Respiratory Virus Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

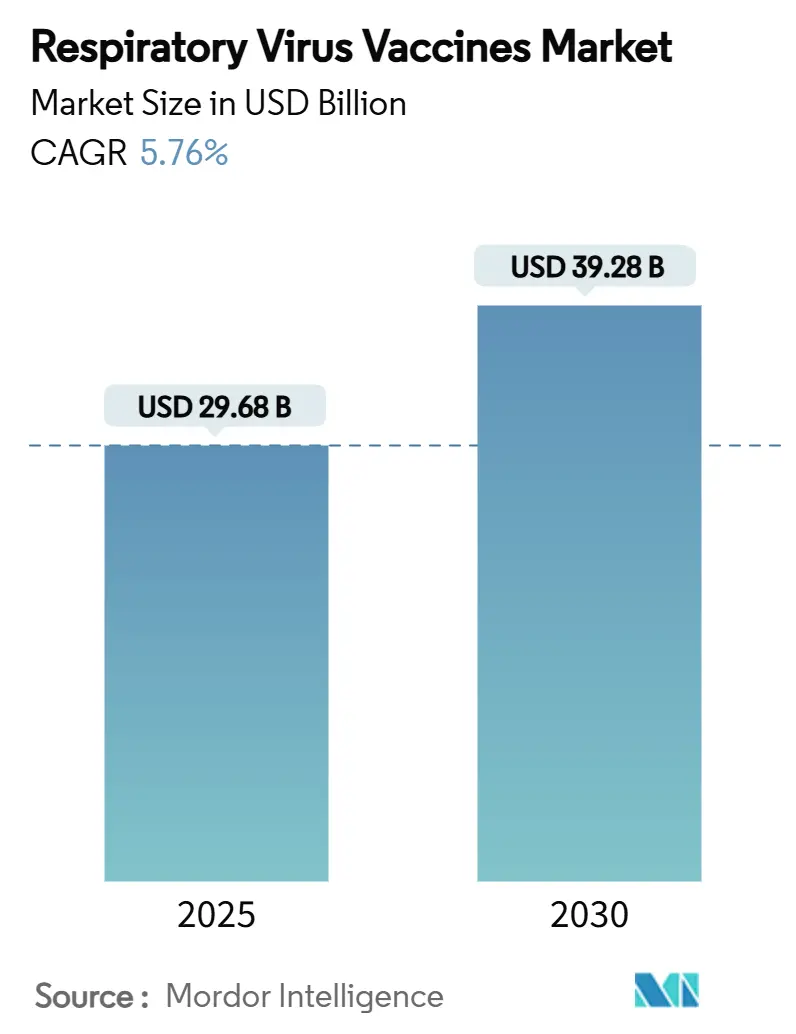

| Market Size (2025) | USD 29.68 Billion |

| Market Size (2030) | USD 39.28 Billion |

| Growth Rate (2025 - 2030) | 5.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Virus Vaccines Market Analysis by Mordor Intelligence

The respiratory virus vaccines market size reached USD 29.68 billion in 2025 and is forecast to climb to USD 39.28 billion by 2030, advancing at a 5.76% CAGR. This momentum stems from steady influenza demand, the commercial debut of respiratory syncytial virus (RSV) vaccines, and accelerating adoption of next-generation mRNA platforms. RSV vaccines are reshaping growth expectations as first-season uptake among US seniors exceeded forecasts and maternal programs secured global backing after World Health Organization (WHO) pre-qualification. Continuous influenza immunization campaigns retain their primacy, yet manufacturers are reallocating capital toward combination flu-COVID candidates that promise schedule simplification and stronger booster compliance. Rapid scale-up of flexible mRNA capacity in the United Kingdom, Australia, and Canada positions the platform to capture future strain-update cycles, while intranasal delivery technologies cultivate a new channel for self-administered products and mucosal immunity advantages. Regional asymmetry persists: North America commanded the highest 2024 revenue share, but Asia-Pacific is registering the fastest uptake, aided by China’s and Australia’s expedited approvals and sizeable public-sector tenders.

Key Report Takeaways

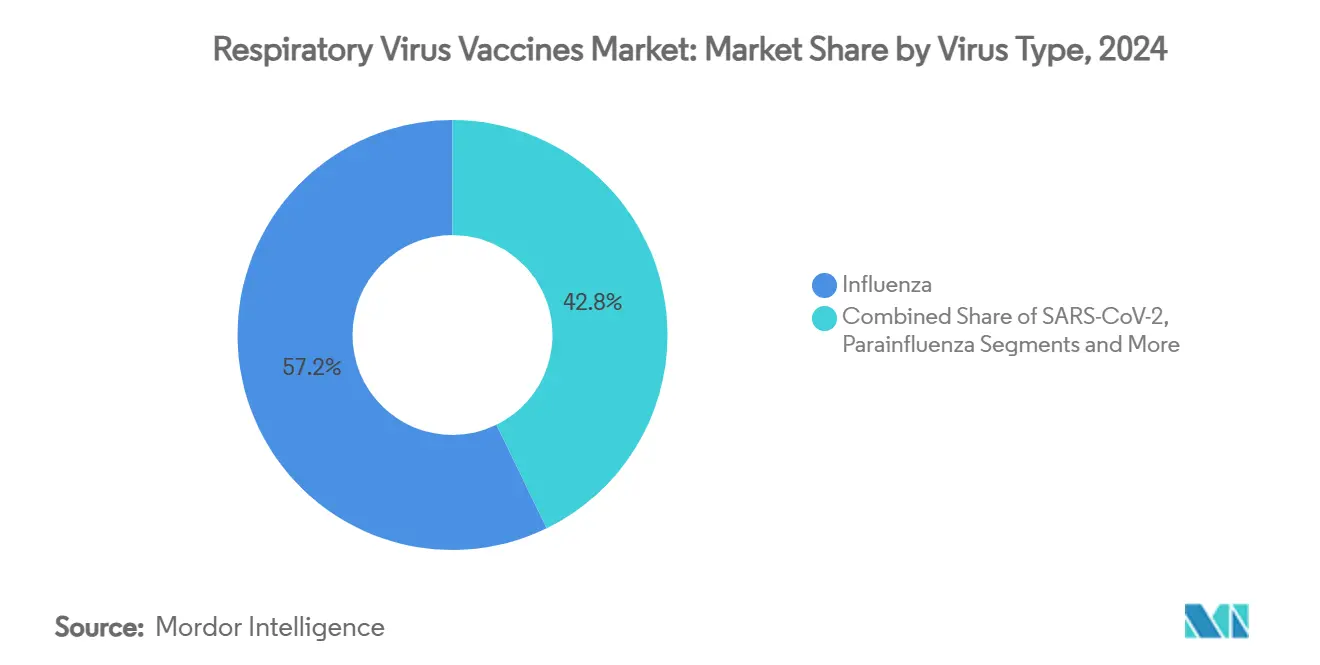

- By virus type, influenza vaccines led with 57.23% of respiratory virus vaccines market share in 2024; RSV vaccines are projected to expand at a 9.24% CAGR to 2030.

- By technology platform, egg-based inactivated products held 49.73% of the respiratory virus vaccines market size in 2024, while mRNA platforms are forecast to rise at an 8.34% CAGR to 2030.

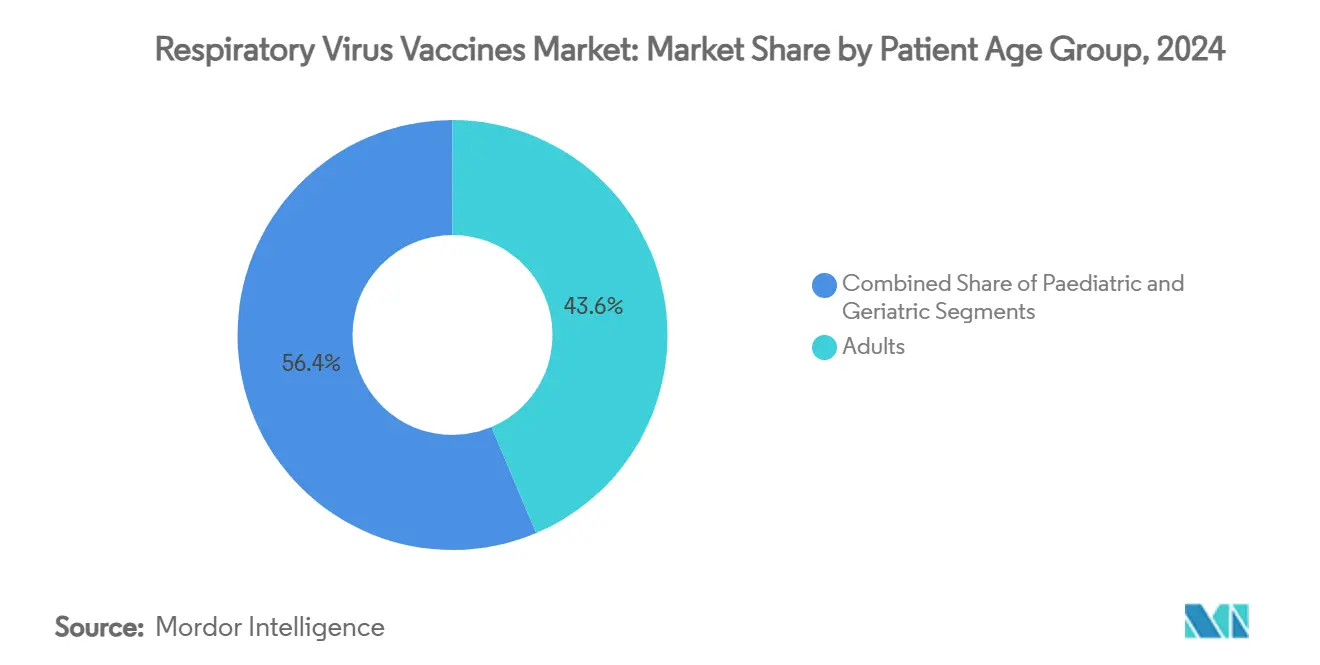

- By patient age group, adults accounted for 43.64% share of the respiratory virus vaccines market size in 2024, yet the geriatric cohort is advancing at a 7.28% CAGR through 2030.

- By route of administration, intramuscular products dominated with 86.13% of 2024 revenue, whereas intranasal vaccines are pacing ahead at a 9.52% CAGR to 2030.

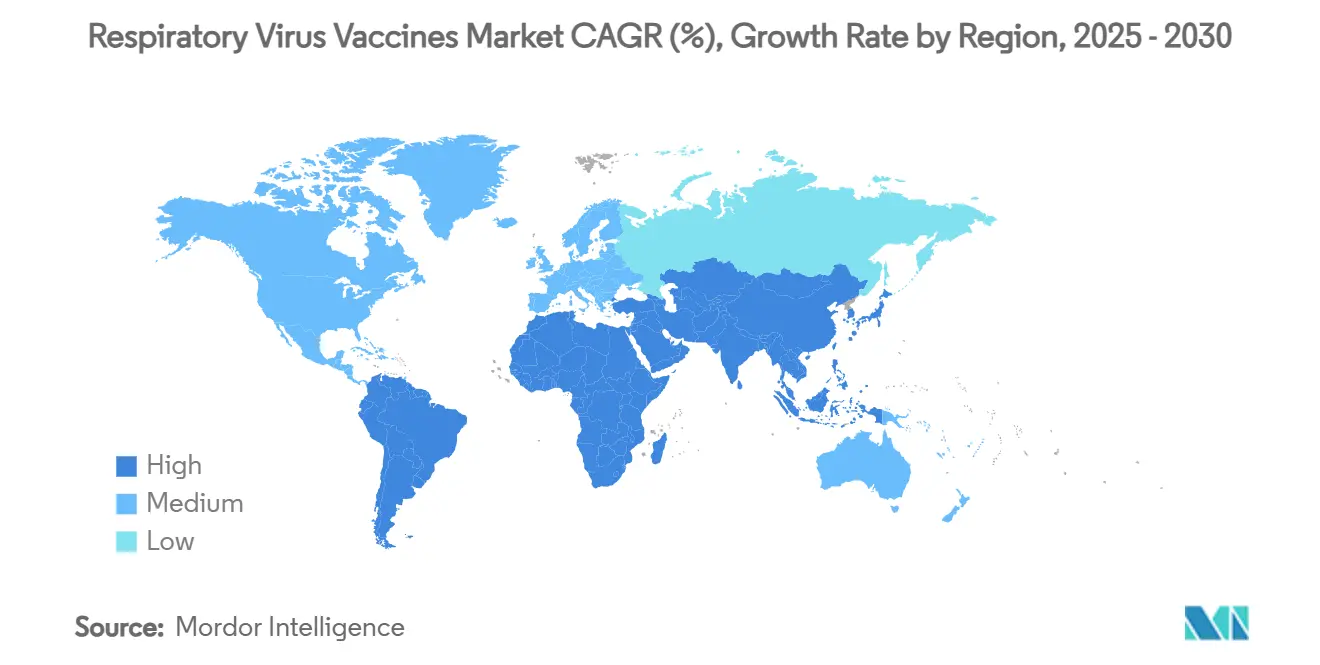

- By geography, North America possessed 36.28% of 2024 revenue; Asia-Pacific exhibits the highest projected CAGR at 7.36% to 2030.

Global Respiratory Virus Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous influenza immunization programmes & public-sector procurement | +1.2% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Commercial launch of RSV vaccines for seniors & maternal immunisation | +0.8% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Endemic COVID-19 boosters and forthcoming combination respiratory shots | +0.6% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Rapid scale-up of mRNA and other next-gen vaccine platforms | +0.5% | North America & Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Emergence of self-administered intranasal vaccines | +0.4% | Global, regulatory timelines vary | Long term (≥ 4 years) |

| Counter-season stock-piling in Southern Hemisphere markets | +0.3% | Australia & South America focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Continuous Influenza Immunization Programmes & Public-Sector Procurement

Annual influenza drives the baseline revenue that underwrites long-range manufacturing investments.[1]Centers for Disease Control and Prevention, “Influenza, COVID-19, and Respiratory Syncytial Virus Vaccination Coverage Among Adults — United States, Fall 2024,” CDC.gov US adult coverage rose from 32.6% in 2023 to 34.7% in 2024, highlighting untapped upside in mature economies. Public-sector forward purchases guarantee volume, enabling firms to redirect capital toward faster cell-based and mRNA processes. Government stock-piling in Australia and Chile smooths utilisation across counter-season demand windows, reducing idle capacity costs. Cell-based formulations post 12-14% higher effectiveness than egg-based peers, encouraging premium contracting despite higher unit costs.

Commercial Launch of RSV Vaccines for Seniors & Maternal Immunisation

Three approvals in 2024 unlocked a high-value category, though US guidelines narrowed routine use to adults 75+ or 60-74 at elevated risk, adding volume uncertainty. GSK’s Arexvy posted over 94% efficacy and generated GBP 1.2 billion in 2023 sales, seizing first-mover advantage. Maternal protection reached 66% of US infants by early 2025, yet only 32.6% of eligible pregnant women accepted vaccination, underscoring education gaps. WHO pre-qualification in March 2025 opens GAVI procurement, enabling accelerated entry in low-income regions. Manufacturers anticipate repeat-dose clarity and multivalent RSV-flu formulations to stabilise lifecycle revenue.

Endemic COVID-19 Boosters and Forthcoming Combination Respiratory Shots

Endemic COVID-19 has established a recurrent booster baseline, with 17.9% of US adults receiving the 2024-25 formulation. Moderna’s Phase 3 flu-COVID candidate yielded superior immune responses versus separate injections and predicted a 56% uplift in COVID-19 uptake among older adults. Sanofi and Novavax secured FDA Fast Track in December 2024 for two high-dose flu-COVID combinations aimed at adults 50+, signalling regulatory enthusiasm.[2]Sanofi Media Office, “Two Combination Vaccine Candidates Granted Fast Track Designation in the US,” Sanofi.com Japanese safety data supporting same-day dual administration sets a global precedent for broader schedule integration. Combination shots promise fewer clinic visits, lower payer outlays, and improved adherence.

Rapid Scale-Up of mRNA and Other Next-Gen Vaccine Platforms

Moderna inaugurated three mRNA plants across the UK, Australia, and Canada in 2025, cutting lead times and augmenting surge capacity. mRNA products offer rapid strain-switch agility and refrigerated stability that mitigate ultra-cold chain burdens. mRESVIA’s approval in Australia validated the modality beyond COVID-19, fostering confidence among regulators and payers. Cell-based lines post meaningful efficacy gains yet remain supply-constrained, while viral vector, DNA, and novel adjuvants diversify risk across pipelines. Patent filings on prefusion-stabilised antigens and lyophilised mRNA underline platform innovation intensity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain & ultra-cold logistics cost burden | -0.7% | Global, highest in low- and middle-income countries | Medium term (2-4 years) |

| Antigenic drift forcing frequent influenza reformulations | -0.5% | Global, seasonal variability | Short term (≤ 2 years) |

| Booster-fatigue & vaccine misinformation in high-income countries | -0.4% | North America & Europe | Medium term (2-4 years) |

| Sparse surveillance data for non-influenza viruses in low-income countries | -0.3% | Sub-Saharan Africa focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain & Ultra-Cold Logistics Cost Burden

Distribution expenses remain a binding constraint, especially where last-mile refrigeration is unreliable. Freeze-preventive cold boxes cut wastage by 40% in Nepal field studies.[3]Priya Sharma, “Freeze-Preventive Cold Boxes Reduce Vaccine Wastage in Nepal Field Study,” Nature.com mRNA stability upgrades ease yet do not eliminate the requirement for multi-point monitoring. Artificial-intelligence route optimisation software predicts equipment failure, but upfront capital is prohibitive for many donors. UAV-based temperature-controlled shipments unlock high-altitude access yet scale is nascent. Progress toward thermostable lyophilised platforms could neutralise this restraint longer term.

Antigenic Drift Forcing Frequent Influenza Reformulations

Rapid viral evolution compels semi-annual WHO strain selections, locking manufacturers into six-month production cycles that limit responsiveness. Drift-induced mismatches suppress vaccine effectiveness and erode public confidence. mRNA agility offers shorter lead times, but regulatory review windows still impose delays. Extra reformulation batches increase inventory costs and risk stock-outs if yields drop. Next-generation broadly neutralising antigens are in early development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Virus Type: RSV Acceleration Alters Legacy Mix

Influenza vaccines captured 57.23% of the respiratory virus vaccines market share in 2024, reflecting the depth of long-standing seasonal programs. RSV launches are shifting the landscape as the respiratory virus vaccines market size for this pathogen is projected to post a 9.24% CAGR to 2030, the fastest within the category. SARS-CoV-2 boosters carved out a steady niche after the pandemic peak, anchoring a recurring but smaller annual revenue stream. Human metapneumovirus accounted for 6.2% of positive respiratory tests in 2025 yet still lacks an approved shot, leaving a sizable white space. Parainfluenza and adenovirus remain underserved despite their documented disease burden.

Influenza’s dominance persists because global procurement cycles guarantee volume and fund manufacturing upkeep, but antigenic drift compels costly yearly reformulations. RSV demand is broadening through maternal and senior recommendations that heighten multi-dose lifetime potential. COVID-19 strain updates will likely fold into combination regimens that bundle flu and RSV, compressing clinic visits and enhancing convenience. Developers are monitoring hMPV outbreaks to justify accelerated trials, and early-stage virus-like particle candidates could leapfrog to clinical phases by 2027. Pipeline diversification across pathogens positions manufacturers to hedge exposure against shifting epidemiology.

By Technology Platform: mRNA Momentum Challenges Egg-Based Stronghold

Egg-based inactivated products held 49.73% of 2024 revenue, keeping the legacy process at the front of the respiratory virus vaccines market. The respiratory virus vaccines market size tied to mRNA is forecast to climb at an 8.34% CAGR as new UK, Australian, and Canadian plants come online in 2025. Cell-based alternatives deliver 12-14% higher effectiveness than egg-based lots, though bioreactor costs slow rapid scale-up. Recombinant protein subunit shots such as Arexvy validate commercial success outside influenza. Live-attenuated intranasal formulations maintain niche appeal among paediatric and needle-averse cohorts.

Egg-adaptation mutations that sometimes blunt effectiveness are nudging payers toward higher-priced next-gen options. mRNA’s strain-switch agility and refrigerated stability present a credible path to displace egg capacity over the forecast window. Cell-based lines will expand as contract manufacturers retrofit idle pandemic plants, reducing unit costs. Viral vector and DNA platforms offer thermostability advantages that could ease cold-chain constraints in emerging economies. A wider technology mix ultimately mitigates supply risk and sustains healthy rivalry within the respiratory virus vaccines industry.

By Patient Age Group: Seniors Propel Future Uptake

Adults aged 18-64 accounted for 43.64% of the respiratory virus vaccines market share in 2024, supported by workplace flu mandates and broad COVID-19 booster eligibility. The geriatric cohort is on track for a 7.28% CAGR, the quickest among age brackets, as RSV guidance now covers adults 75+ and those 60-74 with risk factors. Paediatric programs remain reliable thanks to school immunisation rules and rising maternal RSV coverage, which protected 66% of US infants by early-2025. Demographic ageing globally expands the addressable pool for high-dose and adjuvanted formulations.

Seniors benefit disproportionately from combination schedules that lower clinic visits and co-payment hurdles. Employers drive adult compliance through on-site campaigns that bundle flu and COVID-19 boosters in a single session. Paediatric uptake could jump once intranasal needle-free RSV options enter the market, improving adherence among anxious toddlers. Maternal vaccination is poised to widen as WHO pre-qualification unlocks donor funding in low-income countries. Collectively, differentiated age-specific products strengthen portfolio resilience across the respiratory virus vaccines industry.

By Route of Administration: Nasal Delivery Gains Traction

Intramuscular injections dominated with 86.13% of 2024 revenue, reflecting entrenched clinical workflows across the respiratory virus vaccines market. Intranasal candidates are projected to expand at a 9.52% CAGR through 2030 as self-administration and mucosal IgA benefits resonate with consumers. Subcutaneous delivery maintains modest share for select allergy-sensitive populations, while oral approaches remain limited by gastric-acid degradation.

The respiratory virus vaccines market size for intranasal formats should widen once additional approvals follow India’s iNCOVACC precedent. Self-dosing reduces staffing costs during peak seasons and can lift overall coverage among needle-phobic individuals. Microneedle patches under development could offer a hybrid pathway, pairing dermal delivery with room-temperature stability. Thermostable nasal gels would further erode cold-chain spending in remote geographies. As administration options diversify, manufacturers can segment offerings by setting, age, and convenience, enriching value across the respiratory virus vaccines market.

Geography Analysis

North America held 36.28% of 2024 revenue, buoyed by early RSV launches, robust procurement budgets, and high insurance coverage. US adult flu coverage reached 34.7% while COVID-19 booster uptake hit 17.9%, leaving meaningful headroom for expansion. FDA Fast Track designations for combination vaccines signal a regulatory environment conducive to innovation. Canada’s new mRNA facility augments domestic supply resilience. Mexico presents a cost-effectiveness case for maternal RSV programmes that could avert 15,768 hospitalisations annually.

Asia-Pacific is forecast to log a 7.36% CAGR through 2030, the highest globally. China endorsed nirsevimab in late 2023 and is streamlining labelling reviews to accelerate market access. Australia approved mRESVIA in March 2025, further legitimising mRNA RSV solutions. India’s BioE3 policy nurtures domestic production, while intranasal R&D illustrates local innovation capacity. Japan’s simultaneous COVID-flu administration precedent is likely to spread across the region, fostering acceptance of multivalent scheduling.

Europe commands significant volume through mature reimbursement systems, yet heterogenous national policies add market entry complexity. The European Medicines Agency recommended expanding Arexvy to adults 50-59 at risk, broadening the addressable population. Central and Eastern Europe lag in adult booster rates, offering upside for outreach campaigns. Middle East and Africa show large unmet needs, where WHO pre-qualification can unlock donor funding for maternal RSV shots. South America benefits from local fill-finish capabilities and is trialling subsidised pricing models to scale uptake among low-income groups.

Competitive Landscape

The respiratory virus vaccines market exhibits moderate concentration. Five leading firms capture a sizeable share through deep pipelines and global manufacturing footprints, yet the entry of agile biotechnology innovators tempers monopolistic tendencies. Sanofi’s USD 1.6 billion Vicebio acquisition in July 2025 expanded its multivalent pipeline and demonstrated a strategic pivot toward next-generation platforms. The concurrent USD 500 million Sanofi–Novavax partnership seeks to commercialise flu-COVID combinations, illustrating cross-platform synergies.

GSK leads the RSV field: Arexvy recorded GBP 1.2 billion 2023 sales and captured roughly two-thirds of US retail doses in the launch season, reinforcing first-mover moat advantages. Moderna has parlayed COVID-19 windfalls into respiratory diversification, advancing mRNA RSV, flu, and combo regimens while constructing manufacturing hubs across three continents. Novavax is leveraging protein nanoparticle know-how to differentiate its combination candidate now in Phase 3.

White-space opportunities persist in hMPV and parainfluenza where no licensed vaccines exist, drawing venture investment toward virus-like particle and AI-guided antigen design. Delivery innovation remains a battleground: firms compete on intranasal devices, microneedle patches, and thermostable formulations that promise distribution cost savings. Patent activity centres on prefusion-stabilised antigens and lyophilised mRNA, signalling an arms race for platform defensibility.

Respiratory Virus Vaccines Industry Leaders

GlaxoSmithKline plc

Sanofi SA

CSL Seqirus

Pfizer Inc.

Moderna, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sanofi finalised the USD 1.6 billion acquisition of Vicebio, adding multivalent respiratory candidates to its pipeline.

- March 2025: WHO pre-qualified the first maternal RSV vaccine, ABRYSVO, enabling GAVI procurement for low-income markets.

- March 2025: Australia authorised Moderna’s mRESVIA for adults 60+ years, the first mRNA RSV approval outside the United States.

Global Respiratory Virus Vaccines Market Report Scope

| Influenza |

| Respiratory Syncytial Virus (RSV) |

| SARS-CoV-2 |

| Parainfluenza |

| Human Metapneumovirus |

| Adenovirus & Others |

| Egg-based Inactivated |

| Cell-based Inactivated |

| Live-attenuated |

| Recombinant Protein Subunit |

| mRNA |

| Viral Vector |

| DNA & Other Novel Platforms |

| Paediatric (0-17 yrs) |

| Adult (18-64 yrs) |

| Geriatric (≥65 yrs) |

| Intramuscular |

| Subcutaneous |

| Intranasal (mucosal) |

| Oral |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Virus Type | Influenza | |

| Respiratory Syncytial Virus (RSV) | ||

| SARS-CoV-2 | ||

| Parainfluenza | ||

| Human Metapneumovirus | ||

| Adenovirus & Others | ||

| By Technology Platform | Egg-based Inactivated | |

| Cell-based Inactivated | ||

| Live-attenuated | ||

| Recombinant Protein Subunit | ||

| mRNA | ||

| Viral Vector | ||

| DNA & Other Novel Platforms | ||

| By Patient Age Group | Paediatric (0-17 yrs) | |

| Adult (18-64 yrs) | ||

| Geriatric (≥65 yrs) | ||

| By Route of Administration | Intramuscular | |

| Subcutaneous | ||

| Intranasal (mucosal) | ||

| Oral | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is demand rising for combined flu-COVID boosters?

Phase 3 data suggest the candidate could increase COVID-19 booster uptake by 56% among adults aged 50+ and drive a 0.6% contribution to the forecast CAGR.

Which virus category is growing the quickest?

RSV vaccines post a 9.24% CAGR through 2030, the highest across all pathogen segments because of new senior and maternal indications.

Why are intranasal vaccines gaining traction?

They induce mucosal immunity, enable self-administration, and are forecast to grow at 9.52% CAGR, outpacing traditional injections.

What keeps egg-based vaccines dominant despite newer platforms?

Legacy infrastructure, lower regulatory complexity, and a 49.73% 2024 revenue share sustain the platform even as mRNA gains ground.

Where is the fastest regional growth occurring?

Asia-Pacific registers the highest regional CAGR at 7.36% to 2030, supported by rapid approvals in China and Australia and expanding middle-class demand.

What limits vaccine uptake in high-income countries?

Booster fatigue and misinformation suppress coverage; nursing-home COVID-19 uptake sat at 30% despite broad access, reducing overall volume potential.

Page last updated on: