Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

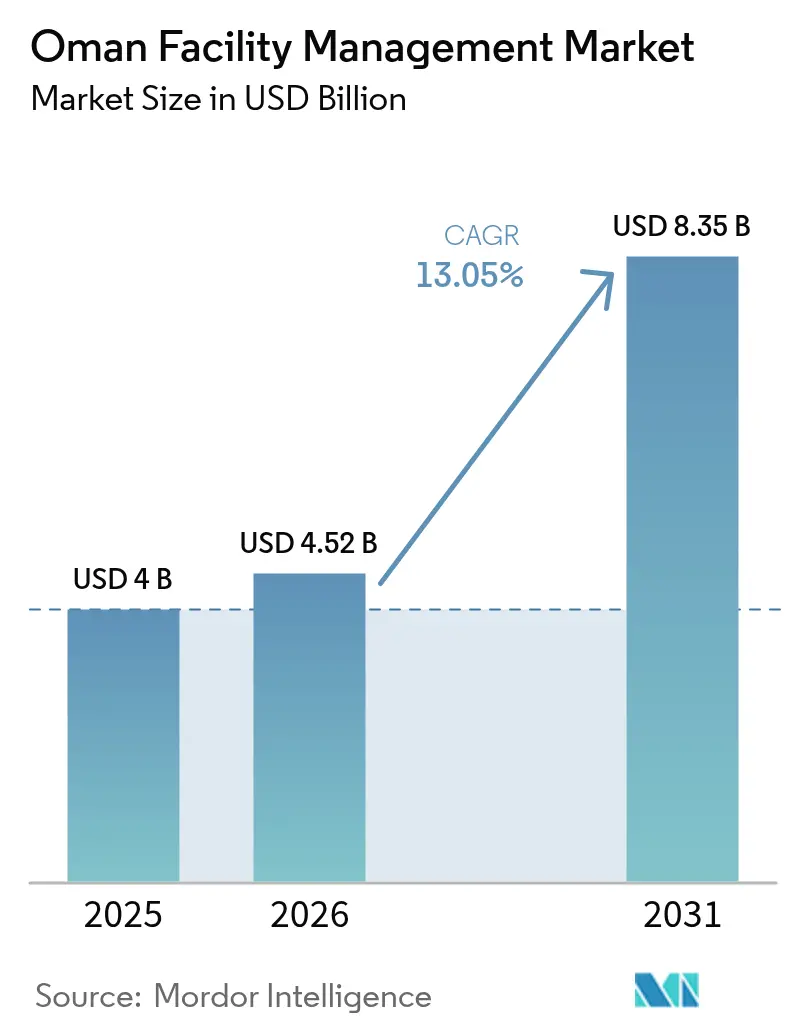

| Base Year Market Size (2025) | USD 4 Billion |

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 8.35 Billion |

| Growth Rate (2026 - 2031) | 13.05% CAGR |

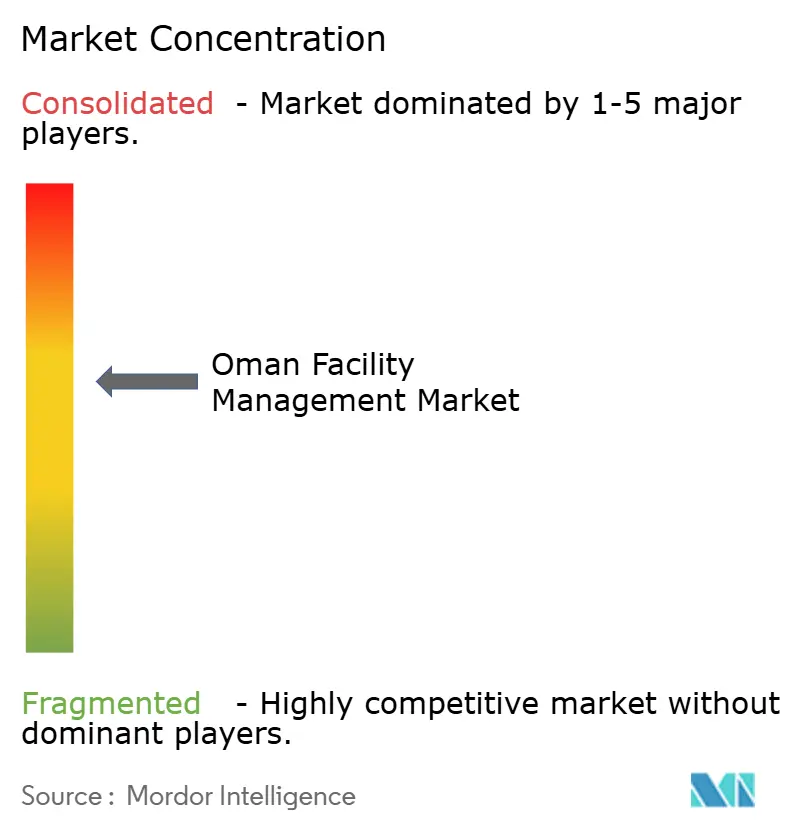

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Facility Management Market Analysis by Mordor Intelligence

The Oman facility management market size is expected to grow from USD 4 billion in 2025 to USD 4.52 billion in 2026 and is forecast to reach USD 8.35 billion by 2031 at 13.05% CAGR over 2026-2031. Rapid commercial real-estate expansion, Vision 2040 infrastructure spending, and the steady replacement of in-house teams with integrated service providers anchor demand and keep the Oman facility management market on a steep upward trajectory. Hard services continue to dominate project scopes because large industrial assets require specialised mechanical, electrical, and fire-safety maintenance; however, soft services register the quickest percentage gains as employers redesign workplaces around employee well-being and visitor experience. A parallel shift toward outsourced, multi-disciplinary contracts allows clients to focus on core activities, while providers differentiate through Internet of Things (IoT) platforms, predictive maintenance analytics, and energy-management solutions. Moderate market concentration persists as incumbents such as Renaissance Services and G4S compete with agile, technology-first entrants, a situation likely to spark partnerships and digital investments through 2030.

Key Report Takeaways

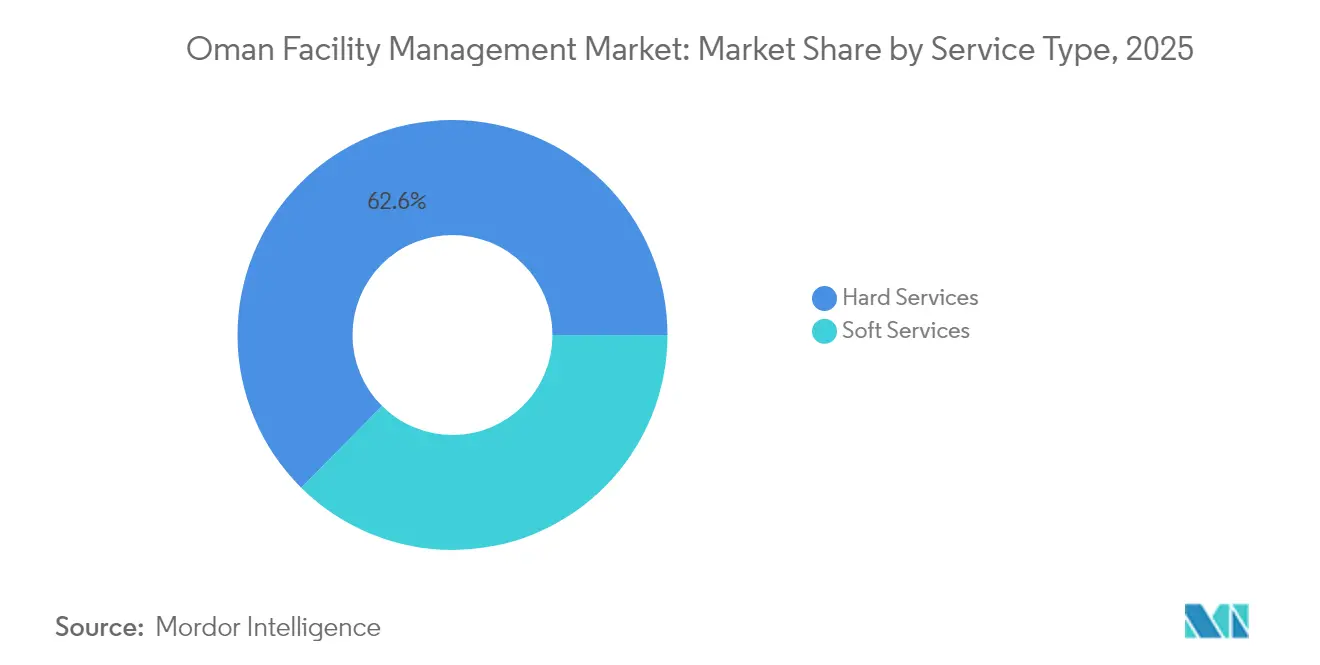

- By service type, hard services led with 62.58% of the Oman facility management market share in 2025, while soft services are set to advance at a 13.62% CAGR through 2031.

- By offering type, outsourced models accounted for 66.78% of the Oman facility management market size in 2025; the same category is projected to grow at a 13.28% CAGR to 2031 as clients replace fragmented in-house teams with integrated contracts.

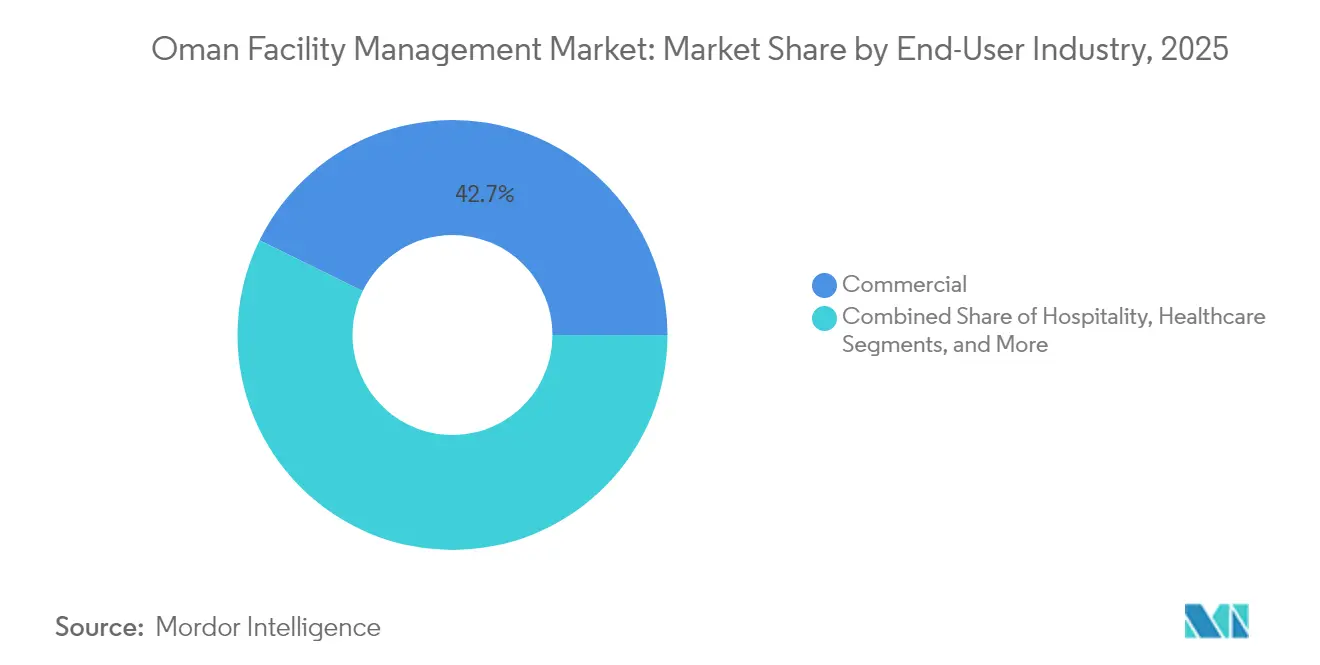

- By end-user industry, commercial facilities held 42.74% of the Oman facility management market size in 2025, whereas industrial and process sites record the highest expected CAGR of 13.12% through 2031 on the back of energy and manufacturing projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid commercial real-estate expansion | +3.2% | Muscat, Salalah, Duqm | Medium term (2-4 years) |

| Technology integration (IoT, AI, automation) | +2.8% | Urban centres, industrial zones | Long term (≥ 4 years) |

| Increasing outsourcing trend | +2.1% | National, commercial hubs | Short term (≤ 2 years) |

| Rising focus on workplace experience | +1.7% | Commercial districts, government assets | Medium term (2-4 years) |

| Government Vision 2040 diversification | +2.4% | National, special economic zones | Long term (≥ 4 years) |

| Growth in tourism and hospitality footprint | +1.3% | Coastal regions, heritage sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technology Integration (IoT, AI, Automation)

Predictive analytics, cloud-based asset registers, and sensor-rich building management systems are redefining how the Oman facility management market approaches reliability, safety, and energy optimisation.[1]IBM, “Petroleum Development Oman LLC,” ibm.comPetroleum Development Oman used an IoT-enabled platform to cut procurement steps from 46 to 14, saving 2,300 hours a year, and proving the operational payback of digital retrofits. Renaissance Services set up a Centre of Excellence for Energy Management in Muscat that pilots automation for cleaning, environmental monitoring, and Wi-Fi management in large accommodation villages. Government smart-city pilots in Knowledge Oasis Muscat further validate the business case for integrated digital infrastructure that feeds real-time data to facility dashboards. Continuous data flows reduce unplanned downtime, lower energy bills, and help providers meet stricter environmental, social, and governance criteria demanded by multinational tenants. Over the long term, widespread adoption of AI-driven diagnostics is expected to lift service margins and reinforce the competitive edge of technology-savvy contractors.

Rapid Commercial Real-Estate Expansion

Multi-billion-dollar projects such as Sultan Haitham City (15 million m²) and New City Salalah waterfront (7.3 km²) add vast new inventories of offices, malls, and mixed-use assets that need round-the-clock maintenance, cleaning, and security. The Duqm Special Economic Zone already hosts USD 30 billion in committed capital and maintains occupancy rates above 85%, translating into a steady pipeline for hard and soft facility services. Every new square meter of grade-A space increases lifecycle spending on HVAC, fire-detection systems, and elevators, thereby expanding the Oman facility management market. Developers also specify green-building certifications, which require continuous commissioning, energy audits, and waste-management programmes. Medium-term impact is reinforced by Rakiza’s infrastructure fund that channels institutional investment into logistics parks, hospitality complexes, and healthcare campuses, locking in multi-year service contracts across governorates.

Increasing Outsourcing Trend

Corporate and public-sector owners increasingly outsource non-core operations to focus scarce managerial bandwidth on revenue generation. Outsourced contracts already command two-thirds of the Oman facility management market and are advancing faster than any other service model. PDO’s Manazil accommodation villages illustrate the shift from fragmented self-operation to end-to-end design, build, operate, and maintain agreements that unify cleaning, catering, and technical services under one vendor. The economic logic centres on lower total cost of ownership and guaranteed service-level agreements that mitigate compliance risk. Short contracting cycles in retail and small office tenancies speed decision-making, while large industrial clients move towards 5- to 10-year integrated deals that bundle energy, water, and waste optimisation. As service depth expands, providers invest in cross-trained teams to maximise resource utilisation and minimise call-out delays, strengthening the outsourcing value proposition nationwide.

Government Vision 2040 Diversification Initiatives

Vision 2040 targets 6% headline growth from non-hydrocarbon sectors, triggering USD 69.3 billion in foreign direct investment by Q3 2024. Tourism, logistics, renewable energy, and manufacturing clusters each generate specialised facility-management needs that propel the Oman facility management market into new verticals such as green hydrogen, data centres, and full-service logistics hubs. The government also aims for 11.7 million tourists by 2040, a target that drives hotel chains and leisure developers to secure long-term soft-service contracts covering housekeeping, guest services, and front-of-house operations. Through the Tanfeedh programme, each governorate is tasked with developing a sector focus—for example logistics in Al Batinah North and knowledge industries in Al Dakhiliya—creating spatially diverse demand pools for facilities upkeep. Long-term impact on the Oman facility management market is reinforced by mandates for smart, low-carbon infrastructure, which foster adoption of digital twin technology and energy-efficiency retrofits.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour shortages and skill gaps | −2.1% | Nationwide, acute in remote zones | Short term (≤ 2 years) |

| Margin pressure from rising costs | −1.8% | Urban centres | Medium term (2-4 years) |

| High reliance on migrant workforce | −1.3% | Service-intensive sectors | Medium term (2-4 years) |

| Delayed payments in public-sector deals | −0.9% | Government facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labour Shortages and Skill Gaps

Omanisation quotas compel every fully foreign-owned firm to employ at least one Omani national within 12 months, yet only 31.4% of hospitality staff are citizens, underscoring a short-term mismatch between policy ambition and skills supply. [2]Fragomen, “Oman: New Labor Law Overhauls Immigration System,” fragomen.com Facility management roles often involve weekend work, night shifts, and physically demanding tasks that attract limited local interest. Providers respond by investing in structured training academies and career-progression pathways to improve retention. Labour codes introduced in 2025 also cut the working week to 40 hours and extend sick leave to 182 days, boosting wage bills and overtime premiums. The short-term drag on the Oman facility management market is acute in remote industrial sites where staff quarters, health facilities, and logistics support add cost layers.

Margin Pressure from Rising Operational Costs

Input price inflation affects cleaning chemicals, HVAC filters, and security equipment, while energy tariffs tighten as subsidies phase out, squeezing contractor margins. [3]MDPI, “Autopsy of Used Reverse Osmosis Membranes from the Largest Seawater Desalination Plant in Oman,” mdpi.comNew regulatory standards mandate enhanced personal protective equipment and formalised refresher training, adding compliance overheads. Clients, however, remain cost-conscious and push for fixed-price contracts, forcing providers to unlock savings through automation and predictive maintenance. Digital work-order systems cut travel time between call-outs, and building-analytics dashboards flag energy anomalies before they erode profitability. Margin pressure will persist through the medium term, prompting continued consolidation in the Oman facility management market as smaller firms struggle to finance technology upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Retain Dominance While Soft Services Accelerate

Hard services captured 62.58% of the Oman facility management market share in 2025 and continue to benefit from capital-intensive assets such as airports, refineries, and integrated tourism complexes that require 24/7 mechanical, electrical, and fire-safety cover. Heavy-duty HVAC systems at Muscat International Airport and extensive utility networks at Duqm’s petrochemical plants anchor long-term maintenance contracts. Predictive condition monitoring helps providers reduce downtime and optimise spare-parts inventory, reinforcing client preference for end-to-end contracts.

Soft services, while starting from a smaller base, are forecast to expand at 13.62% CAGR through 2031, propelled by workplace-experience programmes in corporate offices and the hospitality sector’s pursuit of global service standards. Renaissance Services supplies more than 15 million meals annually to hospitals and construction camps, showing the scale at which catering contracts now operate. Security outsourcing also climbs as malls and large mixed-use complexes deploy analytics-enabled surveillance to meet insurance and tenant requirements. Specialist cleaning services for data centres and healthcare facilities open further growth lanes, ensuring soft services remain the fastest-growing component of the Oman facility management market.

By Offering Type: Outsourcing Gains Ground Through Integrated Agreements

Outsourced models controlled 66.78% of the Oman facility management market in 2025 and are projected to expand at 13.28% CAGR, as bundled and integrated contracts outperform single-service arrangements. Large energy operators migrate to five-year integrated deals that combine asset maintenance, catering, and waste services, reducing vendor interfaces and strengthening accountability. PDO’s Manazil accommodation villages demonstrate the financial and operational advantages of design-build-operate-maintain frameworks.

In-house teams, which account for the remaining 33.22%, persist in mission-critical defence, data-centre, and utilities assets where owners value direct control over security-sensitive systems. However, this share may erode as hybrid governance models use digital dashboards to retain strategic oversight while farming out execution to specialist vendors. Tight labour markets and new workforce regulations increase the cost of maintaining internal teams, tilting boardroom decisions toward outsourcing, thereby reinforcing growth prospects for the Oman facility management market.

By End-User Industry: Commercial Facilities Lead While Industrial Assets Accelerate

Commercial buildings held 42.74% of the Oman facility management market size in 2025 as banking, telecom, and retail tenants demand grade-A spaces with continuous uptime, stringent indoor-air-quality metrics, and five-star guest services. Commercial landlords adopt IoT-enabled energy-management platforms to reduce operating expenses, making comprehensive service contracts attractive. Muscat’s office pipeline continues to expand in Al-Khuwair and Ruwi districts, ensuring a stable flow of new tenders.

Industrial and process facilities register the highest forecast CAGR at 13.12% through 2031. Investments in green hydrogen clusters, solar-wind hybrid IPPs, and the Duqm refinery create specialised opportunities for reliability-centred maintenance, high-voltage asset care, and stringent safety compliance. Healthcare and hospitality properties add further diversity, each with bespoke hygiene, waste-segregation, and guest-services protocols. Together, these trends deepen the service portfolio and geographic reach of the Oman facility management market.

Geography Analysis

Muscat Governorate anchors the Oman facility management market with the highest share of built asset value, driven by the 15 million m² Sultan Haitham City, ongoing airport upgrades, and a dense concentration of government ministries. New mixed-use schemes require integrated hard and soft services delivered through multi-year contracts that incorporate energy benchmarking and smart-meter data analytics.

Dhofar Governorate emerges as a growth pole on the strength of tourism and renewable energy megaprojects. The New City Salalah waterfront plan spans 7.3 km² and dovetails with wind and solar IPPs exceeding 4 GW of installed capacity, creating steady, specialised demand for operations and maintenance services across hotels, malls, and generation assets.

Al Wusta Governorate, home to the Duqm Special Economic Zone, attracts USD 30 billion in pledged capital and rapidly fills logistics, petrochemical, and manufacturing plots. High land-occupancy rates trigger contracting activity for fire-protection systems, utilities operations, and accommodation services, further enlarging the Oman facility management market.

Competitive Landscape

The Oman facility management market remains moderately concentrated, with the top five providers jointly holding just under 50% of contract revenue. Renaissance Services leads through a portfolio that spans hard and soft services, manages 3 million m² of space, and employs 8,800 staff, supporting its ambition to achieve USD 2 billion market capitalisation by 2025. G4S Oman focuses on security-centric bundles that integrate electronic surveillance, access control, and manned guarding for industrial and commercial complexes. Qurum Business Group leverages its wider business-services footprint to cross-sell integrated facility contracts in sectors ranging from ports to healthcare.

Technology adoption defines the new battleground. Providers deploy IoT sensors for real-time monitoring, AI algorithms for predictive maintenance, and cloud platforms for consolidated help-desk management. Patent activity related to automated structural health monitoring and server-based building control points to emerging digital differentiation.

Sustainability credentials are becoming a decisive tender parameter. Energy-audit services, waste-segregation frameworks, and ESG reporting modules help contractors align with international tenant requirements and government decarbonisation targets. Firms that can marry digital diagnostics with low-carbon solutions stand to capture premium margins as the Oman facility management market enters its next growth phase.

Oman Facility Management Industry Leaders

G4S Limited

Qurum Business Group

Oman International Group SAOC

Renaissance Services SAOG

COMO Oman

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OQ Base Industries reports 70.6% jump in Q1 net profit to OMR 12.8 million (USD 33.3 million), signalling stronger activity for industrial facility services

- April 2023: Wood secures a three-year front-end engineering support contract with Petroleum Development Oman covering energy-transition projects and carbon-capture schemes

- March 2025: The Ministry of Housing and Urban Planning unveils the 7.3 km² New City Salalah masterplan, projecting major facility-management workload across residential and leisure assets

- February 2025: Asyad Group announces plans to float 20% of Asyad Shipping, owner of 89 vessels, adding maritime facility-management opportunities in dry-docking and port services

Oman Facility Management Market Report Scope

Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. While hard services include physical and structural services such as fire alarm system lifts, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-users such as commercial buildings, retail, government, and public entities.

The Oman facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Oman facility management market?

The Oman facility management market size is USD 4.52 billion in 2026 and is projected to reach USD 8.35 billion by 2031.

Which service category is growing fastest?

Soft services, including cleaning, catering, and security, are forecast to grow at a 13.62% CAGR through 2031, outpacing all other categories.

Why are outsourcing models gaining traction in Oman?

Organisations turn to outsourced integrated contracts to reduce total cost of ownership, meet Omanisation rules through specialised vendors, and tap into technology-enabled maintenance platforms.

How does Vision 2040 influence facility management demand?

Vision 2040 channels large-scale investment into tourism, logistics, and renewable energy, each of which requires professional facilities upkeep and thus expands the addressable market for service providers.

What technologies are reshaping facility management operations?

IoT sensors, AI-based predictive maintenance, cloud asset registers, and energy-management dashboards help contractors cut downtime and extend equipment life while supporting sustainability goals.

Which region outside Muscat offers the greatest growth potential?

Dhofar Governorate, driven by renewable energy megaprojects and coastal tourism developments, is emerging as the most dynamic secondary market for facility management services.

Page last updated on: