Browser Isolation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.53 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 24.74% CAGR |

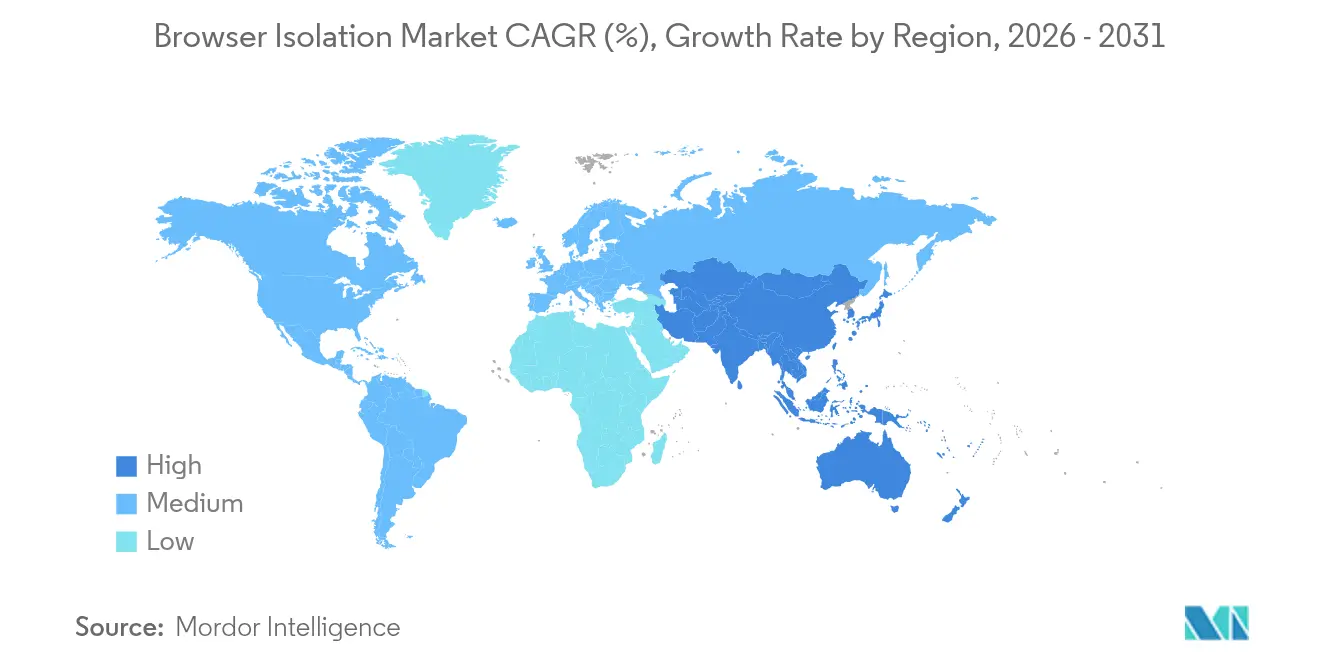

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

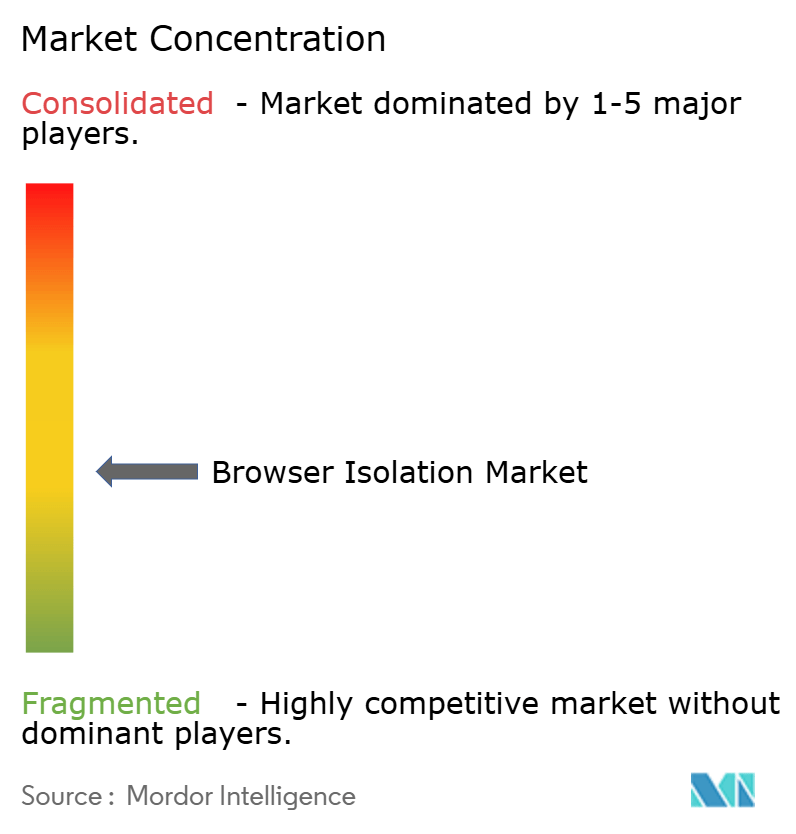

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Browser Isolation Market Analysis by Mordor Intelligence

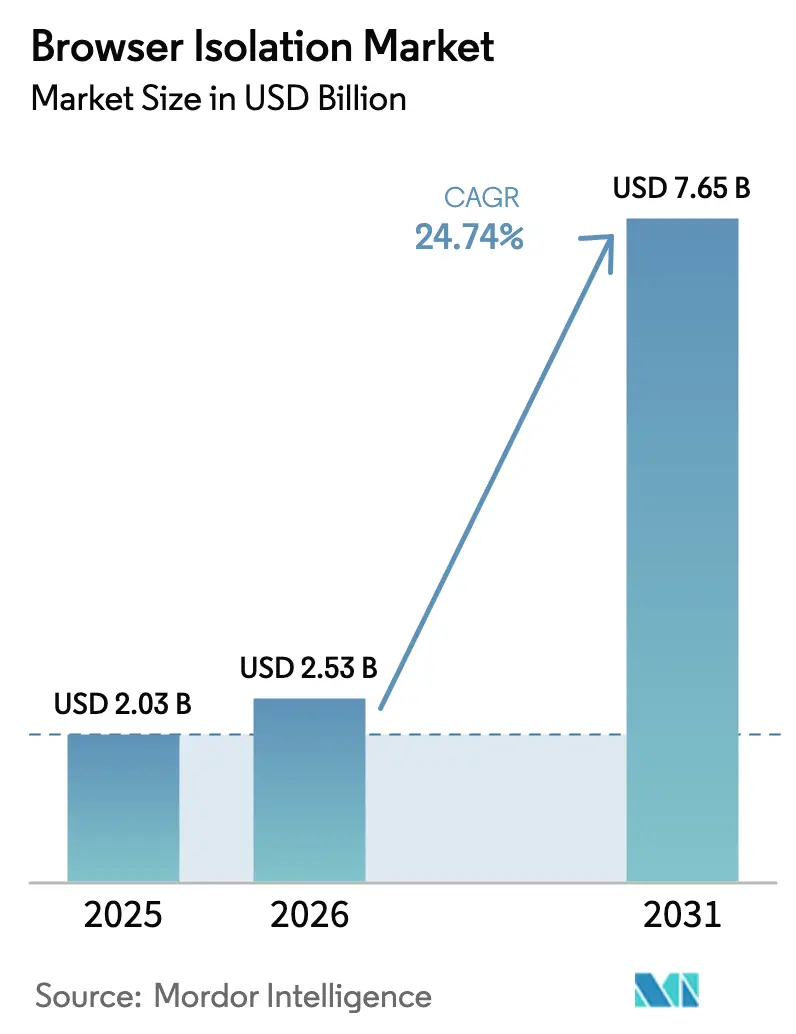

The browser isolation market size is expected to grow from USD 2.03 billion in 2025 to USD 2.53 billion in 2026 and is forecast to reach USD 7.65 billion by 2031 at 24.74% CAGR over 2026-2031. This expansion reflects the shift from a niche defensive layer to a staple in Zero Trust security stacks as organizations realize that most employee activity now takes place inside a web browser. Adoption accelerates when enterprises measure that 85% of the workday depends on the browser, making effective isolation indispensable for risk managers safeguarding distributed workforces. Rising sophistication of browser-based threats, regulatory pressure for rapid breach disclosure, and the bundling of isolation into broader Security Service Edge (SSE) suites further reinforce demand. North America benefits first from federal Zero Trust mandates, while Asia-Pacific records the steepest growth as regional budgets climb and cyber insurance premiums favor firms with isolation controls in place.

Key Report Takeaways

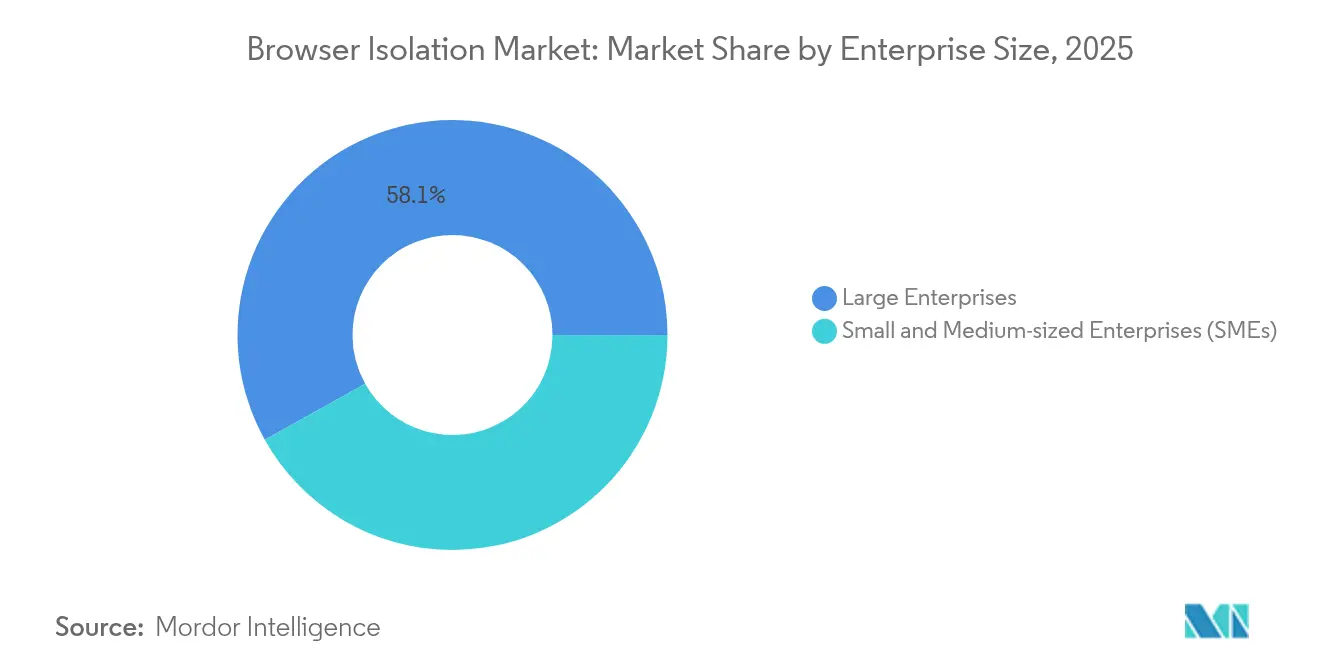

- By enterprise size, large enterprises commanded 58.10% of browser isolation market share in 2025; small and medium-sized enterprises (SMEs) post the fastest expansion at a 28.86% CAGR to 2031.

- By deployment mode, cloud-based implementations held 60.92% revenue share in 2025, while hybrid deployments advance at a 27.62% CAGR through 2031.

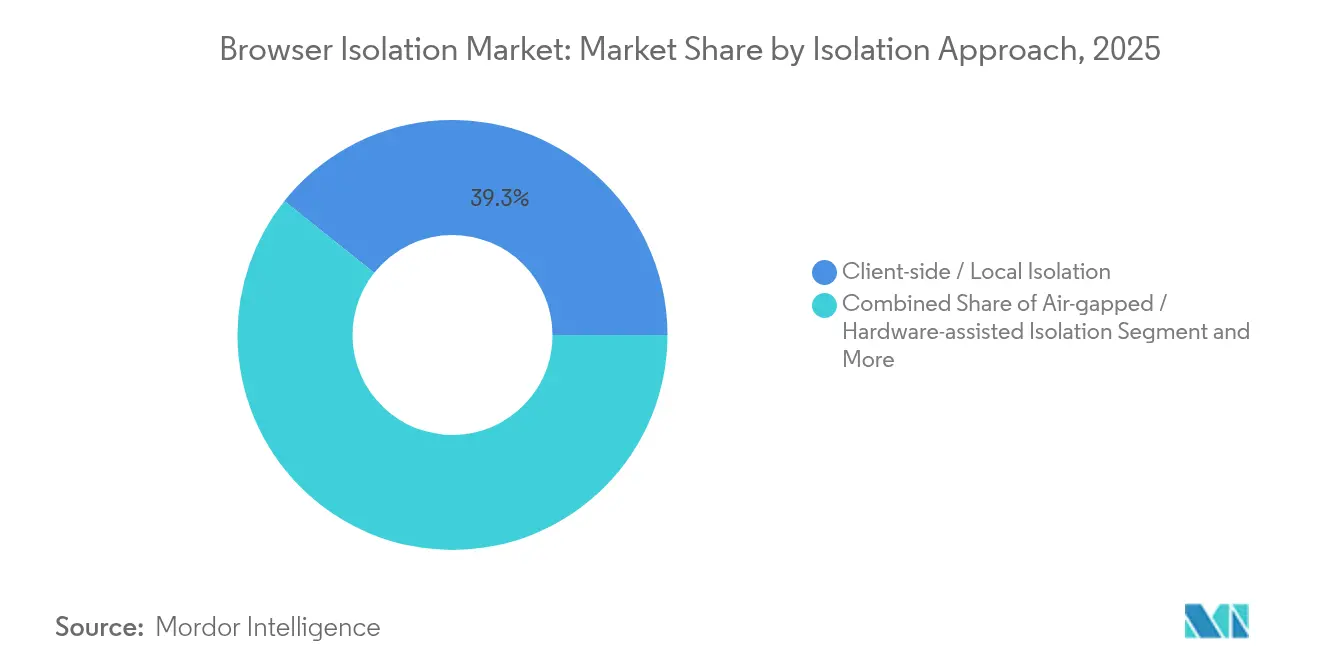

- By the isolation approach, client-side/local techniques secured 39.30% of the browser isolation market size in 2025, whereas remote browser isolation (RBI) records the highest 31.95% CAGR.

- By end-user industry, banking, financial services, and insurance (BFSI) led with a 32.40% share in 2025; healthcare and life sciences grow the quickest at a 30.52% CAGR.

- By geography, North America retained a 42.85% share in 2025; Asia-Pacific registers the strongest 29.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Browser Isolation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in sophisticated browser-based cyber-attacks | +6.2% | Global | Short term (≤ 2 years) |

| Expansion of hybrid and remote workforces | +5.8% | North America and EU, Asia-Pacific core | Medium term (2-4 years) |

| Compliance push toward Zero-Trust / SASE architectures | +4.9% | Global, with early gains in North America | Medium term (2-4 years) |

| Vendor bundling of RBI into SWG and SSE suites | +3.7% | Global | Long term (≥ 4 years) |

| Rise of enterprise browsers redefining RBI TAM | +2.8% | North America and EU | Long term (≥ 4 years) |

| Integration of RBI in CI/CD pipelines for supply-chain security | +1.9% | Global, concentrated in tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Sophisticated Browser-Based Attacks

Critical vulnerabilities such as CVE-2025-2783 show how a single Chromium flaw can impact a broad ecosystem, forcing security teams to treat the browser as high-risk infrastructure.[1]Cloudflare, “Network Vector Rendering: A New Approach to Secure Browsing,” cloudflare.com Security advisories from government agencies amplify the urgency, and incident data indicating that more than 80% of initial infections originate from web activity underscores the need for isolation. Enterprises replace or augment endpoint defenses with RBI, viewing it as a non-negotiable shield for software supply-chain developers and DevOps teams.

Expansion of Hybrid and Remote Workforces

Permanent hybrid staffing means users connect from unmanaged devices and variable bandwidth links. Browser isolation lets security teams enforce identical controls without a VPN, keeping sensitive web traffic off endpoints while meeting user experience targets. Government health agencies scaled cloud isolation during the pandemic, proving its capacity to secure millions of remote sessions with minimal disruption.[2]Menlo Security, “HHS Deploys Cloud Web Isolation to Secure Remote Work,” menlosecurity.com

Compliance Push Toward Zero-Trust / SSE Architectures

Mandates such as the U.S. federal Zero Trust directive and the Securities and Exchange Commission’s 30-day consumer notification rule for breaches prompt firms to embed RBI inside incident-response playbooks. NIST guidance lists isolation as a core pattern for web access, giving security leaders a blueprint for budget justification.[3]National Institute of Standards and Technology, “Zero Trust Architecture: Special Publication 800-207,” nist.gov

Vendor Bundling of RBI into SWG and SSE Suites

Major platforms combine RBI with secure web gateways and data protection, easing procurement and integration headaches. Zscaler inserts isolation into traffic inspected on its Zero Trust Exchange, which now processes over half a trillion transactions daily. Bundling drives down per-user cost and accelerates time-to-value, especially for mid-market buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for large deployments | -3.4% | Global, particularly cost-sensitive SMEs | Short term (≤ 2 years) |

| Latency and UX degradation in pixel-pushing architectures | -2.7% | Asia-Pacific, regions with limited bandwidth | Medium term (2-4 years) |

| Chrome monoculture delaying stand-alone RBI adoption | -1.8% | Global | Long term (≥ 4 years) |

| Substitution by lightweight virtualization / endpoint isolation | -1.3% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Large Deployments

Scaling browser isolation to tens of thousands of concurrent users requires regional points of presence, premium bandwidth commitments, and integration effort that inflate operational budgets. SMEs feel the pinch first because license tiers assume enterprise-scale volumes, narrowing ROI.

Latency and UX Degradation in Pixel-Pushing Architectures

Legacy designs that stream images introduce perceptible lag on dynamic sites. Cloudflare’s vector-rendering approach mitigates the issue, yet many buyers still associate RBI with poor responsiveness, hindering rollouts in countries where last-mile throughput is inconsistent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: SMEs Drive Democratization

Large enterprises retained 58.10% of browser isolation market share in 2025, supported by budgets earmarked for compliance and advanced threat defense. Smaller firms move fastest, logging a 28.86% CAGR as SaaS offerings remove infrastructure hurdles. The browser isolation market size for SMEs is set to eclipse USD 3.1 billion by 2031, confirming that isolation is no longer a luxury for Fortune-500 players alone. Lower-tier licenses, managed-service bundles, and marketplace deals allow IT generalists to activate protection in hours instead of months. At the same time, global banks keep expanding seats to guard e-trading floors and MandA teams that handle regulated data.

Demand diversification reshapes vendor roadmaps. Providers integrate wizard-driven deployments, lightweight agents, and policy templates that map to common audit frameworks. As enterprise browsers reach 25% adoption by 2028, even micro-enterprises will expect built-in RBI. Competition intensifies around the mid-market, forcing suppliers to differentiate through ease of use, partner ecosystems, and total cost transparency.

By Deployment Mode: Hybrid Models Gain Momentum

Cloud-hosted delivery held 60.92% of 2025 revenue, buoyed by instant scalability and global coverage. Nevertheless, hybrid designs grow the fastest at 27.62% CAGR as organizations split traffic: low-risk browsing runs in the cloud, while high-sensitivity workloads stay on-premises. This flexible architecture keeps latency low for trading desks and complies with data-sovereignty laws without forfeiting cloud elasticity. Enterprises deploying a hybrid stack observe a 35% drop in help-desk tickets tied to blocked content, which improves user sentiment.

The browser isolation market size attributed to hybrid deployments is projected to surpass USD 2.85 billion by 2031. Vendors now ship unified consoles that orchestrate both cloud and appliance nodes so that policy remains consistent. Government agencies such as the U.S. Patent and Trademark Office validate the model, citing seamless coverage of external and internal browsing while preserving FedRAMP compliance. Future roadmaps emphasize automated traffic steering, selecting the optimal engine based on content risk, user location, and latency telemetry.

By Isolation Approach: RBI Moves to the Forefront

Client-side techniques accounted for 39.30% share in 2025, but remote browser isolation posts a 31.95% CAGR that will make it the default within five years. Security officers value how RBI eliminates local code execution, locking down unmanaged devices. Cloud-native engines allocate compute on demand, which lowers capital expenditure for seasonal businesses. The browser isolation market gains trust among auditors because all web content is rendered in disposable cloud containers.

Advances such as streaming draw commands instead of pixels cut bandwidth by up to 60%, addressing one of the longest-standing objections. Pricing also shifts: subscription tiers reflect consumed minutes rather than named seats, matching the consumption patterns of gig-economy and contractor networks. Hardware-assisted isolation remains niche inside defense and critical-infrastructure operators that accept higher cost in exchange for air-gapped assurance.

By End-User Industry: Healthcare Accelerates Adoption

BFSI led with 32.40% revenue in 2025 after regulators raised expectations for breach transparency and secure consumer portals. Financial firms embed RBI inside online brokerage and client-advice platforms, protecting both employees and customers. In parallel, healthcare and life sciences grow at a 30.52% CAGR as hospitals digitize patient records and telemedicine usage climbs. The Department of Health and Human Services demonstrates scale, running a cloud isolation service that secures millions of daily sessions.

Government and defense remain reliable buyers, evidenced by multi-year DISA contracts. Technology service providers consume RBI for internal defense and to pre-integrate it into managed security offerings, multiplying the downstream installed base. Manufacturing plants use isolation to safeguard intellectual property exchanged through supplier portals, while universities protect research data during collaborative projects.

Geography Analysis

North America retained 42.85% of 2025 revenue and continues to expand steadily through 2031. Federal Zero Trust deadlines ensure ongoing budget allocations, and breach-notification rules tilt buyer preference toward proactive controls. Headquarters of major suppliers such as Zscaler and Palo Alto Networks in the region speeds feature commercialization and channel coverage. Public-sector success stories, including the U.S. Department of Health and Human Services’ rapid pandemic rollout, illustrate maturity and scale.

Asia-Pacific emerges as the fastest-growing theatre at a 29.74% CAGR. Regional security budgets rise as insurers offer premium discounts to firms that deploy RBI controls. Singapore’s economic agency invested directly in Island, supporting local customer pilots and talent development. Japan’s largest backbone provider partners with Menlo Security to deliver isolation as a managed service, validating appetite for cloud-first defenses across varying bandwidth conditions. Markets such as India, Vietnam, and Indonesia follow suit as government frameworks encourage secure digital-service delivery.

Competitive Landscape

The browser isolation market displays moderate concentration with vigorous rivalry. Platform vendors leverage existing customer footprints: Zscaler’s cloud security portfolio generated USD 678 million in Q3-2025 revenue, up 23% year over year, with isolation cited as a key workload. Palo Alto Networks’ next-generation security annual recurring revenue hit USD 4.8 billion, advancing 37% as customers consolidate point products. These incumbents converge isolation, secure web gateway, and data loss prevention to boost stickiness.

Specialists sustain premium valuations; Island raised USD 250 million at a USD 4.8 billion valuation, framing its enterprise browser as a lighter alternative to traditional virtual desktop infrastructure. Menlo Security surpassed USD 100 million in annual recurring revenue, propelled by a federal contract that covers classified and unclassified networks. Differentiation hinges on rendering technique, AI-driven threat analytics, and the breadth of pre-integrated compliance templates.

Partner ecosystems matter. Telecom operators white-label RBI to complement managed SD-WAN, while MSSPs bundle it with incident-response retainers. Vendors court hardware OEMs to embed isolation agents at the firmware layer, anticipating a wave of secure-browser-first laptops. Consolidation looms as platforms acquire specialty players to widen features and shorten RandD cycles, signaling an eventual transition toward fewer, full-stack providers.

Browser Isolation Industry Leaders

Cisco

Bitdefender

Proofpoint

Citrix Systems, Inc.

Broadcom (Symantec)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Menlo Security completed a USD 100 million Series E led by Vista Equity Partners, valuing the company at USD 800 million and reporting 155% annual recurring-revenue

- September 2024: Zscaler disclosed FY-2024 revenue of USD 2.17 billion, a 34% rise year on year, attributing a portion of the expansion to integrated browser isolation services.

- August 2024: Palo Alto Networks projected stronger annual results following elevated demand for cloud-delivered security that includes RBI functionality.

- April 2024: Island secured USD 175 million in Series D funding at a USD 3 billion valuation, earmarking capital to position the browser as the centerpiece of enterprise security.

Global Browser Isolation Market Report Scope

Browser isolation is a security method that confines browsing activities to a secure, remote environment to protect users from potentially malicious websites and web content applications.

Browser isolation market is segmented by enterprise size (large enterprises and SMEs), end-user industry (BFSI, government, IT & telecom, manufacturing), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| Cloud-based |

| On-premises |

| Hybrid |

| Remote Browser Isolation (RBI) |

| Client-side / Local Isolation |

| Air-gapped / Hardware-assisted Isolation |

| BFSI |

| Government and Defense |

| IT and Telecom |

| Healthcare and Life Sciences |

| Manufacturing |

| Education |

| Retail and eCommerce |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By Deployment Mode | Cloud-based | ||

| On-premises | |||

| Hybrid | |||

| By Isolation Approach | Remote Browser Isolation (RBI) | ||

| Client-side / Local Isolation | |||

| Air-gapped / Hardware-assisted Isolation | |||

| By End-User Industry | BFSI | ||

| Government and Defense | |||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Education | |||

| Retail and eCommerce | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected browser isolation market size in 2031?

The browser isolation market size is forecast to reach USD 7.65 billion by 2031 on a 24.74% CAGR.

Which enterprise segment is growing the fastest?

SMEs expand at a 28.86% CAGR as cloud delivery and simple licensing reduce barriers to entry.

Why is remote browser isolation gaining preference over client-side methods?

RBI renders web content in the cloud, eliminating local code execution and simplifying device management, which improves security and operational efficiency.

How do Zero Trust regulations influence adoption?

Mandated architectures require strict web-access controls; RBI satisfies the “never trust, always verify” principle and helps meet breach-notification timelines.

Page last updated on: