Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

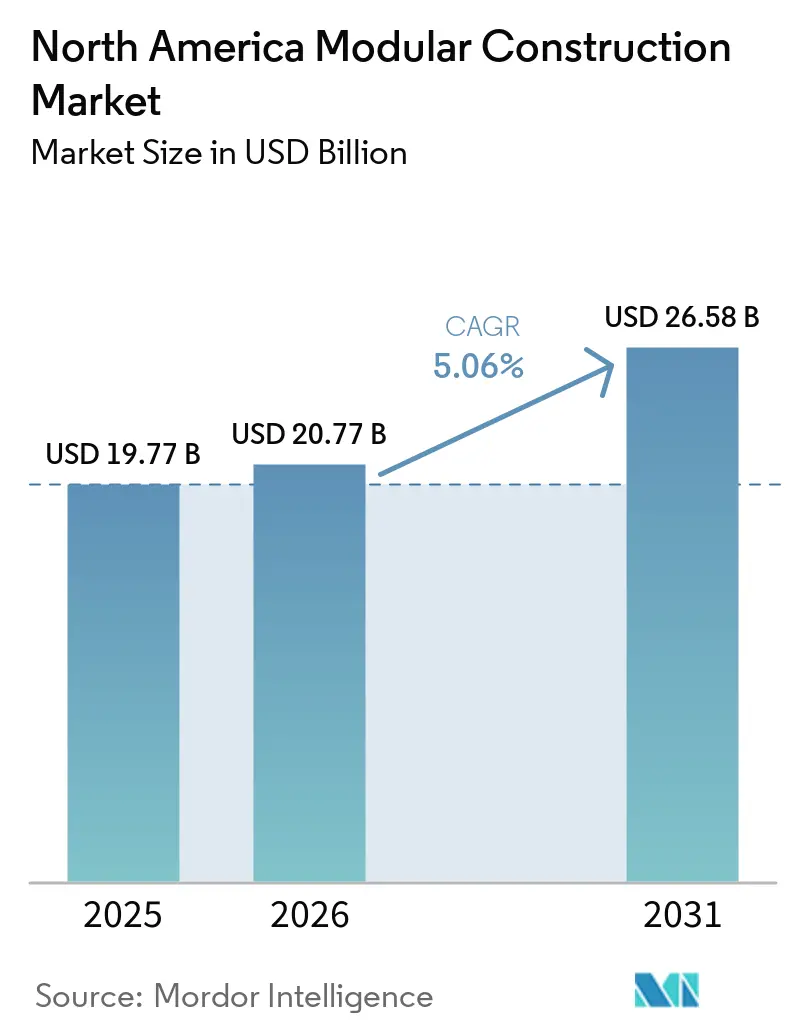

| Base Year Market Size (2025) | USD 19.77 Billion |

| Market Size (2026) | USD 20.77 Billion |

| Market Size (2031) | USD 26.58 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

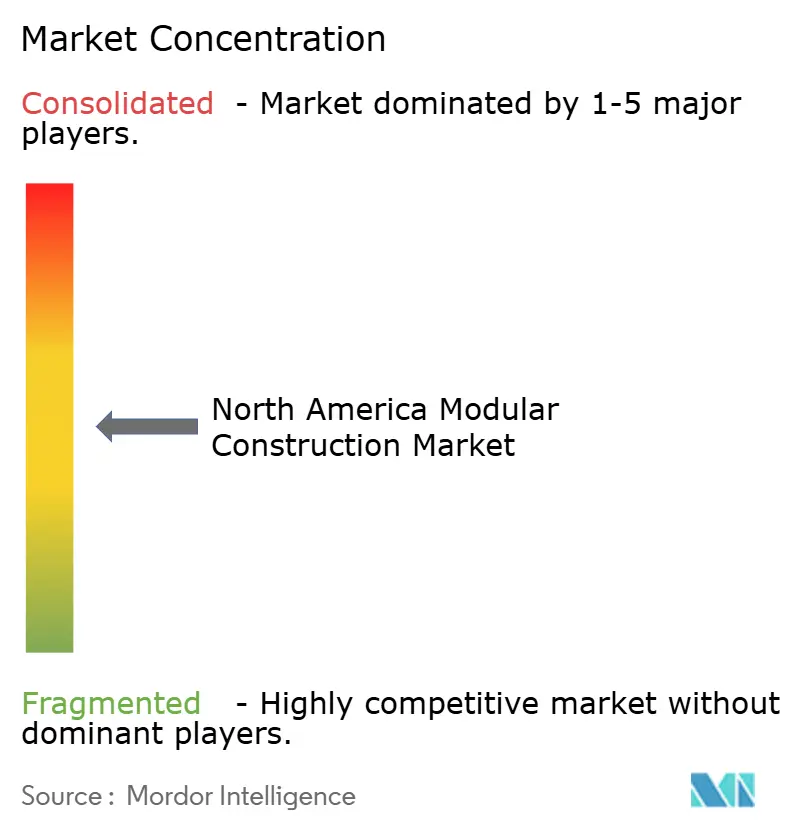

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Modular Construction Market Analysis by Mordor Intelligence

The North America Modular Construction Market size was valued at USD 19.77 billion in 2025 and estimated to grow from USD 20.77 billion in 2026 to reach USD 26.58 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031). Factory-built delivery models are shifting from niche adoption toward baseline project planning as skilled-trade shortages deepen across the United States, Canada, and Mexico. Developers increasingly value predictable schedules, with modular workflows compressing project timelines by up to half, which mitigates financing costs and lease-up risk. Heightened policy support in the United States and Canada, combined with sustainability mandates that reward material efficiency, continues to steer capital toward off-site manufacturing. At the same time, foreign direct investment from precision-manufacturing leaders is injecting automation, robotics, and rigorous quality standards that raise regional competitive thresholds.

Key Report Takeaways

- By construction type, permanent modular solutions held 64.62% of North America modular construction market share in 2025 while relocatable units are projected to record a 5.84% CAGR through 2031.

- By material, steel accounted for 45.73% share of the North America modular construction market size in 2025, whereas wood-based systems are forecast to expand at a 6.12% CAGR through 2031.

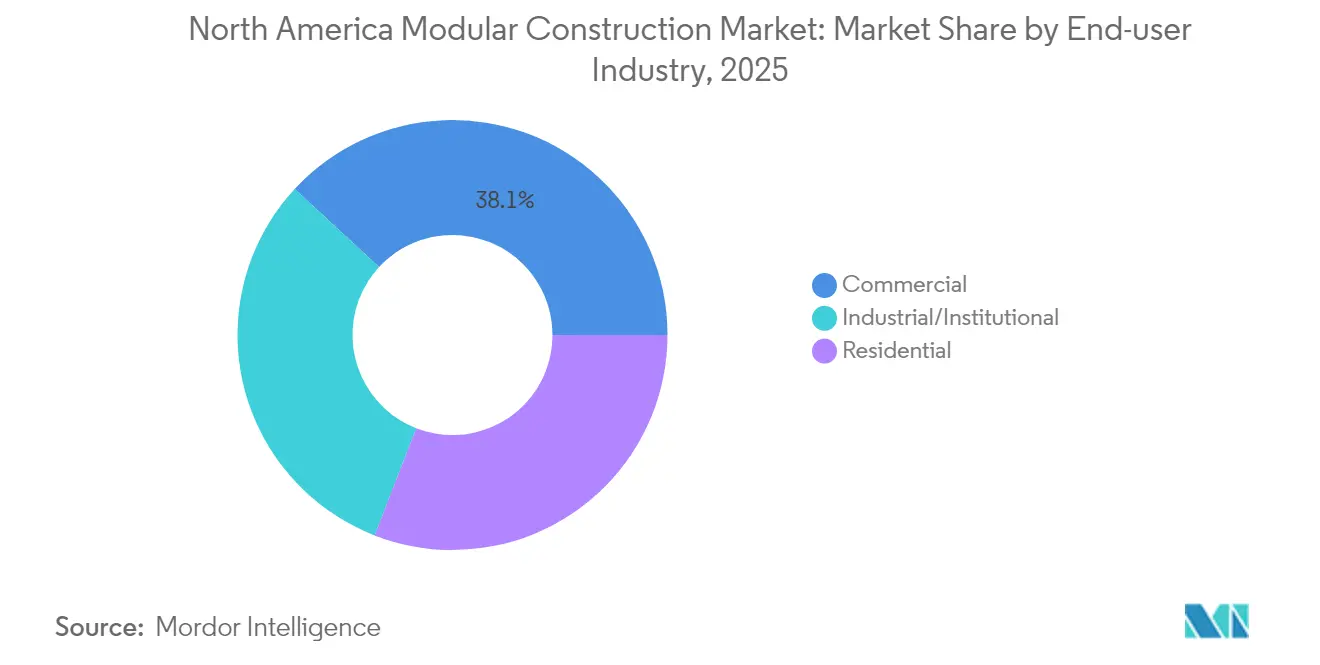

- By end-user industry, commercial applications led with 38.12% revenue share in 2025 in the North America modular construction market, yet residential demand is expected to grow at a 6.78% CAGR to 2031.

- By geography, the United States captured 78.91% share of the North America modular construction market in 2025 and is projected to advance at a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Modular Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Faster completion than conventional builds | +1.2% | United States metro cores | Medium term (2-4 years) |

| Labor-shortage pressure on site-built housing | +1.8% | Canada and U.S. Southwest | Long term (≥ 4 years) |

| Green-building mandates and waste reduction | +0.9% | California and several Canadian provinces | Long term (≥ 4 years) |

| Government incentives and code alignment | +0.7% | Federal and provincial programs | Medium term (2-4 years) |

| Hyperscale data-center shell demand | +0.6% | U.S. and Canadian technology corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Short Construction Timelines vs. Conventional Builds

Parallel site preparation and factory production routinely trim schedules by 30-50%, a decisive factor for investors seeking rapid revenue activation in the North America modular construction market. Large multifamily developers now embed modular execution into baseline pro-formas to hedge against weather-related downtime and labor bottlenecks. Digital production tracking synchronizes fabrication with just-in-time on-site craning, which secures critical-path activities such as façade installation and MEP commissioning. Quicker delivery also aligns with public-sector procurement targets that mandate occupancy within specified fiscal windows. Nevertheless, projects that require extensive design revisions during fabrication can erode speed advantages if approvals lag behind manufacturing queues.

Labor-Shortage Pressure on Site-Built Housing

The industry faced a shortfall of roughly 439,000 craft professionals in 2025, while one-fifth of the existing workforce is approaching retirement. By shifting trade-intensive work into climate-controlled plants, modular producers leverage specialization that elevates output per worker and stabilizes year-round employment in the North America modular construction market. Regionally unbalanced housing activity—from surging Atlantic Canada starts to slower Alberta pipelines—encourages national builders to source modules from hubs where talent pools remain deeper. In factory environments apprenticeship programs can operate consistently, whereas rotating field crews undermine training continuity.

Rising Green-Building Mandates and Waste-Reduction Goals

Factory precision drives material yield improvements that cut construction waste by roughly 50% and lower embodied carbon footprints. Energy-code leaders such as California favor envelope quality that is easier to demonstrate under plant-controlled conditions. Enhanced traceability of sourced lumber, steel, and insulation underpins certification pathways for LEED and net-zero frameworks. As embodied-carbon accounting accelerates, proprietary life-cycle assessment software is becoming a standard pre-bid deliverable for North America modular construction market participants.

Government Incentives and Code Adoption for Modular

Updated versions of the International Building Code and commitments under Canada’s National Housing Strategy streamline review pathways for volumetric modules, reducing duplicative inspections in the North America modular construction market. State-level adoption of ICC/MBI protocols in Virginia and others trims weeks from permitting calendars, directly improving project net present value. Federal grants that prioritize quick-turn social infrastructure additionally direct funds toward modular bids that guarantee delivery within program-year budgeting cycles. Ongoing challenges include inconsistent oversize-permit processes among U.S. states, which add administrative cost to multi-jurisdictional logistics.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital and logistics costs | -0.8% | Smaller developers across all three countries | Medium term (2-4 years) |

| Quality-perception and design-flexibility doubts | -0.5% | U.S. and Canada | Long term (≥ 4 years) |

| Interstate oversize-load transport rules | -0.3% | Key U.S. corridors and U.S.–Canada border crossings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Capital and Logistics Costs

Launching a volumetric plant can require USD 10–50 million for line equipment, automated gantries, and quality-control labs in the North America modular construction market. Completed modules often travel hundreds of miles on escorted carriers, with freight representing as much as 15% of installed cost when fuel surcharges spike. Tariff exposure on imported steel and lumber further complicates fixed-price quoting. Small-scale developers struggle to finance such outlays unless long-term pipeline commitments lock in utilization above breakeven thresholds. Consolidation among regional haulers specializing in over-dimensioned cargo is underway to mitigate fragmented transport capacity.

Quality-Perception and Design-Flexibility Concerns

Legacy associations with low-end manufactured housing still influence lender underwriting and buyer expectations in some sub-markets of the North America modular construction market. Although leading producers now offer high-grade finishes and mass-customized façades, luxury single-family buyers frequently equate factory production with stylistic limits. Certification programs such as ICC/MBI Acceptance Criteria 462 and ISO-9001 audits are helping re-frame perceptions by validating structural longevity and energy performance. Digitally driven kitting techniques can now accommodate high-mix floor plans, yet extensive bespoke features lengthen shop-drawing cycles and dilute throughput gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Construction: Permanent Solutions Drive Market Maturation

Permanent units accounted for 64.62% of the North America modular construction market in 2025, underscoring the segment’s ascendance from temporary classrooms to code-compliant multifamily and office assets. Clearer mortgage guidance and insurer parity with site-built structures underpin financing acceptance, while agencies purchasing securities now treat volumetric apartments equivalently to stick-built comparables. The segment’s acceleration reflects landlords’ preference for predictable life-cycle costs and tighter building envelopes that lower tenant energy expenses.

The relocatable sub-category is projected to grow at a 5.84% CAGR through 2031, propelled by disaster relief, remote workforce housing, and flexible educational capacity. Manufacturers increasingly offer hybrid chassis that bolt permanently yet can be disassembled if repurposing becomes attractive. Such optionality appeals to public agencies wary of stranded assets when demographic shifts alter space demand.

By Material: Steel Dominance Faces Wood Innovation

Steel solutions held 45.73% share of the North America modular construction market size in 2025, favored for mid-rise hotels, student housing, and data-center shells requiring long spans and high fire ratings. Welded box sections and cold-formed studs meet seismic codes prevalent along the Pacific Rim and deliver consistent tolerances critical for stacking accuracy. Steel prices have moderated from pandemic peaks, supporting cost planning.

Wood is forecast to expand at a 6.12% CAGR, buoyed by cross-laminated timber (CLT) and glue-laminated beams that now reach 18 stories in select jurisdictions. Modular CLT panels arrive with integrated insulation and vapor control, enabling Passivhaus-level performance. Bio-based sequestered carbon advantages resonate with ESG-focused investors seeking reductions in Scope 3 emissions. Regional sawmill proximity in British Columbia and the U.S. Pacific Northwest provides logistics savings, narrowing steel’s historical cost advantage.

By End-User Industry: Residential Growth Outpaces Commercial Leadership

Commercial applications commanded 38.12% share of the North America modular construction market size in 2025, historically driven by hospitality chains standardizing guest-room pods for uniformity and rapid refresh cycles. Recent office retrofits incorporate modular façade upgrades that minimize tenant displacement. Institutional clients such as hospitals favor volumetric rooms for infection-control compliance, delivering pre-certified HVAC modules that slot into live campuses.

Residential demand is projected to climb at a 6.78% CAGR to 2031, reflecting affordability imperatives in gateway metros and remote community housing programs. Sekisui House’s USD 4.95 billion strategic entry via acquisition of MDC Holdings brought Japanese robotics, precision jigging, and zero-energy home platforms to the United States, demonstrating foreign confidence in long-run suburban growth. Multifamily developers targeting tax-credit allocations increasingly rely on modular stacking to satisfy delivery deadlines required for credit capture.

Geography Analysis

The United States dominated with 78.91% market share in 2025, driven by deep capital markets, high labor costs, and federal infrastructure outlays that prioritize shovel-ready execution. The Bipartisan Infrastructure Law funnels USD 550 billion toward transport and broadband upgrades, with design-build procurements rewarding schedule certainty. State variation persists; Virginia’s early adoption of ICC/MBI standards trims approval cycles, whereas California’s seismic testing protocols add upfront engineering but offer long-term resilience branding. Land-heavy Sunbelt counties grant zoning bonuses for factory-assembled workforce housing, widening adoption outside traditional coastal strongholds.

Canada benefits from the National Housing Strategy’s emphasis on innovative delivery for both urban densification and remote community relief. Provincial planners leverage volumetric units to assemble winterized dwellings in fly-in northern territories where short construction seasons constrain on-site execution. The Nunavut 3000 initiative illustrates scale, with more than 50 of 114 2025 contracts awarding modular procurement to accelerate occupancy before seasonal ice roads close.

Mexico remains nascent yet strategically important as near-shoring trends propel manufacturing corridors along Nuevo León and Chihuahua. U.S.–Mexico–Canada Agreement provisions for duty-free component movement support cross-border module supply, though domestic code harmonization lags behind northern neighbors. Early adopters include multinational electronics firms erecting expansion space adjacent to maquiladoras through turnkey modular lines assembled in Texas and craned across the border.

Competitive Landscape

North America’s modular ecosystem is moderately fragmented, with a long tail of regional fabricators supplying fewer than 300 units annually, while only a handful exceed 5,000 units. Consolidation is accelerating; Sekisui House’s acquisition of MDC Holdings instantly added U.S. distribution reach to advanced Japanese panelization know-how. Technology integration differentiates front-runners. Skender’s Chicago facility embodies the vertically integrated design-engineer-manufacture-construct model, using BIM-to-robot workflows that drive tolerance to ±1 mm and enable field stacking without shim packs[2]Jeff Yoders, “Skender Pursues a Mission to Boost Its Modular Capabilities,” ENR, enr.com . Competitors invest in computer-numerical-control routers and automated stud-framing lines to cut labor minutes per module, directly improving contribution margins in the North America modular construction market.

North America Modular Construction Industry Leaders

ATCO Ltd.

Boxx Modular (Black Diamond Group)

Clayton

Mobile Modular Management Corporation (McGrath RentCorp, Inc.)

WillScot

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sekisui House’s Sommers Bend community in California captured four Gold Awards at The Nationals 2025, signaling mainstream U.S. recognition for the SHAWOOD precision-manufactured wood-frame system.

- January 2025: Cavco Industries completed the purchase of American Homestar Corporation, adding two Texas plants and multiple retail centers to expand regional reach in factory-built housing.

North America Modular Construction Market Report Scope

Modular construction is a construction technique that involves the prefabrication of 2D panels or 3D volumetric structures in off-site factories and transportation to construction sites for assembly. This process has the potential to be superior to traditional construction in terms of both time and cost. The North American modular construction market is segmented by type, sector, and country. By type, the market is segmented into permanent, and relocatable. By sector, the market is segmented into residential, and commercial. By country, the market is segmented into the United States, Canada, and Mexico.

By Construction

| Permanent Modular |

| Relocatable Modular |

By Material

| Steel |

| Wood |

| Concrete |

| Plastic |

By End-user Industry

| Commercial |

| Industrial/Institutional |

| Residential |

By Geography

| United States |

| Canada |

| Mexico |

| By Construction | Permanent Modular |

| Relocatable Modular | |

| By Material | Steel |

| Wood | |

| Concrete | |

| Plastic | |

| By End-user Industry | Commercial |

| Industrial/Institutional | |

| Residential | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America modular construction market in 2026?

The North America Modular Construction Market is valued at USD 20.77 billion with a 5.06% CAGR forecast to 2031.

Which construction type currently leads adoption?

Permanent modular solutions held 64.62% share in 2025.

Which material is gaining fastest in modular applications?

Engineered wood systems are projected to grow at a 6.12% CAGR through 2031.

Why does the United States dominate regional demand?

Deep capital markets, federal infrastructure funding, and acute labor shortages give the U.S. 78.91% share and continued 5.63% CAGR growth.

What restrains smaller developers from using modular?

High upfront factory investments and oversize-load logistics can elevate cost by 15% of the project budget.

Which company recently expanded its U.S. presence through acquisition?

Sekisui House invested USD 4.95 billion to acquire MDC Holdings and scale its SHAWOOD platform in North America.

Page last updated on: