Mobile Card Reader Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 10.14 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Card Reader Market Analysis by Mordor Intelligence

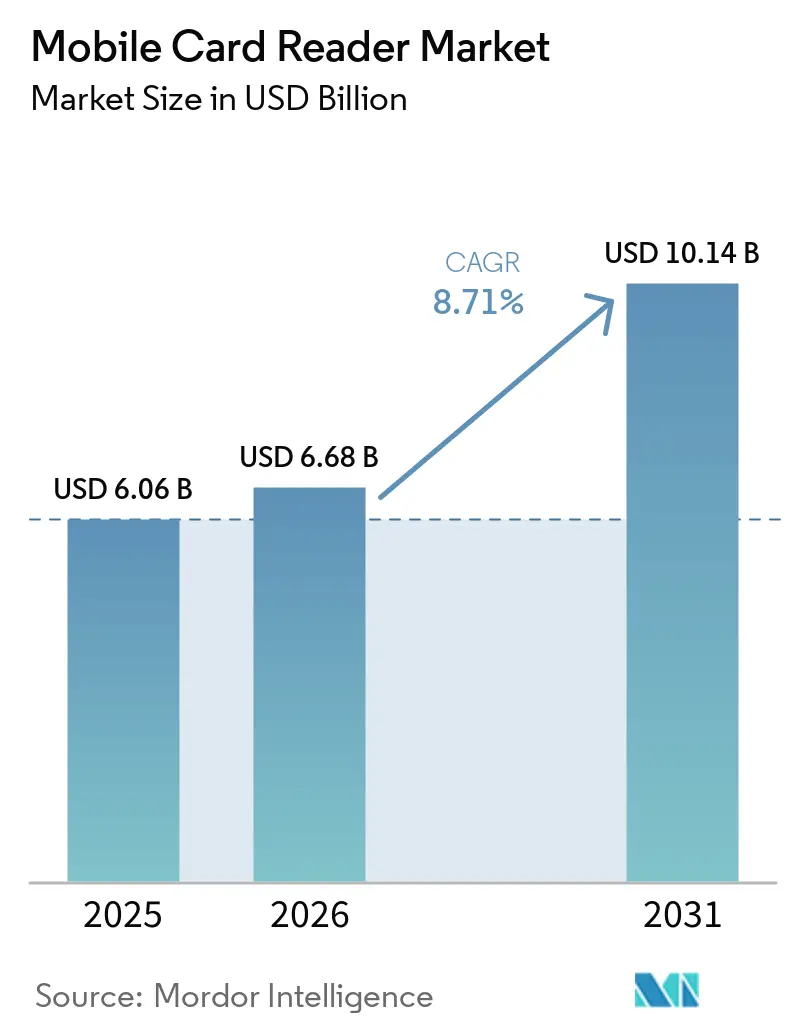

The mobile card reader market size is projected to expand from USD 6.06 billion in 2025 and USD 6.68 billion in 2026 to USD 10.14 billion by 2031, registering a CAGR of 8.71% between 2026 and 2031. Growth is being shaped by a faster hardware replacement cycle as merchants move away from fixed checkout equipment and replace devices that cannot support contactless acceptance. NFC and contactless capabilities have become a basic buying requirement for merchants, keeping demand firm for new companion readers and smart mobile terminals. North America remains the largest revenue base because its merchant network is deep, cards remain central to point-of-sale activity, and SMEs continue to account for a large share of deployments. Cloud-linked reader management is also changing the revenue model, as vendors are building recurring software revenue through analytics, updates, and terminal control rather than relying solely on one-time hardware sales. Cybersecurity risks and hardware margin pressure still limit upside, but faster software and services growth, broader healthcare adoption, and expanding soft POS adoption continue to broaden the addressable market for mobile card readers.

Key Report Takeaways

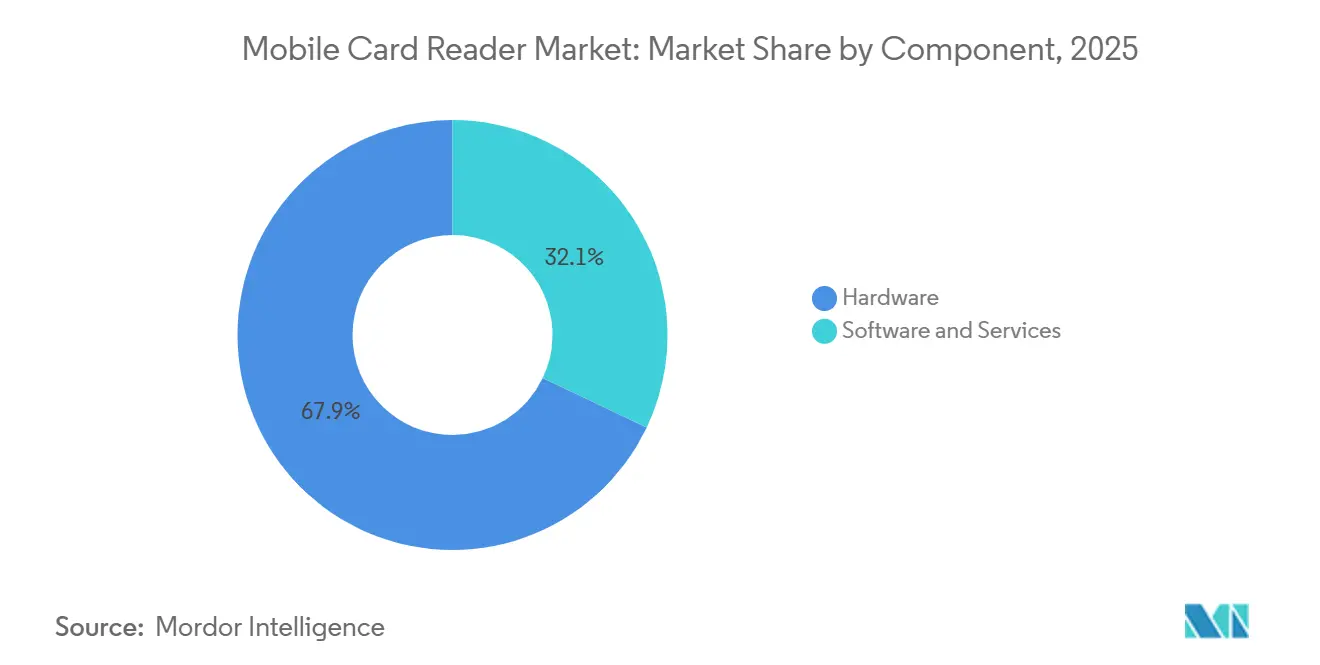

- By component, hardware held 67.93% share of the mobile card reader market in 2025, while software and services are forecast to grow at a 9.11% CAGR through 2031.

- By deployment mode, on-premise held 56.66% share in 2025, while cloud is projected to expand at a 9.03% CAGR through 2031.

- By technology, NFC and contactless held 52.31% share in 2025 and is also the fastest-growing technology segment at a 9.51% CAGR through 2031.

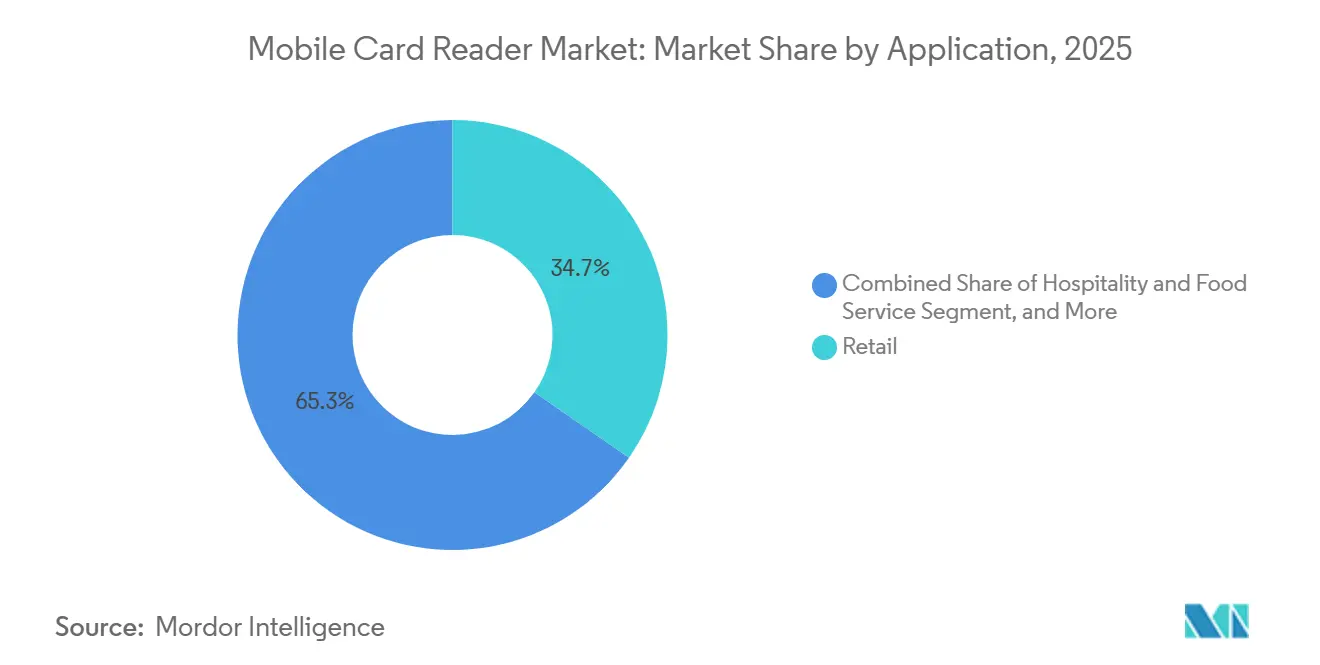

- By application, retail held 34.68% share in 2025, while healthcare is forecast to expand at a 9.71% CAGR through 2031.

- By end user, SMEs held 63.71% share in 2025, while micro-merchants and sole traders are projected to grow at a 9.28% CAGR through 2031.

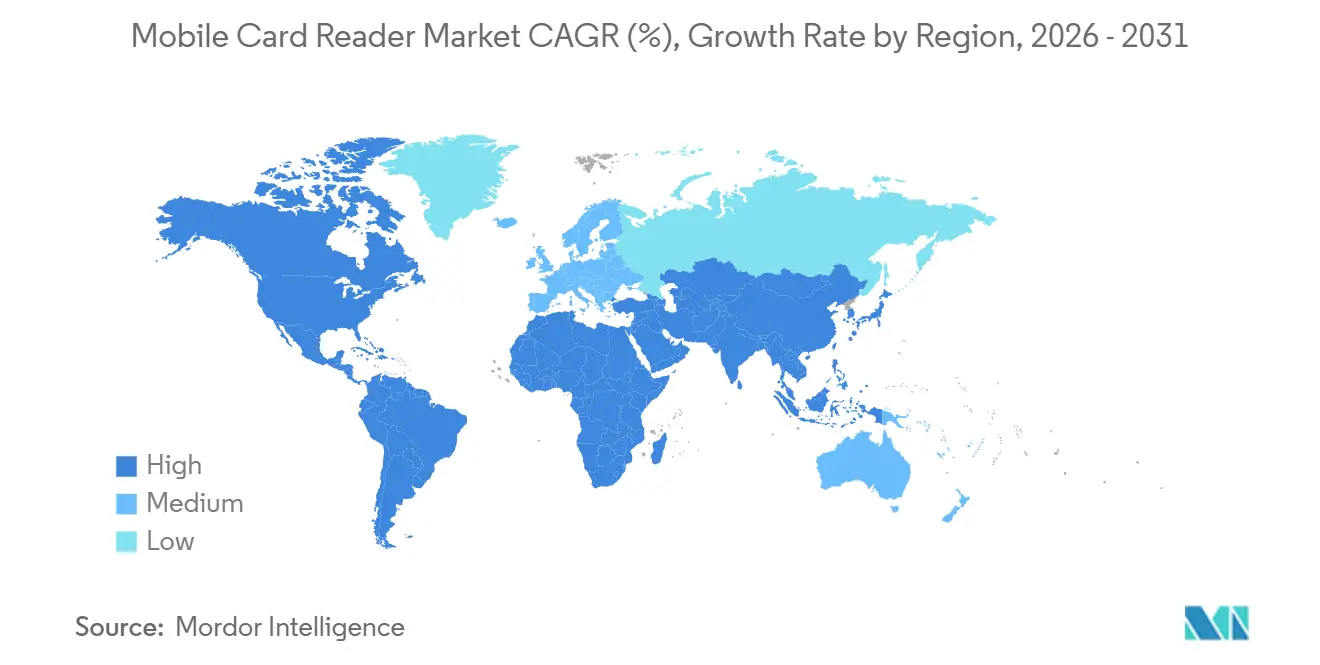

- By geography, North America held 46.39% share of the mobile card reader market in 2025, while Asia-Pacific is forecast to grow at a 9.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Card Reader Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Contactless And NFC Payment Acceptance | +2.2% | Global | Short term (≤ 2 years) |

| SME And Micro-Merchant Digitization | +1.9% | Asia-Pacific, South America, Africa | Medium term (2-4 years) |

| Omnichannel Retail And Tableside Checkout Expansion | +1.4% | North America and European Union | Medium term (2-4 years) |

| Cloud-Linked Value-Added POS Software Adoption | +1.2% | Global | Medium term (2-4 years) |

| PCI MPoC Certification Expanding Reader-Plus-Phone Deployments | +1.1% | Global, North America and European Union early movers | Short term (≤ 2 years) |

| Embedded Merchant Services Increasing Reader Attachment Rates | +0.9% | North America and European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Contactless And NFC Payment Acceptance

NFC and contactless technology accounted for a major portion of the technology segment in 2025, indicating that the mobile card reader market is now centered on tap-ready acceptance rather than optional contactless support. Merchants are no longer treating contactless as a feature upgrade because it now affects checkout speed, customer experience, and terminal relevance across daily retail activity. That shift has shortened the viable life of older devices, especially in developed markets where replacement timelines have moved from 5 years to less than 3 years. It has also driven demand toward smart mobile terminals and companion readers that support multiple payment modes on a single device. The same trend is reinforced by PCI MPoC standards, which are widening the range of compliant mobile acceptance options around NFC-capable devices and reader-linked phone deployments.

SME And Micro-Merchant Digitization

SMEs accounted for a large share of end-user demand in 2025, which makes small business digitization one of the clearest growth engines in the mobile card reader market. Merchant activation is expanding beyond traditional storefronts and into delivery, service, and market-trader use cases where portability matters more than full counter infrastructure. Government-led payment digitization programs in India, Indonesia, and Southeast Asia are supporting this shift by moving more small merchants into formal acceptance systems. Ant International’s EPOS360 rollout shows how payment acceptance is now bundled with settlement, financing, and business management functions for smaller merchants, making the reader a gateway to a broader service stack. As a result, the mobile card reader market is seeing growth not only from hardware sales but also from merchant onboarding models that trade lower device pricing for longer-term transaction and software revenue.

Omnichannel Retail And Tableside Checkout Expansion

The mobile card reader market is also benefiting from merchants seeking a single device to connect payment, order flow, loyalty, and inventory across sales channels. This is especially evident in retail, hospitality, and food service, where mobile checkout is now more closely tied to store operations than to standalone payment acceptance. Tableside checkout has become a standard operating need in many service environments because it supports tipping, split billing, and faster customer turnover with less friction. That is why demand is moving beyond basic dongles and toward smart terminals with larger screens, stronger connectivity, and application support. PAX reinforced this direction in May 2026, introducing new payment and restaurant devices for high-volume service settings that need mobile, countertop, and self-service coverage in a single, unified hardware environment.

Cloud-Linked Value-Added POS Software Adoption

Cloud deployment is one of the strongest structural shifts in the mobile card reader market. The main appeal is operational rather than purely technical because merchants gain remote device management, software updates, analytics, and easier multi-site oversight. This changes vendor economics because recurring platform subscriptions begin to replace the one-time hardware margin that once defined the business. Ingenico’s February 2026 launch of the Ingenico 360 platform reflected this model by combining device management, transaction services, analytics, and developer tools into one cloud-led environment across Europe, the Americas, and Asia-Pacific. The mobile card reader market is therefore moving toward a managed-service structure in which platform depth matters as much as the physical terminal itself.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forcast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity And Compliance Burden | -1.8% | Global | Medium term (2-4 years) |

| Hardware Price Compression And Margin Pressure | -1.5% | Global | Long term (≥ 4 years) |

| Tap-to-Phone SoftPOS Cannibalization Of Entry-Level Readers | -1.2% | North America and European Union | Medium term (2-4 years) |

| Secure Element And Certification Bottlenecks | -0.5% | Asia-Pacific core, spill-over to Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cybersecurity And Compliance Burden

Cybersecurity remains a major restraint because the mobile card reader market is moving deeper into open Android ecosystems and cloud-linked device fleets. The European Payments Council reported that financial service firms face cyberattack exposure far above most other sectors, which keeps payment infrastructure under sustained pressure to strengthen controls and monitoring.[1]European Payments Council, “2025 Payments Threats and Fraud Trends Report,” European Payments Council, europeanpaymentscouncil.eu In April 2026, ESET Research disclosed a new NGate malware variant that abused a legitimate Android NFC payment application to relay card data and capture PINs, demonstrating how quickly the threat landscape is evolving around mobile acceptance tools. Smaller merchants are affected more sharply because they often lack dedicated security teams but still need to meet payment and data protection standards. This raises onboarding friction, increases support needs for providers, and limits how quickly some merchant groups can scale within the mobile card reader market.

Hardware Price Compression And Margin Pressure

Hardware price pressure is another clear restraint because the mobile card reader market has become more crowded at the low end of the device stack. Entry-level readers are increasingly used as acquisition tools, which means vendors often accept weaker upfront economics in exchange for future processing or software income. That creates a difficult position for manufacturers that do not control a platform, since they face lower device pricing without the same recurring revenue cushion. SumUp’s April 2026 expansion in the United States kept that pressure visible by promoting portable card readers with pay-as-you-go pricing and no long-term contracts, which reflects the pricing benchmark many SME-focused providers now face. The result is a mobile card reader market where software attachment, merchant retention, and cloud services matter more each year for margin defense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Subscriptions Reshaping Hardware-Led Revenue Models

Hardware accounted for 67.93% of the mobile card reader market share in 2025, confirming that physical acceptance devices still anchor spending across the category. Companion card readers and smart mobile terminals remain the starting point for merchant activation because every card-accepting business needs certified hardware before it can begin processing. The hardware layer is also changing in the mobile card reader market, as integrated smart terminals are taking share from single-function dongles that depend on a host phone for broader tasks. Merchants increasingly prefer a single device that handles payment acceptance, barcode scanning, receipts, and broader store activities within a single workflow.

Software and services are projected to grow at a 9.11% CAGR through 2031, which shows where the revenue mix is moving next in the mobile card reader market. Payment software, terminal management, security tools, and merchant applications are becoming more important because they create recurring income after the device is installed. PAX said its PAXSTORE ecosystem now supports more than 110 million deployed terminals across 120 countries, which illustrates how app distribution and fleet management have become part of the core value proposition rather than an added layer.[2]PAX Technology, Inc., “PAX Technology, Inc. Introduces the Next-Generation A920Pro PCI 7,” pax.us The mobile card reader industry is therefore shifting from hardware-led procurement toward platform-led relationships that last far beyond the initial terminal sale.

By Deployment Mode: Cloud Enabling A Managed-Service Transition

On-premises deployment accounted for 56.66% in 2025, indicating that a large installed base still prefers local control over payment environments. This is most visible in larger retail fleets and in regulated settings where network policies, audit demands, or system integration needs still favor a locally managed model. Many merchants also keep on-premises setups because existing infrastructure is embedded in daily operations and replacement can be disruptive. Even so, the mobile card reader market is steadily moving away from purely site-bound management as merchants expect faster updates and easier device oversight.

Cloud deployment is the fastest-growing segment of the mobile card reader market, advancing at a 9.03% CAGR through 2031. The appeal is practical because remote software updates, terminal monitoring, and multi-location visibility reduce operational friction for both vendors and merchants. Ingenico’s 360 platform launch in February 2026 showed how providers are packaging device services, analytics, and transaction tools into a single cloud environment that can scale across regions. This leaves the mobile card reader industry with a clearer divide between vendors that can support managed fleets through the cloud and those that still depend mainly on hardware shipment volume.

By Technology: NFC Consolidates Dominance As Legacy Interfaces Fade

NFC and contactless technology held a 52.31% share in 2025 and is projected to grow at a 9.51% CAGR through 2031, keeping it at the center of the mobile card reader market. Contactless acceptance is now a base requirement in many merchant buying decisions, making NFC capability essential across new device launches. The technology shift also affects replacement timing, as merchants with older terminals risk a faster loss of relevance as customer payment habits change. In practice, that means the mobile card reader market rewards vendors that can combine NFC, EMV, and software support in a single, flexible form factor.

EMV chip and PIN still play a meaningful role, with PIN verification remaining standard and transaction settings requiring stronger card-present controls. Hybrid readers that combine NFC, an EMV chip, and a magnetic stripe continue to matter because not all markets are moving at the same pace away from older interfaces. Magnetic stripe-only devices are losing ground quickly because new deployments now require at least dual-interface support to remain useful through the forecast period. SUNMI’s elevation to principal participating organization status within the PCI Security Standards Council in 2026 also showed how closely device makers are tying product development to evolving payment security standards around mobile acceptance hardware.

By Application: Healthcare Emerging As A High-Value Adjacency

Retail accounted for 34.68% of the market in 2025, making it the largest application segment in the mobile card reader market. The retail lead is grounded in store density, the long-standing use of portable checkout among SMEs, and the need for flexible payment acceptance at counters, pop-ups, and assisted selling points. Hospitality and transportation also remain important because tableside payment, delivery collection, and field-service billing all depend on portable hardware that can move with staff. These use cases continue to support a broad installed base across the mobile card reader market, even as device requirements become more software-driven.

Healthcare is the fastest-growing application within the mobile card reader market, rising at a 9.71% CAGR through 2031. Growth is tied to bedside checkout, ambulatory billing, and point-of-care payment capture in settings that historically relied more on cash collection or delayed settlement. UROVO and MagTek both highlighted healthcare as a core use case for their recent mobile terminal and mobile POS solutions, reflecting greater alignment with clinical and frontline workflows. Entertainment and events remain smaller in scale, but they add steady demand for portable acceptance in temporary or space-constrained venues, where fixed infrastructure is not available.

By End User: SME Volume Masks Faster Micro-Merchant Activation

SMEs accounted for 63.71% of the mobile card reader market share in 2025, which makes them the central customer group for vendors and acquirers. Their needs shape product design across portability, inventory integration, recurring billing, and multi-channel selling. SMEs also tend to adopt integrated software more readily than many smaller operators do, as they need reporting, staff controls, and business management tools alongside payment acceptance. That is why much of the mobile card reader market continues to revolve around bundled solutions rather than around standalone devices.

Micro-merchants and sole traders are projected to grow at a 9.28% CAGR through 2031, outpacing all other end-user groups in the mobile card reader market. This demand is coming from previously cash-only operators, such as market sellers, delivery workers, and independent service providers, who would not have invested in full POS hardware earlier. In 2026, SumUp said it served more than 4 million merchants across 37 markets, demonstrating that this low-friction merchant-acquisition model can work at a global scale when pricing and onboarding are simple. Large enterprises still matter because they buy managed fleets with service commitments, but the strongest new-unit activation is increasingly coming from the smaller end of the mobile card reader market.

Geography Analysis

North America accounted for 46.39% of the mobile card reader market in 2025, maintaining its lead. The United States remains the core revenue contributor because the card-based payment culture is strong and SME merchant density is high. The region also benefits from established card network infrastructure and from payment platforms that simplify onboarding for smaller merchants. These factors support recurring refresh demand as devices age and merchant expectations for software and contactless capabilities rise. South America remains smaller in absolute terms, but the mobile card reader market is gaining ground there as formal merchant payment infrastructure expands and digital acceptance becomes more important for underbanked merchant groups.

Europe held a significant share in 2025 and remains one of the most mature regions in the mobile card reader market. Demand is supported by NFC-readiness requirements, high smartphone use, and dense retail networks that sustain steady terminal demand. Germany offers a clear example of this shift, VR Payment reported that contactless girocard payments accounted for 88.5% of all girocard transactions in December 2025, and the active POS estate rose to more than 1.34 million terminals.[3]VR Payment, “Girocard, Kontaktloszahlen Erreicht Neuen Rekord,” VR Payment, vr-payment.de The United Kingdom, France, Italy, and Spain also remain important because they combine large merchant bases with continued migration toward portable and smart payment devices. Europe, therefore, remains a key replacement and upgrade market rather than only a first-time deployment market.

Asia-Pacific is the fastest-growing regional segment in the mobile card reader market, with a 9.67% CAGR through 2031. Growth comes from merchant digitization programs, wider wallet use, tourism-linked payment acceptance, and the need for merchants to support multiple payment rails in the same environment. TNG Digital and EPOS launched EPOS360 and EPOS360 BlueTap in Malaysia in January 2026 to support local SMEs through the TNG eWallet ecosystem, which shows how payment providers are targeting this merchant base with integrated acceptance tools. The Middle East and Africa remain smaller contributors, but both are gaining relevance as cashless mandates, mobile payment infrastructure, and merchant formalization programs improve the long-term setup for the mobile card reader market.

Competitive Landscape

The mobile card reader market is moderately fragmented globally, with large OEMs competing alongside regional hardware makers, fintech-platform hybrids, and Android-first device specialists. Ingenico Group S.A. and PAX Technology Limited remain two of the most visible global names, while VeriFone, Castles Technology, BBPOS, Miura Systems, MagTek, Newland, SUNMI, UROVO, Posiflex, Dspread, DATECS, Centerm, New POS Technology, SZZT, Smartpeak, and Dejavoo all add to the competitive spread. This wide field means the mobile card reader market does not operate as a winner-take-most structure, even though a few vendors have strong brand recognition and deep certification. Product competition now depends on platform capability, Android readiness, certification status, security credibility, and the ability to support merchant applications beyond payment acceptance. Pricing pressure is strongest at the lower end, where hardware is often used to acquire merchants rather than to generate margin on its own.

Strategic moves in 2025 and 2026 show how the mobile card reader market is shifting toward unified hardware and software ecosystems. Ingenico’s February 2026 launch of the AXIUM device family and the Ingenico 360 cloud platform marked a clear push toward a managed-service model in which devices, analytics, and transaction tools work together as a single stack. PAX followed with new Android 14 devices in April and May 2026, including the A920Pro PCI 7 and new restaurant-focused hardware, which strengthened its position across mobile, countertop, and service-led use cases. Ingenico also partnered with Samsung and Talus in January 2026 to bring a mobile business operating solution to North America, which showed how soft POS, mobile device ecosystems, and business software are converging in the mobile card reader market. These moves show that scale is no longer defined only by device shipments but also by the strength of cloud services and software attachment.

White-space opportunity remains visible in healthcare, in micro-merchant activation across South Asia and Africa, and in the path from soft POS to dedicated hardware. Vendors that can convert smartphone-based acceptance users into higher-value terminal customers should be better positioned as merchant needs become more complex. SISA’s recognition in March 2026 as India’s first PCI-recognized laboratory for full MPoC security evaluations may also help reduce certification frictions for providers targeting one of the largest future merchant pools.[4]SISA, “SISA Joins Global Group of PCI Recognized Labs to Perform Security Evaluations of Payment Acceptance Devices and Solutions,” SISA, sisainfosec.com The mobile card reader market, therefore,e remains open enough for new challengers, but a durable advantage is moving toward vendors that can combine certification, software, device breadth, and merchant service integration.

Mobile Card Reader Industry Leaders

Ingenico Group S.A.

VeriFone, Inc.

PAX Technology Limited

Castles Technology Co., Ltd.

Newland Payment Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: PAX Technology unveiled next-generation A360 and A380 PIN pad devices featuring Android 14, 6- and 8-inch displays, and PCI PTS 7 certification, alongside a self-ordering Smart Kiosk (SK900) running Android 16 at the National Restaurant Association Show 2026. The launches reinforced PAX's strategy to deliver a complete hardware ecosystem for high-volume foodservice environments across mobile, countertop, and self-service form factors.

- April 2026: PayTabs Group acquired UAE-based contactless platform TAPn'GO, integrating smartphone-based contactless checkout into its MENA Super App and targeting adoption by over 20,000 regional businesses. The deal positions PayTabs at the intersection of SoftPOS technology and super-app consolidation in a region where the contactless segment is growing quickly.

- April 2026: Euronet Worldwide signed an agreement to acquire PaynoPain, a Spanish fintech specializing in online payment solutions, with the deal expected to close in Q3 2026. The acquisition is intended to strengthen Euronet's direct merchant acquiring footprint in Spain and Portugal and enhance its omnichannel payment capabilities across Europe, with Euronet operating approximately 610,000 EFT point-of-sale terminals globally.

- March 2026: payabl. launched a SoftPOS Tap to Pay solution on Android, converting NFC-enabled smartphones into certified payment terminals. The company cited UK in-store card payments under GBP 100 (approximately USD 127) as 94.6% contactless, and noted that 65% of early user Nafais's transactions are now processed digitally following live deployment.

Global Mobile Card Reader Market Report Scope

The Mobile Card Reader Market is the global industry comprising hardware devices, software platforms, and related services that enable portable electronic payment acceptance via smartphones, tablets, or dedicated compact terminals. These systems allow merchants and service providers to process card-based transactions using technologies such as EMV chip and PIN, near-field communication (NFC), magnetic stripe, and hybrid multi-interface readers.

The Mobile Card Reader Report is Segmented by Component (Hardware [Companion Card Readers, Smart Mobile Terminals, and Reader Accessories and Docks], and Software and Services [Payment Acceptance Software, Terminal Management and Security Software, and Value-Added Merchant Applications]), Deployment (On-Premise and Cloud), Technology (EMV Chip and PIN, Near-Field Communication and Contactless, Magnetic Stripe, and Hybrid Multi-Interface Readers), Application (Retail, Hospitality and Food Service, Transportation and Field Services, Healthcare, and Entertainment and Events), End User (Micro-Merchants and Sole Traders, Small and Medium-Sized Enterprises, and Large Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Companion Card Readers |

| Smart Mobile Terminals | |

| Reader Accessories and Docks | |

| Software and Services | Payment Acceptance Software |

| Terminal Management and Security Software | |

| Value-Added Merchant Applications |

| On-Premise |

| Cloud |

| EMV Chip and PIN |

| Near-Field Communication and Contactless |

| Magnetic Stripe |

| Hybrid Multi-Interface Readers |

| Retail |

| Hospitality and Food Service |

| Transportation and Field Services |

| Healthcare |

| Entertainment and Events |

| Micro-Merchants and Sole Traders |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | Companion Card Readers |

| Smart Mobile Terminals | ||

| Reader Accessories and Docks | ||

| Software and Services | Payment Acceptance Software | |

| Terminal Management and Security Software | ||

| Value-Added Merchant Applications | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Technology | EMV Chip and PIN | |

| Near-Field Communication and Contactless | ||

| Magnetic Stripe | ||

| Hybrid Multi-Interface Readers | ||

| By Application | Retail | |

| Hospitality and Food Service | ||

| Transportation and Field Services | ||

| Healthcare | ||

| Entertainment and Events | ||

| By End User | Micro-Merchants and Sole Traders | |

| Small and Medium-Sized Enterprises | ||

| Large Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the mobile card reader sector?

The mobile card reader market reached USD 6.06 billion in 2025, is expected at USD 6.68 billion in 2026, and is forecast to reach USD 10.14 billion by 2031 at an 8.71% CAGR.

Which component leads revenue in mobile card reader deployments?

Hardware led in 2025 with a 67.93% share because every merchant still needs a certified physical device to begin card acceptance.

Why is cloud deployment gaining traction in payment reader systems?

Cloud deployment is forecast to grow at a 9.03% CAGR through 2031 because merchants want remote updates, terminal management, analytics, and easier control across multiple locations.

Which technology segment is shaping future device demand the most?

NFC and contactless leads technology demand with a 52.31% share in 2025 and a 9.51% CAGR through 2031, making tap-ready devices the core purchase requirement.

Which end-user group creates the biggest volume opportunity?

SMEs remain the largest customer base with a 63.71% share in 2025, while micro-merchants are growing faster at a 9.28% CAGR as more cash-only operators move into digital acceptance.

Which regions offer the strongest growth prospects through 2031?

North America leads with 46.39% share in 2025, but Asia-Pacific offers the fastest growth at a 9.67% CAGR because merchant digitization and multi-rail payment acceptance are expanding quickly.

Page last updated on: