EClinical Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

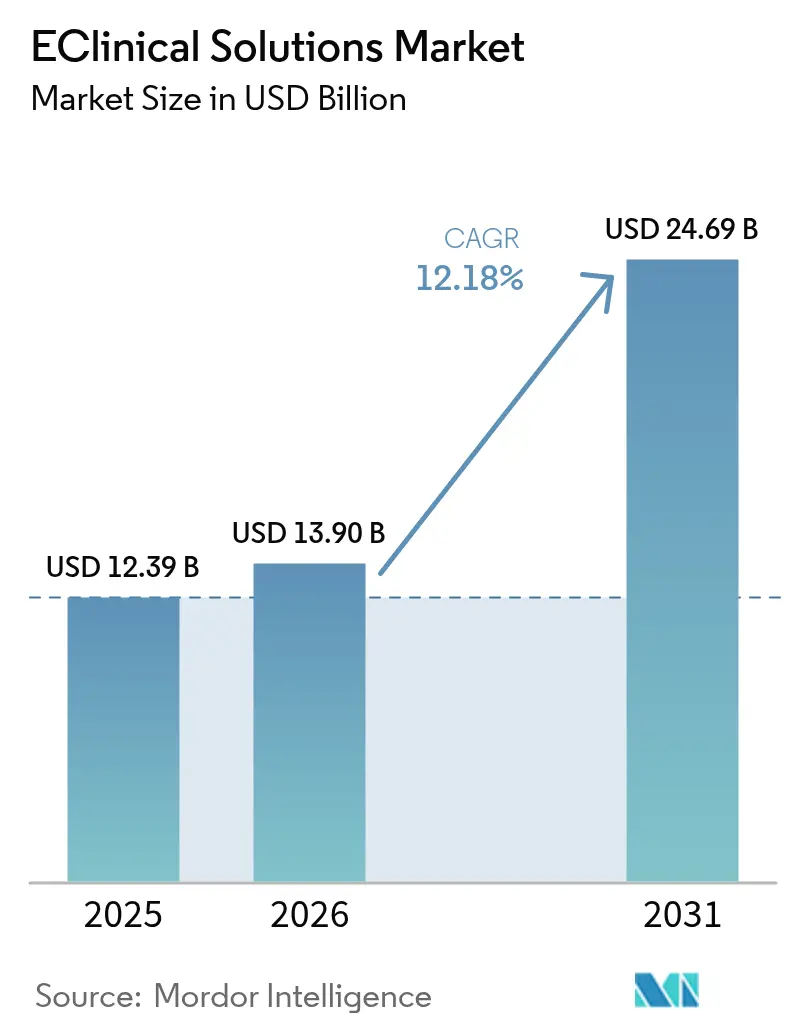

| Market Size (2026) | USD 13.90 Billion |

| Market Size (2031) | USD 24.69 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

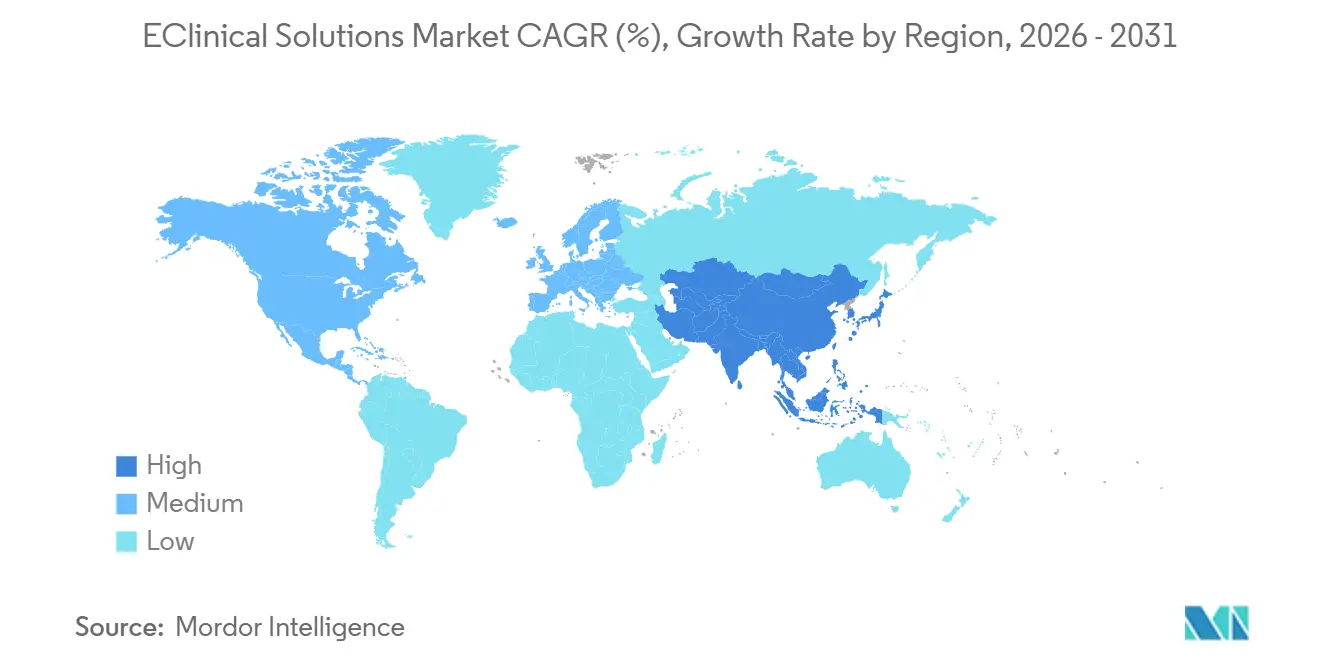

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EClinical Solutions Market Analysis by Mordor Intelligence

The eClinical solutions market size is expected to grow from USD 12.39 billion in 2025 to USD 13.9 billion in 2026 and is forecast to reach USD 24.69 billion by 2031 at 12.18% CAGR over 2026-2031. The run-rate shows how fully digital trial execution has shifted from an optional efficiency play to a core requirement for competitive drug development. Sponsors now transmit larger, multi-modal data sets across more global sites and face tighter disclosure windows, making sophisticated capture, monitoring, and analytics systems indispensable. Near-real-time connectivity has become even more valuable as decentralized and hybrid trials move from emergency workaround to mainstream design, accelerating demand for unified platforms that connect participants, monitors, statisticians, and regulators. As Tier-1 vendors bundle electronic data capture (EDC), electronic clinical outcome assessment (eCOA), randomization and trial-supply management (RTSM), and safety reporting under single contracts, pricing dynamics favor subscription models that match study life cycles and support slimmer biotech budgets, implying that platform completeness rather than lowest point cost will decide future purchasing.

Key Report Takeaways

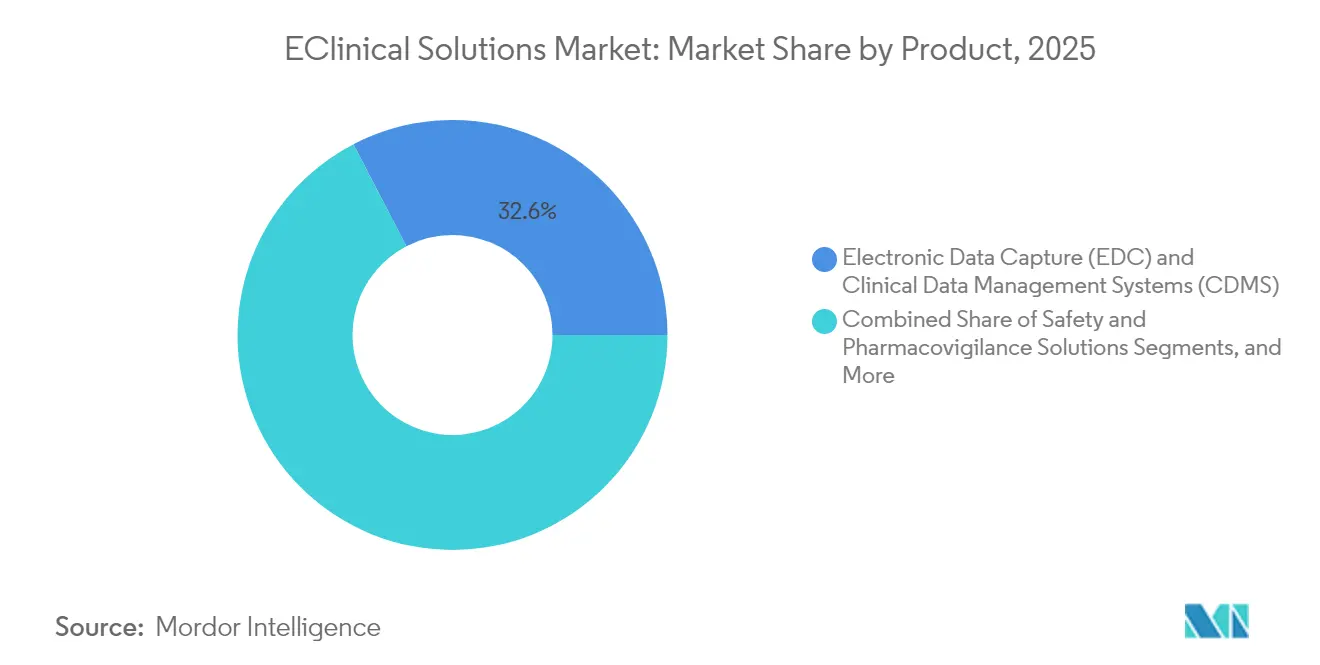

- By product, electronic data capture and clinical data management systems led with a 32.62% eClinical solutions market share in 2025, while electronic clinical outcome assessment platforms are projected to expand at a 14.79% CAGR to 2031.

- By delivery mode, cloud-based deployments accounted for 48.05% of the eClinical solutions market size in 2025 and are advancing at a 14.21% CAGR through 2031.

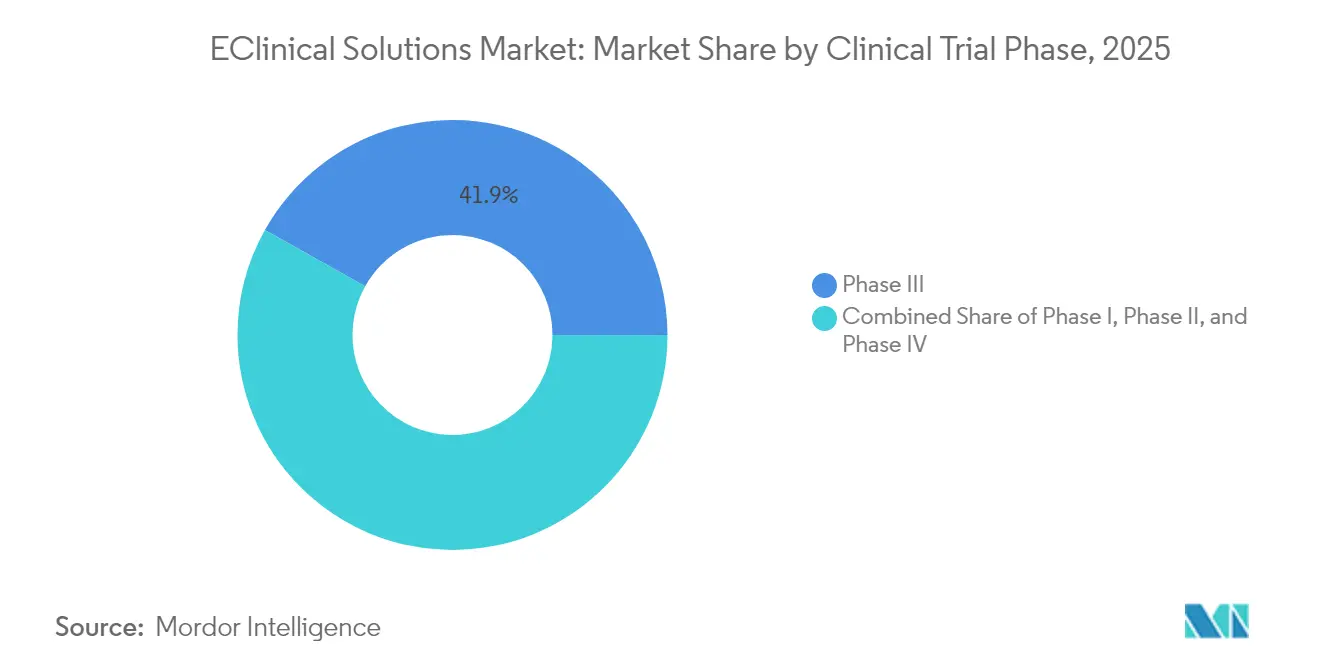

- By clinical trial phase, Phase III captured 41.88% of the eClinical solutions market share in 2025, whereas Phase I revenue is set to grow at 13.33% CAGR between 2026 and 2031.

- By end-user, pharmaceutical and biotechnology companies held 59.40% of 2025 revenue, but contract research organisations are expected to post the fastest 13.12% CAGR through 2031.

- Regionally, North America contributed 48.62% of 2025 revenue, yet Asia-Pacific is forecast to notch a 14.46% CAGR to 2031, the highest of any geography.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EClinical Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enormous data mounting from healthcare industry | +3.2% | Global, early gains in North America & Europe | Medium term (2-4 years) |

| Growing incorporation of software solutions in clinical trial | +2.8% | Global | Short term (≤ 2 years) |

| Growing biopharma R&D investment | +2.1% | North America, Europe; emerging Asia-Pacific | Medium term (2-4 years) |

| Rapid shift toward patient-centric and decentralized models | +2.6% | Global, early gains in North America | Short term (≤ 2 years) |

| Expansion of global clinical trial activities | +1.9% | Asia-Pacific, Latin America, Eastern Europe | Long term (≥ 4 years) |

| Surge in Phase II/III Oncology Trials in APAC Requiring Scalable Cloud Platforms | +1.2% | Global, early gains in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Enormous Data Mounting from Healthcare Industry

The volume of trial data has climbed steeply, prompting sponsors to embed automated quality checks, natural-language processing, and predictive analytics directly inside core EDC platforms. IQVIA reports that AI-driven review of unstructured sources halves data-cleaning cycles while preserving audit readiness. In turn, data-science teams are now engaged during protocol build, not merely after first-patient-in, ensuring downstream interoperability. Cloud storage budgets therefore outpace on-premise outlays as elastic capacity overtakes hardware purchase cycles. Oncology studies provide the blueprint: once niche, their analytics frameworks now replicate across inflammatory and metabolic pipelines. As data per subject multiplies, the eClinical solutions market gains a stable tailwind that is independent of therapeutic area focus.

Growing Incorporation of Software Solutions in Clinical Trial

Sponsors routinely juggle three or more discrete eClinical applications per study, yet fragmented log-ins and unsynchronized data flows have become a clear bottleneck. Veeva’s 2025 roadmap showcases rising demand for single sign-on environments that merge start-up, monitoring, and submission workflows [1]Veeva, “Unified Clinical Operations Roadmap 2025,” Veeva, veeva.com. Early adopters report materially shorter protocol-finalization cycles because duplicate data entry disappears between modules, reducing validation cost as well. Consolidated suites now outperform best-of-breed purchasing, allowing governance teams to shift head-count from manual queries to advanced statistical programming. The observable outcome is a rise in multiyear platform contracts, which converts sporadic license spend into predictable SaaS revenue inside the eClinical solutions market.

Growing Biopharma R&D Investment

Global R&D budgets keep rising in nominal terms, and a larger slice is funneled into digital infrastructure that can handle adaptive, basket, and biomarker-driven protocols. LLR Partners logged a strong uptick in venture funding for vendors embedding machine-learning inside safety surveillance tools, demonstrating that investors see enduring returns in this niche. Sponsors piloting those tools confirm reduced regulatory queries because real-time signal detection surfaces adverse events early. Precision-medicine trials further amplify demand because each additional biomarker multiplies data points per participant, raising the marginal value of automated data pipelines. Collectively, these factors encourage CFOs to protect software budgets even when molecule investment slows, sustaining the eClinical solutions market.

Rapid Shift Toward Patient-Centric and Decentralized Models

Remote trial oversight, first forced by pandemic restrictions, has proved so effective that hybrid designs are now mainstream in Phase II and Phase III studies. Medable shows that dynamic eConsent and configurable eCOA libraries can be created in minutes, compressing first-patient-in timelines by double-digit days. Participants experience fewer site visits, boosting retention and cutting recruitment costs. Investigative centers that embraced remote monitoring early report larger outsourced volumes, hinting at an emerging competitive edge for digitally mature sites. The ripple effect runs through the eClinical solutions market as sponsors demand platforms that integrate secure telehealth, real-time data capture, and immediate safety reporting.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs | −1.4% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Shortage of certified clinical data managers in emerging markets | −0.8% | Asia-Pacific, Latin America, Middle East | Medium term (2-4 years) |

| Escalating cyber-security and patient-data breach concerns | −1.2% | Global | Short term (≤ 2 years) |

| Data Interoperability Gaps Between Legacy & Modern eClinical Modules | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs

Comprehensive platform roll-outs frequently require budgets well into seven figures once validation, integration, and multi-user training are considered. Merative benchmarks show that sponsors with tight treasury adopt phased deployment, starting with a core EDC and layering RTSM or eTMF later. While the staged path trims initial outlay, it extends project timelines, delaying productivity gains that full suites deliver. Vendors offering flexible, consumption-based pricing therefore capture accounts that might otherwise postpone digitization. Nevertheless, high entry costs still weigh on smaller biotech and academic sponsors, tempering eClinical solutions market growth in resource-constrained settings.

Shortage of Certified Clinical Data Managers in Emerging Markets

Rapid trial volume growth in Asia-Pacific and Latin America has highlighted a shortage of staff skilled in CDISC standards and advanced statistical programming. Sponsors increasingly route complex tasks to global hubs while limiting on-site roles to patient engagement. IQVIA’s pharmacovigilance upskilling initiative shows how vendor-provided curricula partially close skills gaps and improve retention. In the interim, platforms with embedded automation and guided workflows compensate for limited human expertise, but skill scarcity still slows onboarding speed and dampens regional contribution to the eClinical solutions market.

Escalating Cyber-security & Patient-Data Breach Concerns

Healthcare faced a rise in cyber incidents during 2024, pushing secure architectures to the top of board agendas. Peer-reviewed studies of blockchain pilots confirm that immutable audit trails can deter tampering across multi-site trials [2]National Institutes of Health, “Blockchain for Clinical Trial Data Integrity,” NIH, pubmed.ncbi.nlm.nih.gov . Vendors now embed zero-trust frameworks, tokenization, and continuous penetration testing by default. Although early certification under proposed AI-in-trials guidance offers reassurance, breach anxiety lengthens procurement cycles, reducing near-term velocity in the eClinical solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Electronic Data Capture Dominance Amid Fast-Growing eCOA Adoption

Electronic data capture and clinical data management systems controlled the largest eClinical solutions market size in 2025, contributing 32.62% of total revenue on the strength of universal deployment at study start-up. License renewals remain high because sponsors prize system familiarity and integrated risk-based monitoring dashboards that flag anomalies before interim analysis. The market now values embedded predictive queries more than basic data entry, creating a shift toward AI-infused upgrades that command premium pricing. Vendors that pre-integrate EDC with RTSM and safety modules further raise switching costs, cementing leadership positions.

Electronic clinical outcome assessment platforms represent the fastest expanding subsegment, expected with 14.79% CAGR through 2031 as patient centricity moves from rhetoric to requirement. Medable’s instrument builder allows drag-and-drop creation of psychometric and quality-of-life tools that feed directly into EDC tables without manual mapping. Sponsors appreciate the seamless handoff because it cuts reconciliation cycles by weeks and supports real-time dashboard review. As decentralized trials proliferate, eCOA functionality often decides overall platform selection, nudging incremental revenues toward full-suite vendors inside the eClinical solutions market.

By Delivery Mode: Cloud Ascendance with Web-Hosted Niches

Cloud-based deployments captured the largest eClinical solutions market share by delivery mode in 2025 at 48.05% and are projected to post a 14.21% CAGR to 2031. Multi-tenant SaaS models offer immediate scalability, automatic version upgrades, and audit logs that regulators increasingly deem equivalent to on-premise controls. Sponsors migrating from owned hardware document double-digit reductions in maintenance hours, freeing IT teams for analytics work. Lower entry cost also helps smaller biotech sponsors keep cash burn aligned with trial milestones, reinforcing cloud traction.

Web-hosted, single-tenant environments maintain a resilient mid-thirty-percent share, acting as a transitional option for organizations reluctant to jump straight to multi-tenant architecture. These environments still offload infrastructure ownership yet provide perceived isolation that risk-averse quality groups favor. Recent advances in tenant-level encryption and dedicated-key management, however, narrow the security gap between web-hosted and SaaS. Over the forecast horizon, some displacement toward multi-tenant offerings is likely, but conservative sponsors will preserve a viable niche that sustains web-hosted vendors within the eClinical solutions market.

By Clinical Trial Phase: Phase III Scale Meets Phase I Momentum

Phase III programs accounted for 41.88% of the eClinical solutions market size in 2025 and remain the single largest revenue pool because late-stage trials span continents and manage high patient loads. The complexity demands enterprise-grade platforms with granular site monitoring, safety surveillance, and regional regulatory templates. Rising per-patient costs in Phase III subtly drive digital investment because sponsors look to recover savings via operational efficiency.

Phase I studies show the fastest revenue trajectory, forecast to grow 13.33% CAGR as first-in-human cell and gene therapies multiply. Signant Health’s early-phase toolkit consolidates eConsent, randomization, and pharmacy management, shortening set-up windows and aligning seamlessly with adaptive dose-escalation protocols. Early adoption in Phase I often cements vendor preference that carries into Phases II and III, delivering a customer-lifecycle dividend to platform providers. These dynamics ensure that upstream growth complements the downstream heft of Phase III inside the eClinical solutions market.

By End-User: Pharma & Biotech Scale Versus CRO Agility

Pharmaceutical and biotechnology companies held 59.40% of 2025 revenue, leveraging robust internal R&D pipelines and strategic digital transformation mandates. Selection criteria now emphasize AI readiness, lineage tracking, and configurability that supports complex biomarker studies. Larger enterprises favor bundled contracts that consolidate systems under unified governance and shorten validation cycles, expanding average order values for Tier-1 suppliers.

Contract research organisations constitute the fastest-growing customer group, posting 13.12% CAGR to 2031 as sponsors continue to outsource both operations and analytics. Leading CROs deploy proprietary overlays atop partner platforms, differentiating services and capturing incremental revenue per protocol. Because many biotech companies follow CRO technology recommendations, vendor reach amplifies through outsourcing channels, augmenting total addressable revenue in the eClinical solutions market.

Geography Analysis

North America retained the largest eClinical solutions market size in 2025, contributing 48.62% of global revenue due to deep capital pools, early regulatory acceptance of digital signatures, and dense clusters of experienced investigative sites. Vendors often launch new AI modules first in the United States and Canada because local data-governance norms support rapid iteration. Despite market maturity, double-digit renewal growth persists as sponsors migrate legacy on-premise deployments to SaaS and pursue advanced analytics that speed inspection readiness.

Asia-Pacific represents the fastest growth trajectory, set to register a 14.46% CAGR through 2031 as global sponsors shift recruitment eastward to access large patient pools and cost-efficient site networks. Governments in China, South Korea, and India actively champion domestic biopharma, funding cloud infrastructure grants that reduce implementation hurdles. Regional vendors fine-tune interfaces to local languages and privacy statutes, increasing competitive pressure on Western incumbents and diversifying the supplier base inside the eClinical solutions market.

Europe commands roughly one-quarter of worldwide revenue and benefits from harmonization under the EU Clinical Trials Regulation, which streamlines multi-country submissions. The region’s stringent data-privacy rules function as a proving ground for security features that later roll out globally. Germany, the Nordics, and the Netherlands exhibit rising adoption of electronic patient diaries and eConsent, signaling cultural receptivity to patient-facing technology. High regulatory oversight lengthens sales cycles yet boosts long-term contract values because sponsors embed compliance commitments within platform scopes.

Competitive Landscape

The five largest vendors control about 45% of global revenue, indicating moderate concentration and leaving ample opportunity for mid-tier disruptors. Oracle and Veeva epitomize a full-suite strategy designed to minimize integration points for large sponsors. IQVIA capitalizes on its data-curation heritage to offer life-cycle partnerships that encompass design, execution, and post-marketing, blurring lines between technology vendor and CRO.

Strategic acquisitions redefine product breadth and regional reach at a brisk pace. GI Partners’ majority investment in eClinical Solutions demonstrates private-equity appetite for AI-centric assets that can scale quickly [3]eClinical Solutions, “GI Partners Investment Announcement,” eclinicalsol.com . Charles River’s Apollo expansion suggests pre-clinical CROs are moving upstream into digital trial oversight, teeing up convergence across R&D stages. Deal flow favors companies with proprietary AI engines that shorten data management timelines and deliver measurable cycle-time savings.

Technology differentiation in the eClinical solutions market revolves around embedded AI that automates data cleaning, anomaly detection, and patient matching. ArisGlobal’s natural-language generation for safety narratives replaces manual medical writing, freeing scarce pharmacovigilance resources for higher-order analysis. Vendors that deliver transparent algorithm audit trails and ethical-AI attestations gain procurement preference, reinforcing a virtuous loop where operational wins fund further innovation.

EClinical Solutions Industry Leaders

Oracle Corporation

Veeva Systems

Mednet Solutions

PAREXEL International (Calyx)

Saama Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Argenx SE expands adoption of the elluminate Clinical Data Cloud to enhance clinical data processes, reflecting growing traction among global immunology leaders.

- February 2026: AI & RBQM focus intensifies investments in agentic AI and risk-based quality management (RBQM), aiming to improve efficiency across clinical development.

- December 2025: AI Agents Launch: Introduced elluminate AI agents embedded across four pillars Data Mapping, Data Review, RBQM, and Study Operations bringing explainable intelligence and governed data to clinical trials.

Global EClinical Solutions Market Report Scope

As per the scope of the report, eClinical is a term used within the biopharmaceutical domain. eClinical solutions manage the clinical technologies and expertise to accelerate clinical development.

The market is segmented by product type (clinical data management systems (CDMS), clinical trial management systems (CTMS), randomization and trial supply management, electronic data capture (EDC), electronic clinical outcome assessments (eCOA), and electronic patient-reported outcomes (ePRO), clinical analytics platforms, electronic trial master file (eTMF), and other product types), by deployment mode (cloud-based eClinical solutions and on-premise eClinical solutions) by end-user, (pharmaceutical and biotechnology companies, contract research organizations (CROs), and other end users)by geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across significant regions globally. The report offers the value (USD) for the above segments.

| Electronic Data Capture (EDC) & Clinical Data Management Systems (CDMS) |

| Clinical Trial Management Systems (CTMS) |

| Randomization & Trial Supply Management (IRT/RTSM) |

| Electronic Clinical Outcome Assessment (eCOA/ePRO) |

| Clinical Analytics & Data-Integration Platforms |

| Safety & Pharmacovigilance Solutions |

| Electronic Trial Master File (eTMF) |

| Other Products |

| Cloud-based (SaaS) |

| Web-hosted (On-Demand) |

| On-premise |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Medical Device Manufacturers |

| Academic & Research Institutions |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| South Africa | |

| Rest of Middle East | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Electronic Data Capture (EDC) & Clinical Data Management Systems (CDMS) | |

| Clinical Trial Management Systems (CTMS) | ||

| Randomization & Trial Supply Management (IRT/RTSM) | ||

| Electronic Clinical Outcome Assessment (eCOA/ePRO) | ||

| Clinical Analytics & Data-Integration Platforms | ||

| Safety & Pharmacovigilance Solutions | ||

| Electronic Trial Master File (eTMF) | ||

| Other Products | ||

| By Delivery Mode | Cloud-based (SaaS) | |

| Web-hosted (On-Demand) | ||

| On-premise | ||

| By Clinical Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End-user | Pharmaceutical & Biotechnology Companies | |

| Contract Research Organizations (CROs) | ||

| Medical Device Manufacturers | ||

| Academic & Research Institutions | ||

| Other End-users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| South Africa | ||

| Rest of Middle East | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the eClinical Solutions Market?

The eClinical Solutions Market size is expected to reach USD 13.9 billion in 2026 and grow at a CAGR of 12.18% to reach USD 24.69 billion by 2031.

Why does cloud deployment lead adoption in the eClinical solutions market?

Multi-tenant SaaS platforms cut hardware spend, provide instant scalability, and meet regulatory audit needs, driving 48.05% revenue share in 2025.

Who are the key players in eClinical Solutions Market?

Oracle Corporation, Veeva Systems, Mednet Solutions, PAREXEL International (Calyx) and Saama Technologies, Inc. are the major companies operating in the eClinical Solutions Market.

Which is the fastest growing region in eClinical Solutions Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in eClinical Solutions Market?

In 2025, the North America accounts for the largest market share in eClinical Solutions Market.

Page last updated on: