Dengue Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

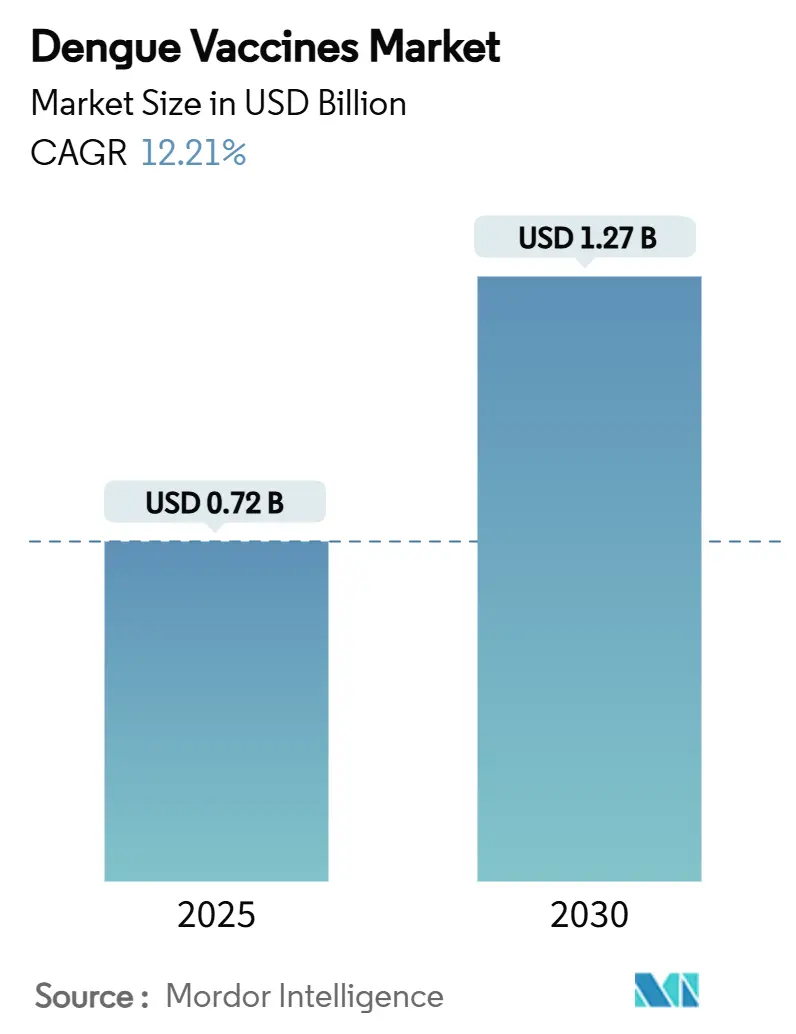

| Market Size (2025) | USD 0.72 Billion |

| Market Size (2030) | USD 1.27 Billion |

| Growth Rate (2025 - 2030) | 12.21% CAGR |

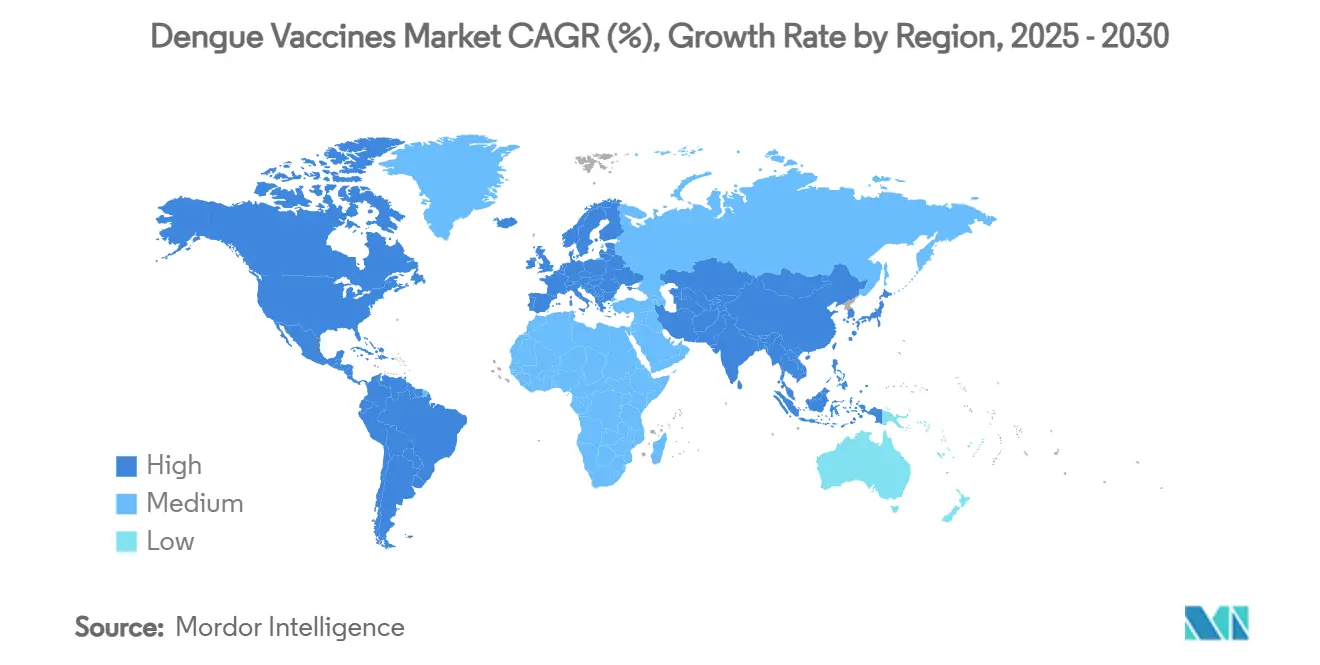

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dengue Vaccines Market Analysis by Mordor Intelligence

The dengue vaccines market size reached USD 0.717 billion in 2025 and is on course to attain USD 1.27 billion by 2030, reflecting a 12.21% CAGR over 2025-2030. Escalating incidence—12.3 million confirmed cases in 2024 alone—fuels public-sector demand, while climate change broadens Aedes mosquito habitats into temperate regions, creating fresh endemic zones. Rapid regulatory clearances, notably WHO prequalification of Takeda’s Qdenga, compress national roll-out timelines and unlock pooled procurement channels through UNICEF and PAHO.[1]World Health Organization, “WHO prequalifies new dengue vaccine,” WHO.intGovernments in Brazil, Indonesia and Thailand embed vaccination into routine childhood schedules, catalysing sustained volumes. Pharmaceutical strategies revolve around single-dose formulations and mRNA or DNA platforms designed to curb antibody-dependent enhancement, reduce cold-chain stress and accelerate serotype updates.

Key Report Takeaways

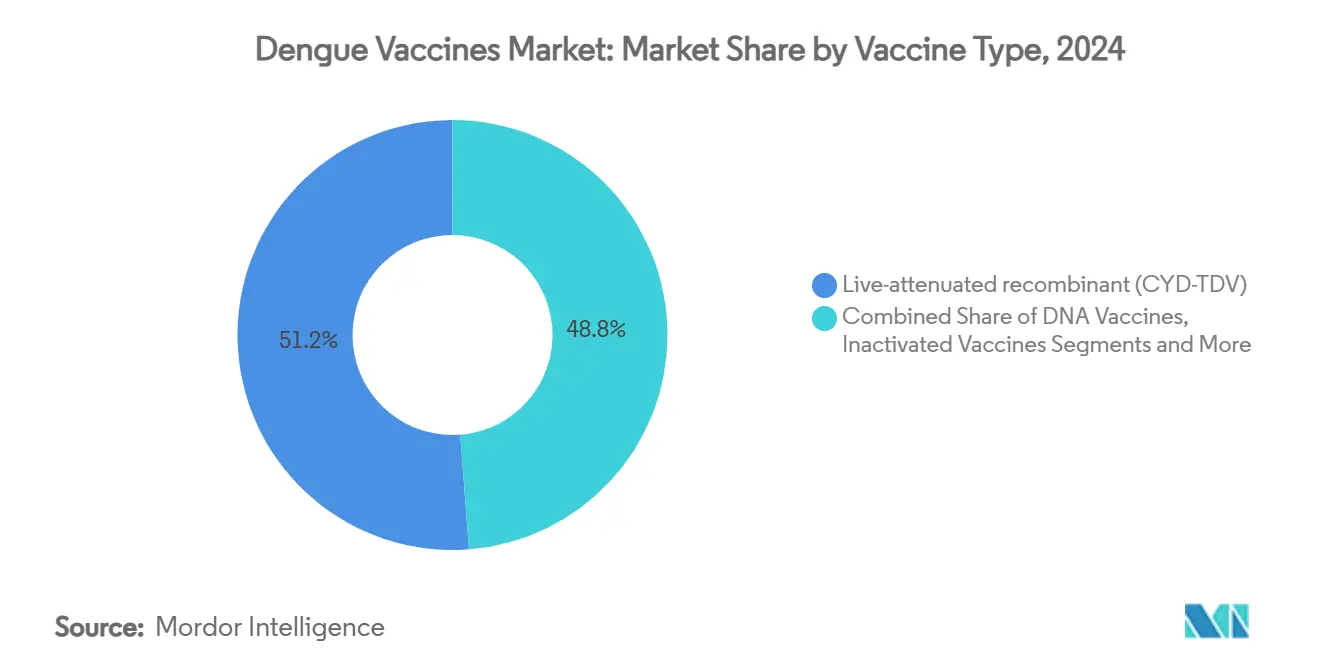

- By vaccine type, live-attenuated recombinant products captured 51.23% of dengue vaccines market share in 2024, while DNA platforms are forecast to grow at a 15.12% CAGR through 2030.

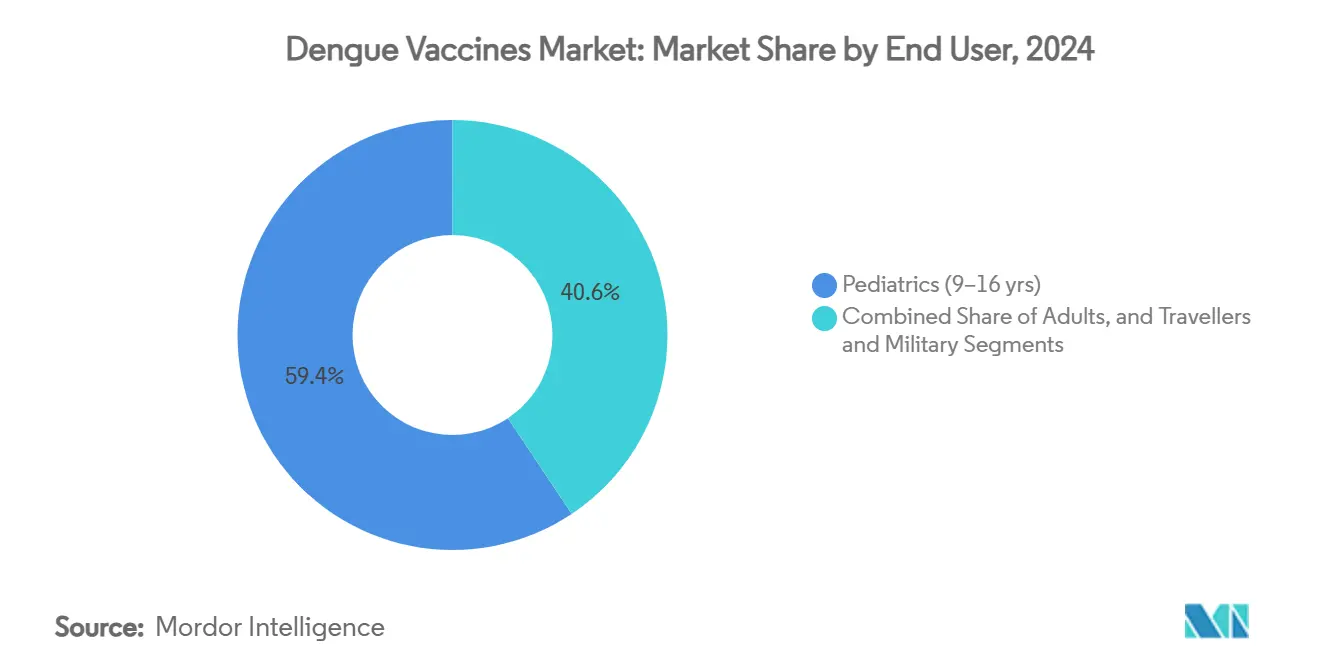

- By end user, paediatrics 9-16 years held 59.36% share of the dengue vaccines market size in 2024; travellers & military personnel represent the fastest-rising cohort with a 14.74% CAGR to 2030.

- By distribution channel, public immunisation programmes accounted for 62.34% share of the dengue vaccines market size in 2024, whereas travel clinics & other private outlets are advancing at a 15.02% CAGR over the same period.

- By geography, Asia-Pacific led with 38.42% revenue share in 2024; North America is projected to register the highest 14.04% CAGR through 2030.

Global Dengue Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endemic prevalence and economic burden | +2.8% | Global, concentrated in APAC & Latin America | Long term (≥ 4 years) |

| Rising regulatory approvals and country roll-outs | +2.1% | Global, early gains in Brazil, Indonesia, Thailand | Medium term (2-4 years) |

| Government immunisation programme adoption | +1.9% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Growth in international traveller vaccinations | +1.4% | North America & EU, expansion to MEA | Short term (≤ 2 years) |

| mRNA/DNA platform acceleration for dengue | +1.6% | Global, R&D centred in North America & EU | Long term (≥ 4 years) |

| Climate-change-driven vector range expansion | +2.3% | Global, with new hotspots in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Endemic Prevalence and Economic Burden

Persistent hyper-endemicity underpins the dengue vaccines market, with Brazil logging 1.6 million probable cases in 2024 and authorising emergency procurement of 5.2 million Qdenga doses. Cost-effectiveness studies in Puerto Rico forecast a 34% reduction in symptomatic cases and USD 408 million savings over two decades by implementing TAK-003.[2]Luis Florentin, “Public Health Impact and Cost-Effectiveness of a New Dengue Vaccine (TAK-003) With a Large Catch-Up Cohort in Puerto Rico,” ISPOR.org Productivity losses across tourism, education and the labour force magnify national income drains, driving ministries of finance to view vaccination as fiscally neutral when compared with repeated vector-control campaigns. Severe paediatric outcomes, including intensive-care admissions, sharpen the policy focus on childhood coverage. As a result, the dengue vaccines market gains recurrent budget lines within national immunisation plans, supporting multi-year purchase commitments that underpin manufacturer capacity-planning.

Rising Regulatory Approvals and Country Roll-Outs

WHO prequalification of Qdenga in 2024 allowed low- and middle-income countries to tap revolving funds for procurement, collapsing access gaps that once spanned years between licence and deployment. Vietnam fast-tracked a national launch within four months of dossier submission, signalling improved regulatory agility across Southeast Asia. The European Medicines Agency’s endorsement set a precedent for other stringent authorities, while Indonesia’s pioneering licence became a template for endemic geographies. Regulators increasingly apply benefit-risk models that weigh population-level gains over individual-level uncertainty, especially as safety data accrue from real-world campaigns. The trend streamlines multi-country studies and shortens pathway timelines, accelerating volume ramp-up in the dengue vaccines market.

Government Immunisation Programme Adoption

Brazil targets children aged 10-14 in municipalities with highest incidence, exemplifying data-driven resource allocation. Gavi’s 2026-2030 strategy contemplates co-financing for more than 50 endemic economies, contingent upon robust burden metrics. National procurement often favours domestic production; Instituto Butantan’s alliance with WuXi Biologics aims at 60 million annual single-dose vials starting 2026 to secure vaccine sovereignty. Governments also prize one-shot schedules that simplify outreach to remote districts, reinforcing uptake in resource-constrained settings. These policies collectively stabilise baseline demand and deepen market penetration.

Growth in International Traveller Vaccinations

The CDC recorded a 168% rise in travel-associated dengue cases during 2010-2021, foreshadowing post-pandemic resurgence. As dengue spreads into Iran and Southern Europe, travel clinics adopt risk-stratified protocols prioritising frequent flyers and those with prior exposure who face heightened severe disease risk upon reinfection. Corporate mobility programmes embed vaccination within pre-departure medicals, creating predictable volume off-takes for private providers. Compliance rates above 70% in North America and the EU translate into steady growth pockets inside the wider dengue vaccines market. Bundled travel-health services further enhance clinics’ margins, reinforcing private-channel expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety and efficacy concerns of first-generation vaccines | -1.8% | Global, acute in Philippines & Latin America | Medium term (2-4 years) |

| High R&D cost and complex tetravalent trials | -1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Funding diverted to other emerging-disease vaccines | -0.9% | Global, impacting NIH-funded research | Short term (≤ 2 years) |

| Cold-chain constraints in low-resource regions | -1.4% | Sub-Saharan Africa, rural APAC, remote Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety and Efficacy Concerns of First-Generation Vaccines

Dengvaxia’s controversial rollout in the Philippines revealed elevated hospitalisation risks for seronegative children, compelling global programmes to mandate pre-vaccination serological screening.[3]Kai Kupferschmidt, “Controversy over dengue vaccine risk,” Science.org Sanofi will cease production by 2026, citing low demand and complex eligibility protocols. Antibody-dependent enhancement remains a critical challenge; even TAK-003 shows muted responses to DENV-3 and DENV-4 among seronegative recipients. Regulatory bodies insist on extensive pharmacovigilance, with Brazil logging 501 hypersensitivity events—including 124 anaphylaxis cases—between March 2023 and September 2024. These concerns temper uptake, restraining growth in parts of the dengue vaccines market.

High R&D Cost and Complex Tetravalent Trials

Balanced immunity against four serotypes inflates trial sizes and durations. Instituto Butantan enrolled more than 16,000 participants in a multi-year phase 3 study to capture seasonal variation and long-term safety signals. Manufacturing needs tight quality controls to ensure consistent potency of every component. Regulatory guidance varies across jurisdictions, forcing companies to navigate bespoke dossiers that lengthen timelines and inflate costs. Risk-averse investors focus on probability-weighted returns, limiting early-stage capital flows and constraining pipeline diversity in the dengue vaccines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Live-Attenuated Dominance Faces DNA Disruption

Live-attenuated recombinant products represented 51.23% of dengue vaccines market share in 2024, buoyed by established distribution networks and inclusion in public programmes. Qdenga’s WHO prequalification accelerates multilateral procurement, while the impending phase-out of Dengvaxia consolidates volumes toward Takeda. DNA platforms, however, are expanding at a 15.12% CAGR and could command larger slices of the dengue vaccines market size by 2030 if single-dose efficacy demonstrated in preclinical studies translates into clinical success. Integration of CRISPR-Cas13 targeting promises broad serotype coverage with lower manufacturing complexity, encouraging venture funding and public-sector grants.

Innovation pressure extends to inactivated, subunit and VLP formats, which serve immunocompromised cohorts and travellers prioritising safety. Yet, their limited immunogenicity necessitates adjuvant enhancements, capping near-term expansion. Live-attenuated chimeric constructs sustain moderate growth through label extensions and catch-up campaigns in high-burden geographies. Overall, competition between traditional and platform-based technologies will shape the pace at which the dengue vaccines market shifts toward next-generation modalities.

By End User: Pediatric Focus Drives Military Growth

Paediatric recipients aged 9-16 accounted for 59.36% of the dengue vaccines market size in 2024 as governments integrate Qdenga into national schedules. The segment maintains double-digit expansion thanks to demographic momentum in Asia and Latin America, where under-15 populations remain large. Adult immunisation lags because safety trials in seronegative cohorts are still ongoing, but single-dose candidates reporting 90% efficacy among adults 18-59 could unlock a sizeable catch-up opportunity after 2027.

Travellers and military personnel represent the fastest 14.74% CAGR. The Pentagon’s Walter Reed Institute advances a purified inactivated candidate, reflecting institutional recognition of operational risk in tropical deployments. Corporate expatriate policies and adventure tourism growth further widen adult demand outside public channels. Combined, these trends diversify revenue streams and reinforce growth prospects for the overall dengue vaccines market.

By Distribution Channel: Public Programmes Enable Private Growth

Public immunisation platforms generated 62.34% of sales in 2024, underpinned by Brazil’s and Indonesia’s mass campaigns. Budgeted multi-year tenders allow manufacturers to forecast capacity utilisation and negotiate tiered pricing. Nonetheless, travel clinics and private hospitals are growing at a 15.02% CAGR as high-income consumers pursue elective protection for leisure and business travel. Cold-chain innovations and microneedle patches could broaden private-sector reach into suburban pharmacies, improving convenience and boosting uptake.

The interplay of public bulk volumes and private premium pricing offers a balanced revenue mix. As single-dose formats enter the market, private channels may gain share by marketing convenience to time-pressed adults, increasing competitive intensity in the dengue vaccines market.

Geography Analysis

Asia-Pacific retained 38.42% leadership through established vaccination infrastructure and dense urban clusters where dengue is endemic. Indonesia pioneered TAK-003 approval while Thailand embedded vaccination into a multi-pillar plan combining vector control and digital surveillance. India’s regulator is evaluating Takeda’s dossier and, alongside a Biological E partnership targeting 50 million annual doses, could significantly enlarge regional demand. Japan’s R&D incentives attract platform innovators, laying groundwork for future export capacity and further expanding the dengue vaccines market.

South America follows, propelled by Brazil’s emergency procurements and Instituto Butantan’s 79.6%-efficacy single-dose candidate. Serotype 3’s resurgence after 16 years underscores epidemiological volatility, cementing vaccination as a strategic pillar. Argentina’s early adoption of TAK-003 reinforces regional momentum, while domestic manufacturing initiatives position the continent as a potential export hub post-2026.

Europe and North America together display double-digit growth as climate change and increased travel introduce local transmission events, prompting stronger clinic demand and updated public-health advisories. The Middle East and Africa remain nascent but high-potential; improved surveillance and pending Gavi support could unlock new cohorts in sub-Saharan Africa by the end of the decade. These geography dynamics collectively sustain a diverse and resilient growth path for the dengue vaccines market.

Competitive Landscape

The dengue vaccines market is moderately concentrated. Takeda and Sanofi held 71% share in 2024, but Sanofi’s retreat will shift balance toward Takeda, likely lifting its stake above 50% by 2026. Instituto Butantan disrupts incumbents with a high-efficacy single-dose candidate and localised manufacturing scale backed by Brazilian state funding. Merck has initiated phase 3 for quadrivalent V181, adding a heavyweight contender. Chugai and GSK collaborate on monoclonal antibodies that could serve prophylactic roles for high-risk adults.

Strategic moves include Takeda’s supply alliance with Biological E for production in India, Sanofi’s acquisition of Vicebio to refresh its pipeline, and WuXi Biologics’ partnership with Butantan, collectively underscoring the shift toward platform diversification and end-to-end regional supply chains. Competition increasingly hinges on single-dose convenience, broad serotype coverage and cold-chain flexibility. Market entrants capable of addressing these factors stand to erode incumbent positions and accelerate innovation cycles.

Dengue Vaccines Industry Leaders

Sanofi

Takeda Pharmaceutical

Serum Institute of India

GlaxoSmithKline

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: India’s Dengue all enrolled 7,248 participants in a phase 3 trial led by ICMR and Panacea Biotec.

- June 2025: Merck launched MOBILIZE-1 phase 3 to evaluate single-dose V181, beginning enrolment in Singapore.

- February 2025: Instituto Butantan partnered with WuXi Biologics to produce 60 million single-dose vials annually from 2026, targeting ages 2-59 years.

Global Dengue Vaccines Market Report Scope

| Live-attenuated recombinant (CYD-TDV) |

| Live-attenuated chimeric (TAK-003) |

| DNA Vaccines |

| Inactivated Vaccines |

| Subunit / VLP Vaccines |

| Pediatrics (9–16 yrs) |

| Adults (≥17 yrs) |

| Travellers & Military |

| Public Immunisation Programs |

| Private Clinics & Hospitals |

| Travel Clinics & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Live-attenuated recombinant (CYD-TDV) | |

| Live-attenuated chimeric (TAK-003) | ||

| DNA Vaccines | ||

| Inactivated Vaccines | ||

| Subunit / VLP Vaccines | ||

| By End User | Pediatrics (9–16 yrs) | |

| Adults (≥17 yrs) | ||

| Travellers & Military | ||

| By Distribution Channel | Public Immunisation Programs | |

| Private Clinics & Hospitals | ||

| Travel Clinics & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the dengue vaccines market in 2025 and what CAGR is expected to 2030?

The dengue vaccines market stands at USD 0.717 billion in 2025 and is projected to climb to USD 1.27 billion by 2030 with a 12.21% CAGR.

Which region currently leads demand for dengue vaccines?

Asia-Pacific commands 38.42% share owing to long-standing endemicity and mature immunisation networks.

Which vaccine type is growing fastest?

DNA-based platforms are expanding at a 15.12% CAGR, driven by CRISPR-enabled single-dose potential.

What role do traveller vaccinations play in market growth?

International traveller demand is adding 1.4% to forecast CAGR and is expanding fastest through private clinics across North America and Europe.

Why is Sanofi exiting Dengvaxia production?

Persisting safety concerns and mandatory pre-vaccination screening depressed demand, prompting Sanofi to halt production by 2026.

How does climate change influence future vaccine demand?

Rising temperatures and altered rainfall patterns extend Aedes mosquito habitats, increasing the at-risk population and driving new country roll-outs.

Page last updated on: