Cobalt Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

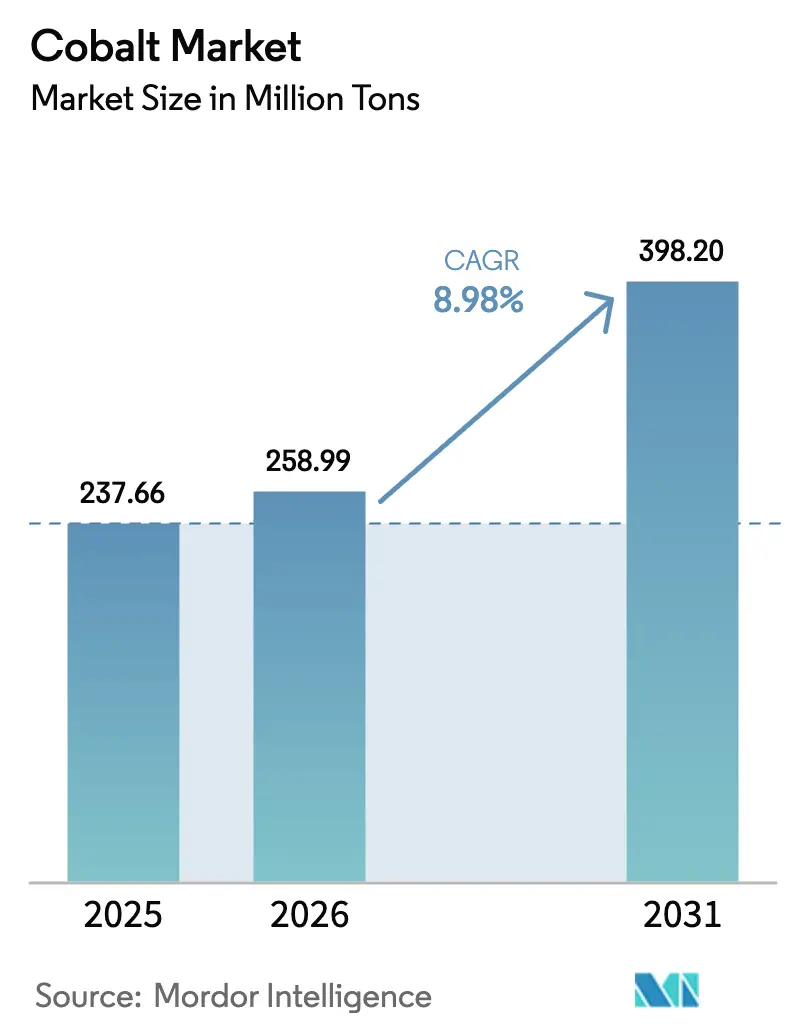

| Market Volume (2026) | 258.99 Million tons |

| Market Volume (2031) | 398.2 Million tons |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

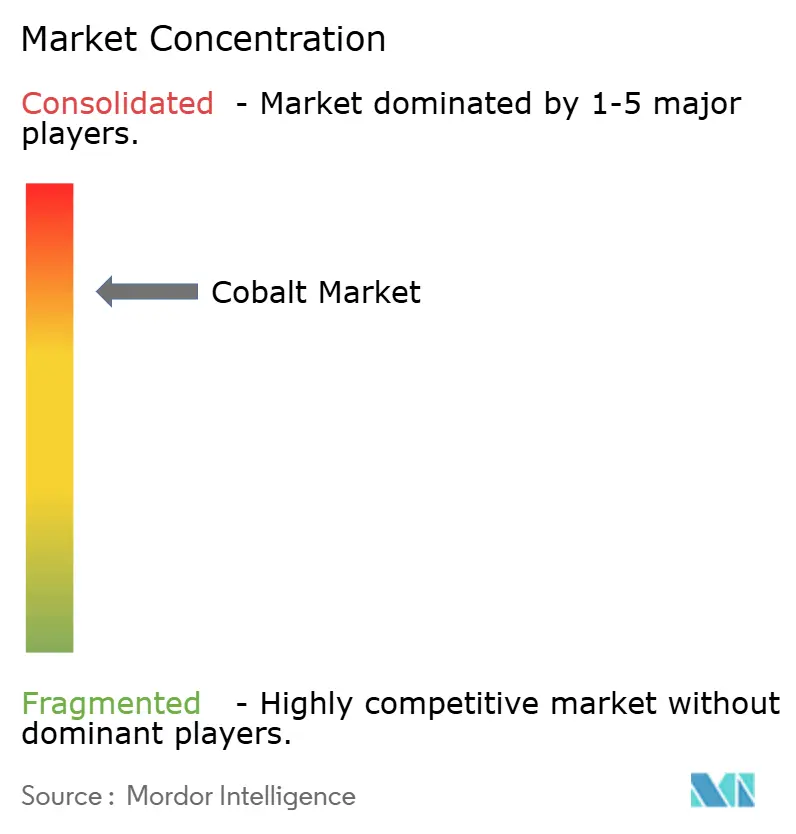

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cobalt Market Analysis by Mordor Intelligence

Cobalt market size in 2026 is estimated at 258.99 Million tons, growing from 2025 value of 237.66 Million tons with 2031 projections showing 398.2 Million tons, growing at 8.98% CAGR over 2026-2031. Robust demand for battery‐grade sulfate, aerospace superalloys, and high-performance magnetic alloys is expanding the market even as refined output struggles to keep up. Supply security remains a central theme because the Democratic Republic of Congo (DRC) delivers 76% of mined cobalt; a four-month export suspension in early 2025 drove spot prices sharply higher, exposing systemic vulnerability to policy shocks. Outside Central Africa, Indonesia’s high-pressure acid-leach projects and scattered North American sulfide developments will add new tons. End-use diversity further underpins the cobalt market because batteries, aerospace, defense machining, and 5 G hardware each contribute independent growth streams that dilute the impact of cyclical swings in any single sector.

Key Report Takeaways

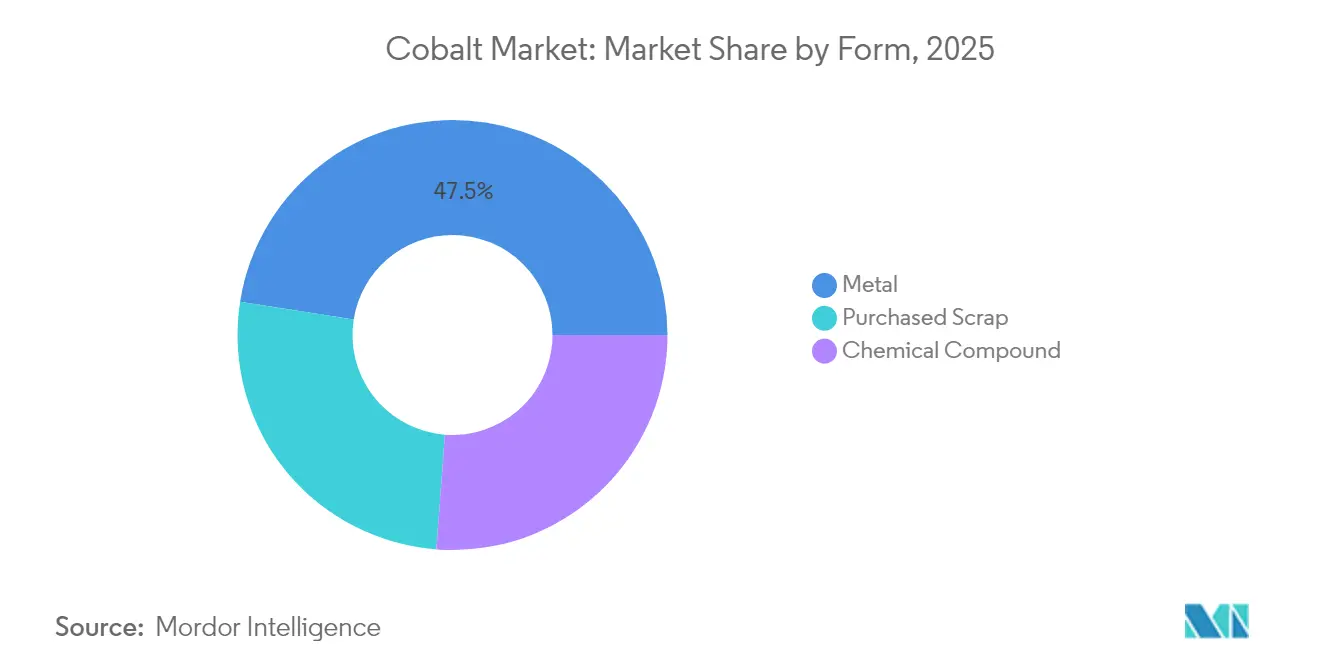

- By form, metal led with 47.52% cobalt market share in 2025, while purchased scrap is forecast to expand at a 10.82% CAGR between 2026 and 2031.

- By application, batteries accounted for 57.65% of the cobalt market size in 2025 and are poised for an 11.63% CAGR to 2031.

- By production source, primary mining supplied 81.55% of the 2025 output; secondary supply records the fastest growth at a 10.14% CAGR through 2031.

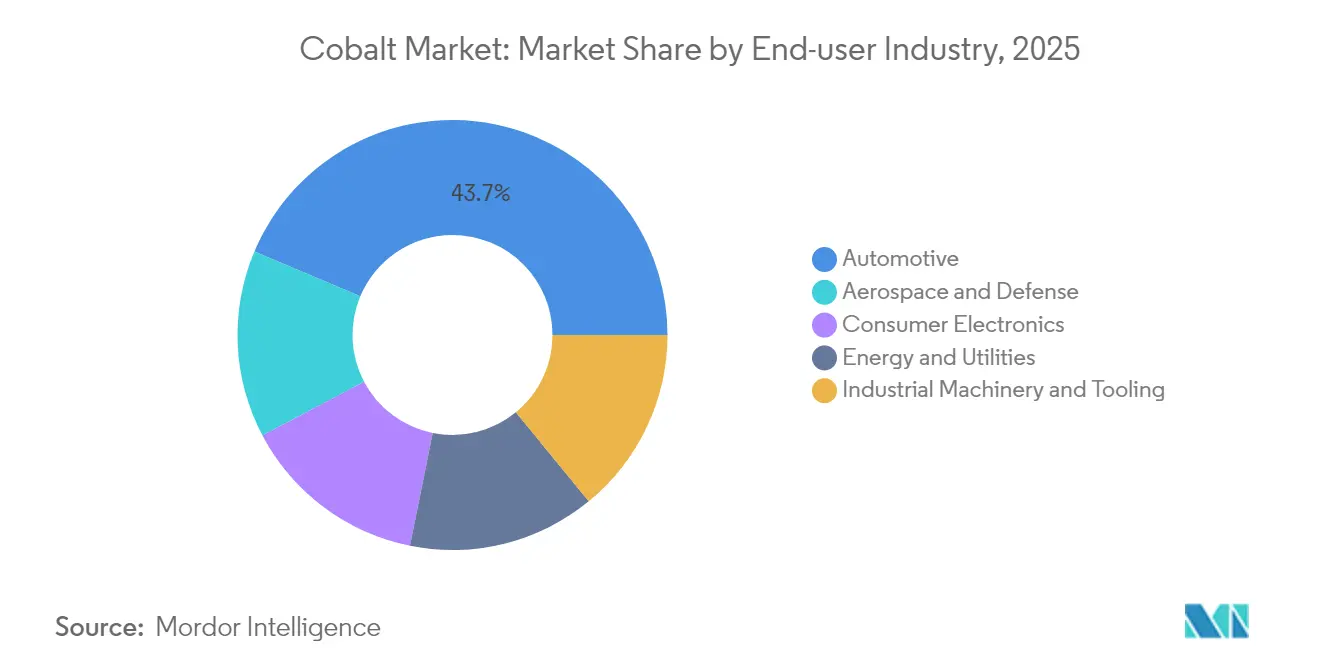

- By end-user industry, automotive commanded 43.65% cobalt market share in 2025 and shows the highest forward CAGR of 14.89%.

- By geography, Asia-Pacific held 51.32% cobalt market share in 2025 and is projected to grow at an 11.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cobalt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Usage in rechargeable batteries | +3.2% | Global – China, Europe, North America | Medium term (2-4 years) |

| Superalloy demand from engine restarts | +1.1% | North America, Europe, China | Short term (≤ 2 years) |

| High-speed cutting tools | +0.7% | North America, Europe, China | Short term (≤ 2 years) |

| 5 G/IoT magnetic materials | +0.8% | East Asia early-adopter cluster | Medium term (2-4 years) |

| Regulatory Push for Conflict-Free, Traceable Cobalt Supply Chains | +0.5% | Global, with emphasis on EU, North America | Long term |

| Source: Mordor Intelligence | |||

Rising Usage in Rechargeable Batteries

Battery manufacturers consumed over half of total cobalt demand in 2024, driven by record electric-vehicle (EV) sales exceeding 17 million units. Even with ongoing efforts to reduce cobalt intensity in nickel-rich NCM cathodes, the metal remains essential for high-voltage stability and long cycle life. Major cell producers are actively stockpiling cobalt sulfate to hedge against price volatility, a strategy that amplifies short-term market swings. The practice also supports government designation of cobalt as a strategic material, unlocking public financing for new refining and recycling assets. These feedback loops strengthen the cobalt market by ensuring that supply-side investments track expanding battery footprints.

Growing Demand for Superalloys from Commercial Aerospace Engine Restarts

Commercial jet output has rebounded, and turbine manufacturers have restarted lines that rely on cobalt-rich discs and combustor liners. NATO’s 2024 defense-critical raw-materials list explicitly includes cobalt, highlighting the alloy’s irreplaceable heat resistance[1]European Commission, “CNSTech Programme Results,” cordis.europa.eu. With backlogs above 12,000 aircraft, original equipment makers forecast high-single-digit growth in superalloy demand through 2030. Qualification barriers deter substitution, so aero-engine offtake contracts offer miners and refiners a predictable, high-margin outlet. This stable pull complements the more volume-driven battery segment and supports long-term allocations.

Increasing Adoption of Cobalt-Rich Cutting Tools

Cobalt levels between 8% and 20% are now common in cemented-carbide tools machining next-generation nickel and titanium aerospace parts. The EU-funded CNSTech program demonstrated cobalt-based high-entropy alloys that outperform traditional nickel grades in thermal-fatigue tests[2]North Atlantic Treaty Organization, “Defence-Critical Raw Materials List 2024,” nato.int . Tool makers report solid order books as airlines accelerate engine overhauls, signalling that this specialized demand will retain premium pricing. Because margins on cutting-tool alloys exceed those on battery chemicals, miners are keen to protect allocations to tooling customers, reinforcing diversified demand within the cobalt market.

Accelerated 5G/IoT Roll-Out Driving High-Frequency Magnetic Materials

Telecom vendors are adopting cobalt-based amorphous and nanocrystalline alloys for compact gigahertz-grade filters and antennas. These materials exhibit high permeability and low coercivity, enabling lower power consumption in 5 G radios. As connected devices multiply into the tens of billions, specialized ribbon and powdered cores enlarge the customer base beyond mobility and machining. Diversification lowers the probability that any single technology pivot, such as cobalt-free batteries, could derail aggregate growth, supporting resilience in the cobalt market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex refining from ore | −1.2% | DRC, Indonesia | Medium term (2-4 years) |

| Limited solvent extraction outside China | −1.8% | All except China | Long term (≥ 4 years) |

| ESG and Human Rights Scrutiny Increasing Supply Chain Costs | -0.9% | Global, with emphasis on DRC | Medium term |

| Source: Mordor Intelligence | |||

Complex Refining from Ore

Most cobalt originates as a by-product of copper or nickel mining, and complex mineralogy complicates downstream hydrometallurgy. High-pressure acid-leach circuits in the DRC and Indonesia face permitting hurdles, reagent logistics, and energy constraints. These challenges slow capacity ramp-ups and raise operating costs, restraining near-term supply growth in the cobalt market. Policy pressure for more environmentally managed flows adds further capital requirements that extend project timelines.

Limited Solvent Extraction Capacity Outside China

China hosts most of the solvent-extraction and crystallization infrastructure required for battery-grade cobalt chemicals. Emerging projects in Europe and North America strain to secure proprietary extractants and engineering talent, delaying diversification. As a result, non-Chinese refiners pay premiums for intermediates or must ship mixed hydroxide back to Asia, adding freight and working-capital burdens. Unless new regional plants reach scale, the cobalt market will continue to exhibit geographic bottlenecks that temper supply elasticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Growing Dominance of Metal and Recycled Feedstock

Metal accounted for 47.52% of the cobalt market share in 2025, reflecting versatile use in superalloys, cutting tools, and soft magnetic components. High-temperature alloy producers lock in multi-year contracts to secure consistent quality, and recent price spikes led several aerospace primes to negotiate toll-refining deals that guarantee physical delivery, further tightening spot availability. Preference for long-term offtake could lengthen lead times for smaller buyers, encouraging exploration of recycled briquettes as a hedge.

The purchased-scrap sub-segment is forecast to post a 10.82% CAGR from 2026 to 2031 as regional battery recycling plants ramp up. Regulatory quotas for recycled content, paired with economic gains from recovering nickel and lithium, make cobalt extraction from black mass financially attractive even at moderate prices. Companies such as Electra Battery Materials are building hydrometallurgical circuits dedicated to scrap, signalling confidence in steady feedstock supply. Over time, increasing secondary flows will erode metal’s dominance in the cobalt market while elevating resource efficiency.

By Application: Batteries Maintain Majority Share Amid Alloy Resilience

Batteries represented 57.65% of the cobalt market size in 2025 and are on track for an 11.63% CAGR to 2031, powered by EV rollouts and premium consumer electronics. Nickel-rich NCM cathodes still incorporate 10%–15% cobalt to maintain lattice stability under fast-charge conditions, a requirement unlikely to disappear in the medium term. Even partial thrifting leaves absolute tonnage needs high because total cell output is expanding so quickly.

Outside batteries, alloy applications hold a durable niche in gas-turbine engines, while catalysts gain traction from cobalt-based Fischer–Tropsch routes that convert captured CO₂ into synthetic aviation fuel. Magnetic powders enjoy steady growth alongside 5G base-station deployments, and ceramic pigments move to lower‐cobalt blends that still meet color fastness standards. This broad portfolio allows the cobalt market to absorb moderate substitution in one application without derailing overall growth.

By Production Source: Primary Mining Remains Dominant, but Secondary Supply Scales

Primary mining delivered 81.55% of global cobalt output in 2025, underpinned by DRC copper–cobalt ores. When the DRC temporarily halted exports, quarter-on-quarter prices advanced despite soft demand, underscoring high concentration risk. Indonesia’s HPAL projects will raise cobalt output to mid-double-digit kiloton levels by 2030, adding geographic diversity and attracting advance offtake agreements from non-Chinese refiners seeking to hedge Central African exposure.

Secondary supply is the fastest-growing source, with a projected 10.14% CAGR through 2031. The International Energy Agency estimates that recycling could cut the need for virgin cobalt by up to 40% by mid-century. Rising volumes of spent EV batteries and consumer devices create predictable feedstock flows, anchoring new hydrometallurgical capacity in jurisdictions with strict environmental standards. Shorter transport distances and lower carbon footprints strengthen the sustainability narrative across the cobalt market.

By End-User Industry: Automotive Accelerates While Aerospace Sustains High Margins

Automotive commanded 43.65% cobalt market share in 2025 and shows the highest forward CAGR of 14.89% as policy incentives amplify EV adoption. Original equipment manufacturers have moved upstream through direct procurement and joint-venture mine stakes, signalling that secure cobalt supply is now a board-level priority. Suppliers able to certify traceability stand to win longer contracts at premium prices, supporting investment in responsibly managed operations.

Aerospace and defense consume smaller volumes yet demand superalloys with very high cobalt percentages, multiplying value per kilogram. Air-traffic recovery and military modernization programs ensure a steady, high-margin outlet. Electronics maintains relevance for lithium-cobalt-oxide batteries in smartphones and laptops, though growth is moderating as replacement cycles lengthen. Industrial tools and machinery provide an enduring baseline demand, giving the cobalt market a balanced portfolio across end industries.

Geography Analysis

Asia-Pacific held 51.32% cobalt market share in 2025 and is forecast to grow at an 11.03% CAGR to 2031. China refines a major portion of the global cobalt chemicals and maintains equity stakes in many DRC mines, securing an integrated mine-to-cathode chain that underpins its battery dominance. South Korea and Japan have responded by taking minority stakes in Indonesian HPAL ventures, pointing toward a more multipolar supply map later in the decade. Heightened competition for concentrates meeting stringent ESG criteria is already driving premium payments.

North America is accelerating supply-chain localization under the United States Inflation Reduction Act and Defense Production Act. In August 2024, the Department of Defense granted USD 20 million to Electra Battery Materials to establish sustainable cobalt-sulfate refining. Europe sustains sizable downstream demand through a growing battery-cell ecosystem backed by the EU Battery Regulation, which links market access to life-cycle reporting.

Competitive Landscape

The cobalt industry exhibits high consolidation. The top five miners control most ore, but a wider set of refiners and recyclers manage downstream chemistry. Chinese groups such as CMOC and Zhejiang Huayou leverage integrated mine-to-chemical chains to secure bargaining power with cathode makers. European and North American buyers are countering by underwriting non-Chinese capacity, as evidenced by long-term offtake agreements between automakers and emerging producers in Australia and Canada. These moves signal a gradual shift from a global supply oligopoly toward regionally ring-fenced value chains, each with distinct pricing.

Cobalt Industry Leaders

CMOC

Eurasian Resources Group

Glencore

Huayou Cobalt Co., Ltd.

Vale S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Glencore stated that a large portion of its cobalt production might remain unsold by 2025 due to the Democratic Republic of Congo's cobalt export ban, aimed at reducing global oversupply.

- October 2023: Eurasian Resources Group signed a five-year memorandum with EVelution Energy to deliver cobalt hydroxide to a planned processing plant in the United States.

Global Cobalt Market Report Scope

The chemical symbol of cobalt is Co, and the atomic number is 27. It is a hard, lustrous, silver-gray metal that belongs to the transition metal group in the periodic table. Cobalt is commonly found in the Earth's crust in mineral ores such as cobaltite, erythrite, and smaltite, often associated with other metals such as nickel, copper, and arsenic.

The cobalt market is segmented by form, product type, application, and geography. By form, the market is segmented into chemical compounds, metals, and purchased scrap. By application, the market is segmented into batteries, alloys, catalysts, tool materials, magnets, ceramics, pigments, and other applications (medical devices). The report also covers the market size and forecasts for the cobalt market in 11 countries across major regions. For each segment, market sizing and forecasts were made based on volume (tons).

| Chemical Compound |

| Metal |

| Purchased Scrap |

| Batteries |

| Alloys |

| Catalysts |

| Tool Materials |

| Magnets |

| Ceramics and Pigments |

| Other Applications |

| Primary |

| Secondary |

| Automotive |

| Aerospace and Defense |

| Consumer Electronics |

| Energy and Utilities |

| Industrial Machinery and Tooling |

| Australia |

| Canada |

| China |

| Democratic Republic of Congo |

| Cuba |

| Indonesia |

| Morocco |

| Russia |

| United States |

| Rest of World |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Chemical Compound | |

| Metal | ||

| Purchased Scrap | ||

| By Application | Batteries | |

| Alloys | ||

| Catalysts | ||

| Tool Materials | ||

| Magnets | ||

| Ceramics and Pigments | ||

| Other Applications | ||

| By Production Source | Primary | |

| Secondary | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Consumer Electronics | ||

| Energy and Utilities | ||

| Industrial Machinery and Tooling | ||

| Geography (Production) | Australia | |

| Canada | ||

| China | ||

| Democratic Republic of Congo | ||

| Cuba | ||

| Indonesia | ||

| Morocco | ||

| Russia | ||

| United States | ||

| Rest of World | ||

| Geography (Consumption) | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the cobalt market?

The cobalt market size is 258.99 million tons in 2026 and is forecast to reach 398.2 million tons by 2031.

Which segment dominates cobalt consumption today?

Rechargeable batteries account for 57.65% of the cobalt market size in 2025 due to strong electric-vehicle demand.

How dependent is supply on the Democratic Republic of Congo?

The DRC supplies 76% of mined cobalt, making the global supply chain highly sensitive to policy changes in that country.

What growth rate is expected for automotive demand?

Automotive applications are projected to grow at a 14.89% CAGR, the fastest among end-use industries

Can recycling significantly reduce primary cobalt requirements?

Yes. The International Energy Agency estimates recycling could displace up to 40% of virgin cobalt needs by mid-century, and secondary supply already shows a 10.14% CAGR outlook.

Page last updated on: