Real-World Evidence Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

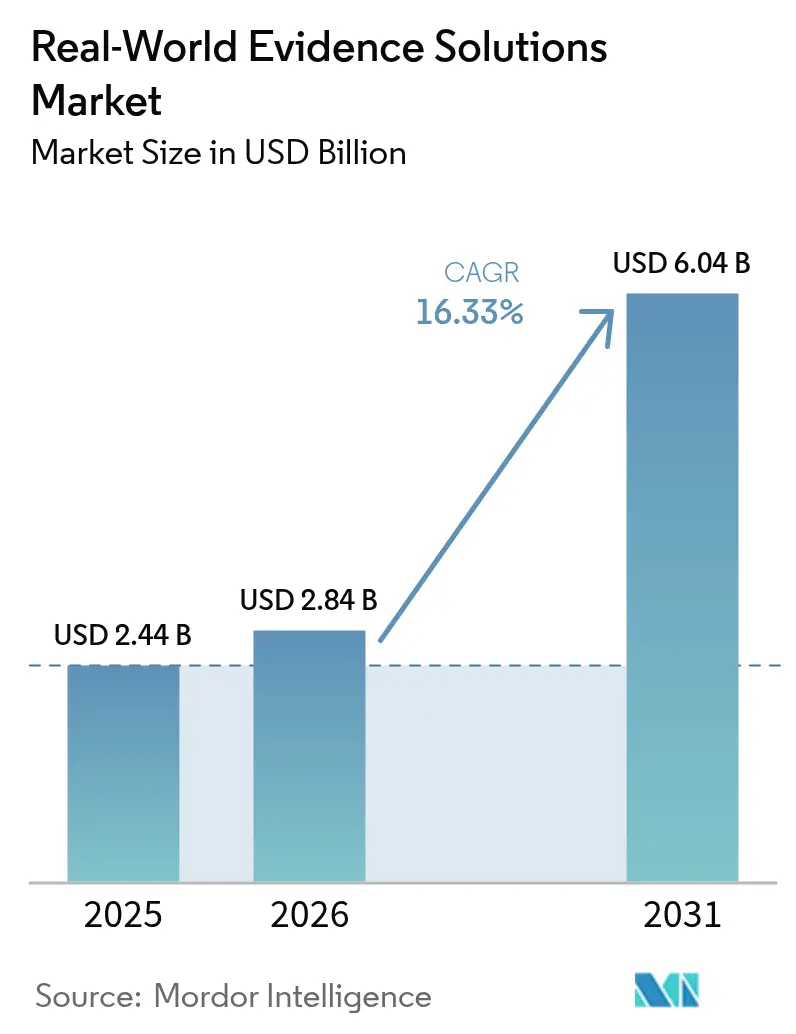

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 6.04 Billion |

| Growth Rate (2026 - 2031) | 16.33% CAGR |

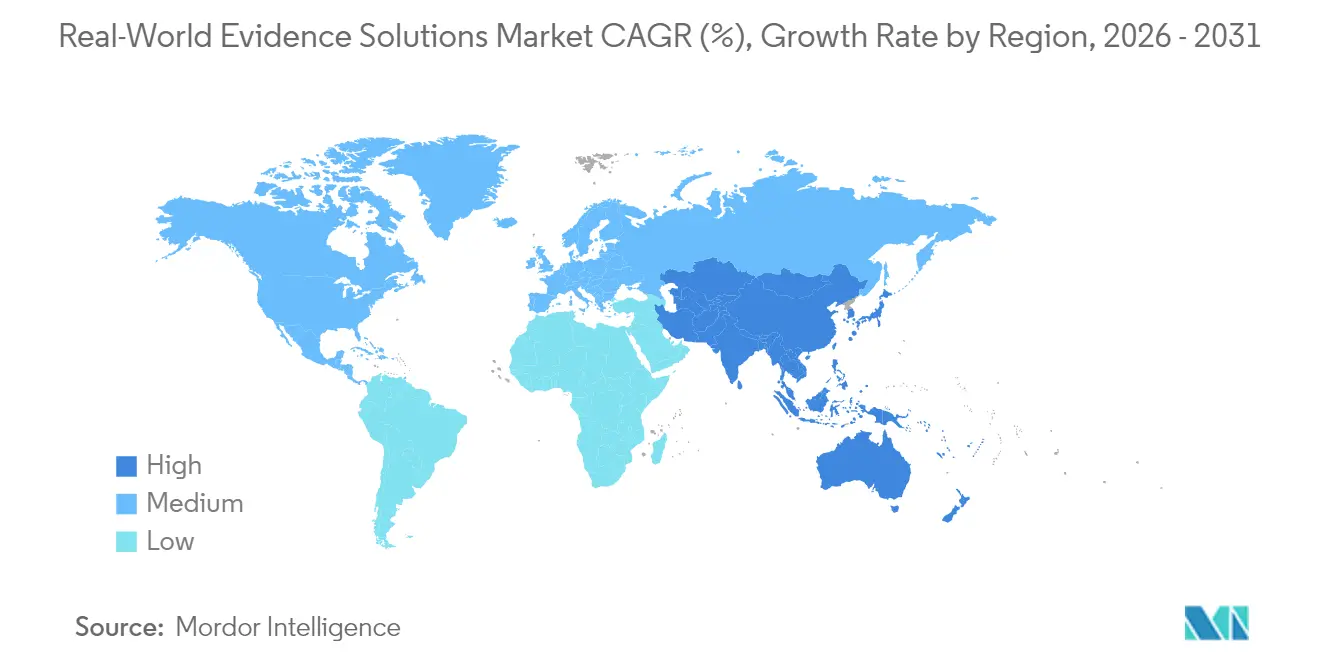

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Real-World Evidence Solutions Market Analysis by Mordor Intelligence

The real-world evidence solutions market size is expected to grow from USD 2.44 billion in 2025 to USD 2.84 billion in 2026 and is forecast to reach USD 6.04 billion by 2031 at 16.33% CAGR over 2026-2031. Digitized clinical, genomic and administrative data sets are expanding at double-digit rates across major healthcare systems, while regulators in the United States, European Union and Japan continue to publish guidance on how sponsors can incorporate non-traditional data into submissions, cutting development timelines without sacrificing scientific rigor[1]Food and Drug Administration, “Framework for Real-World Evidence Program,” fda.gov. Biopharma budgets are tilting toward large, curated patient cohorts that lower recruitment risk, and payers are tying premium pricing to outcomes, forcing manufacturers to adopt analytics that validate real-world effectiveness at launch. Venture capital inflows favor platform companies with scalable cloud architectures, giving them the capital to acquire niche datasets and consolidate share. At the same time, privacy-preserving techniques such as tokenization and federated learning are becoming procurement prerequisites, steering contracts toward vendors with proven security and governance.

Key Report Takeaways

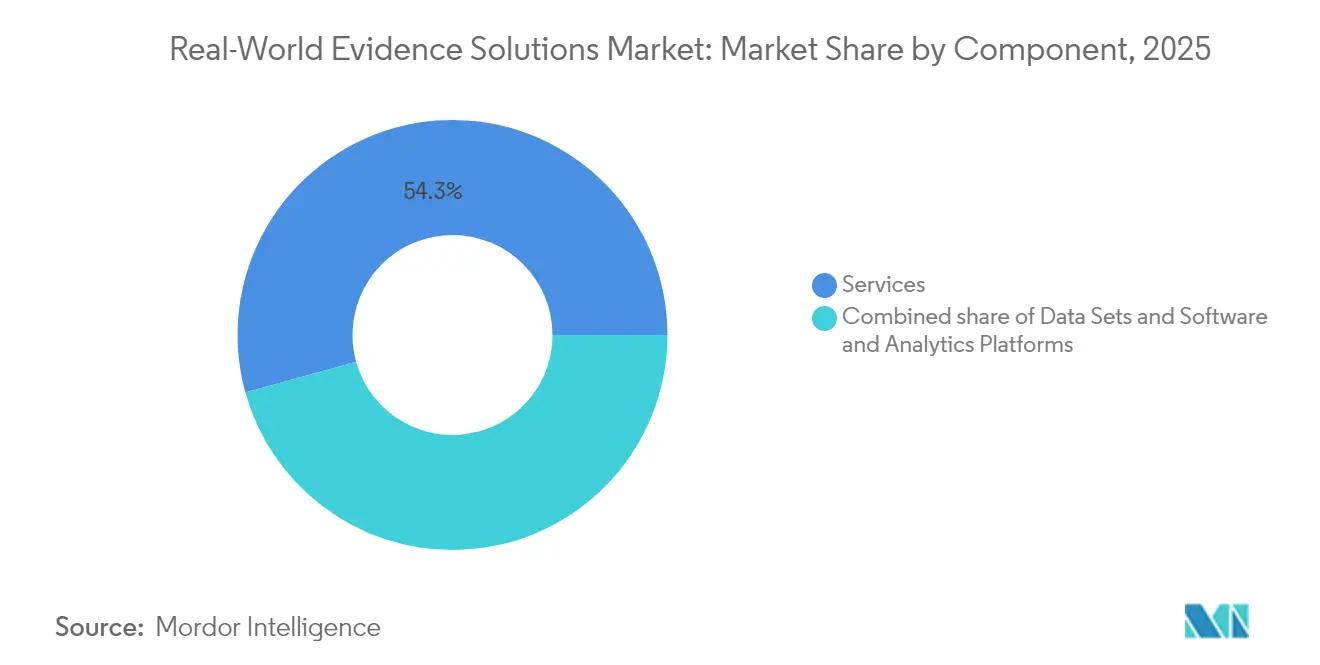

- By component, services led with 54.30% of the real-world evidence solutions market share in 2025, while software & snalytics platforms is advancing at a 17.78% CAGR through 2031.

- By deployment mode, cloud captured 64.35% of the real-world evidence solutions market size in 2025, while hybrid is advancing at a 20.66% CAGR through 2031.

- By therapeutic area, oncology commanded 34.65% of the real-world evidence solutions market share in 2025; neurology is advancing at a 18.72% CAGR through 2031.

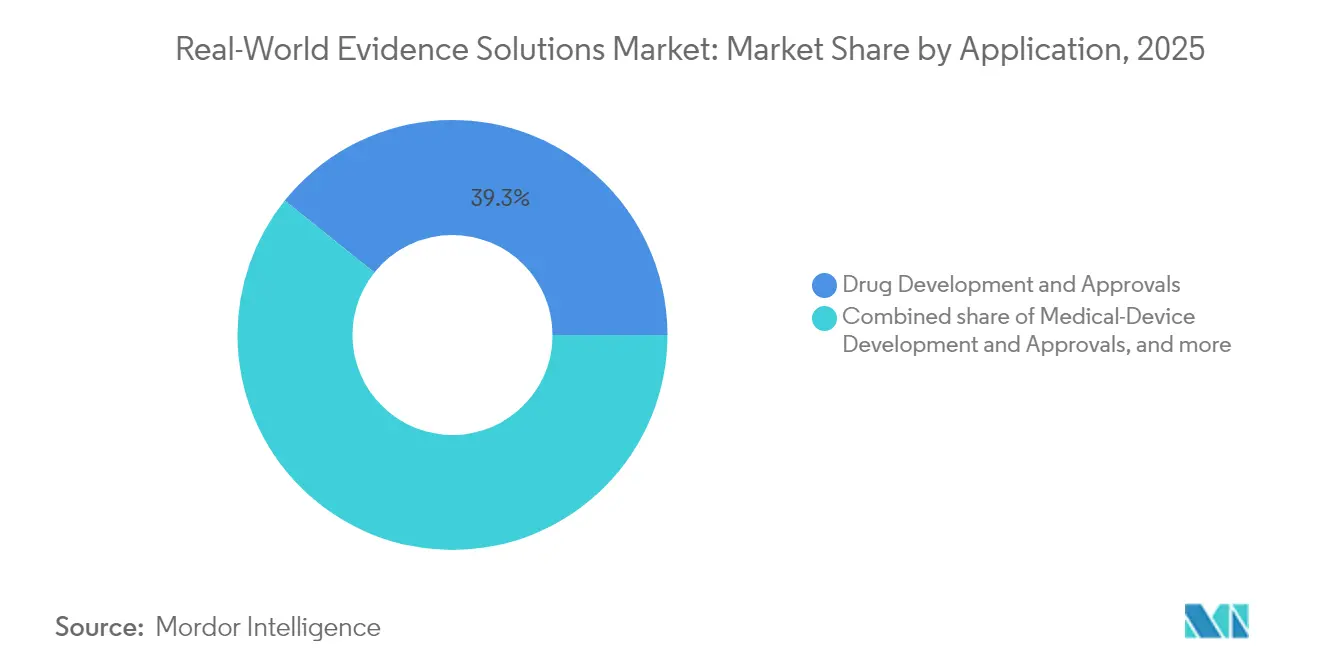

- By application, drug development & approvals accounted for 39.25% of the real-world evidence solutions market size in 2025, while regulatory decision-making & reimbursement is growing at an 17.69% CAGR.

- By end user, pharmaceutical and medical-device companies held 49.20% of the real-world evidence solutions market in 2025.Whereas, healthcare providers & payer-provider networks segment is anticipated to grow at fastest CAGR of 16.82%

- By region, North America led with 40.95% of the real-world evidence solutions market share in 2025, Whereas, Asia- Pacific is anticipated to grow at fastest CAGR of 17.46%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Real-World Evidence Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory acceptance across major agencies | +3% | North America, Europe, Japan | Medium term (2-4 years) |

| Expansion of digitized healthcare data | +4% | Global | Long term (≥ 4 years) |

| Pharmaceutical use of external control arms | +2% | North America, Asia-Pacific | Medium term (2-4 years) |

| Value-based reimbursement models | +3% | North America, Europe | Long term (≥ 4 years) |

| Artificial-intelligence and advanced analytics platforms maturing | +2% | Global | Medium term (2-4 years) |

| Strategic collaborations between CROs, tech vendors, and health systems | +2% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Regulatory Acceptance Across Major Agencies

The U.S. FDA’s Real-World Evidence Framework and corresponding pilot programs have formalized pathways for submitting externally controlled cohorts built from claims and EHR records. The European Medicines Agency mirrors this trend under its Data Analysis and Real-World Interrogation Network, publishing positive qualification opinions for multiple synthetic-arm proposals. Japan’s PMDA followed with its 2024 guidance on real-world data reliability testing[2]Pharmaceuticals and Medical Devices Agency, “Guidance on Reliability of RWD,” pmda.go.jp. Sponsors now embed observational endpoints as early as phase II, reducing uncertainty in pivotal trials. Transparent data lineage has thus shifted from a compliance afterthought to a frontline differentiator, rewarding vendors that deliver audit-ready pipelines and accelerating contract sign-offs among risk-averse biopharma procurement teams.

Rapid Expansion of Digitized Healthcare Data

Electronic health record adoption levels surpassed 89.0% among U.S. non-federal acute-care hospitals in 2024, adding petabytes of structured data to the real-world evidence solutions market. Wearables generate continuous physiologic streams, while next-generation sequencing outputs enrich disease registries with molecular signatures. Multi-modal linkages enable researchers to combine imaging, pharmacy claims and social-determinant indicators, uncovering phenotypes invisible to traditional trials. Yet stricter privacy statutes such as the EU’s GDPR and California’s CPRA are sharpening oversight. Tokenization providers that convert identifiers into non-reversible hashes have become central partners, and federated-learning networks that move code to the data rather than aggregating raw files allow cross-border collaboration without breaching residency rules. Vendors able to harmonize disparate taxonomies under common data models shorten study start-up by months, gaining a measurable edge.

Pharmaceutical Companies Leverage RWE to Curb R&D Timelines and Costs

External control arms built from existing oncology registries trimmed recruitment timelines by up to 25 weeks in several 2024 filings, according to public FDA review memos. Synthetic cohorts lower per-patient monitoring costs, freeing capital to fund additional indication expansions. AI-powered cohort-finding tools—commercialized by firms such as ConcertAI—map inclusion criteria against tens of millions of longitudinal records, slashing screen-fail rates. Observational follow-ups extend asset life-cycle value, supporting label extensions and reinforcing formulary positions. Financial reporting from top-20 pharmas indicates stable cost-of-goods sold yet a double-digit uptick in evidence-generation budgets, validating the market’s growth trajectory.

Value-Based Reimbursement Models Drive Outcomes-Oriented Evidence

U.S. commercial insurers executed more than 90 outcomes-based agreements in 2024, often tying specialty drug rebates to real-world response metrics disclosed via shared dashboards. Europe’s multiple-payer systems replicated this model as agencies in Germany and France added conditional reimbursement clauses contingent on real-world effectiveness. Vendors that integrate economic and clinical metrics into unified portals allow payers to visualize incremental cost-effectiveness ratios (ICERs) by subpopulation, supporting faster negotiation cycles. Health-plan clients now request contract clauses mandating continuous data refreshes, transforming episodic service engagements into recurring subscriptions that stabilize vendor revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and interoperability hurdles | -2% | Global | Medium term (2-4 years) |

| Regulatory fragmentation in cross-border studies | -1% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| High acquisition and licensing costs for curated longitudinal datasets | -1% | Global | Short term (≤ 2 years) |

| Stakeholder skepticism regarding methodological rigor and bias in RWE studies | -1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI and Advanced Analytics Platforms Mature to Extract Actionable Insights

Transformer-based natural language processing models achieved F1 scores above 0.90 on extracting oncology endpoints from unstructured pathology reports in 2024 validation studies, cutting manual abstraction costs by more than 60%. NVIDIA’s DGX H100 clusters, deployed through IQVIA’s Applied AI portfolio, reduce model training times from days to hours, enabling rapid iteration on predictive models[3]IQVIA, “IQVIA and NVIDIA Announce Strategic Collaboration,” iqvia.com. Synthetic-data generation techniques address class imbalance and privacy constraints, broadening training sets without exposing identifiable records. Such productivity gains justify premium license fees, pushing AI platform growth faster than the overall real-world evidence solutions market. GPU-accelerated inferencing also lowers query latency, a key buying criterion for medical-affairs teams conducting on-demand evidence searches during payer negotiations.

Data Privacy and Interoperability Challenges Hinder Seamless Integration

HIPAA updates, state-level consumer privacy acts and divergent international adequacy decisions complicate cross-border dataset pooling. For example, French health-data hosts must hold a local HDS certification, creating friction for U.S. vendors seeking to analyze European claims at scale. Tokenization vendors solve part of the puzzle but introduce new trade-offs: linkage error or limited demographic fields can erode analytic power. Federated-learning frameworks promise compliance but require heavy DevOps investment; as a result, smaller analytics firms increasingly partner with infrastructure specialists rather than build proprietary stacks. These dynamics consolidate share among incumbents that pair security certifications with high-availability architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Maintain Scale, Software Accelerates

Services generated 54.30% of the real-world evidence solutions market in 2025, reflecting sponsor dependence on external epidemiologists, HEOR consultants and biostatisticians for study design, data curation and regulatory strategy. Large service providers such as IQVIA, ICON and Syneos Health bundle tokenization pipelines that connect pharmacy claims with EHR feeds, extending longitudinal follow-up and raising client switching costs. Multi-year outsourcing frameworks ensure predictable revenue visibility, cushioning macro-economic swings. Services teams also advise on privacy-impact assessments required under GDPR, expediting European study approvals.

Software, though currently smaller, is scaling at an 17.78% CAGR as platform vendors commercialize cloud-native architectures. Subscription models replace volatile project fees, improving vendor cash flow. AI modules embedded in core platforms automatically extract endpoints from radiology and genomic reports, eliminating manual coding bottlenecks. ConcertAI’s SaaS suite, for example, ingests unstructured pathology notes, classifies tumor staging with transformer models and returns structured data formats ready for analysis. Platform adoption often triggers follow-on service requests for bespoke analytics, creating a symbiotic growth loop between software and consulting units.

By Deployment Mode: Cloud Dominates, Hybrid Gains Momentum

Cloud captured 64.35% of the real-world evidence solutions market size in 2025, benefiting from elastic compute and pay-as-you-go pricing. AWS Marketplace listings for RWE analytics rose by more than 40% year on year, indicating strong buyer preference for pre-approved vendors that satisfy shared-responsibility security models. Early migrations involve de-identified cohorts, with protected health information moving only after encryption frameworks and key-management policies mature. U.S. health systems leverage public cloud GPU bursts to train NLP models during peak demand, avoiding capital-intensive server purchases.

Hybrid deployment is advancing at 20.66% CAGR as academic medical centers and publicly funded research networks balance on-premise data sovereignty with scalable analytics. Oracle’s Cloud@Customer nodes, for instance, sit behind hospital firewalls yet federate with public regions for high-intensity compute jobs, satisfying European Data Protection Board residency guidance. Vendors that deliver policy-based workload orchestration—automatically routing PHI-sensitive queries to private clusters—address a critical adoption hurdle and displace legacy on-prem installations. Capital-intensive sites extend the lifespan of existing server racks while accessing cloud GPUs for burst workloads, improving total cost of ownership.

By Therapeutic Area: Oncology Retains Scale, Neurology Accelerates

Oncology commanded 34.65% of the real-world evidence solutions market share in 2025. Rich biomarker datasets, routine genomic profiling and high drug-launch velocity make cancer pathways ideal for evidence generation. Real-world tumor-response metrics derived from imaging and pathology files support accelerated approval submissions and label expansions. NeoGenomics and ConcertAI’s joint hematology registry, covering 370 000 patients, illustrates how linked pathology assays and longitudinal EHR data shorten eligibility screening. The proliferation of precision oncology products ensures sustained demand for updated cohorts, cementing oncology’s scale advantage.

Neurology is the fastest-growing segment, projected at 18.72% CAGR. Digital biomarkers captured by gait-analysis wearables and speech-pattern applications allow continuous monitoring in neurodegenerative disorders, widening real-world data inputs. The Alzheimer’s Association notes a surge in device-enabled observational studies that reduce caregiver burden and improve signal detection. Multi-condition analyses that combine cognitive, mental-health and cardiovascular data enhance payer insights into comorbidity-driven cost drivers, encouraging broader reimbursement of neurology datasets. Vendors expanding neurology modules position themselves for the next wave of precision-therapy launches.

By Application: Drug Development Leads, Reimbursement Evidence Rises

Drug development & approvals held 39.25% of the real-world evidence solutions market size in 2025. External control arms derived from established registries streamline pivotal trials and lower attrition risk. ICON’s AI-enhanced startup toolkit projects patient availability across global sites, cutting screen-fail rates and accelerating first-patient-in milestones. Integration of real-world evidence into early discovery phases helps biopharma teams stratify patient populations, optimizing capital allocation.

Regulatory decision-making & reimbursement, growing at 17.69% CAGR, is fueled by payer mandates for outcomes proof at launch. Germany’s Federal Joint Committee (G-BA) now requests observational data for orphan-drug benefit assessments, forcing sponsors to collect post-launch effectiveness measures. Vendors capable of merging clinical, economic and patient-reported outcomes into single submissions reduce sponsor burden and secure premium contracts. Methodological rigor—such as adjusting for immortal-time bias—has become a baseline requirement, pushing analytics firms to certify their processes under ISO/IEC 27001 and similar frameworks.

By End User: Life-Science Firms Dominate, Provider Networks Outpace

Pharmaceutical and medical-device companies represent 49.20% of the real-world evidence solutions market, as pressure to demonstrate post-launch value rises. Pfizer’s adoption of real-world evidence dashboards across oncology brand teams enables near-real-time safety surveillance and label-expansion decision making. Integrated toolchains that connect pharmacovigilance and market-access functions reduce silo-related delays, strengthening competitive positions.

Healthcare providers and payer-provider networks are the fastest-growing end-user cohort at 16.82% CAGR. U.S. integrated delivery networks embed real-world evidence outputs inside care-pathway redesign projects, targeting unwarranted clinical variation. InterSystems’ IntelliCare EHR, launched in 2025, comes pre-integrated with analytics APIs that surface population-health insights to frontline clinicians, minimizing reliance on back-office analysts. Vendors emphasizing intuitive UIs and minimal training budgets gain traction, as clinician time constraints elevate usability to a critical purchase factor.

Geography Analysis

North America led the real-world evidence solutions market in 2025 with a 40.95% share. The FDA’s RWE pilot programs provide clear procedural guidance, reducing evidentiary risk for sponsors, while U.S. insurers embed outcome metrics into high-cost drug contracts, indirectly driving demand for compliant analytics. Capital markets reward data-centric business models; valuations for listed RWE vendors on Nasdaq trade at revenue multiples above clinical CRO peers, enabling aggressive reinvestment in product roadmaps.

Europe ranked second, supported by the upcoming European Health Data Space regulation, which mandates technical and legal frameworks for cross-border data reuse. GDPR-compliant architectures and HDS accreditation smooth vendor onboarding with national health services. Multi-payer environments foster niche opportunities: France’s ATU system and Germany’s AMNOG pathway increasingly accept real-world evidence to confirm added benefit, opening business for specialized oncology and rare-disease datasets.

Asia-Pacific is the fastest-growing region, projected at a 17.46% CAGR. China’s National Medical Products Administration issued 2024 guidance on accepting foreign real-world data for supplemental New Drug Applications, lowering submission barriers for multinational sponsors. Japan’s MHLW funds digital-biomarker pilots, expanding sources for neurology studies. Australia’s My Health Record system surpasses 95% population coverage, creating robust longitudinal datasets that attract overseas sponsors. Cross-border public-private partnerships are standardizing data dictionaries, enabling multi-country cohort pooling and improving algorithm generalizability for global AI models.

Competitive Landscape

The real-world evidence solutions industry remains moderately concentrated. The top five vendors collectively command a little over 60% of global revenue, leveraging proprietary longitudinal datasets that span prescriptions, diagnostics and procedure claims. IQVIA pairs these assets with Applied AI modules and GPU-accelerated modeling, delivering turnkey analytics that embed directly into sponsor pipelines. Similar integrated offerings from Optum Life Sciences and Veradigm entrench client dependency by covering data ingestion, tokenization, analysis and regulatory submission support.

Strategic alliances intensify in response to AI-driven workloads. IQVIA’s 2025 partnership with NVIDIA aligns curated health datasets with GPU infrastructure, cutting model training times and unlocking new use-cases in multi-modal analytics. Acquisition pipelines prioritize niche datasets that are hard to replicate—imaging repositories, genomic libraries and patient community portals—allowing incumbents to differentiate without lengthy data-collection cycles. Valuation premiums attach to targets holding rare-disease cohorts with strong patient consent frameworks.

Transparent governance and auditability are now core differentiators. Vendors offering documented data lineage from ingestion through algorithmic transformation to output command premium pricing, as sponsors seek to de-risk regulatory audits. Technology-centric firms are therefore expanding advisory benches: Oracle Health, for example, created a regulatory-science unit that guides clients on methodology, blurring the line between software vendor and consulting partner. This convergence raises the competitive bar and may accelerate future consolidation.

Real-World Evidence Solutions Industry Leaders

IQVIA Inc.

Optum Inc.

Oracle Health

ICON plc

IBM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: IQVIA and NVIDIA entered a strategic collaboration to automate complex healthcare workflows with healthcare-grade AI, aligning DGX infrastructure with curated datasets.

- January 2025: Helix expanded its research network by adding three health systems and linked its platform to Komodo Health’s Healthcare Map, enriching genomic-claims linkages.

- January 2025: Picnic Health partnered with Orsini to build AI-enhanced registries for rare diseases, merging EMR records with patient-reported outcomes PicnicHealth.

- Dec 2024: ConcertAI and NeoGenomics launched an AI SaaS solution for hematology research covering 370 000 patient lives.

- December 2024: The FDA issued draft guidance on good clinical practice for trials incorporating decentralized elements and real-world data

- March 2025: InterSystems unveiled IntelliCare, an AI-powered EHR aimed at boosting clinical and administrative efficiency

- January 2025: ICON plc enhanced its AI toolkit to accelerate study startup and resource forecasting

- January 2025: Charles River Laboratories extended its Apollo ecosystem, providing cloud platforms that capture preclinical data feeding downstream RWE pipelines

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the real-world evidence (RWE) solutions market as the aggregate revenue earned from software platforms, curated data sets, and professional services that convert real-world data, electronic health records, claims, pharmacy dispenses, registries, patient-generated inputs, and connected-device feeds into structured evidence used by life-science companies, healthcare payers, providers, and regulators for research, safety, reimbursement, and commercialization decisions. The assessment spans cloud, on-premise, and hybrid deployments across 17 countries within North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

Scope Exclusions: Stand-alone consumer wellness apps, raw wearable sensor data brokers, and generic hospital IT outsourcing fees lie outside the market boundary.

Segmentation Overview

- By Component

- Services

- Data Sets

- Clinical-Settings Data

- Claims & Billing Data

- Pharmacy Dispensing Data

- Patient-Powered & PRO Data

- Other Components

- Software & Analytics Platforms

- By Deployment Mode

- Cloud-based

- On-premise

- Hybrid

- By Therapeutic Area

- Oncology

- Cardiology

- Diabetes

- Neurology

- Psychiatry

- Immunology

- Other Therapeutic Areas

- By Application

- Drug Development & Approvals

- Medical-Device Development & Approvals

- Pharmacovigilance & Safety Studies

- Regulatory Decision-making & Reimbursement

- By End User

- Pharmaceutical & Medical-Device Companies

- Contract Research Organizations (CROs)

- Healthcare Providers & Payer-provider networks

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews and surveys with pharmacovigilance directors, HEOR leads, CRO executives, payers, and health-system informaticians across the United States, Germany, Japan, India, Brazil, and the Gulf states. These conversations validate spending ranges, typical deal sizes, and adoption roadblocks, filling gaps that literature alone cannot close.

Desk Research

We begin by mapping the information universe through freely accessible authorities such as the US FDA RWE Framework, EMA DARWIN EU briefs, CMS open-claims files, and national EHR adoption statistics, alongside publications from ISPOR, PhUSE, and peer-reviewed journals in BMJ or JAMA. Company 10-Ks, investor decks, and key press releases supply pricing and contract clues, which are then cross-checked in paid databases, D&B Hoovers for revenue splits, Dow Jones Factiva for deal flow, and Questel for analytics software patent activity. These sources anchor basic market math while revealing growth triggers like regulatory pilots or AI-enabled study designs. The list above is illustrative; many additional references inform data collection and sense-checking.

Market-Sizing & Forecasting

A top-down reconstruction starts with national healthcare IT spend and the proportion allocated to RWE initiatives, followed by a prevalence-to-treated cohort demand pool for oncology and chronic disease pipelines. Selective bottom-up checks, sampled average selling price multiplied by active client counts, fine-tune totals. Key variables include EHR penetration, global biopharma R&D outlay, count of FDA approvals citing external control arms, cloud service price trajectories, and specialty drug launch volumes. A multivariate regression blends these drivers to project value through 2030, with scenario analysis overlaying regulatory or economic shocks.

Data Validation & Update Cycle

Model outputs undergo variance scans against independent metrics, after which a second analyst reviews assumptions before sign-off. Reports refresh every twelve months, and we trigger interim updates when material events, major RWE-backed approvals, pricing inflections, or data privacy rules shift the baseline.

Why Our Real-World Evidence Solutions Baseline Is Dependable

Published estimates often differ because firms pick unique scopes, input variables, and refresh cadences.

Key gap drivers include whether subscription data licensing is bundled, if payer analytics spend is rolled in, how exchange rate conversions are handled, and the depth of primary source verification. Mordor's disciplined scope centers on life-science use cases only, applies blended currency averages for the calendar year, and interviews market participants each cycle, producing a balanced figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.44 B (2025) | Mordor Intelligence | - |

| USD 5.42 B (2025) | Global Consultancy A | Includes broader healthcare analytics and minimal primary validation |

| USD 20.03 B (2025) | International Research Publisher B | Bundles raw data brokerage, software for providers, and aggressive currency conversion |

| USD 2.03 B (2024) | Trade Journal C | Earlier base year and excludes software platforms, relying on straight-line extrapolation |

In sum, the disciplined variable selection, recurring expert touchpoints, and clearly stated exclusions ensure Mordor Intelligence delivers a transparent, repeatable baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the real-world evidence solutions market?

The market is valued at USD 2.84 billion in 2026 and is projected to reach USD 6.04 billion by 2031, reflecting a 16.33% CAGR.

Which component dominates the real-world evidence solutions market?

Services account for 54.30% of the market, as sponsors still rely on external experts for study design, data curation and regulatory strategy

Why do oncology datasets command the largest share?

Oncology holds 34.65% of the real-world evidence solutions market because biomarker-rich registries and high launch velocity require continuous evidence generation to support precision-therapy approvals

How fast is the Asia-Pacific market expanding?

Asia-Pacific is the fastest-growing region with a 17.46% CAGR to 2031, driven by rapid digitization of health records in China, Japan and Australia and increasing regulator acceptance of foreign real-world data

What role does AI play in real-world evidence generation?

AI automates extraction from unstructured data, reduces manual review time and provides predictive insights, allowing vendors to command premium license fees and grow faster than the overall market

What are the main barriers to broader adoption of real-world evidence?

Fragmented privacy regulations and interoperability challenges slow cross-border studies, though tokenization and federated learning are mitigating obstacles for vendors with strong engineering capabilities

Page last updated on: