Qatar Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

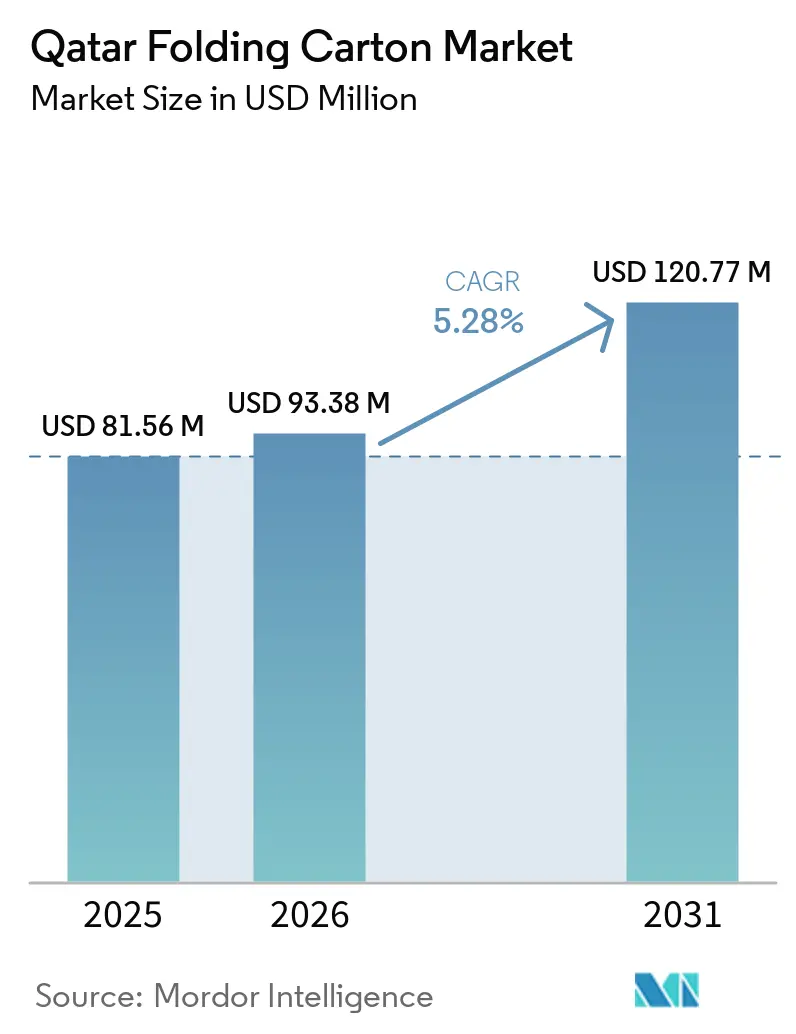

| Base Year Market Size (2025) | USD 81.56 Million |

| Market Size (2026) | USD 93.38 Million |

| Market Size (2031) | USD 120.77 Million |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

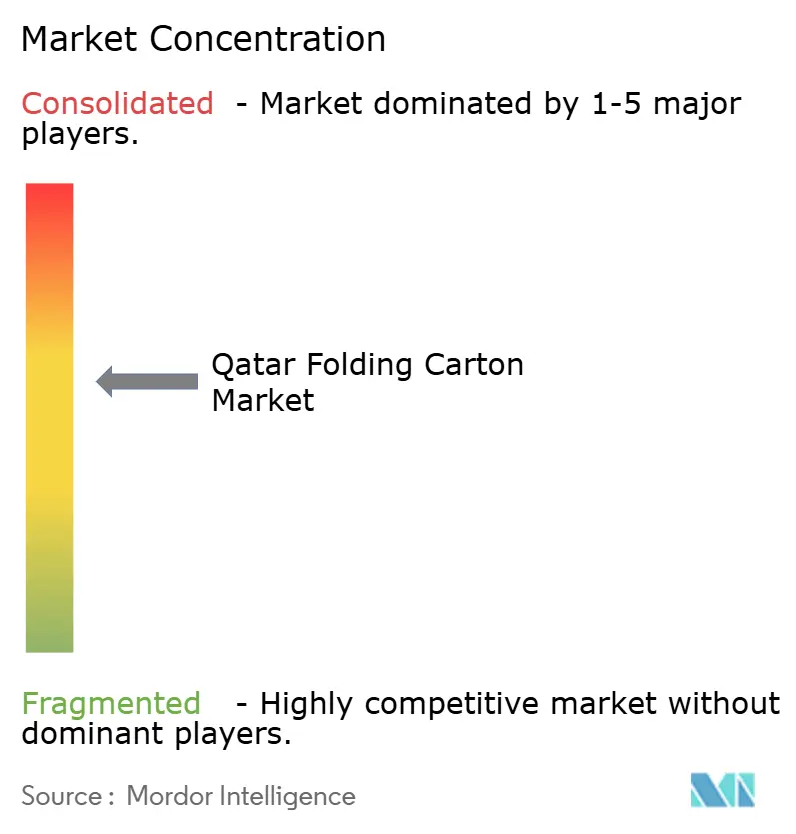

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Folding Carton Market Analysis by Mordor Intelligence

The Qatar folding carton market size is expected to increase from USD 81.56 million in 2025 to USD 93.38 million in 2026 and reach USD 120.77 million by 2031, growing at a CAGR of 5.28% over 2026-2031. Brisk uptake of paper-based secondary packaging, propelled by sustainability mandates and the phase-out of single-use plastics, underpins this trajectory. E-commerce expansion, infrastructure linked to the FIFA 2030 bid, and foreign direct investment in food, beverage, and pharmaceutical facilities are broadening the demand base for retail-ready cartons. Brand owners are pivoting toward substrates that convey natural aesthetics, while converters invest in digital printing to serve short-run, variable-data requirements. Exposure to pulp price volatility and limited domestic recycling capacity, however, temper near-term margin growth and amplify the need for supply-chain risk mitigation.

Key Report Takeaways

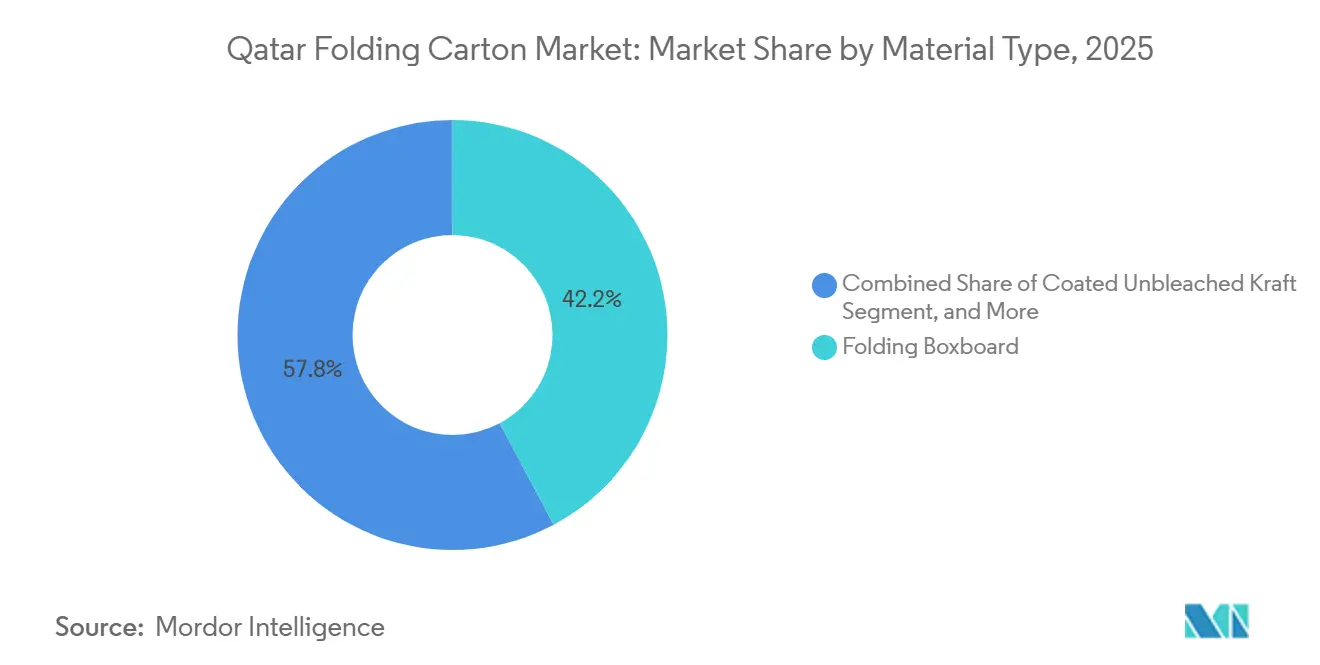

- By material type, folding boxboard captured with 42.19% of the Qatar folding carton market share in 2025.

- By printing technology, the Qatar folding carton market size for digital printing is projected to grow at a 6.59% CAGR to 2031.

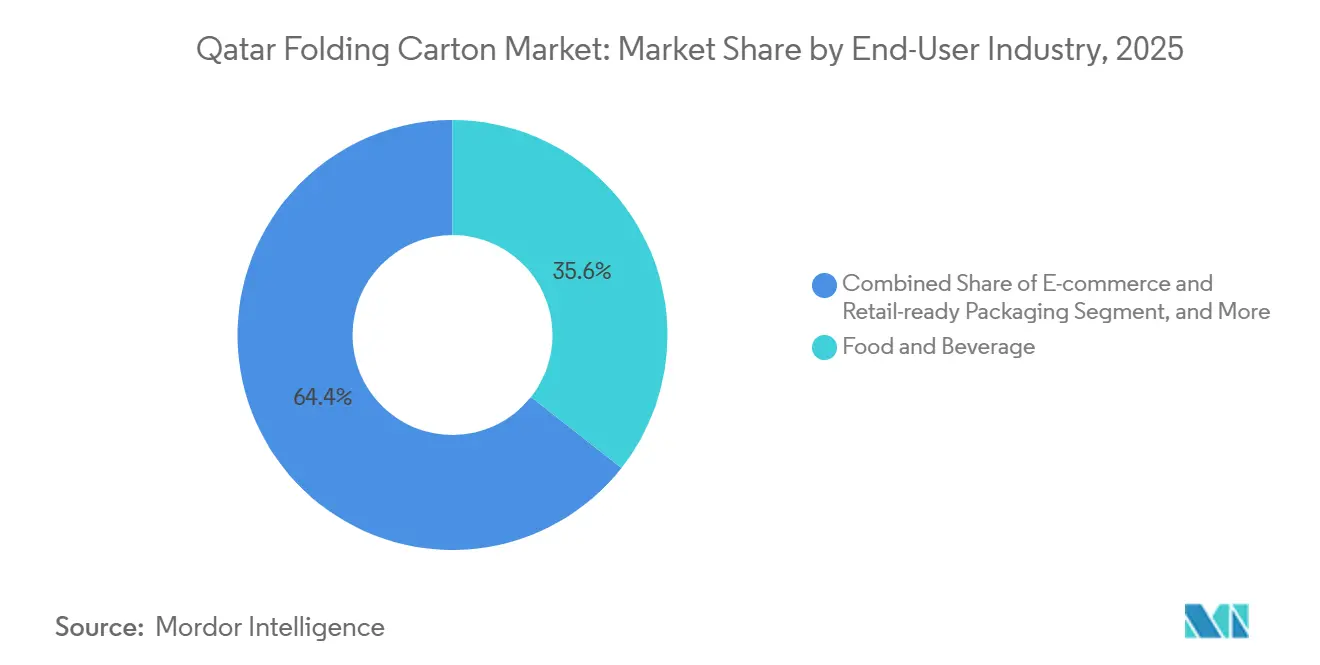

- By end-user industry, the food and beverage industry captured 35.62% of the Qatar folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-Driven Government Policies Supporting Paper-Based Packaging | +1.8% | National (Doha, Al Rayyan, Al Wakrah) | Medium term (2-4 years) |

| Growth of Qatar's E-Commerce Sector Fueling Demand for Branded Secondary Packaging | +1.5% | National (Doha metro, Lusail City) | Short term (≤ 2 years) |

| FIFA 2030 Bid Infrastructure Developments Boosting FMCG Demand | +1.2% | National, spillover to northern municipalities | Medium term (2-4 years) |

| Rising Health-Conscious Consumption Driving Demand for Pharmaceutical Folding Cartons | +0.9% | National (Doha healthcare clusters) | Long term (≥ 4 years) |

| Digital Printing Advancements Enabling Short-Run, Customized Cartons | +0.7% | National (Doha Industrial Area) | Short term (≤ 2 years) |

| Increasing Foreign Direct Investment in Food Processing Facilities | +0.6% | National (Mesaieed, Al Afjah) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Driven Government Policies Supporting Paper-Based Packaging

Resolution No. 143 of 2022 banned single-use plastic bags, and the National Strategy 2024-2030 flags extended producer responsibility that internalizes end-of-life costs. The Qatar Central Bank sustainability framework, in force from 2026, obliges listed companies to disclose Scope 3 emissions, nudging brands toward recyclable substrates. Folding cartons, therefore, displace pouches in ready-to-eat meals and personal-care refills because they align with the national 95% recycling target. Demand for Forest Stewardship Council-certified fiber is rising, and converters without chain-of-custody documentation risk delisting in export channels. The new regulatory landscape thus delivers predictable volume growth but compresses margins for plants still reliant on non-certified virgin inputs.

Growth of Qatar's E-Commerce Sector Fueling Demand for Branded Secondary Packaging

Online transaction value reached USD 5.07 billion in 2025, driven by 99% smartphone penetration and ubiquitous 5G coverage. Business-to-consumer orders dominate, yet digitally enabled wholesalers lift business-to-business volumes, expanding demand for robust folding cartons that survive multi-touch distribution. Brands now specify tear strips, QR authentication, and interior graphics that enhance the unboxing moment, a design brief best served by digital presses capable of lot-specific output. Converters offering sub-1,000-unit minimum runs gain share over plants tied to lithographic workflows. Absent such agility, domestic players could cede contracts to neighbors in the United Arab Emirates and Saudi Arabia, where HP Indigo 200K installations already anchor regional capacity.

FIFA 2030 Bid Infrastructure Developments Boosting FMCG Demand

A second wave of transit-oriented projects, Qatar Rail extensions to Al Khor and Al Wakra, and the 12 km Sharq Crossing, reduces logistics friction and enables just-in-time replenishment models that prefer folding cartons over flexible bulk packs.[1]Knight Frank, “Qatar Infrastructure and Real Estate Report,” KNIGHTFRANK.COMRetail space in Lusail City, designed for 200,000 residents, adopts automated micro-fulfillment systems that need dimensionally consistent cartons. Construction spend reaching USD 123.1 billion by 2030 sustains industrial-grade packaging needs across building-material retail. Hypermarkets are rationalizing their assortments toward shelf-stable SKUs, favoring cartons for frozen foods, ambient grocery, and bakery lines, reinforcing volume growth through the forecast horizon.

Rising Health-Conscious Consumption Driving Demand for Pharmaceutical Folding Cartons

Medicine imports valued at USD 1.13 billion in 2024 are set to climb to USD 1.8 billion by 2030, supported by per capita healthcare spending of USD 1,827. The Gulf Cooperation Council’s highest. The Ministry of Public Health backed a domestic plant slated for 2028 with a 140-drug pipeline, guaranteeing local off-take for ISO 15378-compliant cartons. Serialization, tamper-evidence, and elemental-impurities standards lift unit pricing by 20-30% above FMCG grades, presenting margin upside for converters investing in clean-room environments. Current certified capacity remains scarce, signaling room for entrants able to marry GMP protocols with rapid digital print capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Pulp Prices Affecting Profit Margins | -1.3% | Global, acute in Qatar | Short term (≤ 2 years) |

| Limited Domestic Recycling Infrastructure Constraining Recycled Board Supply | -0.9% | National (Mesaieed, Al Afjah) | Medium term (2-4 years) |

| Competition from Flexible Plastic Pouches in Ready-to-Eat Foods | -0.6% | National (ambient snack categories) | Medium term (2-4 years) |

| Skilled Labor Shortages in High-Quality Converting and Printing | -0.5% | National (across industrial zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices Affecting Profit Margins

Southern Bleached Hardwood Kraft climbed to USD 740 per tonne in February 2026 after a six-month rally, while European Bleached Eucalyptus Kraft breached USD 1,220 per tonne. With pulp accounting for roughly 60% of folding-carton costs, converters face 8-12%-point margin erosion unless they pass through surcharges. Qatar’s 100% import dependency magnifies sensitivity as Strait of Hormuz disruptions add freight premiums. Flexible pouches, priced up to 25% lower per unit, become attractive substitutes when carton prices spike. Hedging strategies and partial backward integration into recycled fiber are therefore gaining board-level attention.

Limited Domestic Recycling Infrastructure Constraining Recycled Board Supply

Only 12-15% of Qatar’s 2.5 million-tonne municipal solid waste stream is diverted from landfill. Elite Paper Recycling collects 4,500 tonnes of waste paper monthly but exports up to 80% of its output due to limited local demand. Although the Domestic Solid Waste Management Center processes 828,000 tonnes per year and Al-Afjah Recycling Hub has earmarked 51 plots, fewer than half the units are operational. Converters consequently import recycled pulp at 20-30% cost premiums, hindering the business case for circular packaging and delaying progress toward the 38% national recycling target.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Accelerate as Natural Visual Cues Gain Traction

Folding Boxboard retained 42.19% of the Qatar folding carton market share in 2025, thanks to its stiffness-to-weight ratio and printable surface, which meet food and beverage shelf-life needs. Coated Unbleached Kraft, forecast to expand at a 7.35% CAGR, appeals to premium personal-care and pharmaceutical brands seeking natural fibers without barrier trade-offs. Solid Bleached Sulfate remains favored for luxury confectionery due to its high brightness, which supports foil accents, yet its virgin-fiber makeup exposes buyers to pulp volatility. White Line Chipboard, derived from recycled materials, underpins cost-sensitive household goods, helping meet corporate Scope 3 goals by reducing embedded emissions.

Specialty grades such as grease-resistant boards serve frozen meals and quick-service channels where cold-chain durability is pivotal. Thin-caliper development and micro-flute innovations allow lighter boxes while preserving crush resistance, enabling freight savings that resonate in e-commerce workflows. Mondi’s 420,000 tonne recycled containerboard line in Italy exemplifies regional integration that can shorten lead times into Qatar. Converters unable to source Forest Stewardship Council-certified supply may miss out on export opportunities to retailers mandating traceable fiber, underscoring certification as a hygiene factor rather than a differentiator.

By Printing Technology: Digital Platforms Capture Short-Run Growth Sweet Spot

Lithographic Printing maintained a 38.17% revenue lead in 2025 by efficiently handling runs of 10,000 units or more and accommodating specialty coatings. Digital Printing, however, is projected to advance at 6.59% CAGR, buoyed by the escalating need for variable data, rapid design refreshes, and SKU proliferation. Over 80% of regional short- and medium-run printing is expected to migrate to digital in the next five years, driven by the economics of inkjet and electrophotographic presses.

Flexographic Printing endures in corrugated post-print but yields quality gaps in fine halftones, limiting penetration in folding cartons. HP Indigo 200K installations and Sigma Labels’ Epson SurePress L-6534VW showcase investments that cut order cycles from weeks to days.[2]Epson, “Sigma Labels UAE Digital Press Installation,” EPSON.COM Hybrid workflows pair offset solids with digital personalization, enabling converters to achieve modularity across order bands. Yet a chronic skills shortage, as only one in five operators master color management, according to industry surveys, threatens utilization rates and underscores the value of continuous workforce development.

By End-User Industry: E-Commerce Redraws Carton Specifications and Volumes

Food and Beverage captured 35.62% of demand in 2025, its prospects buoyed by retail sales poised to rise from QAR 70.87 billion (USD 19.44 billion) in 2026 to QAR 86.37 billion (USD 23.73 billion) by 2031. Yet E-commerce and Retail-ready Packaging is the fastest mover, projected to grow at a 7.18% CAGR, driven by unboxing aesthetics and tamper-evident features vital to direct-to-consumer logistics. Healthcare and Pharmaceuticals demand escalates as new domestic production comes online, commanding higher price realizations linked to ISO 15378 serialization.

Personal Care and Cosmetics leans into Coated Unbleached Kraft’s natural shade to signal clean formulas, while Electrical and Electronics cartons integrate anti-static layers. Tobacco, under plain-pack regulations, faces volume drag, but duty-free retail at Hamad International Airport preserves niche volume. Converters offering bundled solutions, folding cartons, corrugated outers, and serialized labels win share by simplifying procurement for omnichannel brands.

Geography Analysis

Doha and Mesaieed Industrial Zone host most converter capacity, benefiting from proximity to FMCG plants and the Domestic Solid Waste Management Center. Household waste-segregation pilots raised Doha’s residential recycling rates to over 85% in 2025, improving the feedstock for recycled fiber. Commercial segregation still lags, leaving high-volume retail and foodservice scrap under-recovered.

Northern municipalities, including Al Khor and Al Shamal, gain relevance as Qatar Rail extensions near completion by 2030, widening retail catchment and driving folding-carton demand for grocery and quick-service outlets. Lusail City’s micro-fulfillment nodes require precision-cut cartons compatible with robotics, rewarding converters adept at meeting tight tolerances and verifying barcodes.

Mesaieed’s Al-Afjah Recycling Hub, though only 21 of 51 plots are active, is on track to become a Gulf Cooperation Council recycling cornerstone. Elite Paper Recycling’s 4,500-tonne monthly collection, coupled with Ministry of Municipality incentives that granted factories 28,000 tonnes of free recyclables in 2024, lowers input costs for plants willing to substitute virgin grades.[3]Sustainable Packaging Middle East and Africa, “Qatar Advances Circular Economy,” SUSTAINABILITYMEA.COM Nonetheless, sustained export of recovered fiber underscores the urgency of local end-market development to advance circularity.

Competitive Landscape

The market remains moderatly concentrated as the local players Gulf Carton Factory, Elite Paper Recycling, Doha Modern Factory, and Al Zaini Converting Industries service fast-moving consumer goods orders, while multinationals Smurfit WestRock, Mondi, Huhtamaki, and International Paper supply premium and export-oriented niches. Smurfit WestRock’s 2024 merger created a USD 34 billion integrated supplier, giving it procurement leverage and innovation budgets beyond regional rivals.

Mondi’s March 2025 acquisition of Schumacher Packaging assets added 2,200 staff and deepened corrugated converting scale, a template for future Middle East consolidation.[4]Mondi Group, “Q1 2025 Trading Update,” MONDIGROUP.COM Napco National’s August 2025 purchase of Arabian Flexible Packaging highlights strategic bundling of folding cartons with flexible films, catering to brands seeking single-supplier convenience. Doha Modern Factory’s four-color press upgrade lifts monthly throughput to 1,000 tonnes, signaling its intent to capture import-substitution opportunities amid national self-sufficiency goals.

Competitive differentiation now centers on digital print agility, ISO 15378 pharmaceutical certification, and guaranteed recycled-content sourcing. Talent scarcity in advanced color management and high-speed die-cutting remains a cross-industry pain point, inflating recruitment and training costs. Plants embedding apprenticeship schemes or automating make-ready processes mitigate exposure. Greenfield investment could rise as FIFA-related infrastructure expands consumer catchment areas; however, pulp price swings oblige cautious capital budgeting.

Qatar Folding Carton Industry Leaders

Gulf Carton Factory Co.

Al Zaini Converting Industries W.L.L

Papercut Factory

Al Bayader International LLC

Hotpack Packaging Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bobst showcased its new zero-fault folding carton production lines at regional events, introducing inline inspection and defect detection to maximize production efficiency.

- March 2026: Papercut Factory finalized the acquisition of Ecoleaf Food Packaging & Printing Company, expanding its domestic capacity for eco-friendly folding cartons and food-grade paper products.

- August 2025: Napco National, via Dubai subsidiary, acquired Arabian Flexible Packaging to broaden regional manufacturing reach.

- May 2025: Hotpack Global committed USD 100 million for its first United States manufacturing site in New Jersey.

Qatar Folding Carton Market Report Scope

The folding carton market refers to the industry that produces, distributes, and uses paperboard-based packaging solutions that are folded into various shapes and sizes to package goods. These cartons are widely used across industries such as food and beverage, healthcare, personal care, and others for their lightweight, recyclable, and customizable properties. The report analyzes the folding carton market in Qatar, focusing on market trends, growth drivers, challenges, and opportunities. The study also examines the competitive landscape, supply chain dynamics, and market forecasts for the defined study period.

The Qatar Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Qatar folding carton market?

The Qatar folding carton market size is USD 93.38 million in 2026.

Which material type leads demand in Qatar?

Folding Boxboard led with 42.19% market share in 2025, reflecting its stiffness and printability advantages.

How fast will digital printing grow within Qatari folding cartons?

Digital Printing is forecast to register a 6.59% CAGR through 2031 as brands shift to short-run, variable-data jobs.

What is the key restraint facing local converters?

Volatile virgin pulp prices, which lifted to USD 740 per ton in February 2026, erode converter margins by up to 12% points.

Which end-user segment shows the fastest growth?

E-commerce and Retail-ready Packaging is advancing at a 7.18% CAGR, driven by direct-to-consumer fulfillment needs.

Page last updated on: