Internal Talent Marketplace Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

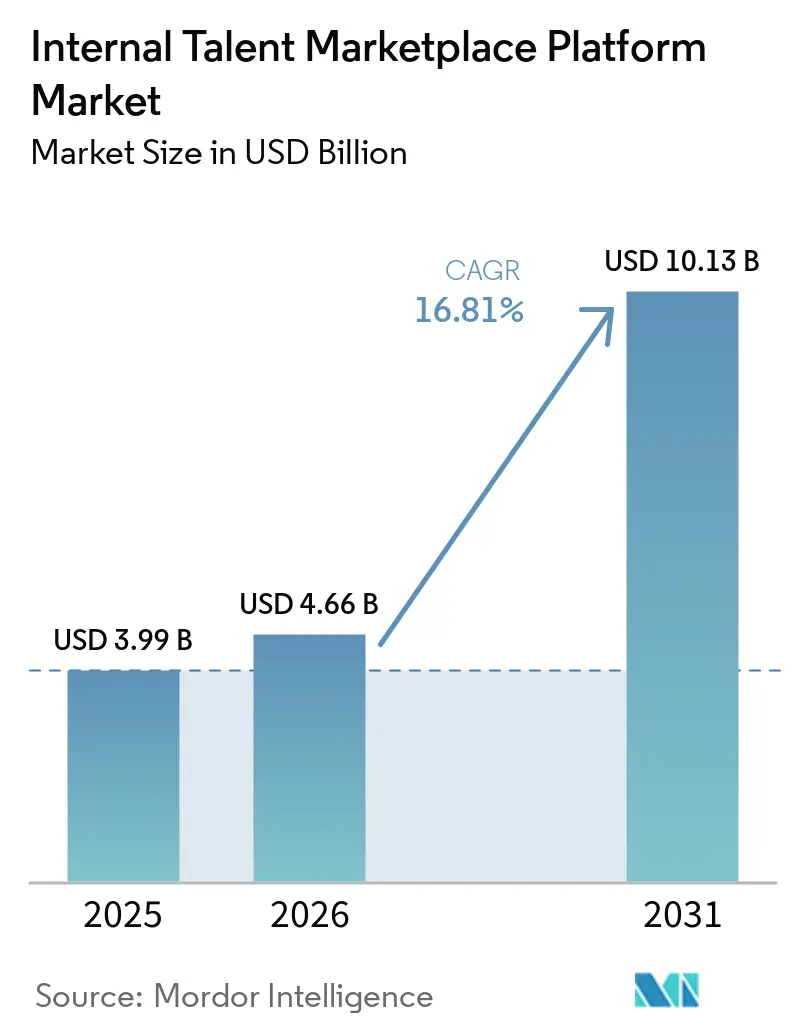

| Market Size (2026) | USD 4.66 Billion |

| Market Size (2031) | USD 10.13 Billion |

| Growth Rate (2026 - 2031) | 16.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internal Talent Marketplace Platform Market Analysis by Mordor Intelligence

The internal talent marketplace platform market size is expected to increase from USD 3.99 billion in 2025 to USD 4.66 billion in 2026 and reach USD 10.13 billion by 2031, growing at a CAGR of 16.81% over 2026-2031. Skills-based operating models, accelerating adoption of generative AI for competency inference, and rising pressure on finance leaders to cut external recruiting costs are converting the internal marketplace from a human-resources experiment into an enterprise-wide optimization lever. Global organizations are embedding opportunity discovery into everyday collaboration channels, allowing employees to match to stretch roles in real time, while finance and operations teams use marketplace analytics to forecast capacity under multiple growth scenarios. Vendor consolidation is under way as suite providers buy best-of-breed specialists to defend installed bases, yet independent platforms continue to differentiate through faster release cadences, deeper AI explainability, and niche vertical workflows. Meanwhile, regional regulations such as the EU AI Act and New York City’s Local Law 144 are forcing suppliers to hard-wire audit trails and bias-mitigation controls, raising the compliance bar for new entrants.

Key Report Takeaways

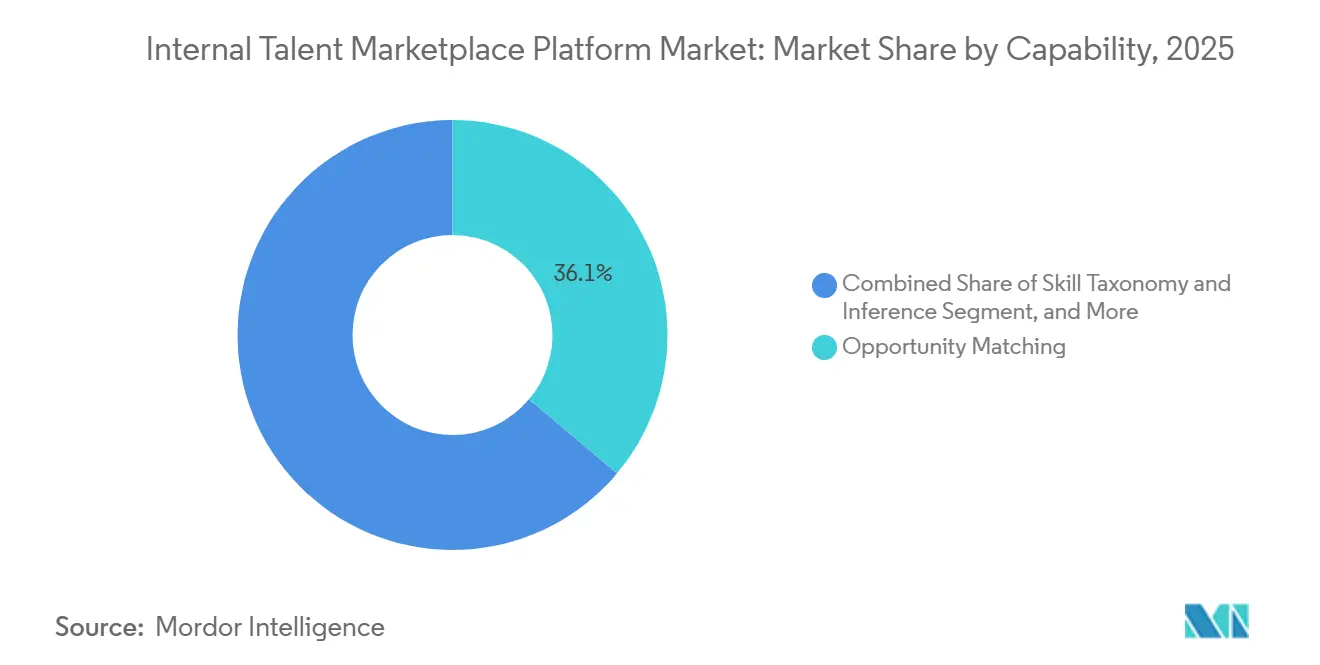

- By capability, opportunity matching led with 36.12% of the internal talent marketplace platform market share in 2025, while skill taxonomy and inference engines are projected to expand at an 18.71% CAGR through 2031.

- By delivery model, integrated HR suite modules accounted for 56.44% of 2025 deployments, whereas standalone platforms are advancing at a 19.04% CAGR to 2031.

- By deployment mode, on-premises installations represented 61.78% of the 2025 installed base, yet cloud variants are rising at 19.88% as elastic infrastructure becomes essential for AI workloads.

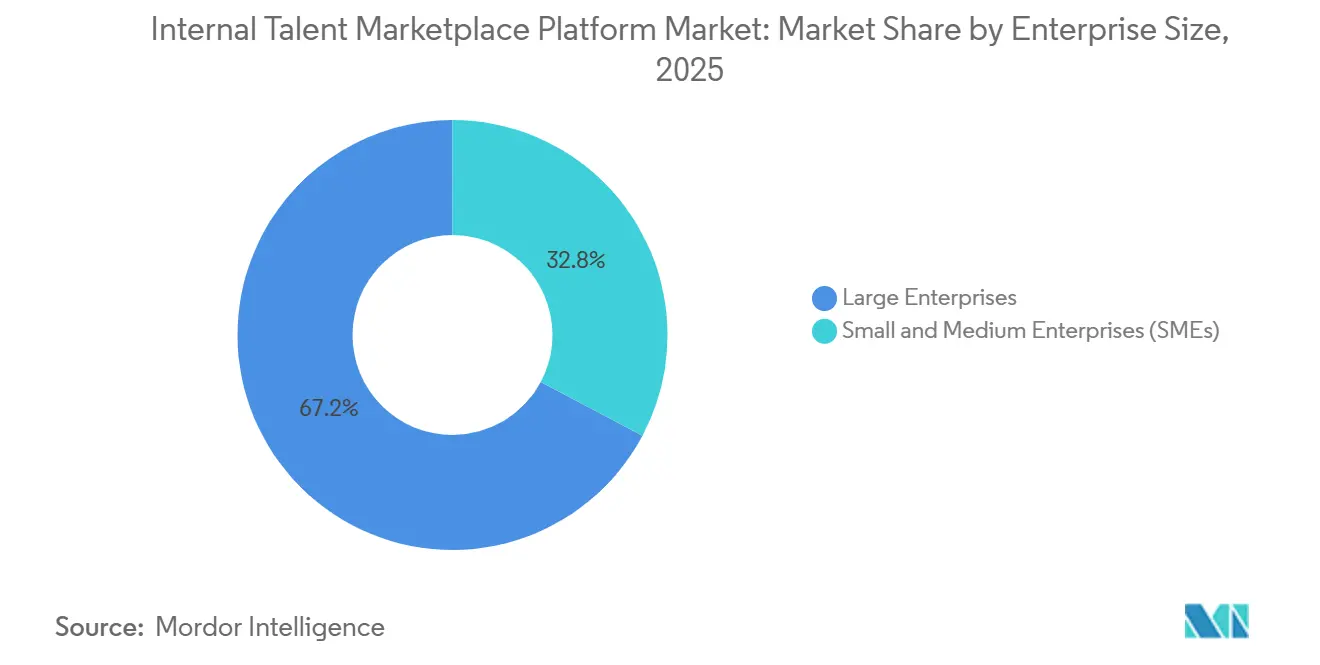

- By enterprise size, large organizations captured 67.23% of 2025 spending, but small and medium enterprises are scaling adoption at a 19.54% CAGR by leapfrogging legacy HRIS constraints.

- By industry vertical, IT and telecommunications commanded 28.56% of 2025 revenue, yet healthcare is forecast to grow at 17.94% as hospitals redeploy scarce clinical talent to reduce agency spend.

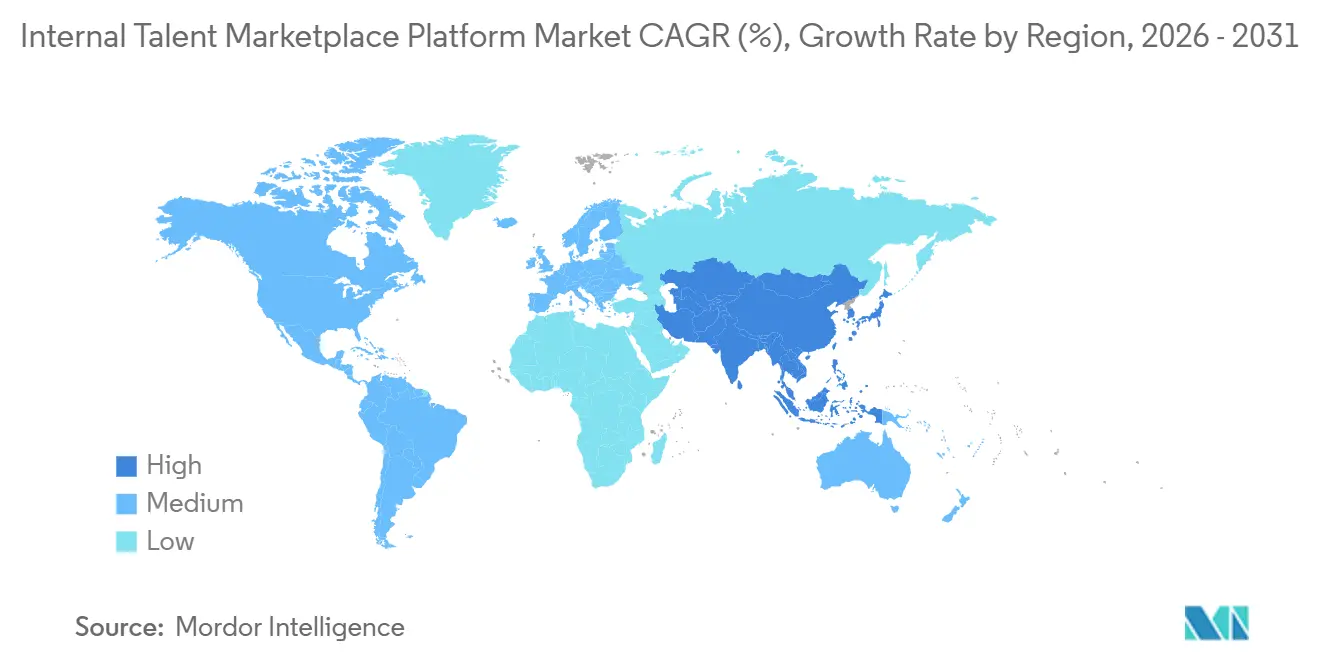

- By geography, North America held 37.21% of 2025 revenue, while Asia-Pacific is set to grow at 18.45% through 2031 on the back of rapid cloud uptake and skills-localization mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Internal Talent Marketplace Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills-Based Workforce Planning | +4.2% | Global, early in North America and Europe | Long term (≥ 4 years) |

| Employee Demand for Agile Career Paths | +3.8% | North America, Europe, Asia-Pacific cities | Medium term (2-4 years) |

| Generative AI Skill Inference | +3.5% | Global, led by tech hubs | Medium term (2-4 years) |

| Recruiting Cost Reduction Pressure | +2.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Diversity, Equity and Inclusion Focus | +1.6% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Remote and Hybrid Work Expansion | +1.0% | Global knowledge sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skills-Based Workforce Planning

Organizations are dismantling rigid job architectures in favor of fluid talent pools that allocate work according to verified competencies, shortening reaction times when priorities shift. Internal talent marketplace platform market deployments automate skills validation with project outcomes, peer endorsements, and course completions, creating a living inventory of enterprise capabilities that finance and strategy teams can model alongside capital budgets. The World Economic Forum projects that 39% of core skills will change by 2030, amplifying the urgency of continuous reskilling. Platforms that weave learning paths into opportunity suggestions ensure workers close gaps without leaving the ecosystem, linking development directly to value creation.

Employee Demand for Agile Career Paths

Transparent internal mobility is becoming a decisive factor in retention, especially among early-career professionals who expect consumer-grade recommendation engines to surface stretch assignments. Engagement metrics from large deployments show triple-digit growth in internal applications once algorithmic matching replaces static job boards. Employees stay longer because marketplace analytics illuminate multiple progression routes, even across functions, giving them reasons to build cross-domain portfolios instead of seeking advancement elsewhere. Retailers, logistics providers, and hospitality chains that experience demand spikes use the same mechanics to redeploy seasonal labor, smoothing workforce utilization without mass hiring.

Generative AI Skill Inference

Large language models embedded in the internal talent marketplace platform market scrape meeting transcripts, code repositories, and customer tickets to infer transferable skills that workers may not self-identify. Workday’s March 2026 Sana AI Agent lets employees ask about their cybersecurity background and receive a ranked list of roles plus curated upskilling content.[1]Workday, “Workday Launches Sana AI Agent Platform,” blog.workday.com Such conversational interfaces remove the need to master system taxonomies, widening adoption beyond digital natives. The models also reconcile synonym divergence across regions, mapping Vue.js in one unit to front-end JavaScript frameworks in another, thereby unlocking cross-border mobility that was previously blocked by vocabulary silos.

Recruiting Cost Reduction Pressure

Finance teams facing margin compression are shifting spend from external agencies to technology that fills vacancies internally. Case studies report double-digit drops in time-to-fill along with multimillion-dollar savings; Mastercard avoided USD 21 million by sourcing roles through its marketplace. Savings resonate in sectors with high turnover, where agency fees can equal 15-20% of salary and first-year failure rates for external hires are materially higher than for internal moves. The ability to quantify avoided costs converts the marketplace from an HR discretionary item into a line-item efficiency lever.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy HRIS Integration Challenges | -2.1% | Global, acute with on-prem SAP and Oracle | Medium term (2-4 years) |

| Data Privacy and Security Concerns | -1.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Managerial Resistance to Talent Mobility | -1.3% | Global, heightened in hierarchical cultures | Short term (≤ 2 years) |

| Ambiguous Enterprise Skill Taxonomies | -0.9% | Global conglomerates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy HRIS Integration Challenges

Many corporations still run core HR on batch-oriented systems that were never designed for real-time skill updates, forcing marketplace vendors to rely on flat-file transfers that create latency and data-quality gaps. Enterprises locked into on-premises SAP or Oracle must decide whether to endure suboptimal user experiences or fund costly middleware projects. Workday’s acquisition of Sana embeds marketplace functions natively within its cloud suite, sidestepping integration friction for customers already on its platform, but organizations tied to other HR stacks face longer project timelines and diluted ROI.

Data Privacy and Security Concerns

Marketplaces aggregate sensitive performance ratings, compensation bands, and career aspirations. The EU AI Act categorizes automated HR decision systems as high-risk, mandating conformity assessments, documentation, and human oversight. New York City’s Local Law 144 requires annual bias audits, and similar bills are surfacing in other jurisdictions. Vendors unable to prove encryption, role-based access, and comprehensive audit trails risk disqualification, particularly in banking and healthcare where regulators scrutinize workforce data flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capability: Inference Engines Outpace Posting Boards

Skill inference engines, a subset of the internal talent marketplace platform market, are set to grow at an 18.71% CAGR through 2031 as employers learn that match quality hinges on ontology richness rather than volume of listings. While opportunity matching accounted for 36.12% of the internal talent marketplace platform market size in 2025, feature parity is narrowing and differentiation is shifting to engines that detect emerging skills from unstructured artifacts. Generative AI reduces time spent curating profiles and surfaces adjacent capabilities, allowing finance teams to redeploy staff into growth programs without external hires. Learning-integration modules follow closely, linking upskilling directly to open roles so workers can bridge gaps in real time. Workforce-planning analytics appeal to operations leaders who need to scenario-plan capacity, making these add-ons a logical upsell path for vendors.

Second-tier functions, including succession planning and alumni networks, remain niche yet demonstrate strategic potential as organizations look beyond active employees to retired specialists and boomerang hires. Conversational interfaces launched in 2026 compress search friction by answering plain-English queries, a design choice that is lifting adoption among non-technical staff. The EU AI Act’s transparency mandate slows rollouts in some European multinationals because exposed reasoning chains require additional validation, but the same auditability features, once certified, become competitive differentiators when bidding for regulated clients.

By Delivery Model: Standalone Platforms Gain as Suite Fatigue Sets In

Integrated modules within broad HR suites held 56.44% of revenue in 2025 thanks to incumbent relationships and uniform data models. Yet the internal talent marketplace platform market is witnessing a 19.04% CAGR for best-of-breed vendors that deliver shorter implementation cycles and avoid vendor lock-in. Procurement teams value the ability to negotiate shorter contracts and swap components without disrupting the HR core. Suite providers, recognizing the gap, are buying specialists to accelerate road maps, evident in Workday’s USD 1.10 billion Sana purchase.

Organizations with lean IT teams still gravitate toward modules that run on their existing suite, but growing dissatisfaction with quarterly upgrade windows is pushing even risk-averse buyers toward API-first specialists. Mid-market firms, in particular, prize the 8- to 12-week deployment promise that standalone vendors present, allowing pilots to prove ROI before an enterprise-wide roll-out. Over the forecast horizon, hybrid approaches, where a specialist handles matching while the suite manages compliance workflows, are likely to become mainstream.

By Deployment Mode: Cloud Ascends as AI Workloads Demand Elasticity

Cloud instances of the internal talent marketplace platform market are advancing at 19.88% through 2031, eclipsing growth in on-premise pools that still accounted for 61.78% of installed sites in 2025. Real-time inference runs best on elastic compute, and regional data centers now satisfy residency rules for governments and banks that once mandated on-prem hardware. Audit obligations under the EU AI Act, which require event-level logging of recommendations, further incentivize cloud because storage scaling is automatic.

Early adopters show productivity spikes; Schneider Electric’s cloud marketplace processes 10,000 skill inferences each day and logged USD 15 million savings in its first year.[2]Gloat, “Schneider Electric Case Study,” gloat.com Small and medium enterprises benefit disproportionately, bypassing capital expense entirely, while larger multinationals pursue hybrid setups to keep sensitive comp data behind the firewall. Although hybrid reduces some latency, it introduces orchestration complexity that only organizations with mature DevOps teams can manage.

By Enterprise Size: SMEs Leapfrog as SaaS Lowers Barriers

Small and medium enterprises, representing a minor share today, are forecast to increase their spend at a 19.54% CAGR, narrowing the gap with large enterprises that held 67.23% of the internal talent marketplace platform market size in 2025. SaaS subscription tiers let a 500-employee consultancy pilot opportunity matching for under USD 50,000 annually, realizing ROI within one budgeting cycle. Flatter org charts ensure minimal resistance from middle management, allowing internal gig rotations to become cultural norms quickly.

Large enterprises, though slower to roll out, still anchor vendor revenues because of scale. Their marketplaces train richer models by ingesting millions of historical project records, leading to precision in cross-functional redeployments. However, change-management overhead is significant; managers hesitate to release top performers, necessitating policy interventions that tie mobility participation to performance metrics. Vendors that supply adoption dashboards and nudging algorithms find receptive audiences among HR business partners tasked with driving usage.

By Industry Vertical: Healthcare Accelerates Amid Workforce Shortages

IT and telecommunications captured 28.56% of 2025 revenue, reflecting early digital affinity, yet the fastest expansion to 2031 comes from healthcare at 17.94%. Hospital systems face nurse shortfalls projected to top 3.2 million by 2026, and talent marketplaces allow real-time redeployment across departments based on patient census, curbing agency spend. Banking and financial services follow as regulators elevate operational-resilience metrics, and manufacturing firms pivot from manual assembly to automated cells requiring reskilled operators.

Retailers leverage the marketplaces to swing staff between stores and e-commerce fulfillment centers during promotional peaks. Government agencies, coping with hiring freezes, are piloting internal mobility to fill policy analyst roles with existing civil servants who possess adjacent competencies. Over time, industry-specific compliance layers, such as patient-privacy controls in healthcare, will drive the emergence of verticalized versions of the internal talent marketplace platform industry.

Geography Analysis

North America maintained 37.21% of internal talent marketplace platform market revenue in 2025, buoyed by a mature vendor ecosystem and regulatory catalysts like Local Law 144, which requires annual bias audits of automated employment decision tools. Adoption is deep among Global 500 enterprises, yet growth is shifting to mid-market organizations and the public sector as large-enterprise penetration approaches the ceiling. Suite vendors headquartered in the region are using M&A to defend share, but independent specialists remain competitive through rapid feature launches focused on AI transparency.

Europe delivers steady, regulation-driven uptake, as GDPR familiarity gives buyers confidence in structured compliance roll-outs. The EU AI Act, finalized in 2025, extends procurement cycles because buyers demand documented explainability before signing multiyear contracts.[3]European Commission, “Regulatory Framework on AI,” digital-strategy.ec.europa.eu Germany and France lead deployments in manufacturing and financial-services organizations that must reskill aging workforces. The internal talent marketplace platform market size in the bloc benefits from pan-European skills alliances, which encourage cross-border talent mobility that marketplaces facilitate.

Asia-Pacific is projected to record the highest CAGR at 18.45% through 2031. India’s IT outsourcers deploy marketplaces to keep attrition-prone engineers engaged on internal gigs between client projects, while China’s state-owned enterprises pilot platforms to align talent redeployment with industrial policy objectives. In Southeast Asia, cloud-native mid-caps adopt marketplaces to plug regional skill shortages without expanding recruiting teams. Gulf Cooperation Council economies, classified here under the broader Asia-Pacific growth narrative due to similar adoption drivers, install specialized platforms that embed localization metrics mandated by Saudisation and Emiratisation policies.

Competitive Landscape

The internal talent marketplace platform market remains moderately fragmented; the top five vendors, Gloat, Eightfold AI, Fuel50, Workday, and SAP, control roughly 40% of revenue. Competition centers on three vectors: depth of AI inference, breadth of pre-built integrations, and vertical workflow customization. Workday’s USD 1.10 billion Sana acquisition embeds conversational AI into its suite, signaling how critical natural-language discovery has become for user adoption.

Gloat counters by partnering with learning providers to deliver one-click transition paths from skill gap to accredited certificate, positioning itself as the orchestration layer that overlays any HRIS. Fuel50 distinguishes itself through career-path visualization that appeals to professional-services firms seeking to retain consultants during bench periods. Eightfold AI invests heavily in explainability, an area gaining purchasing importance in regulated sectors.

Among newer entrants, Resquad AI develops compliance dashboards tuned to Gulf localization mandates, a regional niche global players have yet to fully address. The top five share is expected to rise modestly as consolidation quickens, but vertical and regional specialists will continue to win deals where domain knowledge outweighs scale advantages.

Internal Talent Marketplace Platform Industry Leaders

Workday, Inc.

Oracle Corporation

SAP SE

Gloat Ltd.

Eightfold AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Workday released the Sana AI Agent, adding conversational skill inference and personalized upskilling recommendations directly inside Workday HCM.

- November 2025: Workday closed its USD 1.10 billion purchase of Sana, folding advanced learning-content curation into its talent marketplace module.

- June 2025: Schneider Electric reported that its Gloat-powered Open Talent Market hit 89% adoption and saved USD 15 million by replacing external hires with internal mobility.

- May 2025: The European Commission published final EU AI Act guidelines, classifying automated HR matching as high-risk and mandating transparency measures.

Global Internal Talent Marketplace Platform Market Report Scope

The Internal Talent Marketplace Platform Market match employees to projects, gigs, learning pathways, and internal job opportunities, all based on skills, interests, and organizational demand. By creating a dynamic internal labor market, these platforms enhance workforce mobility, boost talent retention, and facilitate agile staffing. They seamlessly integrate with HRIS and skills frameworks, offering real-time insights into internal capabilities and resourcing needs. The market's expansion is fueled by a transformation towards skills, a push for cost optimization, and a growing preference for flexible, project-based work models.

The Internal Talent Marketplace Platform Market Report is Segmented by Capability (Opportunity Matching, Skill Taxonomy and Inference, Learning and Development Integration, Workforce Planning Analytics, Internal Gigs and Projects Management, and Other Capabilities), Delivery Model (Standalone Internal Talent Marketplace Platforms, and Integrated HR Suite Modules), Deployment Mode (Cloud, and On-Premises), Enterprise Size (Large Enterprises, and Small and Medium Enterprises [SMEs]), Industry Vertical (IT and Telecommunications, Banking Financial Services and Insurance, Healthcare, Manufacturing, Retail and E-Commerce, Government, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Opportunity Matching |

| Skill Taxonomy and Inference |

| Learning and Development Integration |

| Workforce Planning Analytics |

| Internal Gigs and Projects Management |

| Other Capabilities |

| Standalone Internal Talent Marketplace Platforms |

| Integrated HR Suite Modules |

| Cloud |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunications |

| Banking, Financial Services and Insurance |

| Healthcare |

| Manufacturing |

| Retail and E-Commerce |

| Government |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Capability | Opportunity Matching | |

| Skill Taxonomy and Inference | ||

| Learning and Development Integration | ||

| Workforce Planning Analytics | ||

| Internal Gigs and Projects Management | ||

| Other Capabilities | ||

| By Delivery Model | Standalone Internal Talent Marketplace Platforms | |

| Integrated HR Suite Modules | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Industry Vertical | IT and Telecommunications | |

| Banking, Financial Services and Insurance | ||

| Healthcare | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Government | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the internal talent marketplace platform market size through 2031?

The internal talent marketplace platform market size is projected to reach USD 10.13 billion by 2031, expanding at a 16.81% CAGR over 2026-2031 (Mordor Intelligence).

Which capability is growing fastest inside these platforms?

Skill inference engines are advancing at an 18.71% CAGR as employers prioritize ontology quality for accurate matching.

Why are cloud deployments accelerating within talent marketplaces?

Real-time AI workloads require elastic compute and continuous logging, making cloud infrastructure the preferred option, especially under EU AI Act audit obligations.

How do internal marketplaces improve recruiting economics?

Case studies such as Mastercard’s show multimillion-dollar cost avoidance by filling roles internally, slashing agency fees and time-to-fill.

Which region is forecast to record the highest growth?

Asia-Pacific is expected to grow at 18.45% through 2031, driven by rapid cloud adoption and localization mandates in markets like India and the Gulf.

Page last updated on: