Qatar Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

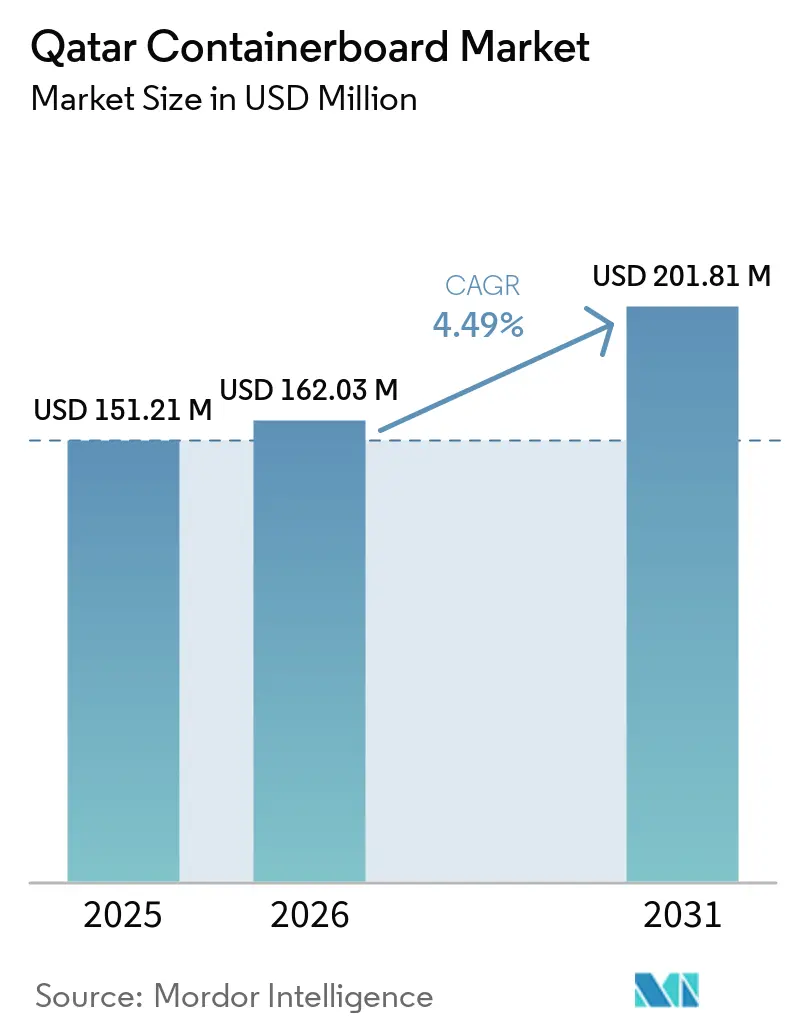

| Base Year Market Size (2025) | USD 151.21 Million |

| Market Size (2026) | USD 162.03 Million |

| Market Size (2031) | USD 201.81 Million |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

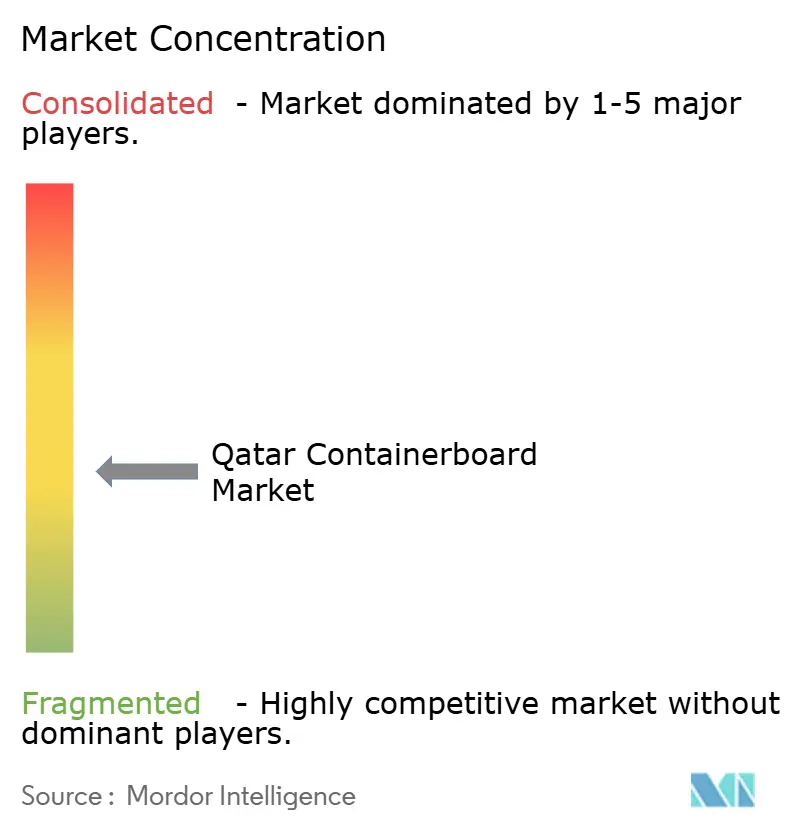

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Containerboard Market Analysis by Mordor Intelligence

The Qatar containerboard market size is projected to expand from USD 151.21 million in 2025 and USD 162.03 million in 2026 to USD 201.81 million by 2031, registering a CAGR of 4.49% between 2026 to 2031. Growth in the Qatar containerboard market is being shaped by structural packaging demand from e-commerce, food manufacturing, and broader import-linked trade flows rather than by short-term shipment swings. Faster fulfillment models in Doha and nearby urban centers are increasing corrugated box use per order, while steady growth in domestic food production is supporting repeat demand for secondary packaging across staple categories. The plastic bag phaseout has also widened the role of paper-based formats in retail and transport packaging, which is reinforcing demand visibility for the Qatar containerboard market over the forecast period. Qatar’s role as a transshipment hub adds a separate layer of packaging demand, as re-export cargo drives box consumption beyond domestic retail sales. Import dependence remains a key feature of the Qatar containerboard market, so regional capacity additions in the UAE and Saudi Arabia are likely to influence pricing, availability, and converter margins over the medium term.

Key Report Takeaways

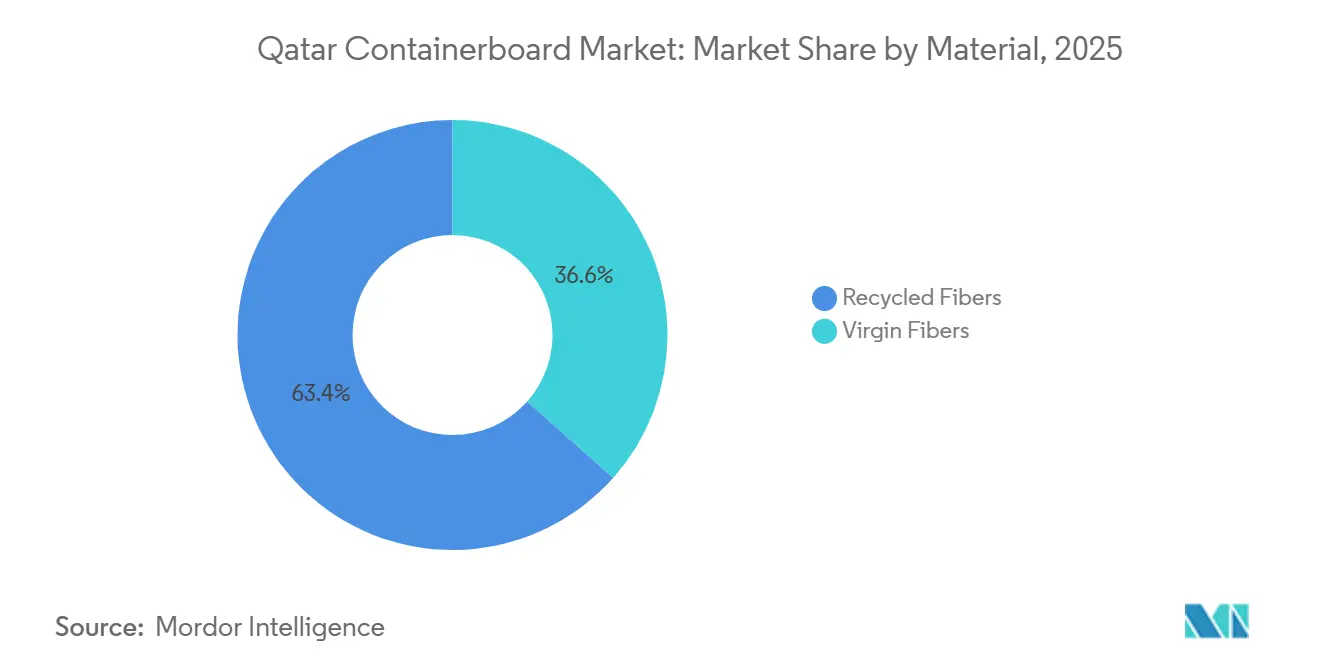

- By material, recycled fibers captured 63.44% of the Qatar containerboard market share in 2025.

- By product type, the Qatar containerboard market size for the kraftliners segment is forecast to advance at a 4.94% CAGR through 2031.

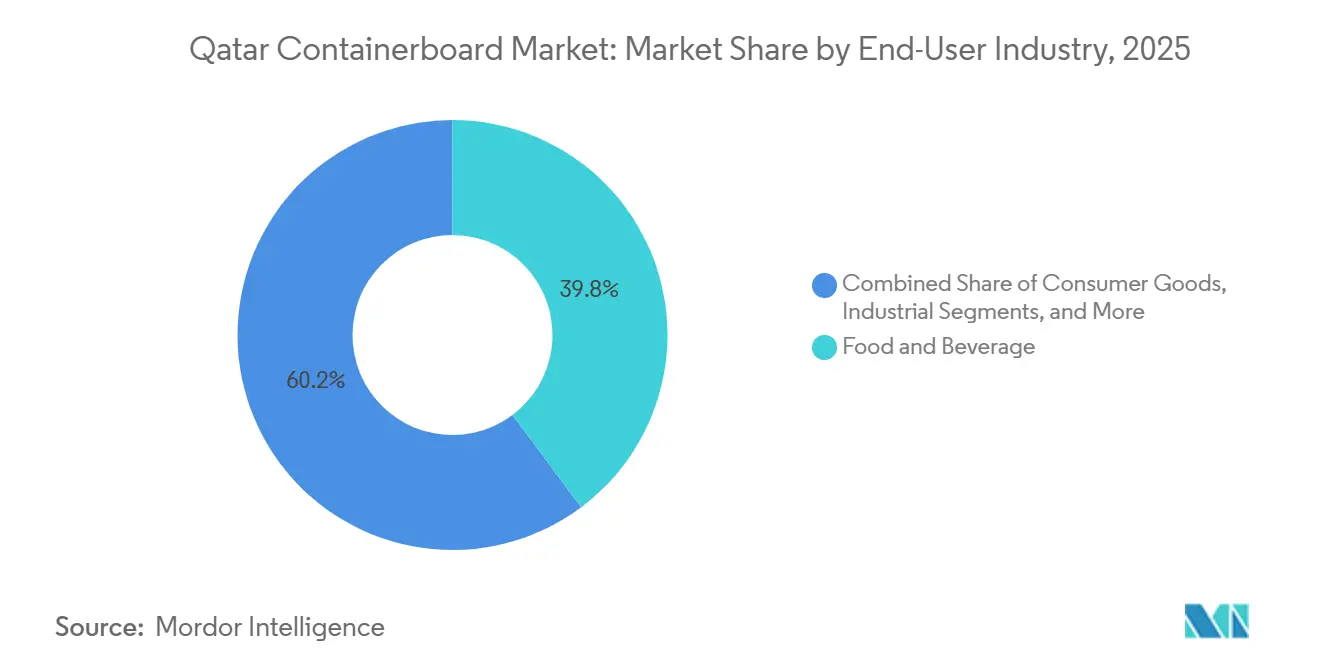

- By end-user industry, food and beverage captured 39.78% of the Qatar containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce And Quick-Commerce Shipment Density | +1.2% | Qatar, concentrated in Doha, Lusail, and Al Rayyan urban cores | Short term (≤ 2 years) |

| Expansion Of Food Manufacturing And Delivery Packaging Demand | +0.9% | Qatar, with production activity centered in Mesaieed and Doha Industrial Area | Medium term (2-4 years) |

| Plastic Substitution And Paper-Friendly Retail Compliance | +0.7% | Qatar, national rollout under Ministerial Decision No. 143/2022 | Medium term (2-4 years) |

| Growth In Industrial Output And Local Product Sales | +0.5% | Qatar, led by Mesaieed Industrial City and Ras Laffan Industrial City | Medium term (2-4 years) |

| Rising Re-Export And Port-Linked Secondary Packaging Needs | +0.4% | Qatar, centered at Hamad Port with spillover to transshipment corridors | Short term (≤ 2 years) |

| Improving Waste Segregation And Recovered Fiber Circularity | +0.2% | Qatar, with Doha as early pilot zone expanding to Al Daayen and Al Khor by 2026 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce And Quick-Commerce Shipment Density

Qatar’s e-commerce sector reached USD 4.54 billion in 2025 and is projected to reach USD 4.96 billion in 2026, with a CAGR of 9.34% through 2031. Qatar Central Bank data also showed that e-commerce transactions grew 15% year over year in June 2025, reaching QR 4.28 billion in value, suggesting a direct rise in box and mailer demand per order. The compact urban layouts of Doha, Lusail, and Al Rayyan support same-day and next-day delivery models, which are pushing the Qatar containerboard market toward lighter single-wall corrugated grades used in more frequent shipments. This shift is important because smaller parcel sizes still require packaging integrity, which means converters need a steady supply of lightweight testliner and fluting grades for high-speed boxmaking. The Qatar containerboard market is therefore benefiting not only from higher online spending, but also from the growing shipment density that comes with mobile-led purchasing behavior.

Expansion Of Food Manufacturing And Delivery Packaging Demand

Qatar’s food manufacturing base exceeded 138 national factories operating at full capacity in early 2026, covering dairy, meat processing, bakery, grains, juice, and edible oils. The manufacturing sector added QAR 26.84 billion (USD 7.36 billion) to GDP in the first half of 2025, with food among the main contributors to that expansion. Each increase in local food output creates repeat demand for corrugated transport boxes, food-grade inner liners, and retail-ready display cartons, which keeps the Qatar containerboard market closely tied to domestic production plans. Delivery packaging adds another layer, as meal kits, prepared food, and chilled products often require corrugated formats with higher performance requirements. The food and beverage sector remains a stabilizing force for the Qatar containerboard market, as it supports both factory shipments and urban delivery channels.

Plastic Substitution And Paper-Friendly Retail Compliance

Ministerial Decision No. 143 of 2022 banned single-use plastic bags across establishments in Qatar and required the use of paper, biodegradable, or reusable alternatives.[1]Ministry of Municipality, “Ministerial Decision No. 143 of 2022 on the Controls of the Use of Plastic Bags,” Ministry of Municipality, lexismiddleeast.com Enforcement activity continued through 2025, and nationwide campaigns kept the shift visible to retailers and consumers. This policy does not replace plastic with containerboard on a one-to-one basis, but it does push paper formats deeper into retail operations, shelf-ready packaging, and product protection. Al Meera’s July 2025 campaign with Al Rayan Bank showed that compliance had moved beyond a legal requirement and had become part of retailer branding and customer communication. For the Qatar containerboard market, that matters because long-duration paper commitments from retailers and food producers give converters more stable medium-term demand visibility.

Growth In Industrial Output And Local Product Sales

Qatar’s industrial investment volume reached QAR 270 billion (USD 74.2 billion) in Q1 2026, and 17 new factories commenced production during the period. The Industrial Production Index rose to 107.4 points in January 2026, up 6.3% month on month, which reflected stronger activity across manufacturing and related industrial lines.[2]Qatar National Planning Council, “Qatar’s Industrial Production Index Rises 6.3% in January,” Qatar News Agency, qna.org.qa The number of operating factories also increased to over 1,000 in 2025, while nationally produced products rose to over 1,815, indicating that more goods are moving through domestic distribution channels. That trend supports the Qatar containerboard market because every new product line needs outer packaging for storage, transport, and wholesale movement. Heavier corrugated grades used for machinery, construction materials, chemicals, and industrial goods are also benefiting as more local output moves through the national supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Fiber And Linerboard Price Volatility | -0.8% | Global, with concentrated import-cost exposure across Qatar’s converter base | Short term (≤ 2 years) |

| Small Domestic Market And Limited Mill Scale | -0.6% | Qatar, national, inability to achieve economies of scale comparable to Saudi Arabia or UAE peers | Long term (≥ 4 years) |

| Limited Domestic OCC Recovery Depth | -0.5% | Qatar, particularly Doha and surrounding municipalities in early collection build-out | Medium term (2-4 years) |

| Red Sea And Gulf Shipping Disruption Risk | -0.4% | GCC-wide, with direct operational impact on Qatar’s import-dependent containerboard supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Imported Fiber And Linerboard Price Volatility

The Qatar containerboard market remains exposed to imported input pricing, as no domestic mill produces the full range of linerboard and fluting grades required by the converting sector at commercial scale. Converters therefore depend on regional and international mills for recycled testliner, corrugating medium, and virgin kraftliner, which ties landed costs to freight conditions and benchmark paper prices. Shipping disruptions in Gulf trade routes during early 2026 added pressure to regional logistics and further exposed import-dependent buyers to vulnerability. In practice, this often leads to margin compression rather than an immediate drop in demand, because converters cannot always pass through cost increases to food, FMCG, and industrial customers. The Qatar containerboard market can therefore continue growing in volume while still facing profitability pressure when input prices move sharply.

Small Domestic Market And Limited Mill Scale

At USD 162.03 million in 2026, the addressable market for containerboard in Qatar remains modest compared with the largest GCC packaging markets, which limits the case for a large dedicated paper machine. Al Suwaidi Group’s paper manufacturing operation marked an important local step, but its board capacity remains narrower than the full set of containerboard grades required by converters serving the local box market.[3]Ministry of Commerce and Industry, “Al Suwaidi Group,” Made in Qatar Portal, madeinqatar.qa This means the Qatar containerboard market will remain structurally dependent on imported supply through the forecast period, even as downstream conversion demand expands. The same scale limit also affects new investment decisions, because any new mill would likely need export volumes to operate efficiently, which would put it directly against established suppliers from Saudi Arabia, Kuwait, and the UAE. As a result, local converters in the Qatar containerboard market are still more likely to compete on service, customization, and delivery than on upstream fiber integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Grades Anchor The Value Chain

Recycled fibers held 63.44% of the Qatar containerboard market in 2025, which made OCC-based testliner and fluting the core feedstock for the domestic corrugated supply chain. This mix reflects the basic structure of the Qatar containerboard industry, where converters rely on regional imports of recycled-content boards from Kuwait, Saudi Arabia, and the UAE rather than on a fully integrated domestic paper base. Brown testliner and corrugating medium remain the practical choice for many food service, retail, and industrial applications because they balance cost, availability, and functional performance. That has kept recycled grades at the center of the Qatar containerboard market even as premium packaging needs have become more visible.

Qatar’s waste segregation program also supported this trend in 2025, when household compliance in Doha exceeded 85%, and the Ministry of Municipality distributed more than 10,858 recycling containers across the city. The same program recovered nearly 2,183 tonnes of recyclable materials, indicating a gradually improving recovered paper pool that can support regional circularity over time. Virgin fibers are the fastest-growing sub-segment, with the Qatar containerboard market size for this tier projected to expand at a 4.86% CAGR through 2031. The growth outlook is tied to premium kraft linerboard demand in fresh food, export packaging, and branded retail applications, where moisture resistance, burst strength, and visual quality matter more than the lowest-cost recycled board.

By Product Type: Testliners Lead, Kraftliners Gain Momentum

Testliners held 42.17% of the Qatar containerboard market share in 2025, confirming that recycled-content linerboard remains the mainstay of box production for retail, e-commerce, and food delivery. Its position is supported by volume economics and by the fact that many day-to-day packaging applications do not require the higher performance of virgin kraft linerboard. At the same time, Kraftliners is the fastest-growing product type and is set to record a 4.94% CAGR through 2031 as export-oriented packaging and industrial shipments demand stronger outer facings. This is where the Qatar containerboard market is showing a clearer split between cost-driven grades for broad use and performance-driven grades for heavier, moisture-sensitive, or higher-value goods.

Regional supply changes are likely to influence this product mix over the next few years. Star Paper Mill commenced production at its recycled containerboard facility in KEZAD in April 2026, adding 135,000 tonnes per year of testliner and corrugating medium to the regional base. MEPCO’s PM5 line in Jeddah is also scheduled to add 450,000 tonnes per year of high-quality recycled containerboard by Q4 2027, with a product mix that directly addresses lightweight testliner needs in the GCC.[4]Voith SE and Co. KZ, “MEPCO Commissions Voith With Construction of Complete Production Line for Recycled Containerboard at Its Jeddah Mill in Saudi Arabia,” Voith, voith.com In the Qatar containerboard market, these additions should gradually improve access to lighter recycled grades and may reduce the need to source niche, low-basis-weight board from farther markets. That would support converters looking to match the packaging profile of dense urban parcel shipments without taking on the same import premium seen in earlier periods.

By End-User Industry: Food And Beverage Dominates, Consumer Goods Gains Pace

Food and beverage accounted for 39.78% of the Qatar containerboard market in 2025, making it the largest end-user segment by a clear margin. This base is closely linked to Qatar’s food security agenda and to the steady expansion of domestic processing capacity across dairy, meat, bakery, grains, juice, and edible oils. Corrugated secondary packaging remains essential in this segment because it supports both wholesale movement and retail presentation for goods that must move through temperature-controlled and fast-turn channels. The consumer goods segment, however, is projected to grow at a 5.02% CAGR through 2031, making it the fastest-moving demand pocket in the Qatar containerboard market.

That growth is tied to broader FMCG manufacturing, stronger household goods distribution, and the packaging needs created by online retail channels. Brand owners are also influencing specifications, especially where sustainability requirements favor certified paperboard and better print quality for consumer-facing transport packs. The industrial segment remains smaller than the food and beverage segment, but it is benefiting from the rising factory base in Mesaieed and Ras Laffan, where heavier double- and triple-wall formats are used for machinery, chemicals, and construction-related goods. The other end-user category, which includes pharmaceuticals, retail, and logistics, is also expanding as healthcare infrastructure and pharmaceutical distribution requirements grow. That part of the Qatar containerboard industry favors higher-specification cartons because packaging integrity standards are stricter, often pushing converters toward stronger virgin outer liners.

Geography Analysis

Hamad Port handled nearly 1.46 million TEUs in 2025, with transshipment cargo accounting for nearly 50% of throughput, making the port catchment the strongest geographic demand node for packaging linked to trade and re-export activity. The Qatar containerboard market is otherwise concentrated across 3 clear zones: Doha and its surrounding urban districts, the Mesaieed Industrial City corridor, and the Ras Laffan Industrial City corridor. Doha, Lusail, Al Rayyan, and West Bay generate the densest consumer packaging demand because they house major retail activity, fulfillment hubs, and a large share of food delivery traffic. That urban concentration matters because higher order frequency can lift corrugated unit demand even when average shipment weight remains modest. In parallel, large industrial clusters outside the capital create a more stable baseline for the Qatar containerboard market through recurring factory shipments.

The Industrial Production Index reached 107.4 points in January 2026, up 6.3% month on month, reflecting stronger manufacturing activity in major industrial areas. Mesaieed and Ras Laffan account for a large share of heavy industrial output, including chemicals, refining, and food manufacturing, and each operating plant adds a regular need for corrugated transport packaging. That gives the Qatar containerboard market a geographic demand base that is not tied only to household spending or retail cycles. It also means industrial packaging demand is likely to remain geographically concentrated even as urban consumer packaging continues to grow.

Transshipment through Hamad Port adds a distinct layer, as secondary packaging is also required for goods moving onward to South Asia, East Africa, and nearby Gulf routes. Container transshipment volumes surged 11% in the first half of 2025, and Qatar ports recorded a further 14% month-on-month increase in container handling in April 2026. Mwani Qatar’s March 2026 decision to extend storage periods for import, export, and transshipment containers supports this role by giving port users greater operating flexibility. Within the GCC, the Qatar containerboard market is smaller than those of Saudi Arabia and the UAE, yet higher income levels support a packaging mix that leans toward better print quality and stronger board specifications. This geography also carries a risk premium because shipping disruptions in Gulf routes during early 2026 forced some cargo to reroute and added lead time to import-dependent packaging supply.

Competitive Landscape

The Qatar containerboard market is moderately fragmented because no single domestic player controls supply across all product grades and end-user needs. Al Suwaidi Group remains the most visible local paper manufacturing name, operating a multilayer kraft board capacity of up to 300 tonnes per day at 120-400 GSM through advanced recycling technologies. Gulf Carton Factory Qatar, Rosco Pack LLC, and other local corrugated producers mainly serve converter-level demand by processing imported board into finished boxes for food manufacturers, FMCG suppliers, and industrial customers. Regional suppliers such as MEPCO, United Carton Industries, Napco National, and Gulf Paper Manufacturing also shape the Qatar containerboard market by supplying a large share of the linerboard and corrugating medium used by local box makers. Qualification standards set by multinational FMCG buyers further reinforce this structure because smaller entrants must meet consistent quality, sustainability, and food-contact expectations before they can win larger contracts.

Recent strategic moves show how regional players are positioning around this gap. United Carton Industries moved ahead with its IPO in 2025, thereby strengthening access to capital for its wider GCC expansion plans. It also approved an expansion project for its Ras Al Khaimah Packaging subsidiary in January 2026, which supports the company’s stated push into markets beyond Saudi Arabia, including Qatar. Star Paper Mill’s full production start in Abu Dhabi in April 2026 added a nearby supply source for recycled containerboard and created a model for how a mid-scale GCC free zone mill can serve proximate markets such as Qatar. These developments matter because the Qatar containerboard market still lacks domestic commercial-scale testliner and fluting production, so regional board capacity remains a key competitive lever.

The clearest white space remains domestic recycled containerboard production aimed at local converters. No mill currently supplies commercial-scale testliner and fluting in Qatar, leaving the supply chain exposed to import pricing and regional freight conditions. There is also room in the Qatar containerboard market for lightweight, high-performance corrugated designed for e-commerce fulfillment because much of the local supply base has historically leaned toward heavier industrial grades. A second opening exists in certified sustainable packaging for multinational consumer brands that require recycled-content claims or chain-of-custody documentation. MEPCO’s PM5 project is important here because its future output is expected to improve the regional availability of lighter recycled containerboard grades that have often been harder to source competitively in the GCC. The Qatar containerboard market, therefore, remains competitive at the converter level, but the upstream advantage still sits with regional producers that combine scale, access to recovered fiber, and shorter delivery routes to the Gulf.

Qatar Containerboard Industry Leaders

Hotpack Packaging Industries LLC

Rosco Pack LLC

Fadel Group

QK International

Napco National

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: GII (Gulf Islamic Investments) completed a minority equity investment in Hotpack Global Holding Ltd, with proceeds designated to scale recently commissioned manufacturing capacity and accelerate Hotpack's international expansion, including a new food packaging facility in Al Kharj, Saudi Arabia, among the Kingdom's largest specialized food packaging projects, anchored by long-term supply agreements with key customers.

- April 2026: Star Paper Mill Paper Industry LLC commenced full production at its recycled containerboard facility in KEZAD, Abu Dhabi, UAE, officially inaugurated by UAE Minister of Industry and Advanced Technology H.E. Dr. Sultan Al Jaber at Make it in the Emirates 2026, the plant has an annual capacity of 135,000 tonnes and will recycle up to 80% of waste paper sourced domestically, easing regional supply pressure on GCC importers including Qatar.

- April 2026: Qatar ports recorded a 14% rise in container handling volumes in April 2026 compared to March, with Hamad, Ruwais, and Doha ports collectively processing 50,738 TEUs and receiving 93 vessels, up 9% month on month, reinforcing Qatar's expanding role as a transshipment hub with direct implications for secondary packaging demand.

- March 2026: Mwani Qatar activated an exceptional package of port tariff facilitations, extending full container export storage periods from 10 to 30 days and transshipment container storage from 15 to 30 days, in a move to reduce operational pressure on port users and support supply chain growth tied to re-export packaging activities.

Qatar Containerboard Market Report Scope

The Qatar Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Qatar Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and forecast of the Qatar containerboard market?

The Qatar containerboard market was valued at USD 151.21 million in 2025, is estimated at USD 162.03 million in 2026, and is projected to reach USD 201.81 million by 2031 at a 4.49% CAGR.

What is driving demand for containerboard in Qatar?

Demand is being supported by e-commerce growth, expanding food manufacturing, paper-based packaging adoption after the plastic bag ban, and higher industrial output.

Which material segment leads in Qatar?

Recycled fibers led with 63.44% share in 2025 because OCC-based testliner and fluting remain the main supply inputs for local corrugated conversion.

Which product type is growing the fastest?

Kraftliners is projected to grow at a 4.94% CAGR through 2031, while testliners remained the largest product type with 42.17% share in 2025.

Which end-user category contributes the most demand?

Food and beverage was the largest end-user segment with 39.78% share in 2025, supported by more than 138 national food factories operating at full capacity in early 2026.

Why does Hamad Port matter for packaging demand?

Hamad Port handled nearly 1.46 million TEUs in 2025, with nearly 50% tied to transshipment, so re-export cargo creates added need for secondary corrugated packaging beyond domestic retail demand.

Page last updated on: