Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

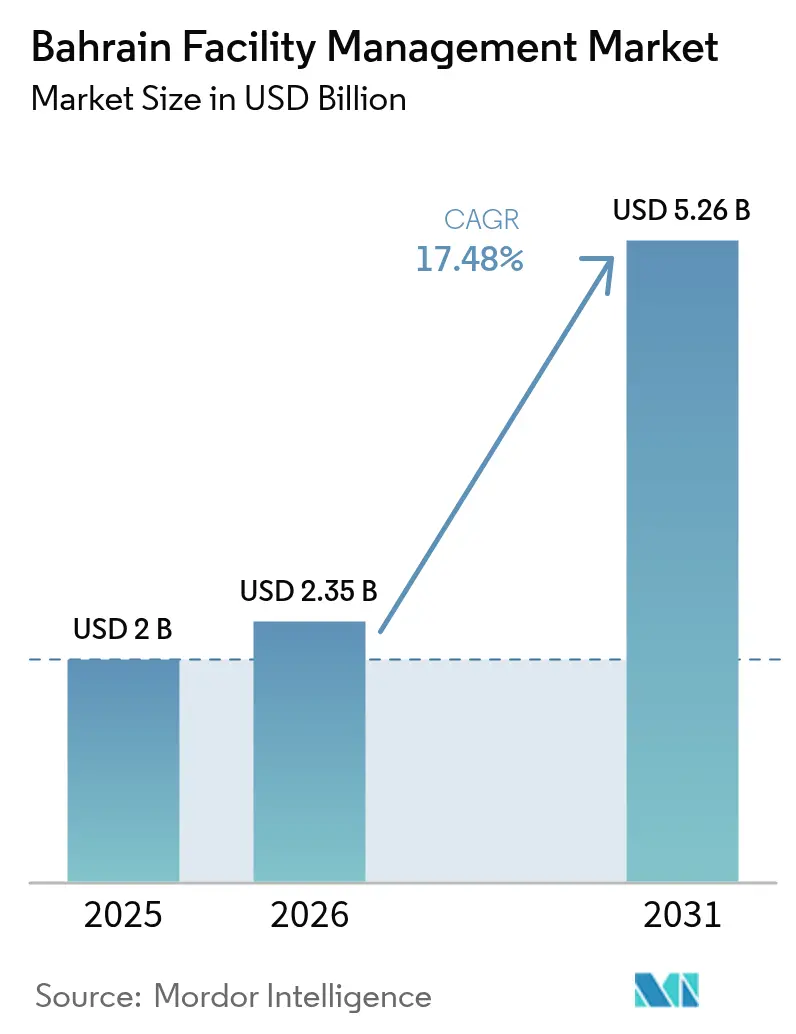

| Base Year Market Size (2025) | USD 2.00 Billion |

| Market Size (2026) | USD 2.35 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 17.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Facility Management Market Analysis by Mordor Intelligence

The Bahrain facility management market size was valued at USD 2.00 billion in 2025 and estimated to grow from USD 2.35 billion in 2026 to reach USD 5.26 billion by 2031, at a CAGR of 17.48% during the forecast period (2026-2031). Sustained government spending on large-scale transport, energy, and mixed-use projects, led by the USD 30 billion Vision 2030 pipeline, underpinned the market’s rapid growth through 2025 while creating a visible backlog of new assets that will require integrated operations and maintenance services across the forecast horizon.[1]The Daily Tribune, “Bahrain to invest in 22 major infrastructure projects, including five artificial islands,” newsofbahrain.com Private developers increasingly outsourced hard and soft services to specialist vendors, accelerating demand for bundled and integrated delivery models. Heightened ESG regulations triggered strong investment in energy-efficient retrofits and green-building certifications, favouring providers with IoT-enabled maintenance and AI-based energy-optimisation platforms. The technology adoption wave also narrowed cost differentials between in-house and outsourced models, encouraging corporates to sign outcome-based, multi-year contracts that secure predictable operating costs and performance guarantees.

Key Report Takeaways

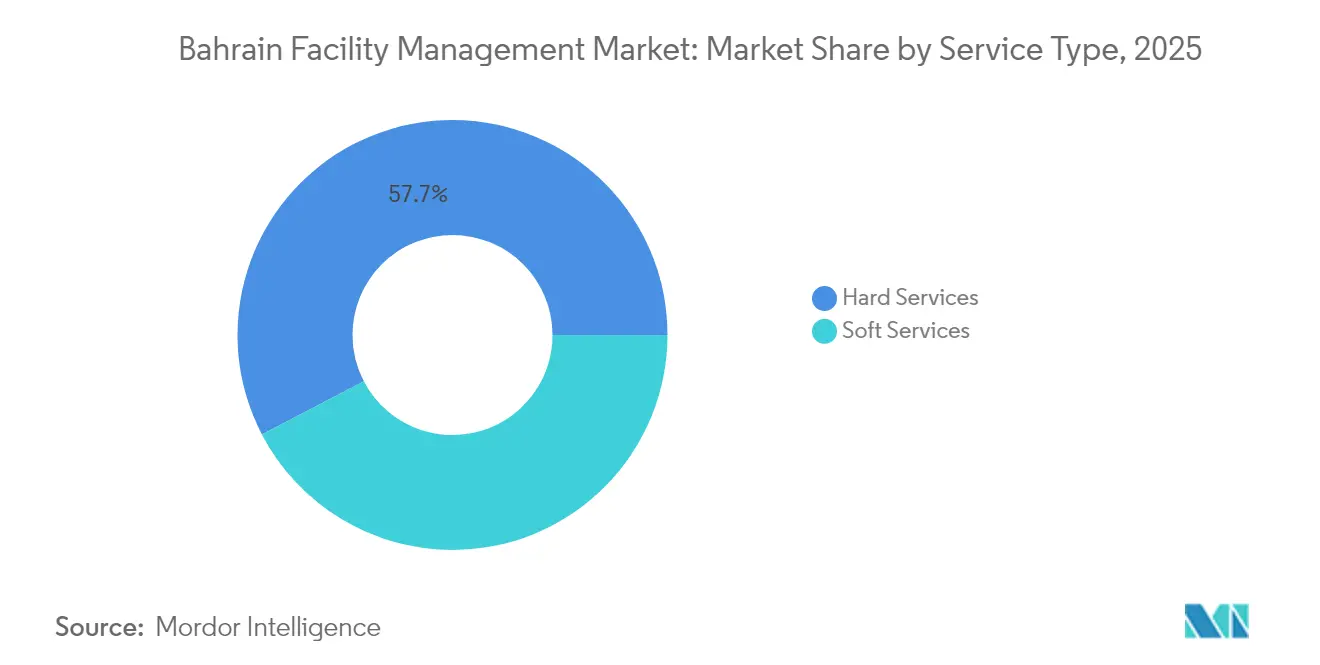

- By service type, hard services led with 57.65% of the Bahrain facility management market share in 2025, and soft services are projected to advance at an 18.04% CAGR to 2031.

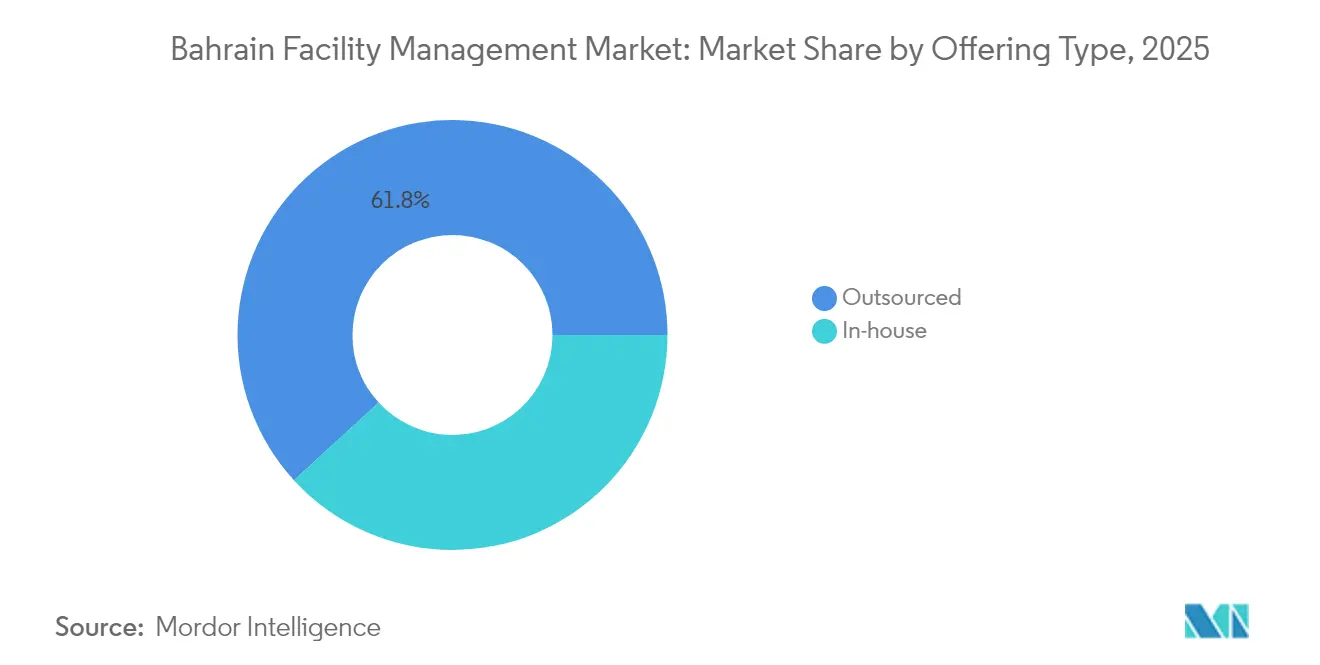

- By offering type, the outsourced model commanded a 61.80% share of the Bahrain facility management market size in 2025, while integrated service portfolios are forecast to expand at an 18.22% CAGR through 2031.

- By end-user industry, commercial facilities accounted for 39.10% share of the Bahrain facility management market size in 2025, and the industrial and process segment is growing the fastest at 18.39% CAGR, thanks to new aluminium and petrochemical capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure development and a USD 30 billion project pipeline | +4.2% | National, concentrated in Manama and industrial zones | Medium term (2-4 years) |

| Digital transformation and IoT integration in facility operations | +3.8% | Global, with early adoption in commercial and healthcare sectors | Short term (≤ 2 years) |

| Outsourcing trend acceleration and integrated service delivery models | +3.1% | Regional GCC spillover, strongest in Bahrain urban centers | Medium term (2-4 years) |

| ESG compliance requirements and net-zero emissions targets by 2060 | +2.9% | National regulatory mandate with international standards alignment | Long term (≥ 4 years) |

| Healthcare sector expansion and specialized facility requirements | +2.4% | National, with a concentration in Manama and emerging medical districts | Medium term (2-4 years) |

| Industrial manufacturing growth and Alba-BAPCO partnership initiatives | +1.7% | Industrial zones, particularly Sitra and Alba facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Development Catalyses Market Expansion

The state’s USD 30 billion commitment to 22 flagship projects—including the USD 3.5 billion King Hamad Causeway and the USD 2 billion Bahrain Metro—dramatically expanded the Bahrain facility management market by adding high-spec assets that need round-the-clock technical upkeep. The USD 1.1 billion airport modernisation programme alone introduced complex passenger-flow, security, and energy-management systems that require integrated FM from day one. Public-private partnership structures lock in long-term O&M contracts, granting vendors revenue visibility while increasing customer expectations around service-level guarantees. As construction proceeds, refurbishment of legacy buildings further multiplies addressable spend, reinforcing the Bahrain facility management market’s double-digit trajectory.

Digital Transformation Accelerates Operational Efficiency

Bahrain’s cloud-first policy, nationwide 5G, and international fibre-optic links allowed FM firms to shift from reactive to predictive maintenance models. IoT sensors continuously capture HVAC runtime, vibration, and energy-use data; AI analytics pre-empt failures and cut unplanned downtime by up to 30 percent, lowering total cost of ownership and improving tenant satisfaction. IBM’s Maximo deployment in the King Abdullah Financial District pushed work-order closure rates above 95% and trimmed annual maintenance spend, a benchmark now mirrored by Manama’s Grade-A office towers. Local innovators such as ARRAY Innovation signed 2025 agreements with Alba and NBB to overlay AI algorithms on large industrial campuses, setting a new service baseline across the Bahrain facility management market.

Outsourcing Acceleration Drives Service Integration

Corporate tenants prioritised core business functions and transferred non-core services—including security, cleaning, MEP, and cafeteria operations—to external specialists. Government rules permitting 100% foreign ownership and fast-track licensing attracted global FM majors and regional incumbents, amplifying competition and capability depth. Landmark Hospitality’s 2025 GCC-wide IT outsourcing deal with Gulf Business Machines illustrated a shift toward bundled, outcome-based contracts that place performance risk with the vendor. The model favours firms that couple field staff with cloud dashboards, resulting in longer contract tenures and higher switching costs within the Bahrain facility management market.

ESG Compliance Requirements Transform Service Delivery

Bahrain pledged net-zero emissions by 2060 and interim renewable-energy targets of 5% in 2025 and 10% in 2035, compelling asset owners to retrofit lighting, chillers, and water systems. The Alba-BAPCO green-industrial alliance designed hydrogen-reuse and zero-waste projects that demand specialist FM oversight, elevating vendors proficient in environmental compliance and energy dashboards. Mumtalakat’s capital-allocation policy embedded ESG clauses into procurement, pushing FM providers to publish Scope 1-3 emissions baselines and annual reduction plans. These mandates turned sustainability performance from a nice-to-have into a core contract requirement across the Bahrain facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages and workforce development challenges | -2.8% | National, with acute shortages in technical and digital skills | Short term (≤ 2 years) |

| Supply chain volatility and material cost inflation | -2.1% | Regional GCC impact with global supply chain dependencies | Medium term (2-4 years) |

| Regulatory compliance complexity and evolving safety standards | -1.4% | National regulatory framework with international alignment requirements | Medium term (2-4 years) |

| Economic uncertainty and oil price volatility are affecting investment decisions | -1.2% | Regional GCC economic conditions with global commodity exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortages Constrain Service Capacity

Despite the Ministry of Labor surpassing its 2024 hiring target with 27,147 citizen placements, FM employers struggled to secure technicians adept at BMS programming, sensor calibration, and data analytics.[2]Ministry of Labor, “Ministry of Labor,” mol.gov.bh Competing demand from fintech and cloud-services firms intensified wage pressures, while visa processes for expatriate specialists elongated mobilisation timelines. Tamkeen’s 2024 skills report highlighted gaps in digital literacy within vocational programmes, forcing FM firms to invest in in-house academies and remote-support platforms. Until training pipelines catch up, staff shortages will cap near-term growth in the Bahrain facility management market.

Supply-Chain Volatility Pressures Operating Costs

Rising global freight rates, extended delivery lead times, and commodity price swings inflated HVAC spares, elevator parts, and cleaning chemicals budgets. Strategy& estimated that better procurement planning could save GCC contractors 10-20%, but FM firms still faced year-on-year cost hikes that eroded fixed-price contract margins. CBRE recorded a peak in FM cost inflation in late 2022, and although pressures moderated, vendors adopted “just-in-case” inventory buffers, tying up working capital. The need to renegotiate escalation clauses became routine across the Bahrain facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: Outsourced Model Widens its Lead

Outsourced vendors controlled 61.80% of the Bahrain facility management market size in 2025 as corporates shifted capex and HR risks to external partners. Multi-site portfolios spanning offices, warehouses, and retail outlets increasingly favoured single-invoice providers who could guarantee service-level compliance nationwide. Internally, FM buyers pivoted to integrated platforms that merge help-desk, work-order, and asset-life-cycle analytics, reinforcing dependence on technology-enabled outsourcers. The Bahrain facility management industry also saw higher RFP scoring for ISO 41001-certified providers, pushing smaller firms toward consolidation.

In-house operations, with a 38.20% share, persisted mainly in sensitive government and defence installations such as Isa Air Base, where a USD 29.85 million 2024 BOS contract option underscored the value placed on direct oversight. Yet rising wage costs and technology complexity led many agencies to test hybrid models where they retain strategic command while subcontracting field services, realigning spending patterns inside the Bahrain facility management market.

By End-User Industry: Commercial Core Faces Industrial Upswing

Commercial facilities produced 39.10% of the Bahrain facility management market size in 2025, underwritten by telecom, IT parks, and a burgeoning logistics sector. DHL’s EUR 218 million (USD 239.8 million) 2024 hub expansion at Bahrain International Airport exemplified the scale of new FM opportunities in temperature-controlled warehousing and time-critical aircraft handling.Retail developers redesigned malls into mixed-use destinations, adding entertainment and coworking attributes that increased cleaning and security complexity.

Industrial and process manufacturing assets are expected to grow fastest at 18.39% CAGR, thanks to Alba’s line-7 aluminium capacity and the Alba-BAPCO green-hydrogen initiative. These heavy-industry plants require high-reliability electrical, conveyor, and environmental systems, raising demand for predictive vibration analysis and hazardous-area maintenance. Healthcare facilities also expanded rapidly; specialised FM vendors now manage sterile areas, negative-pressure rooms, and backup-power infrastructure at King Hamad American Mission Hospital, elevating service margins for clinical-grade operators.

By Service Type: Hard-Service Dominance and Soft-Service Momentum

Hard services held 57.65% of the Bahrain facility management market share in 2025, anchored by complex MEP, HVAC, and fire-safety systems embedded in new transport, petrochemical, and metro projects. The USD 7 billion BAPCO modernisation alone added thousands of assets requiring lifecycle management. Continuous high-temperature conditions and stricter fire codes raised the frequency of preventive checks, cementing recurring revenue for technical specialists. Asset-management software uptake also increased ticket volumes while improving first-time-fix rates, strengthening vendor lock-in across government and private portfolios.

Soft services are projected to grow at an 18.04% CAGR, fuelled by the hospitality and healthcare boom. Luxury openings such as Raffles Al Areen Palace and Kempinski Bahrain Harbour elevated benchmarks for cleaning, concierge, and catering standards. The Amana Healthcare centre, scheduled for 2025, demands infection-control protocols aligned with international accreditation, boosting specialised cleaning contract values. Corporates also adopted hybrid-workplace models that blend facilities services with workplace-experience apps, expanding the scope of soft-service deliverables within the Bahrain facility management market.

Geography Analysis

The Manama metropolitan area anchored the largest cluster of assets within the Bahrain facility management market, driven by the concentration of ministries, financial institutions, and premium mixed-use towers across Bahrain Bay, Seef, and the Diplomatic Area. Grade-A offices demanded advanced BMS platforms, while high-footfall retail complexes required expanded soft-service headcounts. Traffic-dense locations compelled providers to establish rapid-response hubs along the King Fahd Causeway corridor for 24/7 coverage, consolidating economies of scale.

Industrial zones in Sitra and around the Alba smelter formed the fastest-growing sub-market, booking a double-digit rise in outsourced technical contracts. Green-industrial initiatives, including hydrogen-reuse pilots, necessitated specialist safety skills and environmental monitoring equipment, differentiating vendors who could supply certified technicians on short notice. Proximity to Khalifa Bin Salman Port shortened spare parts lead times, enhancing service-level compliance for process industries.

The northern and southern coastal developments—including the artificial islands, Marassi Al Bahrain, and Digital City in Hamala—broadened residential and hospitality workloads. Aecom’s 2024 appointment as master planner for the 380,000 m² Digital City intensified FM tender activity for smart-parking, district-cooling, and medical-facility maintenance. Muharraq’s heritage restoration projects added specialist stone conservation and crowd-management responsibilities, while the airport precinct demanded aviation-compliant cleaning, waste, and GSE-equipment services. Compact national geography enabled central dispatching, allowing providers to service multi-region portfolios economically and enhance competitiveness inside the Bahrain facility management market.

Competitive Landscape

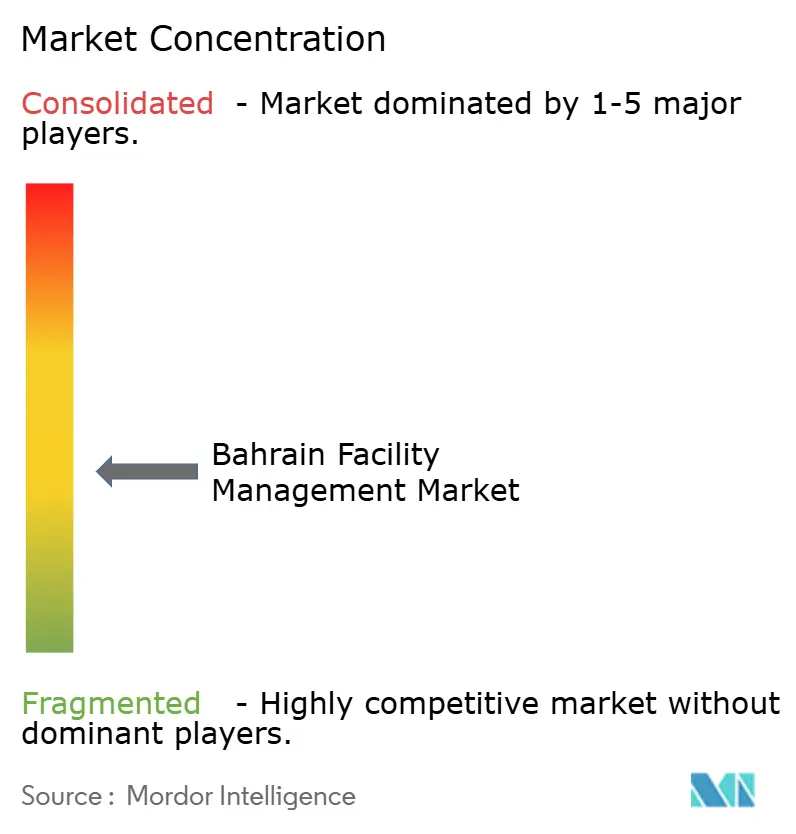

The Bahrain facility management market displayed moderate fragmentation, with local champions BMMI Group and Almoayyed Contracting controlling diversified hard- and soft-service lines, but each below a 10% revenue share. Mid-tier specialists such as VATES shifted into healthcare and complex industrial niches, while Renaissance Services leveraged pan-GCC scale to win integrated catering-and-maintenance packages for 70 clinic and hotel sites. Competitive intensity rose as global entrants formed joint ventures or technology alliances, keen to transfer best-practice analytics and robotic cleaning platforms.

Digital capabilities became the decisive battleground. ARRAY Innovation’s 2025 AI agreements with Alba and NBB front-loaded data-science competencies as a purchasing criterion, squeezing firms reliant on manual workflows.[4]The Daily Tribune, “ARRAY Innovation Strengthens Commitment to Bahrain's Digital Transformation,” newsofbahrain.com FM bidders increasingly needed ISO 27001, ISO 41001, and cyber-security compliance to win banking, data-centre, and defence contracts. To close gaps, incumbents accelerated M&A and talent-acquisition programmes focused on data engineers and sustainability consultants.

Sustainability credentials also shaped vendor shortlists. Companies that quantified carbon-reduction roadmaps secured renewals at premium margins, especially on sovereign-wealth-funded projects. The arrival of performance-linked payment clauses aligned provider remuneration with energy-saving outcomes, rewarding firms that invested early in smart meters and AI-optimisation tools. Overall, the Bahrain facility management market continued trending toward a technology-intensive, partnership-driven structure.

Bahrain Facility Management Industry Leaders

ATLANTIS Engineering

ASF Facility Management

Royal Ambassador Property and Facility Management Co

Metropolitan Holding CO WLL

HomeFix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ARRAY Innovation signed strategic agreements with Aluminium Bahrain, National Bank of Bahrain, and Tamkeen to deploy AI-powered facility operations platforms and job-matching tools.

- November 2024: Beyon appointed Aecom as master planner for its 380,000 m² Digital City in Hamala, adding new smart-facility workloads.

- November 2024: NAVFAC awarded a USD 29.85 million base-operations support option for Isa Air Base, sustaining demand for military-grade FM services.

- October 2024: Gulf Hotel Bahrain secured a three-year premium catering contract at Bahrain International Circuit, expanding event-driven FM revenues.

Bahrain Facility Management Market Report Scope

Facility management encompasses multiple disciplines to ensure the functionality of the built environment by integrating people, place, process, and technology. Also, facility management is the coordination of a facility's operations meant to make the organization as a whole more effective at what it does. The facility management is applied in various industry verticals like retail, education, and healthcare, among others, as per the need of the business.

The Bahrain facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

Key Questions Answered in the Report

What is the current size of the Bahrain facility management market?

The Bahrain facility management market size reached USD 2.35 billion in 2026.

How fast is the Bahrain facility management market expected to grow?

It is forecast to expand at a 17.48% CAGR between 2026 and 2031, reaching USD 5.26 billion.

Which segment is growing the fastest?

Soft services are projected to record an 18.04% CAGR, driven by healthcare and hospitality demand.

Why are outsourced models so popular in Bahrain?

Corporates prefer specialised vendors that supply integrated hard- and soft-service bundles, achieving cost savings and compliance with Bahrain’s cloud-first and ESG regulations.

What is the main restraint facing FM providers?

A shortage of technicians skilled in IoT and building-automation systems is limiting short-term capacity.

How do ESG targets affect facility management contracts?

Net-zero pledges require energy-efficient retrofits and carbon-tracking dashboards, so clients increasingly award contracts to FM firms with proven sustainability expertise.

Page last updated on: