inc. announced the acquisition of Money Money Servicos Financeiros S.A., a Brazilian fintech. This acquisition strengthens Fiserv’s presence in Brazil, enabling SMBs to access capital through tailored financial solutions, integrating risk analysis and predictive insights, and advancing capital backed by future receivables to support business growth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Brazil retail banking market as all consumer-facing deposit, payment, and credit activities, transactional and savings accounts, debit and credit cards, personal loans, mortgages, and allied fee-based services delivered by licensed banks and regulated digital challengers to individuals across Brazil.

Scope Exclusions: Corporate lending, investment banking, private-wealth mandates, and insurance underwriting stay outside our boundary to avoid mixing enterprise risk and revenue pools.

Segmentation Overview

- By Product

- Transactional Accounts

- Savings Accounts

- Debit Cards

- Credit Cards

- Loans

- Other Products

- By Channel

- Online Banking

- Offline Banking

- By Customer Age Group

- 18-28 Years

- 29-44 Years

- 45-59 Years

- 60 Years and Above

- By Bank Type

- National Banks

- Regional Banks

- Neobanks & Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with branch managers of incumbent banks, product leads at neobanks, fintech association officers, and BCB supervisors across São Paulo, Rio, and Recife. Their insights clarified consumer churn rates, digital-onboarding costs, and planned footprint shifts, letting us stress-test secondary figures and refine model drivers.

Desk Research

We began with macro-financial data from the Central Bank of Brazil (BCB), the National Monetary Council, and IBGE household surveys, then added payment rails statistics such as Pix transaction dashboards, trade-body briefs from FEBRABAN, and regional press releases capturing branch closures and neobank account launches. Company filings, investor decks, and press statements supplied product volumes and pricing spreads. Select paid archives, Dow Jones Factiva for news runs and D&B Hoovers for balance-sheet line items, filled historic gaps. The sources cited are illustrative; many additional repositories informed our desk work.

Market-Sizing & Forecasting

A top-down construct starts from BCB data on outstanding retail deposits, loan books, and card spend, which are then segmented by product, channel, and age cohort. Results are cross-checked with bottom-up approximations derived from sampled bank reports and average service fees to validate totals before adjustments. Key variables like household disposable income, smartphone penetration, Selic policy rate, Pix share of payments, and branch density power a multivariate regression, while an ARIMA overlay smooths cyclical shocks. Where bank-level disclosures are partial, gaps are bridged using rolling three-year growth averages vetted during interviews.

Data Validation & Update Cycle

Outputs pass variance checks against historical trends and alternative industry ratios; anomalies trigger re-work rounds and senior review. Reports refresh once a year, with interim updates whenever policy moves or M&A materially shift the market. A final sweep just before publication ensures clients receive the freshest baseline.

Why Mordor's Brazil Retail Banking Baseline Proves Reliable

Published estimates often differ because firms define 'market value' in dissimilar ways and apply unique growth levers.

Key gap drivers include scope width (some tally only net interest income), treatment of one-off fee streams, currency conversions, and refresh cadence. Mordor's base year aligns with BCB fiscal cut-offs, and our dual-pass modelling balances regulatory tallies with sampled bank roll-ups, reducing both under- and over-counts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 146.6 B (2025) | Mordor Intelligence | - |

| USD 58.7 B (2024) | Global Consultancy A | Counts net interest income only, omits fees and interchange |

| USD 65 B (2024) | Industry Research Firm B | Uses listed-bank sample, then applies fixed uplift for unlisted cohort |

| USD 197.33 B (2024) | Forecast Publisher C | Adds gross transaction value to revenue, inflating baseline |

In sum, Mordor's disciplined scope, transparent driver set, and yearly audit furnish decision-makers with a balanced, repeatable baseline they can track against internal dashboards with confidence.

Key Questions Answered in the Report

What is the size and growth outlook for the Brazil retail banking market to 2031?

The Brazil retail banking market size is USD 158.67 billion in 2026 and is projected to reach USD 235.62 billion by 2031 at an 8.23% CAGR.

How is Pix changing customer behavior in Brazil retail banking?

Pix accounted for 26% of retail transactions by late 2025, reduced merchant costs, and enabled near-instant settlement, which increased account engagement and expanded cross-sell opportunities.

Which product lines are leading, and which are growing fastest within Brazil retail banking?

Loans led with 39.48% share in 2025, while credit cards are the fastest growing with a projected 12.21% CAGR through 2031.

What role is open finance playing in Brazil retail banking?

Open finance supports consent-based data sharing and payment initiation across tens of millions of accounts, which improves underwriting and lowers switching frictions as credit portability comes online in 2026.

How are incumbents and neobanks competing in Brazil's retail banking?

Incumbents are optimizing cost and investing in technology, while neobanks scale low-cost distribution and AI-enhanced underwriting, with digital banks achieving a 19.1% ROE by mid-2024.

Which regions show the highest activity in Brazil's retail banking payments?

The Southeast leads with 42.8% of Pix transactions, followed by the Northeast at 26.6%, with the South at 12.3%, reflecting differences in merchant density and income profiles.

Page last updated on: