Recycled Asphalt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.22 Billion |

| Market Size (2031) | USD 9.95 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recycled Asphalt Market Analysis by Mordor Intelligence

The recycled asphalt market size is projected to expand from USD 7.91 billion in 2025 and USD 8.22 billion in 2026 to USD 9.95 billion by 2031, registering a CAGR of 3.89% between 2026 to 2031. North America held the largest regional position in 2025, yet Asia-Pacific is accelerating on the back of China’s updated GB/T25033 recycling standard and India’s large-scale highway reuse program. Public-sector procurement mandates, volatile crude-linked bitumen prices, and the rapid rollout of warm-mix plant retrofits are tilting competitive advantage toward producers that can run high-RAP formulations. Equipment makers that integrate foamed-asphalt systems with real-time quality data capture are winning share, while contractors without stockpile management capability face rising compliance costs. Carbon accounting is now a bid qualifier, and verified Environmental Product Declarations are beginning to support premium pricing on long-duration contracts.

Key Report Takeaways

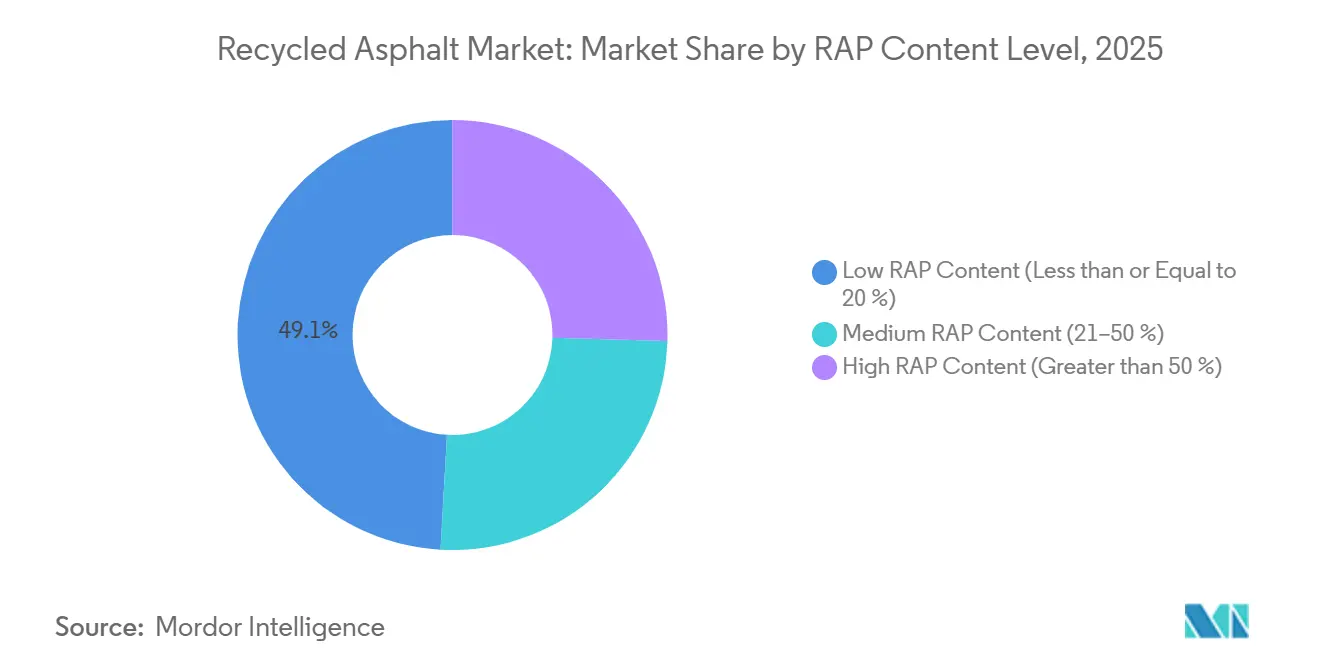

- By RAP content level, low RAP content mixes accounted for 49.12% of the recycled asphalt market share in 2025, while high RAP content formulations are advancing at a 3.98% CAGR through 2031.

- By application, hot mix asphalt led with 41.11% revenue share in 2025; new asphalt shingles are forecast to expand at a 4.21% CAGR to 2031.

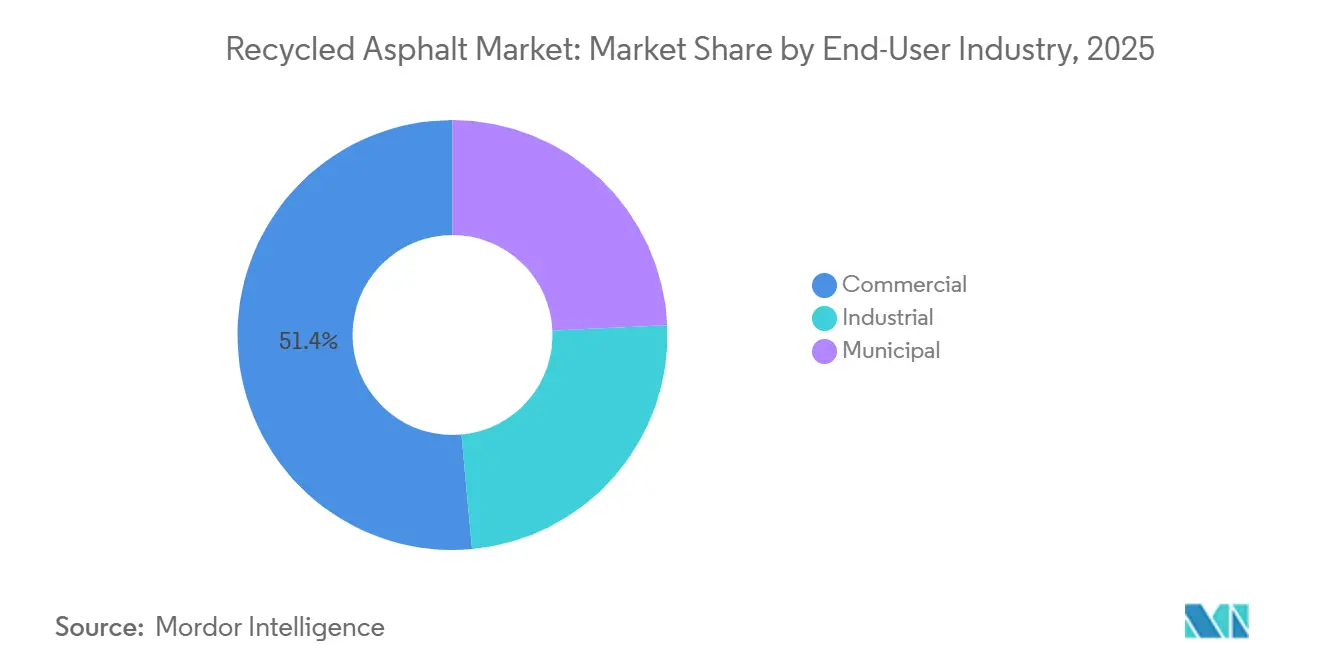

- By end-user industry, municipal entities commanded a 51.44% share of the recycled asphalt market size in 2025, and industrial buyers are growing at a 4.22% CAGR through 2031.

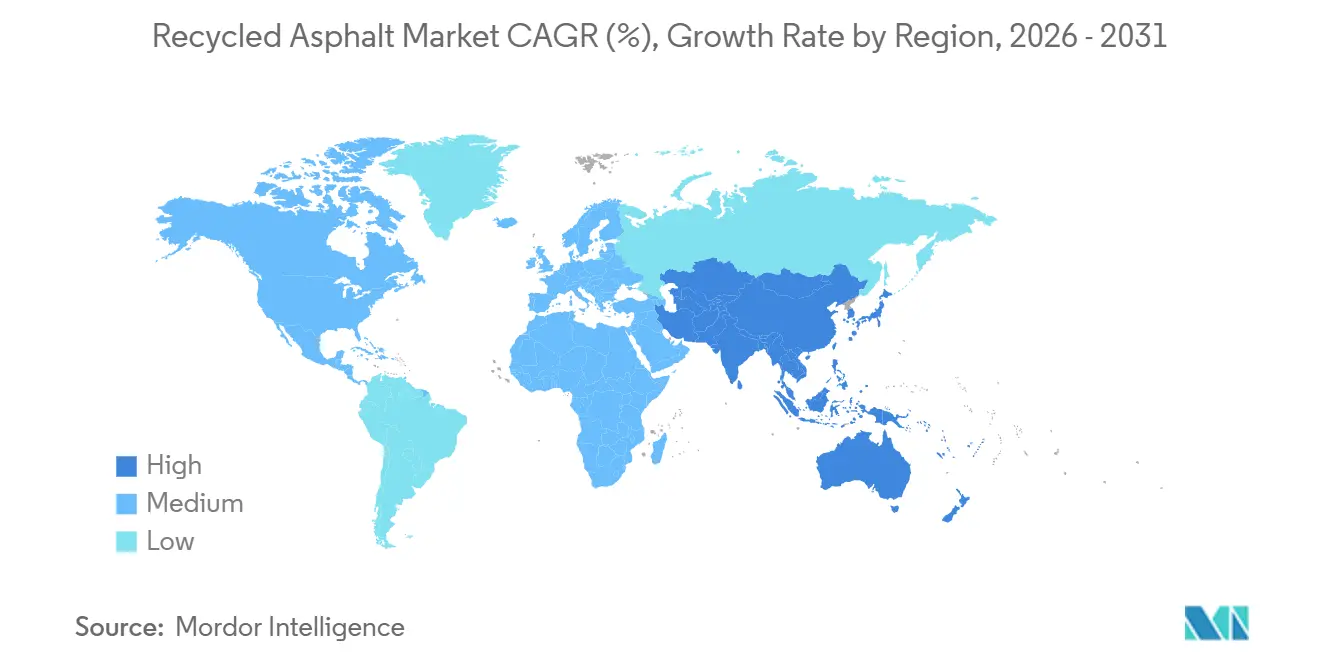

- By geography, North America controlled 41.89% of the value in 2025, whereas the Asia-Pacific is projected to grow the fastest at a 4.41% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recycled Asphalt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost competitiveness of RAP versus virgin mixes | +1.2% | Global, strongest in North America & Asia-Pacific | Short term (≤ 2 years) |

| Stringent sustainability procurement mandates by DOTs and municipalities | +1.0% | North America & EU, early adoption in APAC (China, India) | Medium term (2-4 years) |

| Expansion of 100%-RAP and warm-mix plant technologies | +0.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Corporate net-zero targets spurring carbon-negative pavement credits | +0.6% | Global, led by North America & the EU | Long term (≥ 4 years) |

| Secondary materials trading platforms are unlocking high-quality RAP supply | +0.4% | North America & EU, nascent in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Competitiveness of RAP Versus Virgin Mixes

The National Asphalt Pavement Association reported USD 3.4 billion in U.S. producer savings in 2023 through the use of 96.1 million tons of Reclaimed Asphalt Pavement (RAP) at an average inclusion rate of 21.9%[1]National Asphalt Pavement Association, “Annual Asphalt Pavement Industry Survey,” asphaltpavement.org. This demonstrates the role of RAP in managing raw material costs. Field data from the Florida Department of Transportation indicated that RAP-rich pavements provide comparable performance at a lower delivered cost in subtropical climates. Cost advantages increase during crude oil price rises; for example, when Brent crude exceeds USD 85 per barrel, the price difference between virgin and reclaimed binder can double. This has enabled contractors in India to achieve cost reductions of 25-30% on highway projects. Furthermore, municipal budget limitations support RAP adoption, making its usage less influenced by fluctuations in virgin asphalt demand.

Stringent Sustainability Procurement Mandates By DOTs And Municipalities

California’s Assembly Bill 2953, New Jersey’s Public Law 2023 c.134, Colorado’s Buy Clean Act, and Minnesota’s 2025 EPD rule require bidders to document carbon intensity, integrating reclaimed asphalt content into all qualifying projects[2]Florida DOT, “Reclaimed Asphalt Pavement Performance Report,” fdot.gov Source: California Legislature, “Assembly Bill 2953,” leginfo.legislature.ca.gov. Non-compliance penalties include measures such as contract holdbacks and disqualification, establishing a compliance baseline that ensures consistent demand regardless of crude oil price fluctuations. These regulations support suppliers that have invested in life-cycle assessment tools.

Expansion Of 100%-RAP And Warm-Mix Plant Technologies

Marini-Ermont’s TRX100% mobile plant enabled Eurovia to pave one kilometer of France’s A10 motorway using reclaimed material, reducing carbon emissions by nearly 50%. Astec’s ReMix Cold Central Plant system, introduced in 2024, processes up to 100% RAP at ambient temperatures, eliminating the energy costs of aggregate heating. Warm-mix technology lowers operating temperatures by 20-40 °C, extends paving seasons, and reduces burner fuel consumption, making plant retrofits a viable option for mid-sized contractors.

Corporate Net-Zero Targets Spurring Carbon-Negative Pavement Credits

The National Asphalt Pavement Association’s Road Forward initiative focuses on aligning producers, equipment suppliers, and industrial buyers with a 2050 net-zero roadmap. Carbon-credit platforms such as SurfaceCycle enable owners to monetize emissions reductions achieved through bio-char modified asphalt and renewable diesel-powered construction fleets. Retailers and logistics operators are specifying pavements with measurable Scope 3 emission reduction potential, increasing demand for high-recycled-content mixes supported by third-party-verified Environmental Product Declarations (EPDs).

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented logistics and stockpile management for RAP | -0.6% | Global, acute in APAC and South America | Short term (≤ 2 years) |

| Emergent microplastics scrutiny on recycled pavement runoff | -0.5% | North America & EU, regulatory lag in APAC | Medium term (2-4 years) |

| Volatility of bitumen-rejuvenator additive pricing | -0.4% | Global, the strongest impact in oil-importing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Logistics and Stockpile Management For RAP

Moisture absorption, contamination, and variability in gradation impact the performance margins of Reclaimed Asphalt Pavement (RAP) and increase blending costs. Many public storage facilities lack fractionation and protective covering, leading Departments of Transportation (DOTs) to limit RAP content to 20-30% unless additional laboratory testing is conducted. Investments in covered storage, on-site screening, and continuous sampling are essential for the recycled asphalt market to achieve its high-RAP potential.

Emergent Microplastics Scrutiny on Recycled Pavement Runoff

A 2025 study published in the Journal of Hazardous Materials found that asphalt wear produces microplastics that move through stormwater systems. If the EPA classifies pavement-derived fragments as a priority pollutant, contractors may incur additional costs for implementing permeable pavements or filtration retrofits. European regulators are assessing particle-emission limits, while North America is monitoring scientific developments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By RAP Content Level: Low-Content Comfort Zone Gives Way to High-RAP Upside

In 2025, low RAP content (less than or equal to 20%) held the largest share of the recycled asphalt market. This is due to most DOT standards relying on legacy performance data. These mixes provide consistent compaction and are compatible with unmodified batch plants, reducing adoption risks. Medium RAP blends (21-50%) have seen increased usage due to dual-bin feed retrofits and advancements in rejuvenator chemistries, offering balanced fatigue resistance at a competitive cost.

High RAP content (greater than 50%) is expected to lead the recycled asphalt market with a 3.98% CAGR through 2031. Initiatives such as Eurovia’s 100% RAP motorway trial and Astec’s ReMix CCPR plant have demonstrated field feasibility. Furthermore, the introduction of ternary composite rejuvenation in 2026 addressed earlier concerns regarding low-temperature brittleness. Project bids incorporating at least 40% RAP now qualify for additional scoring credits in several U.S. states, prompting specifiers to reassess the cost-risk balance. Contractors investing in fractionation and automated dosage controls are positioned to expand this segment into a profitable market opportunity.

By Application: Hot Mix Core, Shingle Recycling Surges

Hot mix asphalt accounted for 41.11% of the projected 2025 revenue, highlighting its significance in interstate resurfacing and airport runways where structural integrity determines mix selection. Balanced mix design protocols allow the use of up to 40% Reclaimed Asphalt Pavement (RAP) without performance issues, ensuring hot mix asphalt remains a key component in public-works budgets. Cold patch materials with over 90% RAP content extend maintenance periods, while temporary roadway base layers utilize surplus millings not suitable for higher-value applications.

New asphalt shingles are experiencing growth, with a compound annual growth rate (CAGR) of 4.21%, supported by advancements such as Sky Quarry’s ECOSolv process, which achieves 95% material recovery and 99% hydrocarbon recovery in partnership trials with Atlas Roofing. Utilities and telecommunication companies, which frequently require trench repairs, benefit from fast-curing patch compounds with high recycled content. Energy recovery from RAP remains limited due to emission restrictions, while contaminated stockpiles unsuitable for paving are used in industrial boilers operating under strict flue-gas control regulations.

By End-User Industry: Municipal Dominance, Industrial ESG Pull-Through

Municipal agencies are projected to account for 51.44% of the recycled asphalt market size in 2025, driven by budget allocations for pavement preservation and mandates focused on job creation. Commercial property owners select recycled asphalt due to its cost efficiency and shorter project timelines, particularly in retail parking lots where minimizing operational disruptions is important.

Industrial buyers are expected to achieve the highest compound annual growth rate (CAGR) of 4.22% through 2031, supported by net-zero commitments and opportunities to generate revenue from carbon-negative pavement credits. Distribution hubs and data centers increasingly require high-recycled asphalt pavement (RAP) mixes with third-party Environmental Product Declarations (EPDs) to meet investor reporting requirements. Producers with digital traceability platforms gain competitive advantages by certifying the composition of asphalt mixes and the fuel sources used during construction, enabling them to secure higher margins.

Geography Analysis

Asia-Pacific is projected to grow at a CAGR of 4.41% through 2031. China produces approximately 200 million tons of Reclaimed Asphalt Pavement (RAP) annually, but reuses only 30%, indicating potential for increased recycling as GB/T25033 supports hot, warm, and cold recycling methods. In India, over 63 million tons of waste were reused in FY 2023-24 across 6,634 kilometers of highways, with several states testing 40% RAP surface courses. Japan, with a 99% pavement recycling rate, has advanced collection logistics, while new PWRI test methods aim to validate mixes containing up to 70% reclaimed binder. Australia and South Korea currently maintain capped reuse levels but face fiscal considerations to increase thresholds.

North America: Market Share Driven by Policy and Cost Savings. North America accounted for 41.89% of the recycled asphalt market in 2025. In 2023, U.S. contractors saved USD 3.4 billion in material costs by utilizing 96.1 million tons of RAP. State regulations, such as California AB 2953 and Colorado’s Buy Clean Act, mandate Environmental Product Declarations, while balanced mix design pilots are increasing allowable RAP percentages to 45–50%. Training partnerships between Wirtgen and state Departments of Transportation (DOTs) are enhancing operator skills for on-site cold recycling processes.

Europe recycled 95% of its 100 million-ton RAP output in 2024, driven by landfill bans and carbon taxes. France’s A10 trial validated the use of 100% RAP in highway layers, while Colas expanded its recycling capabilities in Germany, Europe’s largest road market, through the acquisition of Frauenrath. These developments reflect Europe’s focus on sustainable road construction practices.

South America and the Middle East & Africa are smaller but growing markets. In Brazil, cold recycling systems were incorporated into São Paulo’s urban infrastructure upgrades. Saudi Arabia approved the use of 25% RAP for national highways. Infrastructure stimulus budgets and circular-economy policies in these regions indicate a gradual increase in recycling adoption.

Competitive Landscape

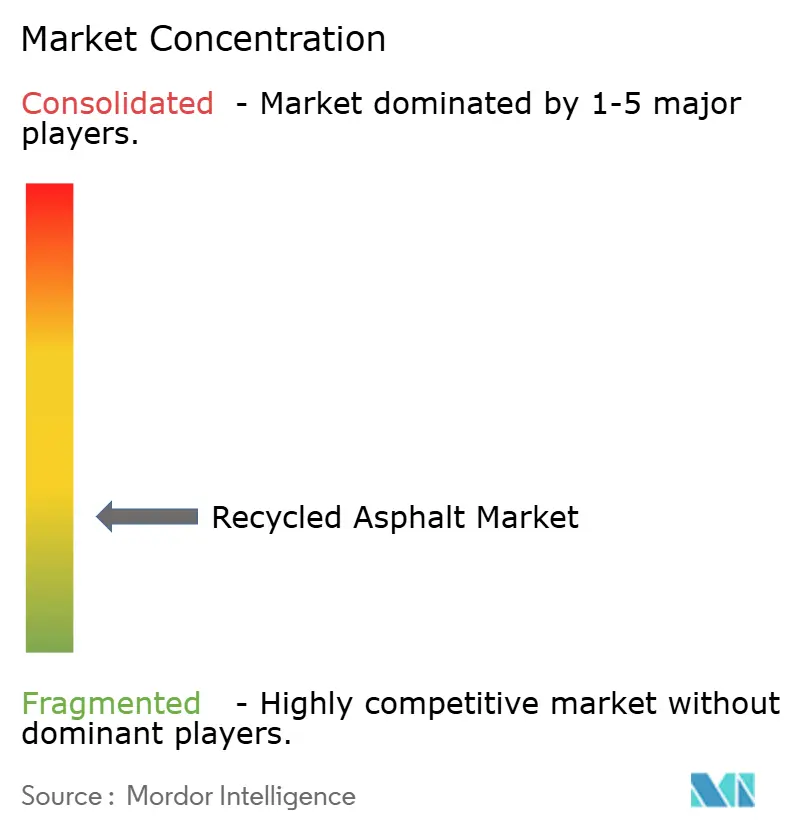

The recycled asphalt market is fragmented, with manufacturers, contractors, and material brokers competing to create value along a logistics-intensive supply chain. Astec Industries utilizes up to 70% recycled input in its latest plants and has expanded vertical integration by acquiring CWMF and TerraSource to enhance materials handling capacity. Colas’ EUR 150 million (USD 172.55 million) investment in Germany reflects ongoing European consolidation aimed at ensuring a consistent recycled asphalt pavement (RAP) supply. Granite Construction processes over 1 million tons of recycled materials annually and secured a USD 20 million U.S. 101 rehabilitation project incorporating rubberized high-recycled asphalt.

Companies like GreenRap provide proprietary rejuvenators to optimize the stiffness profiles of high-RAP mixes, while Sky Quarry addresses low shingle recycling rates through closed-loop extraction methods. Digital platforms are increasingly utilized for traceability: Astec’s Signal system captures real-time mix data for warranty compliance, and ProRAP platforms facilitate the exchange of information on stockpiles, lab results, and transportation logistics. Competitive advantages are increasingly driven by advancements in material science and data transparency rather than equipment scale.

Regulatory developments concerning microplastics and carbon disclosure are driving the need for adaptive research and development. Companies that fall behind in binder chemistry innovation or lack adequate covered storage facilities risk exclusion from procurement lists as specifications become more stringent. Firms adopting balanced mix design, warm-mix asphalt production, and verified Environmental Product Declarations (EPDs) are positioned to align with the growth trajectory of the recycled asphalt market.

Recycled Asphalt Industry Leaders

Astec Industries

Colas

CRH

Eurovia

Granite Construction Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Colas entered into an agreement to acquire the German road construction and recycling assets of Frauenrath Group for approximately EUR 150 million (USD 163 million), strengthening its position in recycled asphalt operations.

- January 2026: Granite Construction Inc. received a contract valued at approximately USD 20 million to rehabilitate 8 miles of U.S. 101 in Monterey County. The project includes supplying nearly 32,000 tons of rubberized hot mix asphalt, which incorporates recycled asphalt materials.

Global Recycled Asphalt Market Report Scope

Recycled asphalt refers to the reprocessing of old asphalt roads and driveways into new pavement. This process allows materials to be reused multiple times. The old pavement is milled or crushed and then combined with new binders and aggregates, offering cost efficiency and reduced environmental impact compared to using virgin materials.

The recycled asphalt market is segmented by RAP content level, application, end-user industry, and geography. By RAP content level, the market is segmented into low RAP content (less than or equal to 20%), medium RAP content (21–50%), and high RAP content (greater than 50%). By application type, the market is segmented into patch material, hot mix asphalt, temporary driveways and roads, road aggregate, interlocking bricks, new asphalt shingles, and energy recovery. By end-use industry, the market is segmented into commercial, industrial, and municipal. The report also covers the market size and forecasts for recycled asphalt in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Low RAP Content (Less than or Equal to 20 %) |

| Medium RAP Content (21–50 %) |

| High RAP Content (Greater than 50 %) |

| Patch Material |

| Hot Mix Asphalt |

| Temporary Driveways and Roads |

| Road Aggregate |

| Interlocking Bricks |

| New Asphalt Shingles |

| Energy Recovery |

| Commercial |

| Industrial |

| Municipal |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By RAP Content Level | Low RAP Content (Less than or Equal to 20 %) | |

| Medium RAP Content (21–50 %) | ||

| High RAP Content (Greater than 50 %) | ||

| By Recycled Asphalt Application | Patch Material | |

| Hot Mix Asphalt | ||

| Temporary Driveways and Roads | ||

| Road Aggregate | ||

| Interlocking Bricks | ||

| New Asphalt Shingles | ||

| Energy Recovery | ||

| By End-User Industry | Commercial | |

| Industrial | ||

| Municipal | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the market size in 2025, 2026, and projected value of the recycled asphalt market by 2031?

The recycled asphalt market size is projected to expand from USD 7.91 billion in 2025 and USD 8.22 billion in 2026 to USD 9.95 billion by 2031, registering a CAGR of 3.89% between 2026 to 2031.

Which region is expected to grow the fastest?

Asia-Pacific is projected to record the highest regional CAGR at 4.41% through 2031.

Which segment of RAP content is expanding most rapidly?

High RAP content mixes above 50% are advancing at a 3.98% CAGR, the fastest among content tiers.

What share did hot mix asphalt hold in 2025?

Hot mix asphalt accounted for 41.11% of application revenue in 2025.

Page last updated on: