Self-Consolidating Concrete (SCC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

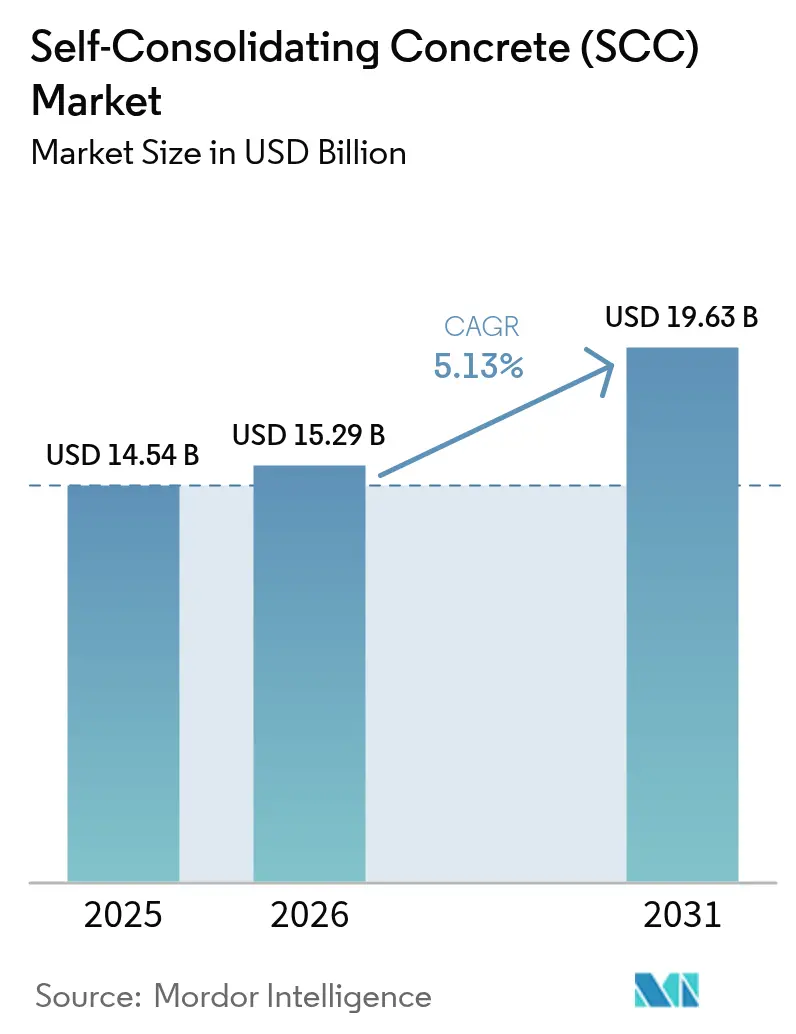

| Market Size (2026) | USD 15.29 Billion |

| Market Size (2031) | USD 19.63 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

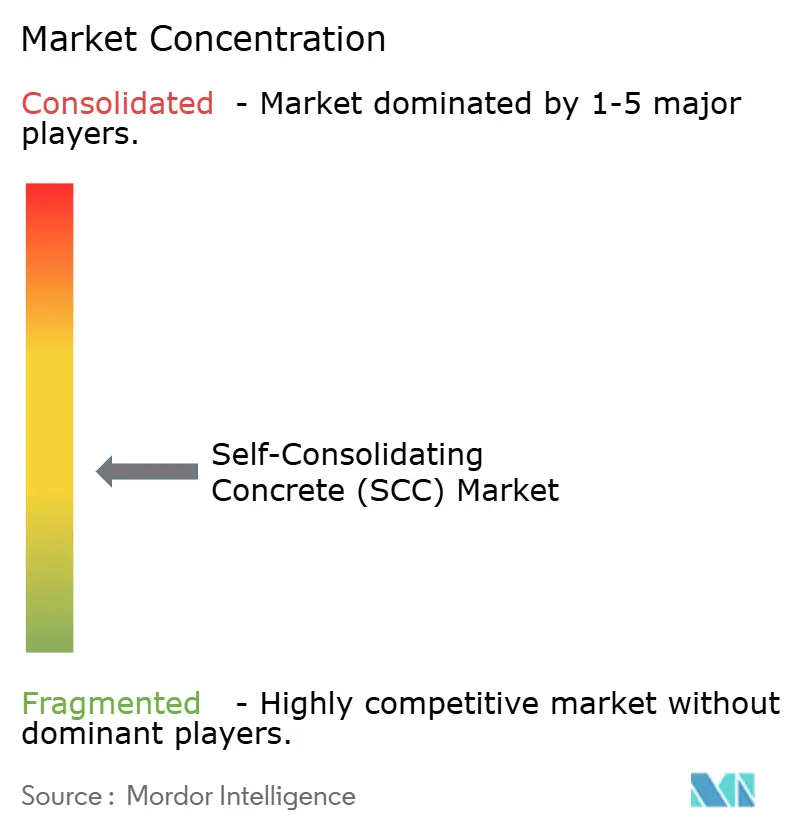

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Consolidating Concrete (SCC) Market Analysis by Mordor Intelligence

Self-Consolidating Concrete Market size in 2026 is estimated at USD 15.29 billion, growing from 2025 value of USD 14.54 billion with 2031 projections showing USD 19.63 billion, growing at 5.13% CAGR over 2026-2031. Robust demand arises from contractors’ need to pour intricate reinforcement cages without mechanical vibration, a requirement that lines up with tightening labor regulations and automation goals. Regulatory pressure to curb embodied carbon, especially in North America and Europe, accelerates the shift toward supplementary-cementitious-material-rich mixes. Established admixture producers leverage polycarboxylate chemistry to enhance flow at lower water–binder ratios, while digital monitoring platforms provide real-time strength data that helps reduce cement content. Collectively, these factors reinforce a virtuous cycle in which better performance, lower labor intensity and sustainability mandates all favor the self-consolidating concrete market.

Key Report Takeaways

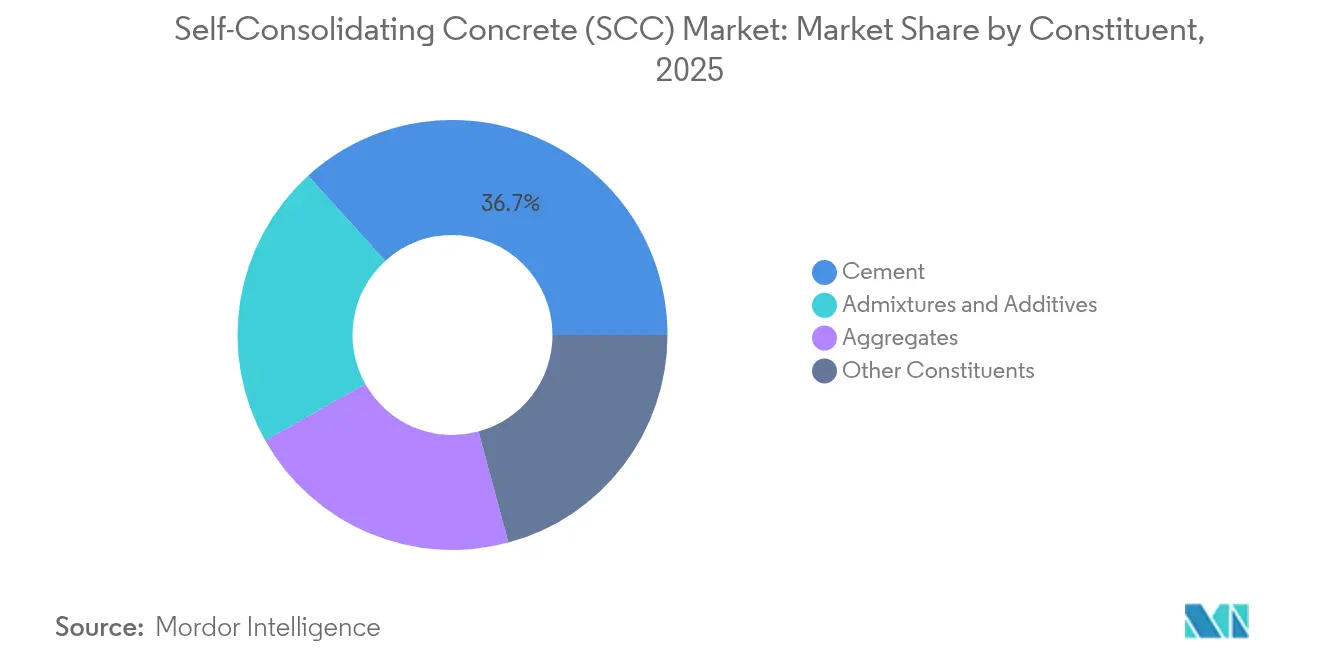

- By constituent, cement maintained the top spot with 36.72% of the self-consolidating concrete market size in 2025; admixtures and additives represent the fastest-growing constituent category with a 6.96% CAGR.

- By application, infrastructure led with 42.55% of self-consolidating concrete market share in 2025, while precast is projected to expand at a 6.71% CAGR through 2031.

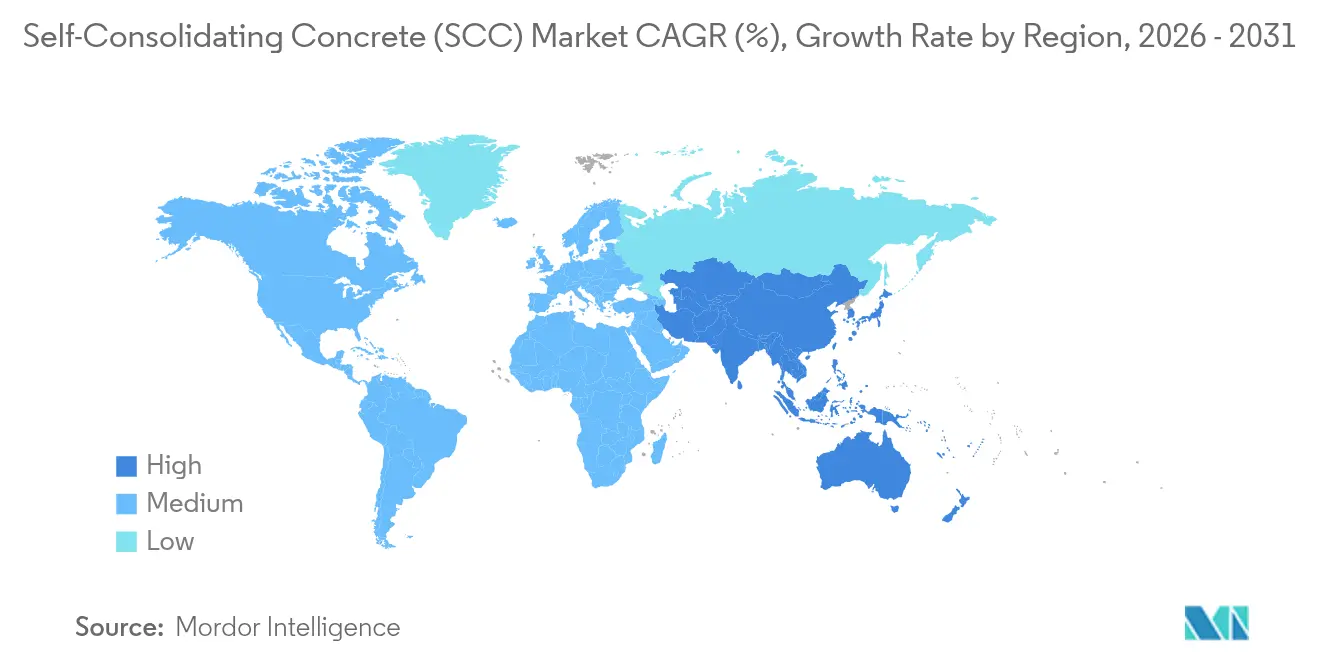

- By geography, Asia-Pacific commanded 49.12% of the self-consolidating concrete market in 2025 and is advancing at a regional-leading 7.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self-Consolidating Concrete (SCC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-saving placement in precast and in-situ works | +1.2% | Global, with highest impact in APAC and North America | Medium term (2-4 years) |

| Accelerating demand for low-carbon, SCM-rich mixes | +0.8% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Surge in automated/robotic casting lines | +0.6% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Adoption in complex, high-rise & mega-infrastructure | +0.9% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Government green-building mandates | +0.7% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-saving placement in precast and in-situ works

Chronic craft-worker shortages prompt builders to adopt vibration-free placement methods that cut cycle times by up to 73% and permit leaner crew sizes. Precast plants record 28% productivity gains when integrating fiber-reinforced self-consolidating mixes, a figure now observable across North America and Japan. Faster turnarounds yield cost parity against conventional concrete despite a 15–25% materials premium. The benefit multiplies on congested rebars where vibration is either impractical or physically impossible, placing the self-consolidating concrete market at the center of high-rise and bridge work.

Demand for low-carbon SCM-rich mixes

State-level “Buy Clean” rules in New York enforce embodied-carbon ceilings for concrete supplied to public projects, pushing producers toward high slag and fly-ash dosages that pair naturally with flowable mixes[1]New York State Office of General Services, “Buy Clean Concrete Guidelines,” ogs.ny.gov. Similar thresholds under California’s CALGreen code and France’s RE2020 framework create a price premium for formulations that deliver 30–50% CO₂ cuts relative to Type I blends. Modern polycarboxylate superplasticizers sustain required flow at reduced clinker factors, reinforcing the self-consolidating concrete market as a sustainability lever rather than just a labor solution.

Surge in automated robotic casting lines

Robotic placement cells under development at Obayashi’s Singapore tech lab rely on concrete that spreads under its own weight while resisting segregation during extended pump runs[2]Obayashi Corporation, “Robotics-Enabled Construction Technologies,” obayashi.co.jp. Viscosity-modifying admixtures fine-tune rheology for continuous robotic casting, improving dimensional accuracy and workplace noise levels. Cloud-connected maturity sensors from Heidelberg Materials feed real-time compressive-strength data, cutting cement dosages by up to 20% while keeping production lines in motion. These advances cement the self-consolidating concrete market as a prerequisite for automated factories.

Adoption in complex high-rise and mega-infrastructure

Projects such as Bulgaria’s 49-story Sky Fort Business Center highlight the ability to pump C 50/60 mixes more than 180 m without segregation, yielding uniform finishes and minimal rework. Bridge decks, pile caps and diaphragm walls benefit from the material’s capacity to self-level through dense reinforcement cages. As mega-projects proliferate across Asia-Pacific’s urban cores, the self-consolidating concrete market enjoys first-call status whenever geometry, access or reinforcement density challenge conventional placement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High mix-design & material cost premium | -1.8% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Limited field know-how in emerging regions | -0.9% | APAC emerging markets, MEA, Latin America | Medium term (2-4 years) |

| Admixture-sensitivity causing quality variability | -0.7% | Global, concentrated in hot weather regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High mix-design & material cost premium

A 15–25% cost delta over conventional concrete remains a headwind wherever wages are low and project owners resist premium pricing. The need for well-graded aggregates and imported admixtures can inflate costs in Southeast Asia and parts of Latin America, dampening self-consolidating concrete market growth despite clear labor savings. Contractors must balance up-front expense against downstream efficiencies, limiting uptake in small-scale jobs.

Limited field know-how in emerging regions

Successful execution hinges on slump-flow, J-ring and segregation testing routines that many local labs lack. Insufficient training leads to over-dosing or under-dosing of admixtures, causing performance swings and sporadic rejections. As suppliers roll out mobile labs and certification schemes, the knowledge gap will narrow, but in the interim the self-consolidating concrete market faces longer sales cycles in less-industrialized geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Constituent: Cement Dominance Amid Admixture Innovation

Cement accounted for 36.72% of the self-consolidating concrete market in 2025, a lead attributable to structural volume rather than growth momentum. Admixtures now post a 6.96% CAGR, underpinned by the rapid uptake of fourth-generation polycarboxylate ethers that enable water-binder ratios near 0.30 without sacrificing flow. Paired with viscosity modifiers, these chemistries unlock higher SCM replacement levels that help producers comply with tightening CO₂ caps. Aggregates rank second by value; demand intensifies for gap-graded stone with low flakiness to mitigate blocking under minimal head pressure. The constituent mix tilts toward chemical optimization as producers emphasize performance over cement tonnage, underscoring why global majors prioritize R&D alliances and acquisitions in the admixture space.

The pivot toward SCM integration reshapes supplier hierarchies. Fly-ash availability remains volatile in Western markets due to declining coal power, spurring interest in calcined clay and ground-glass pozzolans. Fiber additions grow in precast applications, offering crack control that complements vibration-free casting. SikaGrind-400 illustrates how targeted grinding aids elevate early strength when clinker factors drop, widening the addressable self-consolidating concrete market. Cement producers counter by bundling low-carbon binders with in-house admixture lines to retain share, signaling that future competitive advantage depends less on raw tonnage and more on integrated chemical solutions.

By Application: Infrastructure Leadership Drives Precast Innovation

Infrastructure held 42.55% of self-consolidating concrete market share in 2025, thanks to bridges, tunnels and deep foundations that demand full consolidation around congested reinforcement. Public-works pipelines in China, India and the United States guarantee volume visibility, giving material suppliers the scale to amortize formulation R&D. Precast segments, while smaller in absolute terms, clock a 6.71% CAGR as factory automation spreads. Controlled environments suit flowable mixes, and reduced noise from vibration-free casting allows urban plants to operate within stricter zoning limits. Residential high-rise construction also gains traction where elevator-core congestion and labor scarcity overlap, notably in Japan and urban India.

Architectural components—curved façades, fair-faced columns and sculptural elements—tap the material’s form-filling ability to achieve blemish-free finishes without surface treatments. Marine and industrial structures adopt self-consolidating concrete for durability in chloride-rich exposures where internal consolidation is vital. Taken together, the diversity of use cases ensures that no single application dominates growth, cushioning the self-consolidating concrete market against downturns in any one construction segment.

Geography Analysis

Asia-Pacific controlled 49.12% of global revenue in 2025 and is projected to expand at a 7.36% CAGR, reflecting massive infrastructure outlays coupled with acute labor shortages. China’s high-speed-rail viaducts and India’s smart-cities program routinely specify vibration-free concrete for dense reinforcement cages. Japan’s overtime legislation caps site hours, strengthening the business case for automated placement in both precast yards and cast-in-place work. North America ranks second by value; bipartisan infrastructure spending unlocks bridge-deck and highway rehabilitation opportunities that align with New York’s embodied-carbon caps.

Europe remains a mature yet innovative arena. Embodied-carbon ceilings under RE2020 in France and Ireland’s clinker-reduction mandate accelerate SCM adoption, thereby boosting admixture demand. Middle East & Africa and South America start from smaller bases but display rising interest as technical service networks expand and megaprojects proliferate.

Value Chain Analysis

The SCC value chain begins with upstream binders and supplementary cementitious materials (cement producers and SCM processors), aggregates (quarries and sand suppliers with tight grading control), and specialty chemicals, including polycarboxylate ether superplasticizers and viscosity-modifying admixtures. These inputs are then used in mix design and trial batching, followed by production through ready-mix batching plants and precast factories. Distribution relies on transit mixers and pumps, or internal logistics for molded components. Technical service and testing capacity are a core link in SCC, with routine slump-flow and blocking/segregation checks needed to keep rheology stable, particularly in hot-weather placement and long pump runs.

Value creation centers on formulation know-how, especially admixture selection and dosage optimization to sustain flow at low water-binder ratios, along with quality assurance on aggregates and fresh-state performance. Bottlenecks tend to include inconsistent aggregate gradation, admixture sensitivity that drives batch-to-batch variability, and shortages of trained personnel able to run SCC-specific testing and troubleshoot issues. As a result, competitive strategies often emphasize vertical integration, with cement and concrete producers bundling low-carbon binders with in-house admixture systems, plus tighter collaboration with precast operators that deploy automated casting lines where vibration-free placement supports throughput and consistent surface finishes.

Competitive Landscape

The market shows moderate fragmentation. Chemical companies such as BASF and Sika exploit their admixture portfolios to edge into territory once controlled by cement majors. Saint-Gobain’s USD 1.025 billion acquisition of FOSROC in February 2025 underscores the value placed on construction-chemical know-how. Heidelberg Materials pushes digital job-site monitoring via its Giatec alliance, enabling 20% cement reductions and enhancing sustainability credentials.

Strategic thrusts include vertical integration, regional bolt-on acquisitions and R&D partnerships aimed at carbon-reduced binders. Disruptors deploy cloud-linked rheology sensors and AI-driven mix-design engines, lowering the technical barriers for small ready-mix producers. Suppliers that can bundle low-carbon binders with robotic-friendly flow retain an edge, especially in regions where labor constraints and embodied-carbon rules converge. The competitive narrative now extends beyond material cost toward holistic performance packages featuring digital testing, carbon accounting and job-site logistics—attributes that collectively shape the self-consolidating concrete market.

Self-Consolidating Concrete (SCC) Industry Leaders

Cemex SAB de CV

CRH

Heidelberg Materials

Holcim

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace for SCC is emerging around circular-economy feedstocks and quantified mix optimization, because SCC performance depends heavily on aggregate quality and paste rheology, while owners are tightening embodied-carbon requirements. In 2026, technical work has highlighted pathways for high-substitution mixes, including SCC using construction and demolition waste as aggregate replacements under the EU Horizon MOBICCON-PRO project, and optimization frameworks that incorporate up to 100% reclaimed asphalt pavement while targeting structural performance. These strands create commercialization opportunities for admixture suppliers and ready-mix producers that can standardize quality control and offer repeatable specifications for recycled-content SCC.

Another opportunity is application-specific SCC for complex infrastructure where consolidation constraints shape constructability more than material cost. Technical guidance and case-led documentation around specialized placements, including hydropower civil works where SCC is used selectively for embedded liners, tunnel crowns, and complex zones, points to a route for producers to position SCC as a problem-solving system, combining tailored rheology with field support rather than selling it as a generic premium concrete. Digital tools that reduce trial-and-error in mix design also create room for differentiated service models, including 2026 publications on machine learning-based multi-objective optimization of fly ash-based SCC for mechanical performance and environmental impact, linking SCC development to both cost and carbon constraints.

Recent Industry Developments

- March 2026: Amrize launched its EVERtect high-performance concrete range at CONEXPO-CON/AGG 2026, including FLUIDtect as a proprietary self-consolidating concrete mix. The company framed the launch around a branded performance portfolio for contractors, reinforcing differentiation beyond commodity ready-mix supply in North America.

- May 2025: Holcim introduced its grey cement and concrete range in Peru, highlighting specialized products such as self-compacting concrete. Expanding the specialized concrete lineup supports mix-standardization and technical-service pull-through for SCC in a growing construction market.

- November 2024: CRH announced a definitive agreement to acquire a portfolio of cement and ready-mixed concrete assets from Martin Marietta Materials in South Texas in a USD 2.1 billion cash transaction, with self-consolidating concrete included in the product scope. The asset expansion strengthens CRH distribution density and mix capability in a major US construction corridor where performance concretes can be scaled through an integrated local network.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the self-consolidating concrete (SCC) market is defined as the value of SCC mixes sold for construction uses where concrete is designed to flow and self-level without mechanical vibration, across major regions.

Scope exclusions: We exclude conventional vibrated concrete, site labor and placing services, and equipment used for vibration or pumping unless bundled into the concrete selling price.

Segmentation Overview

- By Constituent

- Cement

- Aggregates

- Admixtures and Additives

- Other Constituents

- By Application

- Precast Concrete Products

- Architectural Elements

- Residential Structures

- Infrastructure (Bridges, Tunnels, etc.)

- Other Applications

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base demand picture and to keep assumptions practical for concrete volumes, pricing, and regional construction cycles. We leaned on public construction and infrastructure indicators, along with technical standards that describe SCC behavior in real projects.

Sources referenced include national statistics offices for construction output, transportation and public works publications for infrastructure pipelines, and trade association materials on ready-mix and precast production. We also used standards and guidance from ASTM and ACI, and peer-reviewed cement and concrete journals to cross-check mix design trends, including admixture intensity and cementitious content. Company annual reports, investor presentations, and reputable construction press were used to sanity-check capacity additions and regional demand shifts, while selective paid subscriptions for company financials, news, and patent lookups helped fill gaps around expansions and technology adoption. The sources named here are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where SCC is actually being specified and paid for, since adoption varies by project type and contractor practice. We spoke with ready-mix and precast stakeholders, admixture-focused technical roles, and project-side users to confirm price premiums, typical mix performance targets, and when SCC is switched back to conventional vibrated concrete.

Inputs were also used to tune regional adoption curves and to confirm near-term triggers such as infrastructure tender timing, labor availability, and code-driven durability requirements, which then fed directly into the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 47% |

| Mid tier: 44% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 19% | Managers: 45% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where construction output and infrastructure activity are reconstructed by region, then filtered through SCC penetration by application types that commonly specify it, such as precast products, infrastructure pours, and architecturally exposed elements. To keep totals grounded, we corroborate that view with selective bottom-up approximations, including sampled ready-mix and precast shipment checks, typical SCC price premium ranges, and supplier-side volume signals. These inputs are then used to adjust adoption and pricing assumptions.

Practical inputs used in the model include regional construction spending direction, infrastructure tender awards and project starts, precast production momentum, admixture usage intensity as a proxy for SCC-friendly mixes, and observed SCC price premiums versus conventional mixes in local currencies. Where data is thin, gaps are handled using adjacent-market proxies, for example, ready-mix versus precast split, and then pressure-testing those proxies with interview feedback until the implied volumes and values remain plausible.

For forecasting, scenario analysis is applied around three levers that interviews highlighted, namely infrastructure pipeline timing, labor and productivity constraints that favor SCC, and the pace of specification uptake in precast and high-rebar placements. We convert these scenarios into a central forecast by weighting outcomes that best match the near-term project pipeline and expected pricing progression.

Data Validation & Update Cycle

Outputs are checked against independent signals such as construction output direction, major infrastructure award cycles, and the implied SCC share within ready-mix and precast activity. If a region shows an unusual jump or drop, assumptions are revisited and follow-up calls are triggered to confirm whether the shift reflects a real project wave.

Before sign-off, the model goes through a multi-step analyst review to align input logic, unit consistency, and currency treatment across regions. The report is refreshed annually, and interim updates are made when material events occur, for example, a major capacity addition or a sharp input-cost swing. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Self Consolidating Concrete Scc Market Estimate Compared With Other Published Estimates

Published market sizes for SCC often do not align because the counting rules differ, even when the title uses the same wording. The differences generally trace back to how tightly SCC is defined, how pricing premiums are applied across ready-mix and precast channels, and how currency timing and refresh cadence are handled when construction cycles shift.

Some external estimates take a broader construction materials approach and may blend SCC-like high-flow mixes with conventional concrete upgraded by admixtures. SCC is counted only when it meets the self-placing intent and performance definition in Mordor Intelligence, and value from placing services or vibration equipment is kept out. This keeps totals closer to mix sales rather than total project spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.29 B (2026) | |

| Global Consultancy A | USD 13.06 B (2025) | Uses an earlier base year and a longer horizon, and the 2025 value can reflect different currency conversion timing and a more conservative near-term construction cycle assumption. |

| Industry Publisher B | USD 13.91 B (2025) | May apply a different SCC price-premium progression by application, and it is not always clear how ready-mix versus precast channel splits are normalized across regions. |

The spread in the table mainly comes from year alignment and from how tightly SCC is separated from adjacent high-workability mixes before pricing is applied. By keeping the scope explicit, cross-checking adoption with project-side inputs, and running consistency checks against construction and precast signals, the final total stays traceable to repeatable steps.

Key Questions Answered in the Report

What is driving the fastest growth in the self-consolidating concrete market?

Rapid precast adoption, stricter carbon rules and automation initiatives are combining to push a 6.71% CAGR in the precast segment and a 5.13% CAGR market-wide.

How big will the self-consolidating concrete market be by 2031?

Forecasts indicate USD 19.63 billion by 2031, up from USD 15.29 billion in 2026 at a 5.13% CAGR.

Which region dominates self-consolidating concrete sales today?

Asia-Pacific holds 49.12% of global revenue and is growing fastest at 7.36% through 2031, thanks to infrastructure megaprojects and labor shortages.

Why do precast plants prefer self-consolidating concrete?

The material eliminates vibration, enabling quieter, faster robotic casting lines and 28% productivity gains in controlled factory settings.

Page last updated on: