Healthcare Education Solution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

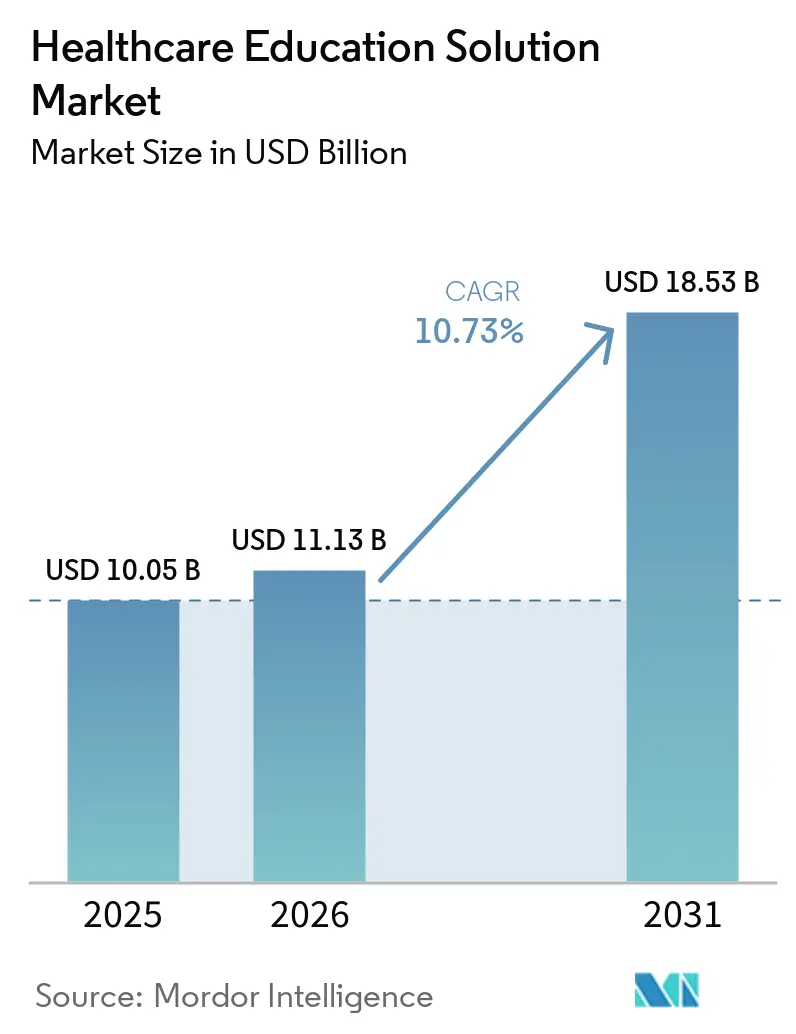

| Market Size (2026) | USD 11.13 Billion |

| Market Size (2031) | USD 18.53 Billion |

| Growth Rate (2026 - 2031) | 10.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

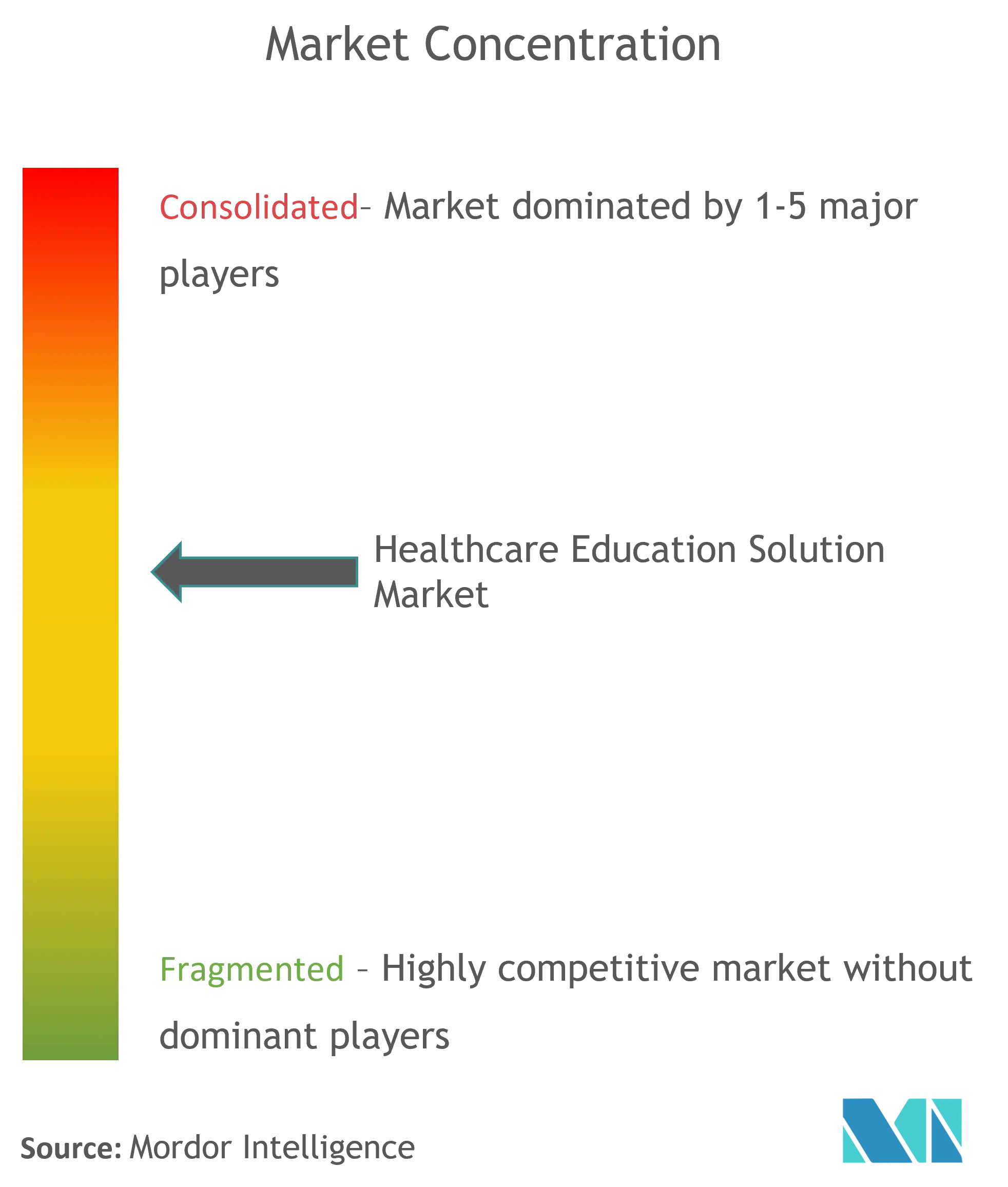

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Education Solution Market Analysis by Mordor Intelligence

Healthcare education solution market size in 2026 is estimated at USD 11.13 billion, growing from 2025 value of USD 10.05 billion with 2031 projections showing USD 18.53 billion, growing at 10.73% CAGR over 2026-2031. A confluence of clinical faculty shortages, expanding continuing‐education mandates, and the rapid digitization of hospital workflows drives sustained demand for scalable learning platforms. North America leads in dollar terms because of stringent compliance frameworks and mature infrastructure, yet Asia-Pacific records the fastest regional growth, supported by large-scale investments in medical schools and public-health modernization programs. Software platforms remain the dominant component because cloud‐hosted learning management systems (LMS) are readily deployable across multi-site networks, while services grow fastest as institutions seek custom content, analytics, and integration expertise. Technology adoption patterns reveal a shift from one-off e-learning modules toward predictive, AI-enabled ecosystems that support just-in-time, point-of-care up-skilling for nurses, physicians, and allied health professionals.

Key Report Takeaways

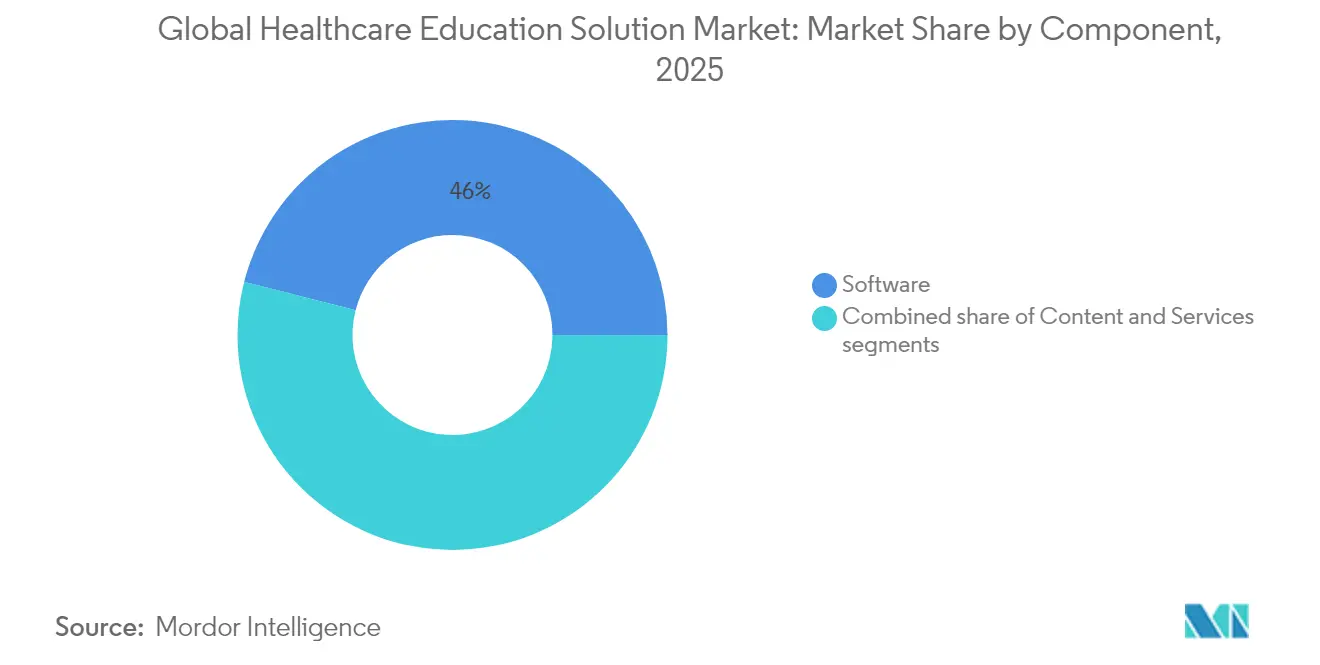

- By component, software platforms accounted for 46.02% of the healthcare education solution market share in 2025, whereas services registered the highest projected CAGR at 11.31% through 2031.

- By delivery mode, e-learning held 54.65% of the healthcare education solution market size in 2025, while simulation-based training is advancing at a 12.12% CAGR over the forecast horizon.

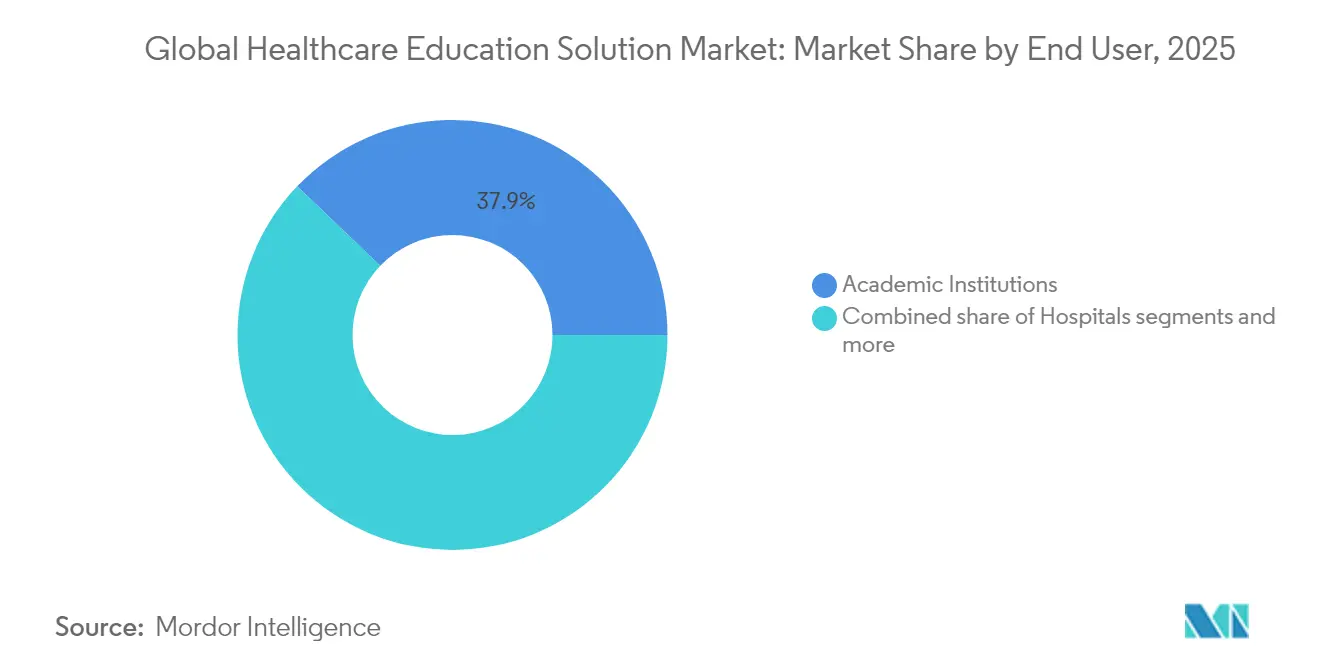

- By end user, academic institutions led with 37.85% revenue share in 2025; hospitals record the fastest growth at an 10.94% CAGR through 2031 as point-of-care learning becomes routine.

- By technology, learning management systems secured 53.21% share of the healthcare education solution market size in 2025, whereas digital-twin simulations expand at a 10.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Education Solution Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-learning adoption to alleviate clinical faculty shortages | +2.8% | Global; highest impact in North America and Europe | Medium term (2-4 years) |

| Government-mandated CME requirements expanding globally | +2.1% | Global; accelerated uptake in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Digitization of hospital workflows integrating training modules | +1.9% | North America and EU leading; Asia-Pacific core following | Medium term (2-4 years) |

| Rapid uptake of AR/VR simulators for high-risk procedures | +1.7% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Emergence of digital-twin patient data sets for scenario-based learning | +1.4% | Global early adoption in developed markets | Long term (≥ 4 years) |

| Micro-credential subscription platforms for allied health workers | +1.1% | Global; strong in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Learning Adoption to Alleviate Clinical Faculty Shortages

Healthcare schools increasingly deploy large-scale e-learning suites to compensate for faculty gaps that limit enrolment capacity. A systematic review covering 6,750 students across multiple health disciplines showed online modules can match or exceed traditional methods in knowledge and skills acquisition. Institutions therefore channel budget toward cloud‐hosted LMS packages with adaptive algorithms that personalize content based on competency analytics. The model is particularly valuable in nursing, where global shortages demand an additional 9 million professionals by 2030. Self-paced digital curricula let a small instructor pool supervise larger cohorts without compromising accreditation standards. Furthermore, asynchronous modules help rural learners balance shift duties with study, reinforcing the healthcare education solution market’s relevance in workforce distribution.

Government-Mandated CME Requirements Expanding Globally

Regulators now require ongoing certification to maintain licenses, spurring demand for platforms that automate credit tracking and multi-jurisdiction reporting. In the United States, the Medication Access and Training Expansion Act obliges providers to complete 8 hours of substance-use-disorder education for DEA renewal. State boards add layers of complexity, with annual hour requirements ranging from 25 to 50 depending on jurisdiction. Internationally, updated standards from the World Federation for Medical Education shift the focus from credit counts to competency-based assessments. Vendors respond by embedding granular analytics that map completed activities to specific skills frameworks, a feature that secures hospital procurement where cross-border physician recruitment is rising. These changes solidify the healthcare education solution market as a compliance backbone for mobile clinical workforces.

Digitization of Hospital Workflows Integrating Training Modules

EHR and clinical-decision-support vendors are embedding micro-learning objects directly into workflow screens, turning education into a continuous background process that improves patient safety. Wolters Kluwer’s Lippincott CoursePoint+ now leverages machine-learning to nudge nurses toward remediation modules when dashboard metrics flag proficiency gaps. Hospitals report shorter orientation periods and lower turnover when bedside devices deliver competency refreshers that relate to current caseloads. Newly hired nurse educators, often transitioning from direct care, find such embedded systems mitigate the lack of formal teaching infrastructure highlighted in qualitative studies[1]Source: BMC Nursing, “Challenges Faced by Newly Employed Nurse Educators,” bmcnurs.biomedcentral.com . As clinical documentation tools become central to care delivery, integrated instruction elevates both staff confidence and quality metrics, reinforcing the healthcare education solution market’s importance in value-based‐care ecosystems.

Rapid Uptake of AR/VR Simulators for High-Risk Procedures

Mixed-reality platforms deliver risk-free rehearsal environments that replicate complex anatomy with haptic feedback. VirtaMed’s ArthroS aligns with ACGME Milestones 2.0 and lets orthopedic residents achieve baseline arthroscopy competence before first live cases. Specialty societies now mandate simulator experience in credentialing pathways, and mobile units such as the Arthroscopy Association of North America’s MAAS trailer bring advanced training to community programs. A systematic review of 17 studies reported significant gains in spatial understanding and procedural accuracy when VR replaced didactic labs in resource-limited settings. Cost concerns are mitigated by subscription access models that spread hardware outlays across cohorts, making immersive simulation a mainstream pillar of the healthcare education solution market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced simulation systems | -1.8% | Global; most acute in emerging markets and small colleges | Short term (≤ 2 years) |

| Bandwidth limitations in low-income regions | -1.2% | Sub-Saharan Africa, rural Asia-Pacific, parts of Latin America | Medium term (2-4 years) |

| Accreditation lag for AI-generated course content | -0.9% | Global; regulatory variations by region | Long term (≥ 4 years) |

| IP litigation over 3-D anatomical model libraries | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Simulation Systems

Immersive simulators require specialized hardware, ongoing content updates, and technical support, placing pressure on budgets at smaller schools. Capital price tags can reach USD 500,000 for fully integrated suites, and maintenance contracts add recurring commitments that compete with essential facility spending. A multi-country survey of Southeast-Asian hospital leaders found that more than half cite staff expertise gaps and data-security concerns alongside pure cost when delaying simulator adoption. Financing innovations such as equipment leasing and pay-per-student cloud rendering lower initial barriers, yet disparities remain. Without equal access, the digital divide widens between urban teaching hospitals and rural institutes, tempering the healthcare education solution market’s near-term penetration.

Bandwidth Limitations in Low-Income Regions

High-definition video and VR assets strain networks where connectivity is patchy. Telemedicine programs in rural India illustrate both the possibilities and bottlenecks: while satellite links expand reach, speed fluctuations limit synchronous instruction. A systematic review of digital-health deployments in Somalia echoes similar infrastructure deficits that impede platform roll-out. Content providers respond with offline-capable mobile apps and compressed media, yet these formats often sacrifice immersive fidelity. As a result, clinicians in bandwidth-constrained zones rely on text-centric microlearning delivered via low-cost smartphones, delaying exposure to advanced simulation experiences and capping the healthcare education solution market’s growth curve in underserved geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integration Demand Elevates Services

Software platforms hold a 46.02% share of the healthcare education solution market thanks to multi-tenant LMS offerings that centralize curriculum governance and learner analytics. These systems scale horizontally across university consortia and vertically inside hospital networks, underpinning credential management, skills mapping, and performance dashboards. Institutions increasingly plug AI-powered recommendation engines into the core stack, raising engagement rates by tailoring pathways to user proficiency levels. Despite platform dominance, the services segment grows at an 11.31% CAGR because configuration, content localization, and API integration require specialized know-how. Hospitals deploying virtual simulators often enlist consultants to embed outcome metrics in electronic health‐record (EHR) workflows, illustrating why services revenue accelerates faster than license fees. As compliance standards evolve, expert support around audit readiness and data-privacy governance further elevates billable engagement, solidifying services as a pivotal growth vector in the healthcare education solution market.

Creating high-quality, evidence-based courseware remains a competitive differentiator because curriculum rigor underpins institutional reputation. Content teams co-develop modules with academic societies to ensure alignment with updated competency frameworks. Simultaneously, AI generators draft item banks and clinical scenarios at scale, but accreditation authorities still demand human review before publication. The resulting hybrid editorial processes intensify demand for instructional-design consultants, reinforcing the services segment’s momentum. Over the forecast horizon, co-development partnerships between publishers and healthcare systems are expected to mature into joint ventures that bundle platform licenses with continuous content refresh agreements, embedding recurring revenue across the healthcare education solution market.

By Delivery Mode: Simulation-Based Learning Gains Momentum

E-learning retains the largest slice of the delivery-mode landscape, commanding 54.65% of the healthcare education solution market share because asynchronous modules cost-effectively disseminate foundational theory across dispersed cohorts. Standardized recordings and quizzes support uniform knowledge transfer, ensuring compliance with regulatory competencies. Yet the fastest-growing format is simulation-based training, expanding at a 12.12% CAGR as high-risk specialties insist on procedural practice before live patient exposure. Multi-modal programs now weave virtual reality drills into broader curricula, moving beyond static screen content.

Blended learning strategies merge online theory with campus-based lab sessions, giving students the flexibility of digital access alongside the accountability of face-to-face feedback. Within acute-care settings, just-in-time micro lessons pop up on mobile workstations to address immediate knowledge gaps, reinforcing the perpetual-learning culture that modern hospitals pursue. As health systems benchmark reduced onboarding durations and fewer adverse events against peers, adoption of simulation modules accelerates, reinforcing growth in the healthcare education solution market size among frontline care providers. Classroom-centric programs will persist in select competencies—ethics discussions or soft-skill coaching—yet continued shifts toward experiential modules underscore the market’s transformative trajectory.

By End User: Hospitals Close the Gap with Academia

Academic institutions lead with a 37.85% contribution to the healthcare education solution market, a heritage advantage rooted in established faculty structures and accreditation familiarity. Universities integrate cloud platforms into registrar systems, automating transcript generation and competency certificates. Grants and philanthropy fund pilot projects, particularly around digital cadavers and mixed-reality anatomy labs, positioning campuses as early adopters. Hospital systems, however, chart the steepest ascent at an 10.94% CAGR because bedside knowledge refreshers boost patient-safety metrics and staff retention. Medical centers embed learning dashboards in EHR portals so clinicians monitor progress without logging into external sites, transforming education from an academic obligation to an operational KPI.

Life-sciences firms leverage the same infrastructure for product-knowledge dissemination and compliance attestations, yet their share trails hospitals and schools because content volumes are narrower. Smaller outpatient networks and allied-health practices make selective purchases—chiefly infection-control modules and device tutorials—often through subscription marketplaces. As inter-professional collaboration and value-based reimbursement expand, cross-sector partnerships will likely create shared digital campuses, distributing costs and amplifying reach across the healthcare education solution market.

By Technology: LMS Maturity Meets Digital-Twin Breakthroughs

Learning management systems possess 53.21% of the healthcare education solution market size, serving as control centers that schedule coursework, capture assessments, and compile audit trails. Vendor APIs now sync LMS data with staffing software so administrators plan rosters around skill readiness, turning education metrics into workforce-planning inputs. Artificial-intelligence layers analyze quiz performance to trigger targeted remediation, elevating pass rates on certification exams such as NCLEX or USMLE. As hospitals adopt competency-based credentialing, LMS platforms evolve into broader talent-management suites.

Digital-twin simulations represent the fastest-advancing segment, registering a 10.78% CAGR by recreating entire patient journeys with real-world EHR data. Learners manipulate virtual physiology to observe downstream effects of therapeutic decisions, an exercise impossible in live wards. Studies show effect sizes up to 0.9 in complex problem solving and 0.7 in communication after digital-twin exposure among nursing cohorts. Vendors collaborate with device manufacturers to embed up-to-date hardware dynamics, ensuring fidelity to current clinical practice. As computing power climbs and graphic pipelines become cloud streamed, digital twins move from tertiary centers into regional hospitals, broadening penetration across the healthcare education solution market.

Geography Analysis

North America commands 41.85% of revenue and continues to set adoption benchmarks for the healthcare education solution market. Federal quality-improvement programs incentivize hospitals to document staff competence, and sizeable endowments underpin college technology purchases. Canadian provinces integrate standardized simulation hours into nursing curricula, reinforcing uniform nationwide competency levels. Proprietary vendors thrive because institutions have sizeable IT budgets and mature cybersecurity frameworks which streamline procurement.

Asia-Pacific records the highest growth trajectory at 13.71% CAGR through 2031. Chinese medical-school surveys show 87.24% of students view digital health literacy as essential, pushing deans to invest in online labs and AI tutors. India’s National Digital Health Mission encourages public-private partnerships around skill platforms, while Indonesia’s hospital chains roll out mobile micro-credential programs for allied workers across archipelagic facilities. Governments across Southeast Asia allocate spectrum and tax incentives to expand broadband, a prerequisite for immersive learning packages. As local ed-tech start-ups partner with multinational publishers, the healthcare education solution market deepens its roots in populous emerging economies. Europe maintains steady, mid-single-digit expansion. The European Commission’s cross-border professional-credential initiative motivates hospitals to adopt LMS modules that issue interoperable digital certificates. National health systems fund VR simulators for stroke management and maternal care, citing improved time-to-treatment metrics. Middle Eastern markets accelerate from a smaller base as strategic visions in the UAE and Saudi Arabia call for AI-enabled hospitals and unified EMRs that dovetail with integrated learning suites. Latin America paces more slowly because fiscal constraints limit capex, yet university consortia pilot cloud libraries to offset faculty shortages. Across these geographies, infrastructure investments and regulatory harmonization dictate the slope of adoption curves in the healthcare education solution market.

Competitive Landscape

The healthcare education solution market is moderately fragmented. Established publishers such as Elsevier and Wolters Kluwer convert decades-old content archives into adaptive, multimedia assets while layering analytics dashboards that appeal to accreditation boards. Specialized simulator makers—including VirtaMed, Laerdal Medical, and CAE Healthcare—bundle hardware with curriculum and instructor training, capturing procedure-specific niches like arthroscopy and neonatal resuscitation. Cloud-native disruptors integrate large-language-model APIs to generate scenario variations on demand, shortening course-development cycles for hospital educators.

Strategic activity skews toward acquisitions and partnerships. Wolters Kluwer’s 2025 purchase of IntelliLearn expands its nursing catalogue into allied-health and infection-control segments. Ascend Learning’s takeover of Clover Learning adds diagnostic-imaging modules with a documented 96% certification-exam pass rate, bolstering differentiation with outcome evidence. AI specialists partner with degree-granting schools: Adtalem and Hippocratic AI co-develop a nurse-assistant certification mapped to Chamberlain University credits, illustrating how content co-creation accelerates time-to-market while sharing risk across stakeholders.

Pricing power remains distributed because buyers range from single-site clinics to multi-state hospital chains and multiversity systems, each with unique procurement rules. Vendor success therefore hinges on interoperability, evidence of learning efficacy, and the ability to wrap advisory services around core platforms. With no participant exceeding even a tenth of global revenue, the healthcare education solution market rewards specialization and ecosystem alliances.

Healthcare Education Solution Industry Leaders

Stryker

GE Healthcare

Medtronic

Siemens Healthineers

FUJIFILM Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Wolters Kluwer acquired IntelliLearn to broaden online courseware for healthcare professionals.

- March 2025: Ascend Learning acquired Clover Learning, enhancing its portfolio with diagnostic-imaging courses that post a 96% exam pass rate

Global Healthcare Education Solution Market Report Scope

As per the scope, health education is the development of the individual, group, institutional, community, and systemic strategies to improve health knowledge, attitudes, skills, and behavior. The healthcare education solution market is segmented by delivery mode (classroom-based courses and e-learning solutions), application (cardiology, radiology, pediatrics, internal medicine, and others), end user (physicians and non-physicians), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Software Platforms |

| Content / Courseware |

| Services (Implementation & Support) |

| Classroom-based Learning |

| E-Learning |

| Blended Learning |

| Simulation-based Training |

| Academic Institutions |

| Hospitals |

| Life-Sciences & Pharma Companies |

| Other Healthcare Providers |

| Learning Management Systems (LMS) |

| Virtual & Augmented Reality Platforms |

| AI-Powered Adaptive Learning |

| Digital-Twin Simulations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component (Value) | Software Platforms | |

| Content / Courseware | ||

| Services (Implementation & Support) | ||

| By Delivery Mode (Value) | Classroom-based Learning | |

| E-Learning | ||

| Blended Learning | ||

| Simulation-based Training | ||

| By End User (Value) | Academic Institutions | |

| Hospitals | ||

| Life-Sciences & Pharma Companies | ||

| Other Healthcare Providers | ||

| By Technology (Value) | Learning Management Systems (LMS) | |

| Virtual & Augmented Reality Platforms | ||

| AI-Powered Adaptive Learning | ||

| Digital-Twin Simulations | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the healthcare education solution market?

The market stands at USD 11.13 billion in 2026 and is forecast to reach USD 18.53 billion by 2031, reflecting a 10.73% CAGR.

Which component leads revenue contribution?

Software platforms account for 46.02% of 2025 revenue because cloud-hosted LMS deployments scale rapidly across large learner bases.

Why are hospitals investing heavily in educational technology?

Hospitals seek point-of-care learning that shortens staff onboarding and boosts patient-safety metrics, driving an 10.94% CAGR for the segment through 2031.

How fast is simulation-based training growing?

Simulation modalities are the fastest-expanding delivery mode, registering a 12.12% CAGR thanks to demand for hands-on rehearsal of high-risk procedures.

Page last updated on: