Recruitment Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

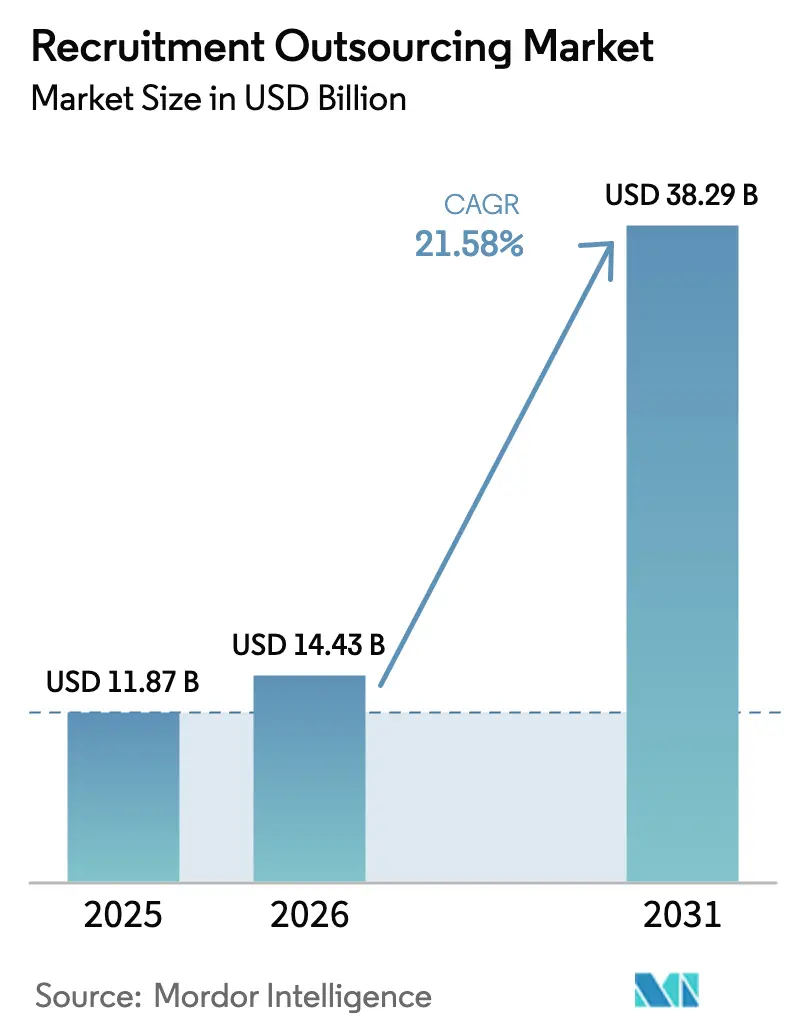

| Market Size (2026) | USD 14.43 Billion |

| Market Size (2031) | USD 38.29 Billion |

| Growth Rate (2026 - 2031) | 21.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recruitment Outsourcing Market Analysis by Mordor Intelligence

The recruitment outsourcing market size is expected to grow from USD 11.87 billion in 2025 to USD 14.43 billion in 2026 and is forecast to reach USD 38.29 billion by 2031 at 21.58% CAGR over 2026-2031. Growth accelerates as employers adopt variable-cost operating models to cope with persistent talent shortages, widening pay-equity mandates, and complex global compliance requirements. Demand concentrates on technology-enabled solutions that blend AI-driven sourcing, data-led decision support, and multi-country regulatory expertise, allowing providers to improve time-to-hire and candidate quality. Competitive fragmentation creates room for niche specialists, especially in healthcare, cybersecurity, and ESG-oriented hiring. At the same time, integration challenges with legacy HCM suites and narrowing RPO margins in transparent-pay jurisdictions place a premium on providers able to deliver seamless platform connectivity and measurable cost reductions.

Key Report Takeaways

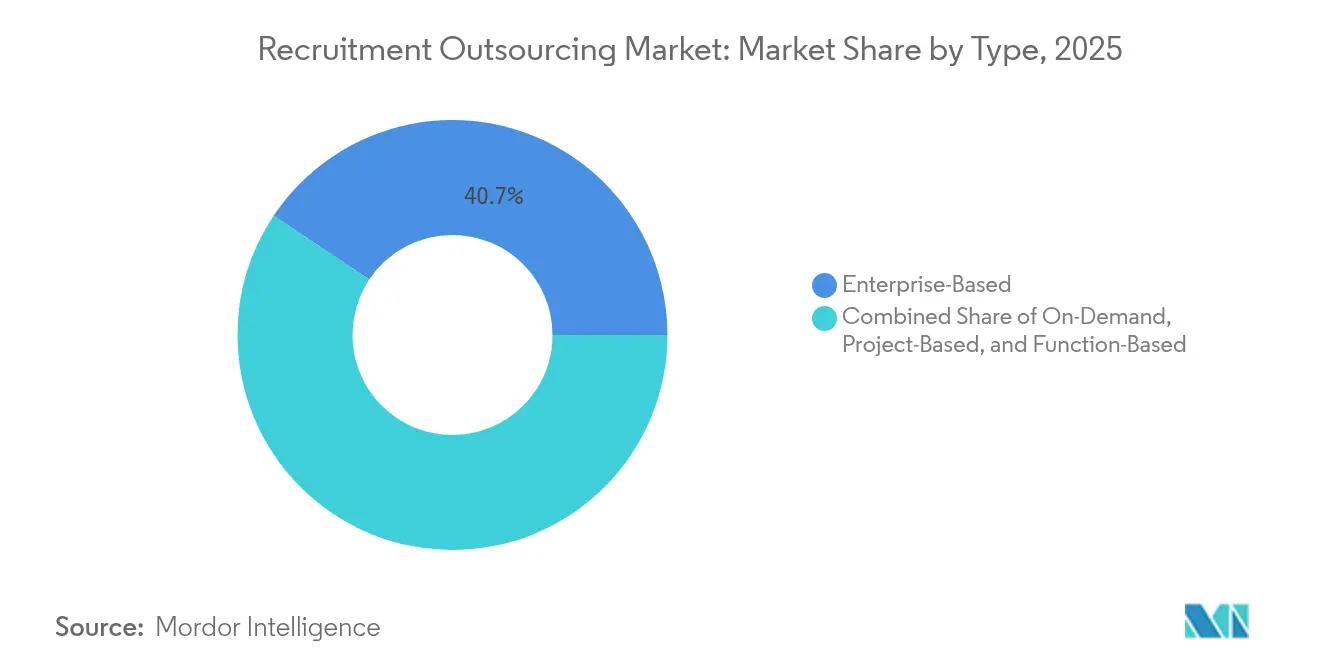

- By type, enterprise-based solutions accounted for 40.65% of the recruitment outsourcing market share in 2025, while project-based engagements are forecast to expand at a 15.34% CAGR through 2031.

- By service delivery mode, off-site models commanded 56.10% of the recruitment outsourcing market size in 2025; hybrid delivery is the fastest-growing approach at 14.92% CAGR.

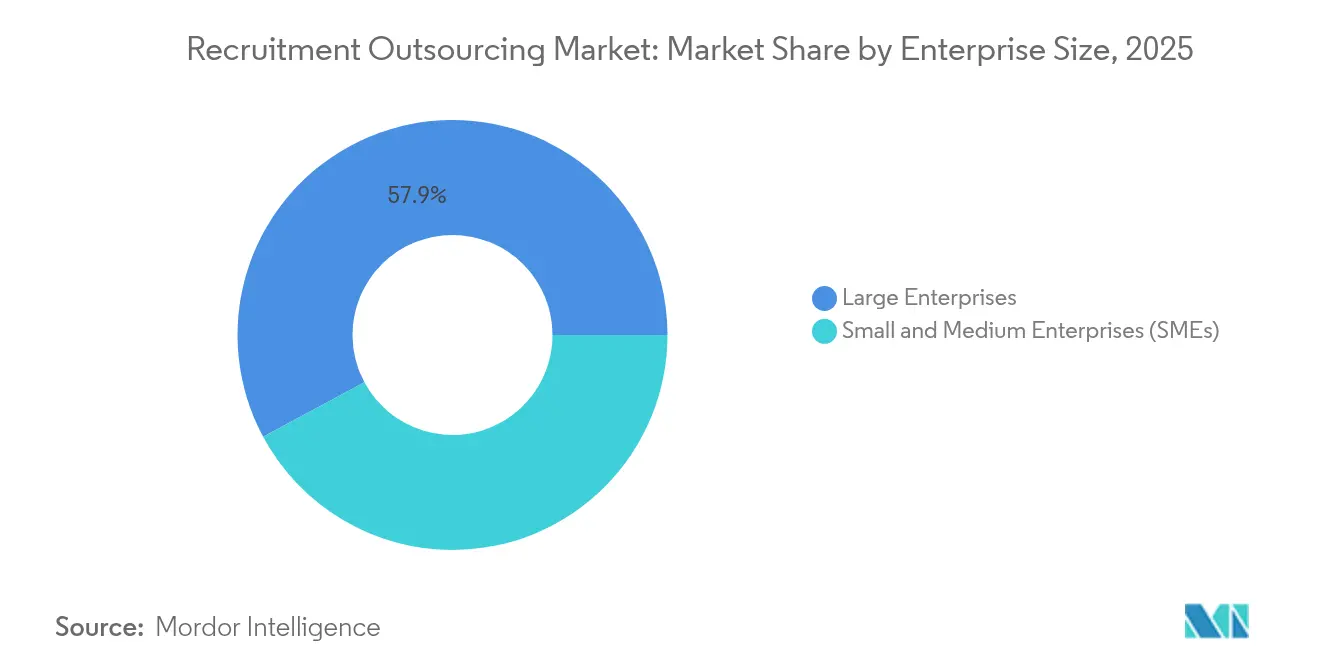

- By enterprise size, large organizations held 57.85% revenue in 2025, whereas SMEs are set to climb at a 14.18% CAGR to 2031.

- By end-user industry, IT and telecom led with 31.05% share of the recruitment outsourcing market size in 2025; retail and e-commerce is poised for 14.88% CAGR growth to 2031.

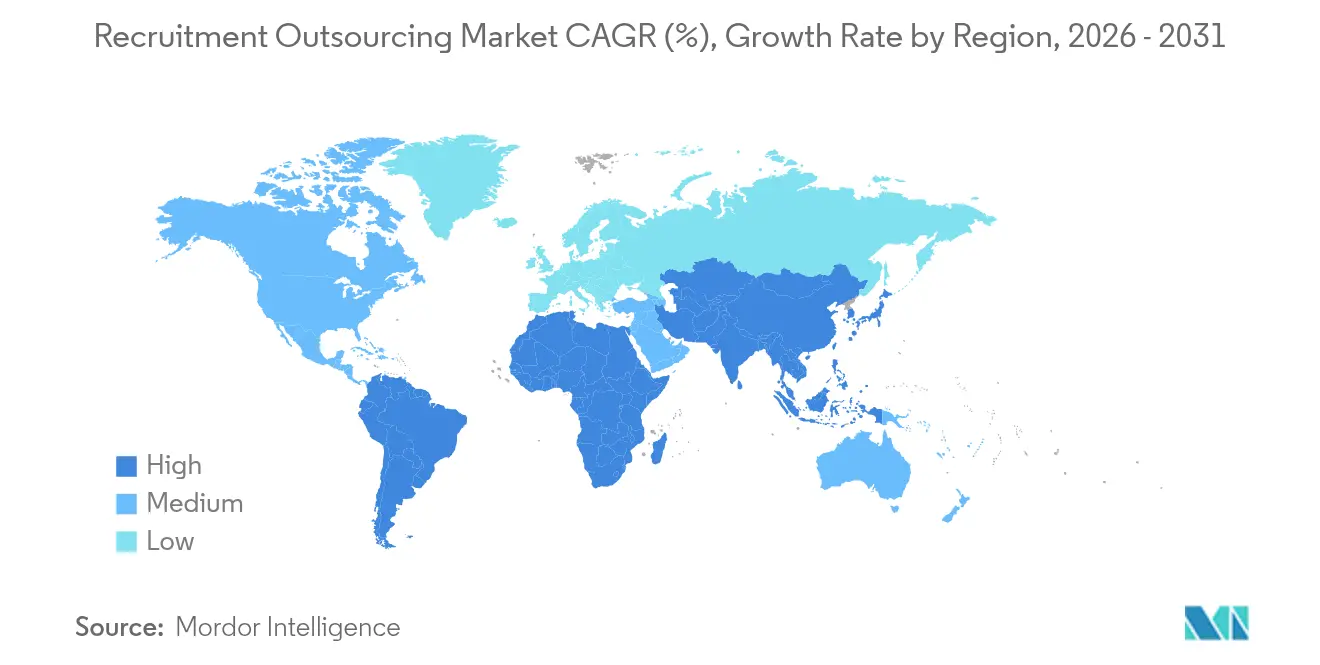

- By geography, North America contributed 37.25% revenue in 2025; Asia-Pacific is projected to record the quickest expansion at 13.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recruitment Outsourcing Market Trends and Insights

Driver Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of AI-driven sourcing tools | +4.2% | Global; early uptake in North America and Europe | Short term (≤ 2 years) |

| Growing multi-country recruitment needs | +3.8% | North America and EU expanding into Asia-Pacific and Latin America | Medium term (2-4 years) |

| Persistent tech and healthcare skills shortages | +5.1% | Global; most acute in North America and Europe | Long term (≥ 4 years) |

| Shift toward variable-cost HR operating models | +3.5% | Global; led by North America and Europe | Medium term (2-4 years) |

| Rise of data-privacy regulations | +2.7% | EU, North America, expanding worldwide | Long term (≥ 4 years) |

| Demand for diversity-focused hiring programs | +2.9% | North America and EU, spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of AI-Driven Sourcing Tools

Cielo launched CLO.ai, the first generative AI built for talent acquisition, combining large-language-model parsing of job descriptions and résumés to speed matching and reduce bias [1]Cielo, “Introducing CLO.ai, the First Generative AI for Talent Acquisition,” cielotalent.com. Always-on engagement, predictive fit scoring, and automated scheduling lift recruiter productivity, yet client satisfaction hinges on balancing algorithms with human judgment. A ManpowerGroup survey reported that 58% of employers believe AI will create net new jobs, underlining the need for hybrid human-AI workflows. Providers that fold AI into screening, chatbot communication, and analytics while preserving recruiter oversight gain a sustainable advantage.

Growing Multi-Country Recruitment Needs from Global Expansion

Seventy-two percent of executives plan international hiring to close skill gaps, forcing RPO partners to master compliance across tax, labor, and data-privacy regimes while maintaining speed-to-hire . São Paulo alone supports 500,000 software developers and feeds a USD 27.79 billion technology market by 2028, illustrating the scale of cross-border opportunity. Providers that bundle legal advisory, multijurisdictional payroll, and localized sourcing shorten market-entry timelines and de-risk expansion efforts.

Persistent Skills Shortages in Tech and Healthcare Verticals

Hospitals confront credentials-heavy vacancies, driving RPO demand for specialty pipelines, university partnerships, and competency-based hiring. In technology, passive-candidate engagement and community stewardship differentiate providers able to fill AI, cybersecurity, and cloud roles quickly. Scarcity allows RPO partners to command premium fees when they lower time-to-productivity and improve retention in business-critical positions.

Shift Toward Variable-Cost HR Operating Models

Volatile economic cycles push employers to convert fixed recruiting overhead into elastic capacity. Variable-cost models enable scale-up during growth sprints and controlled roll-back in downturns, while offering immediate access to analytics platforms and deep talent databases. Proof points such as cost-per-hire reduction and quality-of-hire uplift position RPO providers as strategic enablers rather than transactional vendors, accelerating contract renewals and expansion.

Restraint Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy HCM suites | -2.8% | Global; most acute in large enterprises | Short term (≤ 2 years) |

| In-house talent acquisition centers of excellence | -1.9% | North America and Europe, rising in APAC | Medium term (2-4 years) |

| Heightened data-security concerns | -2.1% | Global; stringent in EU and regulated industries | Long term (≥ 4 years) |

| Margin pressure from pay-transparency laws | -1.6% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy HCM Suites

Enterprises running multiple HR systems face inconsistent coding, data corruption risks, and cumbersome reporting when overlaying an RPO partner. RSM US LLP notes that requirement gathering alone can take three to six months, with total integration exceeding a year for multifaceted environments [2]RSM US LLP, “Integrating HR Systems During M&A,” rsmus.com. When successful, automated workflows and synchronized data improve recruiter efficiency and analytics integrity, but providers without pre-built connectors or change-management playbooks struggle to scale.

In-House Talent Acquisition Centers of Excellence

Large companies invest in centralized recruiting hubs to conserve institutional knowledge and preserve employer branding. These centers leverage shared services cost structures yet often lack the external reach, niche talent pools, and cutting-edge technology an RPO can provide. Winning providers now position their offerings as overflow or specialized extensions, supplying hard-to-find skills, regional expertise, or compliance coverage that internal teams cannot replicate at competitive cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Project-Based Models Drive Flexibility Revolution

Project-based engagements are expanding at a 15.34% CAGR, eroding the dominance of enterprise-wide contracts that owned 40.65% recruitment outsourcing market share in 2025. Outcome-based scopes appeal to employers needing surge hiring for seasonal ramps or specialized talent clusters without locking into multi-year terms. The recruitment outsourcing market benefits as buyers use pilot projects to rate provider performance before broader rollout. Enterprise-based partnerships still underpin long-term cost optimization for organizations with steady demand across many sites. Function-specific offerings—for example, outsourcing only executive search or technical screening—attract mid-market firms wanting targeted expertise without full-process change. Competitive advantage therefore rests on modular service design, transparent SLAs, and flexible pricing, allowing vendors to address varied buyer appetites while deepening wallet share.

Providers able to switch seamlessly from project to enterprise scopes protect client continuity and secure upsell revenue. They standardize playbooks, deploy AI-assisted sourcing, and maintain on-demand recruiter benches, permitting fast mobilization regardless of contract size. By linking fees to metrics such as time-to-fill and quality-of-hire, they align incentives with client outcomes, reinforcing the value of the recruitment outsourcing market. Those lacking scale in specialized domains, however, risk commoditization as buyers weigh vendors on price and measurable output.

By Service Delivery Mode: Hybrid Approaches Reshape Engagement Models

Off-site delivery controlled 56.10% of the recruitment outsourcing market size in 2025, but hybrid models are gaining at 14.92% CAGR. Employers discovered during pandemic-era remote work that they can combine local liaison roles with centralized sourcing hubs to lower cost and retain strategic proximity. Under a hybrid construct, on-site resources focus on stakeholder management, workforce planning, and cultural alignment, while off-site teams handle high-volume sourcing, screening, and administrative workflows. This balance preserves institutional insight without sacrificing the labor-arbitrage economics the recruitment outsourcing market offers.

Providers that unify these distributed teams through collaboration platforms and shared analytics achieve stronger candidate pipelines and consistent employer branding. They standardize virtual assessment centers, video interviewing, and chatbot pre-screening to accelerate cycle times. Off-site-only contracts remain relevant for volume programs in lower-margin sectors, yet buyers increasingly prefer engagement blueprints that adjust recruiter presence as hiring intensity fluctuates. Consequently, differentiation shifts toward service-design agility and the ability to integrate omni-channel candidate touchpoints seamlessly.

By Enterprise Size: SME Adoption Accelerates Digital Transformation

Large organizations held 57.85% of 2025 revenue, but SMEs are expanding uptake at 14.18% CAGR as they seek enterprise-grade technology without building internal infrastructure. SMEs rely on cloud-based applicant-tracking systems, AI matching, and pay-per-hire pricing to compete for scarce talent. Providers package tiered services, enabling smaller companies to scale up or down as funding cycles shift. In parallel, the recruitment outsourcing market size contribution from global majors remains significant because complex multinational programs demand extensive compliance, integration, and analytics.

Dual-segment positioning lets vendors cross-subsidize innovation. Economies of scale achieved with Fortune-level clients finance platform upgrades that later trickle to smaller customers. SMEs benefit through faster time-to-value and reduced overhead, while providers capture a diversified revenue mix resistant to single-client volatility. Competitive pressure will intensify as productized, self-service RPO portals emerge, letting entrepreneurs launch campaigns with minimal onboarding friction.

By End-User Industry: Retail Transformation Drives Outsourcing Acceleration

IT and telecom commanded 31.05% share of the recruitment outsourcing market size in 2025, reflecting chronic shortages in AI, cybersecurity, and cloud skills. Retail and e-commerce, however, will post the highest 14.88% CAGR through 2031 as omnichannel strategies, logistics digitization, and seasonal peaks strain internal teams. Providers that master high-volume frontline hiring, last-mile scheduling, and shopper-experience roles capture rapid wallet share.

Healthcare and life sciences adopt RPO for credential-heavy positions, seeking shorter vacancy durations without compromising compliance. Manufacturing and BFSI sectors follow, outsourcing specialist technical recruitment to accelerate Industry 4.0 and fintech rollouts. Energy and utilities, propelled by renewables expansion, emerge as a nascent vertical for providers versed in ESG reporting and skilled-trades sourcing. Diversification across industries helps vendors stabilize revenue and shields them from cyclic downturns in any single sector, underscoring the broad opportunity within the recruitment outsourcing market.

Geography Analysis

North America maintained 37.25% revenue in 2025, buoyed by twelve state pay-transparency laws that compel employers to publish salary ranges in job postings. Compliance complexity, coupled with intense competition for digital talent, sustains premium demand for AI-enabled, metrics-driven RPO solutions. Providers differentiate through advisory services that interpret evolving legislation and embed wage-equity analytics into hiring workflows. Although margin pressure rises as open pay ranges narrow placement fees, the recruitment outsourcing market continues to expand as firms recognize the cost of non-compliance.

Asia-Pacific is forecast to lead growth at 13.21% CAGR to 2031. India anchors regional momentum, with 81% of local companies planning to enlarge the outsourcing scope. Access to vast English-speaking engineering talent, time-zone advantage, and supportive government policies make the region attractive for global delivery centers. China’s focus on high-end manufacturing and AI, along with Southeast Asia’s maturing digital ecosystem, compounds demand for cross-border recruitment capability.

Europe registers steady progress under the EU Pay Transparency Directive, which obliges employers to reveal pay bands and close a 13% gender wage gap . RPO partners that provide pan-European compliance playbooks and multilingual sourcing widen market share. Latin America advances on nearshoring trends; proximity to North America, growing developer communities, and cultural alignment enable cost-effective talent acquisition programs. Together, these dynamics sustain balanced expansion across the recruitment outsourcing market.

Competitive Landscape

The market remains fragmented. ManpowerGroup generated USD 17.9 billion in revenue in 2024, leveraging global delivery centers and analytics dashboards to streamline volume hiring. Korn Ferry reported USD 84.7 million in RPO income for Q3 FY 2025, bolstered by consultative leadership assessment layered onto recruitment contracts HeadFirst’s USD 632 million purchase of Impellam Group consolidated spend under management exceeding USD 9.1 billion, signaling an acceleration in scale-building acquisitions.

Technology integration now defines differentiation. Adecco Group’s AI workforce platform, built with Salesforce, uses agent orchestration to match candidates, schedule interviews, and forecast workforce needs, illustrating the shift toward AI-centric operating models. Niche disruptors deploy API-first engines and large action models to automate résumé parsing, outreach, and compliance checks, enabling transparent pay-for-performance pricing. Providers that demonstrate cost-per-hire savings of 50% and recruiter productivity gains above 35% while preserving human oversight advance fastest within the recruitment outsourcing market. Conversely, firms lacking modern tech stacks or industry-specific insight risk relegation to subcontract status on larger programs.

Recruitment Outsourcing Industry Leaders

Randstad N.V.

Alexander Mann Solutions

Cielo, Inc.

Allegis Global Solutions

Talent Solutions RPO (ManpowerGroup)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Remote introduced Recruit, a global talent intelligence and compliant offer solution enabling one-click hiring worldwide.

- March 2025: Adecco Group and Salesforce launched an AI-powered workforce management platform that merges human and artificial agents for strategic planning.

- February 2025: Persol invested in Indian platform Vahan, expanding technology-enabled recruitment reach in high-growth APAC markets.

- September 2024: SGF Global acquired Adecco Uruguay to enhance nearshore delivery capabilities in Latin America.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the recruitment outsourcing market as all third-party contracts in which an employer transfers some or all permanent-hire recruiting activities, sourcing, screening, interviewing, onboarding, and analytics, to a specialist provider in order to gain cost, speed, and quality advantages.

Engagements covering only temporary staffing or stand-alone payroll processing are outside our scope.

Segmentation Overview

- By Type

- On-Demand

- Project-Based

- Function-Based

- Enterprise-Based

- By Service Delivery Mode

- On-Site

- Off-Site

- Hybrid

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Energy and Utilities

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with HR executives, procurement heads, and service-provider solution leaders across North America, Europe, Asia-Pacific, and the Middle East. These dialogues test secondary assumptions, surface region-specific cost drivers, and calibrate average contract sizes, onboarding cycle times, and technology adoption levels.

Desk Research

We start with structured reviews of publicly available data from authorities such as the U.S. Bureau of Labor Statistics, Eurostat, and national labor ministries, which reveal hiring volumes, vacancy rates, and wage movements. Trade associations like the Staffing Industry Analysts, the Recruitment Process Outsourcing Association, and the Society for Human Resource Management help our team understand program adoption trends. Company filings, investor decks, reputable business press, and academic journals enrich the evidence base. Paid datasets, including D&B Hoovers for employer counts and Dow Jones Factiva for deal news, support competitor benchmarking. The sources cited here are illustrative; many additional publications are examined to collect, validate, and clarify figures.

Market-Sizing & Forecasting

We anchor the 2025 baseline by reconciling a top-down hiring pool reconstruction, built from full-time vacancy creation, replacement rates, and outsourcing penetration, against sampled bottom-up checks that multiply average selling price by disclosed contract volumes for major providers. Key variables feeding the model include global professional hiring volumes, unemployment rates, enterprise HR tech spending, average time to hire, data privacy regulation counts, and RPO technology utilization rates. Gaps appearing in bottom-up samples are adjusted through weighted interpolation before the totals are finalized. Forecasts to 2030 rely on a multivariate regression that links RPO penetration to the above drivers plus GDP growth, producing scenario bands that our experts refine after stress testing against client feedback.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, anomaly checks against external labor indices, and variance reconciliation with prior editions. Reports refresh annually; significant regulatory or macro events trigger interim updates, and every delivery is preceded by a last-minute data sweep to keep clients current.

Why Our Recruitment Outsourcing Baseline Commands Reliability

Published estimates often diverge because firms choose different service mixes, geographic splits, and refresh cadences.

Readers therefore encounter numbers that look inconsistent at first glance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.87 B (2025) | Mordor Intelligence | |

| USD 10.3 B (2024) | Regional Consultancy A | Uses narrower geographic scope and omits project-based RPO engagements |

| USD 8.53 B (2023) | Global Consultancy B | Relies on historic ASPs without adjusting for post-pandemic wage inflation |

In sum, Mordor's disciplined mix of verified labor statistics, practitioner insight, and annually refreshed models yields a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the recruitment outsourcing market?

The recruitment outsourcing market size is USD 14.43 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 21.58% CAGR, hitting USD 38.29 billion by 2031.

Which engagement model is gaining momentum?

Project-based RPO, growing at a 15.34% CAGR, is outpacing traditional enterprise contracts.

Why is Asia-Pacific considered the fastest-growing region?

Cost-efficient talent pools, digital-transformation initiatives, and 81% of Indian firms boosting outsourcing plans underpin a 13.21% regional CAGR.

How are AI tools influencing recruitment outsourcing?

Platforms such as CLO.ai automate candidate matching, enhance 24/7 engagement, and cut manual screening, giving providers measurable productivity gains.

What challenges could slow market growth?

Complex integration with legacy HCM suites and lower fee margins tied to pay-transparency rules may dampen provider profitability, though they also spur demand for compliant, tech-enabled solutions.

Page last updated on: