Egypt Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

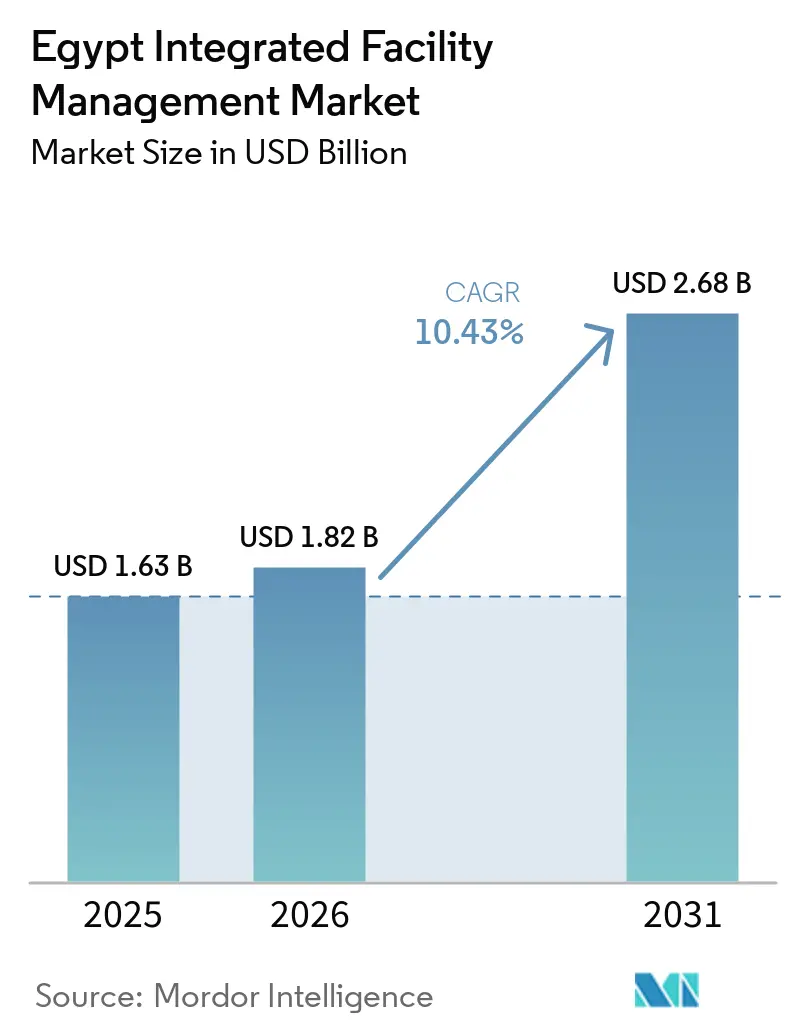

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 10.43% CAGR |

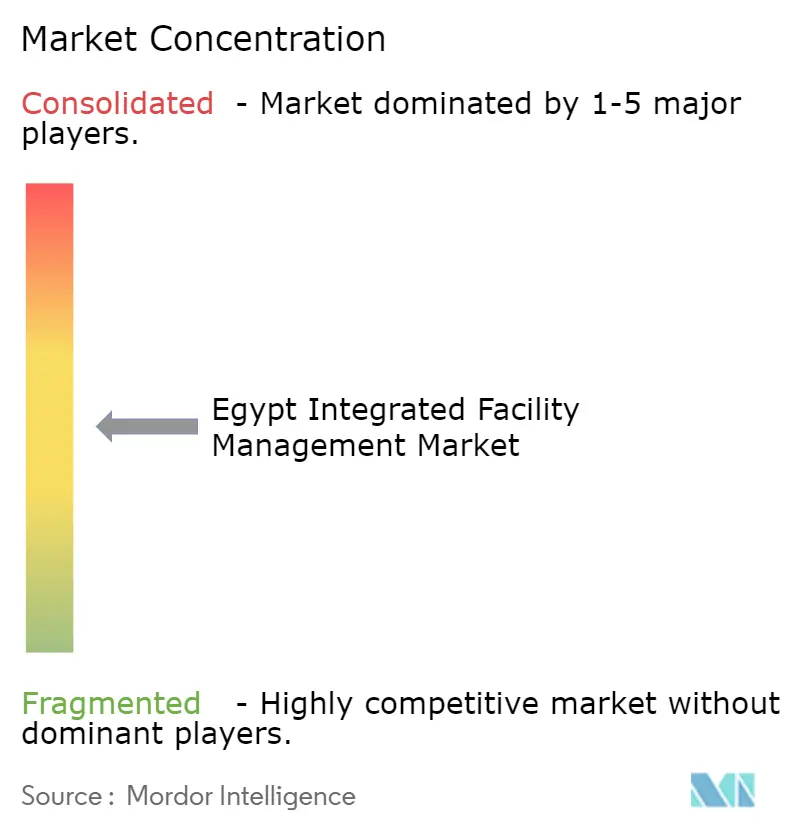

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Integrated Facility Management Market Analysis by Mordor Intelligence

The Egypt integrated facility management market size is expected to increase from USD 1.63 billion in 2025 to USD 1.82 billion in 2026 and reach USD 2.68 billion by 2031, growing at a CAGR of 10.43% from 2026 to 2031. The Egypt integrated facility management (IFM) market is being shaped by a large pipeline of new operating assets linked to the New Administrative Capital and other state-backed urban developments, which are expanding the need for professional operations and maintenance from the first day of occupancy. Clients are also moving toward integrated contracts that combine hard and soft services because they want clearer performance tracking, easier vendor management, and better visibility on asset life cycle costs. The Egypt IFM market is therefore growing not only because more buildings are entering service, but also because the contract model is shifting toward larger and more technical scopes. Compliance needs tied to energy efficiency, green building standards, and digital building systems are also raising the value of capable providers that can support measurable operating outcomes.

Key Report Takeaways

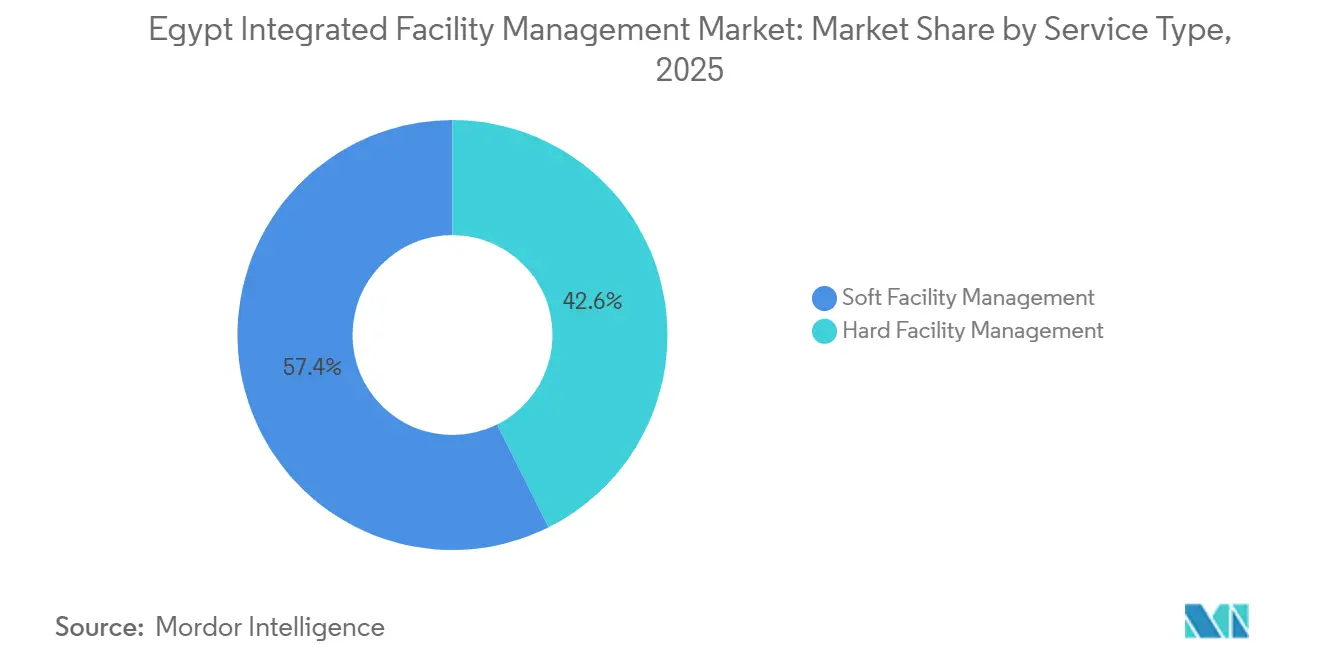

- By service type, soft facility management segment held 57.38% share of revenue in 2025, while hard facility management segment in the Egypt integrated facility management market is projected to expand at a 10.49% CAGR through 2031.

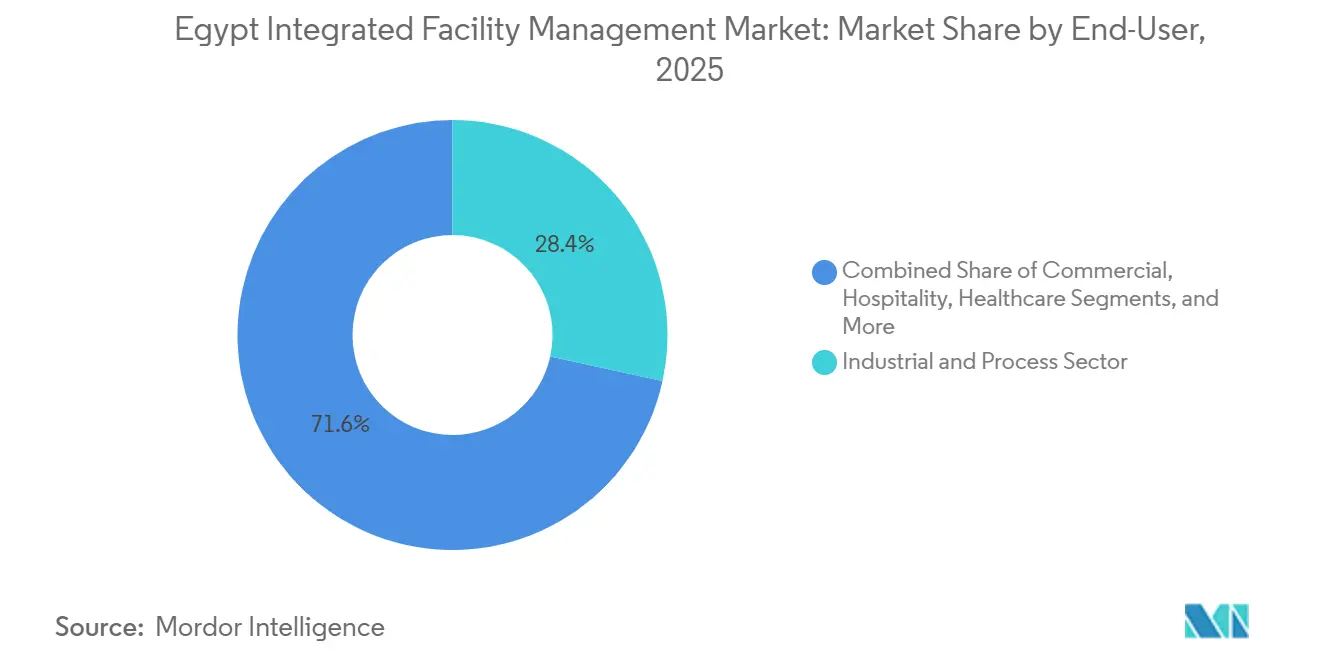

- By end user, the industrial and process segment held 28.44% share in 2025, while the commercial segment in the Egypt integrated facility management (IFM) market is projected to grow at a 10.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Commercial Real Estate in New Administrative Capital | +2.8% | Greater Cairo and New Capital, with spillover to New Cairo and October City | Short term (≤ 2 years) |

| Government Push for Public-Private Partnerships in Infrastructure O&M | +2.2% | National, with early gains in Cairo, Suez, and Alexandria | Medium term (2-4 years) |

| Rising Energy Efficiency Mandates Driving Demand for Smart FM Solutions | +1.8% | National, concentrated in commercial and industrial centers | Medium term (2-4 years) |

| Growing Foreign Direct Investment in Industrial Zones and Freeports | +1.5% | Suez Canal Zone, 10th of Ramadan, New Borg El-Arab, and New Alamein | Medium term (2-4 years) |

| Post-COVID Shift Toward Outsourcing Non-Core Services for Cost Optimization | +1.2% | National, strongest in Cairo and Alexandria CBDs | Short term (≤ 2 years) |

| Adoption of Building Information Modeling for Lifecycle FM Optimization in Egypt | +0.8% | New Administrative Capital, New Cairo, and major new-build commercial districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Commercial Real Estate in New Administrative Capital

The New Administrative Capital has become the strongest single demand center for the Egypt integrated facility management (IFM) market because it concentrates new government, office, hospitality, and retail assets in one operating zone. The Central Business District alone includes 20 towers with 806,000 square meters of administrative and commercial floor space, which means a large volume of building systems must move quickly from construction delivery to managed operations. That scale supports recurring demand for cleaning, security, technical maintenance, energy management, and front-of-house services under integrated contracts. It also changes the bidding environment because winning flagship sites in the New Capital is strategically important for providers that want long-term visibility and stronger credentials for future tenders. The pressure point is that many qualified firms are chasing the same pipeline, so margins can tighten on marquee contracts even while contract values rise. Phase II development across another 40,000 feddans will keep the Egypt integrated facility management market tied to this location through the forecast period.

Government Push for Public-Private Partnerships in Infrastructure O&M

Public-private partnerships are widening the addressable scope of the Egypt IFM market because operations and maintenance are becoming part of the state’s broader infrastructure delivery model. Egypt’s Ministry of Finance announced 8 new PPP projects in June 2025 with a total value of EGP 40 billion, equal to USD 812.5 million using the 2025 IRS average exchange rate, across desalination, wastewater, electricity substations, and waste recycling.[1]Ministry of Finance, “Official Ministry of Finance Website,” Government of Egypt, mof.gov.eg These assets matter for FM providers because they usually come with long-duration operating requirements and a closer link between service delivery, uptime, and public accountability. The procurement cycle is still difficult because operators need to work across investment bodies and line ministries, which raises tender complexity and favors firms with stronger compliance and project management capability. That favors companies that can manage documentation, reporting, and technical standards at the same time rather than only supply labor. As more public assets shift toward outsourced O&M structures, the Egypt integrated facility management (IFM) market is likely to see a larger share of revenue come from long-tenure contracts rather than short renewal cycles.

Rising Energy Efficiency Mandates Driving Demand for Smart FM Solutions

Energy regulation is moving the Egypt integrated facility management market toward smarter and more accountable service delivery because building performance is becoming a compliance issue as well as a cost issue. The Ministry of Housing, Utilities and Urban Communities, working with the Egyptian Green Building Council, introduced a national green building strategy that requires new public buildings to achieve at least Tier 2 certification from January 2026. That raises the role of FM teams because maintaining certification depends on consistent control of energy use, water use, operating records, and service response. Egypt’s State Information Service reported in January 2025 that energy efficiency measures had saved the country USD 900 million in 10 months, which reinforces the policy view that operating efficiency has national importance.[2]State Information Service, “Official State Information Service Website,” Arab Republic of Egypt, sis.gov.eg The financing link is also becoming clearer because EDGE-certified assets have been used as measurable benchmarks for sustainability-linked lending, including Orascom Development’s USD 155 million IFC facility for El Gouna hotels. Providers that can show verified reductions in operating consumption are therefore supporting client financing outcomes as well as day-to-day building performance in the Egypt integrated facility management (IFM) market.

Growing Foreign Direct Investment in Industrial Zones and Freeports

Foreign investment is widening the industrial client base for the Egypt integrated facility management market because new tenants in free zones and industrial clusters need dependable hard FM support from the start of operations. Egypt recorded 152 new free zone projects in 2025, taking the total to 1,243 projects with invested capital of USD 14.2 billion. UNCTAD also reported in January 2026 that Egypt ranked first in Africa for FDI inflows for the fourth consecutive year, which supports the view that industrial and logistics demand will stay active.[3]United Nations Conference on Trade and Development, “Official UNCTAD Website,” United Nations, unctad.org GAFI is overseeing 4 new public free zones in 10th of Ramadan, New October, New Borg El-Arab, and New Alamein, with operations targeted by the end of 2026 after high occupancy in existing zones. Each new industrial cluster increases demand for MEP maintenance, fire systems, asset management, and reporting tools that many smaller soft-service operators cannot provide. This gives better-positioned vendors in the Egypt IFM market a route into multi-site contracts with multinational manufacturers that prefer standardized procurement, ISO-led compliance, and digital reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Vendor Landscape Limiting Standardized Service Quality | -0.9% | National, most acute in secondary cities including Upper Egypt and the Delta region | Medium term (2-4 years) |

| Persistent Delays in Government Payment Cycles Affecting Cash Flow | -0.7% | National, concentrated in public-sector contracts in Cairo and Giza | Short term (≤ 2 years) |

| Shortage of Certified Facility Management Professionals in Egypt | -0.5% | National, most critical in New Administrative Capital and emerging smart-city projects | Long term (≥ 4 years) |

| High Customs Duties on Specialized FM Equipment Hindering Technology Adoption | -0.4% | National, with highest impact on hard FM technology deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Vendor Landscape Limiting Standardized Service Quality

The Egypt integrated facility management (IFM) market still carries a large long tail of small and mid-sized operators with uneven service depth, technology use, and balance-sheet strength. That fragmentation keeps price competition intense in routine outsourcing categories because many buyers still compare offers mainly on labor cost rather than performance consistency. The result is lower average contract value and weaker confidence in multi-year integrated agreements, especially outside the top tier of corporate and government assets. The push to develop an Egyptian FM Code in collaboration with the Housing and Building National Research Center shows that standardization has become a central market issue, especially for contract quality and vendor qualification. Without firmer operating standards, clients can move between vendors with limited switching friction, which slows the transition from simple outsourcing to deeper service partnerships. This restraint matters across the Egypt IFM market, but it is more visible in secondary cities where formal procurement filters are lighter and quality benchmarks are less consistently enforced.

Persistent Delays in Government Payment Cycles Affecting Cash Flow

Payment delays remain a practical constraint on the Egypt integrated facility management market because public assets still account for an important share of demand across ministerial buildings, hospitals, universities, and infrastructure facilities. When payment cycles extend beyond contractual terms, working capital pressure rises quickly and mid-sized operators face the greatest stress because they have fewer financing options. That changes competition because larger firms with credit lines can absorb delays for longer periods, while smaller firms either reduce service intensity or step away from public-sector tenders. The result is a narrower field for complex public contracts even though the addressable demand remains attractive. The EBRD’s USD 100 million investment in AAIB’s sustainability bond shows that development finance is flowing into the built environment, but that support has not yet translated into meaningful working-capital solutions for FM vendors. Until that funding gap narrows, cash conversion risk will remain a limiting factor for expansion in the Egypt IFM market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Gaining Ground in a Soft-Dominated Market

Soft Facility Management (Soft FM) Services held 57.38% of the market in 2025, which means this category represented the largest part of the Egypt integrated facility management market share during the base year. The dominance came from cleaning, catering, office support, and security contracts, which were already more widely outsourced across hospitality, healthcare, and commercial real estate. These services were often the first outsourced functions because clients could assess quality through visible daily outcomes and did not need complex technical integration to start a contract. Catering also benefited from renewed demand in hotels and institutional settings tied to expansion in coastal developments and new-city projects. Other soft FM activities such as pest control, landscaping, and waste management helped local providers raise wallet share within existing accounts by widening service scope rather than relying only on new client wins.

Hard Facility Management (Hard FM) Services is expected to grow at a 10.49% CAGR from 2026 to 2031, making it the fastest-growing service category in the Egypt integrated facility management (IFM) market. This pace reflects the technical profile of new assets, especially smart buildings that use SCADA-linked HVAC, fire systems, and digital controls that need more than routine mechanical support. A 2025 study in Engineering, Technology and Applied Science Research found that integrating building management system data with FM software platforms was a primary technical barrier to BIM adoption in Egypt, which supports the view that technically stronger providers can command better pricing. Asset management and MEP and HVAC services remain the largest hard FM activities because commercial offices, industrial sites, and infrastructure assets depend on uptime and system reliability. Fire systems and safety are also becoming more important as taller mixed-use developments and more complex occupancy profiles expand the technical demands placed on the Egypt integrated facility management industry.

By End User: Industrial Dominance Meets a Commercial Surge

The Industrial and Process Sector held 28.44% of the market in 2025, which gave it the leading position in the Egypt integrated facility management (IFM) market size among end-user groups. This lead reflects the value of long-duration O&M contracts in manufacturing, energy, mining, and process-heavy environments where equipment uptime directly affects output and asset utilization. Industrial buyers also tend to favor service-level agreements with clear repair metrics, escalation protocols, and penalty structures, which supports recurring revenue and deeper operational involvement from providers. Egypt’s petrochemicals, cement, and fertilizer activities remain the core of this demand base, while the free zone manufacturing pipeline continues to add new addressable sites. Energy management is increasingly being bundled into these contracts because industrial clients are under pressure to manage electricity costs and operate assets with greater efficiency.

The Commercial segment is expected to grow at a 10.73% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the Egypt IFM market. Demand is being lifted by the spread of banking, fintech, telecom, retail, and warehousing assets into new urban districts and logistics corridors. These occupiers typically want integrated contracts because they need workspace services, technical maintenance, security, cleaning, and reporting in one operating framework rather than through multiple vendors. Hospitality and healthcare remain meaningful mid-tier demand pools, with hospitality supported by tourism-linked development and healthcare supported by growing outsourcing in both public and private settings. Institutional and public infrastructure also remain important because airport, railway, and government assets increasingly require structured service delivery, while residential, entertainment, sports, and leisure uses are building relevance as gated communities seek broader operating support from the Egypt integrated facility management industry.

Geography Analysis

Greater Cairo remained the dominant demand cluster in 2025 and it continues to anchor the Egypt integrated facility management market in 2026. This concentration comes from the mix of government assets, commercial buildings, industrial corridors, and newly delivered stock across the New Administrative Capital, New Cairo, and the 10th of Ramadan City corridor. The New Administrative Capital alone added more than 806,000 square meters of commercial floor space in its Central Business District, which turned project completions into live operating contracts as occupancy progressed. The earlier relocation of ministries had already converted planned demand into active operational requirements, and continuing development activity in 2026 is reinforcing Cairo’s role as the main contracting center for large integrated assignments. Phase II expansion across another 40,000 feddans means the Egypt integrated facility management (IFM) market will continue to be led by this geography throughout the forecast period.

Alexandria and the Mediterranean coastal corridor form the second major geographic cluster for the Egypt integrated facility management market. This area benefits from a large installed base of industrial and commercial assets, active logistics activity around ports, and a broader hospitality footprint along the North Coast. The integrated FM award for the SAWARI Complex in Alexandria in February 2025 showed that institutional-grade expectations are spreading beyond Greater Cairo and into other urban nodes with large mixed-use projects. The Suez Canal Economic Zone and Red Sea coastal belt add a third important sub-market because manufacturing, energy infrastructure, and tourism assets in those locations depend more heavily on hard FM capability and consistent technical service delivery.

Upper Egypt and other secondary governorates remain less penetrated by credentialed operators, so much of the service base still comes from informal or single-service vendors. That weakens standardization and keeps the quality gap wide between tier-1 locations and the rest of the country. The Egyptian FM Code under discussion is the main policy lever that could narrow this gap by creating clearer operating expectations across regions. Green building specifications are also beginning to appear more often outside the main cities, which creates a compliance path for vendors with stronger energy management capability. Over time, this geographic diffusion will widen the addressable base of the Egypt IFM market even if Greater Cairo continues to hold the largest contract values.

Competitive Landscape

The Egypt integrated facility management market is moderately fragmented, with the highest competitive intensity concentrated in Greater Cairo and New Capital contracts where scope, visibility, and technical thresholds are strongest. International operators such as EFS Facilities Services Group, Sodexo Egypt, ISS A/S, and CBRE Group compete for larger integrated assignments, especially in commercial, industrial, and government-linked assets. Local operators such as Orascom Facility Management, Eden Facility Management, FMG Egypt, and Egy Trans Facility Management remain important because they understand domestic procurement, compliance, and service delivery conditions. The broader market still includes many smaller single-service firms, and that split creates one competitive arena for complex integrated work and another for price-driven commodity services. EFS illustrates the upper tier of this structure because it operates across 27 countries, offers more than 75 service lines, and manages over 75 million square meters through 40 operating companies globally.

Competition is shifting from simple scale toward service breadth, digital capability, and the ability to manage measurable outcomes. Providers that can bundle fire safety, pest control, food services, workplace support, and technical maintenance under one platform are better placed to increase revenue per client without competing only on headline price. The market is also opening space for smart-building integrators that can connect asset data, occupancy management, and performance reporting in one operating model. This matters because new government and commercial assets are being handed over with more digital infrastructure than older buildings, which raises the value of data-led service delivery. The Egypt integrated facility management (IFM) market is therefore rewarding firms that can combine labor management with systems integration, reporting discipline, and better visibility on operating efficiency.

Digital FM remains underused outside the top tier, which leaves room for stronger differentiation over the next several years. Predictive maintenance, CAFM deployment, IoT-enabled monitoring, and asset life cycle tools are not yet widespread, but they are becoming more relevant as clients ask for better uptime and documented savings. ISO 41001 is not yet mandated, but it is beginning to appear as a prequalification marker in larger tenders, which raises the barrier for smaller vendors without structured management systems. Building automation companies such as Johnson Controls International and Honeywell International also have an advantage because they can extend existing hardware relationships into operating service agreements. That vertical model increases competitive pressure on pure-play FM firms in the Egypt IFM market, especially where clients prefer one accountable counterparty for both systems and services.

Egypt Integrated Facility Management Industry Leaders

Sodexo Egypt

Enova Facilities Management Services LLC

EFS Facilities Services Group

CBRE Group, Inc.

Compass Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ÈLM Developments signed a management and operations agreement with Savills Egypt for the ÈLM Tree Business Center. The agreement covers operational consultancy, leasing, cost management, and integrated facility management services.

- April 2026: Saudi-based Bravo Facility Management partnered with Ebdaa Development to launch Ouda Developments with planned investments exceeding EGP 50 billion between 2026–2029, integrating FM expertise into mixed-use community developments.

- March 2026: Triumph Hotels and M|A Group announced a partnership to develop and operate the Triumph Pyramids Hotel project in West Cairo, strengthening Egypt’s hospitality facility management segment.

- February 2026: Inertia Egypt announced expansion plans including new mixed-use developments and enhanced operational infrastructure across Cairo and Ras El Hekma, creating additional long-term demand for integrated facility management services.

- January 2026: Eltizam Egypt was appointed to manage and operate Val Plaza Mall in West Cairo. The company expanded its Egyptian IFM footprint, with more than 120 contracts and over 2 million sqm of managed assets nationwide.

Egypt Integrated Facility Management Market Report Scope

The Egypt Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User | ||

Key Questions Answered in the Report

What is the current value of Egypt integrated facility management activities in 2026?

The 2026 value stands at USD 1.82 billion, and the projected 2031 value is USD 2.68 billion with a forecast CAGR of 10.43%.

Which service category leads demand in Egypt?

Soft FM Services led in 2025 with a 57.38% share, supported by established outsourcing in cleaning, security, catering, and office support.

Which service category is expanding the fastest through 2031?

Hard FM Services is projected to grow at a 10.49% CAGR because newer assets require stronger technical maintenance, MEP support, and systems integration.

Which end-user group generates the largest revenue base?

The Industrial and Process Sector led in 2025 with a 28.44% share because long-duration O&M contracts are common in manufacturing, energy, and process facilities.

Why is the Commercial segment growing so quickly in Egypt?

The Commercial segment is expected to grow at a 10.73% CAGR as banking, telecom, retail, and warehousing assets expand into new urban districts and logistics corridors.

Page last updated on: