Lightweight Aggregate Concrete Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.29 Billion |

| Market Size (2031) | USD 12.59 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lightweight Aggregate Concrete Market Analysis by Mordor Intelligence

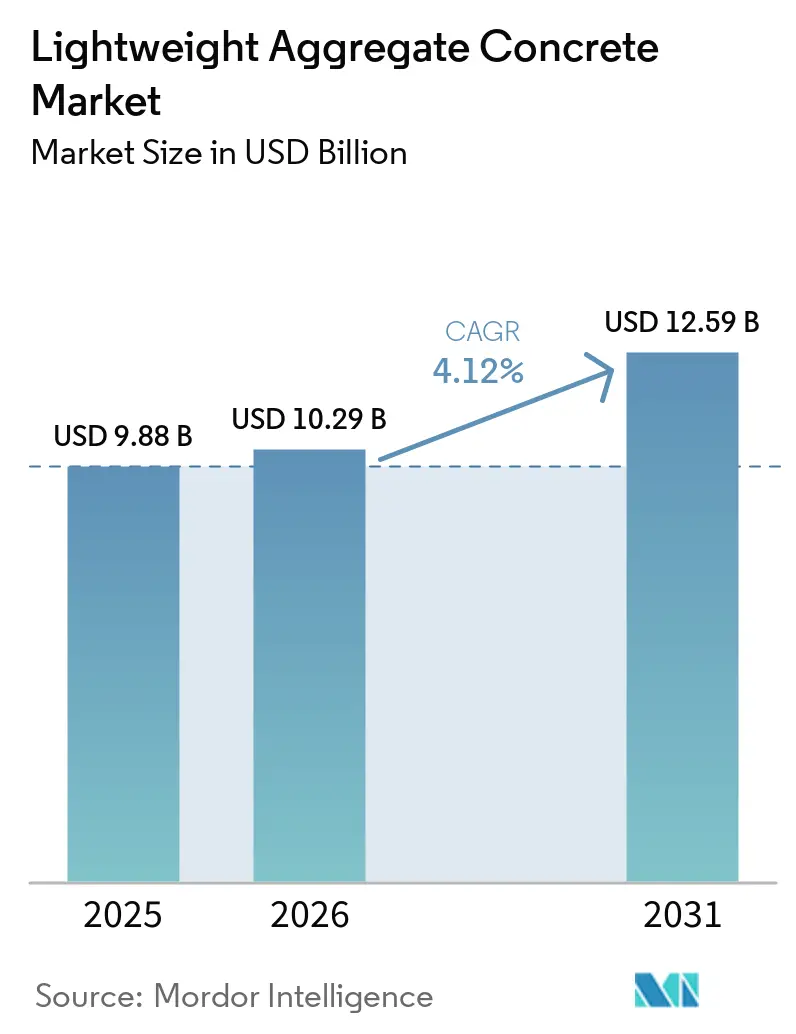

The Lightweight Aggregate Concrete Market size is expected to grow from USD 9.88 billion in 2025 to USD 10.29 billion in 2026 and is forecast to reach USD 12.59 billion by 2031 at 4.12% CAGR over 2026-2031. Rising demand is attributed to infrastructure retrofits, offshore energy platforms, and modular building systems that emphasize lower dead-load, multi-functional performance, and reduced embodied carbon. Producers are reallocating capital toward higher-margin structural grades, as shown by Arcosa’s divestiture of its barge unit and its acquisition of aggregate assets in the U.S. Southeast. At the same time, vertical integration in cementitious binders, reflected in recent acquisitions by Heidelberg Materials and CRH, suggests that global companies view low-carbon, lightweight formulations as a significant revenue opportunity. Regulatory measures, such as recycled-content mandates in China and stricter insulation codes in North America and Europe, are accelerating adoption. However, supply-side constraints on premium aggregates continue to create moderate price pressure, driven by declining coal fly-ash volumes and increasing shipping distances for expanded shale and slate.

Key Report Takeaways

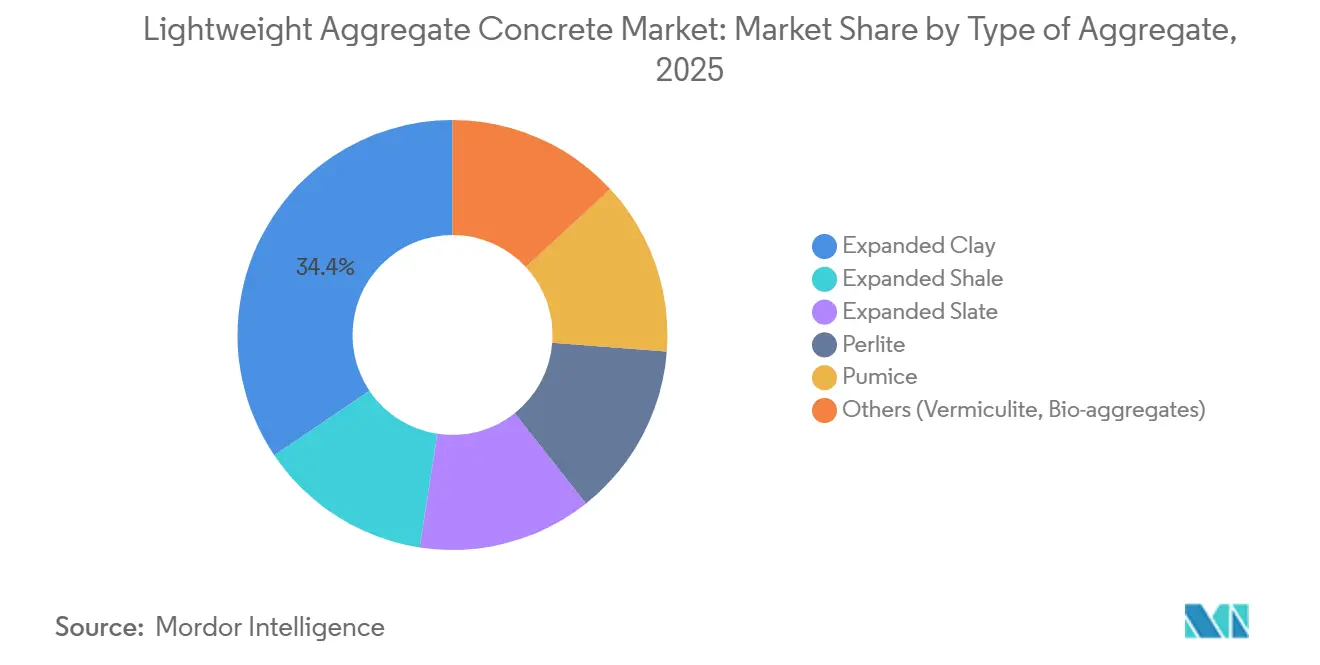

- By type of aggregate, expanded clay led with 34.44% revenue share in 2025, while perlite is projected to expand at a 4.28% CAGR through 2031.

- By application, structural concrete captured 37.82% of the lightweight aggregate concrete market share in 2025, and precast and prefabricated elements are forecast to grow at 4.58% through 2031.

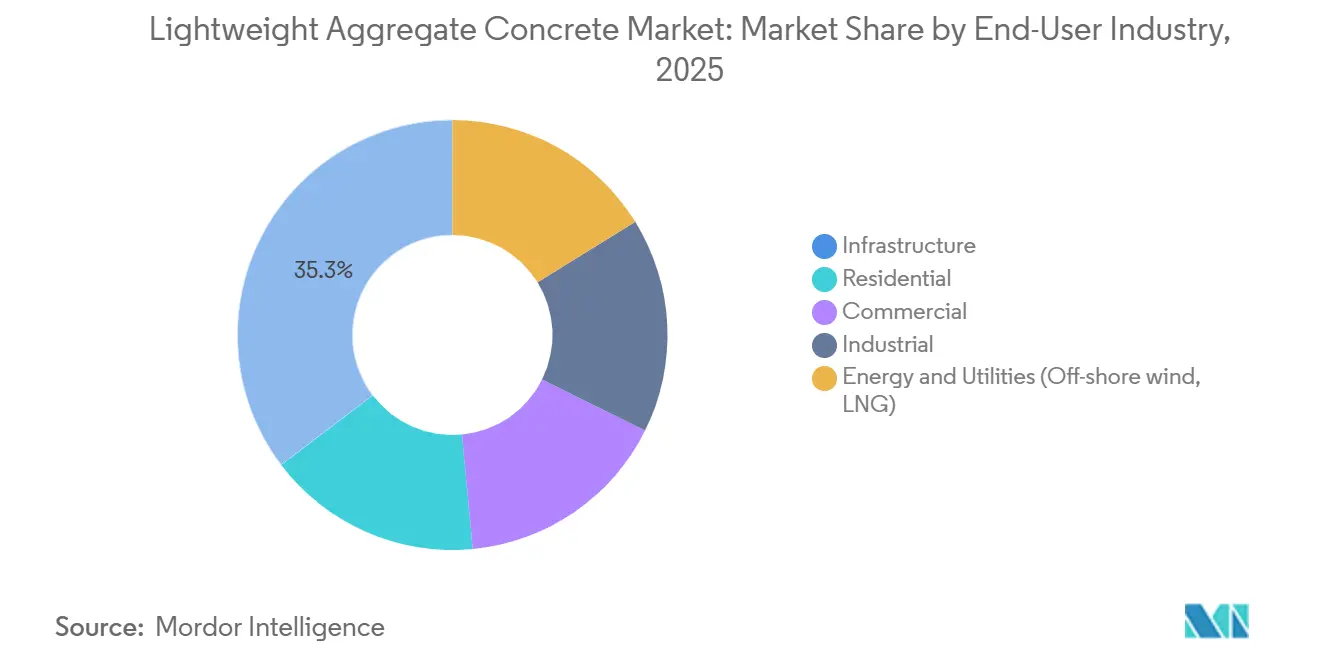

- By end-user industry, infrastructure accounted for 35.33% of 2025 revenue, whereas energy and utilities recorded the highest projected CAGR at 3.81% to 2031.

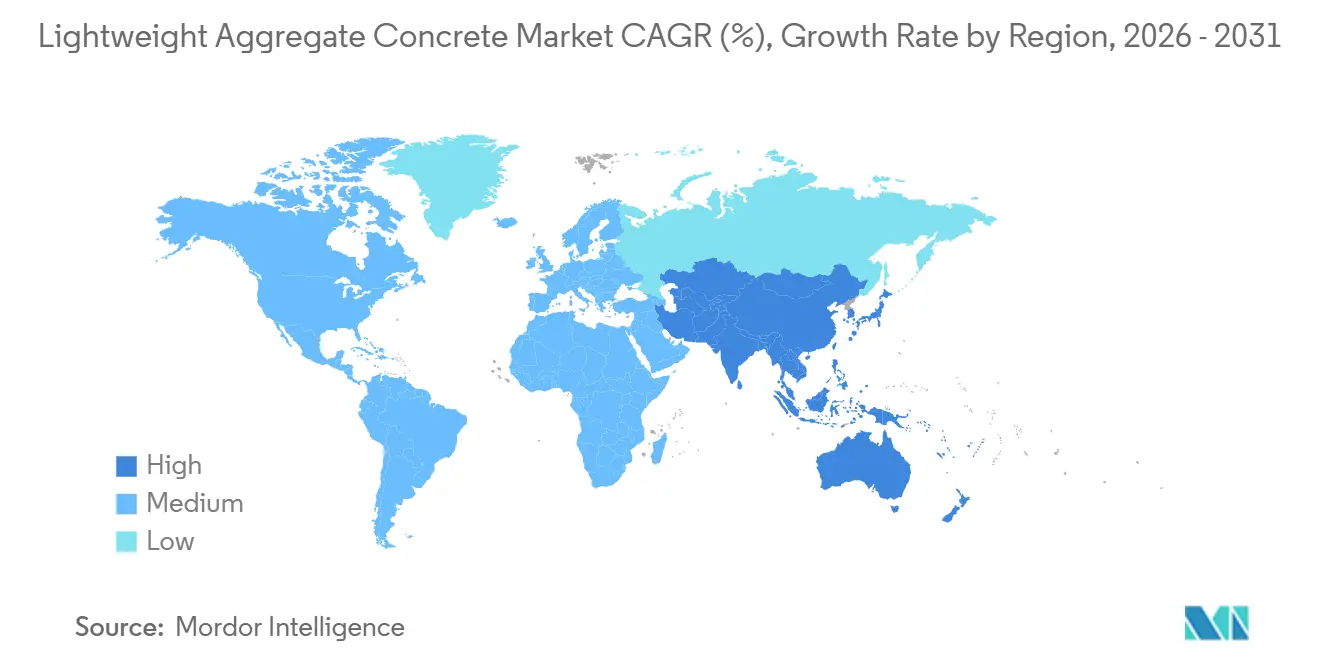

- By geography, Asia-Pacific retained 47.89% share in 2025 and is set to register the highest 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lightweight Aggregate Concrete Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Lightweight and High-Strength Construction Materials | +1.2% | Global, with concentration in Asia-Pacific high-rise corridors and North American precast hubs | Medium term (2-4 years) |

| Increasing Use in High-Rise and Precast Structures | +1.0% | Asia-Pacific (China, India, Southeast Asia), North America (Mid-Atlantic, Florida), Europe (Germany, Austria) | Medium term (2-4 years) |

| Reduction in Dead Load Enabling Cost-Efficient Designs | +0.8% | Global, particularly infrastructure-heavy regions (Asia-Pacific, North America, the Middle East) | Long term (≥ 4 years) |

| Stricter Energy-Efficiency and Insulation Codes | +0.7% | Europe (EN standards), North America (Florida Building Code, ASHRAE), and emerging in the Asia-Pacific | Short term (≤ 2 years) |

| Emerging 3D-Printed Concrete Applications | +0.4% | North America, Europe (R&D clusters), pilot deployments in the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweight and High-Strength Construction Materials

Project engineers are specifying lightweight aggregate concrete to achieve span-to-depth ratios that exceed the capabilities of normal-weight mixes. This enables the construction of 100-meter prestressed bridge girders without surpassing deflection limits. Rotary-kiln shale aggregates have demonstrated compressive strengths of 6,000 pounds per square inch (psi) at densities around 1,920 kilograms per cubic meter (kg/m³), showing that reducing mass does not compromise strength. Research conducted in 2025 highlighted lightweight ultra-high-strength formulations achieving compressive strengths of 102-123 megapascals (MPa) while reducing self-weight by up to 20%[1]MDPI Editorial Team, “Lightweight Ultra-High-Strength Concrete Performance,” mdpi.com. In seismic regions such as Japan and California, lower dead loads directly reduce base shear, leading to cost savings in foundation construction. Holcim’s ECOPact platform combines lightweight aggregates with supplementary cementitious materials to achieve LC60 classes while reducing embodied carbon dioxide (CO₂) by 30-50%, demonstrating that structural performance and decarbonization objectives can align.

Increasing Use in High-Rise and Precast Structures

Labor shortages are driving developers toward modular and precast construction methods, where pumpability and lighter panels help reduce crane cycle times. For instance, a 2025 balcony retrofit project in Halle-Neustadt utilized Liapor LC30/33D1.8, successfully pumping concrete to the 18th floor and completing 220 slabs within weeks, showcasing vertical conveyance without segregation. Case studies in Hong Kong revealed a 10.1% reduction in embodied carbon for non-structural floors after substituting lightweight materials, with even greater benefits when prefabrication is adopted. In India, suppliers are promoting lightweight mixes that also function as passive cooling masses in tropical high-rise buildings. Additionally, fabricators using welded-wire mesh and glass fibers in lightweight expanded clay aggregate (LECA)-based self-consolidating slabs report a 45% increase in load-carrying capacity compared to unreinforced alternatives.

Reduction in Dead Load Enabling Cost-Efficient Designs

On soft soils, foundation and substructure costs can account for up to 30% of total project expenses. Reducing self-weight offers direct capital savings. For example, Germany’s Xaver-Hafner-Brücke widening project reduced approximately 100 tons by using LC30/33D1.6, eliminating the need for an entire pier reinforcement scope. Horizon-Europe’s MADE4WIND initiative is developing 50 MPa compressive strength lightweight concrete for half-thickness shells in floating turbines, reducing steel reinforcement requirements and enhancing platform stability. Comparative cost analyses indicate that prestressed ultra-high-performance concrete (UHPC) floating foundations cost EUR 450-500 (USD 525.58-583.98) per ton, which is one-fifth the price of equivalent steel jackets for deep-water applications.

Stricter Energy-Efficiency and Insulation Codes

Stricter energy-efficiency and insulation codes in the European Union (EU) and North America are driving the integration of insulation into load-bearing walls. Lightweight aggregate concrete with perlite achieves thermal conductivity as low as 0.08 watts per meter-kelvin (W/mK), meeting Passive House standards in a single wythe. Florida’s hurricane codes reference ASTM C330-series standards, while lighter screeds help reduce uplift forces on roof decks. Testing conducted in 2025 demonstrated 240-minute fire resistance in 3D-printed perlite walls with a thickness of 4 inches, meeting American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 90.1 requirements. Verified Environmental Product Declarations (EPDs) for expanded clay under European Norm (EN) 15732 standards now enable European projects to secure Building Research Establishment Environmental Assessment Method (BREEAM) and Leadership in Energy and Environmental Design (LEED) certifications while aligning with 2030 carbon reduction targets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost Versus Conventional Concrete | -0.6% | Global, most acute in price-sensitive residential and light commercial segments in Asia-Pacific and South America | Short term (≤ 2 years) |

| Scarcity of Premium Lightweight Aggregates | -0.3% | North America (fly-ash supply tightening), Europe (expanded shale capacity constraints), emerging in Asia-Pacific | Medium term (2-4 years) |

| Moisture-Induced Variability in Mechanical Properties | -0.2% | Global, particularly in humid climates (Southeast Asia, coastal regions) and projects with inadequate pre-wetting protocols | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Cost Versus Conventional Concrete

Lightweight concrete mixes incur a 15-25% cost premium due to the rotary-kiln energy requirements of 1.5-2.0 gigajoules (GJ) per ton, significantly higher than the 0.5 GJ per ton for crushed stone[2]Liapor, “Energy Demand of Rotary Kiln Expanded Clay,” liapor.com. While sintered fly-ash technology reduces fuel consumption, turnkey plants remain 30-40% more expensive than crushing units. Developers with single-digit profit margins face challenges in transferring these additional costs to homebuyers, limiting the use of lightweight concrete to high-end construction projects. Value-engineering studies indicate 5-10% total project savings when accounting for foundation costs, crane time, and schedule compression, but these life-cycle benefits are often overlooked due to siloed procurement practices.

Scarcity of Premium Lightweight Aggregates

The decline in coal plant operations is reducing fly-ash supplies by double digits annually, prompting producers to turn to alternatives such as reservoir silt, demolition waste, and industrial sludge, which require expensive beneficiation processes. Cemex’s 2024 acquisition of a Berlin recycling facility added 400,000 tons per annum (tpa) of capacity but still falls short of meeting projected demand growth. Geographic concentration further exacerbates the supply gap; for instance, delivered prices of expanded shale in the U.S. Pacific Northwest can exceed USD 150 per ton, which is 50-70% higher than prices in Mid-Atlantic markets. Additionally, the exploration of perlite deposits in Central Asia and East Africa involves permitting lead times of 12-18 months, creating supply chain risks for large-scale projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Aggregate: Expanded Clay Performs, Perlite Advances

Expanded clay accounted for 34.44% of the lightweight aggregate concrete market in 2025, supported by established rotary-kiln infrastructure in Europe and Asia-Pacific. Perlite is the fastest-growing aggregate, with a projected growth rate of 4.58% through 2031. The market size associated with this segment is expected to grow steadily, driven by its suitability for bridge builders and retrofitting agencies due to its strength classes exceeding 40 megapascals (MPa). Perlite is anticipated to grow 16 basis points faster than the overall aggregate category, benefiting from its low thermal conductivity of 0.08 watts per meter-kelvin (W/mK), which is particularly suitable for 3D printing and ultra-insulating screeds.

In the United States, expanded shale and slate are widely used in structural applications requiring densities above 1,600 kilograms per cubic meter (kg/m³) and compressive strengths exceeding 6,000 pounds per square inch (psi), as demonstrated by projects like California’s Shasta Arch Bridge. Pumice is primarily used in decorative and landscaping applications, with sourcing concentrated in the western United States and the Aegean region. Vermiculite and emerging bio-aggregates together account for less than 5% of the market volume due to cost and durability constraints. In China, pre-screened reservoir-silt pellets are expected to diversify supply once JC/T 2772-2024 standards enable non-structural applications up to LC25.

By Application: Precast Surges on Modular Timelines

Structural cast-in-place concrete held the largest share of the lightweight aggregate concrete market in 2025, accounting for 37.82%. Precast and prefabricated elements are the fastest-growing segment, with a forecasted growth rate of 4.58% through 2031. This growth is driven by factors such as reduced crane cycle times, lower labor costs, and improved carbon accounting, which are reshaping job-site economics. For instance, pumpable mixes used in Germany have demonstrated the feasibility of reaching 18th-floor balconies without the need for heavy tower cranes, making high-rise retrofits more efficient.

Block and panel manufacturers prioritize insulation and weight reductions that meet Passive House U-value standards without requiring exterior cladding. Lightweight self-consolidating composite slabs reinforced with glass-fiber mesh now offer 45% higher load capacities while reducing weight by 20-30 kilograms per square meter (kg/m²), enabling thinner floor plates and lower inter-story heights. In the U.S. mid-Atlantic region, more than 5,000 cubic yards (yd³) of ultra-high-performance concrete (UHPC) overlay was installed on the Delaware Memorial Bridge, marking the first suspension bridge to adopt such a system. This demonstrates that lightweight UHPC can rehabilitate aging infrastructure without necessitating new pier caps.

By End-User Industry: Infrastructure Leads, Energy & Utilities Accelerate

The infrastructure segment accounted for 35.33% of revenue in 2025, driven by bridge upgrades, rail deck replacements, and road widening projects that replace heavy concrete with lightweight alternatives to avoid substructure expansion. The energy and utilities sector is experiencing the highest growth, with a CAGR of 3.81%. This growth is supported by applications such as offshore wind gravity foundations and liquefied natural gas (LNG) terminal slabs, where material weight directly impacts buoyancy and pile requirements.

In residential construction, lightweight concrete is increasingly used in high-rise Asian cities for partitions and roof fills, enhancing thermal comfort and reducing heating, ventilation, and air conditioning (HVAC) loads. In Europe, commercial developers are adopting monolithic lightweight concrete envelopes to eliminate thermal bridges and achieve Deutsche Gesellschaft für Nachhaltiges Bauen (DGNB) Gold certification. Industrial floors and mezzanines utilize low-density screeds to minimize loads on soft soils, while logistics centers in Switzerland have demonstrated 72-hour trafficability, significantly reducing commissioning times.

Geography Analysis

Asia-Pacific accounted for 47.89% of the projected 2025 revenue and is expected to grow at a rate of 6.11% through 2031, nearly 50% higher than the global lightweight aggregate concrete market growth rate. In China, the JC/T 2772-2024 mandate for recycled content in lightweight aggregates has introduced new supply chains, diverting demolition waste from landfills. Additionally, 26-story towers in Benxi demonstrated a 21-25% reduction in self-weight, leading to smaller seismic base shear forces. In India, precast operators have reduced project timelines by up to 50% using branded lightweight mixes, which also serve as passive cooling mass in tropical climates. Japan’s adoption is driven by seismic performance improvements, with lightweight ultrahigh-strength concrete achieving 100 megapascals (MPa) strength at densities below 2,100 kilograms per cubic meter (kg/m³).

North America’s market growth is supported by Arcosa’s kiln network, strategic mergers and acquisitions, and Bridge Authority pilot projects. Following a USD 450 million barge divestiture and a USD 60 million aggregate acquisition in Florida, Arcosa has redirected capital toward higher-margin infrastructure-grade products. Titan America’s artificial intelligence (AI)-enabled mix design platform optimizes performance and carbon footprint predictions, reducing quotation cycles from weeks to hours. Florida’s regulatory endorsement of lightweight roof fills for hurricane-prone areas highlights growing regional acceptance.

Europe emphasizes carbon reduction and heritage rehabilitation. Projects such as the Kabelstraßen-Brücke in Wuppertal and the bridge widening in Straubing achieved 100-ton weight savings, preserving existing structural piers. Norway’s BetongVIND initiative and the Horizon-Europe MADE4WIND consortia are positioning lightweight concrete as a critical component for deep-water wind projects, targeting an 80% reduction in carbon dioxide (CO₂) emissions for serial gravity-foundation production. In the United Kingdom, LECA’s third-party-verified Environmental Product Declarations (EPDs) support buildings in securing Building Research Establishment Environmental Assessment Method (BREEAM) credits while aligning with 2030 carbon reduction goals.

South America benefits from Votorantim Cimentos’ BRL 5 billion (USD 0.97 billion) expansion, which will increase Mato Grosso’s production capacity to 1.2 million tons and achieve a 90% renewable energy grid mix by March 2026. The Middle East and Africa are in the early stages of adoption, with applications concentrated in Saudi Arabia’s high-rise cores and liquefied natural gas (LNG) terminals, where weight reductions help minimize quay wall reinforcement. However, reliance on imports and high freight costs remain significant barriers to broader regional uptake.

Competitive Landscape

The lightweight aggregate concrete market remains moderately fragmented. Regional companies such as Liapor, Leca International, and Poraver maintain established positions in Central Europe, operating long-standing rotary-kiln production lines and fostering direct relationships with precasters. Global companies, including HOLCIM, Cemex S.A.B. de C.V., and Heidelberg Materials AG, are utilizing their ready-mix networks to promote lightweight grades while acquiring supplementary cementitious material (SCM) suppliers to ensure binder availability. Upstream, feedstock shortages have led to actions such as Cemex’s acquisition of a Berlin-based recycler, while downstream, digitalization initiatives like Titan America’s artificial intelligence (AI) platform are reducing design costs and quotation times.

Arcosa’s planned shift by 2026 away from marine logistics highlights its focus on structural infrastructure mixes that command higher pricing. Heidelberg Materials’ USD 600 million acquisition of Giant Cement and CRH’s USD 2.1 billion purchase of Eco Material demonstrate vertical integration efforts to secure low-carbon binder inputs critical for lightweight grades. New market entrants, such as Boral Resources, are introducing innovations like sintered fly-ash pellets, which utilize residual carbon as fuel. These pellets, produced at a capacity of 50,000 tons per annum in Poland, offer bulk densities of 550-720 kilograms per cubic meter (kg/m³), suitable for high-performance concrete applications.

Growth opportunities are emerging in areas such as offshore wind foundations, 3D-printed structural components, and recycled aggregate supply. GICON’s prestressed ultra-high-performance concrete (UHPC) floats reduce costs to one-fifth of the steel cost curve for waters deeper than 60 meters. Perlite’s nozzle-compatible shape prevents clogging in 3D-printed walls, while Cemex’s Regenera initiative targets 14 million tons per annum of recycled input by 2030, though this remains below the projected increase in European demand.

Lightweight Aggregate Concrete Industry Leaders

Arcosa Lightweight

Cemex S.A.B DE C.V.

CRH

Heidelberg Materials AG

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Arcosa acquired a Florida aggregates operation for USD 60 million, increasing its rotary-kiln expanded shale and clay production capacity in the Southeast. This acquisition supports the production of lightweight aggregate concrete and reinforces its position as the largest lightweight aggregate producer in North America.

- January 2026: Norway's BetongVIND consortium has initiated a NOK 20 million (USD 1.9 million) project aimed at developing serial production of gravity-based concrete foundations for offshore wind. The project aims to achieve an 80% reduction in carbon dioxide (CO2) emissions compared to conventional designs by utilizing optimized lightweight aggregate concrete mixes and modular fabrication methods.

Global Lightweight Aggregate Concrete Market Report Scope

Lightweight aggregate concrete is a type of concrete that uses porous, low-density materials such as expanded clay, shale, or pumice instead of conventional gravel or stone. This type of concrete reduces structural dead loads, enhances thermal and sound insulation, and provides high fire resistance, typically weighing less than standard concrete.

The lightweight aggregate concrete market is segmented by type of aggregate, application, end-user industry, and geography. By type of aggregate, the market is segmented into expanded clay, expanded shale, expanded slate, perlite, pumice, and others (vermiculite, bio-aggregates). By application, the market is segmented into structural concrete, precast and prefabricated elements, block and panel production, bridge decks and infrastructure, insulating screeds and roof fills, and others. By end-user industry, the market is segmented into residential, commercial, industrial, infrastructure, and energy and utilities (off-shore wind, LNG). The report also covers the market size and forecasts for lightweight aggregate concrete in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Expanded Clay |

| Expanded Shale |

| Expanded Slate |

| Perlite |

| Pumice |

| Others (Vermiculite, Bio-aggregates) |

| Structural Concrete |

| Precast/Prefabricated Elements |

| Block and Panel Production |

| Bridge Decks and Infrastructure |

| Insulating Screeds and Roof Fills |

| Others |

| Residential |

| Commercial |

| Industrial |

| Infrastructure |

| Energy and Utilities (Off-shore wind, LNG) |

| Asia-pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type of Aggregate | Expanded Clay | |

| Expanded Shale | ||

| Expanded Slate | ||

| Perlite | ||

| Pumice | ||

| Others (Vermiculite, Bio-aggregates) | ||

| By Application | Structural Concrete | |

| Precast/Prefabricated Elements | ||

| Block and Panel Production | ||

| Bridge Decks and Infrastructure | ||

| Insulating Screeds and Roof Fills | ||

| Others | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| Infrastructure | ||

| Energy and Utilities (Off-shore wind, LNG) | ||

| By Geography | Asia-pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the lightweight aggregate concrete market be by 2031?

The Lightweight Aggregate Concrete Market size is expected to grow from USD 9.88 billion in 2025 to USD 10.29 billion in 2026 and is forecast to reach USD 12.59 billion by 2031 at 4.12% CAGR over 2026-2031.

Which aggregate type is growing the fastest?

Perlite-based products exhibit the highest forecast growth at 4.28% CAGR due to superior insulation and 3D-printing suitability.

Why is offshore wind important to demand outlook?

Gravity-based and floating foundations use lightweight mixes to cut weight and reinforcement, driving the energy and utilities segment’s 3.81% CAGR.

What is the main cost restraint for adoption?

Lightweight mixes carry a 15-25% cost premium over normal-weight concrete, driven by high rotary-kiln energy inputs and freight.

Page last updated on: