Online Recruitment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 37.49 Billion |

| Market Size (2031) | USD 64.93 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Recruitment Market Analysis by Mordor Intelligence

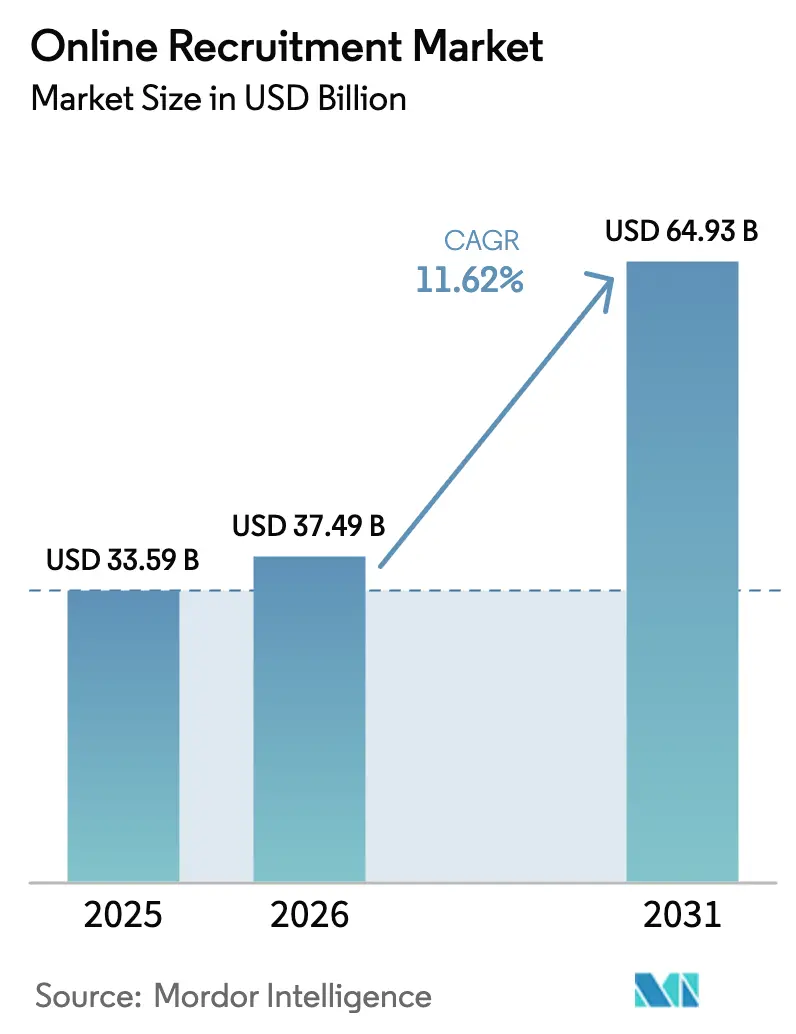

The online recruitment market size is expected to grow from USD 33.59 billion in 2025 to USD 37.49 billion in 2026 and is forecast to reach USD 64.93 billion by 2031 at 11.62% CAGR over 2026-2031. Digitization of hiring, rapid artificial-intelligence adoption, and the normalization of remote work combine to shorten time-to-hire by up to 40%, expand global talent pools, and lower cost-per-hire across industries. Enterprises accelerate platform spending as government agencies shift toward skills-based evaluation, compelling vendors to embed competency analytics and soft-skill assessment modules. Meanwhile, cloud-native tools and consumption-based pricing models reduce entry barriers for small and medium businesses, broadening platform addressability. Intensifying competition from AI-first disruptors forces incumbents to invest in full-suite solutions that unify job distribution, candidate engagement, evaluation, and onboarding.

Key Report Takeaways

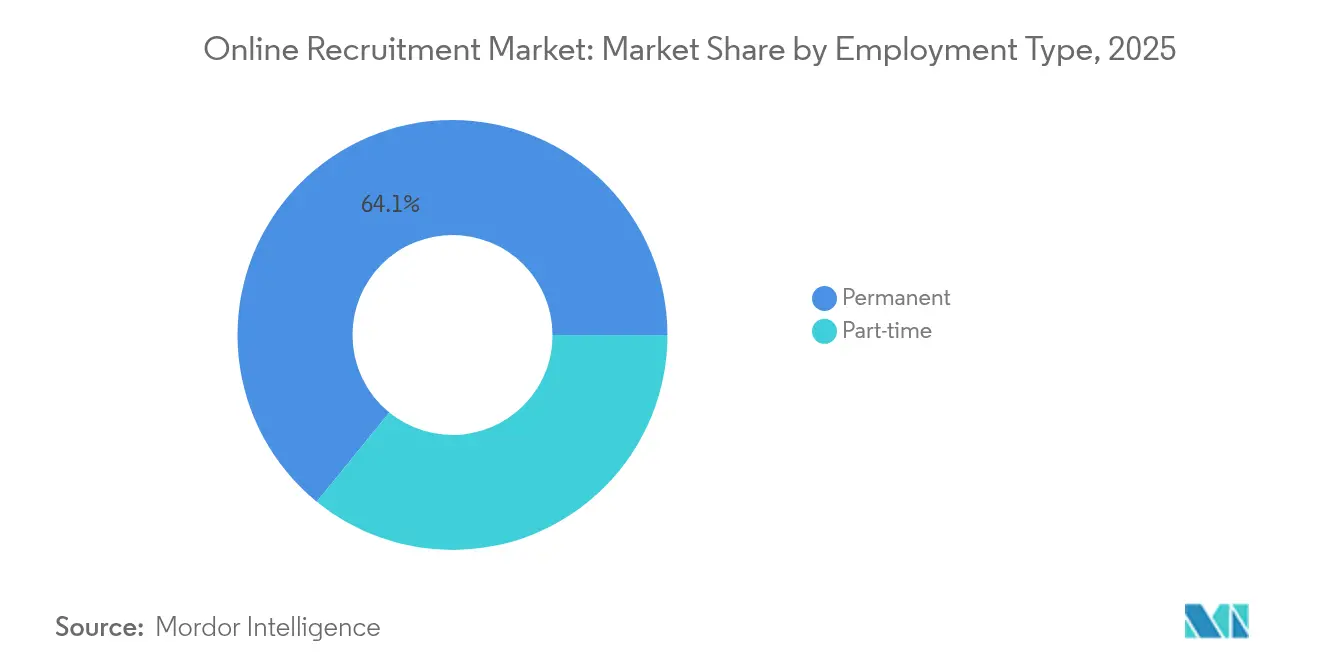

- By employment type, permanent roles led with 64.12% of the online recruitment market share in 2025, whereas part-time hiring is projected to advance at an 11.74% CAGR to 2031.

- By industry application, IT and Telecom commanded 27.85% revenue share in 2025; healthcare recruitment is expanding at a 13.15% CAGR through 2031.

- By platform category, job boards accounted for 44.72% share of the online recruitment market size in 2025, while video-interview platforms are growing at a 39.2% CAGR.

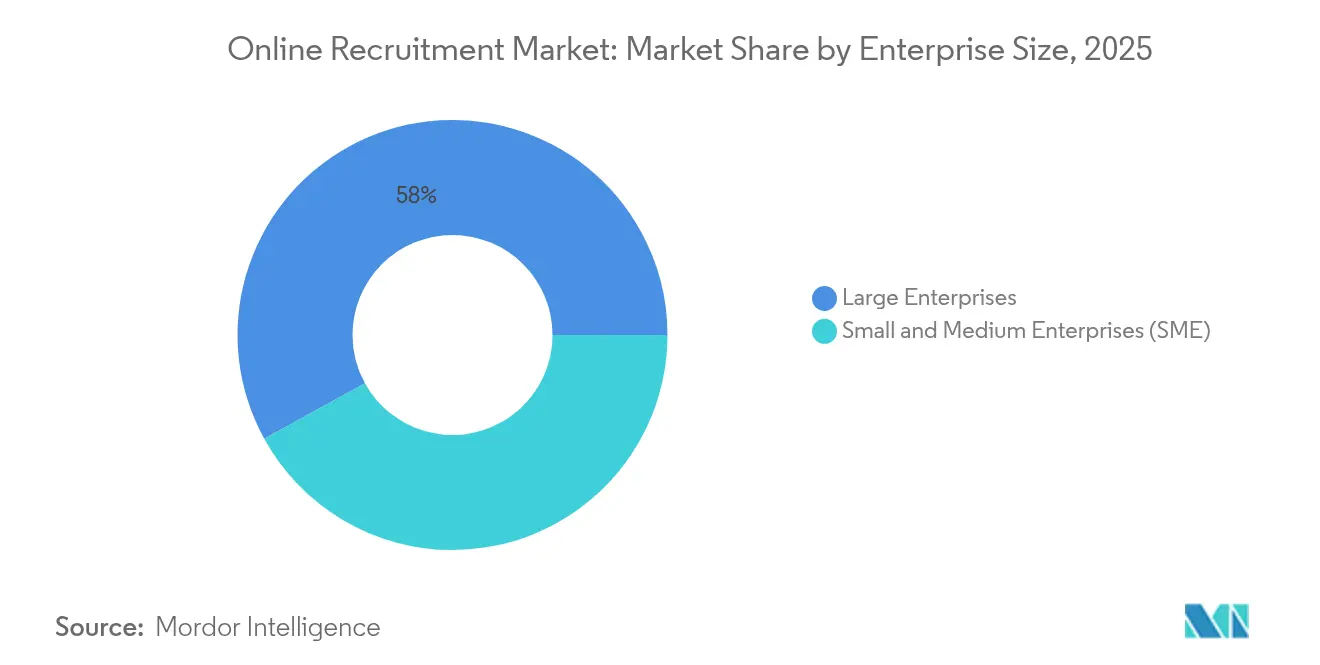

- By enterprise size, large enterprises held 58.02% share in 2025, yet SMEs record the fastest CAGR at 12.54% through 2031.

- By pricing model, subscription services captured 52.01% revenue share in 2025, whereas freemium offerings are expanding at a 14.22% CAGR.

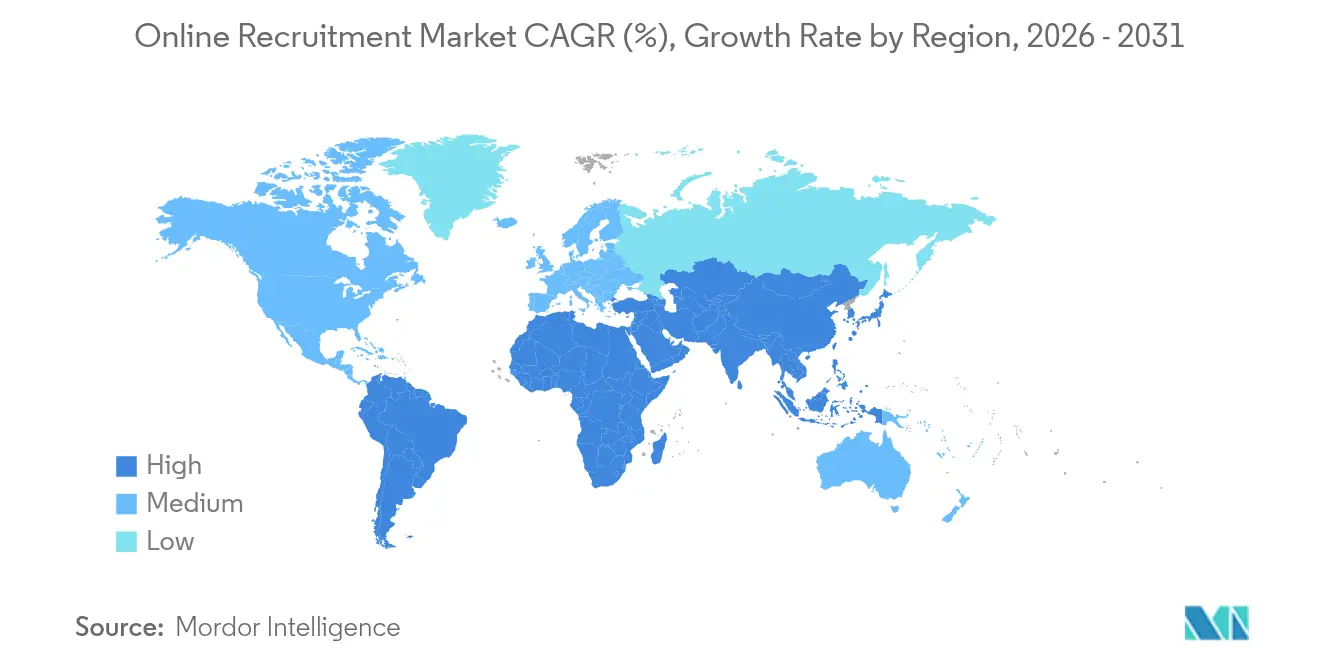

- By geography, North America represented 37.28% market share in 2025; Asia-Pacific is forecast to post the highest regional CAGR at 11.86% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Recruitment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven hiring automation | +2.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Social-media-led talent sourcing | +1.9% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Remote-work demand spike | +2.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Gig-ATS integrations | +1.6% | North America and Asia-Pacific core, expanding to Europe | Medium term (2-4 years) |

| Blockchain credentials | +0.8% | Early adoption in North America and select European markets | Long term (≥ 4 years) |

| Government skills-based hiring mandates | +1.4% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-driven hiring automation

AI platforms now parse résumés, rank applicants, and conduct first-round interviews, with 87% of large enterprises embedding at least one AI module into recruitment workflows. Microsoft’s LinkedIn reports that machine-learning-based suggestions lift recruiter response rates by 35%. Fortune 500 employers rely on AI for more than three-quarters of applicant evaluations, and autonomous agents that draft outreach messages, schedule calls, and compile interview notes now enter pilot production. Vendors differentiate by pairing these agents with human oversight dashboards that satisfy new audit requirements under the EU AI Act.

Social-media-led talent sourcing

Recruiters integrate professional-network data streams directly into applicant-tracking systems, merging peer endorsements, content engagement, and network reach into a single talent score. Cross-platform analytics reveal that passive candidates contacted via targeted ads convert to applicants at double the rate of generic job-board traffic. Advanced dashboards map follower demographics to pipeline gaps, letting teams reposition campaigns in real time. As regional preferences differ—Asia-Pacific favors messaging apps while North America focuses on professional networks—platform vendors embed localization templates that automate channel selection and post timing.

Remote-work demand spike

Seventy-four percent of roles capable of remote execution moved to hybrid schedules in 2025, widening recruiter access to global talent pools. The number of digital nomads exceeded 40 million, prompting companies to recalibrate compensation bands and compliance checks by jurisdiction. AI interview schedulers cut cross-time-zone coordination by 60%, and virtual-reality office tours help candidates visualize team culture despite distance. Yet visibility bias risks emerge: studies show remote workers receive 18% fewer high-impact project assignments, driving employers to redesign performance metrics. Platform roadmaps now include inclusion analytics to detect geography-driven progression gaps and surface remedial actions to HR leaders.

Gig-ATS integrations

Mainstream applicant-tracking systems add APIs to leading freelance marketplaces, merging short-term and permanent requisitions in one dashboard. Randstad’s 2024 report notes a 42% increase in enterprise use of integrated gig modules to meet project surges [1]Randstad N.V., “Annual Report 2024,” randstad.com. AI matching engines rank contingent workers on verified project ratings, enabling next-day onboarding for specialized tasks in cybersecurity, design, or analytics. Analytics loops then compare gig-worker retention, re-hire frequency, and performance to optimize future talent mixes. The model solves workforce elasticity pain points yet forces HR teams to master dual compliance regimes for employees and contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fake and deceptive applications | –1.8% | Global, particularly acute in North America | Short term (≤ 2 years) |

| Data-privacy compliance costs | –1.4% | Europe and North America, expanding globally | Medium term (2-4 years) |

| AI-bias regulatory scrutiny | –1.1% | North America and Europe, Asia-Pacific following | Medium term (2-4 years) |

| Job-board consolidation impact | –0.9% | Global, strongest in mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fake and deceptive applications

Generative-AI tools automate résumé fabrication and deep-fake video interviews, flooding recruiter inboxes with synthetic profiles. U.S. federal agencies recently introduced multi-layer identity verification after detection rates of fraudulent applications rose to 15% in remote-first postings. Vendors respond with document-forensics AI, liveness checks, and blockchain-anchored credential wallets, but the added layers extend screening times and raise platform costs. Smaller employers lacking budget for advanced verification outsource vetting to specialized providers, introducing extra steps that can deter genuine applicants.

Data-privacy compliance costs

Recruitment platforms operating in Europe must now classify candidate-evaluation algorithms as “high risk” under the EU AI Act, triggering mandatory bias testing, human override mechanisms, and external audit submission. Concurrently, GDPR enforcement actions exceed EUR 1.5 billion in fines industry-wide, incentivizing heavy investment in consent orchestration engines and data-retention vaults. Multinational platforms incur parallel expenses complying with the California Privacy Rights Act and Brazil’s LGPD. Compliance headcount and tooling together consume up to 9% of annual platform operating budgets, diverting resources from feature innovation and slowing release cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Employment Type: Permanent hiring underpins workforce continuity

Permanent positions accounted for 64.12% of total placements in 2025, underscoring employers’ preference for institutional knowledge retention and strategic capability building. This dominance anchors the online recruitment market, providing recurring demand that steadies vendor revenue even during macro-economic swings. Investing in leadership-track roles, firms deploy competency assessments to evaluate cultural fit and succession potential. Skills-based mandates issued by U.S. federal bodies now enable candidates without traditional degrees to compete for permanent roles, broadening available talent and easing diversity targets. Part-time and project-based arrangements, while secondary, register an 11.74% CAGR to 2031 as organizations seek cost agility and employees value flexibility. Integration of gig-market APIs into applicant-tracking suites lets HR staff toggle requisitions between permanent and contingent settings, fostering a hybrid model. As a result, the online recruitment market supports blended workflows where core staff handle strategic tasks while external specialists address surge requirements. Recruiters thus recalibrate talent pipelines, maintaining passive pools of both full-time and fractional professionals ready for activation on short notice.

By Industry Application: Healthcare outpaces IT for growth

IT and Telecom held 27.85% share of the online recruitment market in 2025, buoyed by constant demand for cloud architects, data engineers, and cybersecurity analysts. Employers refine screening algorithms to weight practical code-challenge scores above academic pedigree, aligning with skills-based trends. Yet vacancy backlogs in nursing, allied health, and geriatric care trigger a 13.15% CAGR for healthcare recruitment, the fastest among tracked verticals. Automated license verification and clinical-skill simulations embedded into hiring portals reduce compliance bottlenecks and accelerate clinician onboarding timelines. Budget-constrained hospital systems adopt AI chatbots that triage inquiries, schedule interviews, and push personalized offers, cutting recruiter load by 40%. Meanwhile, finance, engineering, and sales functions maintain steady volumes, integrating behavioral-assessment videos for soft-skill evaluation. Renewable-energy developers, grouped under “others,” leverage niche platforms that match technicians based on turbine-maintenance certifications, further diversifying application demand across the online recruitment market.

By Platform Category: Video interviewing accelerates digital screening

Job boards still contribute 44.72% of placements, acting as top-of-funnel aggregators for keyword-based searches. However, the online recruitment market is pivoting toward richer assessment mediums: HireVue alone hosted 33 million on-demand interviews in the past year. Video-interview platforms grow at a 39.2% CAGR as asynchronous recording eliminates scheduling friction and AI models evaluate vocal tone, sentiment, and problem-solving approach in real time. Applicant-tracking systems remain the workflow spine, integrating calendar tools, background checks, and onboarding modules. Recruitment marketplaces introduce direct employer–candidate matching algorithms that minimize intermediary steps, while social-recruiting plug-ins syndicate requisitions across professional networks. Vendors increasingly bundle these capabilities into unified suites, enabling clients to manage sourcing, screening, and offer management without switching contexts, thereby boosting platform stickiness in the online recruitment market.

By Enterprise Size: SMEs narrow the technology gap

Large enterprises generated 58.02% of 2025 revenue, leveraging sizable HR budgets to license full-stack suites such as Workday Recruiting; Workday added USD 2.24 billion in subscription revenue last fiscal year . These corporates layer AI matching, predictive attrition analytics, and gamified assessments to safeguard global talent pipelines. They also pilot blockchain credential wallets, anticipating long-term compliance savings. Small and medium enterprises increase spending at a 12.54% CAGR, enabled by cloud delivery, freemium entry tiers, and template-driven onboarding that removes the need for dedicated IT staff. Such democratization expands the addressable base of the online recruitment market. Lightweight browser extensions post vacancies to multiple boards in one click, and embedded pay-per-candidate options align costs to hiring cycles. SMEs thus adopt features once limited to Fortune 500 budgets, intensifying overall market competition and pushing vendors to release tiered functionality roadmaps.

By Pricing Model: Freemium widens funnel while subscriptions anchor revenue

Subscription contracts captured 52.01% share in 2025, favored by enterprises seeking predictable budgeting and full-feature access. Multi-year deals often bundle analytics modules and candidate-relationship management add-ons, stabilizing vendor cash flows across business cycles. In contrast, freemium plans grow at a 14.22% CAGR, targeting startups and micro-firms. Such models expose basic applicant-tracking features at no cost, monetizing through premium upgrades, contextual ads, or usage-based video assessment credits. Pay-per-post retains relevance for episodic hiring, especially in construction or seasonal retail, where requisition volumes fluctuate. Hybrid pricing emerges as vendors experiment with per-hire success fees layered atop base subscriptions, ensuring alignment with client outcomes. This diversity underscores how the online recruitment market caters to heterogeneous procurement preferences while migrating steadily toward value-based, data-rich service bundles.

Geography Analysis

North America generated 37.28% of 2025 revenue, underpinned by early cloud-HR adoption, high digital-skill penetration, and extensive venture funding for talent-tech startups. LinkedIn exceeded USD 16.4 billion in platform revenue, reflecting network-effect resilience. Indeed’s migration toward an agency model broadens monetization by embedding sourcing, screening, and pay-per-start payroll services. Federal skills-first hiring directives further stimulate platform upgrades as agencies require assessment engines that de-emphasize credentials in favor of competency outcomes.

Asia-Pacific delivers the fastest growth at 11.86% CAGR. India’s production-linked-incentive program drives manufacturing payroll expansion, feeding demand for digital screening solutions that can process multilingual applicant pools. The International Labour Organization projects 34 million net new positions regionwide in 2025 despite slowing macro indicators, magnifying platform importance . Digital-skills bootcamps across Vietnam and the Philippines funnel graduates directly into marketplace portals, while mobile-first interfaces dominate user-experience design given smartphone dependency. Europe advances steadily, balancing innovation with privacy safeguards. Clear guidance under the EU AI Act encourages enterprise investment by clarifying audit, documentation, and human-oversight requirements. Brexit-driven visa complexities elevate cross-border hiring service demand, encouraging platforms to embed work-authorization checks natively. Meanwhile, Middle East and Africa witness early-stage acceleration as governments digitize public services and diversify economies beyond hydrocarbons. GCC employers compete for scarce AI and cybersecurity talent, elevating premium placement fees and boosting region-specific platform entries into the broader online recruitment market.

Competitive Landscape

The online recruitment market exhibits moderate concentration. LinkedIn leverages network data depth to secure unrivaled sourcing reach, while Indeed expands downstream into agency services to defend share. Workday augments its human-capital-management suite by purchasing niche AI firms, integrating bias-detection and explainable-scorecard modules. Bullhorn’s acquisition of Textkernel adds semantic-search capabilities that raise candidate-matching accuracy by 20%.

Disruptors such as Mercor achieve USD 2 billion valuations by marketing AI agents that autonomously rank applicants and schedule interviews, selling workflow automation rather than job ads. Their cloud-native architecture reduces onboarding time for clients from weeks to hours, a key differentiator in the SME segment. Incumbents respond with venture-funded innovation arms and open-API ecosystems to encourage third-party extensions and protect installed bases.

Strategic priorities increasingly converge on three pillars: bias-aware AI, verifiable credentials, and holistic talent-lifecycle analytics. Partnerships between technology vendors and staffing majors (e.g., Workday–Randstad) illustrate a trend toward full-service offerings combining software, advisory, and on-demand recruiter capacity. Geographic expansion strategies focus on Asia-Pacific and the GCC, where double-digit growth offsets plateauing North American volumes.

Online Recruitment Industry Leaders

LinkedIn Corporation

Recruit Holdings Co., Ltd.

StepStone Group GmbH

ZipRecruiter Inc.

Seek Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Salesforce acquired Moonhub, an AI recruiting startup, to enhance Agentforce platform capabilities.

- June 2025: Metaview raised USD 35 million to automate recruiter administrative tasks with AI-powered transcription and note-taking.

- January 2025: Mercor closed a USD 100 million Series B round at a USD 2 billion valuation to scale its AI hiring platform.

- January 2025: Workday and Randstad formed a strategic partnership to integrate global staffing expertise with Workday’s HCM suite.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the online recruitment market as all fee-based digital venues, job boards, applicant-tracking suites, social media hiring modules, video-interview tools, and AI-matching services through which employers post vacancies, search resumes, screen candidates, and purchase value-added analytics.

Scope exclusion: Purely offline staffing agencies and stand-alone payroll outsourcing are outside the study.

Segmentation Overview

- By Employment Type

- Permanent

- Part-Time

- By Industry Application

- IT and Telecom

- Finance

- Sales and Marketing

- Engineering

- Healthcare

- Hotel and Catering

- Others

- By Platform Category

- Job Boards

- Applicant Tracking Systems (ATS)

- Recruitment Marketplaces

- Freelance and Gig Platforms

- Video Interview Platforms

- Social Recruiting Tools

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Pricing Model

- Subscription

- Pay-Per-Post

- Freemium / Ad-Supported

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed HR directors, talent-tech product managers, and independent recruiters across North America, Europe, and Asia-Pacific. Conversations clarified average spend per job post, free-to-paid upgrade triggers, and regional compliance costs, which let us challenge and refine desk findings.

Desk Research

Mordor analysts began by mining authoritative, open datasets such as International Labour Organization labor participation files, US Bureau of Labor Statistics employment services revenue tables, Eurostat ICT usage surveys, World Bank broadband penetration series, and patent counts from Questel for recruitment tech innovations. Company filings, investor decks, respected HR trade associations, and regulatory consultation papers supplied price points and adoption cues. Dow Jones Factiva helped us track quarterly platform revenue shifts. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct starts with national employment service turnover, internet user counts, and job-ad penetration rates, which are then blended with platform take-rates to derive the value. Selected bottom-up roll-ups include public vendor sales, sampled subscription pricing times active customers, and channel checks that cross-verify totals. Key variables modeled include global hiring volumes, average digital recruitment spend per hire, internet and mobile adoption, share of ad budgets shifting to programmatic recruiting, and regulatory pushes for fair-hiring tech. Multivariate regression projects each driver, while scenario analysis stress-tests optimistic and cautious hiring cycles. Any data gap in bottom-up layers is bridged by regional averages validated through expert calls.

Data Validation & Update Cycle

Outputs undergo variance scans against external indicators, peer benchmarks, and earlier editions. Senior reviewers sign off only after anomalies are addressed. We refresh the model annually, with interim updates when material events, large M&A or regulatory shifts, occur, and a last-mile validation happens just before client release.

Why Mordor's Online Recruitment Baseline Earns Decision-Maker Trust

Published estimates often diverge because firms adopt distinct market scopes, base years, and currency conversions.

Key gap drivers include whether gig platforms are counted, how average spend per posting is trended, refresh cadence, and the balance between vendor revenue rolls and macro labor statistics that others overlook.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.59 B (2025) | Mordor Intelligence | ― |

| USD 57.70 B (2025) | Global Consultancy A | Merges broader HR tech revenues with recruitment spend, inflating total |

| USD 36.80 B (2024) | Trade Journal B | Uses constant 2022 exchange rates and omits emerging-market currency impact |

| USD 13.20 B (2024) | Industry Publisher C | Focuses only on recruitment software licences, excluding job-board advertising |

The comparison shows that when scope, drivers, and annual updates are aligned, Mordor delivers a balanced, transparent baseline traceable to clear variables and repeatable steps, giving clients confidence for strategic planning.

Key Questions Answered in the Report

What is the current size of the online recruitment market?

It reached USD 37.49 billion in 2026 and is projected to climb to USD 64.93 billion by 2031.

Which region is growing fastest in online recruitment adoption?

Asia-Pacific leads with an 11.86% CAGR, driven by manufacturing expansion and digital-skills initiatives.

Which platform category is expanding most rapidly?

Video-interview platforms grow at a 39.2% CAGR as employers embrace asynchronous screening.

How are government policies influencing hiring platforms?

Skills-based mandates push vendors to embed competency assessments, while EU AI regulations drive audit-ready algorithm design.

Page last updated on: