Remote Monitoring And Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

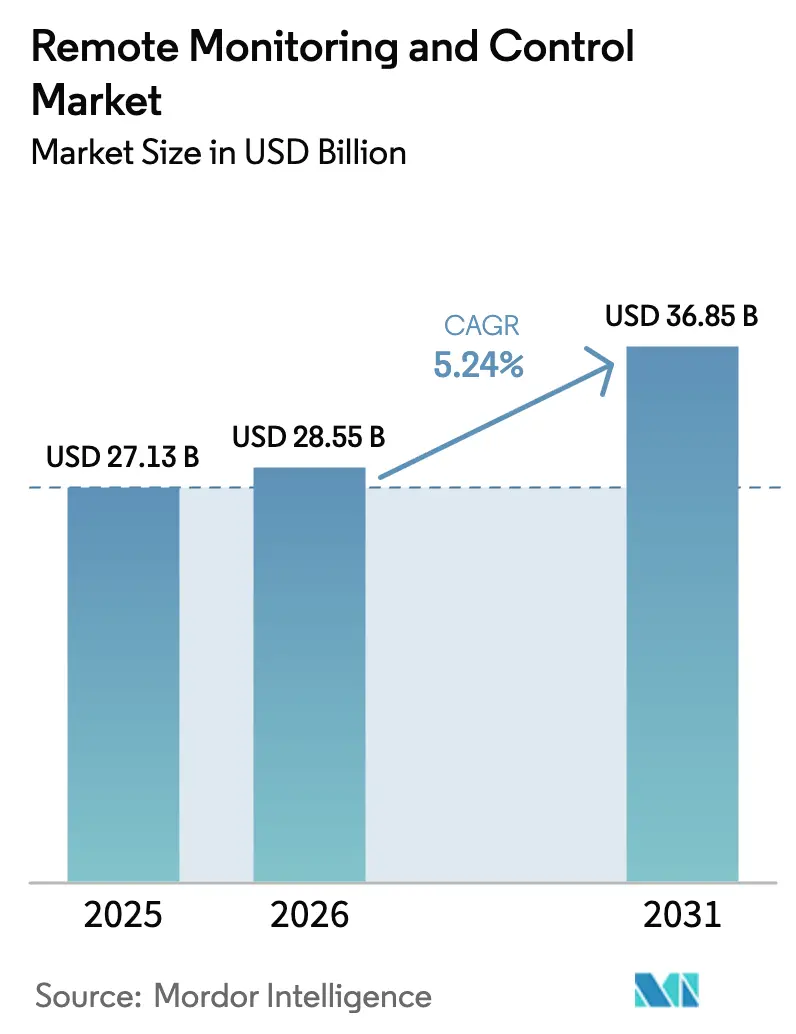

| Market Size (2026) | USD 28.55 Billion |

| Market Size (2031) | USD 36.85 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

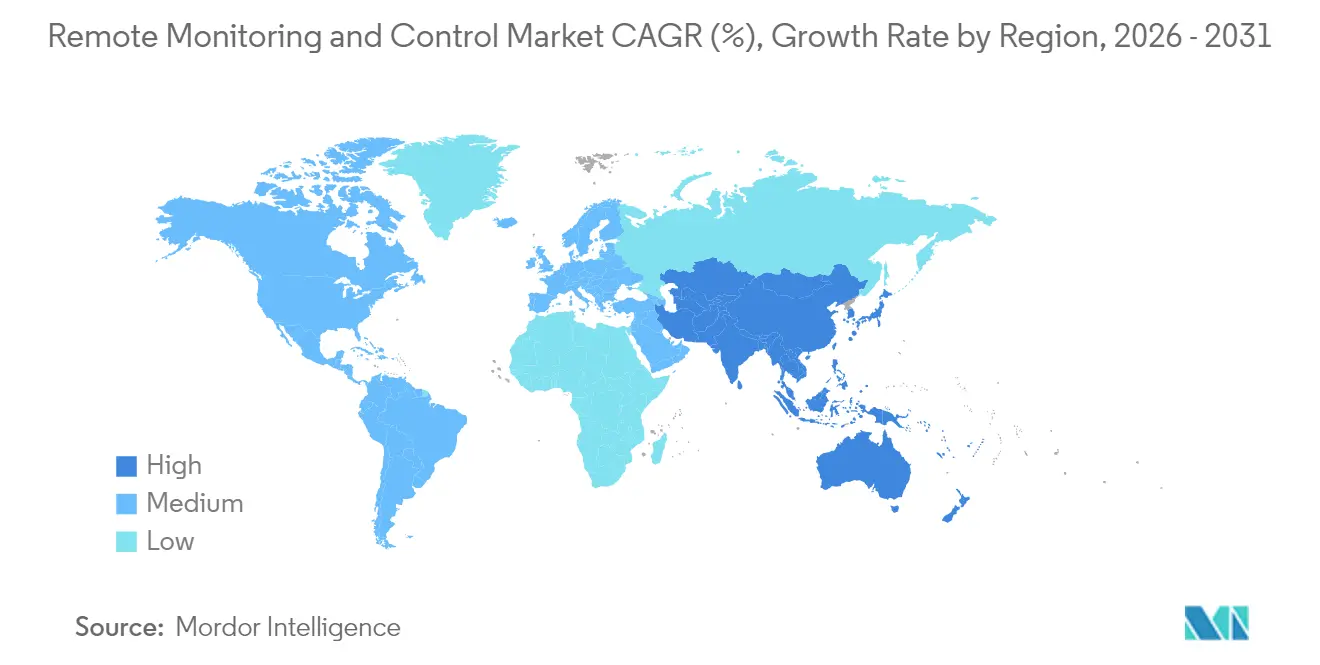

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

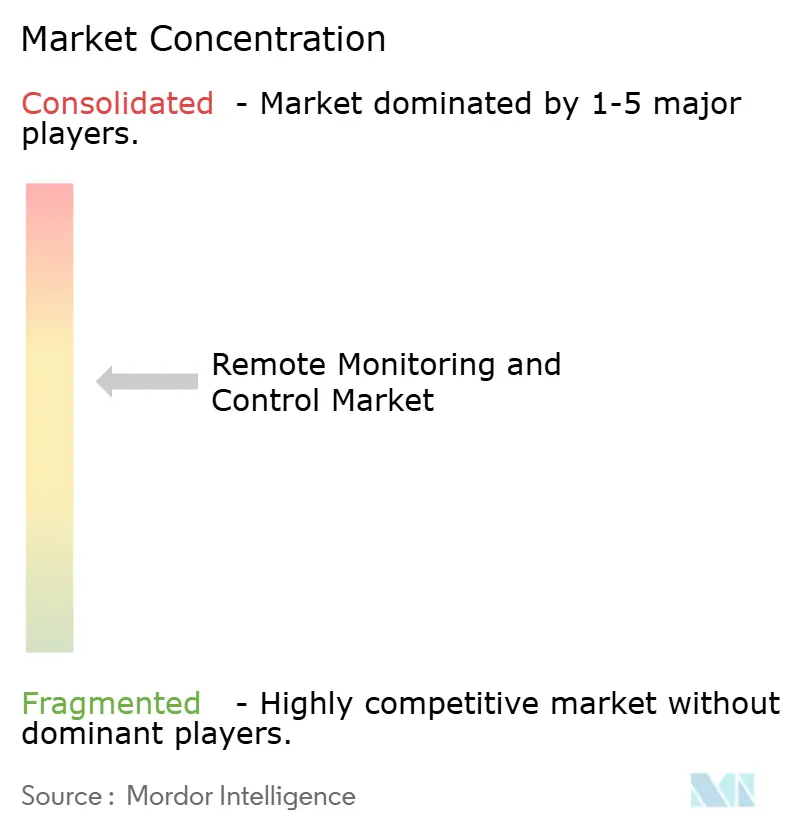

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Remote Monitoring And Control Market Analysis by Mordor Intelligence

The remote monitoring and control market size is expected to grow from USD 27.13 billion in 2025 to USD 28.55 billion in 2026 and is forecast to reach USD 36.85 billion by 2031 at 5.24% CAGR over 2026-2031. Growth reflects the convergence of operational technology and advanced connectivity, stricter carbon-tracking rules, and rising IIoT deployments that cut downtime and maintenance costs. [1]Environmental Protection Agency, “Revisions and Confidentiality Determinations for Data Elements Under the Greenhouse Gas Reporting Rule,” epa.gov Private 5G networks and edge-AI controllers now deliver real-time analytics in hazardous sites, trimming field visits and improving safety. Cloud-native SCADA platforms reduce capital outlay, while subscription pricing opens the technology to smaller operators. Oil and gas keeps the largest user share, but life-science facilities adopt remote monitoring rapidly to meet new FDA digital-device guidance. Regionally, North America leads on the strength of environmental regulations, whereas Asia-Pacific shows the fastest expansion thanks to automation investments and large infrastructure projects.

Key Report Takeaways

- By component, solutions dominated with 59.70% of remote monitoring and control market share in 2025; field instruments are forecast to rise at an 7.86% CAGR through 2031.

- By deployment mode, on-premise systems held 58.05% share of the remote monitoring and control market in 2025, while cloud platforms are advancing at a 9.12% CAGR to 2031.

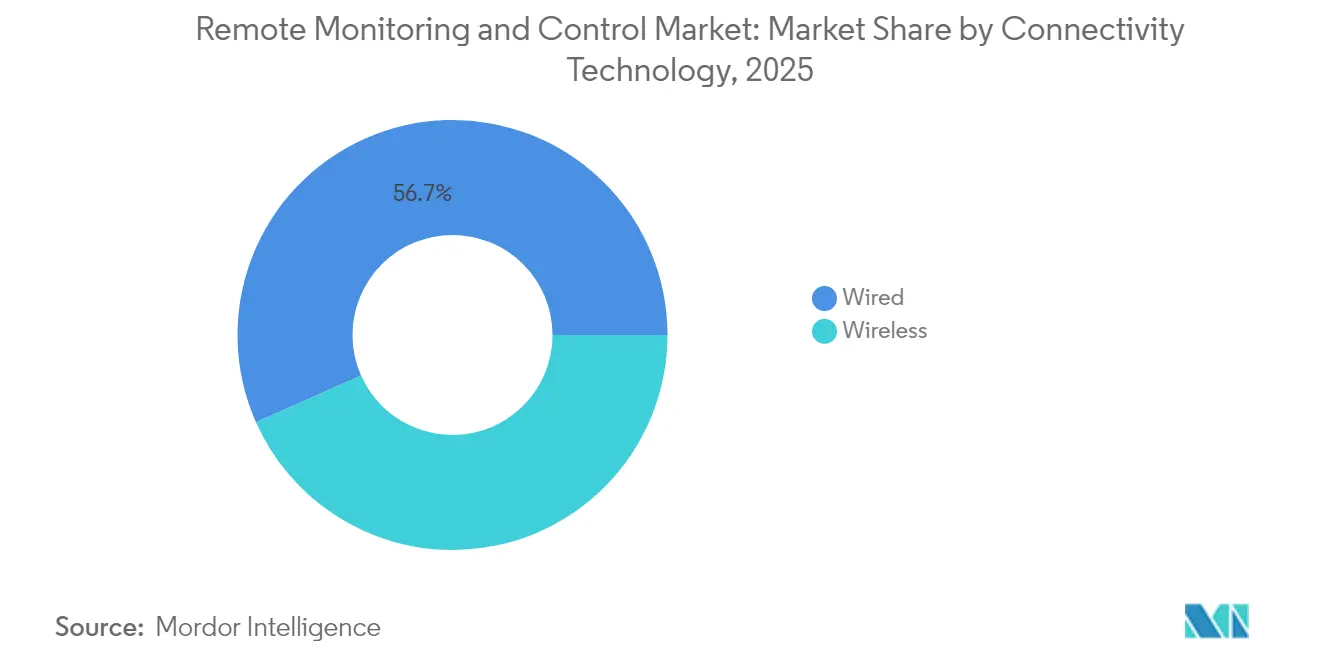

- By connectivity, wired networks accounted for 56.65% share, yet wireless technologies are expanding at an 8.43% CAGR through 2031.

- By end-user industry, oil and gas led with 22.05% revenue share in 2025; pharmaceuticals and life sciences are projected to grow at a 7.38% CAGR to 2031.

- By geography, North America commanded 33.85% of the remote monitoring and control market size in 2025, while Asia-Pacific is set to expand at an 7.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Remote Monitoring And Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for industrial automation | +1.2% | Global; strongest in APAC and North America | Medium term (2-4 years) |

| Increasing use of industrial mobility and remote management | +0.8% | Global; concentrated in oil and gas and mining regions | Short term (≤ 2 years) |

| Expanding IIoT-enabled predictive maintenance programs | +1.0% | North America and EU lead; APAC adoption accelerating | Medium term (2-4 years) |

| Proliferation of edge-AI controllers in hazardous sites | +0.7% | Global; early uptake in developed markets | Long term (≥ 4 years) |

| Stricter carbon-tracking regulations needing real-time data | +0.9% | North America and EU primary; expanding to APAC | Short term (≤ 2 years) |

| Emerging private-5G networks for ultra-reliable low-latency links | +0.6% | Global; industrial clusters leading deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for industrial automation

Manufacturers view automation as a primary lever for offsetting labor shortages and boosting throughput. Private 5G networks built by Rockwell Automation and Nokia support real-time control over Citizens Broadband Radio Service spectrum, enabling autonomous operations in discrete and process plants. [2]Rockwell Automation, “Digital Transformation through 5G Standalone (SA),” rockwellautomation.com Collaborative robots, AI vision, and predictive analytics now run side-by-side on unified platforms, letting operators re-configure production lines with minimal downtime. The result is lower cost per unit and safer work environments. Similar benefits appear in mining and petrochemical facilities where wireless sensors alert technicians before a fault escalates. Companies that delay adoption risk competitive erosion as peers capture savings from faster cycle times and reduced scrap.

Expanding IIoT-enabled predictive maintenance programs

FactoryTalk Analytics Guardian AI uses machine-learning models at the asset layer to catch anomalies early, extending equipment life and shrinking spare-parts inventories. [3]Rockwell Automation, “Advancements in Predictive Maintenance & the IIoT,” rockwellautomation.com Edge computing allows vibration and temperature data to be processed locally, cutting cloud bandwidth and providing instant feedback for maintenance crews. In harsh mining locations, wireless gateways stream health metrics from haul-truck drivetrains, enabling just-in-time service that maximizes fleet availability. Manufacturers similarly track spindle wear on CNC machines, avoiding costly unplanned shutdowns. Across industries, these programs translate into consistent OEE improvements and measurable ROI within one budget cycle.

Proliferation of edge-AI controllers in hazardous sites

Autonomous robots now drill and haul ore while transmitting real-time telemetry that protects workers from blast zones. Edge-AI vision systems watch for gas leaks on offshore rigs and trigger automatic shutdowns in seconds. Battery-backed processors onboard each device ensure continuity if connectivity drops, meeting safety-integrity targets. Vendors have bundled AI chips inside smart cameras, removing the need for bulky servers in explosive areas. The technology also feeds compliance reports automatically, easing audit workloads. As costs decline, adoption is shifting from pilot projects to multi-site rollouts in chemicals, power, and logistics.

Stricter carbon-tracking regulations needing real-time data

The EPA’s updated Greenhouse Gas Reporting Rule makes continuous emissions monitoring mandatory for facilities emitting 25,000 metric tons of CO₂e or more. Oil and gas producers have begun replacing manual checks with laser-based sensors that capture methane leaks every second. TotalEnergies targets a 60% methane-emission cut by 2025, using cloud-linked detectors that sync with existing SCADA layers. Automated logs help verify compliance and avoid penalties, while also revealing energy-efficiency opportunities. The result is a dual benefit of regulatory certainty and operating-cost reduction, reinforcing the business case for real-time monitoring upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX and complex brown-field integration | -0.8% | Global; particularly affects SMEs in developing markets | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in OT-IT convergence | -0.6% | Global; heightened concerns in critical infrastructure | Medium term (2-4 years) |

| Skilled workforce shortage for multi-vendor platforms | -0.5% | North America and EU most affected; emerging in APAC | Long term (≥ 4 years) |

| Legacy protocol lock-in limiting interoperability | -0.4% | Global; notable in established industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial CAPEX and complex brown-field integration

Retrofitting decades-old pumps, drives, and valves with modern sensors often requires custom gateways and protocol converters. Engineering teams must stage upgrades carefully to keep plants running, lengthening project timelines and inflating budgets. Water utilities upgrading to advanced SCADA face the added burden of mapping thousands of I/O points while maintaining regulatory reporting. These factors delay decision-makers, particularly in resource-constrained municipalities and SMEs, despite clear long-term savings.

Cyber-security vulnerabilities in OT-IT convergence

Connecting previously air-gapped control networks exposes programmable logic controllers to ransomware and phishing attacks. Emerson advocates zero-trust frameworks that authenticate every device and enforce least-privilege policies. Yet many operators lack specialists who understand both IT firewalls and OT protocols. Auditing and patch management remain onerous across multi-vendor environments, which can include gear installed 20 years ago. Budget holders must balance cyber-risk mitigation with production targets, slowing adoption in certain verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Hardware Transition

Solutions accounted for 59.70% of remote monitoring and control market share in 2025, affirming the shift toward software-centric architectures. Cloud dashboards, analytics engines, and cybersecurity modules form the digital backbone that binds diverse field devices. Vendors bundle licensing, updates, and support into subscription plans that trim upfront costs and smooth cash flow. Field instruments, while holding a smaller slice, represent the fastest-growing sub-segment at an 7.86% CAGR. Smart sensors embed microcontrollers that run local diagnostics, easing network traffic and ensuring resilience during link outages. Early adopters report fewer site visits and quicker anomaly detection, which feeds back into efficiency gains.

Field instruments’ rise also signals a broader move to edge intelligence. Devices now host algorithms that once lived on centralized servers, compressing data before transfer and cutting cellular fees. This evolution widens the remote monitoring and control market as firms attach low-cost nodes to legacy pumps, motors, and conveyors. Software publishers, in turn, enhance their platforms with drag-and-drop configuration, helping non-specialists deploy new sensor packs. The combined momentum of smarter hardware and agile software underpins steady expansion of the remote monitoring and control industry across diverse plants and utilities.

By Deployment Mode: Cloud Acceleration Reshapes Infrastructure

On-premise systems kept 58.05% share of the remote monitoring and control market in 2025, reflecting entrenched investment and regulatory data-residency rules. They remain vital where sub-second control loops govern safety-critical processes. Yet cloud deployments are rising at a 9.12% CAGR as firms favor scalability and lower maintenance overhead. Emerson’s DeltaV SaaS SCADA exemplifies this swing by delivering secure browser access and elastic compute for analytics.

Hybrid topologies now blend edge servers for latency-sensitive tasks with cloud layers for long-term optimization. Such designs let operators modernize without discarding sunk-cost assets, accelerating the remote monitoring and control market size expansion. Standardized APIs streamline data export into enterprise resource-planning suites, turning plant metrics into financial dashboards. As 5G coverage broadens, bandwidth constraints ease, making full-cloud control viable even for high-speed production lines.

By Connectivity Technology: Wireless Innovation Drives Transformation

Wired Ethernet and fieldbus links still carry 56.65% of plant traffic thanks to deterministic performance and electromagnetic immunity. However, wireless nodes are gaining fastest at an 8.43% CAGR. LPWAN protocols like LoRaWAN and NB-IoT enable battery-powered sensors to report once every minute for several years, ideal for remote pipelines and tank farms. Private 5G adds gigabit-speed, ultra-reliable links for autonomous haul trucks and collaborative robots.

These breakthroughs extend the remote monitoring and control market into terrains once deemed unreachable. Maintenance crews receive vibration alerts on handheld tablets instead of walking miles to inspect equipment. Meanwhile, mesh topologies self-heal around obstacles, raising uptime. Interoperability standards such as OPC UA FX over TSN reduce lock-in fears, broadening adoption across conservative industries.

By End-User Industry: Oil and Gas Leadership Faces Pharmaceutical Challenge

Oil and gas retained 22.05% of revenue in 2025, driven by pipeline integrity, flare management, and offshore platform surveillance. Electro-hydraulic valves and all-electric subsea trees from Baker Hughes supply granular process control while cutting hydraulic leakage risks. Yet pharmaceuticals and life sciences now outpace others at a 7.38% CAGR as FDA guidance for AI-enabled devices pushes plants toward continuous environmental monitoring.

Regulated cleanrooms demand constant logging of temperature, humidity, and airborne particles. Remote dashboards flag deviations instantly, reducing batch rejections and safeguarding patient safety. These strict requirements enlarge the remote monitoring and control market size among life-science firms. Utilities, chemicals, and food processors also expand spend to meet traceability rules and sustainability targets, diversifying vendor revenue streams and cushioning sector dependence on hydrocarbons.

Geography Analysis

North America led the remote monitoring and control market with 33.85% share in 2025, anchored by the United States’ stringent emissions legislation and broad IIoT maturity. Federal infrastructure funds stimulate upgrades in water and wastewater utilities, while shale operators fit methane-detection arrays to comply with the 2025 EPA rule. Canada augments demand through carbon price mechanisms that reward real-time energy analytics. Mexico’s automotive clusters digitalize assembly lines to maintain export competitiveness, ensuring steady regional inflows for solution providers.

Asia-Pacific, projected to rise at an 7.95% CAGR, benefits from China’s smart-manufacturing subsidies and India’s production-linked incentive schemes. Semiconductor fabs in Taiwan and South Korea deploy private 5G to orchestrate mobile robots, while Australian miners automate haulage in remote deserts. ASEAN nations invest in smart-city water grids that rely on cloud SCADA to minimize leakage. This diverse set of projects expands the remote monitoring and control market footprint across developing and advanced economies alike.

Europe records consistent uptake as companies chase Green Deal targets and adopt predictive maintenance to offset high energy costs. German automotive OEMs retrofit legacy lines with edge gateways, whereas UK utilities adopt SaaS SCADA to modernize century-old networks under tight budgets. The Middle East leverages oil revenue to digitize gas processing trains, and South Africa pilots smart-grid telemetry in mining towns. Together, these efforts highlight a global demand curve that is both geographically widespread and use-case specific.

Competitive Landscape

The competitive arena remains moderately concentrated. Multinationals such as ABB, Siemens, Schneider Electric, Emerson, Honeywell, and Yokogawa offer end-to-end stacks spanning sensors to analytics. Their global service arms and deep domain expertise keep switching costs high. To defend share, incumbents acquire niche software firms that add AI engines, cybersecurity modules, or cloud orchestration features. Siemens, for instance, unveiled the Simatic Automation Workstation, which shifts PLC logic into a virtualized environment and reduces hardware SKUs.

Challengers such as Inductive Automation and ICONICS court mid-tier manufacturers with browser-based tools that deploy in hours rather than months. Subscription pricing resonates with CFOs wary of large capital layouts. Partnerships between automation vendors and telecom carriers further reshape value chains; private 5G offerings bundle radios, SIMs, and remote-monitoring apps under one SLA. This convergence blurs traditional product boundaries and intensifies feature wars around latency, cybersecurity, and scalability.

White-space opportunities appear in pharmaceutical cleanroom monitoring, edge-AI video analytics for worker safety, and microgrid optimization for renewable assets. Vendors able to certify solutions under multiple regulatory regimes hold an edge. Meanwhile, the shift to zero-trust security drives demand for integrated identity management across PLCs and cloud APIs, rewarding firms with proven frameworks. As ecosystems mature, differentiation will hinge less on hardware specs and more on software agility and lifecycle services.

Remote Monitoring And Control Industry Leaders

ABB Ltd.

Emerson Electric Co.

Honeywell International Inc.

Schneider Electric SE

General Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Siemens introduced the software-based Simatic Automation Workstation, first deployed at Ford manufacturing plants.

- March 2025: City of Denison allocated USD 4 million to replace legacy remote water-monitoring products with a modern SCADA system.

- February 2025: Siemens Mobility secured a EUR 2.8 billion (USD 3.0 billion) contract with Deutsche Bahn for long-term control and safety technology.

- February 2025: Baker Hughes launched SureCONTROL Plus interval control valves and all-electric subsea production systems for remote offshore operations.

- January 2025: Siemens expanded its industrial-grade private 5G infrastructure to support up to 24 radio units covering around 5,000 m² each.

- January 2025: Siemens Mobility won four contracts worth EUR 670 million (USD 720 million) with HS2 Ltd for real-time train control and monitoring.

- December 2024: TAQA Water Solutions announced a USD 26 million SCADA project integrating 2,000+ sensors across Abu Dhabi water infrastructure.

- December 2024: Goodman Fielder rolled out Inductive Automation SCADA and Sepasoft MES at three bakeries for quality management.

- December 2024: Delta IABG signed 2025 cooperation contracts with channel partners in Taiwan, targeting IIoT and smart manufacturing.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study views the remote monitoring and control market as all hardware, software, and connected sensor networks that let operators watch, diagnose, and adjust industrial assets from a distance, most often through SCADA platforms, vibration-analysis tools, and smart transmitters that feed data to cloud or on-premise dashboards. Values are expressed in constant 2025 US dollars and cover solutions and field instruments installed in discrete and process industries worldwide.

Scope Exclusions: mobile consumer wearables, purely IT network observability tools, and post-install maintenance contracts are left outside this assessment.

Segmentation Overview

- By Component

- Solutions

- Field Instruments

- By Deployment Mode

- On-premise

- Cloud

- By Connectivity Technology

- Wired

- Wireless

- By End-user Industry

- Oil and Gas

- Power Generation and Utilities

- Chemicals and Petrochemicals

- Metals and Mining

- Water and Wastewater

- Food and Beverages

- Pharmaceuticals and Life Sciences

- Pulp and Paper

- Semiconductor and Electronics

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviews plant engineers, automation-system integrators, and regional distributors across North America, Europe, and fast-industrializing Asian economies. These conversations test preliminary market totals, surface real-world adoption barriers, and refine penetration assumptions for cloud deployments and wireless nodes, ensuring our narrative stays anchored to current shop-floor realities.

Desk Research

We begin by mapping production footprints and installed-base trends using public datasets such as United Nations Comtrade export codes for pressure and level transmitters, OECD manufacturing output indices, and International Energy Agency plant capacity files. Next, we mine authoritative association portals, including the International Society of Automation, American Water Works Association, and World Steel Association, for commissioning statistics, standards updates, and retrofit rates that shape equipment turnover. Company 10-Ks, investor decks, and D&B Hoovers snapshots round out revenue splits and average selling prices, while Questel patent analytics signal emerging sensor designs that influence our forecast price curve.

Statistical releases from the US Energy Information Administration and Eurostat, complemented by Dow Jones Factiva news flows, let Mordor analysts cross-check shipment pulses with project announcements. The sources above illustrate our desk-research base; many additional public and paid references are consulted throughout validation.

Market-Sizing & Forecasting

A top-down build starts with sectoral capex and replacement cycles to size the demand pool, which is then pressure-tested through sampled ASP × unit roll-ups from key vendors. Variables that move the model include refinery turnaround schedules, municipal water stimulus outlays, industrial IoT gateway shipments, average sensor price erosion, and regional labor-cost differentials that sway remote-operations ROI. A multivariate regression, updated annually, blends these drivers with macro indicators to project values through 2030. Where bottom-up totals diverge materially, we iterate assumptions before locking the baseline.

Data Validation & Update Cycle

Outputs pass a three-layer review: model variance scan, analyst peer check, and senior sign-off. We refresh every twelve months, with mid-cycle updates if plant-shutdown waves, major currency swings, or step-change regulations alter demand signals. Clients therefore receive the latest vetted view.

Why Mordor's Remote Monitoring & Control Baseline Figures Stand Firm

Published estimates often differ because firms pick contrasting scopes, currencies, and refresh cadences. Component mix (solutions versus field instruments), inclusion of aftermarket services, and the year chosen as the anchor all sway totals.

Key gap drivers here relate to whether agricultural telemetry, retrofit software, or Asia-Pacific greenfield projects are counted, and to how aggressively price-compression is modeled beyond 2027. Mordor aligns scope to equipment that ships with an industrial control objective, applies rolling five-year ASP decay verified by distributors, and updates the base each June, which competitors rarely match.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.13 Bn (2025) | Mordor Intelligence | - |

| USD 24.98 Bn (2025) | Regional Consultancy A | Narrower field-instrument coverage and static price deck |

| USD 28.60 Bn (2024) | Global Forecast Service B | Includes aftermarket services and uses 2024 currency without inflation restatement |

| USD 24.60 Bn (2022) | Industry Journal C | Early base year extrapolated linearly, omits Asia-Pacific process plants |

In short, when scope rigor, timely refresh, and dual-path validation converge, Mordor's baseline emerges as the most dependable starting point for planning and investment decisions.

Key Questions Answered in the Report

What is the current value of the remote monitoring and control market?

The market is valued at USD 28.55 billion in 2026 and is forecast to reach USD 36.85 billion by 2031.

Which segment is growing fastest within the remote monitoring and control market?

Cloud deployment leads growth at a 9.12% CAGR, reflecting demand for scalable, subscription-based platforms.

Why are pharmaceuticals adopting remote monitoring rapidly?

FDA guidance on digital health technologies requires continuous cleanroom and process monitoring, driving a 7.38% CAGR in the segment.

How do private 5G networks enhance remote monitoring?

They deliver ultra-reliable, low-latency links that support autonomous equipment and real-time analytics in demanding industrial settings.

What is the main restraint hindering wider adoption?

High initial capital expenditure and complex brown-field integration slow projects, particularly for smaller operators.

Which region shows the highest growth potential?

Asia-Pacific is projected to expand at an 7.95% CAGR to 2031, propelled by large automation investments in China, India, and Southeast Asia.

Page last updated on: