Ethernet Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.36 Billion |

| Market Size (2031) | USD 18.78 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

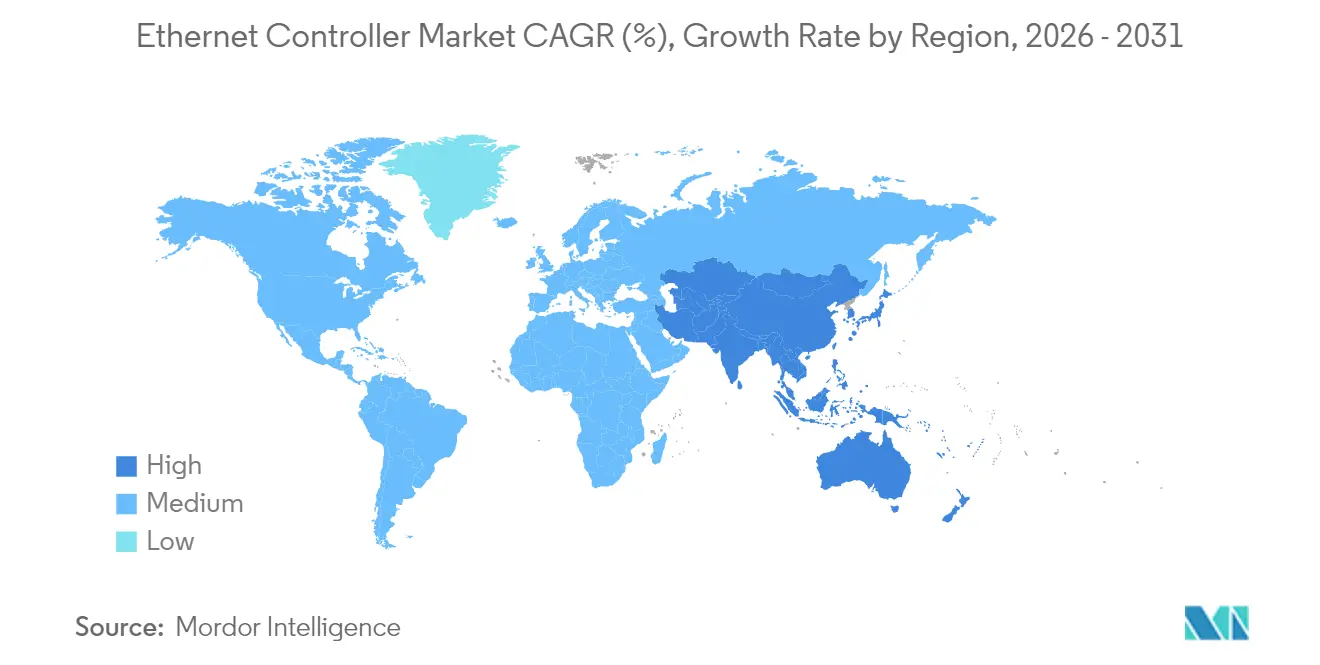

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethernet Controller Market Analysis by Mordor Intelligence

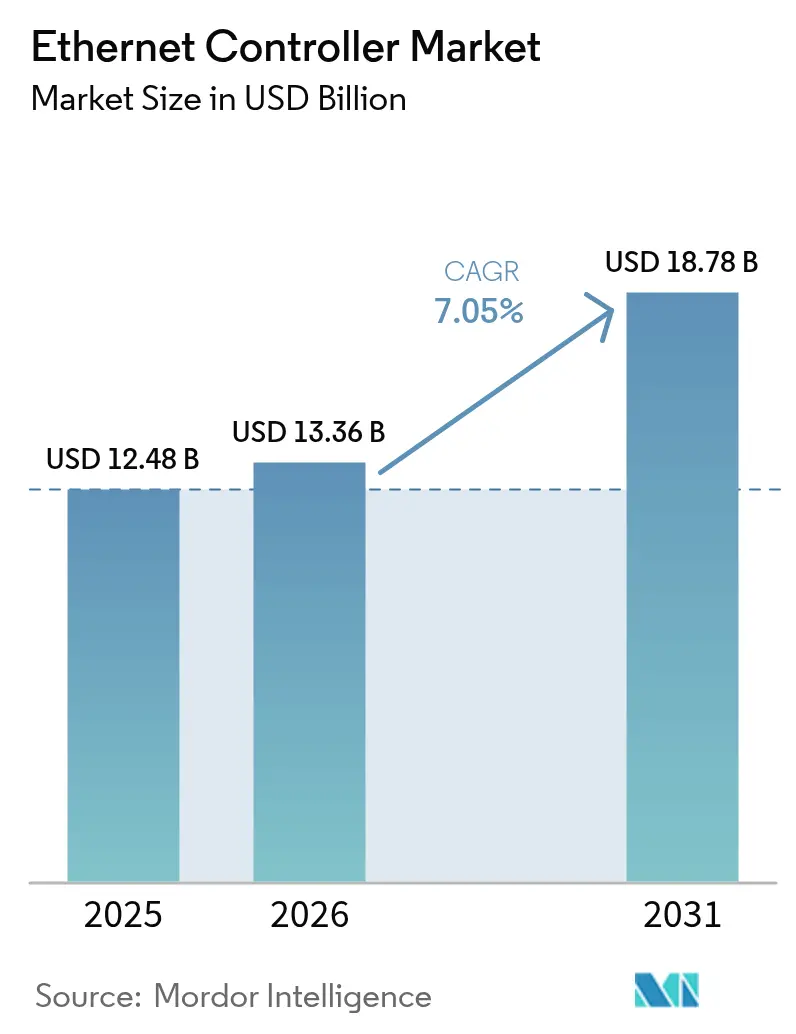

The Ethernet Controller Market size was valued at USD 12.48 billion in 2025 and estimated to grow from USD 13.36 billion in 2026 to reach USD 18.78 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031).

Continuous hyperscale data-center investment in 800 G and 1.6 T Ethernet, the rapid shift toward zonal E/E automotive architectures, and PoE++ roll-outs in smart buildings sustain strong revenue visibility despite near-term semiconductor supply constraints. Vendors differentiate through power-optimized designs, MAC-PHY integration, and Smart NIC off-load engines that lower total cost of ownership for hyperscalers. Competitive intensity rises as Asian fabs chase design wins with aggressive pricing even while legacy-node shortages pressure PHY production capacity. Opportunities remain compelling for suppliers embedding functional-safety features for autonomous vehicles, single-pair PHYs for harsh industrial sites, and high-power PoE controllers for smart-building subsystems as the Ethernet controller market pursues balanced growth across consumer, enterprise, and operational-technology domains.

Key Report Takeaways

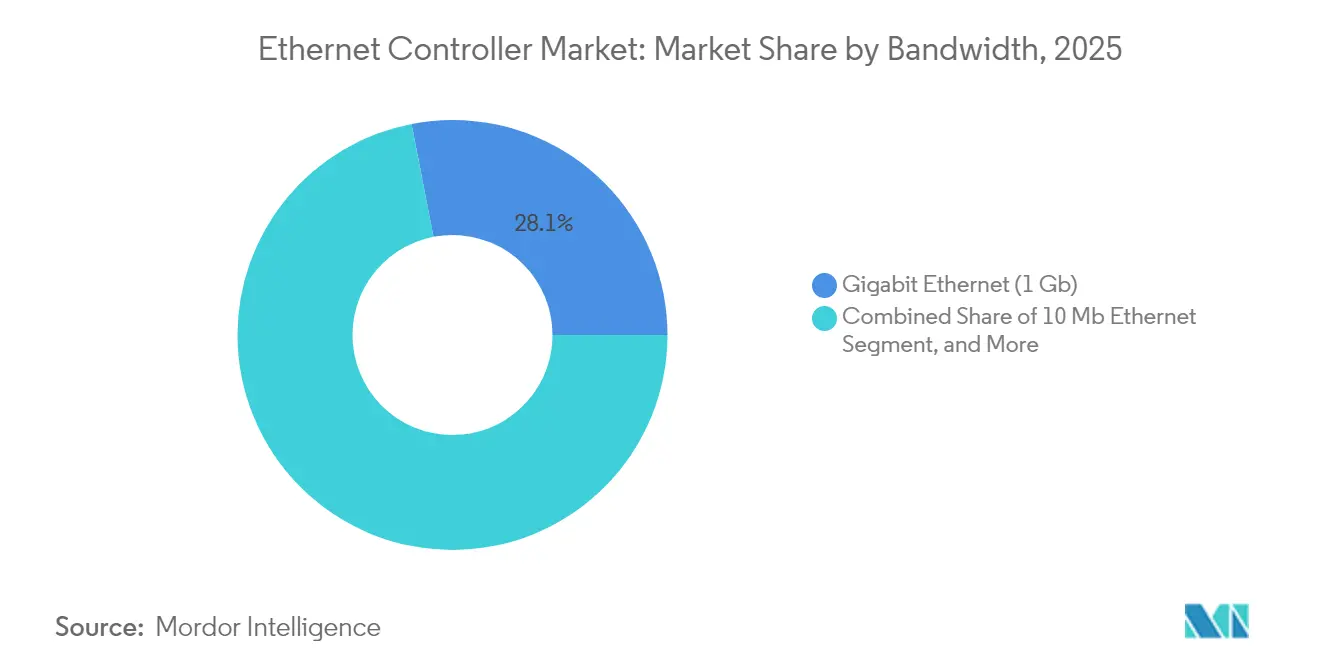

- By bandwidth type, Gigabit Ethernet led with 28.05% revenue share of the Ethernet controller market in 2025 while the combined 200/400/800 G and 1.6 T segment is projected to advance at a 12.1% CAGR to 2031.

- By function, integrated MAC-PHY devices accounted for 30.75% of the Ethernet controller market share in 2025, whereas Smart NIC and IPU solutions are forecast to expand at 12.95% CAGR through 2031.

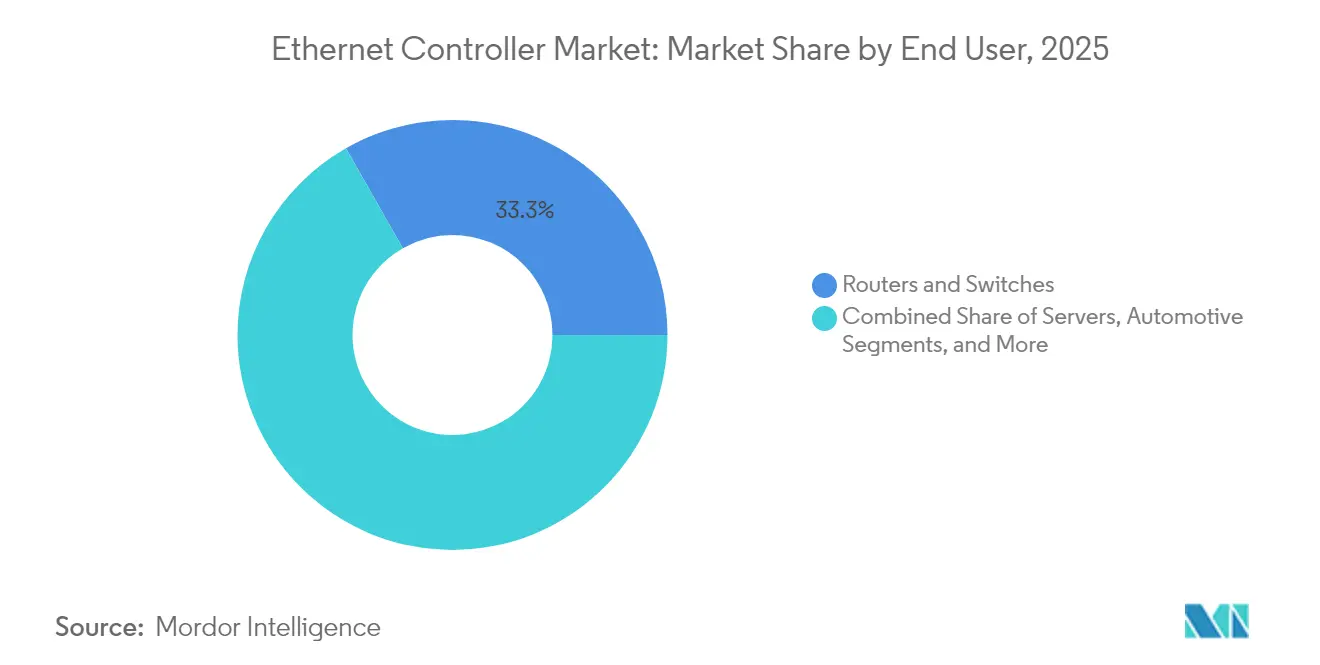

- By end user, routers and switches captured 33.25% share of the Ethernet controller market size in 2025; industrial automation equipment is tracking the fastest 11.3% CAGR between 2026-2031.

- By application, data-center and cloud workloads held 35.45% share in 2025, while connected-vehicle electronics are poised for a 12.4% CAGR over the outlook period.

- By geography, Asia-Pacific dominated with a 38.20% share in 2025; the Middle East & Africa region is forecast to grow at 12.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethernet Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven demand for 800 G and 1.6 T Ethernet in hyperscale data-centers | +2.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Automotive zonal E/E architectures adopting multi-gig Automotive Ethernet | +1.9% | Europe, North America, Global | Long term (≥ 4 years) |

| Industrial 10BASE-T1L enabling single-pair IIoT sensor connectivity | +1.2% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of EtherCAT for real-time machine control | +0.8% | Germany, global industrial clusters | Long term (≥ 4 years) |

| Rapid proliferation of USB-to-Ethernet adapters for ultra-thin clients | +0.6% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Mandatory PoE++ deployment in smart-building lighting and security | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-driven demand for 800 G and 1.6 T Ethernet in hyperscale data-centers

Large language model training pushes east-west traffic beyond the limits of traditional 100 G switching, prompting cloud operators to migrate toward 800 G and 1.6 T Ethernet fabrics that balance cost and performance. The Ultra Ethernet Consortium aligns silicon vendors and hyperscalers on congestion-aware transport and deterministic latency features required for AI workloads. Broadcom reported USD 4.4 billion in AI networking revenue for fiscal 2024, with switching ASICs driving the Ethernet controller market as operators pivot away from InfiniBand. Intel added application-device queues and PTP timestamping to its E810 controllers to optimize distributed training synchronization. While the Ethernet controller market benefits from standardized tooling and multi-vendor sourcing, vendors must continue innovating on telemetry and flow-control mechanisms to maintain parity with proprietary fabrics in latency-sensitive AI pipelines. Standards work inside IEEE 802.3df aims to codify 1.6 T signaling and lane modulation schemes that will underpin second-generation AI cluster roll-outs.

Automotive zonal E/E architectures adopting multi-gig Automotive Ethernet

Original equipment manufacturers transition from domain-based networks to zonal topologies, replacing legacy CAN and LIN buses with 2.5-G, 5-G, and 10-G Automotive Ethernet backbones capable of aggregating radar, lidar, and camera data streams into centralized compute nodes. Texas Instruments’ DP83TG720S-Q1 PHY delivers 1 G transmission over single twisted-pair cable, meeting ISO 26262 ASIL B budgets and enabling reduced harness weight TI.COM. Marvell’s USD 2.5 billion purchase of Infineon’s automotive Ethernet business underscores the value of ASIL-compliant PHY intellectual-property within the Ethernet controller market. NXP integrates time-sensitive networking into controllers to guarantee microsecond-level determinism for drive-by-wire and fail-operational steering systems. Over-the-air update capability and cybersecurity-by-design requirements further elevate Ethernet to a unifying transport for vehicle software platforms. Regulatory pressure from UNECE R155 cybersecurity and R156 software update rules accelerates adoption, locking multi-gig Ethernet into the baseline of future EV platforms.

Industrial 10BASE-T1L enabling single-pair IIoT sensor connectivity

The IEEE 802.3cg-defined 10BASE-T1L PHY extends 10 Mb/s Ethernet over 1 km of single twisted-pair-cabling, allowing intrinsically safe field-instrumentation to connect directly into plant networks IEEE.ORG. Analog Devices’ AD7421 and onsemi’s NCN26010 integrate power delivery so temperature and vibration sensors can draw <500 mW while providing Ethernet-APL connectivity in Zone 0 hazardous areas. Eliminating protocol gateways reduces latency, simplifies maintenance, and dovetails with cloud-based analytics strategies that favor native IP endpoints. Early deployments in petrochemical and pharmaceutical plants demonstrate a 30% wiring-cost reduction versus conventional 4-20 mA loops, reinforcing the Ethernet controller market trajectory toward edge-to-cloud visibility. Certification schemes under IECEx and ATEX validate safe operation, widening addressable scope for vendors offering ruggedized MAC-PHY solutions.

Growing adoption of EtherCAT for real-time machine control

IEEE 802.3bt permits 90 W power on four-pair cabling, allowing LED luminaires, PTZ camera arrays, and Wi-Fi 7 access points to converge on a single structured-cabling layer. Siemon introduced category 6A infrastructure supporting full-power PoE++ across 100 m runs without exceeding 55 °C bundle temperatures. Signify embeds Ethernet-powered drivers in commercial fixtures, enabling granular dimming and occupancy-based automation. Building owners gain centralized energy measurement while avoiding separate AC circuits, a benefit amplified by sustainability mandates under LEED v4.1. For controller vendors, integrating PoE sourcing circuitry with advanced telemetry opens new attach points across lighting and security ecosystems, lifting the Ethernet controller market relevance in intelligent-building retrofits

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent legacy-node semiconductor shortages pressuring PHY supply | -1.4% | Asia-Pacific fabs, Global OEMs | Short term (≤ 2 years) |

| Stiff margin compression from low-cost Asian fabs and design wins | -0.9% | Originating in APAC, global effect | Medium term (2-4 years) |

| InfiniBand and proprietary AI fabrics challenging Ethernet latency | -0.7% | North America, Europe AI clusters | Medium term (2-4 years) |

| Rising power-consumption limits within AI clusters | -0.5% | Global hyperscale data-centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent legacy-node semiconductor shortages pressuring PHY supply

Analog-heavy Ethernet PHYs remain tied to 28 nm and older nodes where wafer shortages persist as foundries divert capital to advanced processes. Reuters linked late-2024 substrate disruptions in North Carolina quartz mines to extended lead times exceeding 52 weeks for certain 65 nm PHY lineups. TSMC commented that expanding mature-node capacity remains economically challenging given tool scarcity and lower ASPs. Automakers and industrial OEMs, which require 15-year longevity and extreme-temperature grades, face the heaviest allocations, compelling controller suppliers to dual-source packaging and explore second-tier foundries. The squeeze threatens near-term revenue capture even as overall Ethernet controller market demand remains healthy.

Stiff margin compression from low-cost Asian fabs and design wins

Analog-heavy Ethernet PHYs remain tied to 28 nm and older nodes where wafer shortages persist as foundries divert capital to advanced processes. Reuters linked late-2024 substrate disruptions in North Carolina quartz mines to extended lead times exceeding 52 weeks for certain 65 nm PHY lineups. TSMC commented that expanding mature-node capacity remains economically challenging given tool scarcity and lower ASPs. Automakers and industrial OEMs, which require 15-year longevity and extreme-temperature grades, face the heaviest allocations, compelling controller suppliers to dual-source packaging and explore second-tier foundries. The squeeze threatens near-term revenue capture even as overall Ethernet controller market demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bandwidth Type: High-speed adoption reshapes deployment economics

Gigabit Ethernet retained a 28.05% revenue foothold in 2025 as enterprises, small data-centers, and industrial controllers continued qualifying mature 1 Gb/s designs for predictable workloads. Nevertheless, hyperscalers now drive a 12.1% CAGR for combined 200 G, 400 G, 800 G, and nascent 1.6 T options, ensuring that the Ethernet controller market size for very-high-speed ports will more than double by 2031. Engineers favor PAM4 signaling with integrated DSP equalization to compress front-panel footprint while curbing channel loss budgets.

Among transition speeds, 2.5 G and 5 G solutions help commercial campuses backhaul Wi-Fi 7 traffic over installed cat-5e cabling, whereas 10 G and 25 G remain popular in storage and telco access aggregation. The Ethernet controller market sees revived interest in 10 Mb/s single-pair implementations for span-length factory sensors, a niche forecast to deliver steady volume albeit limited revenue. Suppliers balance die-area trade-offs by producing segmented silicon families rather than one-size-fits-all PHYs, a strategy preserving gross margins despite intensifying price competition on mature nodes.

By Function: Integration and off-load redefine silicon value

Integrated MAC-PHY devices captured 30.75% of Ethernet controller market share during 2025 as OEMs prioritized bill-of-materials savings and simplified PCB routing in consumer and low-end enterprise gear. Conversely, Smart NICs and Infrastructure Processing Units (IPUs) are scaling at a 12.95% CAGR because cloud architects shift TLS termination, VXLAN encapsulation, and storage RDMA to dedicated accelerators that free up host cores for revenue-generating compute.

Discrete PHYs persist for optical-module makers and rugged industrial boards that demand configuration flexibility and extended temperature ratings. USB-to-Ethernet bridge controllers expand inside ultra-thin laptops and tablets, reflecting employee appetite for wired gigabit docking in bandwidth-constrained offices. Power-over-Ethernet sourcing silicon that meets 802.3bt is another growth pocket, especially when coupled with telemetry engines that feed building-management dashboards. Over the forecast horizon, the Ethernet controller market size for off-load-centric devices is projected to close the revenue gap with traditional integrated solutions, though unit volumes will still favor single-chip MAC-PHYs in high-run-rate consumer SKUs.

By End User: Software-defined infrastructure lifts new verticals

Routers and switches remained the dominant end-user cohort at 33.25% in 2025, anchored by spine-leaf refresh cycles that align with next-generation merchant-silicon releases. Yet industrial automation customers now deliver an 11.3% CAGR tailwind, pulling real-time controllers and sensor gateways into mainstream Ethernet topologies that can compost deterministic traffic alongside standard TCP flows.

Server NIC shipments track overall data-center footprint additions but skew toward higher ASP Smart NICs. Automotive OEMs, while smaller in volume, command premium pricing for AEC-Q100-qualified PHYs and eight-year supply commitments, boosting blended margins across the Ethernet controller market. Consumer electronics, led by USB 2.5 G dongles for cloud gaming and live-streaming PCs, remains cyclical yet strategically important for vendor scale economies. Aerospace and medical device makers add niche layers of demand that reward suppliers willing to pursue stringent regulatory certification.

By Application: AI clouds and intelligent vehicles surge ahead

Data-center/cloud platforms generated 35.45% of 2025 controller revenue as global GPU farms proliferated. The Ethernet controller market size tied to AI training nodes will expand most sharply in absolute dollars, even as year-on-year unit growth for mainstream servers flattens post-2027. Telecom 5G open-RAN installs represent a reliable mid-single-digit CAGR driver as carriers virtualize baseband pools and fronthaul links.

Connected vehicles register the fastest 12.4% CAGR through 2031 because next-gen EV models integrate multigig backbones for HD sensor payloads plus centralized compute zones. Smart-factory projects adopt single-pair topologies to enable loop-power field devices, while enterprise campus networks modernize to support Edge-AI inference boxes at wiring closets. These diverse use cases broaden total addressable opportunity and insulate the Ethernet controller market against macro weakness in any single vertical.

Geography Analysis

Asia-Pacific led the Ethernet controller market with a 38.20% share in 2025, buoyed by China’s semiconductor manufacturing ecosystems, Japan’s automotive electronics dominance, and South Korea’s early adoption of 5G RAN fronthaul over Ethernet. Local supply-chain self-sufficiency initiatives spur additional design wins for domestic fabless firms, yet global vendors still capture high-speed optics and Smart NIC sockets that hinge on advanced process nodes. Government subsidies for AI supercomputer build-outs strengthen regional demand for 800 G switch silicon, sustaining double-digit growth despite episodic export-control uncertainties.

North America remains the innovation epicenter for AI-optimized data-center fabrics, translating into outsized ASPs that elevate regional revenue share relative to unit shipments. The Ethernet controller market benefits from established cloud titans standardizing on programmable Smart NIC architectures and from Tier-1 automotive suppliers in Michigan and Ontario prototyping zonal ECUs. Federal incentives under the CHIPS and Science Act encourage on-shore packaging lines for automotive PHYs, potentially easing supply risk over the medium term.

The Middle East & Africa posts a 12.7% CAGR through 2031 on the back of sovereign wealth-fund-backed hyperscale campuses, smart-city deployments in Saudi Arabia and the UAE, and greenfield industrial zones embracing Ethernet-based condition-monitoring. Fiber build-outs along the Africa Coast to Europe (ACE) cable system, plus educational cloud initiatives, further stimulate controller imports. Europe exhibits steady demand centered on Germany’s Industry 4.0 programs and France’s AI-cloud clusters, while South America’s growth clusters around Brazilian data-center expansions and Argentine automotive redesigns. Across all regions, trade-policy fluidity and currency fluctuations remain secondary variables that Ethernet controller market participants monitor closely.

Competitive Landscape

The Ethernet controller market displays moderate concentration: Intel, Broadcom, and Marvell together control well over half of global revenue, leveraging advanced process access, in-house IP libraries, and expansive software ecosystems. Intel’s integrated LOM strategy secures desktop and server sockets, though recent I226-V reliability fixes illustrate the reputational stakes of silicon-validation rigor. Broadcom leads switching ASICs and Smart NICs, parlaying merchant-silicon dominance into contiguous controller attach-rates, particularly inside hyperscale leaf-spine topologies. Marvell strengthens automotive credentials via the Infineon portfolio acquisition, positioning itself at the convergence of zonal architectures and Ethernet-based battery-management systems.

Competitive pressure intensifies from Realtek, MaxLinear, and emerging Chinese fabless houses that target cost-sensitive 2.5 G and below segments with price points 20-30% beneath incumbent quotes. Start-ups funded by strategic cloud investors pursue data-plane off-load with chiplets and RISC-V cores, hoping to displace legacy FPGA-based accelerators. Intellectual-property barriers reside in equalization algorithms, timing-synchronization accuracy, and certified functional-safety stacks; these attributes shield incumbents from pure-play commodity entrants. Nonetheless, margin compression across low-end lines motivates incumbents to prioritize IP-rich high-speed and vertical-specific designs, sustaining R&D outlays at 15-17% of net sales. Collectively, these dynamics underpin a balanced yet fiercely contested Ethernet controller market awaiting the next disruptive architectural shift.

Ethernet Controller Industry Leaders

Intel Corporation

Broadcom Inc.

Microchip Technology Inc.

Cirrus Logic Inc.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Marvell completed its USD 2.5 billion acquisition of Infineon’s automotive Ethernet assets, broadening ASIL-B/D-grade PHY and switch portfolios for zonal vehicle backbones.

- December 2024: Broadcom reported USD 4.4 billion in AI networking revenue, citing 800 G switching ramps at top three cloud operators.

- November 2024: Intel issued firmware and silicon fixes for I226-V reliability anomalies affecting 13th-gen desktop platforms, restoring OEM confidence.

- October 2024: Texas Instruments launched the DP83TG720S-Q1 1 G single-pair PHY, adding functional-safety diagnostics for EV zonal controllers.

Global Ethernet Controller Market Report Scope

An Ethernet controller is a small chip that handles all the data swapped between two computers or servers through the Internet. This industry's growth is expected to be positive during the forecast period due to increased data traffic, with work cultures leaning toward remote work and BYOD devices.

The ethernet controller market is segmented by bandwidth type (fast ethernet, gigabit ethernet, and switch ethernet), function (PHY, integrated), end users (servers, routers and switches, consumer applications, and other end users), and geography (North America [United States and Canada], Europe [Germany, United Kingdom, France, and Rest of Europe], Asia-Pacific [India, China, and Japan], Latin America, and Middle East and Africa). The market sizes and predictions are provided in terms of value in USD for all the above segments.

| 10 Mb Ethernet |

| Fast Ethernet (100 Mb) |

| Gigabit Ethernet (1 Gb) |

| 2.5 / 5 Gb Multi-Gig Ethernet |

| 10 Gb Ethernet |

| 25 / 40 / 50 Gb Ethernet |

| 100 Gb Ethernet |

| 200 / 400 / 800 Gb and 1.6 Tb Ethernet |

| Discrete PHY |

| Integrated MAC-PHY Controller |

| Smart NIC / IPU |

| USB-to-Ethernet Controller |

| Single-Pair MAC-PHY (SPE / APL) |

| PoE / PoE++ Controller |

| Servers |

| Routers and Switches |

| Industrial Automation and IIoT |

| Automotive |

| Consumer and Smart-Home Devices |

| Others |

| Data-Centre and Cloud |

| Telecommunications and 5G RAN |

| Edge and Enterprise Campus |

| Smart Factory / Industry 4.0 |

| Connected Vehicles (ADAS and IVI) |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Middle East and Africa | GCC |

| South Africa |

| By Bandwidth Type | 10 Mb Ethernet | |

| Fast Ethernet (100 Mb) | ||

| Gigabit Ethernet (1 Gb) | ||

| 2.5 / 5 Gb Multi-Gig Ethernet | ||

| 10 Gb Ethernet | ||

| 25 / 40 / 50 Gb Ethernet | ||

| 100 Gb Ethernet | ||

| 200 / 400 / 800 Gb and 1.6 Tb Ethernet | ||

| By Function | Discrete PHY | |

| Integrated MAC-PHY Controller | ||

| Smart NIC / IPU | ||

| USB-to-Ethernet Controller | ||

| Single-Pair MAC-PHY (SPE / APL) | ||

| PoE / PoE++ Controller | ||

| By End User | Servers | |

| Routers and Switches | ||

| Industrial Automation and IIoT | ||

| Automotive | ||

| Consumer and Smart-Home Devices | ||

| Others | ||

| By Application | Data-Centre and Cloud | |

| Telecommunications and 5G RAN | ||

| Edge and Enterprise Campus | ||

| Smart Factory / Industry 4.0 | ||

| Connected Vehicles (ADAS and IVI) | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Middle East and Africa | GCC | |

| South Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Ethernet controller market?

The Ethernet controller market size stood at USD 13.36 billion in 2026.

How fast is the global market expected to grow?

Revenue is projected to rise at a 7.05% CAGR, reaching USD 18.78 billion by 2031.

Which bandwidth segment is gaining the most momentum?

The aggregated 200 G–1.6 T tier is forecast to post a 12.1% CAGR due to AI data-center upgrades.

Why is Automotive Ethernet important now?

Zonal E/E architectures require multi-gig links to transport ADAS sensor data, propelling double-digit growth in automotive-grade controllers.

What makes PoE++ attractive for building owners?

Up to 90 W per port powers LED lighting, cameras, and Wi-Fi 7 APs on a single cable, reducing electrical installation costs and enabling energy monitoring.

Which region will expand the fastest through 2031?

The Middle East and Africa is projected to grow at a 12.7% CAGR on smart-city and hyperscale data-center investments.

Page last updated on: