Remote Browser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 11.98 Billion |

| Growth Rate (2025 - 2030) | 18.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

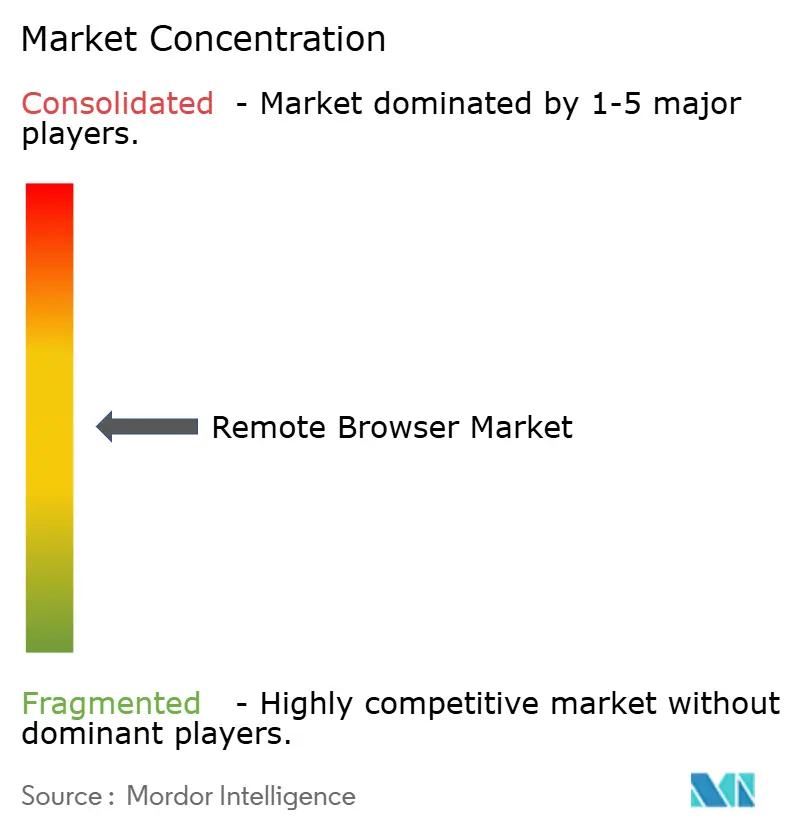

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Remote Browser Market Analysis by Mordor Intelligence

The Remote Browser Market size was valued at USD 4.29 billion in 2025 and estimated to grow from USD 5.11 billion in 2026 to reach USD 11.98 billion by 2031, at a CAGR of 18.56% during the forecast period (2026-2031). The surge reflects regulatory mandates that elevated browser isolation from an optional control to a required safeguard, a global spike in phishing-as-a-service toolkits that bypassed email gateways, and the permanence of hybrid work, which widened the browser-based attack surface. Cloud hyperscalers bundled the capability inside Secure Access Service Edge (SASE) suites, simplifying procurement for enterprises that already consume edge security as a service. Vendors simultaneously released browser-native architectures that reduce latency in pixel-pushing models, improving the user experience in high-fidelity applications such as CAD and telemedicine. Collectively, these moves reshaped purchasing decisions and anchored the remote browser market as a foundational layer of zero-trust programs across regulated industries.

Key Report Takeaways

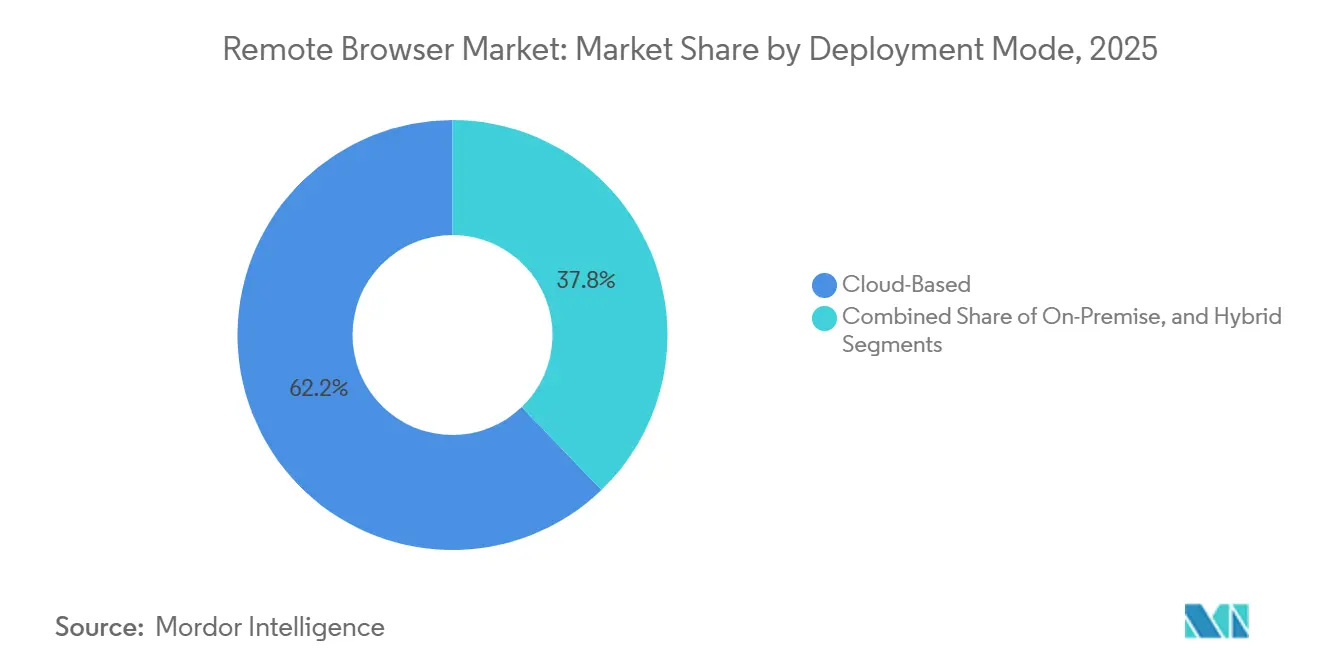

- By deployment mode, cloud-based solutions led with 62.19% of the Remote Browser Market share in 2025, while hybrid deployments are forecast to expand at an 18.22% CAGR through 2031.

- By technology, DOM reconstruction accounted for 55.83% share of the Remote Browser Market size in 2025; network vector rendering is projected to grow at 18.91% between 2026 and 2031.

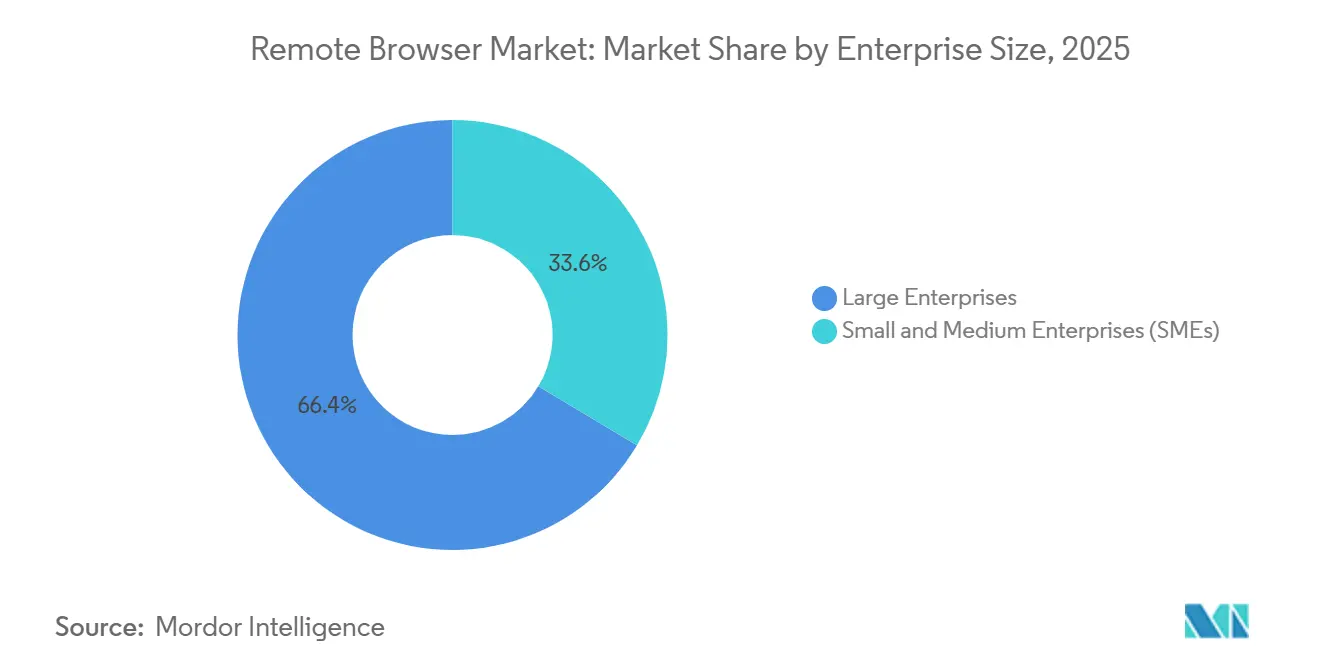

- By enterprise size, large enterprises held 66.42% of the Remote Browser Market share in 2025, whereas small and medium enterprises (SMEs) will experience the highest CAGR at 18.97% through 2031.

- By end-user industry, BFSI commanded 28.79% revenue share in 2025, and healthcare is advancing at an 18.15% CAGR to 2031.

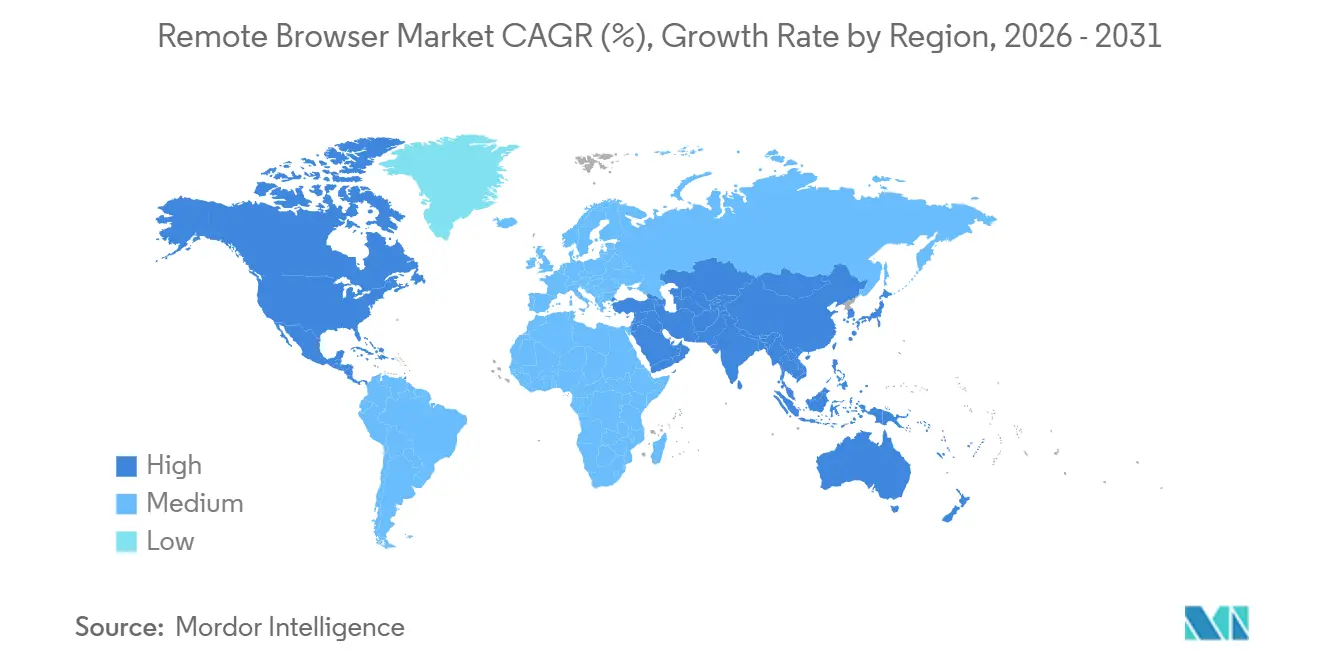

- By geography, North America commanded 45.34% of the revenue share in 2025, and Asia-Pacific is advancing at a 18.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Remote Browser Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Zero-Trust Security Frameworks | +4.2% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Mandatory Browser Isolation for Critical Infrastructure (Post-2025 NIST and EU NIS2) | +3.8% | North America and Europe, spillover into Asia‑Pacific | Short term (≤ 2 years) |

| Surge in Sophisticated Web-Based Phishing-as-a-Service Kits | +3.1% | Global, concentrated in BFSI and IT sectors | Short term (≤ 2 years) |

| Work-From-Anywhere Permanence Expanding SaaS Attack Surface | +2.9% | Global, highest exposure in North America and Europe | Medium term (2-4 years) |

| Browser-Native Ransomware Payloads Targeting Edge and Chrome | +2.3% | Global, elevated risk in Asia‑Pacific and North America | Short term (≤ 2 years) |

| Integration of Remote Browser Isolation Into SASE Suites by Hyperscalers | +2.0% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Zero-Trust Security Frameworks

NIST Special Publication 800-207, CISA’s Zero Trust Maturity Model, and the National Security Agency’s implementation guidance each positioned remote browser isolation as an advanced control for data protection, accelerating budget allocation across U.S. federal and financial sectors.[1]National Institute of Standards and Technology, “Zero Trust Architecture – NIST Special Publication 800-207,” nist.gov The United Kingdom’s Cyber Security and Resilience Act replicated these expectations for digital service providers, thereby driving adoption across telecommunications and public services. Agencies that replaced legacy secure web gateways with browser-native zero-trust controls reported a 30% reduction in latency and a 60% drop in lateral movement incidents within 1 year. Combined, these policies compelled global enterprises to elevate the remote browser market from experimental pilot to core architecture. Vendors responded with modules that map directly to identity-aware proxies, simplifying policy enforcement and closing procurement cycles in months rather than years.

Mandatory Browser Isolation for Critical Infrastructure (Post-2025 NIST and EU-NIS2)

The NIS2 Directive required operators of essential services to isolate browsers by October 2024, while Germany’s BSI broadened C5 attestation to expose data-processing locales, forcing regulated entities toward hybrid or on-premise rendering. In the United States, post-2025 NIST guidance moved browser isolation from recommended to expected for critical infrastructure operators, and FY 2026 federal budgets earmarked USD 1.2 billion for zero-trust browser tools. France’s SecNumCloud qualification compounded pressure by disallowing U.S. administrative access to public-sector data unless sovereign infrastructure is in place. These converging rules turned compliance into an immediate buying trigger, lifting near-term bookings across Europe and North America and solidifying the remote browser market as a compliance necessity.

Surge in Sophisticated Web-Based Phishing-as-a-Service Kits

Microsoft’s March 2026 takedown of Tycoon2FA exposed more than 10,000 compromised Microsoft 365 accounts, demonstrating how browser-in-the-browser kits harvest session cookies and circumvent traditional email filtering.[2]Microsoft Threat Intelligence, “Microsoft Disrupts Tycoon2FA Phishing-as-a-Service Operation,” microsoft.com/security Parallel campaigns such as Sneaky2FA reproduced corporate login pages with pixel-perfect accuracy, enabling adversary-in-the-middle attacks at scale. Georgia Tech research identified over 3,000 malicious Chrome extensions siphoning sensitive data, 200 of which targeted healthcare portals used by 4 million individuals. Pilot deployments in BFSI institutions recorded an 87% decline in phishing-driven breaches after isolating web sessions, underpinning a positive feedback loop that directs security budgets toward the remote browser market.

Work-from-Anywhere Permanence Boosting SaaS Attack Surface

By 2025, 68% of enterprises will allow unmanaged devices to reach production SaaS, and employees will interact with an average of 36 browser applications outside perimeter defense.[3]Palo Alto Networks, “Prisma Browser for Business Launch,” paloaltonetworks.com Cyberhaven found that 77% of staff copied sensitive text into generative AI chatbots weekly, often without data-loss prevention. Browser isolation embeds restrictions such as copy-paste blocking and download prevention directly into the session, eliminating the need for traffic back-haul and preserving user experience. As hybrid work becomes a fixture rather than a contingency, these inline controls make the remote browser market indispensable for compliance with sectoral privacy frameworks that now follow the worker, not the office.

Restraint Impact Analysis*

| (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|

| Latency and User-Experience Issues in High-Fidelity Web Applications | -2.1% | Global; particularly impacting enterprise adoption in North America and Europe | Short term (≤ 2 years) |

| Budget Compression in SME Cybersecurity Stacks | -1.8% | Global; acute pressure among SMEs in Asia‑Pacific and South America | Medium term (2-4 years) |

| Competition From Client-Side Hardening (Embedded Safe-Browsing APIs) | -1.3% | Global; higher adoption in North America and Europe | Long term (≥ 4 years) |

| Fragmented Regional Data-Residency Mandates Complicating Cloud-Based RBI Rollout | -1.5% | Europe, Asia‑Pacific, Middle East; spillover impact on multinational enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Latency and UX Issues in High-Fidelity Web Apps

Pixel-pushing streams introduce connection delays of 1.4 to 11.9 seconds, which are unacceptable for browser-based CAD, video conferencing, and real-time trading platforms. Google’s Interaction to Next Paint metric elevated responsiveness to a ranking factor, raising customer intolerance for any security overlay that hampers speed. Although vendors such as Zscaler adopted network vector rendering through the SquareX acquisition, 41% of IT leaders still cite latency as the top barrier to full deployment. The constrain is most severe in regions with sparse edge nodes, where round-trip times eclipse acceptable thresholds for interactive workloads.

Budget Compression in SME Cybersecurity Stacks

SMEs suffer 3.5 times as many AI-driven attacks as large organizations, yet operate on flat security budgets. Cisco’s 2025 Cybersecurity Readiness Index placed only 4% of firms in the Mature category, estimating that staffing gaps add USD 1.76 million to breach costs. Palo Alto Networks countered with Prisma Browser for Business at USD 99 per seat per year, but SMEs must still juggle funds across email security, endpoint detection, and cyber insurance. Until low-touch managed services proliferate, constrained budgets temper the overall CAGR of the remote browser market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud-First Momentum Outpaces Alternatives

Hybrid deployments are forecast to grow at 18.22% between 2026 and 2031, outpacing cloud-only and on-premise alternatives as organizations reconcile data-residency statutes with performance needs. Cloud-based services owned 62.19% of the Remote Browser Market share in 2025, propelled by SASE bundles from hyperscalers that eliminated integration friction. Europe’s Health Data Space Regulation and France’s SecNumCloud rules forced healthcare providers to keep protected data on EU soil, prompting dual-stack architectures that steer sensitive workflows to on-premise rendering while leaving general browsing to cloud pods.

The hybrid approach also mitigates latency, routing risky domains through isolated cloud containers while allowing trusted SaaS to load natively, slicing response times by as much as 40%. AWS earmarked EUR 7.8 billion (USD 8.8 billion) for European sovereign zones that guarantee operator-only access, a signal that data localization is now mandatory rather than discretionary. As sovereign cloud capacity scales, hybrid isolation is becoming the default blueprint for banks, health systems, and public agencies. This dynamic drives recurring revenue in the remote browser market and cements vendor roadmaps centered on regional compliance.

By Technology Type: Network Vector Rendering Challenges DOM Dominance

DOM reconstruction dominated the Remote Browser Market with a 55.83% share in 2025, as it balances security with near-native UX. However, its reliance on signature updates creates vulnerabilities, leaving gaps for zero-day exploits to bypass detection and infiltrate systems. Pixel-pushing effectively eliminates this risk by providing a more secure approach. This method comes with significant trade-offs, including increased bandwidth consumption and latency exceeding 200 milliseconds, particularly in complex applications.

Network vector rendering grew at an 18.91% CAGR by instructing endpoints on how to render content instead of shipping full frames, halving server compute load and slashing latency. Zscaler’s SquareX integration and Palo Alto Networks’ browser-native engine illustrate how vendors are embedding protection within the runtime rather than in a distant data plane. Financial trading desks and radiology labs, both intolerant of delay, are early adopters. Over time, these advantages are expected to erode DOM reconstruction’s lead and redistribute revenue inside the remote browser market.

By Enterprise Size: SME Adoption Accelerates on Tiered Pricing

Large enterprises controlled 66.42% of deployments in 2025, reflecting early zero-trust investments by banks and federal agencies. Still, SMEs are slated for an 18.97% CAGR through 2031 as vendors slash price points and automate policy creation. Prisma Browser for Business captured 10 million seats in six months by promising 15-minute deployments and bundling threat intelligence tailored for healthcare clinics and professional services outfits.

SME employees juggle dozens of browser apps, yet resource-strapped IT teams struggle to patch endpoints or vet extensions. Managed isolation shifts that burden into the cloud, lowering friction at entry. As compliance frameworks such as HIPAA broaden to smaller covered entities, budget-friendly offerings pull new logos into the remote browser market and diversify the customer mix beyond Fortune 500 accounts.

By End-User Industry: Healthcare Leads on Regulatory Tailwinds

BFSI retained 28.79% of revenue in 2025, but healthcare is growing fastest at 18.15% through 2031, driven by HIPAA’s 2026 amendments requiring AES-256 encryption and a 24-hour breach notice. IBM has quantified the average cost of a healthcare data breach at USD 7.42 million, with an average dwell time of 279 days before detection and containment. These statistics highlight the significant financial and operational risks associated with such breaches, underscoring the return on investment (ROI) of implementing proactive browser controls to mitigate potential threats effectively.

Menlo Security documented a 94% reduction in protected health information leakage after isolating browser sessions in a multi-site hospital network. Coupled with rampant malicious extensions that harvest patient data, regulatory fines over pixel tracking, and a surge of AI chatbots, hospitals now view browser isolation as non-negotiable. This momentum channels disproportionate spend into the remote browser market and fuels vendor specialization in medical compliance.

Geography Analysis

North America accounted for 45.34% of the Remote Browser Market size in 2025, driven by U.S. federal zero-trust mandates and rapid SASE adoption among Wall Street banks. Continued funding in FY 2026 budgets, plus Canada’s GDPR-style breach rules, sustain enterprise demand, though growth moderates as saturation nears in tier-one enterprises. The region’s dense edge grids hold average latency below 20 milliseconds, giving cloud deployments a performance edge. Competition is fierce, with Zscaler, Palo Alto Networks, and Cloudflare racing to compress session start times while niche players such as Authentic8 pitch hardened environments for defense contractors.

Asia-Pacific is projected to expand at 18.28% through 2031, the highest regional CAGR, spurred by localization laws in China, India, and Vietnam that push multinationals toward in-country rendering nodes. Akamai logged more than 80 billion web app attacks in Asia during 2024, including 11 billion targeting APIs, spotlighting the fragility of the perimeter. Japan and South Korea benefit from EU adequacy, yet domestic buyers still prefer hybrid modes to assuage customer data-sovereignty expectations. Australia’s critical infrastructure amendments and Singapore’s fintech push round out a region where regulatory heterogeneity demands multi-region deployments, thereby elevating the total addressable market for the remote browser market.

Europe rides a compliance wave triggered by NIS2, the Data Act, and the forthcoming European Health Data Space Regulation. France’s SecNumCloud rule effectively bars non-sovereign U.S. vendors unless they erect EU-only administrative domains. AWS answered with a EUR 7.8 billion (USD 8.8 billion) sovereign program, while Microsoft pledged in-country Copilot processing for 15 nations. Germany’s BSI added location transparency to C5 audits, driving banks toward hybrid setups that split trusted SaaS from sensitive workloads. South America, the Middle East, and Africa trail but show pockets of acceleration, Brazilian banking regulations, Saudi Vision 2030, and South African finance pilots illustrating how regional statutes continually enlarge the remote browser market.

Competitive Landscape

The field remains moderately fragmented with hyperscaler SASE leaders, endpoint incumbents, and pure-play specialists jostling across architecture, latency, and compliance axes. CrowdStrike bought Seraphic Security for USD 420 million in January 2026 to add runtime browser protection to its Falcon endpoints. Zscaler’s February 2026 close of SquareX's infused network vector rendering into its cloud service, a pivot aimed at erasing the latency complaints dogging pixel-pushing.

Cato Networks and Versa Networks emphasize GPU-accelerated rendering and unified consoles to woo mid-market buyers who crave one-pane management. Meanwhile, Menlo Security doubles down on healthcare workflows with AI-powered threat analytics tailored to HIPAA, and Authentic8 positions its Silo browser for classified environments. Patent filings by Palo Alto Networks reveal a focus on embedded policy engines that update in real time, squeezing response latency to sub-100-millisecond thresholds.

New entrants such as Kasm Technologies push containerized open-source stacks that attract DevOps teams, while Light Point Security courts cost-sensitive SMEs with pay-per-hour isolation instances. Despite consolidation, the top five vendors still account for less than 60% of combined revenue, signaling room for disruption. Differentiation will hinge on sovereign cloud footprints, browser-native performance, and verticalized compliance features, all of which directly influence wallet share within the expanding remote browser market.

Remote Browser Industry Leaders

Forcepoint LLC

Netskope, Inc.

Menlo Security, Inc.

Broadcom Inc.

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Palo Alto Networks launched Prisma Browser for Business at USD 99 per user annually, reaching 10 million seats within six months.

- March 2026: Microsoft disrupted the Tycoon2FA phishing-as-a-service ring that compromised more than 10,000 Microsoft 365 accounts.

- March 2026: Cato Networks unveiled GPU-accelerated rendering, trimming pixel-streaming latency by 35%.

- March 2026: Versa Networks rolled out its Secure Enterprise Browser with real-time threat-intel synchronization.

Global Remote Browser Market Report Scope

The Remote Browser Market pertains to the industry segment that delivers secure browsing solutions by isolating web activity from a user's local device or network, typically utilizing cloud-based or virtualized environments. These solutions safeguard users from web-based threats, including malware, phishing, and malicious scripts, by executing browsing sessions on a remote server and streaming only secure content to the end user.

The Remote Browser Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Technology Type (DOM Reconstruction, Pixel Pushing, and Network Vector Rendering), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, IT and Telecommunications, Government and Defense, Healthcare, Education, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| DOM Reconstruction |

| Pixel Pushing |

| Network Vector Rendering |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| IT and Telecommunications |

| Government and Defense |

| Healthcare |

| Education |

| Other End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Technology Type | DOM Reconstruction | ||

| Pixel Pushing | |||

| Network Vector Rendering | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | BFSI | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare | |||

| Education | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the remote browser market be by 2031?

The remote browser market is projected to reach USD 11.98 billion by 2031, expanding at an 18.56% CAGR during 2026-2031.

Which deployment mode is growing the fastest?

Hybrid deployment is expected to grow the fastest, registering an 18.22% CAGR, as it balances data-sovereignty requirements with performance optimization.

Why is healthcare adopting browser isolation rapidly?

HIPAA amendments effective from 2026 and the high cost of data breaches have driven healthcare providers to adopt browser isolation, resulting in a 94% reduction in protected-health-information leakage.

What is the biggest restraint to browser isolation adoption?

Latency in high-fidelity web applications remains the primary challenge, with 41% of IT leaders citing poor responsiveness as a key barrier.

Which region will see the highest growth through 2031?

Asia-Pacific is expected to record the fastest regional growth at an 18.28% CAGR, driven by stringent data?localization regulations and rising web?application cyberattacks.

Page last updated on: