Black Mass Recycling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.42 Billion |

| Market Size (2031) | USD 39.04 Billion |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

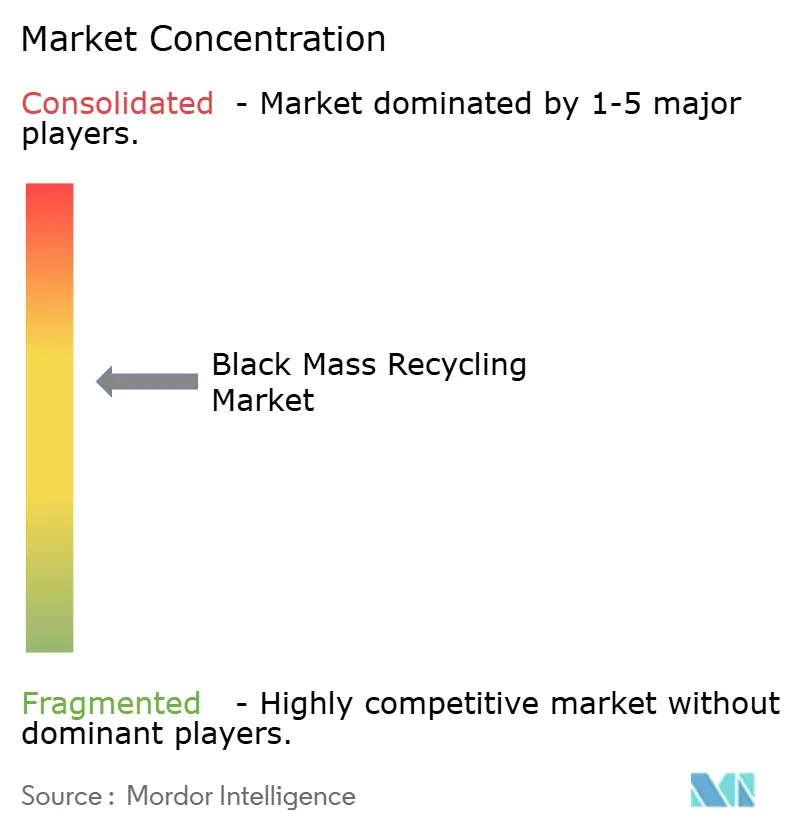

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Black Mass Recycling Market Analysis by Mordor Intelligence

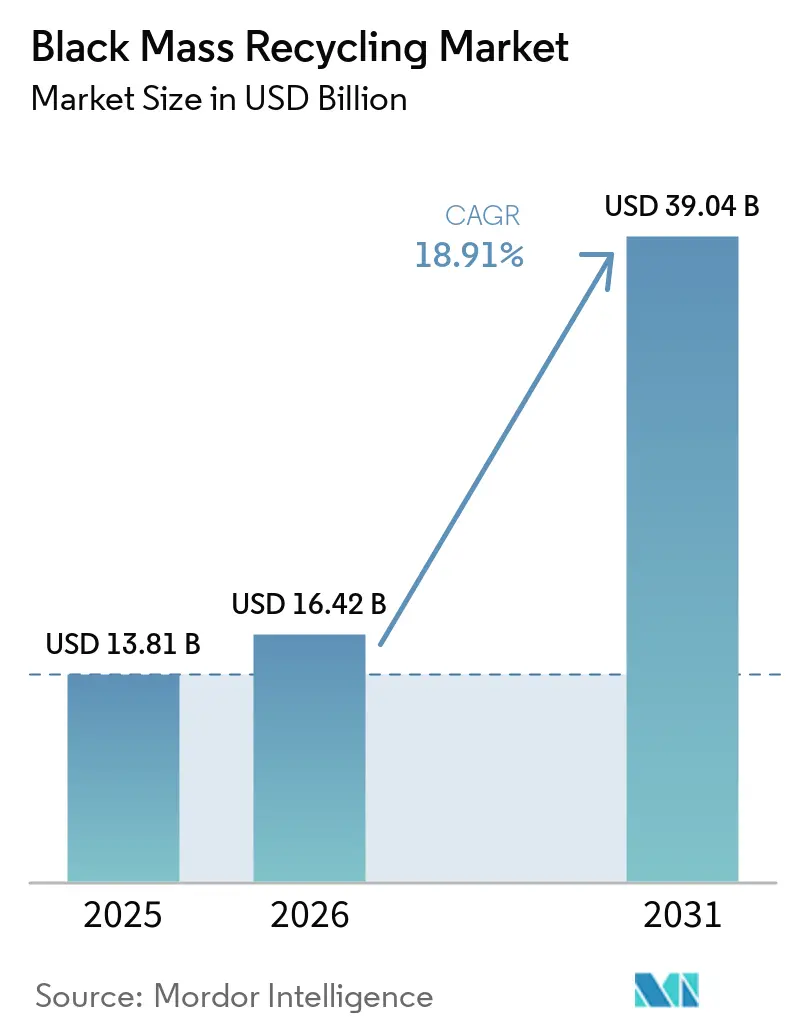

The black mass recycling market size is projected to be USD 16.42 billion in 2026 and reach USD 39.04 billion by 2031, growing at an 18.91% CAGR over 2026-2031. The expansion from USD 13.81 billion in 2025 reflects structural policy shifts that require domestic recovery of lithium, cobalt, nickel, and manganese. In a strategic move, automakers and cell manufacturers are now absorbing end-of-life costs, ensuring access to battery-grade feedstock. Concurrently, major players like the European Union, United States, and China are tightening their grip by restricting exports of critical-mineral scrap. The market's momentum is further bolstered by the rapid establishment of gigafactories, production-tax incentives from the U.S. Inflation Reduction Act, and a notable dip in lithium carbonate spot prices, prompting a shift towards secondary supply hedging. Amidst ongoing price fluctuations in nickel and cobalt, there's a pronounced tilt towards manganese-rich chemistries, amplifying the demand for recycling capacities that can harness every metal unit.

Key Report Takeaways

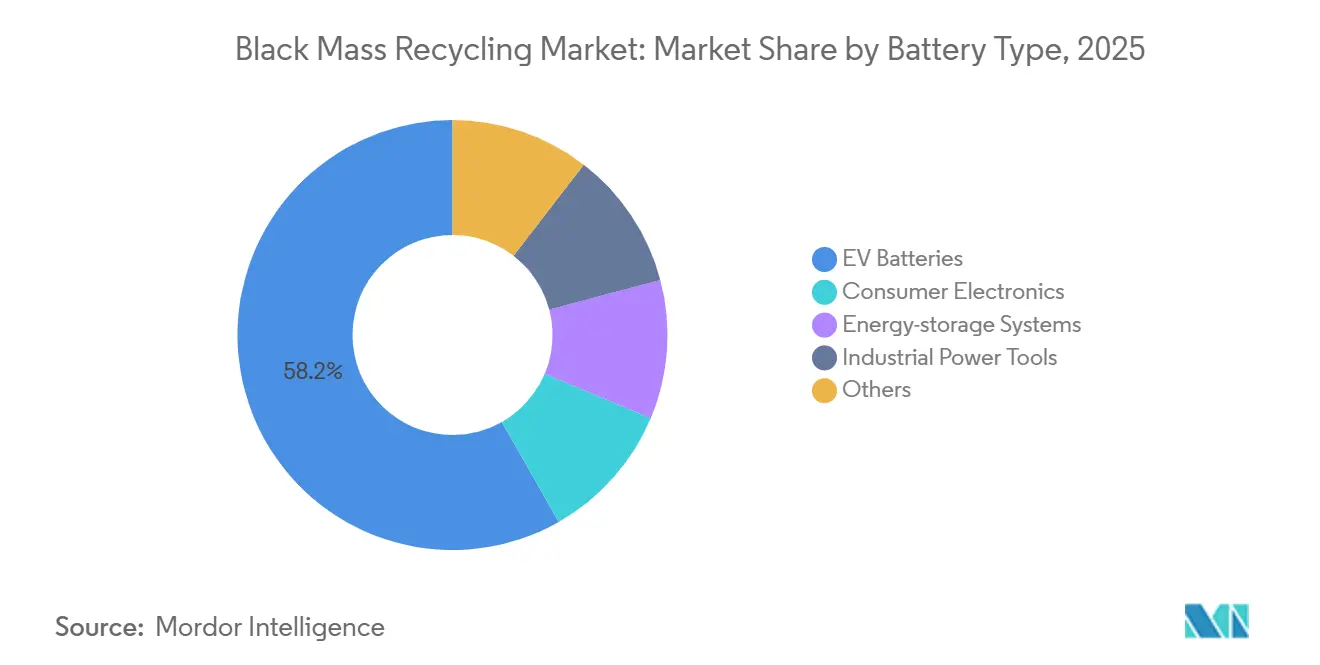

- By source, EV batteries led with 58.23% of the black mass recycling market share in 2025 and are projected to expand at 20.45% CAGR from 2026 to 2031.

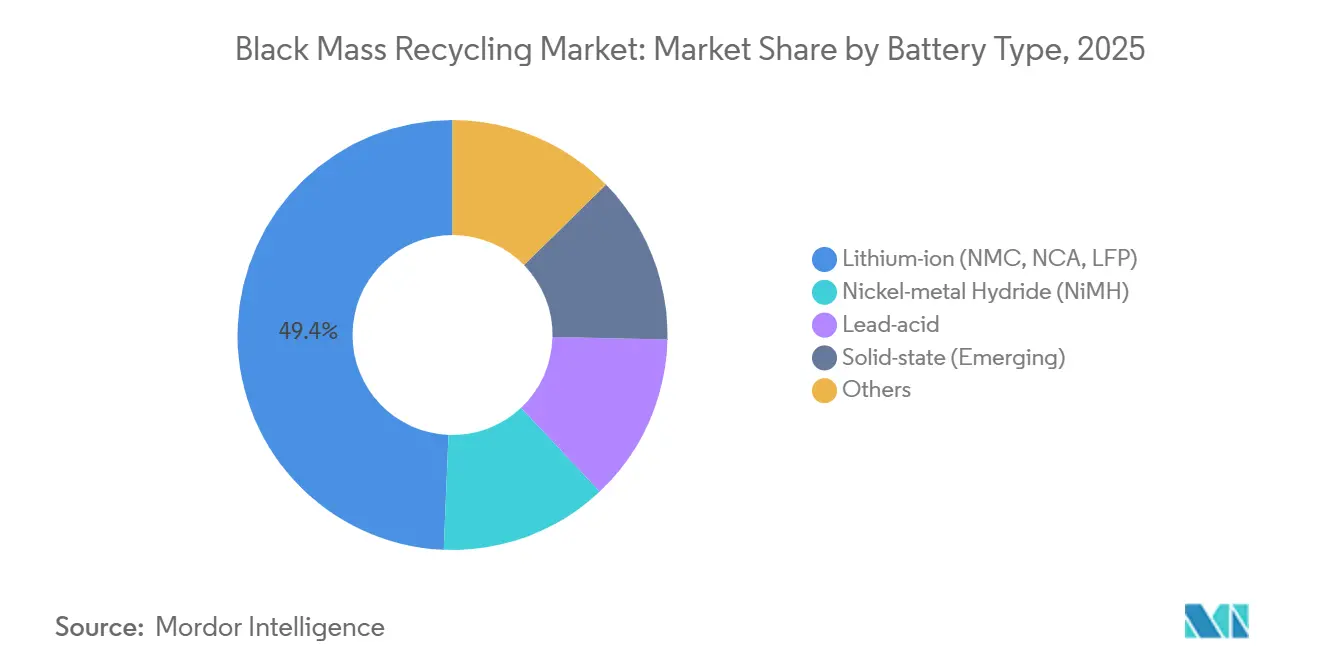

- By battery type, lithium-ion batteries led with 49.35% of the black mass recycling market share in 2025. Additionally, solid-state batteries are projected to be the fastest segment and expand at 20.23% CAGR from 2026 to 2031.

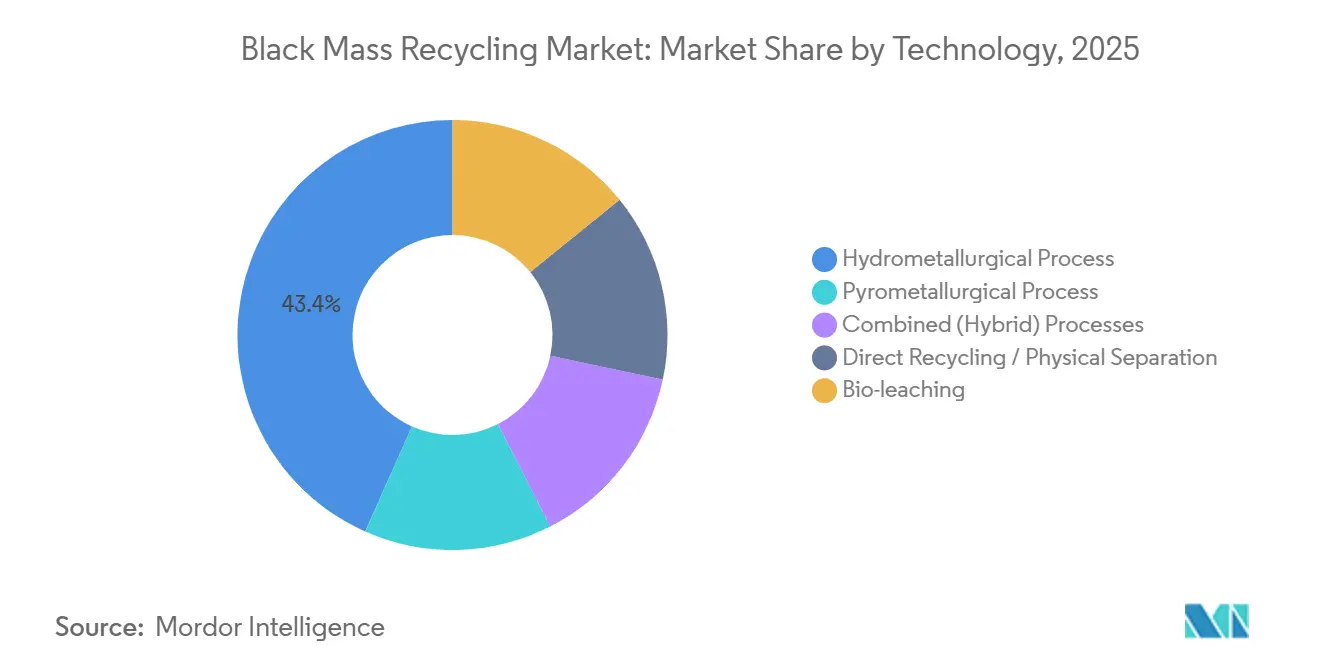

- By technology, hydrometallurgy captured 43.35% share in 2025, while bio-leaching records the highest projected 21.25% CAGR from 2026 to 2031.

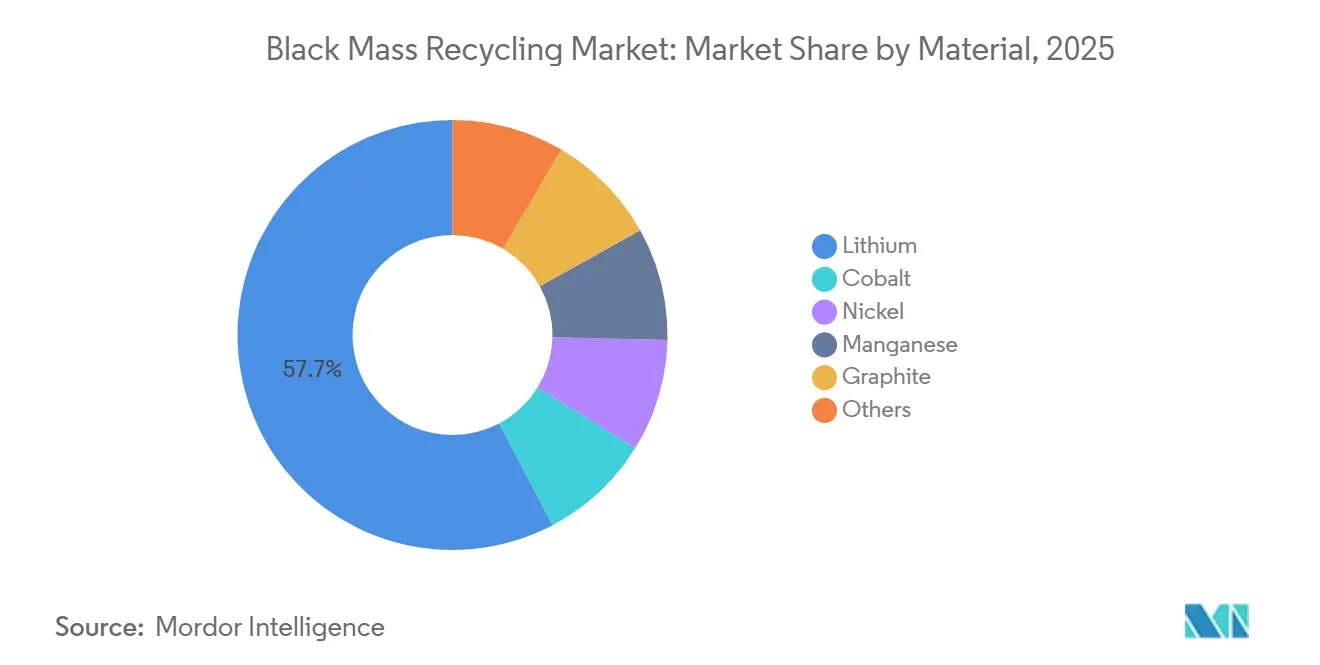

- By material, lithium dominates the market with 57.73% market share in 2025, manganese recovery is slated to rise at 19.89% CAGR CAGR from 2026 to 2031, overtaking nickel as cathode producers migrate toward manganese-rich chemistries.

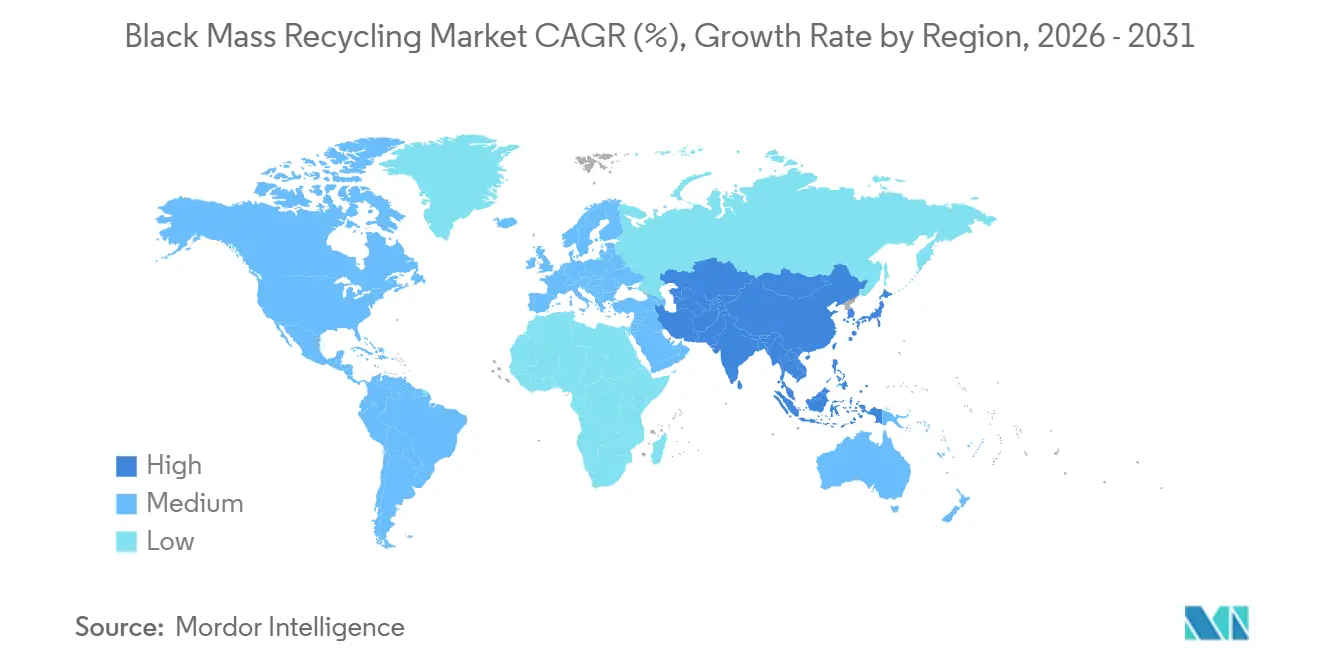

- By region, Asia-Pacific held 48.89% share of the black mass recycling market size in 2025, the region is also projected to be fastest growing at 22.25% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Black Mass Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid scale-up of Li-ion gigafactories | +4.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| EV-OEM take-back mandates in European Union and China | +3.8% | Europe and China, spillover to North America | Short term (≤ 2 years) |

| Inflation Reduction Act clean-material tax credits | +3.5% | United States, indirect pull on Canada and Mexico | Medium term (2-4 years) |

| Down-stream demand from LFP-to-NMC chemistry switch | +2.1% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Municipal e-waste partnerships unlocking urban feedstock | +1.6% | Urban centers in North America, Europe, Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-up of Li-ion Gigafactories

In 2025, global cell production capacity exceeded 2,200 GWh, with an additional 800 GWh slated for completion before 2028. Redwood Materials, strategically positioned alongside Panasonic and Tesla in Nevada, demonstrates how co-located recycling can streamline logistics to under 48 hours. Similarly, in Hunan Province, CATL and Brunp are channeling production scrap directly back into their cathode precursor supply chains. Capital intensity is a significant hurdle: Ascend Elements invested a hefty USD 310 million to establish a 30,000-ton annual capacity in Kentucky, underscoring the necessity of offtake agreements for plant financing. As a result, the black mass recycling market increasingly favors vertically integrated manufacturers and recyclers that can secure long-term feedstock.

EV-OEM Take-back Mandates in EU & China

By 2027, the EU Battery Regulation mandates a 63% collection rate for portable cells and prohibits black mass exports starting December 2026[1]. By 2031, automakers are required to incorporate 16% recycled cobalt and 6% recycled lithium into new batteries, which is driving them to engage with domestic processors sooner. China's traceability-code system demands a 95% recovery rate for packs exceeding 20 kWh, making it essential for local OEMs to ensure collection. In 2025, Volkswagen's pilot in Salzgitter processed 3,600 tons of ID series packs, yet it continues to operate at a loss due to falling lithium prices in the black mass recycling market.

Inflation Reduction Act Clean-material Tax Credits (US)

By 2027, the U.S. Inflation Reduction Act ties the full USD 7,500 EV consumer credit to packs containing 80% domestic critical-mineral content. Meanwhile, Section 45X provides an incentive of USD 10 per kilogram for battery-grade lithium carbonate or cobalt sulfate refined domestically, leading to a noticeable price difference between recycled and imported feedstock[2]United States Internal Revenue Service, “Section 45X Guidance,” irs.gov. Ascend Elements secured a USD 480 million grant for its hydro-to-cathode plant, which has multi-year offtake agreements to supply General Motors and Honda. As a result, the black mass recycling market is now closely aligned with North America's sovereign industrial goals.

Down-stream Demand from LFP-to-NMC Chemistry Switch

Automakers migrating premium models from LFP to nickel-rich NMC chemistries amplify demand for manganese, cobalt, and nickel while still requiring efficient lithium recovery. Flexible recycling plants modify leach-ate composition through programmable pH adjustment to accommodate diverse chemistries. Equipment suppliers now market modular reactors that toggle between sulphuric-acid and hydrochloric-acid circuits, minimising downtime when feedstock blends shift. This chemistry pivot prompts long-term procurement contracts for manganese sulphate, solidifying black mass recycling market revenue visibility for recyclers. Simultaneously, direct-recycling research for LFP cells employs rapid thermal delamination to preserve phosphate lattices, opening secondary markets for regenerated cathode powder.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trace-metal contamination reducing output purity | -1.80% | Global, particularly affecting hydrometallurgical processes | Short term (≤ 2 years) |

| High capex for fire-safe black-mass logistics | -1.20% | North America and Europe, stricter safety regulations | Medium term (2-4 years) |

| Slow permitting cycles for new recycling plants | -1.50% | Global, acute in North America and Europe with complex regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trace-metal Contamination Reducing Output Purity

Iron, aluminium, and copper shavings introduced during shredding and milling in the black mass recycling market can push impurity levels beyond 0.5%, disqualifying recycled salts from premium cathode use. Recyclers respond by installing eddy-current separators and high-frequency inductive sensors that spot inclusions down to 20 microns. Additional crystallisation passes lift operating costs by 12% and shrink overall lithium yield. Failure to meet purity benchmarks forces processors to sell at discounts into lower-margin applications such as lubricants or ceramics, eroding profitability. Collaborative R&D projects with analytical-instrument suppliers now target in-line laser-induced breakdown spectroscopy, yet commercial deployment remains nascent given calibration challenges for mixed chemistries.

High Capex for Fire-safe Black-mass Logistics

Regulators in the black mass recycling market classify black mass as a hazardous material prone to thermal runaway, requiring purpose-built drums, nitrogen-purged containers, and real-time temperature telemetry that drive logistics costs to USD 0.90 per kilogram, triple comparable ore shipments. Warehouse retrofits with sprinkler deluge systems cost USD 12 million for a mid-sized facility, consuming capital that could otherwise fund capacity expansion. Insurance underwriters demand multi-layer risk plans, raising annual premiums by 18%. Emerging solutions such as inert-gas gel packs and vacuum-sealed liners promise to ease capex burdens, yet large-scale validation is pending. Tightening safety rules in the European Union and some US states suggest costs will stay elevated through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: EV Batteries Drive Feedstock Shift

In 2025, EV batteries dominated the black mass recycling market, holding a 58.23% share. Forecasts predict a robust 20.45% CAGR growth for them, solidifying their leading position. Each automotive pack produces a concentrate yield of 60-75 kilograms, streamlining plant operations. As grid batteries reach the end of their 10-12 year lifespan, energy-storage systems are emerging as a lucrative back-end opportunity. While China boasts regulatory capture rates nearing 87%, North America lags with figures under 50%, highlighting regional disparities in feedstock security.

Utilizing second-life energy-storage could extend the recycling timeline for EV packs past the 15-year threshold. This extension might lead to a future supply dip, but urban consumer electronics could bridge the gap. Though industrial power tools, medical devices, and aerospace cells account for only 6% of the tonnage, their diverse chemistry introduces complexities in process control. In China, OEM traceability codes, combined with Europe's mandatory take-back schemes, are set to boost collection efficiency for traction batteries. California's new statewide law, echoing EU policies, paves the way for a unified North American market.

By Battery Type: Lithium-ion Dominance Faces Solid-state Disruption

Lithium-ion packs, spanning NMC, NCA and LFP chemistries, generated 49.35% of Black Mass Recycling market size in 2025 owing to well-established leaching routes that recover up to 95% of lithium and cobalt. High throughput, familiar equipment, and predictable material flows keep processing costs competitive. The segment benefits from process intensification, notably microwave-assisted leaching that cuts residence times by 40%. However, solid-state cells are on a steep 20.23% CAGR trajectory toward 2030, fuelled by their safety and energy-density edge sought by premium automakers. Their ceramic electrolytes, though, introduce alumina and sulfide matrices that demand bespoke chemical or mechanical liberation methods now in pilot trials. Recycling firms that refine polyvalent flowsheets capable of toggling between liquid and solid-state waste are likely to gain early-mover advantage as product mix shifts.

The segmental shift boosts research into direct-recycling approaches that preserve cathode morphology for relithiation, thereby slashing conversion costs. Nickel-metal hydride batteries retain relevance in hybrid cars but contribute diminishing black-mass tonnage, pushing specialised processors toward strategic alliances with fleet operators to secure volume. Lead-acid units are largely excluded from modern black-mass lines due to divergent chemistry; their entrenched closed-loop networks remain distinct. As demand climbs, flexible hydromet lines with adjustable oxidation-reduction potentials will become standard, allowing processors to pivot output purity toward whichever battery chemistry commands premium pricing at any given time.

By Material Type: Lithium Leadership Contends with Manganese Surge

In 2025, lithium commanded a dominant 57.73% share of the black mass recycling market by value. This was primarily driven by the premium attached to battery-grade lithium carbonate. Nickel and cobalt have seen a downward trend as cathode producers aim to mitigate risks associated with sourcing from the Democratic Republic of Congo. Manganese recovery, however, is projected to grow at a 19.89% CAGR. This growth is attributed to the acceleration of LMFP and high-manganese NMC formulations. Stable pricing, ranging between USD 1,800-2,200 per ton, has enhanced cash-flow predictability for recyclers.

Graphite remains a minor revenue contributor. Its purification process requires thermal treatment at 2,500-3,000 °C, which negates any carbon-footprint benefits. Direct recycling offers the potential to maintain graphite's crystallinity, but this method depends on uniform scrap streams, which are rarely provided by municipal programs. These evolving dynamics have diversified the market's reliance away from cobalt. This diversification has also strengthened the black mass recycling market's resilience against shocks from any single metal.

By Technology: Bio-leaching Disrupts Traditional Processing

Hydrometallurgical plants captured 43.35% of Black Mass Recycling market size in 2025 through proven scalability, modular tank farms and mature reagent supply chains that allow recovery rates above 90% for most metals. The approach, however, produces sulfate-rich effluents and demands significant heat and chemical inputs that raise emissions and compliance costs. Bio-leaching, advancing at 21.25% CAGR, deploys iron-oxidising or sulfur-oxidising microbes to liberate metals at ambient temperatures, trimming reagent demand by half and reducing sludge disposal volumes. Pilot plants in Finland and Canada report cobalt recoveries exceeding 80% within 72 hours.

Pyrometallurgical smelters remain for bulk throughput yet face regulatory scrutiny over CO₂ and NOₓ emissions. Hybrid flowsheets combine low-temperature roasting followed by acid leach to offset individual drawbacks, achieving both carbon reduction and high selectivity. Direct-recycling methods that delaminate and relithiate cathode powders bypass complex chemistry entirely, yielding cost and energy savings, but require tight control of feedstock composition and separation of foreign matter such as plastics and steel casings. Technology developers race to patent process-control algorithms and custom reactor linings, aiming to secure royalty streams as adoption widens.

Geography Analysis

Asia-Pacific produced 48.89% of the global Black Mass Recycling market size in 2025 and is forecast to post a 22.25% CAGR through 2030 as it leverages vertically integrated battery value chains centered in China, Japan, and South Korea. Chinese export controls on graphite, effective from December 2024, amplify domestic demand for recycled anode material and attract joint ventures from European cathode makers looking to safeguard feedstock. Government subsidies covering up to 30% of capital costs and preferential electricity tariffs further cement regional leadership. Japan’s JX Metals optimises hydromet plants with renewable power, while Korea’s SK tes combines e-waste streams with automotive packs to hedge chemistry fluctuations.

North America accelerates capacity in the black mass recycling market on the back of federal tax credits that enhance internal rates of return for new facilities. Redwood Materials expands multi-phase complexes in Nevada and South Carolina, while BASF partners with local utilities to secure low-carbon electricity. Canadian provinces align provincial recycling targets with automotive OEM production forecasts, fostering cross-border material flows that streamline logistics under the United States-Mexico-Canada Agreement (USMCA) trade pact. Mexican assemblers explore in-house shredding to reduce the cost of transporting bulky packs to northern facilities.

Europe’s regulatory stringency fuels investment in high-purity hydrometallurgical hubs in the black mass recycling market located in Germany, Sweden and Poland, each tied to local gigafactory clusters. The EU Battery Passport, operational in 2027, mandates granular life-cycle data, steering capital towards traceable, low-emission recycling solutions. Collaborations with African miners supply pre-processed concentrates to European smelters, balancing supply risk. Smaller markets in the Middle East and Africa target niche roles in preprocessing and fire-safe storage, benefiting from proximity to shipping arteries but still constrained by limited downstream demand.

Competitive Landscape

The Black Mass Recycling market exhibits partial consolidation nature. Umicore, Gelncore, BASF, Redwood Materials, and Ganfeng Lithium Group Co., Ltd. make up the top 5 companies in the Black Mass Recycling market. Umicore and Glencore exploit deep metallurgical heritage, extensive trading desks, and captive smelting infrastructure to negotiate long-term feedstock contracts with automakers. Redwood Materials differentiates through patented hydromet-plus-solvent-extraction flowsheets that promise lower capex per tonne and higher lithium yield. SK Tes and BASF pursue strategic partnerships: BASF opened its Schwarzheide black-mass plant in June 2025 with 15,000 tons annual throughput, integrating closed-loop supply for its German cathode factory.

ISO 14001 certification and the EU Battery Passport become entry requirements for OEM business. Redwood achieved certification in 2024 and pilots blockchain traceability at its South Carolina plant. RecycLiCo chose a license model that generated CAD 8 million in 2024 but concedes capacity control to Asian partners. American Battery Technology Company deploys modular plants that fit rural logistics nodes and target underserved regions.

Strategic white space lies in direct recycling for homogeneous scrap, municipal e-waste aggregation to lift collection rates, and solid-state battery processing where incumbents lack capability. The interplay of policy, feedstock control and process innovation shapes future competitive positioning.

Black Mass Recycling Industry Leaders

Glencore

Redwood Materials Inc.

Umicore

Ganfeng Lithium Group Co., Ltd

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Rocklink India launched a lithium-ion battery recycling facility with a capacity of 10,000 tonnes in Sikandrabad, Uttar Pradesh. The facility focused on black mass production and rare earth magnet recovery, utilizing European R2 technology to achieve a 98% metal recovery rate and strengthen India's domestic battery supply chain.

- January 2026: MaxVolt Energy established a subsidiary named 'MaxVolt ReEarth' to enter the lithium battery recycling market in India. The company's strategy emphasized second-life applications and black mass production.

Global Black Mass Recycling Market Report Scope

Black mass recycling is the process of recovering valuable metals, primarily lithium, cobalt, nickel, and manganese, from the powdered mixture produced by shredding spent lithium-ion batteries. It is a critical, high-efficiency stage in the battery circular economy that transforms hazardous waste into battery-grade raw materials using pyro- or hydrometallurgical techniques.

The battery recycling market is segmented by battery type, material type, source, technology and geography. By battery type, the market is segmented into lithium-ion (including NMC, NCA, and LFP), nickel-metal hydride (NiMH), lead-acid, solid-state (emerging), and other battery types. By material type, the market is segmented into lithium, cobalt, nickel, manganese, graphite, and other materials. By source, the market is segmented into EV batteries, consumer electronics, energy storage systems, industrial power tools, and other sources. By technology, the market is segmented into pyrometallurgical processes, hydrometallurgical processes, combined (hybrid) processes, direct recycling/physical separation, and bio-leaching. The report also covers the market size and forecasts for Black mass recyling in 15 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Lithium-ion (NMC, NCA, LFP) |

| Nickel-metal Hydride (NiMH) |

| Lead-acid |

| Solid-state (Emerging) |

| Others |

| Lithium |

| Cobalt |

| Nickel |

| Manganese |

| Graphite |

| Others |

| EV Batteries |

| Consumer Electronics |

| Energy-storage Systems |

| Industrial Power Tools |

| Others |

| Pyrometallurgical Process |

| Hydrometallurgical Process |

| Combined (Hybrid) Processes |

| Direct Recycling / Physical Separation |

| Bio-leaching |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Battery Type | Lithium-ion (NMC, NCA, LFP) | |

| Nickel-metal Hydride (NiMH) | ||

| Lead-acid | ||

| Solid-state (Emerging) | ||

| Others | ||

| By Material Type | Lithium | |

| Cobalt | ||

| Nickel | ||

| Manganese | ||

| Graphite | ||

| Others | ||

| By Source | EV Batteries | |

| Consumer Electronics | ||

| Energy-storage Systems | ||

| Industrial Power Tools | ||

| Others | ||

| By Technology | Pyrometallurgical Process | |

| Hydrometallurgical Process | ||

| Combined (Hybrid) Processes | ||

| Direct Recycling / Physical Separation | ||

| Bio-leaching | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the black mass recycling market in 2026?

The black mass recycling market size stands at USD 16.42 billion in 2026, on track to reach USD 39.04 billion by 2031.

What CAGR will black mass recycling record through 2031?

The market is forecast to advance at an 18.91% CAGR between 2026 and 2031.

Which feedstock contributes most to recycling plants today?

EV batteries delivered 58.23% of black mass tonnage in 2025 and will remain the largest source as warranty returns accelerate.

Which region leads in processing capacity?

Asia-Pacific held 48.89% of global market share in 2025, anchored by China’s integrated ecosystem of cell makers and recyclers.

Page last updated on: