Remote Workplace Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

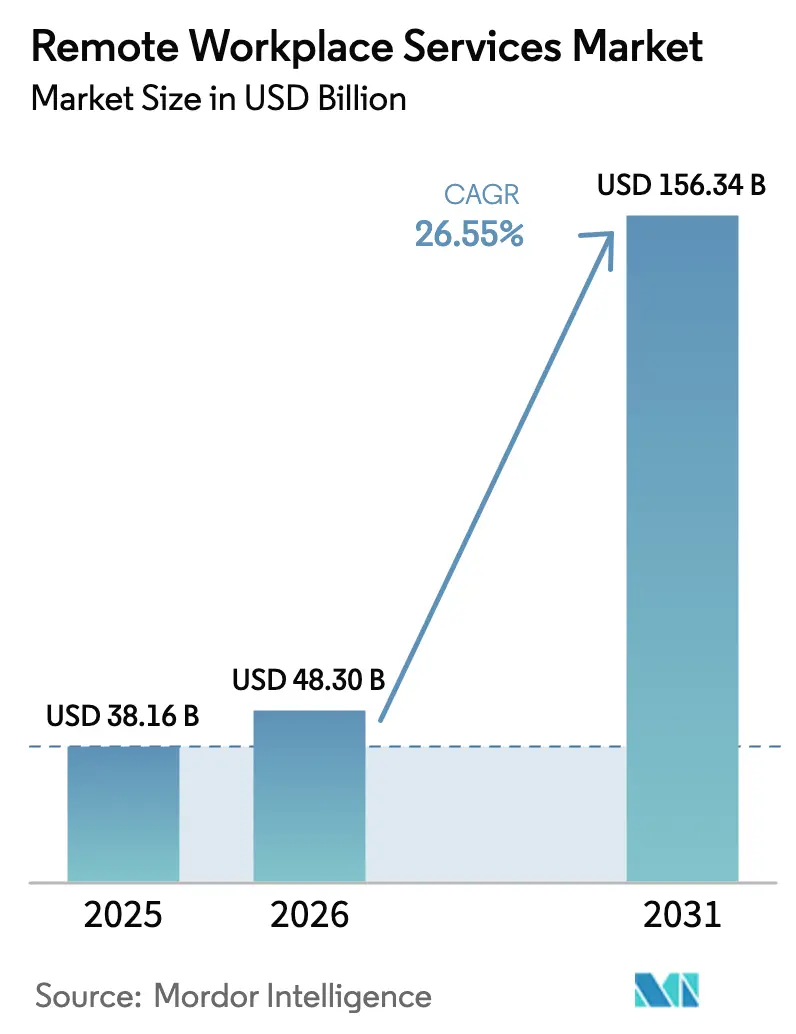

| Market Size (2026) | USD 48.3 Billion |

| Market Size (2031) | USD 156.34 Billion |

| Growth Rate (2026 - 2031) | 26.55% CAGR |

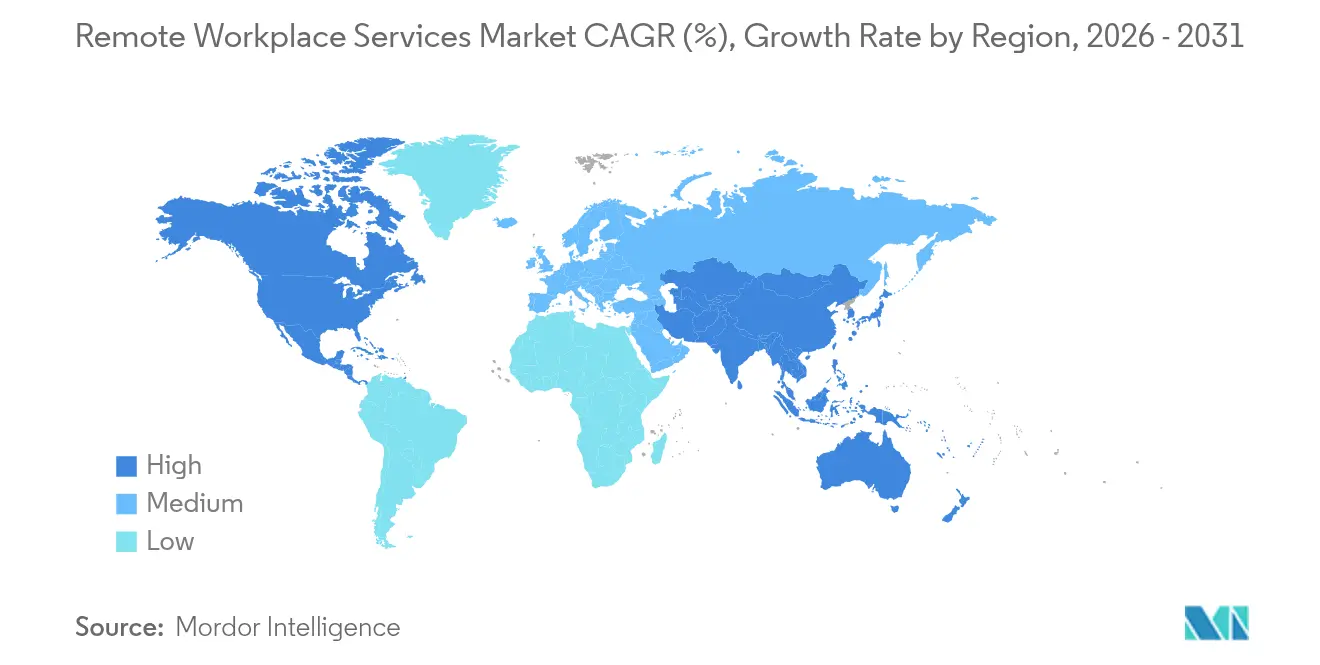

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Remote Workplace Services Market Analysis by Mordor Intelligence

Remote workplace services market size in 2026 is estimated at USD 48.3 billion, growing from 2025 value of USD 38.16 billion with 2031 projections showing USD 156.34 billion, growing at 26.55% CAGR over 2026-2031. Heightened investment in cloud-based collaboration suites, unified endpoint management, and virtual desktop infrastructure delivers the technical backbone for location-agnostic productivity. Generative AI features, embedded across communication and service-management tools, raise user expectations for automation and personalization, prompting accelerated refresh cycles. At the same time, zero-trust roadmaps expand quickly as boards elevate breach mitigation, driving bundled security-plus-workplace deals. Finally, hybrid work mandates create dual infrastructure demand—revitalized office hubs and remote capabilities—supporting both sustained platforms spending and managed-service outsourcing momentum.

Key Report Takeaways

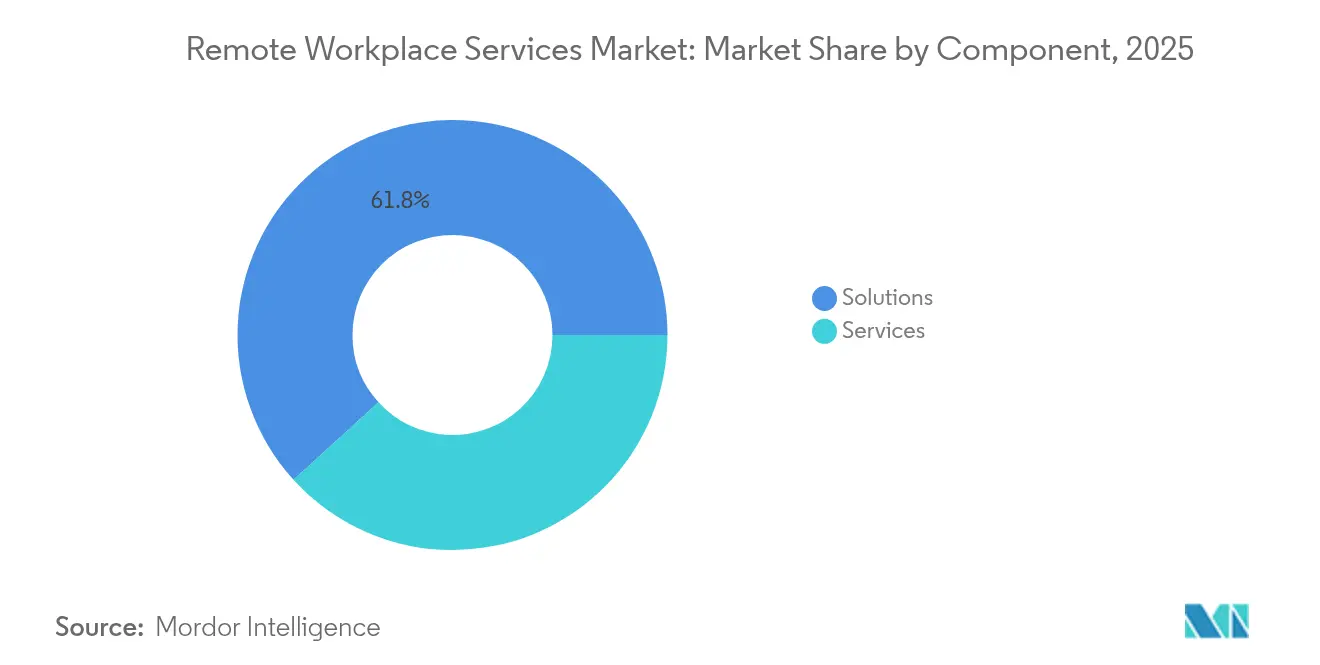

- By component, solutions led with 61.75% revenue share in 2025, while services are forecast to expand at a 16.2% CAGR through 2031

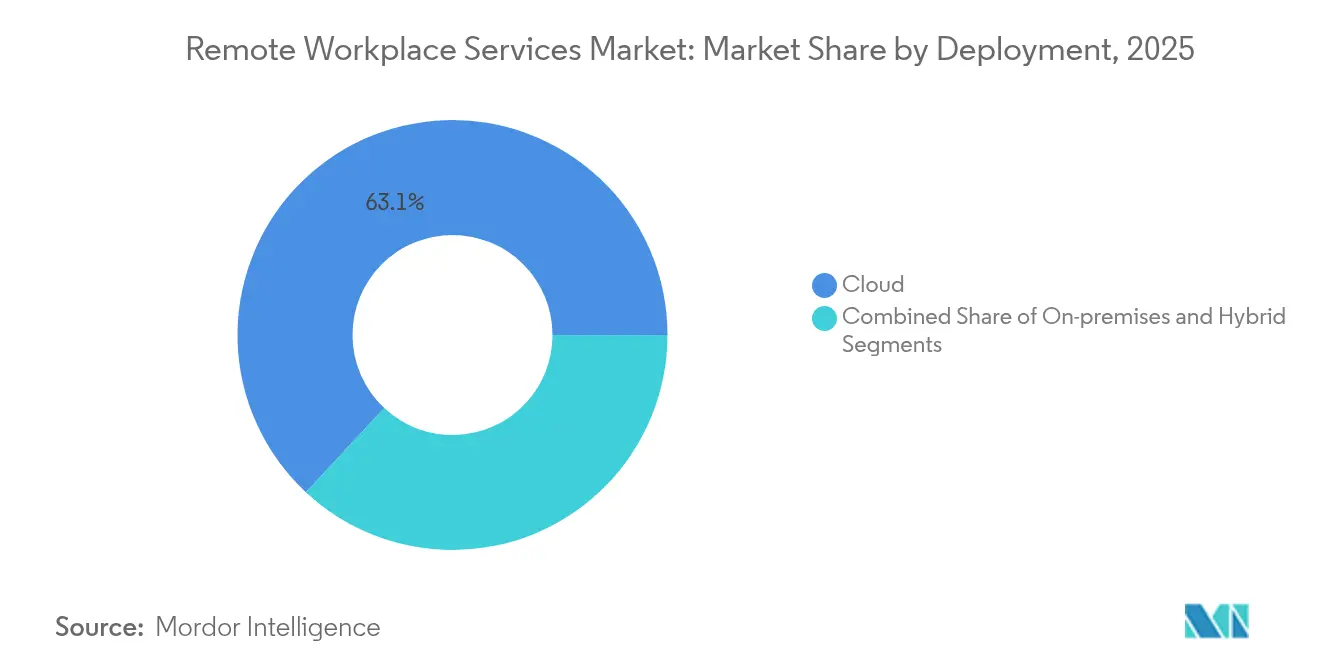

- By deployment, cloud captured 63.05% of the remote workplace services market share in 2025; the model is advancing at a 18.6% CAGR to 2031

- By organization size, large enterprises held 70.35% share in 2025, whereas SMEs are projected to register a 11.7% CAGR over the same period

- By end-user industry, IT and telecommunications accounted for 27.05% of the remote workplace services market size in 2025; healthcare is set to grow at an 17.9% CAGR to 2031

- By geography, North America led with 37.35% share in 2025; Asia-Pacific is on track for a 21.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Remote Workplace Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid and flexible work policies surge | +6.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Rising focus on digital employee experience platforms | +4.2% | Global, particularly strong in Asia-pacific and North America | Short term (≤ 2 years) |

| Cost optimization through managed workplace outsourcing | +3.1% | Global, with higher impact in cost-sensitive SME segments | Long term (≥ 4 years) |

| ESG-linked remote-work solutions demanded by large enterprises | +2.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Zero-trust network access bundling into workplace offers | +1.8% | Global, with enterprise focus in developed markets | Short term (≤ 2 years) |

| Generative AI-driven virtual assistants for remote support | +1.2% | North America and Europe initially, global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid and Flexible Work Policies Surge

Universal adoption of hybrid models across Fortune 500 cohorts restructures procurement toward cloud-first, mobile-first stacks that enable asynchronous collaboration at global scale. Microsoft’s 2025 Work Trend Index finds 30% of meetings now spanning multiple time zones, highlighting the infrastructural expectation for always-available, low-latency tools[1]Jared Spataro, “2025 Work Trend Index,” Microsoft, microsoft.com. Enterprises consequently prioritize unified endpoint management and cross-platform video solutions that balance presence analytics with privacy controls. Office footprints shift into collaboration hubs, yet physical rationalization does not suppress spending; rather, organizations fund dual environments to sustain culture and flexibility. This duality propels the remote workplace services market as buyers seek seamless roaming between on-site and remote contexts without workflow disruption.

Rising Focus on Digital Employee Experience Platforms

Boards increasingly link productivity and retention metrics to the quality of digital experiences. Integrated workplace suites now embed sentiment analytics, workflow orchestration, and AI chatbots that surface contextual guidance, turning reactive IT support into a proactive experience curation. Deloitte forecasts that personalized work journeys will become a primary differentiator in talent acquisition, forcing platform consolidation around single panes of glass for communication, learning, and service delivery. Early adopters report measurable reductions in ticket volumes and onboarding times, reinforcing ROI narratives that unlock additional budget cycles. In APAC, where mobile penetration is high, experience platforms also serve as frontline management tools, widening addressable demand.

Cost Optimization Through Managed Workplace Outsourcing

Managed workplace outsourcing converts capital expenditure into predictable operating costs, a benefit amplified by persistent skills shortages. The Technology Services Industry Association notes migration from labor-based billing to outcome-indexed contracts that reward uptime, user satisfaction, and security posture. Providers leverage automation, AI agents, and global delivery centers to scale support at lower marginal cost, transferring efficiency gains to clients. SMEs recognize a path to enterprise-grade security and compliance without deep internal benches, spurring adoption beyond historical large-enterprise dominance. As subscription bundles mature, multi-year deals lock in road-map co-innovation, embedding service partners deeper into client ecosystems and lifting the remote workplace services market.

ESG-Linked Remote-Work Solutions Demanded by Large Enterprises

Impending EU and SEC disclosure rules push sustainability metrics into technology selection, making carbon-aware workload placement and commute offset dashboards standard features. Gartner projects 80% of digital workplace leaders will integrate ESG tooling by 2027, up from single-digit penetration in 2024. Cloud platforms that map energy-efficient regions and automate power-state optimization help clients quantify Scope 3 reductions. Social pillars also gain prominence; accessible design and distributed hiring widen workforce diversity. Vendors packaging certified green hosting, automated reporting, and employee-wellbeing analytics secure competitive advantage in enterprise RFPs, solidifying ESG as a durable demand vector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity and data-breach risks | -2.1% | Global, with higher impact in regulated industries | Short term (≤ 2 years) |

| Up-front transformation and integration costs | -1.4% | Global, particularly affecting SMEs and cost-sensitive enterprises | Medium term (2-4 years) |

| Shadow-IT proliferation across SaaS tool-sprawl | -1.2% | Global, with higher impact in large enterprises | Short term (≤ 2 years) |

| Cross-border data-sovereignty regulations tightening | -0.8% | Europe and Asia-Pacific primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity and Data-Breach Risks

Proliferating remote endpoints widen attack surfaces, compelling enterprises to fund zero-trust, identity-centric controls that can delay broader rollouts. Regulatory scrutiny intensifies, particularly for healthcare and financial entities operating across jurisdictions where data residency mandates add architectural complexity. Continuous monitoring, micro-segmentation, and device posture checks elevate baseline cost and skill requirements, slowing decisions for budget-constrained buyers. Breach publicity further raises executive risk aversion, causing phased deployments that scale only after pilot hardening. Vendors addressing embedded security, encrypted VDI streams, and automated compliance reporting mitigate this drag, yet the restraint remains material to remote workplace services market expansion.

Up-Front Transformation and Integration Costs

Comprehensive remote-workplace modernization demands investment in network upgrades, identity refactoring, and change-management programs. Legacy ERP, HR, and finance systems often require custom API connectors, extending implementation timelines and elevating professional-service spend. SMEs face acute capital hurdles despite attractive payback periods, as internal cash flow pressures limit large one-time outlays. Even for multinationals, global rollouts must coordinate across business units, local labor rules, and language variants, compounding complexity. These realities lengthen sales cycles and temper near-term growth, although mature templates and accelerators gradually reduce barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Solutions Dominance

Solutions continued to command 61.75% of the remote workplace services market size in 2025, reflecting entrenched demand for endpoint management, collaboration suites, and virtual desktops. Yet the services segment is forecast to rise at a 16.2% CAGR through 2031, underscoring a distinct pivot toward managed outsourcing models that trade capital intensity for subscription flexibility. Enterprises seeking rapid zero-trust alignment and AI enablement increasingly sign multi-tower managed deals that unify device management, service desk, and security monitoring.

Consulting, assessment, and change-management engagements capture early-stage budgets as organizations evaluate platform road maps. Managed workplace offerings gain momentum through service-level commitments tied to experience scores, prompting providers to embed AI agents that pre-empt incident creation. Support and maintenance revenue compounds as installed bases grow, ensuring high-margin annuities. Training investments also climb because user proficiency directly influences experience metrics, sustaining a virtuous loop that enlarges the remote workplace services market.

By Organization Size: SMEs Drive Adoption Acceleration

Large enterprises retained 70.35% share of the remote workplace services market in 2025 due to comprehensive global operations and regulatory obligations requiring advanced security and governance. Their scale ensures continued spend on multi-cloud VDI farms, integrated ITSM platforms, and experience analytics. Nevertheless, the SME cohort is projected to deliver a 11.7% CAGR to 2031, closing maturity gaps through cloud SaaS bundles that mask underlying complexity.

Lower entry costs, consumption-based billing, and verticalized templates enable smaller firms to bypass heavy on-premise stacks. Managed service providers respond with packaged “office in a box” offerings incorporating identity, collaboration, and endpoint security. Case studies now highlight SMEs cutting onboarding time by half and halving device downtime, reinforcing adoption intent. This democratization expands the total addressable remote workplace services market, diversifying revenue away from a few mega-accounts toward a broader base.

By Deployment: Cloud Dominance Accelerates

Cloud deployments captured 63.05% remote workplace services market share in 2025 and are pacing at a 18.6% CAGR, validating the consensus that SaaS, desktop-as-a-service, and browser-delivered applications present the fastest route to scale. Elastic compute and global POP networks support latency-sensitive applications, while consumption pricing aligns cost with usage patterns.

On-premise estates remain relevant for data-sovereignty commitments within public sector and highly regulated workflows. Hybrid topology therefore persists, with sensitive workloads anchored in private clouds and collaboration tiers burst into public regions. Multi-cloud strategies mitigate lock-in and optimize spend; toolchains that simplify policy propagation across providers are increasingly bundled into deals. The result is a fluid deployment continuum where cloud remains dominant but interoperability dictates architecture decisions, lifting overall remote workplace services market demand.

By End-User Industry: Healthcare Transformation Accelerates

IT and telecommunications held the largest remote workplace services market size contribution at 27.05% in 2025, benefitting from inherent digital familiarity and wide endpoint estates that require advanced orchestration. Financial institutions follow closely, driven by compliance and secure customer engagement imperatives.

Healthcare, however, is poised for the swiftest advance at an 17.9% CAGR to 2031 as telemedicine, remote patient monitoring, and distributed clinical documentation gain funding. Virtual desktop infrastructure secures patient records while allowing clinicians to roam across facilities. AI-assisted transcription and diagnostics further illustrate the sector’s appetite for integrated digital workplace stacks. Successful pilots reporting improved clinician satisfaction and reduced administrative burden validate incremental investment, channeling new capital into the remote workplace services market.

Geography Analysis

North America dominated with 37.35% of the remote workplace services market in 2025, supported by mature 5G coverage, cloud hyperscaler availability zones, and board-level commitment to hybrid work as a long-term operating norm. United States enterprises lead AI-infused collaboration adoption, while Canadian public-sector modernization grants accelerate cross-border managed-service awards. Mexico’s maquiladora supply chains increasingly depend on distributed engineering and support teams, broadening regional scope.

Asia-Pacific represents the fastest-growing arena, charting a 21.6% CAGR forecast through 2031. Large-scale investments in fiber and 5G networks intersect with government incentives such as Singapore’s AI Cloud Takeoff program, which offers up to SGD 500,000 per enterprise for AI workplace pilots. China and India anchor volume through vast labor pools and surging cloud data-center footprints. Australian financial services mandates on operational resilience also spur secure virtual desktop adoption, while Southeast Asian SMEs leapfrog legacy infrastructure via mobile-first SaaS bundles.

Europe maintains steady expansion, propelled by ESG-centric procurement and strict data-protection statutes that encourage regional cloud nodes and encrypted endpoint solutions. Nordic governments model remote-ready public administration, reinforcing cultural acceptance. Germany’s Mittelstand invests in hybrid platforms to mitigate skilled-worker shortages, and French regulations on right-to-disconnect shape analytics modules that monitor overtime risk. Collectively, these factors sustain European contribution despite tighter sovereign data requirements, ensuring balanced growth within the remote workplace services market.

Competitive Landscape

The competitive field shows moderate consolidation: platform leaders integrate infrastructure, security, and experience layers to defend share and raise switching barriers. Microsoft and Citrix deepened alignment through a USD 1.65 billion Azure commitment, positioning Citrix as preferred enterprise desktop-as-a-service partner[3]Citrix Investor Relations, “Citrix-Microsoft Expanded Partnership,” Citrix, citrix.com. Such deals blend scale economics with joint road-map acceleration, creating end-to-end stacks that appeal to risk-averse CIOs.

Hyperscalers exploit ecosystem leverage, exemplified by AWS cultivating system-integrator alliances to reach a USD 250 billion services pool. Accenture, Tata Consultancy, and DXC co-invest in solution blueprints, ensuring rapid customer onboarding and reinforcing AWS tenancy. Meanwhile, specialized entrants focus on pain-point niches. Atomicwork raised USD 14 million to build AI-centric service-management hubs, challenging incumbents on usability and agentic automation.

Strategic Mand A accelerates capability aggregation. NTT DATA’s purchase of Niveus adds 1,000 Google Cloud engineers, bolstering multi-cloud delivery depth. Workday’s Agent Partner Network formalizes marketplaces where ISVs embed AI agents that the Agent System of Record governs, signaling a future where human and machine roles are administered under common HR policy. Ultimately, competitive advantage converges on integrated AI, zero-trust by design, and demonstrable business outcomes, factors that collectively expand the remote workplace services market.

Remote Workplace Services Industry Leaders

Atos Group

IBM Corporation

DXC Technology Company

Hewlett Packard Enterprise Company

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Workday launched the AI Agent Partner Network and Agent Gateway, enabling integration of AI agents into workforce platforms.

- June 2025: Google Cloud and Digital Industry Singapore introduced the AI Cloud Takeoff program to fund AI Centers of Excellence in 300 companies.

- May 2025: NTT DATA unveiled the Smart AI Agent Ecosystem, converting legacy RPA bots into autonomous intelligent agents.

- April 2025: TCS rolled out India-focused sovereign cloud networks, contributing USD 2.6 billion to revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the remote workplace services market as every software platform and managed service that enables employees to access corporate applications, files, and support while working away from a head office. This spans digital workplace platforms, unified endpoint management, virtual desktop infrastructure, collaboration suites, and related advisory or managed help-desk offerings. According to Mordor Intelligence, the baseline year 2025 value is USD 38.16 billion, projected to reach USD 127.24 billion by 2030.

Scope Exclusion: Physical coworking real estate and pure-play network security tools fall outside this definition.

Segmentation Overview

- By Component

- Solutions

- Unified Endpoint Management

- Digital Workplace Platforms

- Virtual Desktop Infrastructure (VDI)

- Collaboration and Communication Tools

- Services

- Consulting and Assessment

- Managed Workplace Services

- Support and Maintenance

- Training and Adoption

- Solutions

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Deployment

- Cloud

- On-Premise

- Hybrid

- By End-User Industry

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Retail and E-commerce

- Manufacturing

- Government and Public Sector

- Education

- Media and Entertainment

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed workplace technology architects at managed service providers, HR and procurement heads in large enterprises across North America, Europe, and Asia-Pacific, and niche tool vendors. Insights on pricing dispersion, license utilization, and BYOD policy rollouts allowed us to stress-test desk findings and adjust regional penetration assumptions.

Desk Research

We began with public data from trusted agencies such as the International Telecommunication Union, Eurostat, and the US Bureau of Labor Statistics to size the global pool of remote and hybrid employees. Trade groups, namely CompTIA, the Cloud Industry Forum, and the Asia Cloud Computing Association, provided adoption ratios for VDI, device-as-a-service, and managed workplace outsourcing. Company 10-K filings and investor decks added real contract values and average selling prices, while academic journals in IEEE and ACM helped us gauge technology refresh cycles. Select figures from D&B Hoovers and Dow Jones Factiva enriched firm-level benchmarks. This list is illustrative; many other secondary sources informed data validation.

Market-Sizing & Forecasting

The core model applies a top-down "remote employee demand pool" build-up. We multiply the addressable workforce in each country by remote-work penetration and average annual spend on workplace tools and services. Supplier roll-ups and sampled ASP × volume checks act as bottom-up reasonableness guards. Key variables include (a) remote/hybrid worker share of total employment, (b) enterprise cloud spending per user, (c) virtual desktop licenses shipped, (d) managed service contract values, and (e) churn rates between on-premise and cloud deployments. A multivariate regression, anchored on historical cloud spend and hybrid employee growth, forecasts each driver. Scenario analysis then frames upside and downside cases. Data gaps in smaller markets are bridged using GDP-per-capita elasticity and peer-cluster averages.

Data Validation & Update Cycle

Before release, an analyst compares modeled results with independent payroll outlays, device shipment data, and service provider revenue lines. Variances beyond preset bands trigger a rework. Reports refresh every twelve months, while material events, such as large M&A and regulatory shifts, prompt interim updates.

Why Mordor's Remote Workplace Services Baseline Commands Reliability

Published figures often diverge because firms vary in what they count, how often they refresh numbers, and the aggressiveness of their cloud migration assumptions.

Key Gap Drivers: Some publishers merge real estate coworking revenue with IT services, others assume all hybrid employees purchase full-stack digital workplace suites, and a few extrapolate using static average prices without checking contract renegotiations. Mordor's scope focuses strictly on IT enablement spend, applies verified user pricing, and benefits from an annual update cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.16 bn (2025) | Mordor Intelligence | - |

| USD 30.55 bn (2024) | Global Consultancy A | Combines coworking real estate and uses single global ASP |

| USD 24.19 bn (2024) | Industry Journal B | Omits managed support contracts and uses 2023 pricing throughout forecast |

In short, our disciplined variable selection, dual-track validation, and timely refresh give decision-makers a balanced, transparent baseline they can trace and replicate with clear steps.

Key Questions Answered in the Report

What is the current size of the remote workplace services market?

The remote workplace services market reached USD 48.3 billion in 2026 and is forecast to grow to USD 156.34 billion by 2031 at a 26.55% CAGR.

Which region leads the remote workplace services market?

North America held 37.35% share in 2025 due to comprehensive hybrid work adoption, but Asia-Pacific is the fastest-growing region with a 21.6% CAGR.

What components make up the remote workplace services market?

Solutions—covering unified endpoint management, collaboration platforms, and VDI—accounted for 61.75% share in 2025, while services, including consulting and managed workplace outsourcing, are expanding at a 16.2% CAGR.

Why is cloud deployment favored?

Cloud models captured 63.05% remote workplace services market share in 2025 and are rising at a 18.6% CAGR because they offer scalability, lower capital needs, and faster rollout.

Which industry is growing fastest in adoption?

Healthcare is the fastest-growing end-user industry, advancing at an 17.9% CAGR as telemedicine and remote monitoring become mainstream.

Page last updated on: