Human Respiratory Syncytial Virus Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

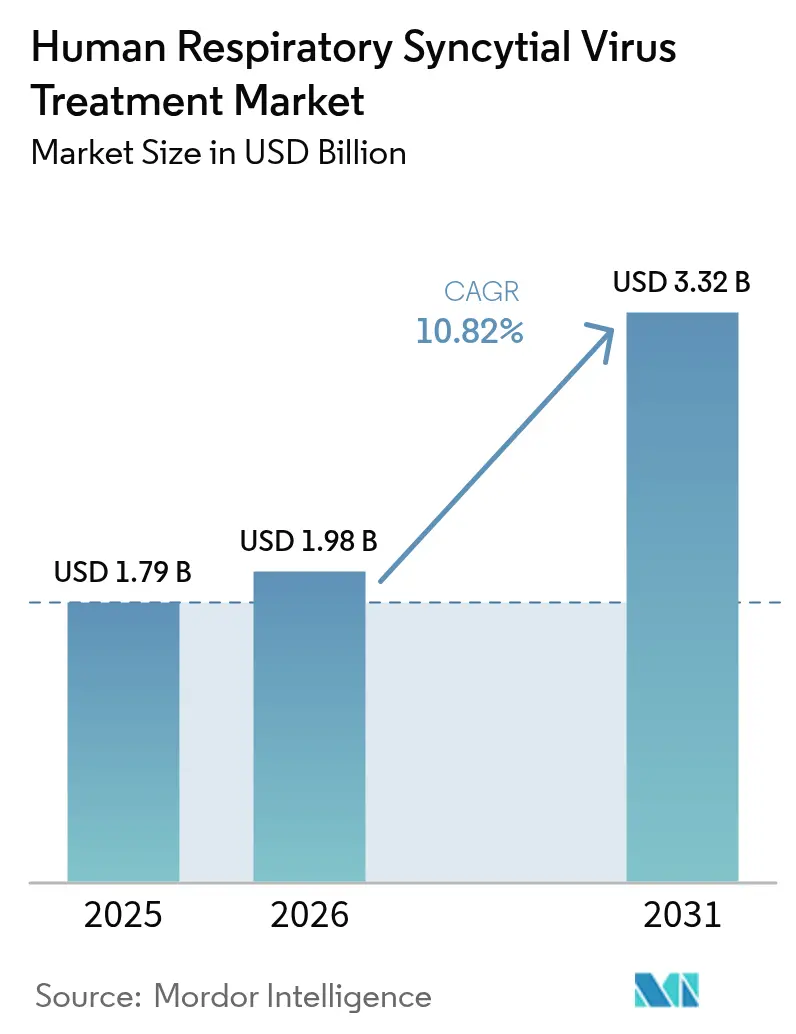

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 10.82% CAGR |

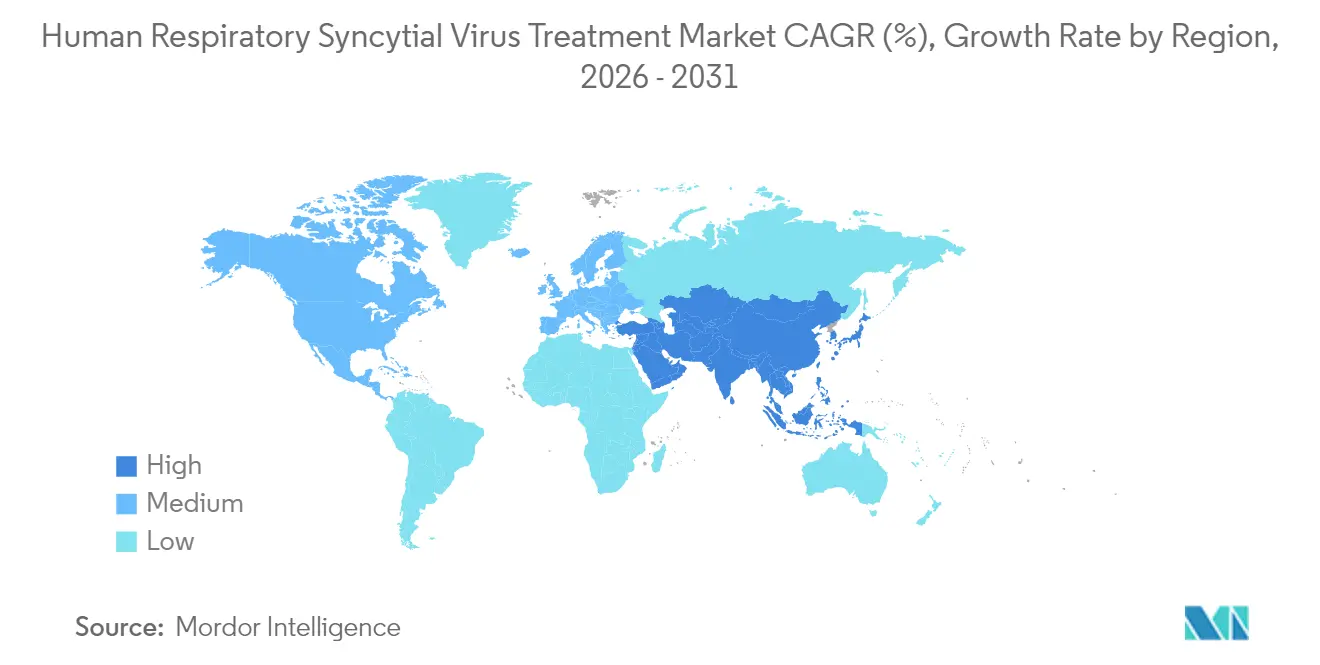

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Respiratory Syncytial Virus Treatment Market Analysis by Mordor Intelligence

The Human Respiratory Syncytial Virus Treatment market size in 2026 is estimated at USD 1.98 billion, growing from 2025 value of USD 1.79 billion with 2031 projections showing USD 3.32 billion, growing at 10.82% CAGR over 2026-2031. Persistent post-pandemic surges in RSV cases, the commercial rollout of three adult vaccines, and sharply rising infant immunoprophylaxis coverage are expanding addressable volumes across high- and middle-income countries. Long-acting monoclonal antibodies are cementing a preventive care paradigm that is reshaping formulary priorities, while accelerated mRNA and small-molecule programs are stretching the innovation cycle beyond traditional fusion inhibitors. Manufacturers are scaling flexible capacity, because seasonal demand swings remain difficult to forecast in a market that is becoming geographically diversified. Competition is intensifying as large vaccine players jockey for public-payer contracts and mid-size biotechs leverage targeted licensing deals to retain optionality for late-stage out-licensing.

Key Report Takeaways

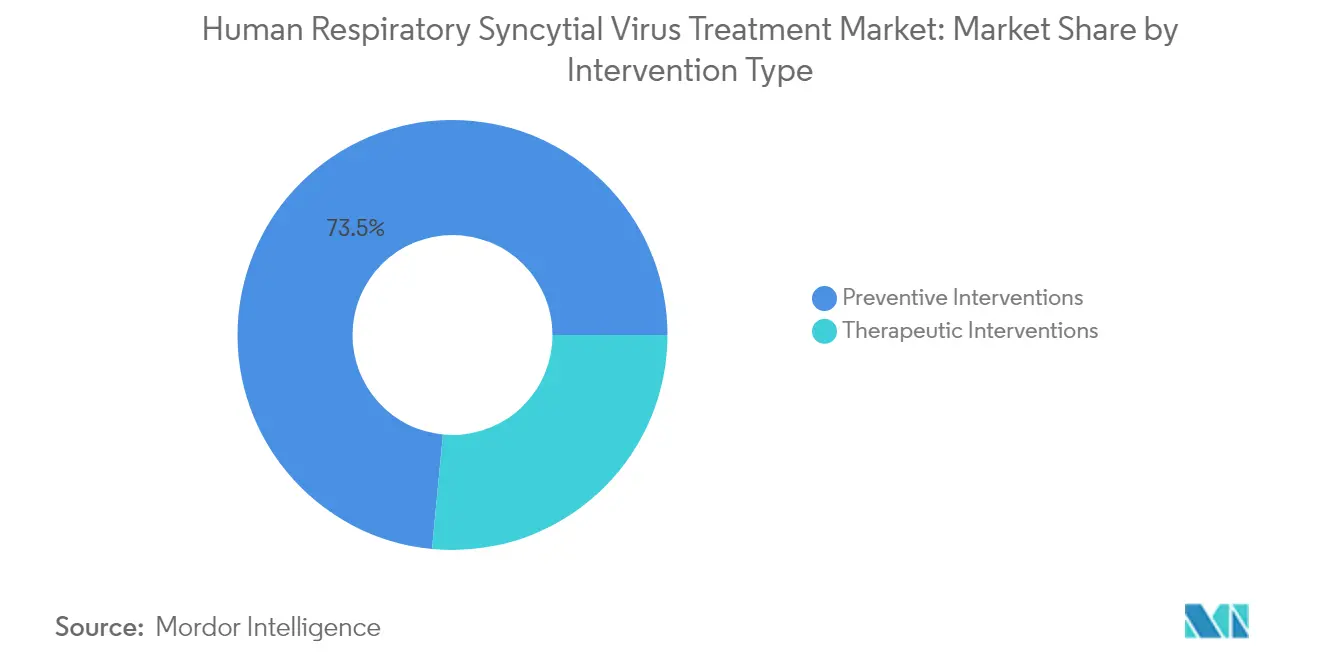

- By intervention type, monoclonal antibody prophylaxis led with 43.98% Human Respiratory Syncytial Virus Treatment market share in 2025, whereas vaccines are expected to post the fastest 11.93% CAGR to 2031.

- By route of administration, injectable products commanded 78.04% of the Human Respiratory Syncytial Virus Treatment market size in 2025; oral antivirals are projected to expand at 12.41% CAGR over 2026-2031.

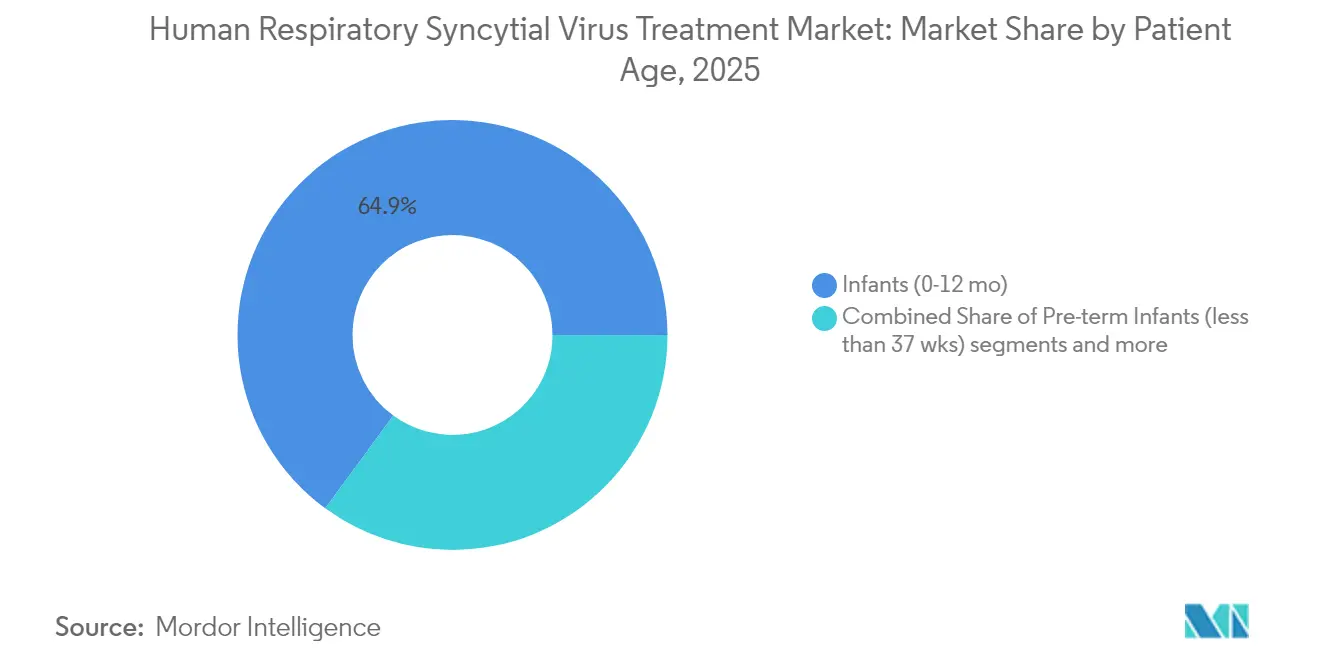

- By patient type, infants <1 year accounted for 64.92% of total revenue in 2025, while the ≥60-year cohort will grow the fastest at a 13.56% CAGR through 2031.

- By geography, North America captured 39.12% revenue in 2025; Asia-Pacific is poised to record an 11.58% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Respiratory Syncytial Virus Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Global Adoption of Long-Acting Monoclonal Antibody Prophylaxis | +4.9% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Rising Hospitalizations of Adults ≥60 Years Triggering Rapid Vaccine Uptake | +2.8% | North America, Europe, Japan | Short term (≤ 2 years) |

| National Infant Immunization Programs in Emerging Economies | +1.5% | Asia-Pacific, Latin America, Middle East | Medium term (2-4 years) |

| Increasing Venture-Capital Flow into Oral Antiviral Therapeutics Boosting Pipeline Breadth | +1.2% | Global, with initial impact in North America | Long term (≥ 4 years) |

| WHO Pre-qualification Pathway for Maternal RSV Vaccines | +0.6% | Global, with emphasis on LMICs | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Surge in Global Adoption of Long-Acting Monoclonal Antibody Prophylaxis

Nirsevimab is providing full-season protection with one injection and showed roughly 70-80% efficacy against medically attended RSV disease in pivotal trials. Supply expansion agreements approved in 2024 ensured wider availability for the 2024-2025 season, improving payer confidence and supporting faster guideline integration. Reimbursement frameworks in the United States and Europe are mitigating the high per-dose cost, enabling hospital systems to shift preventive budgets from palivizumab to longer-acting platforms. Market analytics indicate that each 10-percentage-point gain in eligible infant coverage translates to almost USD 150 million of incremental annual revenue. The clear clinical-economic value is expected to keep the Human Respiratory Syncytial Virus Treatment market in a premium pricing corridor over the medium term.

Rising Hospitalizations of Adults ≥ 60 Years Triggering Rapid Vaccine Uptake

CDC surveillance confirmed 60,000-160,000 hospitalizations and up to 10,000 deaths annually among U.S. seniors, catalyzing payer alignment behind routine RSV vaccination for higher-risk older adults[1]Source: Centers for Disease Control and Prevention, “RSV Vaccine Guidance,” cdc.gov . Three licensed vaccines now cover this cohort, each demonstrating more than 67% efficacy against lower respiratory tract disease. First-season real-world evidence recorded about 75% effectiveness in preventing hospitalization, reinforcing the decision to reimburse a one-dose schedule. Public–private procurement consortia in Germany and Japan are mirroring U.S. coverage, further widening the Human Respiratory Syncytial Virus Treatment market footprint among seniors. Uptake momentum is therefore adding roughly 2.8% to the overall CAGR forecast through mid-decade.

National Infant Immunization Programs in Emerging Economies

Pilot roll-outs in Australia and Brazil have validated delivery models that blend maternal vaccination at 32-36 weeks’ gestation with post-natal monoclonal antibody campaigns[2]Source: Western Australia Department of Health, “Abrysvo and Beyfortus Implementation,” health.wa.gov.au . Governments in India and Indonesia are drafting similar guidelines, supported by Gavi financing and the WHO’s global market study, which encourages pooled procurement. High birth cohorts in South and Southeast Asia accelerate volume ramp-up once policy decisions are finalized. As a result, the Human Respiratory Syncytial Virus Treatment market is benefiting from policy-driven demand rather than purely discretionary spending, lifting the medium-term growth trajectory by 1.5%.

Increasing Venture-Capital Flow into Oral Antiviral Therapeutics Boosting Pipeline Breadth

Deal activity exceeded USD 900 million in disclosed transactions during 2024, underpinning multiple Phase 2 trials for next-generation N- and L-protein inhibitors. Oral delivery promises at-home treatment and better adherence, attributes valued by payers seeking to limit hospital admissions among adults with comorbidities. Early human-challenge data from S-337395 and zelicapavir showed viral load reductions approaching 90%, strengthening investor conviction. These programs broaden competitive dynamics by attracting non-vaccine specialists, ensuring the Human Respiratory Syncytial Virus Treatment market retains an innovation funnel extending beyond large‐cap pharma.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antiviral Resistance Concerns Around Ribavirin Reducing Physician Confidence | -0.8% | Global, with higher impact in regions with extensive ribavirin use | Medium term (2-4 years) |

| Seasonal Demand Volatility Complicating Capacity Planning for Manufacturers | -1.2% | Global, with varying impact based on regional RSV seasonality | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Antiviral Resistance Concerns Around Ribavirin Reducing Physician Confidence

Emerging ribavirin-resistant RSV strains erode clinician trust in the molecule and, by extension, cast uncertainty over the broader field of antiviral therapy. Although ribavirin is now restricted mainly to immunocompromised patients, sporadic resistance reports can influence prescribing attitudes toward new small-molecule candidates. Consequently, developers must demonstrate robust resistance-barrier profiles in clinical dossiers, slightly delaying adoption curves. The drag on overall growth is currently estimated at 0.8%, a modest but noteworthy headwind as the Human Respiratory Syncytial Virus Treatment market moves toward diversified treatment modalities.

Seasonal Demand Volatility Complicating Capacity Planning for Manufacturers

RSV epidemics shifted out of their traditional winter windows during the COVID-19 pandemic, whipping manufacturer forecasts and creating stockouts for Beyfortus in late 2023. Firms are investing in dual-use fill–finish lines and modular cold-chain storage, but production still peaks well before demand becomes visible. Over-ordering risks inventory write-offs, while under-ordering jeopardizes public health goals and erodes brand equity. Until predictive modeling improves, capacity planning challenges are expected to shave 1.2% from the Human Respiratory Syncytial Virus Treatment market CAGR in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Intervention Type: Preventive Strategies Outpace Therapeutic Options

Monoclonal antibody prophylaxis accounted for 43.98% of 2025 revenue, confirming a decisive market pivot toward prevention and providing the single largest revenue base within the Human Respiratory Syncytial Virus Treatment market. Nirsevimab’s once-per-season schedule has been rapidly embedded in pediatric guidelines, while Merck’s investigational clesrovimab could intensify rivalry if approved in 2025. Adult vaccines, although newer, are registering the steepest expansion as payers integrate them into influenza-style procurement frameworks. The vaccines’ collective 11.93% CAGR is forecast to close the revenue gap with antibodies by 2031, demonstrating how the Human Respiratory Syncytial Virus Treatment market is diversifying product modalities without cannibalizing existing franchises.

Therapeutics such as oral antivirals remain a smaller slice but benefit from sustained venture capital, yielding a pipeline of fusion and polymerase inhibitors aimed at ambulatory care. Zelicapavir’s Day-5 viral load drop of 1.4 log against placebo indicates that such agents could address high-risk adult populations in whom vaccines underperform. As these treatments transition to late-stage trials, supportive health-technology assessments will be pivotal. Consequently, competitive positioning now hinges on demonstrating population-specific benefit rather than promising blanket efficacy, shaping future valuation benchmarks across the Human Respiratory Syncytial Virus Treatment market.

By Route of Administration: Injectable Dominance Challenged by Oral Innovation

Injectables delivered 78.04% of 2025 sales and retain logistical advantages in babies and long-term care settings, where single-shot protection simplifies adherence. Prefilled-syringe presentations and combination vaccine workstreams further entrench intramuscular delivery for mass campaigns. Nonetheless, oral antivirals are forecast to gain share at 12.41% CAGR, encouraged by payer preference for outpatient options that limit hospital days and infusion chair-time. This growth illustrates how dose-form-driven convenience can reallocate revenue pools within the Human Respiratory Syncytial Virus Treatment market size for high-risk adults and immunocompromised groups.

Intranasal and inhaled formulations remain exploratory but could complement systemic immunity by boosting mucosal defenses, an attribute attractive for both prophylaxis and rapid post-exposure prophylaxis. Academic consortia have reported promising RSV F-protein stabilization approaches that could underpin future needle-free candidates. If efficacy thresholds are met, such modalities could elbow into school-aged and adolescent segments currently underserved, adding fresh volume streams to the Human Respiratory Syncytial Virus Treatment market.

By Patient Age: Pediatric Focus Expands to Include Older Adults

Infants under 1 year generated 64.92% of 2025 revenue, a reflection of universally endorsed preventive schedules that prioritize this high-burden group. Post-launch epidemiology shows hospitalization rates falling 28-43% in the first northern-hemisphere season of widespread nirsevimab use, validating payer investment. The Human Respiratory Syncytial Virus Treatment market size for the pediatric cohort should remain sizable because global births exceed 130 million annually, yet growth is moderating as coverage saturates in high-income countries.

Adults aged ≥60 are the fastest-growing group, guided by clear morbidity data and new vaccine options. Hospitalization burden rivals influenza, and cost-effectiveness analyses support systematic vaccination for individuals 75 years and older. Uptake in the 60-74 bracket is climbing as ACIP broadens recommendations, enabling risk-stratified coverage and unlocking payer confidence. Emerging regulatory filings target adults aged 18-59 with comorbidities, implying that the Human Respiratory Syncytial Virus Treatment market will gradually embrace a life-course prevention paradigm.

Geography Analysis

North America contributed 39.12% of global revenue in 2025, supported by robust reimbursement, high disease awareness, and rapid codification of vaccine and antibody guidelines. The United States alone dispensed more than 4 million monoclonal antibody doses in the 2024-2025 season, yet coverage remains uneven, with just 22.2% of eligible seniors vaccinated by March 2025. Canada is evaluating a national vaccination program for adults ≥60 years, which could add roughly USD 120 million annual opportunity to the regional Human Respiratory Syncytial Virus Treatment market.

Europe holds the second-largest share, but adoption varies widely between member states. Germany’s endorsement of immunization for people ≥60 years under the statutory insurance scheme is accelerating procurement, while southern European countries still rely on individual physician judgment. EMA approvals for multiple vaccine and antibody options create a harmonized regulatory baseline, yet divergent health-technology assessments shape localized market access. Reimbursement parity efforts spearheaded by the European Commission may improve cross-border equity and lift the Human Respiratory Syncytial Virus Treatment market share in underpenetrated markets.

Asia-Pacific is the fastest-growing region, posting an 11.58% CAGR on the back of rising healthcare expenditure, demographic heft, and trial leadership in RSV prophylactics. Japan’s older-adult vaccine coverage exceeded 40% in its inaugural season, reflecting high consumer responsiveness to physician recommendation. China’s public health agencies are assessing domestic antibody and vaccine candidates, which could unlock multi-billion-dollar volume once national drug reimbursement negotiations conclude. Meanwhile, India and Indonesia prioritize maternal immunization frameworks supported by Gavi, indicating that payer-mix expansion will further extend the Human Respiratory Syncytial Virus Treatment market footprint.

South America and the Middle East & Africa together represent less than 10% of 2025 revenue, but disease burden suggests latent demand. Brazil set aside federal funding for maternal immunization in the 2025 budget cycle, while Gulf Cooperation Council states have initiated tender processes for senior-adult vaccination. Access barriers, including cold-chain infrastructure and budget constraints, hamper immediate uptake, but the WHO pre-qualification pathway and tiered-pricing commitments could hasten inflection points across these emerging Human Respiratory Syncytial Virus Treatment market frontiers.

Competitive Landscape

The Human Respiratory Syncytial Virus Treatment market is moderately concentrated, with the top five suppliers generating significant revenue of 2024. AstraZeneca and Sanofi dominate the monoclonal antibody segment through their co-marketed Beyfortus, whose Q4 2024 revenue hit USD 161 million after capacity constraints eased. GSK and Pfizer occupy leading vaccine positions, each leveraging deep seasonal-influenza infrastructures to streamline commercial roll-outs, whereas Moderna is leveraging mRNA expertise to capture incremental adult share following its 2024 approval.

Strategic acquisitions are reshaping portfolios: AstraZeneca’s USD 1.1 billion purchase of Icosavax secures a dual-pathogen candidate targeting RSV and hMPV, potentially unlocking combination-vaccine premiums. Pfizer’s earlier ReViral deal fortified its antiviral pipeline with sisunatovir, offering diversification beyond vaccines. Partnerships remain favored for regional scalability; for instance, GSK inked supply agreements with the Serum Institute of India to accelerate penetration once Indian regulators approve adult vaccination.

Disruption risk stems from smaller biotechs pushing differentiated modalities. Shionogi’s oral L-protein inhibitor S-337395 and Enanta’s N-protein inhibitor zelicapavir both received FDA Fast Track status, highlighting regulatory appetite for novel treatments. Competitive moats will likely hinge on clinical differentiation in specific patient subgroups, manufacturing agility to handle seasonal surges, and the ability to negotiate value-based contracts. Consequently, companies that deliver multi-virus combination products or cost-effective biosimilar antibodies could reset competitive baselines across the Human Respiratory Syncytial Virus Treatment market.

Human Respiratory Syncytial Virus Treatment Industry Leaders

AbbVie Inc

Merck & Co

AstraZeneca

GSK plc

Bausch Health Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: WHO prequalified Pfizer’s ABRYSVO® maternal vaccine, enabling Gavi financing for LMIC roll-outs

- December 2024: FDA accepted Merck’s BLA for clesrovimab, with decision expected by July 2025.

Global Human Respiratory Syncytial Virus Treatment Market Report Scope

As per the scope of the report, respiratory syncytial virus, or RSV, is a common respiratory virus that usually causes mild, cold-like symptoms. Most people recover in a week or two, but RSV can be serious, especially for infants and older adults. The Human Respiratory Syncytial Virus Treatment Market is Segmented by Route of Administration (Oral, Parenteral), Treatment Type (Supportive Care, Hospital Care), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across the major regions globally. The report offers the value (in USD million) for all the above segments.

| Preventive Interventions | Monoclonal Antibody Prophylaxis |

| Vaccines | |

| Therapeutic Interventions | Antiviral Drugs |

| Immunomodulators | |

| Supportive Care |

| Injectable |

| Oral |

| Inhaled |

| Intranasal |

| Preterm Infants (<37 wks) |

| Infants (0-12 mo) |

| Children (1-5 yr) |

| Adults (18-59 yr) |

| Older Adults (≥60 yr) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Intervention Type | Preventive Interventions | Monoclonal Antibody Prophylaxis |

| Vaccines | ||

| Therapeutic Interventions | Antiviral Drugs | |

| Immunomodulators | ||

| Supportive Care | ||

| By Route of Administration | Injectable | |

| Oral | ||

| Inhaled | ||

| Intranasal | ||

| By Patient Age | Preterm Infants (<37 wks) | |

| Infants (0-12 mo) | ||

| Children (1-5 yr) | ||

| Adults (18-59 yr) | ||

| Older Adults (≥60 yr) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Human Respiratory Syncytial Virus Treatment market?

The Human Respiratory Syncytial Virus Treatment market size is valued at USD 1.98 billion in 2026 and is projected to reach USD 3.32 billion by 2031, advancing at an 10.82% CAGR.

Why are monoclonal antibodies gaining traction over traditional antivirals?

Long-acting antibodies such as nirsevimab provide single-dose, season-long protection and have shown 70-80% efficacy in clinical settings, supporting rapid adoption and guideline inclusion.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to expand at 11.58% CAGR, propelled by rising healthcare expenditure, large birth cohorts, and increasing adult vaccination initiatives.

What are the primary barriers to broader global adoption of RSV vaccines?

Seasonal demand volatility, cold-chain constraints, and affordability challenges in low- and middle-income countries can delay deployment despite WHO pre-qualification efforts.

Page last updated on: