Algeria Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

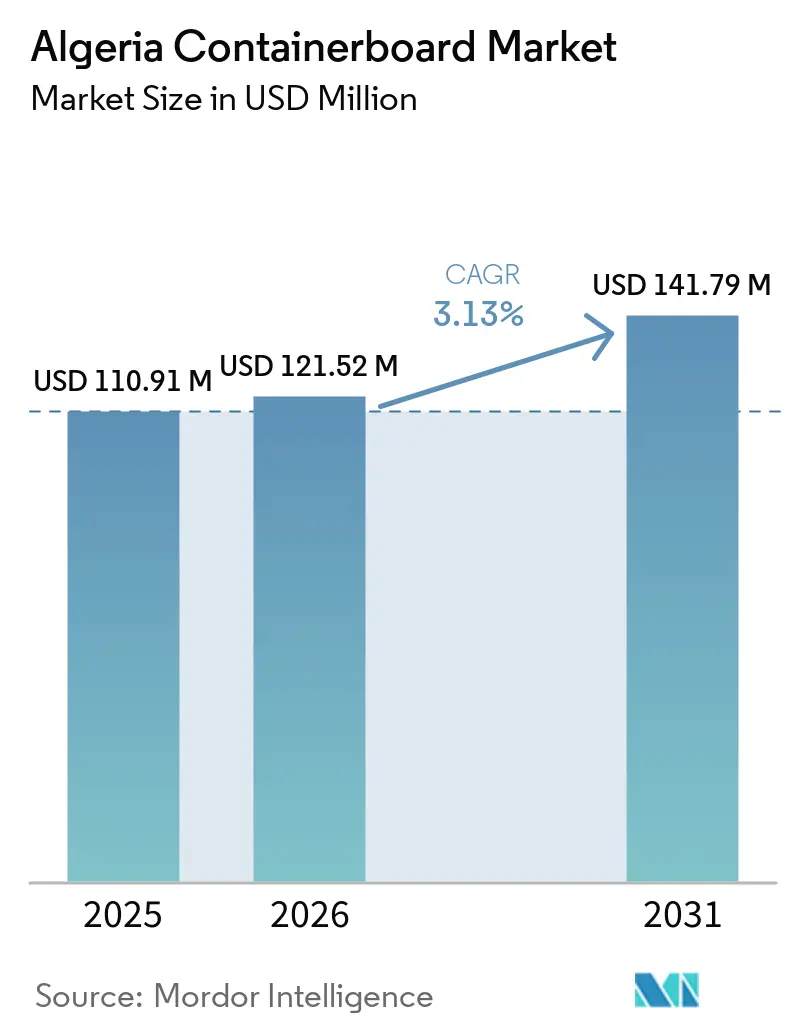

| Base Year Market Size (2025) | USD 110.91 Million |

| Market Size (2026) | USD 121.52 Million |

| Market Size (2031) | USD 141.79 Million |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

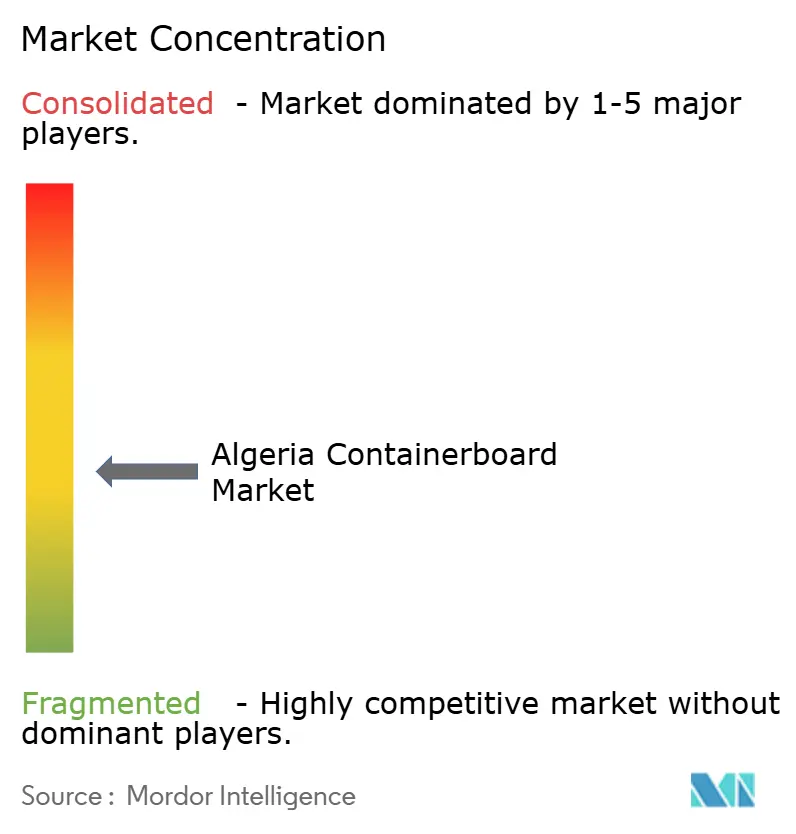

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Containerboard Market Analysis by Mordor Intelligence

The Algeria containerboard market size is expected to grow from USD 110.91 million in 2025 to USD 121.52 million in 2026 and is forecast to reach USD 141.79 million by 2031 at 3.13% CAGR over 2026-2031. This path reflects structural demand creation rather than a short recovery in orders. Public policy continues to direct manufacturing activity beyond hydrocarbons, and food processing, consumer goods, and agro-industrial output remain the main demand anchors for corrugated packaging. The food-processing base plays an outsized role in the industrial economy, giving containerboard demand a broader foundation than Algeria's overall factory scale alone would suggest. The Algeria containerboard market also operates through a two-layer supply structure, with local converters meeting part of demand while imported board still covers a large share of substrate needs. Import controls, tighter payment rules, and planned domestic capacity additions are steadily pushing procurement decisions toward supply security and local substitution.

Key Report Takeaways

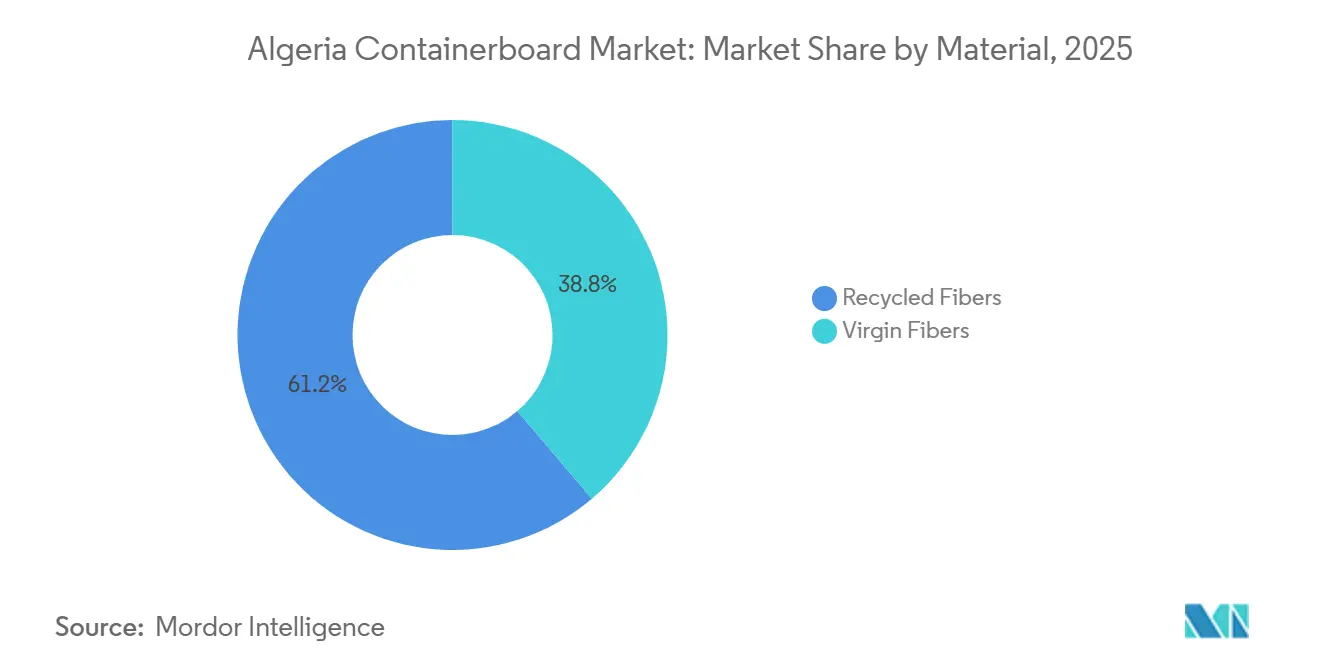

- By material, recycled fibers captured 61.23% of the Algeria containerboard market share in 2025.

- By product type, the Algeria containerboard market size for the kraftliners segment is forecast to advance at a 3.55% CAGR through 2031.

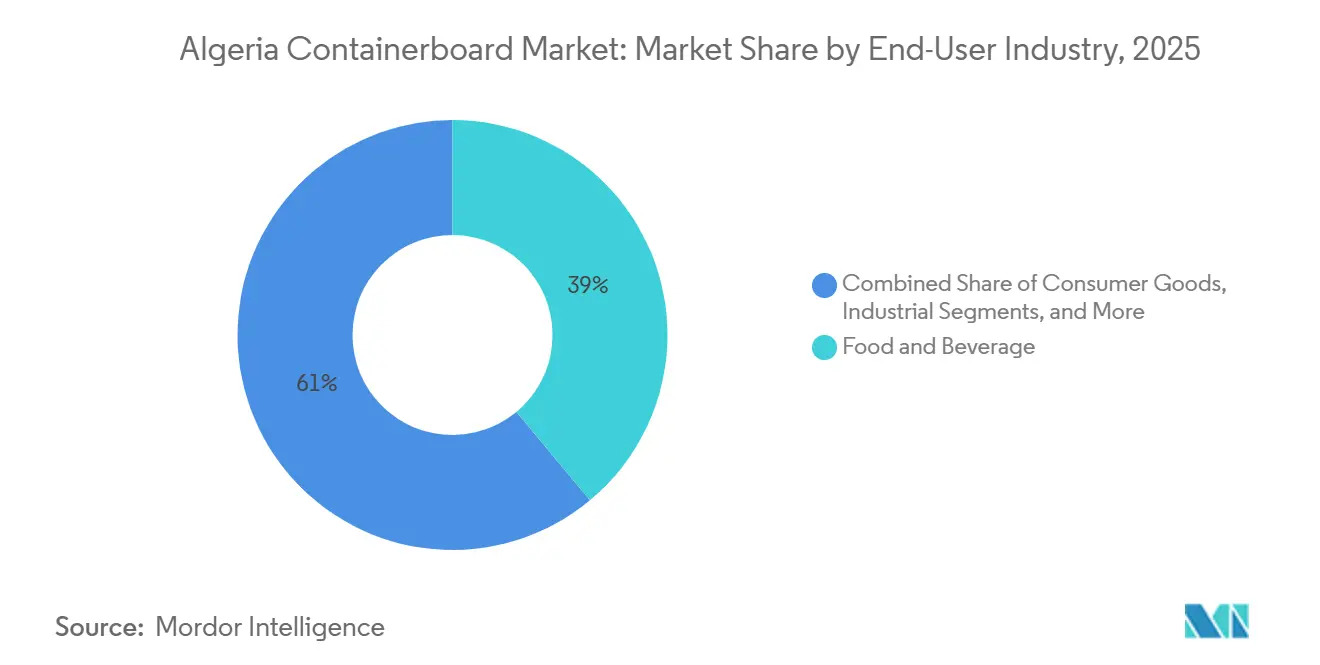

- By end-user industry, food and beverage captured 38.96% of the Algeria containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Algeria Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaged Food And Beverage Output Expansion | +1.2% | National, concentrated in Algiers, Sétif, Oran, and Béjaïa industrial zones | Medium term (2-4 years) |

| Shift Toward Fiber-Based Transit Packaging | +0.8% | National, with early regulatory gains in Algiers and Oran urban retail corridors | Short term (≤ 2 years) |

| Non-Hydrocarbon Manufacturing And Consumer-Goods Expansion | +0.6% | National, spill-over into Blida, Constantine, Annaba, and Tissemsilt | Medium term (2-4 years) |

| Import Substitution In Agro-Industrial Processing | +0.5% | National, anchored to agro-industrial clusters in western and central Algeria | Medium term (2-4 years) |

| Forecast-Program Rules Favor Local Substrate Security | +0.3% | National, with highest immediate impact on Algiers-based import-dependent converters | Short term (≤ 2 years) |

| Waste-Collection Network Expansion Improves Recycled-Fiber Capture | +0.2% | Core sites in Algiers, Oran, and Sétif, spill-over to 12 planned new collection centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Packaged Food And Beverage Output Expansion

Algeria's food and beverage sector remains the largest direct-volume engine for the Algerian containerboard market. The agro-food sector accounted for more than 50% of non-hydrocarbon GDP in 2025 and employed nearly 700,000 people, which kept corrugated demand tied to broad consumer staples rather than isolated export cycles.[1]U.S. Department of Agriculture Foreign Agricultural Service, “Algeria Exporter Guide Annual, AG2025-0004,” USDA FAS GAIN Report, apps.fas.usda.gov Private operators remained active across wheat milling, dairy processing, vegetable oil refining, and beverage production, and each of these categories depends on steady secondary packaging flows. Large upstream food investments also create a packaging multiplier, as new processing capacity increases demand for shippers, trays, and pallet-ready outer cases. The integrated dairy complex under development in Algeria is targeting 100,000 tons of milk powder per year at full capacity, indicating a sizable future need for corrugated shipping cases across retail and institutional channels. That demand base strengthens the Algerian containerboard market because food volumes move regularly and require reliable packaging, even as other industrial orders soften.

Shift Toward Fiber-Based Transit Packaging

The Algeria containerboard market is also benefiting from a clear policy move against single-use plastics in non-primary packaging uses. Law 25-02, enacted on February 20, 2025, amended Algeria's waste-management framework to require the gradual replacement of single-use plastic products, introduce extended producer responsibility, and add eco-design obligations for packaging manufacturers.[2]Journal Officiel de la République Algérienne Démocratique et Populaire, “Loi n° 25-02 du 20 février 2025 modifiant et complétant la loi n° 01-19 relative à la gestion des déchets,” Journal Officiel de la République Algérienne Démocratique et Populaire, joradp.dz This legal shift matters first in transit and secondary formats, where paper-based dividers, wraps, and slip-sheets face fewer technical barriers than primary food-contact packs. Algeria's Finance Law 2025 also raised the plastic bag tax to DZD 200 (USD 1.45) per kilogram, which improved the relative economics of fiber-based alternatives in many transport and retail applications. The result is a wider addressable space for corrugated and paper-based logistics packaging before domestic board capacity fully scales. That substitution effect supports the Algeria containerboard market because it adds fresh volume from regulation-led format change, not only from higher output in existing end uses.

Non-Hydrocarbon Manufacturing And Consumer-Goods Expansion

The Algeria containerboard market is expanding beyond food because non-hydrocarbon manufacturing activity is broadening the country's packaging demand base. Government messaging in 2026 continued to emphasize stronger non-hydrocarbon exports and faster industrial progress across several production lines, signaling a broader need for shipping and handling formats beyond staple goods. Each step from basic assembly toward branded production or export-ready output raises the packaging standard for outer cases, print quality, and compression strength. Consumer goods plants, medical supplies, cosmetics, and light industrial products all require corrugated transport packaging that can withstand longer logistics chains. The same pattern applies to industrial goods because parts, tires, and semi-finished products need inner dividers and stackable cases that ordinary commodity-grade packaging does not always support. This matters for the Algeria containerboard market because industrial diversification creates a second layer of steady demand that is less tied to one single end-use cluster.

Import Substitution In Agro-Industrial Processing

Import substitution in agro-industrial processing is giving the Algeria containerboard market another structural lift. Executive Decree No. 21-94 limited importers of resale goods to a single product category per operator, which increased the appeal of sourcing more packaging inputs locally and reducing dual import exposure.[3]U.S. International Trade Administration, “Algeria's New Regulation on Import of Finished Goods,” Trade.gov, trade.gov The Baladna dairy project in Algeria signed initial Phase 1 contracts worth more than USD 500 million in July 2025 as part of a wider USD 3.5 billion agri-industrial plan aimed at raising domestic milk self-sufficiency. Projects like this not only replace imported food products but also raise demand for moisture-resistant, export-ready corrugated cases that can move through institutional and retail channels. Processors seeking EU-facing quality standards need a consistent board, better traceability, and stable converting performance, which puts greater pressure on local suppliers to improve substrate quality. This dynamic strengthens the Algeria containerboard market because policy support for domestic processing ends up creating a parallel need for stronger local packaging capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Board Price And Freight Volatility | -0.9% | National, most acute for import-dependent converters in Algiers, Oran, and Sétif | Short term (≤ 2 years) |

| Low Recovered-Paper Capture And High Contamination | -0.7% | National, with greatest supply deficit outside the Algiers-Oran-Sétif core triangle | Long term (≥ 4 years) |

| Import Approval And Payment Controls Delay Procurement | -0.5% | National, concentrated impact on SME converters reliant on spot-import sourcing | Short term (≤ 2 years) |

| Utility And Inland Logistics Variability Outside Core Corridors | -0.3% | Interior wilayat beyond the northern coastal strip | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Board Price And Freight Volatility

Imported substrate pricing remains a major restraint because a meaningful part of the Algeria containerboard market still depends on foreign board supply. Smurfit Westrock announced a USD 50 per ton increase effective June 1, 2026, after a USD 20 per ton net increase had already taken effect in the first quarter of 2026.[4]Smurfit Westrock, “Smurfit Westrock Reports First Quarter 2026 Results,” Smurfit Westrock, smurfitwestrock.com Algerian buyers settle many trade transactions in hard currency, so higher board prices feed directly into local working-capital pressure when selling prices are still collected in dinar. The Mandatory Import Forecast Program also requires prior approval for relevant imports, which reduces procurement flexibility when prices change quickly. Buyers often need to carry more buffer stock when shipping or approval timelines become uncertain, which raises financing pressure across the converting chain. This dynamic weighs on the Algeria containerboard market because smaller converters are less able to absorb abrupt cost moves or lock in stable long-term supply terms.

Low Recovered-Paper Capture And High Contamination

Recovered paper remains central to the Algeria containerboard market, yet collection density and fiber cleanliness still limit what domestic mills can use at scale. Général Emballage currently operates collection sites in Algiers, Oran, and Sétif, and plans to add 12 more centers by 2028, which shows that supply infrastructure is still being built rather than fully established. Algeria's Eco-Jem scheme supports packaging recovery, but it covers mixed packaging streams instead of source-separated paper and cardboard. A mixed collection leaves more contamination in the stream and reduces the share of recovered paper that can be used directly in quality-sensitive containerboard production. The Naâma mill is designed to run on 100% locally collected OCC, so its economics depend on a better domestic capture and sorting system than the one available today. Until fiber collection and cleaning improve, the Algeria containerboard market will continue to face a gap between available recovered paper and true mill-ready furnish.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Grades Lead Today, Virgin Fiber Gains For Higher Specifications

Recycled fibers accounted for 61.23% of the Algeria containerboard market share in 2025, while virgin fibers are projected to grow at 3.46% CAGR during 2026-2031. That lead reflects the basic economics of Algeria's converting base, where recycled-grade testliner and fluting remain the most practical choice for cost-sensitive box production. Imported recycled board has usually offered a lower landed cost than virgin kraftliner, even after freight and financing costs are considered. Général Emballage's Naâma project confirms that recycled furnish will remain the supply anchor because the mill is designed to run on 100% OCC and produce 350,000 tons per year at full capacity.

That scale matters because the Algeria containerboard industry still carries a large import burden that local recycled output is intended to replace. ANDRITZ stated that the new line is expected to save Algeria an estimated USD 250 million per year in imported paper once the project is fully operating. Virgin fibers remain smaller in volume, but they are becoming more relevant where exporters and food-safety-focused processors need better cleanliness, stronger burst performance, and more stable print quality. This part of the Algeria containerboard market is growing from a low base, yet it matters more in value terms because higher-grade board supports better margins and stricter packaging specifications.

By Product Type: Testliners Hold The Base, Kraftliners Reflect A Quality Upgrade

Testliners captured 41.17% of the Algeria containerboard market size in 2025. Their lead reflects the current mix of box demand in Algeria, where domestic corrugators mainly supply single-wall and double-wall cases for food distribution and consumer-goods transit. In these uses, recycled-fiber surface quality and compression strength are usually sufficient, especially when converters must balance price, lead time, and substrate availability. Fluting grades complete the supply mix and give box plants flexibility in how they combine facing paper and medium, depending on import access and cost conditions.

Kraftliners are projected to grow at the fastest pace, at 3.55% CAGR during 2026-2031. This change points to a gradual upgrade in the Algerian containerboard market as exporters and branded goods producers seek higher-burst substrates that perform better in long-distance logistics and retail-ready formats. The same shift is evident in applications that require sharper graphics, better print registration, and a more consistent basis weight than standard recycled grades can consistently deliver. Over time, the Algerian containerboard industry is likely to shift from a strongly testliner-led structure toward a more balanced mix, with kraftliner playing a larger role in value-added packaging.

By End-User Industry: Food And Beverage Remains The Core, Consumer Goods Builds Momentum

Food and Beverage accounted for 38.96% of the Algerian containerboard market in 2025, making it the largest end-user group. Demand comes from cereal milling, UHT dairy, edible oils, couscous, and processed meat, all of which rely on corrugated secondary cases built for pallet movement and retail replenishment. These uses also depend on packaging that can withstand cold-chain handling, warehouse stacking, and store-level turnover. The segment therefore provides the Algerian containerboard market with a stable base, as food volumes are consistent and packaging cycles are closely tied to daily consumption.

That base is likely to deepen as new dairy capacity comes online, including the integrated facility under development in Algeria that targets 100,000 tons of milk powder per year at full output. Consumer Goods is the fastest-growing end-user segment and is projected to expand at 3.62% CAGR during 2026-2031, supported by urban retail growth and rising demand for shelf-ready packaging. This part of the Algeria containerboard market benefits from stronger requirements for printability, appearance, and consistency, especially in personal care, home care, and over-the-counter healthcare products. Other end-user industries, including construction materials, ceramics, and glass, add a smaller but steady call on heavy-duty corrugated formats, which keeps industrial demand present even when consumer channels dominate the volume mix.

Geography Analysis

Containerboard demand in Algeria is concentrated in the northern industrial strip, running from Algiers through Béjaïa and Akbou to Sétif, Constantine, and Oran. This corridor accounts for the largest share of converting, food processing, consumer goods, and retail distribution activity in the Algerian containerboard market, even though no formal regional percentage split is disclosed. Béjaïa and Akbou have become the main production heartland because they combine industrial capability with access to the port of Béjaïa, an important entry point for imported board. Oran also serves as a major demand center because it is one of the country's main commercial cities and hosts a meaningful cluster of fast-moving consumer goods and light industrial operations. Général Emballage's industrial footprint in these northern zones reinforces that concentration and helps shorten delivery distances for core converting customers.

Eastern Algeria forms the second layer of demand, centered on Constantine and Annaba, where steel, petrochemicals, and agro-processing support steady use of industrial corrugated packaging. These areas do not match the volume density of the coastal north-central belt, yet they still matter because industrial shipments need heavier-duty cases and regional logistics support. Blida and Bouira are also gaining importance as pharmaceutical and food-processing investment spreads across the Mitidja plain. That spread gives the Algeria containerboard market a wider domestic footprint, even if the northern corridor still dominates national consumption.

The southern interior currently accounts for little demand, but it is set to gain importance as a supply point, as the Naâma mill is planned to start up in the fourth quarter of 2028. Algeria's heavy import exposure remains tied to Mediterranean shipping routes, with Spain, Italy, and France historically serving as key origin points for recycled-grade board and related inputs. FairTrade Messe reported that Algeria ranked as Africa's largest importer of packaging technology in 2024, with EUR 225 million (USD 253 million) in equipment imports, underscoring the scale of downstream converter investment that still depends on a dependable substrate supply. This creates a geographic vulnerability in the Algerian containerboard market because disruptions at Algiers, Oran, or connected sea routes can affect converters across the country simultaneously. The Naâma line is planned to absorb a large share of domestic substrate demand by 2028, thereby reducing some of that exposure by moving part of the board supply inland and closer to national control.

Competitive Landscape

The Algerian containerboard market has a dual structure, with fragmented local converting activity on one side and a significant layer of imported substrate on the other. Général Emballage stands out as the most important domestic player because it combines recovered-paper collection, converting operations, and a large new upstream board investment within one national platform. That position matters in a market where many smaller local converters still compete mainly on delivery speed, regional reach, and customer service rather than clear substrate differentiation. International suppliers, especially European containerboard producers, still influence price and availability because they cover the imported portion of demand that local production has not yet replaced. The Mandatory Import Forecast Program makes that structure more complex because additional overseas supply is not automatically accessible when import approvals and financing checks remain tight.

A clear opening remains in higher-grade kraft substrate, sustainable-certified board for shelf-ready formats, and better supply-chain visibility for food customers that need more traceability. Local converters that invest in higher-end printing and finishing can move beyond plain brown transit packs and compete for retailer-facing packaging contracts. The Naâma mill is central to that shift because its ANDRITZ PrimeLine package includes automation and digitalization systems designed to improve basis-weight consistency and surface quality at scale. If that performance is achieved, the Algerian containerboard market will have a locally available substrate that is better suited to branded food and consumer goods requirements than much of the current commodity-grade supply base. International players without a physical operating presence in Algeria face a disadvantage in these quality-sensitive orders because documentation steps and delivery lead times remain harder to manage from outside the country.

Several strategic moves since 2025 have reshaped competition in the Algerian containerboard market. In April 2026, Général Emballage commissioned ANDRITZ to supply a 350,000-ton-per-year recycled-containerboard line for Naâma, a project that directly targets Algeria's import dependency and future recycled-fiber processing capacity. In February 2026, Smurfit Westrock outlined a plan to achieve USD 7 billion in EBITDA by 2030, and annual capital expenditure of USD 2.4 billion to USD 2.5 billion in 2026, a move that signals continued upstream focus from one of the suppliers serving North African markets. Mondi also completed a major multi-million upgrade in Europe in March 2026, which increases regional supply availability, but Algerian access still depends on import procedures and local purchasing conditions. As a result, the competitive balance in the Algerian containerboard market is shifting less on global capacity alone and more on who can secure a reliable local presence, cleaner fiber access, and faster regulatory navigation.

Algeria Containerboard Industry Leaders

General Emballage S.p.A.

MB Algerian Packaging S.A.R.L.

HWK Pro-Packaging S.A.R.L.

Societe Generale d'Imprimerie S.p.A.

Maghreb Emballage S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bank of Algeria Governor Mohamed Lamine Lebbou signed Directive No. 05-2026, requiring Algerian banks to verify importers' financial strength before approving import-related banking arrangements and capping total uncommitted import transactions across all banks at 100% of a company's equity. The measure materially tightened procurement timelines for containerboard importers by adding a bank-level financial screening step on top of the existing Ministry of Foreign Trade pre-approval requirement.

- April 2026: Général Emballage ordered a complete ANDRITZ PrimeLine recycled-containerboard production line for its greenfield Naâma mill in Algeria. The order, valued in the low three-digit million EUR range and included in ANDRITZ's first-quarter 2026 order intake, covers stock preparation, paper machine, winder, automation, and digitalization systems. The machine, 7.5 m wide at 1,200 m/min design speed and 350,000 tpy capacity, will be the widest and highest-capacity paper machine in Africa, and start-up is scheduled for the fourth quarter of 2028.

- February 2026: Mondi plc completed its EUR 1.2 billion (USD 1.35 billion) multi-mill capital upgrade, including a new machine at Štětí, Czech Republic, and Polish box-plant expansions, adding recycled containerboard and corrugated capacity to its European supply base that serves North African import markets including Algeria.

- February 2026: Smurfit Westrock plc unveiled a medium-term strategic plan targeting USD 7 billion in EBITDA by 2030, anchored by USD 2.4 billion to USD 2.5 billion in annual capital expenditure in 2026. The plan emphasized EMEA and Asia-Pacific customer wins and integration of the 2024 Smurfit Kappa-WestRock merger, directly shaping the supply posture of one of Algeria's key imported-board suppliers.

Algeria Containerboard Market Report Scope

The Algeria Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Algeria Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for containerboard in Algeria through 2031?

The Algeria containerboard market stands at USD 121.52 million in 2026 and is forecast to reach USD 141.79 million by 2031, growing at a 3.13% CAGR over 2026-2031.

Why does food processing matter so much for containerboard demand in Algeria?

Food and Beverage held 38.96% of demand in 2025, and the country's agro-food base remains one of the largest non-hydrocarbon activity centers, which keeps box demand steady across staples and processed goods.

Which material type is leading demand in Algeria?

Recycled fibers led with 61.23% share in 2025 because they remain the most practical and cost-sensitive input for local corrugators, even as virgin fiber gains traction in higher-specification uses.

Which product grade is growing the fastest through 2031?

Kraftliners are projected to expand at 3.55% CAGR through 2031, supported by export-ready packaging needs, better printability requirements, and stronger performance expectations.

What is the biggest supply-side challenge for Algerian converters?

Imported board price volatility and procurement friction remain the main pressure points because a large part of substrate supply still depends on overseas sources and approval-led import processes.

How will the Naâma paper mill change the local supply picture?

The planned 350,000 tpy recycled-containerboard line is designed to reduce import dependence, use 100% locally collected OCC, and improve the availability of domestic board for Algerian converters after start-up in 2028.

Page last updated on: