Healthcare Payer Services (HPS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

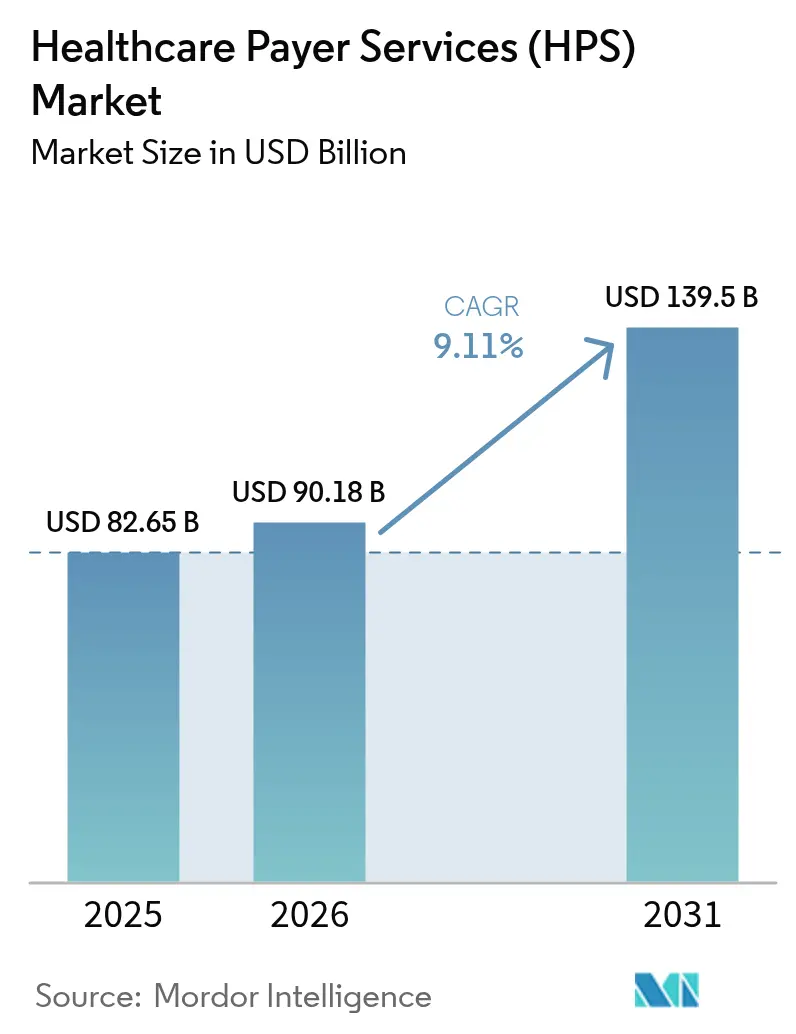

| Market Size (2026) | USD 90.18 Billion |

| Market Size (2031) | USD 139.5 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Payer Services (HPS) Market Analysis by Mordor Intelligence

The healthcare payer services (HPS) market size was valued at USD 82.65 billion in 2025 and estimated to grow from USD 90.18 billion in 2026 to reach USD 139.5 billion by 2031, at a CAGR of 9.11% during the forecast period (2026-2031). Heightened pressure to cut administrative spending, rising regulatory complexity, and the rapid infusion of artificial intelligence into claims workflows are combining to sustain healthy double-digit growth momentum. End-to-end business-process specialists capture shares by bundling claims, members, and provider functions on modern cloud platforms. At the same time, IT-heavy engagements focused on data analytics and robotic process automation are scaling even faster. Generative AI use cases that shorten claims-handling cycles and improve payment integrity are rapidly moving from pilot to production, reinforcing the overall value proposition that outsourcing delivers. At the same time, tightening data-privacy rules and a sharp rise in cyber intrusion attempts are prompting payers to favor partners that can prove zero-trust architectures, audited encryption, and multi-factor access controls.

Key Report Takeaways

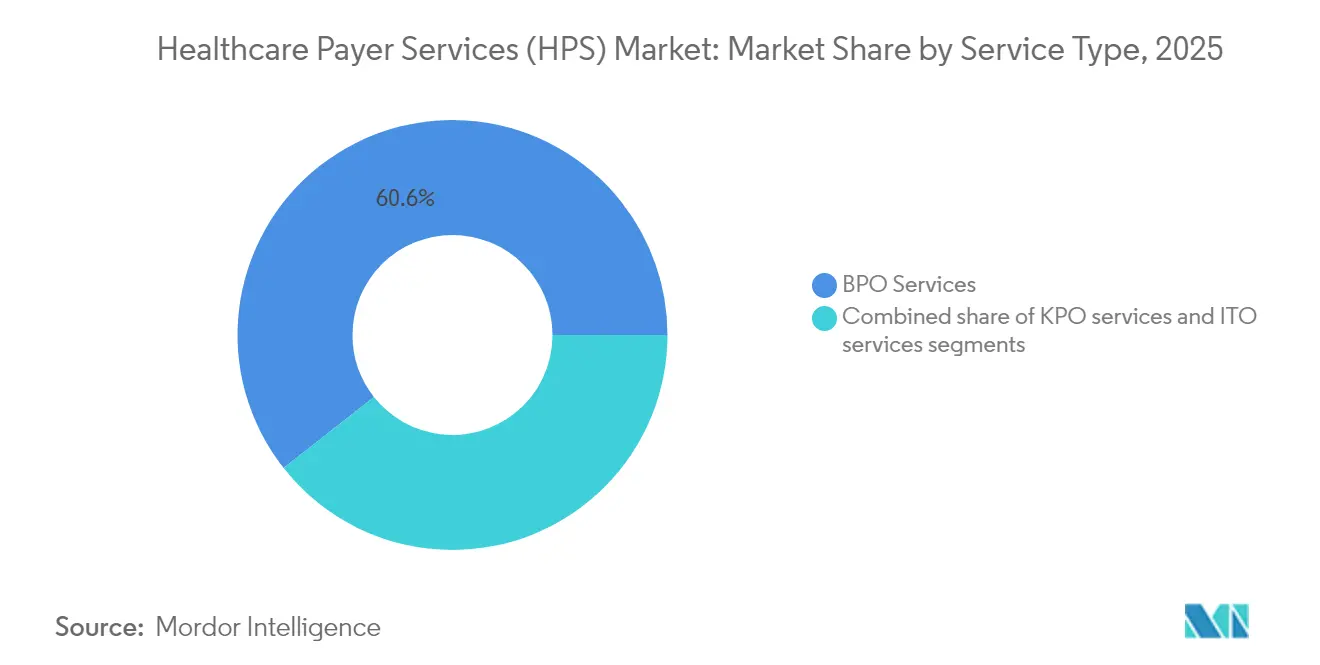

- By service type, Business Process Outsourcing led with a 60.62% healthcare payer services market share in 2025; IT Outsourcing is projected to grow at a 9.74% CAGR through 2031.

- By application, Claims Management accounted for 31.22% of the healthcare payer services market size in 2025, whereas Analytics & Fraud Management is poised to expand at a 10.35% CAGR to 2031.

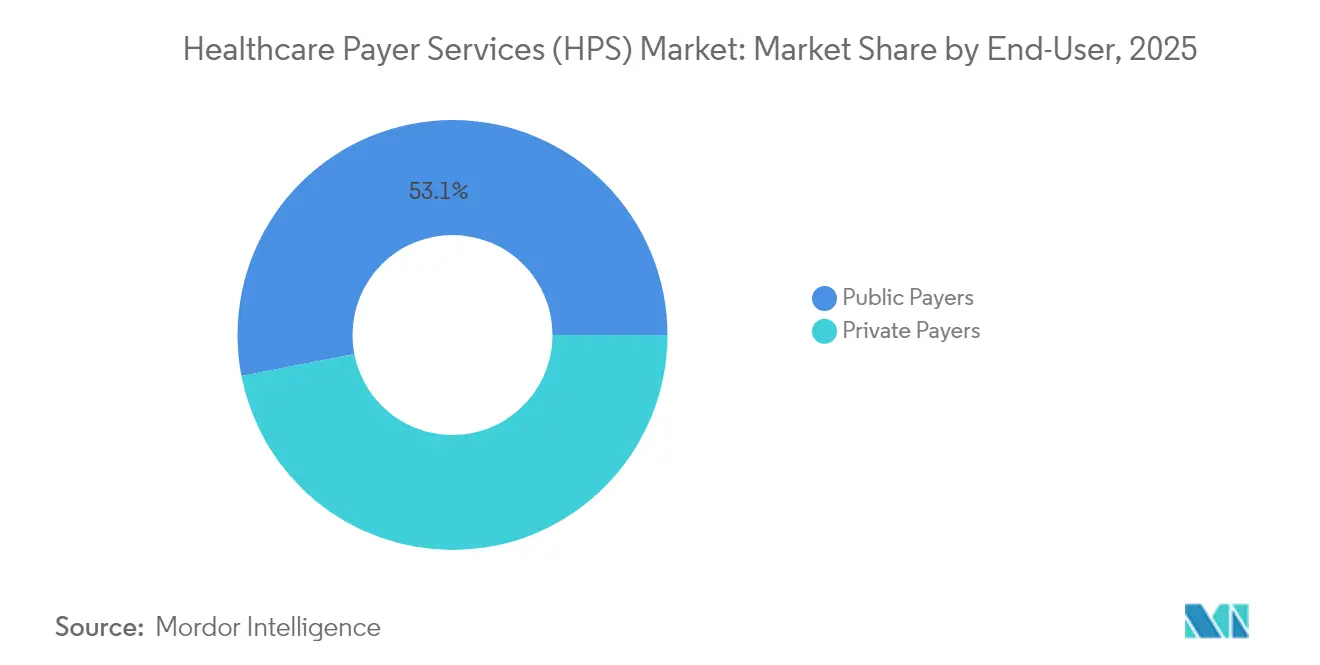

- By end-user, Public Payers commanded 53.05% of 2025 revenue; Private Payers are set to record the fastest 9.48% CAGR during the forecast window.

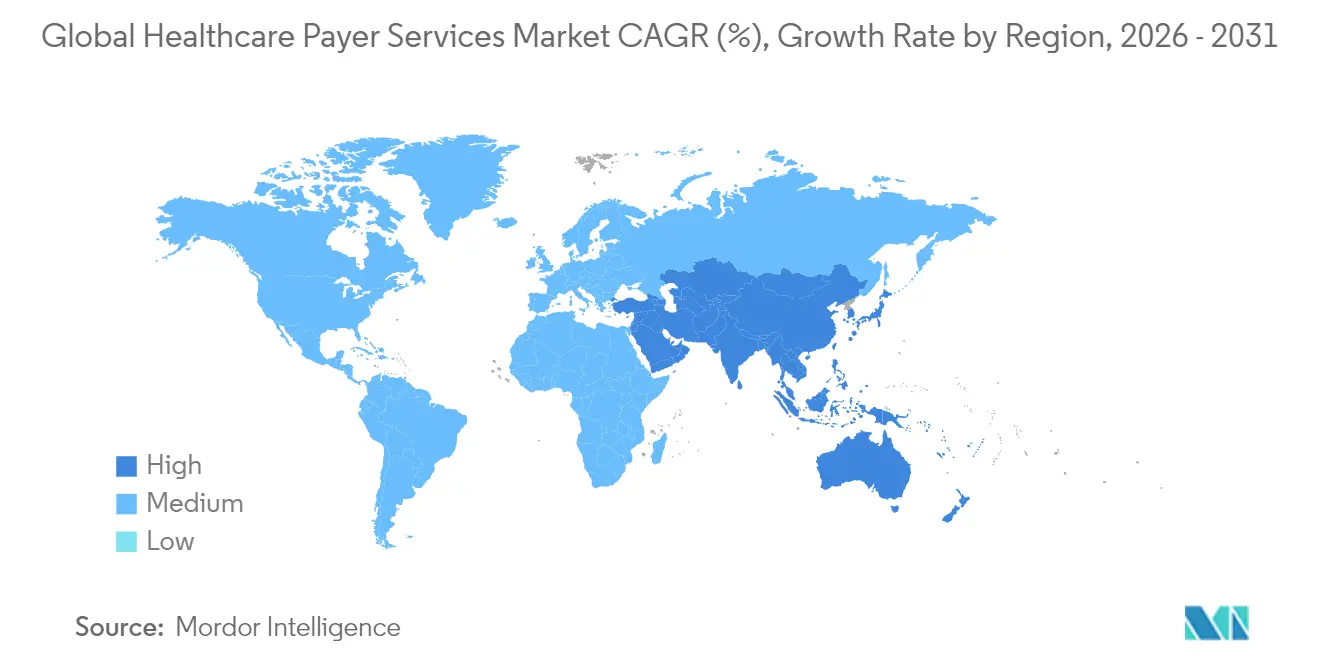

- North America retained 46.10% of global revenue in 2025, while Asia-Pacific is forecast to deliver the highest regional CAGR of 10.12% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Payer Services (HPS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition to value-based reimbursement models | +2.1% | North America; Europe | Medium term (2-4 years) |

| Rising healthcare fraud requiring advanced analytics | +1.8% | Global, emphasis on North America | Short term (≤2 years) |

| Rapid adoption of GenAI & RPA for claims automation | +1.7% | North America; Europe; Asia-Pacific | Short term (≤2 years) |

| Escalating administrative cost pressures on payers | +1.5% | Global | Short term (≤2 years) |

| Expansion of digital health ecosystems and interoperability | +1.3% | North America; Europe; Asia-Pacific | Medium term (2-4 years) |

| Private-equity investment accelerating outsourcing demand | +0.6% | North America; Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transition to Value-Based Reimbursement Models

U.S. policy targets call for every Medicare beneficiary to be enrolled in an accountable care relationship by 2030, pushing payers toward advanced analytics, care-coordination engines, and performance-based contracting. Smaller health plans often lack the capital and expertise to build these capabilities internally, prompting a surge in specialist outsourcing agreements that bundle actuarial insight with risk-based payment administration. Industry surveys[1]Medical Group Management Association, “Less Than Half of Practice Leaders Have Positive Outlook on Value-Based Care,” mgma.com show that fewer than half of medical-practice leaders feel confident about executing value-based care, underscoring a widening skills gap that external partners fill. Providers with proven experience in alternative payment models are therefore winning multi-year contracts to manage episodes of care, measure outcomes, and reconcile shared-savings calculations. These engagements typically start with data-platform modernization and expand into end-to-end member engagement, creating sticky revenue streams for vendors. As quality metrics replace volume metrics, demand for real-time clinical data feeds and predictive cost-of-care algorithms further lifts the adoption of outsourced solutions.

Rising Healthcare Fraud Requiring Advanced Analytics

Fraud and abuse siphon off an estimated 3% of total spending every year, driving payers to deploy machine-learning engines that can score claims before payment. Outsourcing partners that couple domain expertise with proprietary anomaly-detection models are delivering 60% faster adjudication cycles and 12% higher accuracy[2]Ramesh Pingili, “The Integration of Generative AI in RPA for Enhanced Insurance Claims Processing,” iaeme.comin pilot programs. These tangible results are moving fraud analytics from optional add-on to core requirement in new requests for proposal. North American contracts increasingly stipulate shared-savings arrangements, with vendors rewarded for every dollar recovered from improper billing. To sustain model performance, providers are embedding synthetic data generation and continuous-learning pipelines that minimize false positives. As fraud schemes evolve toward identity theft and provider credential manipulation, collaborative threat-intelligence networks between payers and vendors are becoming standard features of master service agreements.

Rapid Adoption of GenAI & RPA for Claims Automation

Nearly 80% of U.S. health plans are modernizing infrastructure to deploy artificial-intelligence tools that read, triage and code clinical documents. Robotic workflows now extract diagnosis codes, apply policy edits and feed structured data directly into core administration systems, cutting average handling time from days to minutes. Outsourcing firms that maintain large labeled datasets and pre-trained language models can on-board new payer clients in weeks, circumventing the long development cycles that in-house initiatives often face. Beyond speed, GenAI improves member satisfaction by enabling instant digital communications that explain denial reasons in plain language. Early adopters report material reductions in re-work and call-center traffic, reinforcing the business case for third-party partnerships. As technology costs fall, mid-sized regional payers are entering the market, broadening the client base for vendors.

Escalating Administrative Cost Pressures on Payers

Administrative expense as a share of premium remains on an upward trajectory, fueled by wage inflation and the rising price of specialized talent. Surveys of payer executives indicate that more than 90% plan to increase third-party vendor use to relieve cost pressure. Outsourcing consolidates repetitive back-office tasks across multiple clients, unlocking economies of scale unavailable to individual health plans. Vendors also absorb technology refresh costs, allowing payers to migrate to cloud-native platforms without significant capital outlay. Contract structures are shifting toward outcome-based pricing, transferring a portion of efficiency risk from payers to service providers. As the labor market tightens further, the relative cost advantage of mature offshore locations such as India and the Philippines remains attractive, even after factoring in security and compliance spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening data-privacy and localization regulations | -1.2% | North America; Europe | Medium term (2-4 years) |

| Heightened cybersecurity breach risk in payer databases | -0.9% | Global | Short term (≤2 years) |

| Labor cost inflation in major outsourcing hubs | -0.8% | Asia-Pacific, notably India | Medium term (2-4 years) |

| Hidden transition and governance costs in outsourcing deals | -0.7% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Tightening Data-Privacy & Localization Regulations

A December 2024 Notice of Proposed Rulemaking from the U.S. Department of Health and Human Services would mandate encryption[3]U.S. Department of Health and Human Services, “HIPAA Security Rule Notice of Proposed Rulemaking,” hhs.gov of all electronic protected health information and formalize multi-factor authentication across the healthcare ecosystem. Parallel restrictions under the Protecting Americans’ Data from Foreign Adversaries Act limit cross-border data flows, compelling vendors to stand up in-country hosting and auditable audit trails. These compliance layers add cost and complexity to offshore delivery models, eroding part of the traditional labor arbitrage. European clients impose similarly strict controls under the General Data Protection Regulation, while several Asia-Pacific jurisdictions now require health data to reside within national borders. Vendors able to demonstrate certified data-segmentation techniques and local sovereign-cloud options gain a competitive advantage. Yet, the capital outlay required to maintain multiple geo-segregated environments can dampen smaller providers’ growth.

Heightened Cybersecurity Breach Risk in Payer Databases

Healthcare records command premium prices on the dark web, pushing threat actors to target insurers through phishing, supply-chain compromise and ransomware. A recent federal review found that earlier HIPAA compliance audits captured only a narrow slice of actual risk exposure, prompting calls for broader, deeper inspection scopes. For outsourcing relationships, elevated breach risk translates into stricter vendor-risk-management protocols, higher cyber insurance premiums and longer contract-negotiation cycles. Service-level agreements now specify recovery time objectives measured in minutes and require independent penetration testing at least annually. Vendors that have invested in zero-trust frameworks and continuous security-monitoring centers can mitigate client concerns, but the incremental security spend may temper margin expansion over the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: BPO Retains Scale, ITO Leads Growth

Business Process Outsourcing captured 60.62% of 2025 revenue, reflecting payers’ long-standing reliance on external partners for claims, enrollment and provider-network tasks. The healthcare payer services market size for BPO activities climbed alongside enrollment growth in government insurance programs, and bundled contracts that embed payment-integrity analytics now anchor multi-year engagements. Emerging vendor platforms blend human adjudication with rules engines, reducing notice-of-deficiency rates in CMS audits and driving measurable medical-loss-ratio improvements.

Information-technology Outsourcing expands at a 9.74% CAGR, the fastest among all service lines. Demand centers on cloud migration, API-based interoperability and data-warehouse modernization that underpins value-based reimbursement analytics. Several regional payers shifted entire core-administration stacks to vendor-hosted platforms in 2024, cutting upgrade cycles from annual releases to quarterly drops. Knowledge Process Outsourcing remains a niche but strategic layer, supplying actuarial modeling and regulatory-reporting muscle where domestic talent shortages persist.

By Application: Claims Management Dominates, Analytics Gains Traction

Claims Management held 31.22% of the healthcare payer services market share in 2025, underscoring the cost impact of adjudication efficiency. Vendors wielding GenAI-driven coding assistants shortened first-pass processing times by 60% and reduced appeal rates, freeing payer staff to focus on complex exceptions. The healthcare payer services market size tied to claims is therefore poised to grow steadily in absolute terms even as its percentage share edges down in favor of data-driven offerings.

Analytics & Fraud Management posts the highest 10.35% CAGR to 2031 as payers prioritize proactive loss avoidance over retrospective recovery. Outsourcing contracts frequently bundle real-time anomaly detection with special-investigation-unit staffing, creating outcome-linked fee models. Integrated member and provider portals, billing automation and human-resource support round out the application stack, contributing incremental volume but remaining secondary to the high-value analytics segment.

By End-User: Public Programs Anchor Volume, Private Carriers Accelerate

Public programs such as Medicare, Medicaid and regional social-insurance funds accounted for 53.05% of 2025 revenue, reflecting their sheer enrollment scale. The healthcare payer services market size attributable to public payers grows alongside federal imperatives to migrate toward accountable-care constructs that require new data-sharing and quality-tracking capabilities. Outsourcing partners supply care-coordination dashboards, risk-adjustment coding and beneficiary outreach modules that small state plans could not afford to build alone.

Private payers record the faster 9.48% CAGR, lifted by brisk Medicare Advantage enrollment and renewed employer interest in innovative benefit designs. Contracts increasingly cover member-engagement chatbots, digital ID cards and real-time cost-estimator tools that differentiate plan offerings. With margins squeezed by medical-trend uncertainty, private carriers favor vendors willing to tie compensation to tangible administration-expense reductions, reinforcing the growth outlook for the segment.

Geography Analysis

North America produced 46.10% of 2025 global revenue and is projected to expand at a 8.96% CAGR through 2031. Mature electronic-data-interchange networks, early GenAI adoption and an active regulatory agenda sustain outsourcing demand. Federal commitments to accountable care intensify the need for data-sharing and outcome-tracking solutions, prompting regional plans to deepen vendor partnerships.

Asia-Pacific delivers the fastest 10.12% CAGR as rising disposable income and expanded insurance penetration in India, Indonesia and mainland China enlarge the addressable base. India continues to dominate as a delivery hub, supplying 55-65% of global capability-center capacity for the healthcare payer services industry, while the Philippines strengthens its niche in voice-based member services. Labor-cost inflation and local data-sovereignty rules temper margin expansion but do not derail growth.

Europe registers a steady 8.71% CAGR driven by digital-health adoption and population aging. Strict General Data Protection Regulation compliance needs elevate the importance of in-region hosting and certified encryption, driving demand for nearshore centers in Central and Eastern Europe. The Middle East & Africa and South America contribute smaller but rising shares, fueled by health-system modernization and the regulatory push to widen coverage.

Competitive Landscape

The healthcare payer services market exhibits moderate concentration. Five global vendors—Accenture, Cognizant, TCS, Infosys, and Optum—collectively account for a sizable share, yet dozens of mid-tier specialists thrive by targeting niche functions such as payment integrity or risk-adjustment coding. Accenture alone executed 27 strategic acquisitions in 2024[4]CRN, “All the Accenture Acquisitions of 2024,” crn.com, deepening public-sector and federal-health capabilities. Cognizant expanded payer analytics through targeted tuck-ins, while Infosys strengthened cloud migration offerings for Blue-plan clients.

Technology differentiation edges out labor arbitrage as the primary competitive lever. Vendors showcase proprietary GenAI models, robotic automation libraries, and curated health-data lakes to win renewals and cross-sell adjacent services. Co-innovation agreements with hyperscale cloud providers accelerate product road maps and embed vendors deeper within client architectures.

Private-equity activity adds a layer of dynamism. Recent deals include EQT’s majority investment in GeBBS Healthcare Solutions, which aims to create an integrated revenue cycle and payer-services platform. Capital inflows fund technology upgrades and geographic expansion, but also heighten competitive intensity as newly capitalized firms bid aggressively for large renewals.

Healthcare Payer Services (HPS) Industry Leaders

Accenture plc

Cognizant Technology Solutions

Infosys Ltd.

Tata Consultancy Services

UnitedHealth Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The U.S. Department of Health and Human Services released its strategic plan for responsible AI adoption in health and human services, outlining principles that directly influence vendor solution design.

- December 2024: The Centers for Medicare & Medicaid Services confirmed the Medicare Advantage VBID model will sunset after 2025, requiring payers and their outsourcing partners to adjust benefit-design and data-reporting workflows.

- September 2024: EQT acquired GeBBS Healthcare Solutions to scale technology-enabled revenue-cycle and payer-services offerings.

- July 2024: Amulet Capital Partners closed a USD 1.2 billion fund targeting life-sciences and payer-services platforms, signaling robust investor appetite for the space.

Global Healthcare Payer Services (HPS) Market Report Scope

As per the scope of the report, the healthcare payer services providers assist payers in actively engaging members, meeting compliance requirements, reducing healthcare costs, and improving overall operational performance. The Healthcare Payer Services Market is Segmented by Service Type (Business Process Outsourcing, IT Outsourcing Services, Knowledge Process Outsourcing Services), Application (Claims Management Services, Integrated Front Office Service and Back Office Operations, Member Management Services, Provider Management services, Billing and Accounts Management Services, Analytics and Fraud Management Services, Human Resource Services), End-User (Private Payers, Public Payers), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Business Process Outsourcing (BPO) Services |

| IT Outsourcing (ITO) Services |

| Knowledge Process Outsourcing (KPO) Services |

| Claims Management Services |

| Integrated Front & Back Office Operations |

| Member Management Services |

| Provider Management Services |

| Billing & Accounts Management Services |

| Analytics & Fraud Management Services |

| Human Resource Services |

| Private Payers |

| Public Payers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Business Process Outsourcing (BPO) Services | |

| IT Outsourcing (ITO) Services | ||

| Knowledge Process Outsourcing (KPO) Services | ||

| By Application | Claims Management Services | |

| Integrated Front & Back Office Operations | ||

| Member Management Services | ||

| Provider Management Services | ||

| Billing & Accounts Management Services | ||

| Analytics & Fraud Management Services | ||

| Human Resource Services | ||

| By End-User | Private Payers | |

| Public Payers | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What operational challenges are pushing health insurers to outsource payer services?

Health insurers face rising administrative costs, tightening reimbursement margins and complex value-based billing rules, prompting them to externalize high-volume tasks such as claims adjudication, member engagement and provider data management to specialists that can spread fixed costs across multiple clients.

How is generative AI reshaping claims processing in healthcare payer services outsourcing?

Generative AI tools automate data extraction from clinical documents, recommend accurate diagnosis codes and flag policy discrepancies in real time, allowing outsourcing partners to cut turnaround times, lower error rates and free payer staff for higher-value exception handling.

Which functional areas see the quickest adoption of outsourcing among private payers?

Private payers are rapidly engaging third-party vendors for advanced analytics, fraud detection and digital member-experience solutions because these capabilities require large data sets, specialized talent and continuous technology refresh that are difficult to maintain internally.

How are evolving data-privacy regulations influencing vendor selection in this market?

New rules mandating encryption, multi-factor authentication and in-country data hosting are steering insurers toward vendors that operate sovereign clouds, demonstrate zero-trust architectures and hold current third-party security certifications.

What role does private-equity investment play in the competitive dynamics of payer services outsourcing?

Private-equity firms are consolidating niche providers into full-service platforms, injecting capital for technology upgrades and aggressive go-to-market campaigns, which intensifies price competition while expanding the range of integrated offerings available to insurers.

Why are Asia-Pacific delivery centers increasingly attractive to global outsourcing contracts?

Asia-Pacific hubs pair large, clinically trained workforces with maturing cybersecurity controls, enabling vendors to deliver multilingual support, 24-hour operations and competitive pricing that appeals to payers seeking both efficiency and compliance.

Page last updated on: