Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Remote Integration Solutions Market is Segmented by Application (Sports Broadcasting, News and Live Events, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Component (Transmitters, Receivers, and More), Deployment Model (On-Premise, Cloud-Based, and Hybrid), Connectivity Technology (Fiber IP, Satellite, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

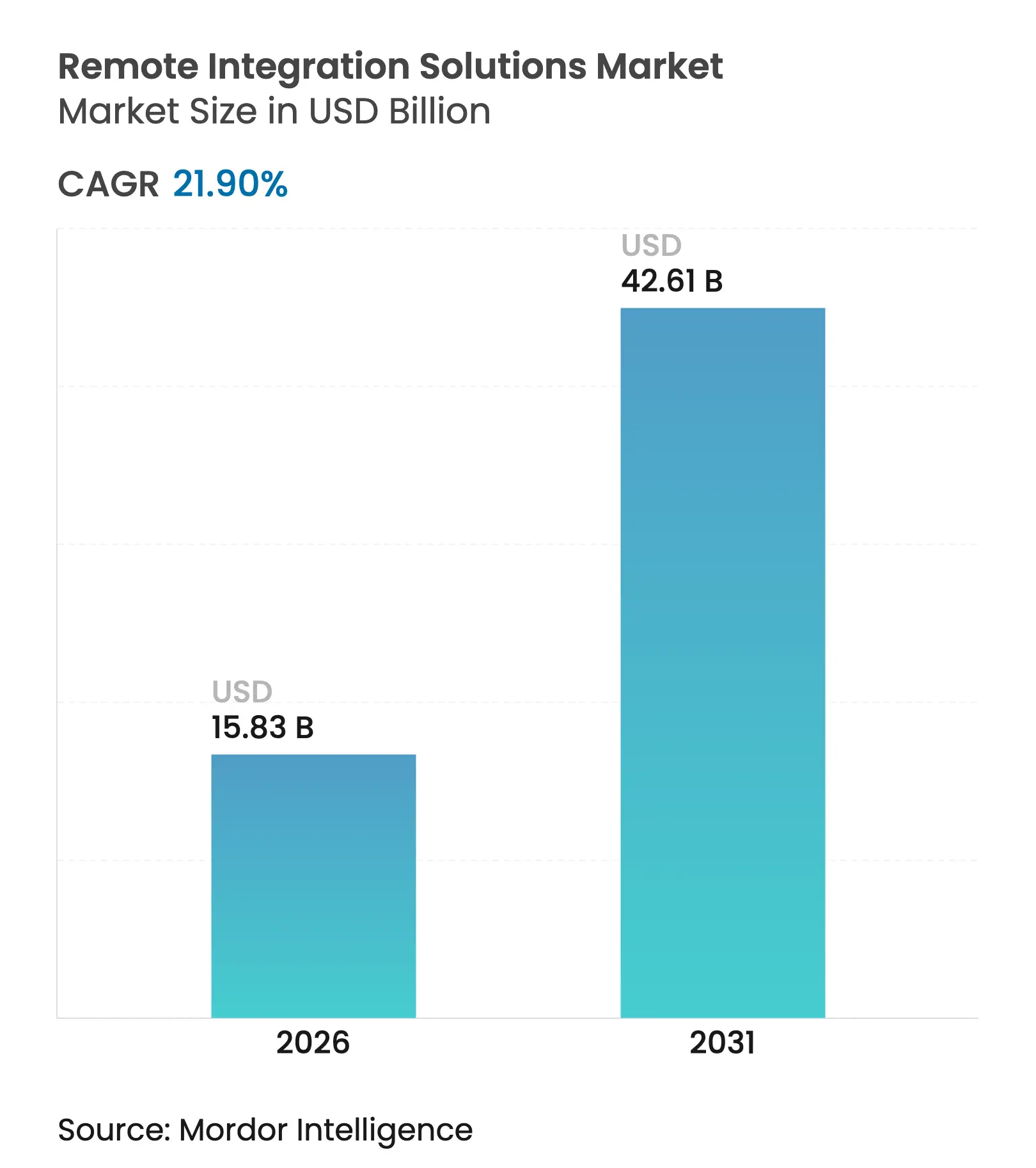

| Market Size (2026) | USD 15.83 Billion |

| Market Size (2031) | USD 42.61 Billion |

| Growth Rate (2026 - 2031) | 21.90 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Remote Integration Solutions Market size is expected to grow from USD 12.99 billion in 2025 to USD 15.83 billion in 2026 and is forecast to reach USD 42.61 billion by 2031 at 21.9% CAGR over 2026-2031. This sharp rise stems from broadcasters replacing on-site production with IP workflows that cut travel, equipment trucking, and set-up costs. Rapid 5G standalone rollouts, proven network-slicing pilots, and software-defined production tools continue to validate the economic case for scalable REMI operations. Live-sports rights holders insist on multi-angle, personalized feeds, which lift demand for remote switching, graphics, and audio mixing nodes that can be spun up instantly in the cloud. The widening 4K and 8K content pipeline raises bandwidth and compute needs and further tips the balance toward IP-centric infrastructure. North America leads adoption thanks to extensive fiber backbones and private 5G deployments, while Asia-Pacific is sprinting ahead on the back of aggressive carrier capex and an expanding calendar of eSports and regional sports leagues.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing live-sports streaming demand Growing live-sports streaming demand | +4.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+4.2% | Geographic Relevance:Global, with concentration in North America and Europe | Impact Timeline:Medium term (2-4 years) |

Acceleration of remote and cloud production cost savings Acceleration of remote and cloud production cost savings | +5.8% | Global, strongest in APAC and North America | Short term (≤ 2 years) | |||

Proliferation of big-data driven broadcast workflows Proliferation of big-data driven broadcast workflows | +3.1% | North America and EU, expanding to APAC | Long term (≥ 4 years) | |||

Expansion of 4K/8K UHD content pipelines Expansion of 4K/8K UHD content pipelines | +3.9% | Global, led by North America and East Asia | Medium term (2-4 years) | |||

Edge-enabled 5G network slicing for REMI Edge-enabled 5G network slicing for REMI | +4.7% | APAC core, spill-over to North America and EU | Medium term (2-4 years) | |||

Sustainability mandates lowering on-site OB units Sustainability mandates lowering on-site OB units | +2.3% | EU leading, followed by North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Live-Sports Streaming Demand

Live-sports audiences expect multi-camera replays, enriched stats, and near-zero latency, forcing rights holders to spin up parallel feeds that only IP-based REMI architectures can sustain. Deutsche Telekom’s private 5G slice for RTL Deutschland delivered 4K pictures at sub-25 ms latency during the European Football Championship, illustrating carrier readiness to support broadcast-grade streams. [1]Deutsche Telekom AG, “Telekom and RTL Deutschland Develop 5G Standalone Network Slicing Solution for Live Video Production,” telekom.com Virgin Media O2’s eSports showcase proved that the same architecture can flex across entertainment genres. These rollouts validate cellular contribution as a complement to fiber and satellite, unlocking venue choice and lowering first-mile costs for tournaments of every scale.

Acceleration of Remote and Cloud Production Cost Savings

LiveU, TVU Networks, and other service providers report 40-70% expense reductions when productions pivot from full OB truck deployments to REMI pipelines that centralize switching, replay, and graphics. [2]LiveU, “Remote Production,” liveu.tv ESPN, faced with 16 NHL playoff games over six days, combined REMI trucks with cloud vision-mixing to stretch crews and equipment across multiple sites. Cloud resource pooling improves asset utilization, while pay-as-you-go pricing lets mid-tier broadcasters gain access to professional toolsets once limited to tier-one networks.

Proliferation of Big-Data Driven Broadcast Workflows

Artificial-intelligence overlays, real-time player tracking, and live language translation turn a single camera feed into a data-rich product. wTVision’s AI engine detects ball trajectories and auto-generates advanced graphics, yet it depends on low-latency compute nodes that sit upstream of the vision mixer. Murata’s generative commentary prototype unlocks long-tail sports coverage that human crews cannot economically justify. These innovations expand the addressable market for remote integration solutions that merge video and data workflows in one control layer.

Expansion of 4K/8K UHD Content Pipelines

Ultra-HD demands quadruple the throughput of HD and magnifies storage as well as graphics-processing loads, straining legacy SDI chains. intoPIX’s visually-lossless TicoXS codec enables 8K transport over 10 GbE links, lowering the barrier to campus-wide 8K REMI deployments. China Mobile streamed a 4K awards show exclusively over a 5G slice, accomplishing contribution and distribution without satellite back-up. As audiences come to expect 4K on every screen, remote integration workflows become the pragmatic path to scale, sidestepping large capital outlays for dedicated UHD trucks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High-capacity, low-latency bandwidth pricing High-capacity, low-latency bandwidth pricing | -3.8% | Global, most acute in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-3.8% | Geographic Relevance:Global, most acute in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Legacy infrastructure and skill-set inertia Legacy infrastructure and skill-set inertia | -2.9% | North America and EU, moderate in APAC | Medium term (2-4 years) | |||

Cyber-security vulnerabilities in IP feeds Cyber-security vulnerabilities in IP feeds | -1.8% | Global, heightened in regulated industries | Short term (≤ 2 years) | |||

Regulatory spectrum allocation delays Regulatory spectrum allocation delays | -1.2% | Regional, varying by jurisdiction | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High-Capacity, Low-Latency Bandwidth Pricing

Dedicated gigabit-class access often costs USD 1,000-1,500 per month, a material hurdle for regional stations and independent producers. [3]Meter, “Dedicated Internet Access Pricing Guide for 2025,” meter.com Supply-chain shocks have already nudged operators from just-in-time to just-in-case hardware procurement, keeping network equipment prices elevated. Connectivity remains concentrated in urban nodes, obliging remote creators to rely on satellite or public internet that rarely guarantees frame-accurate delivery. While carriers study slicing monetization, Ericsson forecasts payback periods stretching up to five years, tempering near-term relief.

Legacy Infrastructure and Skill-Set Inertia

Many broadcasters invested heavily in SDI routers and coaxial cabling less than a decade ago and now hesitate to abandon sunk assets. IP media networks require precision-time-protocol synchronization and software-defined routing skills rarely found in classic broadcast engineering teams. Transitional hybrids force dual-path maintenance and elongate change-management timelines. Smaller houses fear reliability trade-offs, preferring proven baseband until IP tools demonstrate bulletproof performance in marquee events.

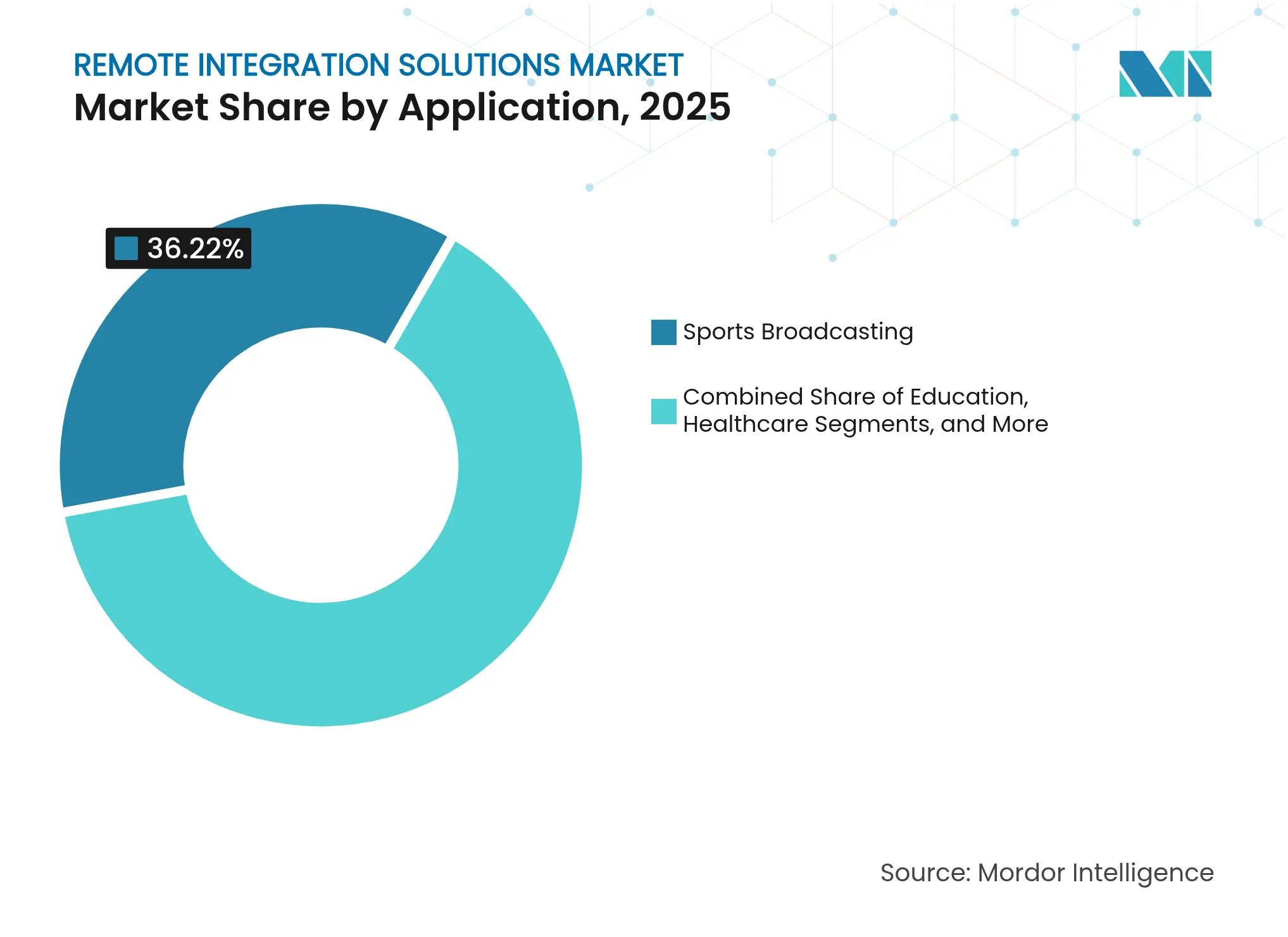

By Application: Sports Broadcasting Drives Market Leadership

Sports broadcasting held 36.22% of the remote integration solutions market share in 2025, a testament to the segment’s relentless requirement for multiple synchronized camera feeds, slo-motion replays, and graphics-heavy storytelling. TNT Sports opted for a full REMI workflow for its MLB Tuesday slate to stretch crews across ballparks and headquarters control rooms. The remote integration solutions market size for sports was bolstered by rights fees that incentivize efficiency without compromising fan experience.

News and live events post the fastest 24.25% CAGR to 2031 as rolling coverage, pop-up studios, and multi-platform publishing demand agile production. Political debates, red-carpet shows, and crisis briefings lean on REMI to cut set-up times and enable cross-border collaboration. As audience attention shifts in minutes, cloud-native editing tools allow producers to push highlights to social channels inside the golden hour, widening reach with minimal incremental cost.

Note: Segment shares of all individual segments available upon report purchase

By Organization Size: Large Enterprises Maintain Dominance

Large enterprises controlled 65.55% revenue in 2025, leveraging central technical operations centers that orchestrate dozens of concurrent feeds. These firms negotiate volume discounts for encoders, network services, and cloud compute, lowering per-event cost curves. They also assign dedicated teams to monitor latency, redundancy, and cybersecurity across high-stakes live shows.

SMEs gain momentum with a 24.65% CAGR as SaaS platforms package vision-mixing, graphics, and intercom in browser-based consoles. Portable all-in-one production tablets let a two-person crew switch a six-camera shoot and output professional-grade streams, closing capability gaps with premium broadcasters. The remote integration solutions industry now counts boutique sports leagues, houses of worship, and universities among active buyers.

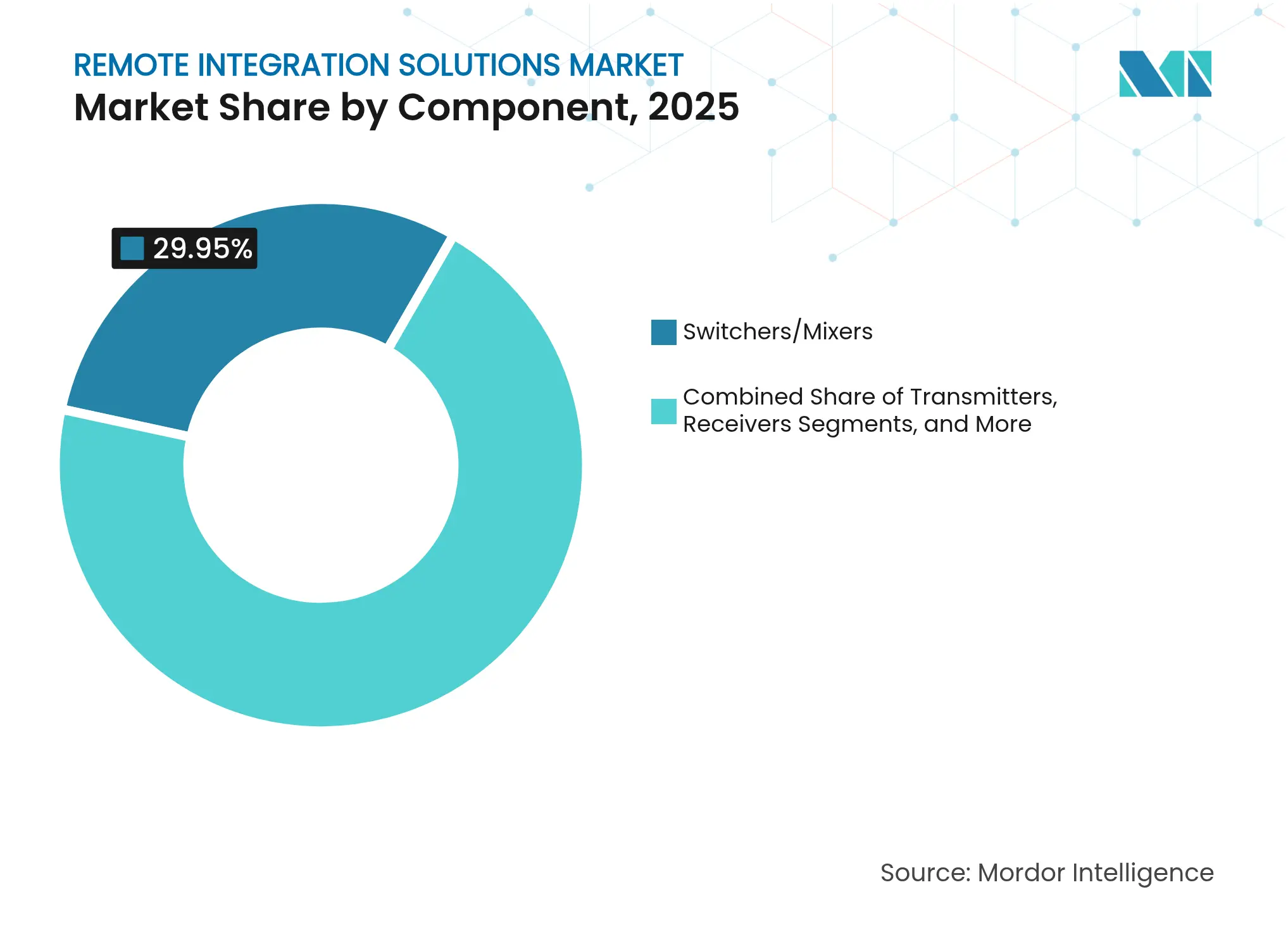

By Component: Software Platforms Drive Innovation

Switchers and mixers retained a 29.95% share in 2025 as the fundamental node that blends cameras, graphics, and replays in real time. Hardware reliability still matters for tent-pole events, yet vendors increasingly expose REST APIs that let these switchers plug into orchestration layers.

Software platforms record the quickest 23.92% CAGR, propelled by microservices that abstract ingest, processing, and distribution. Cloud NLEs tie directly into ingest pipelines, trimming turnaround from hours to minutes. The remote integration solutions market size allocated to software accelerates as broadcasters redirect capex from fixed FPGA boards to subscription-based editorial suites.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Model: Cloud Migration Accelerates

On-premise systems held a 49.85% share in 2025, reaffirming the industry’s cautious approach to latency-sensitive workloads. News networks continue to house master-control rooms and archive clusters behind the firewall, citing editorial sovereignty.

Cloud deployments, however, chart a 24.98% CAGR. Hybrid schemes route delay-tolerant tasks—such as file ingest, closed-caption generation, and archival transcoding—to elastic compute while preserving frame-accurate switching on site. Verizon’s portable private 5G kit, paired with NVIDIA edge AI, shortens the gap between on-prem and cloud response times, legitimizing new workloads at the network edge.

By Connectivity Technology: Cellular Networks Gain Momentum

Fiber IP lines delivered a 39.10% share in 2025, prized for their consistent 1 Gbps uplink and deterministic latency. That said, mid-event venue changes often render fixed fiber impractical. Cellular and 5G links sprint ahead at a 25.28% CAGR. Ericsson and Deutsche Telekom’s pop-up 5G SA network for the European Championship streamed wireless camera feeds at 500 Mbps with flawless synchronization. Hybrid bonding units now aggregate multiple 5G sims with public internet, furnishing a safety net during fiber outages.

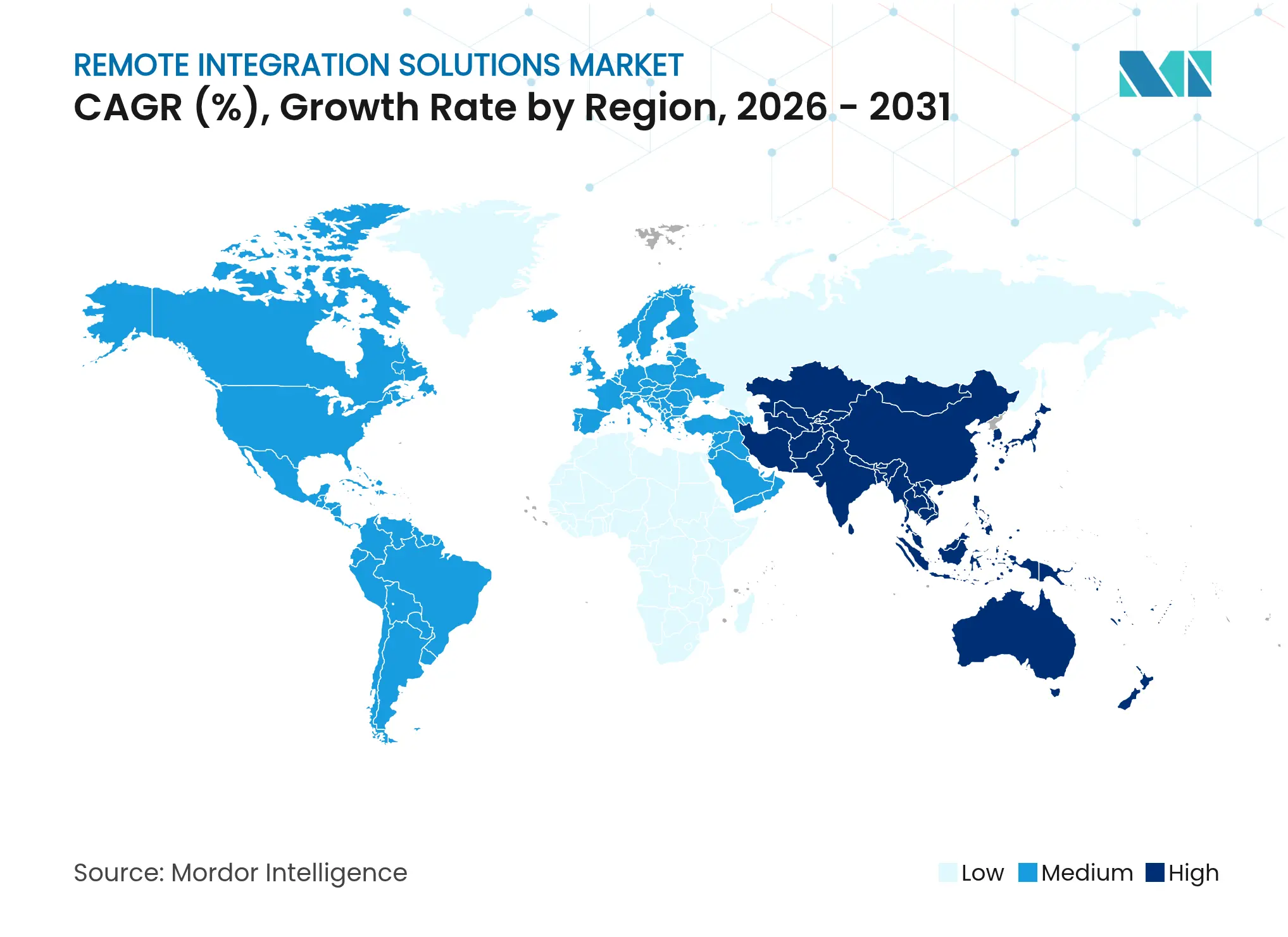

North America held 36.10% of the remote integration solutions market share in 2025 on the strength of dense fiber infrastructure, liberal spectrum policies, and sports leagues that continually pilot production advances. ESPN, Fox Sports, and regional networks have institutionalized REMI workflows, creating a robust ecosystem of system integrators and freelance operators. Verizon’s private 5G and ATSC 3.0 Broadcast Internet trials signal further momentum as operators seek new monetization layers. Government grants for rural broadband also widen the addressable client base, unlocking local news stations previously constrained by DSL or microwave hops.

Asia-Pacific is the fastest-growing territory, advancing at 24.32% CAGR through 2031. National carriers in Japan, South Korea, and China have leapfrogged to 5G standalone cores, paving the way for guaranteed-slice SLAs aimed specifically at media clients. Expereo notes a surge in data-center interconnect builds across Singapore and Hong Kong as content hubs shift closer to viewers. The remote integration solutions market size for APAC is further boosted by eSports producers that stream multilingual tournaments to massive mobile audiences.

Europe exhibits steady uptake, bolstered by strong public-service broadcasters and policy mandates to curb carbon footprints. Telefónica and RTVE’s truck-less field trial underscores how edge compute can eliminate miles of diesel travel while keeping creative control intact. Sustainability goals align with remote production benefits, and the continent’s tight data-protection rules drive interest in hybrid architectures that localize sensitive feeds before pushing proxies to the cloud. Emerging markets in Latin America, the Middle East, and Africa show green-shoot projects as submarine-cable expansions, and LEO satellite constellations bridge connectivity gaps, positioning them for accelerated adoption.

Market Concentration

The remote integration solutions market is moderately fragmented, with roughly two dozen vendors controlling the bulk of revenue. LiveU, Haivision, and TVU Networks leverage decade-long track records across Tier-1 sports, giving them brand trust and global reseller channels. Cloud-native challengers such as Amagi and Kiswe pitch OPEX-friendly models that bundle switching, graphics, and distribution in a single interface.

Acquisition activity is brisk. Acuity Brands’ USD 1.2 billion purchase of QSC folds networked audio and control into a wider intelligent-spaces play, broadening competitive fronts beyond pure broadcast. Avid’s buy-out of Wolftech adds newsroom story-planning in the cloud, evidencing a shift to vertically integrated editorial stacks.

Technology differentiation hinges on latency and codec efficiency. intoPIX, Ateme, and Bitmovin race to deliver perceptually lossless compression that squeezes UHD over commodity links. Meanwhile, patents for virtual collaboration hint at future volumetric or XR production layers, with Meta already securing intellectual property around wireless sidelink streams. Partnerships also multiply: Vislink certifying its DragonFly V encoder on Ericsson’s private 5G underscores how handset-era telecom gear is being refactored for broadcast missions.

Price competition is tempered by high switching costs and customers’ aversion to production risk. Vendors lock in clients through integrated control surfaces, proprietary bonding algorithms, and managed service overlays. Still, transparency on cloud egress fees and slice pricing is emerging as a key buying criterion for mid-market producers who must forecast per-event margins with accuracy.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

A modern form of video broadcasting is Remote Integration (REMI), in which only small capture assets, such as Cameras and Microphones, are installed in the field. The principle behind REMI is to control costly capital in the area to minimize production costs. On-demand online streaming and broadcasting content providers develop an intensive market for conventional broadcasters. Conventional networks are looking to cover community sports and live activities to counter this and to have more options and personalized content for audiences.

The remote integration market is segmented by application (sports, broadcast, government, and healthcare), by type (large enterprise and SME), by products (transmitters, switches, decoders, accessories, and receivers), by geography (North America, Europe, Asia-Pacific, Latin America, Africa & Middle East).

The market sizes and forecasts are provided in terms of value USD for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.