High-Resolution Melting Analysis Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

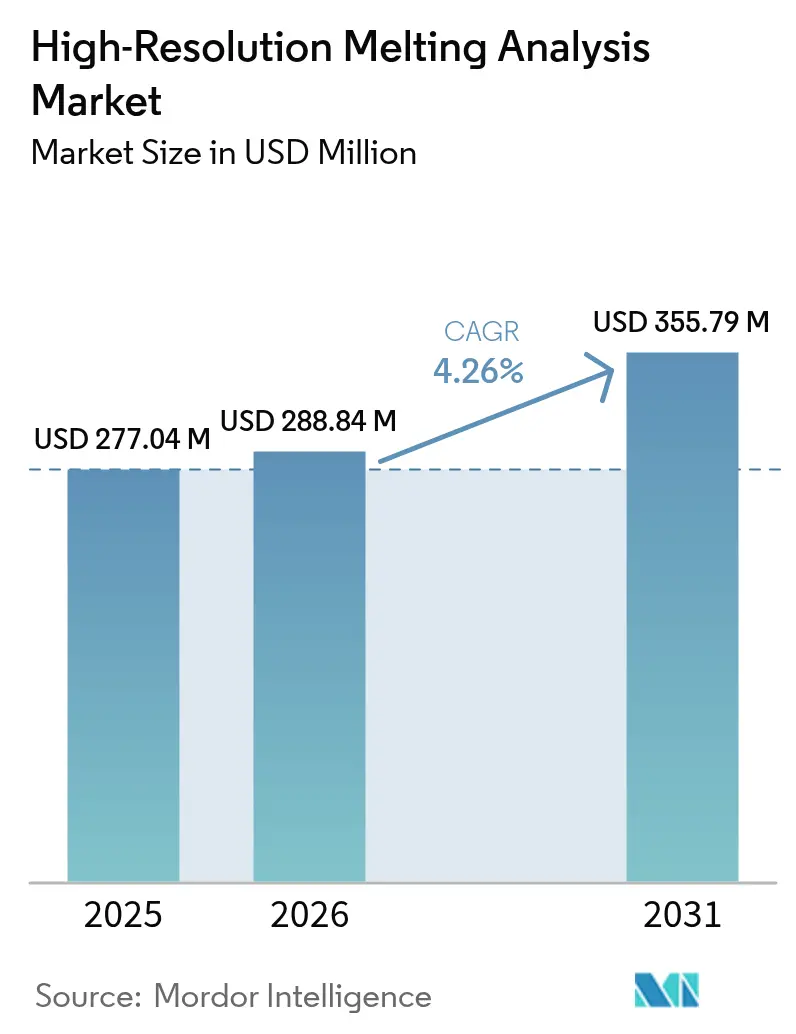

| Market Size (2026) | USD 288.84 Million |

| Market Size (2031) | USD 355.79 Million |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Resolution Melting Analysis Market Analysis by Mordor Intelligence

high-resolution melting analysis market size in 2026 is estimated at USD 288.84 million, growing from 2025 value of USD 277.04 million with 2031 projections showing USD 355.79 million, growing at 4.26% CAGR over 2026-2031. Strong uptake of precision-medicine programs, broader reimbursement for genetic tests, and a clear cost advantage over next-generation sequencing are sustaining demand. Established molecular-diagnostics suppliers keep introducing integrated platforms that combine HRM, digital PCR, and cloud analytics to cut manual steps, speed turnaround, and lower per-test cost. Infectious-disease surveillance programs in Asia-Pacific and Latin America are creating new, high-throughput use cases, while point-of-care innovators are pushing compact instruments into clinics that lack molecular-testing expertise. Meanwhile, labor shortages in clinical labs are accelerating automation, cementing HRM’s position as an accessible, cost-effective genotyping workhorse.

Key Report Takeaways

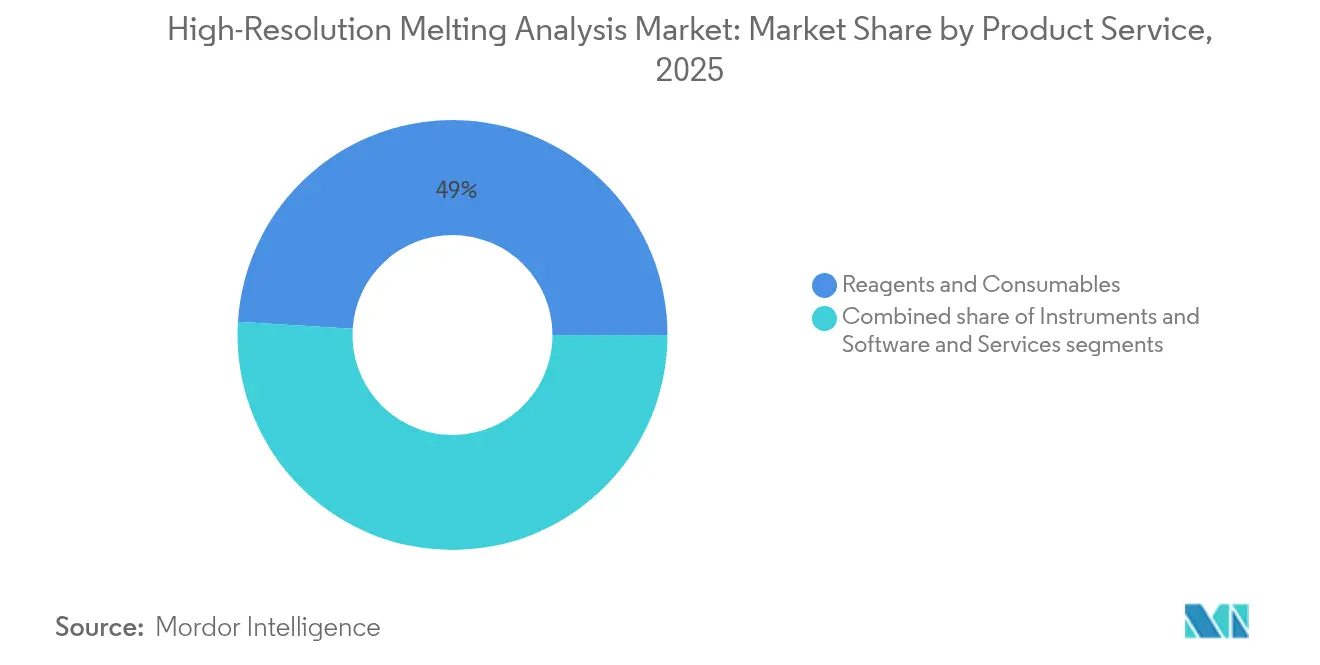

- By product & service, reagents and consumables led with 49.02% of the High-Resolution Melting Analysis market share in 2025, whereas instruments are forecast to post the fastest 6.41% CAGR through 2031.

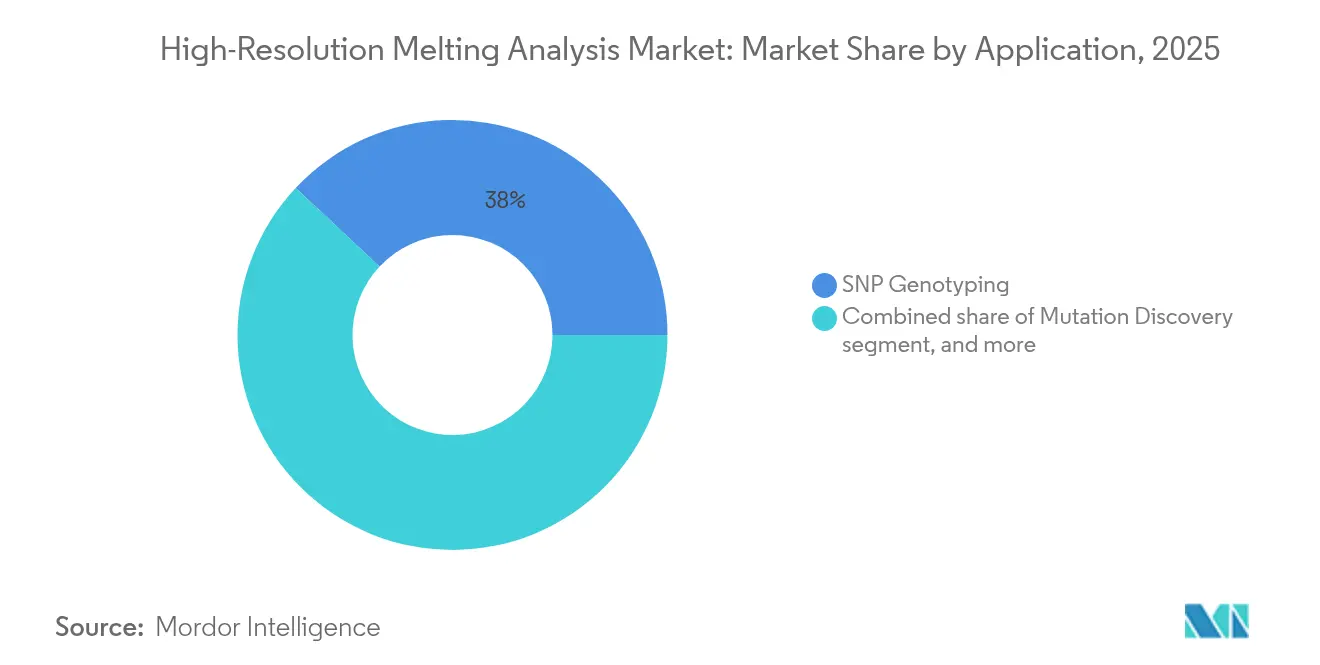

- By application, SNP genotyping commanded 38.01% of the High-Resolution Melting Analysis market size in 2025, while pathogen identification is projected to expand at a 7.26% CAGR to 2031.

- By end-user, research laboratories accounted for 46.10% of the High-Resolution Melting Analysis market size in 2025; hospitals and diagnostic centers record the highest forecast CAGR at 7.68% through 2031.

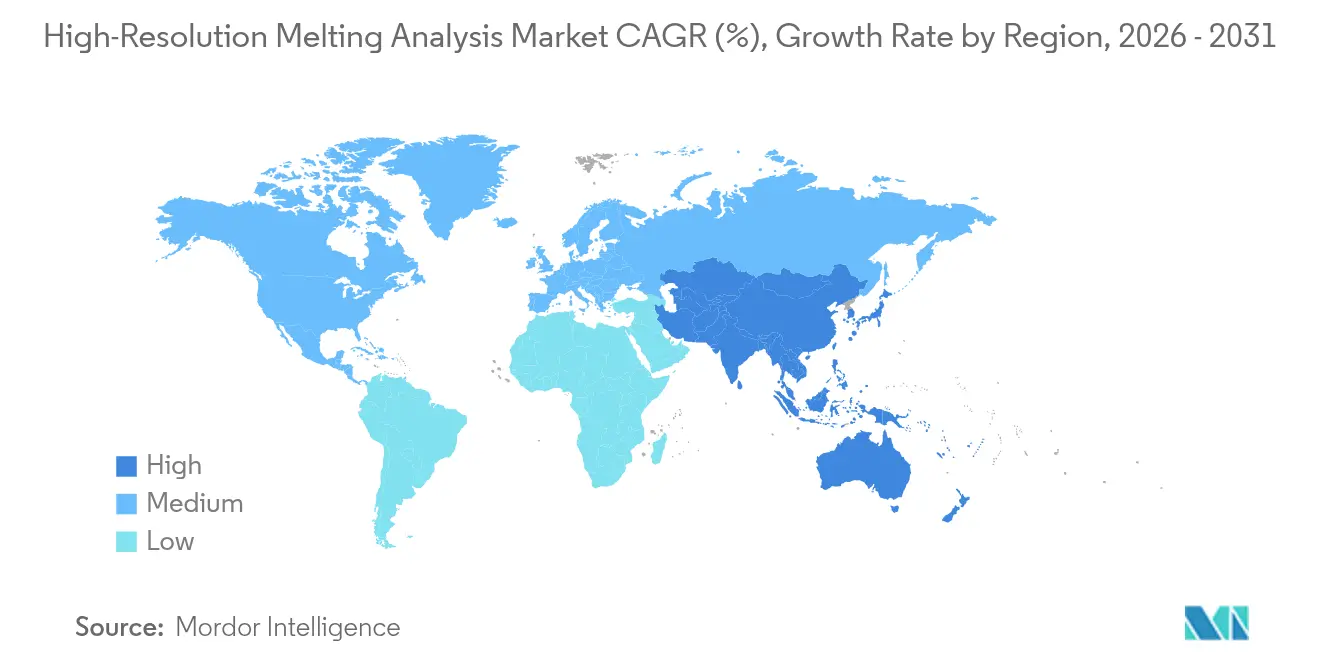

- By geographically, North America held 41.10% of global revenue in 2025, and Asia-Pacific is poised for the quickest 5.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-Resolution Melting Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of precision medicine initiatives | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion of genetic-testing reimbursement policies | +0.8% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Surge in companion-diagnostics development pipelines | +0.7% | Global, led by US, EU, Japan | Long term (≥ 4 years) |

| Increasing government funding for genomic-surveillance programs | +0.6% | APAC core, spill-over to MEA & Latin America | Medium term (2-4 years) |

| Proliferation of decentralized point-of-care molecular testing | +0.5% | Global, with early uptake in resource-limited settings | Short term (≤ 2 years) |

| Integration of cloud-based analytics for high-throughput workflows | +0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Precision Medicine Initiatives

Precision-medicine programs now stretch well beyond oncology into cardiology, psychiatry, and chronic-disease management, and they rely heavily on rapid gene–drug matching assays. The US Centers for Medicare & Medicaid Services proposed coverage for pharmacogenomic testing, enabling HRM platforms to secure reimbursement for clinically actionable variants. Leading payers such as UnitedHealthcare have started aligning policies that grant consistent coverage once clinical utility is proven, creating a stable revenue stream for HRM reagent vendors. Diagnostic manufacturers respond by embedding HRM modules into cartridge-based workflows that deliver genotyping results in under an hour, as illustrated by QIAGEN’s QIAstat-Dx expansion into companion diagnostics. The combination of lower test cost, quicker turnaround, and billing clarity is driving hospital labs to replace Sanger sequencing in routine drug-response panels, thereby broadening the installed base.

Expansion of Genetic Testing Reimbursement Policies

Payers in the United States and Europe are shifting from restrictive, indication-specific rules toward evidence-based frameworks that reward analytical accuracy and clinical usefulness. An American Journal of Managed Care study tracking 110 health-plan policies showed that plans covering ≥15 actionable drug-gene pairs doubled between 2023 and 2025. HRM systems gain because they reach sensitivity thresholds at a fraction of sequencing’s price, which suits high-volume screening. EU payer cooperation under the European Network for Health Technology Assessment has further accelerated cross-border reimbursement decisions, giving multinational labs a uniform outlook. Large platform suppliers capitalize by bundling HRM reagents with cloud portals that auto-generate insurer-ready reports, reducing administrative overhead in small community hospitals.

Surge in Companion Diagnostics Development Pipelines

Pharma pipelines now embed biomarkers early, creating demand for rapid genotyping solutions that can stratify trial subjects on tight timelines. Bio-Rad’s droplet digital PCR partnership with leading cancer centers demonstrated HRM primers detecting circulating tumor DNA at femtomolar levels, offering a same-day screen during study enrollment. AI-driven pattern recognition built into these platforms cuts analyst time by 60%, a critical gain when trial sites lack molecular specialists. Roche’s FDA cleared dual ISH probe cocktail for B-cell lymphoma underscores how integrated reagents and instruments are being validated together, shortening the path from assay concept to market. As biopharma shifts toward multi-omic signatures, vendors layering methylation and copy-number routines onto HRM chemistries are securing multi-year codevelopment agreements.

Increasing Government Funding for Genomic Surveillance Programs

Public-health agencies now budget long-term funding for broad pathogen-genomics capacity. Australia’s Genomics Health Futures Mission earmarked USD 500.1 million over 10 years, including grants to expand HRM-ready workflows in national labs[1]Australian Government Department of Health and Aged Care, “Genomics Health Futures Mission,” health.gov.au. The US CDC’s Advanced Molecular Detection initiative backs similar infrastructure, emphasizing reagent stockpiles and cloud analytics that support variant discovery within 24 hours[2]Centers for Disease Control and Prevention, “Advanced Molecular Detection Program,” cdc.gov. Platforms integrating HRM with digital-PCR confirmatory steps help labs reach variant calling accuracy above 99%, meeting surveillance thresholds. Regional consortia such as AusTrakka interlink lab nodes so that outbreak signals propagate in real time, lifting overall testing volumes and reagent pull-through for suppliers.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment required for HRM instrumentation | -0.9% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Limited standardization of assay protocols across laboratories | -0.6% | Global, particularly affecting multi-site studies | Medium term (2-4 years) |

| Shortage of skilled molecular-diagnostics personnel | -0.5% | Global, most pronounced in developing regions | Medium term (2-4 years) |

| Regulatory uncertainty in emerging economies | -0.4% | Latin America, MEA & parts of APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Required for HRM Instrumentation

Entry-level HRM platforms cost between USD 60,000 and USD 120,000, excluding service contracts, a hurdle for small labs whose reimbursement flows remain volatile. Staffing shortages compound the problem; one 2024 survey found 29.1% of US clinical labs reported difficulty retaining technologists, pushing management to delay equipment upgrades. Digital-twin projects show promise in boosting utilization and lowering amortized cost per test, yet such workflow-optimization software adds another USD 100,000-200,000, keeping total investment high. Financing solutions such as reagent-rental agreements are emerging, but interest-rate hikes since 2024 have raised leasing costs, limiting uptake in low-margin public hospitals.

Limited Standardization of Assay Protocols Across Laboratories

HRM primer design, thermal profiles, and dye chemistries vary widely, which inflates inter-lab result variance and slows regulatory acceptance. The FDA’s stepped rollout of laboratory-developed test regulation aims to push labs toward validated kits, but the four-year transition leaves a compliance gray zone that smaller facilities struggle to navigate. AI-powered reporting tools funded by BARDA, such as BugSeq’s automated pipeline, improve consistency by applying uniform melt-curve calling rules across sites, yet they require bioinformatics training many hospital labs lack. Differing approval pathways in the EU, USA, and Japan further fragment the market, raising costs for suppliers that must compile separate data packages for each jurisdiction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Market Momentum Shifts Toward Integrated Platforms

Reagents and consumables generated the largest revenue in 2025, contributing 49.02% due to recurring refill demand that scales with installed instruments. The High-Resolution Melting Analysis market size attributable to reagents reached USD 135.82 million, and the category is forecast to maintain steady mid-single-digit growth as assay menus widen. Instrument revenue is accelerating at a 6.41% CAGR because multisite health systems invest in unified, automated analyzers that slash technician time and standardize quality across campuses. Manufacturers now bundle instruments with cloud licenses and validated assays, creating all-inclusive contracts that align with outcome-based procurement models. Software and service revenue, although still below 10% of overall value, is climbing fastest in mature markets where labs outsource data interpretation to vendor-operated platforms that guarantee 24/7 support.

By Application: Clinical Priorities Expand HRM’s Reach

SNP genotyping held 38.01% of 2025 revenue as clinicians relied on HRM panels to screen pharmacogenomic hotspots that affect dose and toxicity. That share is expected to erode slightly as pathogen identification rises at a 7.26% CAGR on the back of antimicrobial-stewardship mandates. Multiplex HRM assays that differentiate 20+ respiratory pathogens in a single tube are entering routine use, halving per-sample reagent cost compared with monoplex RT-PCR. Mutation discovery applications leverage HRM’s sensitivity to unknown variants; a recent acute-myeloid-leukemia study delivered 98% sensitivity with a EUR 20 reagent cost per test, underscoring the economic edge over next-generation sequencing. Methylation analysis remains niche but is gaining attention as oncology groups look for fast, low-cost epigenetic screens to complement liquid biopsies.

By End-User: Hospitals Catch Up with Research Labs

Academic and government research labs dominated demand in 2025, holding 46.10% of global revenue, reflecting HRM’s roots in fundamental genetics. Hospitals and diagnostic centers, however, are set to narrow the gap, advancing at 7.68% CAGR as automated instruments and reagent-rental models reduce up-front cost. Pharma and biotech continue to rely on HRM for companion-diagnostic development, but their share of tests stabilizes near 16% because trial volumes fluctuate yearly. Emerging-market public-health agencies represent an untapped segment as surveillance funding rises; early pilots in Southeast Asia already process 250,000 HRM reactions annually for dengue and influenza typing, and the figure is projected to double by 2027.

Geography Analysis

North America produced 41.10% of global revenue in 2025, underpinned by well-funded reference labs, payer policies that cover actionable gene-drug pairs, and a consolidated supplier base that offers nationwide service contracts. The region’s demand is also buoyed by high companion-diagnostic trial activity, which funnels large volumes into contract research organizations equipped with fully automated HRM suites. Workforce shortages remain a challenge; US lab-technologist vacancy rates surpassed 46% in 2024, prompting networks to adopt instruments with walk-away workflows that minimize human intervention.

Asia-Pacific is the fastest-growing territory, projected at a 5.35% CAGR through 2031, propelled by universal-health-coverage programs and government-funded genomic initiatives such as Australia’s USD 500.1 million Genomics Health Futures Mission. China’s hospital-procurement reforms, which favor cost-effective domestic diagnostics, are encouraging local joint ventures that bundle HRM instruments with government-approved reagent menus. Mobile point-of-care pilots in India and the Philippines showcase cartridge-based HRM tests that run off battery packs, broadening access in regions lacking central labs.

Europe commands solid demand thanks to a dense network of academic medical centers and a supportive reimbursement climate for pharmacogenomics. The EU Medical Device Regulation harmonizes post-market surveillance, aiding suppliers in launching pan-European HRM kits. Hospitals in Germany and France are integrating cloud-based analytics that route anonymized melt-curve data into national bio-bank repositories, accelerating translational research links between genomic findings and therapy outcomes.

Middle East & Africa and South America collectively capture under 10% of revenue but record double-digit test-volume growth as infectious-disease programs seek rapid genotyping to guide outbreak response. Deployment of HRM-equipped mobile vans during the 2024 Rift Valley fever outbreak in Kenya cut sample processing times from five days to same day, reinforcing demand for ruggedized platforms in remote regions.

Competitive Landscape

The high-resolution melting analysis market displays moderate fragmentation. Global leaders such as Thermo Fisher Scientific, QIAGEN, and Roche leverage broad reagent portfolios, service networks, and cloud infrastructures, enabling them to capture high-volume hospital contracts. Mid-tier specialists like Bio-Rad and New England Biolabs target niche applications, offering customizable master mixes and digital-PCR extensions that appeal to research institutes and biotech innovators. Recent consolidation—exemplified by bioMérieux’s EUR 111 million acquisition of SpinChip Diagnostics—signals a trend toward integrated point-of-care ecosystems that merge rapid immunoassay readouts with HRM confirmation.

Technology differentiation pivots on automation, connectivity, and AI-assisted interpretation. Vendors embedding AI melt-curve analysis report 20-30% higher throughput due to fewer manual reviews, a key selling point for understaffed labs. Instrument-as-a-service contracts, combining hardware, reagents, cloud analytics, and uptime guarantees for a per-test fee, are gaining traction among health systems migrating to outcome-based purchasing. Meanwhile, open-architecture players invite third-party assay developers, expanding menu breadth without inflating internal R&D spend.

Emerging competitors from Asia focus on rugged, low-maintenance instruments priced 25-40% below incumbent offerings, targeting fast-growing decentralized settings. Western suppliers respond with scaled-down models and strategic manufacturing partnerships to maintain share in value-sensitive markets. With AI, digital PCR, and cloud-connectivity waves converging, vendor success will hinge on seamlessly integrating these capabilities while managing per-test economics and regulatory complexity across jurisdictions.

High-Resolution Melting Analysis Industry Leaders

Thermo Fisher Scientific, Inc.

Bio-Rad Laboratories, Inc.

F. Hoffman-La Roche Ltd.

Qiagen N.V.

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Illumina unveiled multiomic technologies that map rare-disease variants and methylation in a single run, slated for 2026 release to widen access to high-resolution analyses.

- January 2025: bioMérieux finalized a EUR 111 million purchase of SpinChip Diagnostics, adding blood-based immunoassays delivering 10-minute results to its point-of-care lineup.

- January 2025: Roche obtained FDA clearance for the VENTANA Kappa/Lambda Dual ISH Probe Cocktail, a one-slide assay covering over 60 lymphoma subtypes, streamlining diagnosis.

- November 2024: Agilent reorganized into the Life Sciences and Diagnostics Markets Group, representing 38% of revenue, to sharpen focus on pharma, clinical, and diagnostic customers.

- November 2024: Illumina expanded its TruSight Oncology suite with TSO 500 v2, promising quicker turnaround and superior variant calling for comprehensive genomic profiling.

- September 2024: QIAGEN added 100+ validated assays to the QIAcuity digital-PCR platform, strengthening mutation-detection and copy-number applications ahead of planned clinical launches.

Global High-Resolution Melting Analysis Market Report Scope

HRM analysis is a relatively new, post-PCR analysis method used to identify variations in nucleic acid sequences. The method is based on detecting small differences in PCR melting curves. It is enabled by improved dsDNA-binding dyes used in conjunction with real-time PCR instrumentation, precise temperature ramp control, and advanced data capture capabilities.

The High-Resolution Melting Analysis Market is Segmented by Product and Service (Reagents and Consumables, Instruments, Software, and Services), Application (SNP Genotyping, Mutation Discovery, Pathogen Identification, and Other Applications), End-user (Research Laboratories and Academic Institutes, Pharmaceutical and Biotechnology Companies, and Other End-users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments.

| Reagents & Consumables | Intercalating Dyes |

| Master Mixes | |

| DNA Standards & Controls | |

| Instruments | Real-time PCR Systems |

| Digital PCR Systems (HRM-enabled) | |

| Compact POC Devices | |

| Software & Services | Melt-curve Analysis Software |

| Cloud-based Analytics & AI Services | |

| Validation & Training Services |

| SNP Genotyping |

| Mutation Discovery |

| Pathogen Identification |

| Methylation Analysis |

| Other Applications |

| Research Laboratories & Academic Institutes |

| Pharmaceutical & Biotechnology Companies |

| Hospitals & Diagnostic Centers |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product & Service | Reagents & Consumables | Intercalating Dyes |

| Master Mixes | ||

| DNA Standards & Controls | ||

| Instruments | Real-time PCR Systems | |

| Digital PCR Systems (HRM-enabled) | ||

| Compact POC Devices | ||

| Software & Services | Melt-curve Analysis Software | |

| Cloud-based Analytics & AI Services | ||

| Validation & Training Services | ||

| By Application | SNP Genotyping | |

| Mutation Discovery | ||

| Pathogen Identification | ||

| Methylation Analysis | ||

| Other Applications | ||

| By End-user | Research Laboratories & Academic Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Hospitals & Diagnostic Centers | ||

| Other End-users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected revenue for the High-Resolution Melting Analysis market in 2031?

Global revenue is forecast to reach USD 355.79 million by 2031, reflecting a 4.26% CAGR over 2026-2031.

Which region is growing fastest for High-Resolution Melting Analysis?

Asia-Pacific is projected to record the highest 5.35% CAGR through 2031 due to expanded healthcare access and government-backed genomic programs.

Which application segment currently leads High-Resolution Melting Analysis demand?

SNP genotyping leads with 38.01% of 2025 revenue, driven by widespread pharmacogenomic testing.

Why are hospitals adopting High-Resolution Melting Analysis more rapidly now?

Automated instruments and reagent-rental models reduce upfront costs and staffing needs, allowing hospitals to integrate rapid genotyping into routine workflows.

How are vendors addressing the shortage of skilled lab personnel?

Suppliers embed AI-assisted melt-curve interpretation and cloud analytics, cutting manual review time and enabling walk-away operation in understaffed labs.

What recent acquisition highlights consolidation in High-Resolution Melting Analysis?

BioMérieux’s EUR 111 million purchase of SpinChip Diagnostics strengthens its point-of-care capabilities and signals ongoing market consolidation.

Page last updated on: