AI Recruitment Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

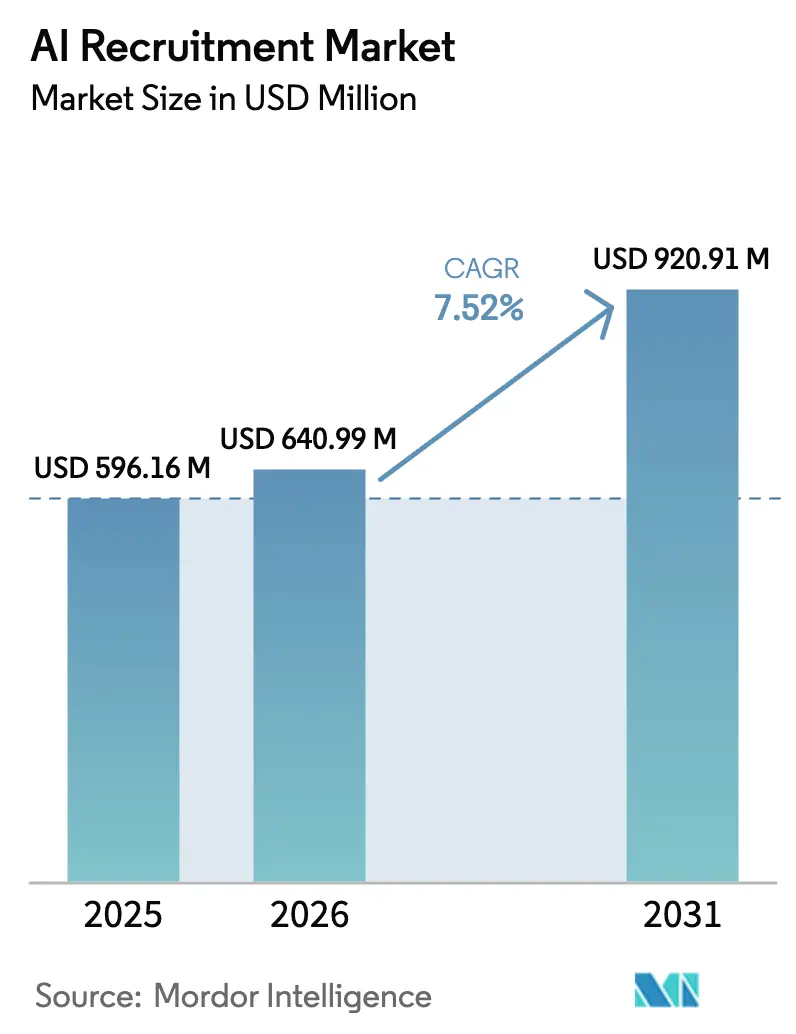

| Market Size (2026) | USD 640.99 Million |

| Market Size (2031) | USD 920.91 Million |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Recruitment Market Analysis by Mordor Intelligence

The AI recruitment market size is expected to grow from USD 596.16 million in 2025 to USD 640.99 million in 2026 and is forecast to reach USD 920.91 million by 2031 at 7.52% CAGR over 2026-2031. Across the globe, enterprises are shifting from small-scale pilots to enterprise-wide roll-outs, with 70% of organizations already experimenting with AI in HR and 92% claiming measurable benefits. Intensifying competition for digital talent, strict compliance requirements, and the need to handle high-volume hiring at speed keep adoption on an upward path. Software remains the principal value driver, yet services outpace it in growth as firms rely on integrators to embed AI tools within existing HR ecosystems. Regionally, North America retains leadership, but Asia-Pacific registers the fastest gains as local investment surges and cloud spending accelerates.

Key Report Takeaways

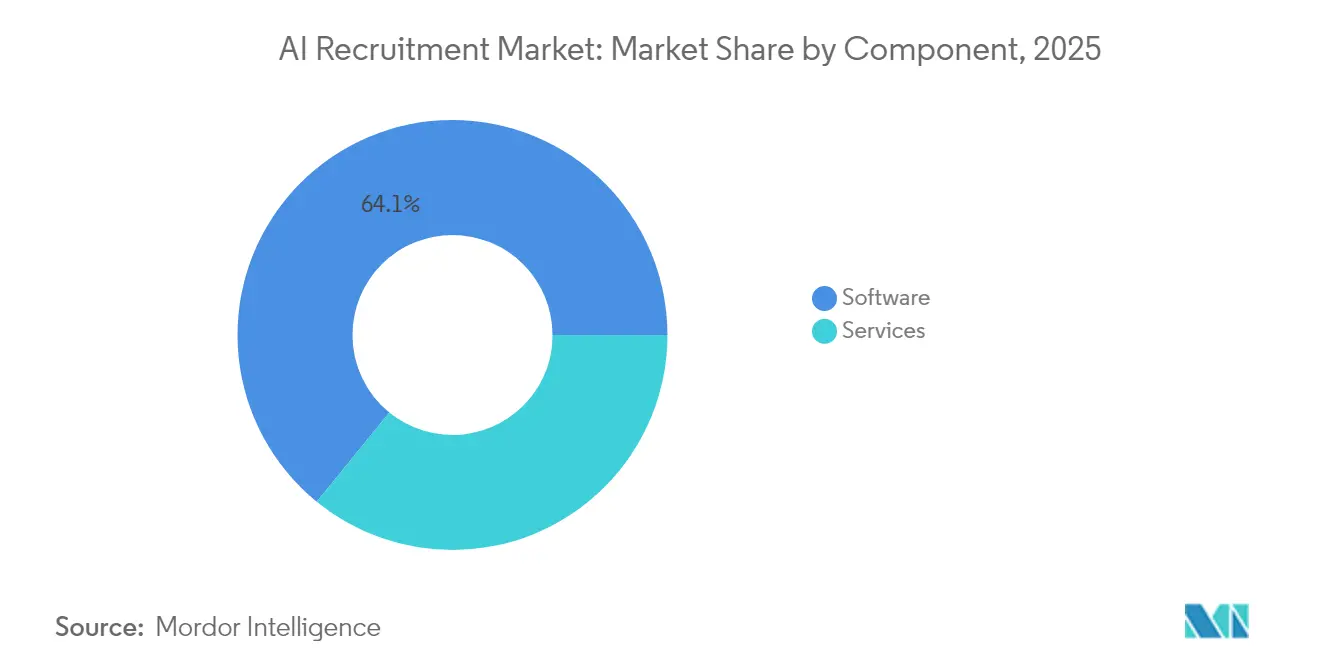

- By component, software held 64.12% of AI recruitment market share in 2025, while services are projected to expand at an 11.52% CAGR to 2031.

- By enterprise size, large enterprises led with 57.22% revenue share in 2025; small and medium enterprises are set to grow at a 10.05% CAGR through 2031.

- By deployment mode, cloud deployment captured 77.94% of the AI recruitment market size in 2025 and is projected to rise at a 19.05% CAGR between 2026-2031.

- By application, candidate screening and assessment represented 31.85% of the AI recruitment market size in 2025, while analytics and reporting will accelerate at a 13.72% CAGR.

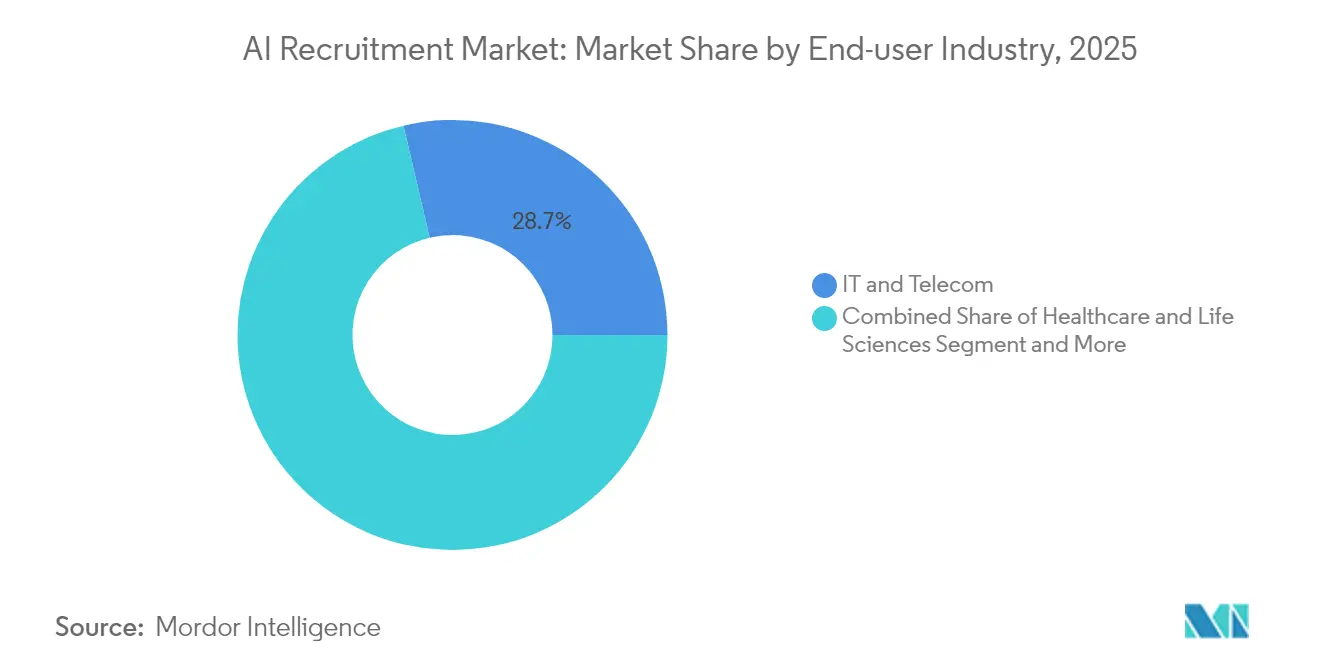

- By industry, IT and telecommunications dominated with 28.66% of AI recruitment market share in 2025; healthcare is forecast to post a 13.05% CAGR through 2031.

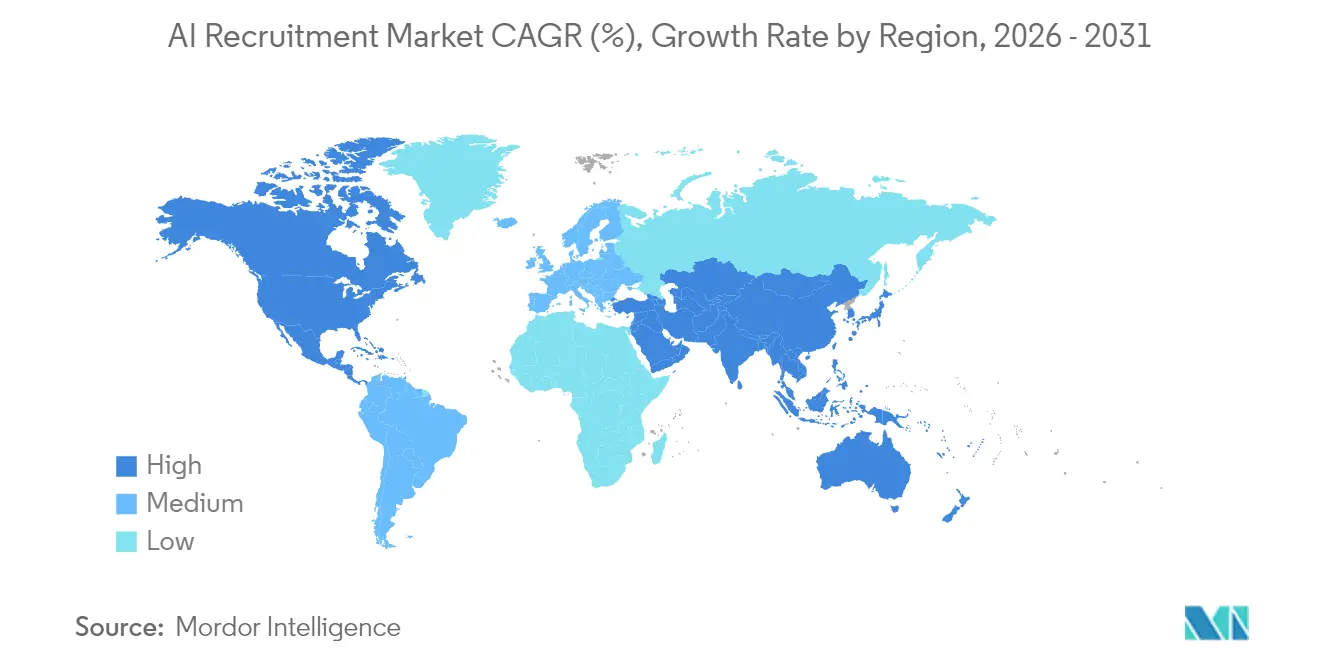

- By geography, North America commanded 41.62% of 2025 revenue, whereas Asia-Pacific is expected to register a 19.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI Recruitment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficiency demand in hiring | +2.1% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Candidate-experience focus | +1.8% | Global, prominent in talent-scarce markets | Medium term (2-4 years) |

| High-volume gig-work recruiting | +1.5% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Generative-AI job-description optimisation | +1.2% | Tech-forward regions worldwide | Short term (≤ 2 years) |

| Ethical-AI certification in vendor choice | +0.8% | Europe and North America, spreading globally | Long term (≥ 4 years) |

| Diversity audits via recruiting analytics | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Efficiency demand in hiring | +2.1% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing need for efficiency in hiring processes

Enterprises routinely report 75% shorter time-to-hire after automating early-stage screening. Unilever, for example, saved GBP 1 million annually and boosted workforce diversity by 16% after embedding conversational AI into graduate recruitment.[1]Unilever, “Digital Recruitment Transformation Case Study,” unilever.comGeneral Motors processed 74,000 video interviews in one year and trimmed scheduling from 5 days to 29 minutes, cutting annual costs by USD 2 million. Platforms with robotic process automation now sift 600+ applications per day while maintaining tailored messaging that keeps candidates engaged. These gains free recruiters to focus on relationship building and strategic workforce planning rather than manual résumé review.

Increasing focus on enhancing candidate experience

Chat-based assistants available 24/7 now reach customer-satisfaction scores near 96%. United Overseas Bank observed a 15% jump in offer acceptance after replacing phone screens with an AI assistant offering asynchronous interviews and instant feedback.[2]Paradox, “Compass Group Automates Hiring with Paradox Olivia,” paradox.ai Surveys show 86% of applicants prefer self-paced interviews that accommodate time-zone differences, widening the global talent pool. Natural-language models can surface overlooked skills and craft tailored coaching tips, reducing drop-off rates among under-represented groups and improving brand perception.

Rise in high-volume recruiting for gig workforce

Service industries that add tens of thousands of hires each year increasingly rely on AI to match workers to short-term assignments within minutes. McDonald’s now interacts with millions of applicants annually through its AI chatbot and records 95% positive sentiment. Compass Group compressed its application flow from 9 minutes to under 3 minutes and multiplied interview conversion sixfold by automating screening and scheduling. These examples underscore the pivotal role of AI in scaling contingent hiring without sacrificing hiring quality.

Integration of generative-AI for job-description optimisation

More than 70% of recent deployments incorporate generative models to draft inclusive, bias-free job adverts. Employers cite 30% more applications after re-writing postings with inclusive vocabulary, and 42% higher shortlist-to-hire conversion when AI suggests realistic skills requirements. Continuous learning loops allow systems to adjust wording based on acceptance trends, keeping advertisements aligned with evolving candidate expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic bias and ethical risks | -1.8% | Global, pronounced in regulated sectors | Medium term (2-4 years) |

| Data-privacy and retention regulations | -1.5% | Europe and North America, broadening worldwide | Long term (≥ 4 years) |

| Recruiter skill-gap resistance | -1.2% | Varies by organizational maturity | Short term (≤ 2 years) |

| High false-positives in multilingual NLP | -0.9% | Asia-Pacific and other multilingual markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns about algorithmic bias and ethical issues

Surveys find 54.5% of employers naming bias risk as the top hurdle to AI recruitment market adoption. Past incidents—such as an AI model inadvertently filtering out qualified female engineers—highlight the danger of training on unbalanced historical data. The forthcoming EU AI Act classifies recruitment tools as “high-risk,” mandating bias audits and human oversight, which raises both compliance cost and implementation complexity.[3]European Union, “Regulation Laying Down Harmonised Rules on Artificial Intelligence (EU AI Act),” eur-lex.europa.eu Vendors are responding with bias-detection dashboards and explainability modules, but enterprises still invest heavily in governance frameworks to preserve trust.

Data-privacy (GDPR/CCPA) and retention constraints

The GDPR’s consent requirements and the CCPA’s deletion rights restrict the volume and longevity of applicant data that can be stored. Non-compliance fines of up to 4% of annual revenue make data governance a boardroom priority. Companies must maintain fine-grained consent records, encryption policies, and cross-border transfer safeguards. Smaller firms often lack the resources to manage these tasks, slowing AI recruitment industry roll-outs or tilting preference toward vendors offering embedded compliance tooling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

Software accounted for 64.12% of 2025 revenue, cementing its role as the backbone of the AI recruitment market. Suites that combine conversational AI, skills inference, and predictive analytics deliver rapid ROI by automating résumé parsing and interview scheduling. In parallel, services—implementation, integration, training—are projected to grow at an 11.52% CAGR as enterprises recognize that successful adoption hinges on change management rather than code alone.

Managed services providers deploy configurable accelerators that stitch AI modules into legacy applicant-tracking systems, ensuring data fidelity and compliance. Demand for optimization workshops and bias-monitoring audits will enlarge the professional-services opportunity, creating a recurring revenue flywheel linked directly to platform renewals.

By End-user Enterprise Size: SMEs Accelerate Adoption

Large organizations retained 57.22% of spending in 2025, drawing on global HRIS footprints to embed AI at scale. Yet the small and medium-enterprise segment leads growth at a 10.05% CAGR as cloud-native platforms deliver enterprise-grade functions via subscription. SMEs now access best-practice templates and auto-generated workflow settings that compress deployment to days.

This diffusion of capability is leveling competitive ground. Mid-sized manufacturers, for instance, can screen qualified welders through skills simulations hosted in the browser, while boutique consultancies deploy automated sourcing agents that comb professional networks overnight. These capabilities, once confined to multinationals, are widening market penetration.

By Deployment Mode: Cloud Supremacy Accelerates

Cloud solutions captured 77.94% share in 2025 and will compound at 19.05% annually through 2031. The AI recruitment market favors cloud because updates, language-model retraining, and security patches roll out instantly. Recruiters working remotely gain browser-based access without VPN hurdles, and vendors leverage elastic compute to run large-language models for résumé matching at peak traffic.

On-premise deployments persist in defense and regulated financial services, where data-sovereignty statutes apply. Even here, hybrid models are common: sensitive personally identifiable information stays on private servers while anonymized skills data routes to public-cloud algorithms for ranking. That arrangement balances control with innovation.

By Application/Function: Analytics Emergence Signals Maturity

Screening and assessment, holding 31.85% of 2025 expenditure, remain the entry point for most buyers as benefits are immediate and measurable. Forecasts, however, show analytics and reporting accelerating at 13.72% CAGR. Boards now demand dashboards that correlate sourcing channels with retention outcomes and diversity ratios, prompting investments in predictive hiring analytics.

Such tools surface patterns—like which assessment questions correlate with six-month performance—helping recruiters continuously refine criteria. The shift illustrates market maturation from transaction automation to evidence-based workforce planning, underpinned by explainable AI modules that justify every recommendation.

By End-user Industry: Healthcare Urgency Drives Growth

IT and telecommunications controlled 28.66% revenue in 2025, consistent with their early adoption culture. Health systems, however, post the fastest 13.05% CAGR. Staffing shortages in nursing and radiology make automation essential. AI platforms that verify credentials against licensing boards and match clinicians to shift openings shorten vacancy windows, improving patient outcomes.

Government and public-sector demand also climbs as agencies follow presidential directives to infuse AI talent across departments. Vendors must satisfy strict equal-employment requirements and handle security-clearance workflows, reinforcing the need for configurable compliance layers.

By AI Technology: RPA Automation Gains Momentum

Natural-language processing accounted for 34.52% revenue in 2025, powering chat interfaces and résumé parsing. Robotic process automation is projected to grow 13.08% per year as back-office tasks—data entry, interview calendar sync, offer-letter generation—shift to bots. Combining RPA with NLP enables end-to-end flow: a chatbot qualifies an applicant, triggers an RPA routine to schedule interviews, and archives documentation for auditors.

Computer-vision modules analyzing video interviews for micro-expression cues remain niche but are gaining acceptance in hospitality and sales hiring. Vendors stress transparent scoring and opt-in consent to mitigate privacy concerns.

Geography Analysis

North America generated 41.62% of 2025 revenue. United States enterprises poured over USD 100 billion into enterprise-AI projects last year, fostering a robust ecosystem of solution providers and venture funding. A federal mandate now requires each agency to appoint a chief AI officer, catalyzing public-sector demand for specialized hiring tools dhs.gov. Canada’s technology clusters in Toronto and Montréal promote cross-border talent mobility programs that integrate seamlessly with AI sourcing engines.

Asia-Pacific is the fastest-growing region, forecast at a 19.18% CAGR. Government incentives and a young, digitally savvy workforce drive adoption across China, India, Australia, and Singapore. Cloud-first procurement policies lower entry barriers for small businesses, while regional hyperscalers host localized large-language models that process multilingual résumés with improved accuracy. Investment momentum is visible in the surge of AI accelerators and hackathons that pair venture capital with corporate HR teams to pilot recruitment bots.

Europe records steady expansion under a strong regulatory framework anchored by the GDPR and the upcoming EU AI Act. Vendors thriving here embed explainability reports, bias-mitigation controls, and granular consent tracking from day one. Countries such as Germany and the Netherlands emphasize apprenticeship programs that integrate AI tools to route candidates into vocational tracks, illustrating how cultural norms shape technology application.

The Middle East and Africa and South America remain emerging but promising, with digital-government agendas and mobile-first populations positioning them for rapid future gains.

Competitive Landscape

The AI recruitment market remains moderately fragmented, yet consolidation accelerates. Salesforce acquired Moonhub to embed AI-first sourcing models within its broader talent suite. Bullhorn followed by buying Textkernel to strengthen semantic-search functions. These moves reflect a platform play: buyers prefer unified ecosystems that cover sourcing, engagement, assessment, and analytics.

Pure-play innovators still thrive in niche domains. Paradox supplies conversational bots optimized for hourly hiring and claims processing of millions of applicant chats yearly. Beamery focuses on skills-graph analytics that forecast future workforce gaps. Meanwhile, SAP and NVIDIA collaborate to accelerate generative-AI workloads inside SAP SuccessFactors, shortening large-model inference times. Oracle partners with OpenAI and Google Cloud so that clients can choose among foundation models hosted in Oracle Cloud Infrastructure, supporting model sovereignty while tapping hyperscale performance.

Competitive differentiation is shifting from feature count to outcome guarantees. Vendors increasingly quote reductions in time-to-fill and gains in diversity as contractual commitments. Ethical AI credentials—ISO/IEC 42001 compliance audits, third-party bias evaluations—now appear in request-for-proposal scoring. In response, leading suppliers open-source fairness libraries and publish annual transparency reports, further professionalizing the AI recruitment industry.

AI Recruitment Industry Leaders

SAP SE

Zoho Corporation

IBM Corporation

Oracle Corporation

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Salesforce completed the acquisition of Moonhub, integrating its team and IP into Agentforce to automate sourcing and screening while retaining human oversight.

- February 2025: The US Department of Homeland Security launched “AI Corps” to recruit 50 specialists, using expedited hiring authorities and flexible pay bands to compete with private sector offers.

- January 2025: The White House issued an executive order directing federal agencies to identify sites for AI-ready data centers powered by clean energy, targeting operational readiness by 2027.

- June 2024: Bullhorn purchased Textkernel, adding semantic search and matching to its recruitment platform to improve candidate discovery speed.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the AI recruitment market as the total annual spend on software and related services that apply machine-learning or natural-language techniques to automate any stage of the hiring life cycle, from talent sourcing and résumé parsing through interview scheduling, assessment scoring, offer generation, and onboarding analytics. Spend on generic HR suites in which AI features are switched off, as well as fees paid to external staffing agencies, fall outside this scope.

Segmentation Overview

- By Component

- Software

- Recruitment-automation suites

- Chatbots and conversational agents

- Assessment and testing platforms

- Services

- Implementation and Integration

- Training and Support

- Software

- By End-user Enterprise Size

- Small and Mid-sized Enterprises

- Large Enterprises

- By Deployment Mode

- Cloud

- On-Premise

- By Application/Function

- Sourcing and Talent Mapping

- Candidate Screening and Assessment

- Interview Scheduling and Communication

- Recruitment Marketing and Campaigning

- Analytics and Reporting

- On-boarding Automation

- By End-user Industry

- IT and Telecommunications

- BFSI

- Healthcare and Life Sciences

- Government and Public Sector

- Education

- Retail and E-commerce

- Manufacturing

- Logistics and Transportation

- By AI Technology

- Natural Language Processing (NLP)

- Machine Learning and Deep Learning

- Computer Vision

- Robotic Process Automation (RPA)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed HR-tech product managers, talent-acquisition leads at large enterprises, and regional compliance consultants in North America, Europe, and Asia-Pacific. Conversations clarified average selling prices, usage intensity by company size, and the likely impact of the EU AI Act on procurement cycles, allowing us to refine assumptions drawn from desk work.

Desk Research

We began with public datasets, including the United States Bureau of Labor Statistics, Eurostat, and Japan's Ministry of Health, Labor and Welfare, to map hiring volume and recruiter head count across regions. Industry bodies such as the Association for Talent Acquisition Professionals and the World Employment Confederation provided adoption benchmarks for applicant-tracking systems. Company 10-Ks, investor decks, and patent filings accessed through Questel helped us gauge vendor revenues and feature rollouts. News archives inside Dow Jones Factiva kept the team abreast of funding rounds and regulatory shifts. These sources illustrate, but do not exhaust, the secondary material reviewed.

Market-Sizing & Forecasting

A top-down demand pool, built from new job postings, average applicants per posting, and penetration rates for AI-enabled recruitment tools, established the 2025 baseline. Supplier roll-ups and channel checks supplied a selective bottom-up cross-check, and gaps were reconciled. Key variables in the model include: (1) cloud HR adoption rates, (2) median ATS price per seat, (3) regulatory audit cost per hire, (4) vacancy fill-time targets, and (5) unemployment-to-vacancy ratios. A multivariate regression, reviewed with our interview panel, projects these drivers to 2030, while scenario analysis handles sudden regulatory shocks.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against independent indicators, and a leadership sign-off. We refresh each model annually and trigger interim updates when funding spikes, major M&A, or new legislation materially alter assumptions.

Credibility Anchor: Why Mordor's AI Recruitment Baseline Resonates with Reality

Published numbers often differ because firms pick dissimilar scopes, currencies, or refresh intervals. When market values conflict, clients need to know which one mirrors hiring-floor reality.

Key Gap Drivers include whether spend on manual staffing services is blended with software, the treatment of bundled HR suites, assumptions on cloud price erosion, and how quickly each publisher adjusts for new audit mandates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 596.16 Mn (2025) | Mordor Intelligence | - |

| USD 660.17 Mn (2025) | Global Consultancy A | Includes non-AI modules inside broad HR suites |

| USD 577.70 Mn (2023) | Regional Consultancy B | Older base year and currency fixed at 2023 average FX rates |

| USD 656.17 Mn (2024) | Trade Journal C | Uses vendor list prices without discount adjustments |

The comparison shows how scope creep, legacy exchange rates, and unverified price lists inflate or suppress totals. By centering on verifiable spend, timely FX conversion, and a transparent variable set, Mordor Intelligence delivers a balanced, decision-ready baseline.

Key Questions Answered in the Report

What is the current value of the AI recruitment market?

The AI recruitment market is valued at USD 640.99 million in 2026 and is projected to grow to USD 920.91 million by 2031.

Which deployment mode is growing fastest in AI hiring platforms?

Cloud deployment leads growth with a 19.05% CAGR as organizations favor scalable, compliance-ready solutions.

Why is healthcare the fastest-expanding industry segment for AI recruitment?

Acute clinical staff shortages and stringent credentialing needs drive hospitals to automate candidate sourcing and verification, resulting in a 13.05% forecast CAGR through 2031.

How are vendors addressing algorithmic bias?

Leading platforms embed bias-detection dashboards, audit trails, and human-in-the-loop review features to comply with regulations such as the EU AI Act.

Page last updated on: