Building And Construction Plastics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

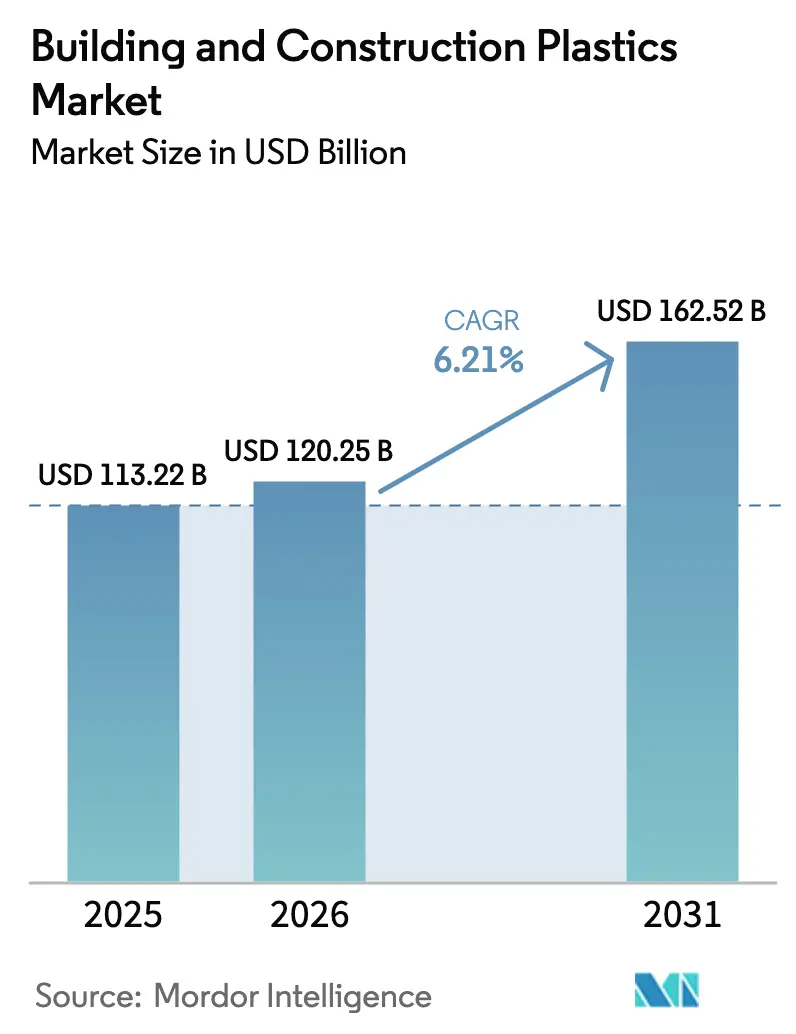

| Market Size (2026) | USD 120.25 Billion |

| Market Size (2031) | USD 162.52 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Building And Construction Plastics Market Analysis by Mordor Intelligence

The Building And Construction Plastics Market size is projected to be USD 113.22 billion in 2025, USD 120.25 billion in 2026, and reach USD 162.52 billion by 2031, growing at a CAGR of 6.21% from 2026 to 2031. Rising code-mandated thermal-performance targets, accelerated project schedules, and pressure to document embodied-carbon reductions are converging to move architects and contractors toward lightweight polymer solutions that install up to 40% faster than metal or concrete systems. Asia-Pacific already contributes the largest revenue slice, underpinned by municipal infrastructure deficits in tier-2 cities that favor prefabricated PVC and polyethylene networks able to meet budget ceilings without compromising service life. Polyvinyl chloride remains the volume leader, but polyurethane foams outpace all other resins on growth as stricter energy codes in the European Union and California drive adoption of closed-cell insulation that meets R-value targets at competitive thickness. End-market momentum is tilting toward data centers and cold-storage hubs, where insurers demand fire-rated, moisture-resistant panels that polymer composites now satisfy at lower installed weight. Competitive intensity stays high because the top five suppliers control 37% of sales, leaving room for regional compounders that incorporate up to 70% post-consumer recyclate without losing ISO 9001 certification.

Key Report Takeaways

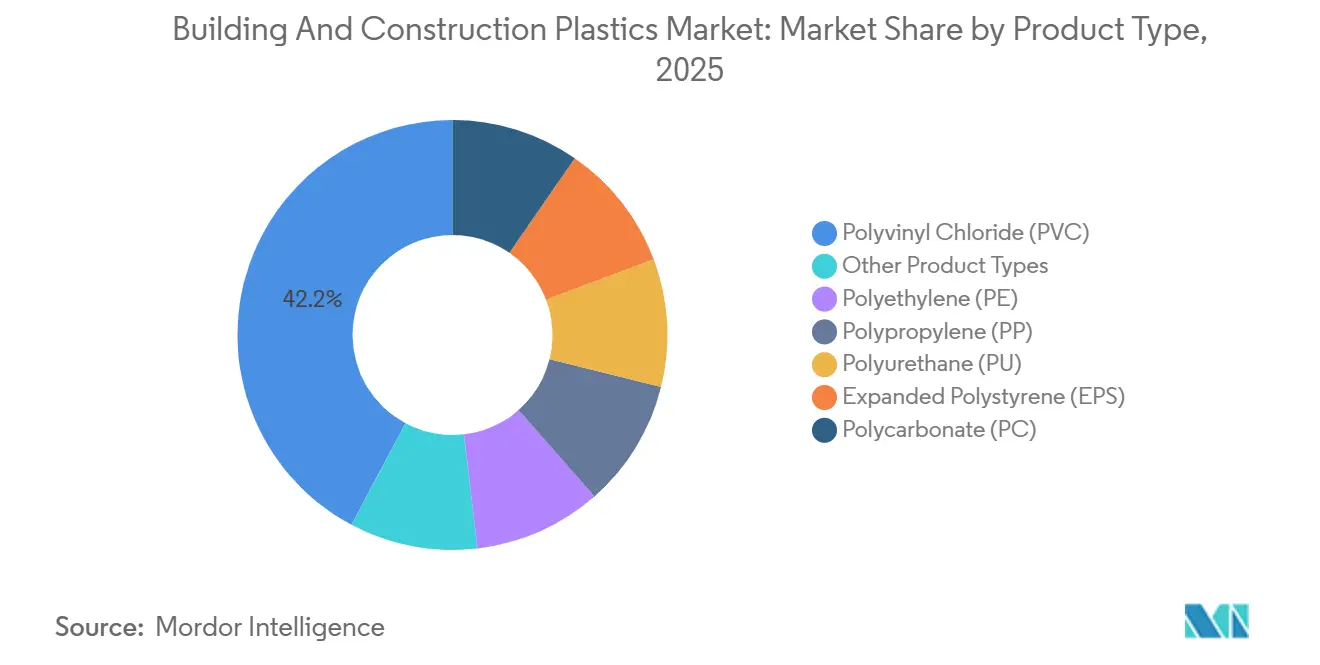

- By product type, polyvinyl chloride led with 42.21% of the building and construction plastics market share in 2025, while polyurethane is advancing at a 6.82% CAGR through 2031.

- By application, piping systems and fittings held 33.37% of the building and construction plastics market share in 2025, whereas insulation materials are advancing at a 6.98% CAGR through 2031.

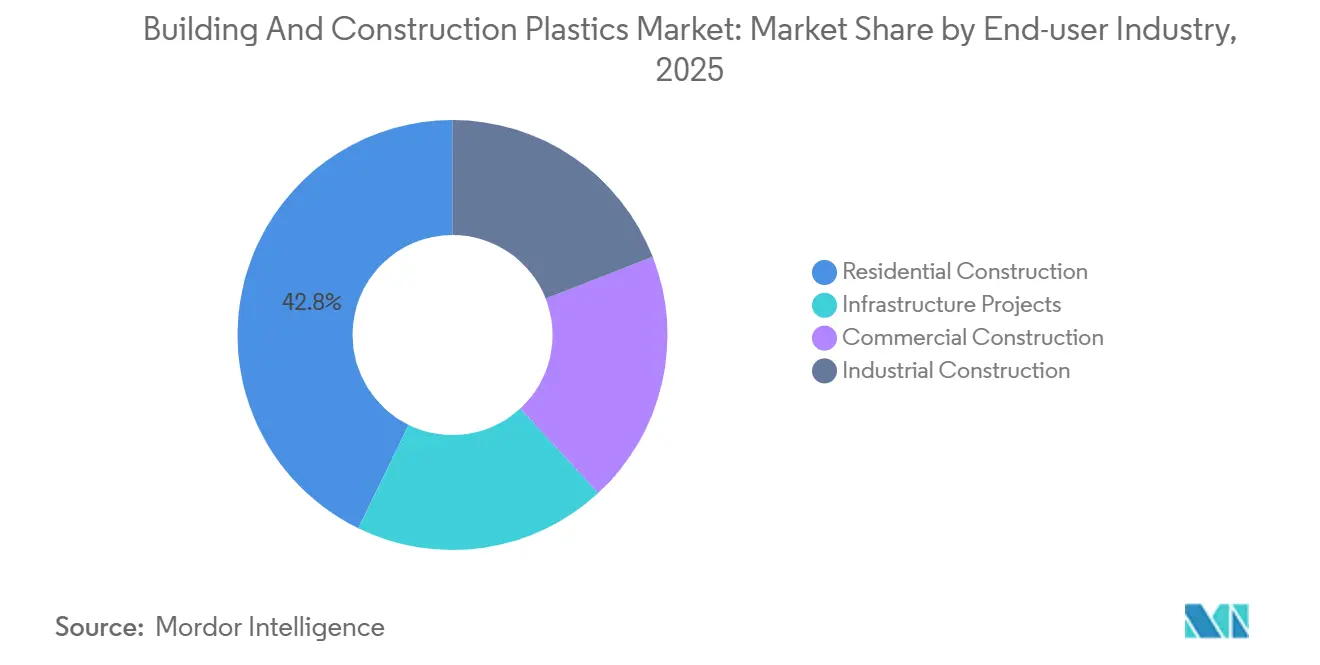

- By end-user industry, residential construction accounted for 42.78% of the building and construction plastics market share in 2025, yet commercial construction is set to expand at a 6.88% CAGR through 2031.

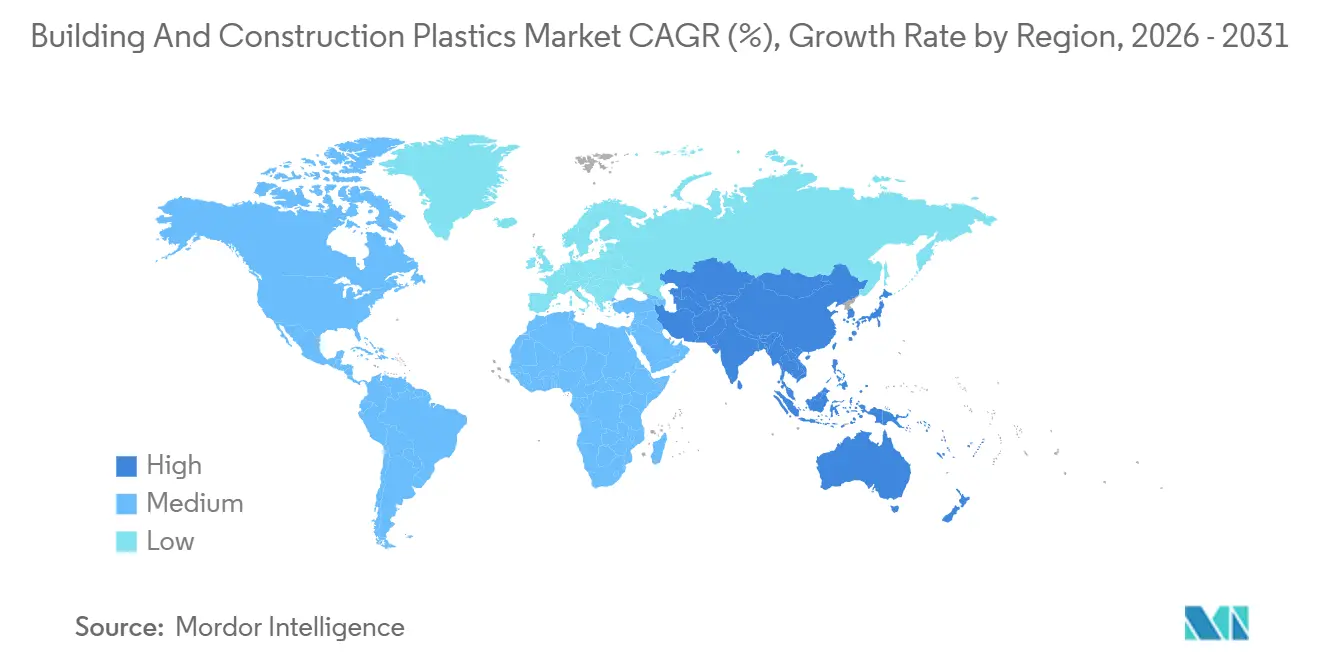

- By geography, Asia-Pacific captured 45.16% of the building and construction plastics market share in 2025 and is growing at 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Building And Construction Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban infrastructure investment in Asia-Pacific | +1.8% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Strict global energy-efficiency building codes | +1.5% | Global, with highest enforcement in EU, California, China | Long term (≥ 4 years) |

| Shift toward lightweight plumbing and conduits | +1.2% | Global, accelerated adoption in North America, India | Short term (≤ 2 years) |

| Prefabricated and 3-D-printed plastic components | +0.9% | North America, Europe, select Asia-Pacific metros | Medium term (2-4 years) |

| Commercial adoption of recycled/Bio-PVC blends | +0.7% | Europe, North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Infrastructure Investment in Asia-Pacific

Tier-2 municipalities across India, China, and Southeast Asia continue to face budget gaps that favor polymer systems able to cut installation labor by up to 40%. India’s plastic-pipes turnover reached INR 54,100 crore (USD 6.5 billion) in fiscal 2024 and is headed for INR 80,500 crore (USD 9.7 billion) by fiscal 2027 under the Jal Jeevan Mission’s aggressive rural-water timetable. China’s building-pipe segment is tracking a 9.2% CAGR to 2030 as corrosion-prone cast-iron networks give way to HDPE and PVC lines delivering leakage rates below 10%. BASF’s expanded compounding hub in Malaysia shortens lead times and trims delivered costs into Indonesia by up to 15%, reinforcing Asia-Pacific’s outsized 2025 revenue share. The building and construction plastics market therefore benefits directly from the region’s sustained infrastructure pipeline, lifting baseline demand even when residential starts soften.

Strict Global Energy-Efficiency Building Codes

Across major economies, developers who miss 2030 carbon-intensity thresholds now face fines or delayed occupancy permits worth 15–20% of project value. China’s GB 55015-2021 standard, the European Union’s 2024/1275 Energy Performance Directive, and California’s 2025 Title 24 update all raise minimum R-values, pushing polyurethane and polystyrene boards that achieve thermal conductivities below 0.035 W/(m·K) into both new-build and retrofit envelopes[1]California Energy Commission, “Title 24 2025 Update,” energy.ca.gov. The 2024 International Energy Conservation Code adds a performance path that rewards continuous exterior insulation, effectively doubling demand for rigid foams in climates where mineral wool cannot meet thickness targets. Because compliance is now non-negotiable, polymer-insulation suppliers secure long-dated order books, anchoring a resilient growth column for the building and construction plastics market.

Shift Toward Lightweight Plumbing and Conduits

Labor-scarcity penalties on late projects make installation speed as critical as material cost. Electrical non-metallic tubing bends without couplings and installs 40% faster than rigid PVC conduit. High-density polyethylene gas lines in India withstand 10 bar pressures for 50-year service lives, encouraging city-gas expansion toward a 70% national coverage goal. Japan’s Super Tough Poly pipes retain impact strength at –20 °C, a specification that metal cannot meet economically. These performance advantages reinforce the building and construction plastics market as contractors pivot away from copper and steel amid price volatility.

Prefabricated and 3-D-Printed Plastic Components

Off-site extrusion of wall panels, window frames, and HVAC ducts compresses on-site schedules by 25–35%. Azure Printed Homes uses robotic 3-D printers to deliver accessory-dwelling walls with under 5% scrap while meeting R-30 thermal codes. MIT’s interlocking eco-voxels enable non-skilled assemblers to raise load-bearing walls within four hours. The 2024 International Building Code now allows modular plastic panels in Type V-B structures up to three stories, expanding market headroom for polymer fabricators. Faster completion translates into immediate cash-flow for developers, strengthening the near-term demand signal for the building and construction plastics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile ethylene and propylene feedstock pricing | -1.3% | Global, acute in Asia-Pacific and Middle-East | Short term (≤ 2 years) |

| Insurance-driven bans on PVC in high-rise façades | -0.8% | Europe, Middle-East, select North America metros | Medium term (2-4 years) |

| Engineered timber carbon-credit advantage | -0.6% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Ethylene and Propylene Feedstock Pricing

Quarter-over-quarter swings of up to 40% in 2025-2026 eroded converters’ gross margins and forced pass-through clauses that stalled contract awards. The March 2026 Strait of Hormuz disruption trimmed naphtha shipments to Asian crackers, lifting polyol quotes by USD 450 per tonne in a single week. China’s heavy reliance on propane dehydrogenation units links geopolitical flashpoints directly to domestic propylene supply, pushing FOB prices to USD 868 per tonne in January 2026. Fabricators faced sub-8% operating margins, leading some to defer capacity builds, a scenario that tempers near-term expansion in the building and construction plastics market.

Insurance-Driven Bans on PVC in High-Rise Façades

Post-Grenfell regulations in the United Kingdom, Dubai, and selected North American metros prohibit combustible façades in high-rise structures unless paired with costly fire-barrier assemblies. Premium hikes of 15–25% from insurers further discourage PVC cladding above 18 meters. Parallel to safety concerns, mass-timber projects that sequester roughly 1 tonne CO₂ per cubic meter enjoy expedited permitting and tax incentives in Oregon and Washington, while EU taxonomy rules channel green-bond capital toward timber over plastics. Combined, these policies divert façade budgets to mineral fillers, fiber-cement, or engineered timber, carving out a measurable drag on the building and construction plastics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PVC Strength Meets PU Momentum

Polyvinyl chloride delivered 42.21% of 2025 revenue, reflecting code familiarity in pipes, window profiles, and siding. Yet polyurethane exhibits the quickest trajectory, posting a 6.82% CAGR to 2031 on the back of spray-foam retrofits that achieve R-6 per inch and satisfy EU 2030 energy targets[2]European Commission, “Renovation Wave Insulation Targets,” europa.eu. Covestro’s LINITHERM bio-attributed boards and BASF’s WALLTITE RSB foams underscore how renewable-feedstock certifications are now pivotal to bid success.

Medium-density polyethylene holds a mid-teen slice thanks to pressure-pipe adoption, while polypropylene gains ground in drainage composites that resist alkaline concrete. Expanded polystyrene, though single-digit in share, benefits from 2024 code revisions permitting continuous insulation up to 75 feet, unlocking mid-rise multifamily demand. Collectively, product innovation focused on lower-carbon footprints strengthens supplier differentiation within the building and construction plastics market.

By Application: Insulation Surges Past Legacy Piping

Piping systems and fittings captured 33.37% of 2025 sales. Insulation materials, however, are projected to expand at a 6.98% CAGR through 2031, outpacing legacy categories as Germany and France enforce 55% energy-intensity cuts ahead of 2030. Foamed plastics, such as EPS, XPS, PIR, and PU, dominate retrofit envelopes because they deliver R-values nearly double that of fiberglass at comparable installed cost.

Doors, windows, flooring, and roofing, with luxury-vinyl tile enjoying moderate growth as homeowners trade down from hardwood. Cladding volumes face headwinds where high-rise fire-safety codes restrict combustible materials, shifting interest to fiber-cement and metal. Specialty items such as conduit spacers and geocomposites grow in line with infrastructure outlays in India and Southeast Asia, reinforcing the diverse demand mix underpinning the building and construction plastics market.

By End-user Industry: Commercial Builds Overtake Residential

Residential construction captured 42.78% of revenue in 2025, yet commercial construction is forecast to log a 6.88% CAGR to 2031 as data centers and cold-storage warehouses proliferate. Data-center specifications require PIR panels with thermal conductivities below 0.020 W/(m·K) and Class A fire ratings, standards that polymer composites can meet cost-effectively.

Industrial construction and public infrastructure are spurred by India’s Jal Jeevan rural water push and China’s urban pipe-replacement campaigns. Although U.S. mortgage rates above 6% suppress near-term residential starts, anticipated easing after 2026 is expected to revive homeowner remodeling, cushioning cyclicality for the building and construction plastics industry.

Geography Analysis

Asia-Pacific remained the primary demand center with 45.16% of global revenue in 2025, and is projected to clock a 7.12% CAGR through 2031. Surging urban migration forces municipalities to choose prefabricated polymer systems that deliver leakage rates under 10% and cut labor inputs by a third. India’s building and construction plastics market size for pipes alone will crest USD 9.7 billion by fiscal 2027 thanks to aggressive rural-water mandates.

North America is constrained by elevated mortgage rates yet bolstered by insulation demand in data-center expansions. The International Building Code’s 2024 allowance for mass timber in 18-story structures creates head-to-head competition, but polymer suppliers are countering with bio-attributed PVC and circular-polypropylene grades.

In Europe, Energy Performance of Buildings Directive phases out fossil-fuel heating in new builds by 2030, indirectly boosting polyurethane and EPS demand. Germany’s retrofit drive and the UK’s fire-safety legislation simultaneously aid and restrict different polymer categories, illustrating the policy-driven complexity of regional trends in the building and construction plastics market.

Competitive Landscape

The top five suppliers, including BASF, Dow, Dupont, LyondellBasell, and SABIC, collectively hold 37% of sales in 2025, signaling a fragmented arena rich with regional specialists. BASF will add 50,000 tons of Neopor graphite EPS capacity at Ludwigshafen by early 2027, introducing renewable (BMB) and mechanical-recycle (Mcycled) variants that claim 30% higher R-value per inch than standard EPS. LyondellBasell’s 35% stake in NATPET secures 400,000 tons of polypropylene capacity in Saudi Arabia, while its MoReTec-1 chemical-recycling unit, slated for 2026 startup in Germany, targets post-consumer streams equal to the annual waste from 1.2 million residents.

Strategic themes center on locking renewable feedstock, expanding Asia-based compounding, and launching products that trim lifecycle CO₂ by up to 58%. Regional compounders in India leverage 20-30% cheaper recyclate and robotic extrusion to underbid multinationals on public-tender pipes. Digital twin simulations are shortening R&D cycles to nine months by optimizing flame retardancy, impact-strength, and weatherability trade-offs, thereby accelerating specialty-grade commercialization in the building and construction plastics market.

Building And Construction Plastics Industry Leaders

BASF

Dow

LyondellBasell Industries Holdings B.V.

SABIC

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: In India, Azelis announced a distribution deal with Milliken & Company. Azelis became the distributor for Milliken's polyurethane (PU) colorant solutions, catering to the coatings, adhesives, sealants, and elastomers (CASE) market.

- December 2025: Westlake Corporation shut down its major chlorovinyl and styrene plants located in Aberdeen, Mississippi, and Lake Charles, Louisiana. The closures included a polyvinyl chloride (PVC) plant, which had an annual capacity of around 1 billion pounds.

Global Building And Construction Plastics Market Report Scope

Building and construction plastics are engineered polymer materials widely used in modern architecture as lightweight, durable, and cost-effective substitutes for traditional materials such as wood, metal, and concrete.

The Building And Construction Plastics Market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into polyvinyl chloride (PVC), polyethylene (PE), polypropylene (PP), polyurethane (PU), expanded polystyrene (EPS), polycarbonate (PC), and other product types. By application, the market is segmented into piping systems and fittings, insulation materials, doors and windows, flooring, roofing, wall panels and cladding, and other applications. By end-user industry, the market is segmented into residential construction, commercial construction, industrial construction, and infrastructure projects. The report also covers the market size and forecasts for building and construction plastics in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polyvinyl Chloride (PVC) |

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyurethane (PU) |

| Expanded Polystyrene (EPS) |

| Polycarbonate (PC) |

| Other Product Types |

| Piping Systems and Fittings |

| Insulation Materials |

| Doors and Windows |

| Flooring |

| Roofing |

| Wall Panels and Cladding |

| Other Applications |

| Residential Construction |

| Commercial Construction |

| Industrial Construction |

| Infrastructure Projects |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Polyvinyl Chloride (PVC) | |

| Polyethylene (PE) | ||

| Polypropylene (PP) | ||

| Polyurethane (PU) | ||

| Expanded Polystyrene (EPS) | ||

| Polycarbonate (PC) | ||

| Other Product Types | ||

| By Application | Piping Systems and Fittings | |

| Insulation Materials | ||

| Doors and Windows | ||

| Flooring | ||

| Roofing | ||

| Wall Panels and Cladding | ||

| Other Applications | ||

| By End-user Industry | Residential Construction | |

| Commercial Construction | ||

| Industrial Construction | ||

| Infrastructure Projects | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the building and construction plastics market?

The building and construction plastics market stands at USD 120.25 billion in 2026 and is forecast to reach USD 162.52 billion by 2031, expanding at a 6.21% CAGR over 2026-2031.

Which region leads demand for building and construction plastics?

Asia-Pacific contributes 45.16% of global revenue in 2025 and is growing at a 7.12% CAGR through 2031.

Which product type is growing the fastest through 2031?

Polyurethane is set to post the highest 6.82% CAGR through 2031 due to its superior insulation performance.

Why are insulation materials outpacing piping applications?

Stricter global energy codes require higher R-values, driving rapid uptake of foamed-plastic insulation.

Page last updated on: