Protein Crisps Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

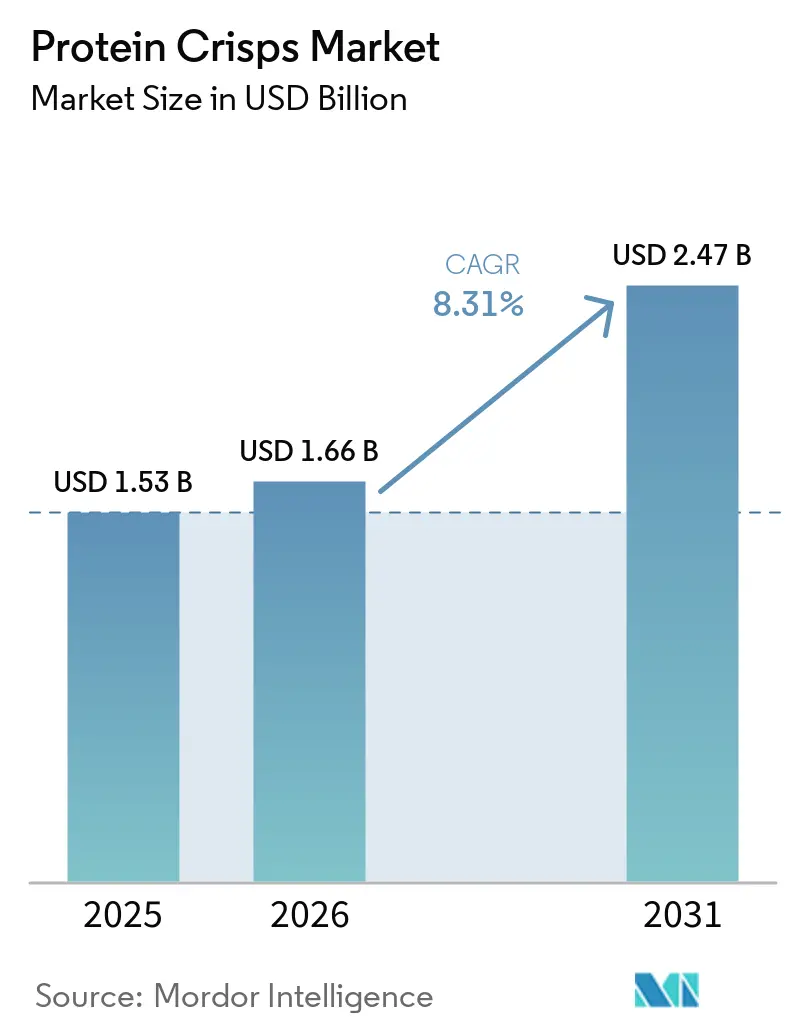

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

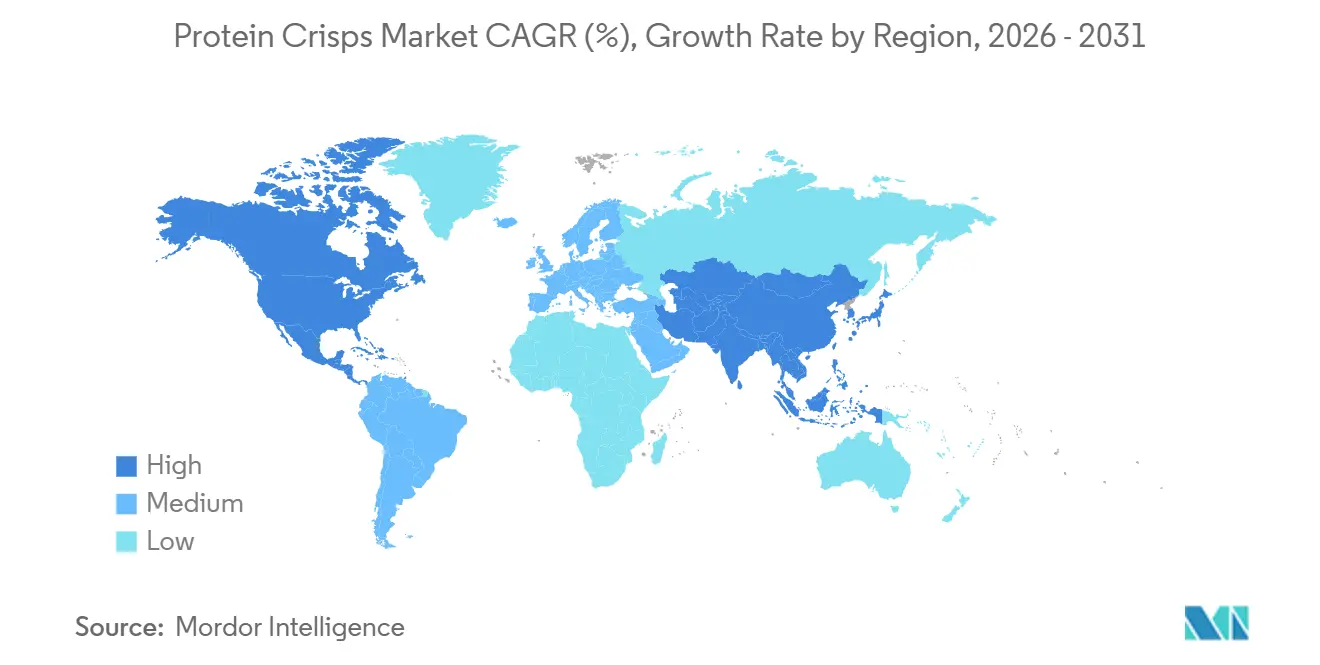

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Crisps Market Analysis by Mordor Intelligence

The protein crisps market size is projected to expand from USD 1.53 billion in 2025 and USD 1.66 billion in 2026 to USD 2.47 billion by 2031, registering a CAGR of 8.31% between 2026 to 2031. As demand surges for convenient, high-protein snacks, and as distribution channels expand across both grocery and online platforms, the category is transitioning from a niche focus on sports nutrition to a mainstream snacking staple. Innovations in ingredients are now seamlessly blending dairy, plant, and upcycled protein sources, catering to evolving consumer preferences for sustainability and health. Hybrid protein formulations are blurring the once-clear lines between dairy and plant-based options. Meanwhile, organic and clean-label endorsements are not just marketing tools; they're justifying premium pricing and prime shelf placements. In response to global brands rolling out indulgent yet functional line extensions, retailers are adjusting their planogram spaces. Furthermore, with the advent of Extrusion 4.0 technology, product development cycles are shrinking, allowing for micro-segmentation and swift flavor introductions. While challenges arise from the volatility of isolate prices and new clean-label regulations limiting binding agents, the long-term outlook remains optimistic. Supermarkets are enhancing their visibility, expanding their online offerings, and aggressively rolling out new products. This strategy, employed by both established food giants and emerging brands, is deepening their penetration into the market. Furthermore, clearer regulations on protein claims in key markets are reducing labeling risks and bolstering premium pricing[1]Source: U.S Food & Drug Administration, "Use of the "Healthy" Claim on Food Labeling", fda.gov. Notably, 12% of U.S. adults on GLP-1 medications are now gravitating towards these protein-rich, satiating snacks.

Key Report Takeaways

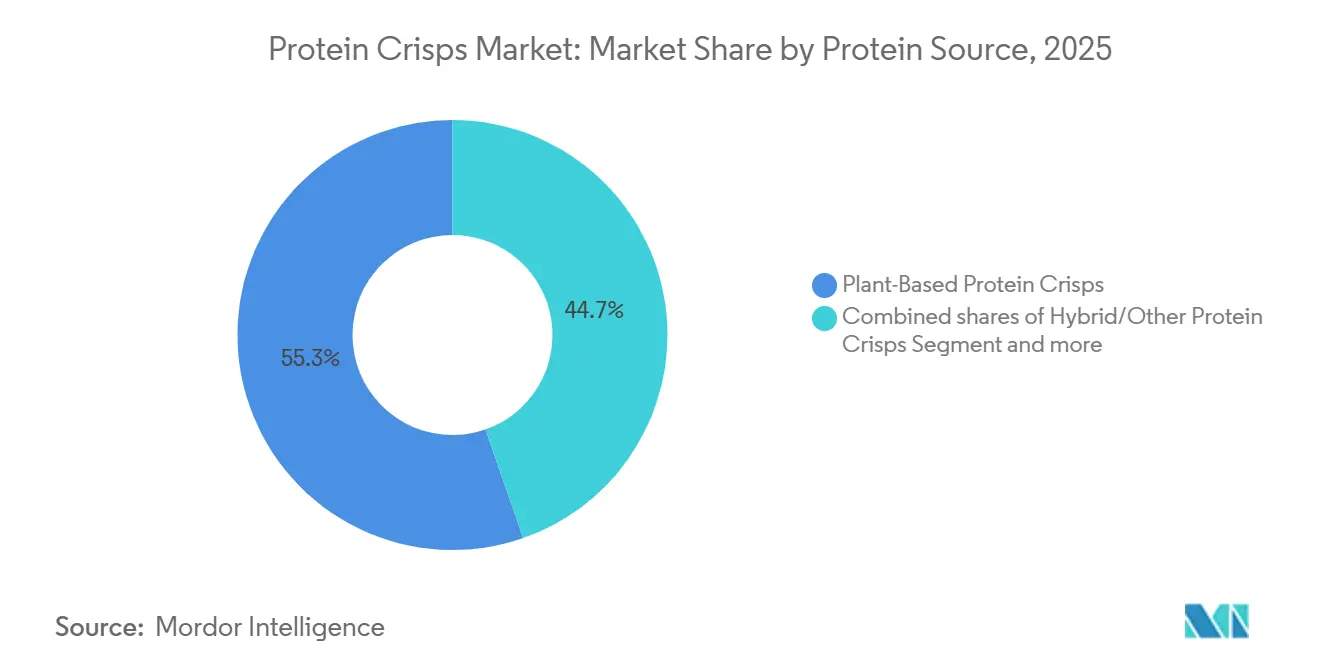

- By protein source, plant-based crisps led with 55.34% of 2025 revenue and hybrids are forecast to advance at a 9.82% CAGR through 2031.

- By category, conventional products held 80.34% share in 2025, while organic variants are set to expand at a 10.32% CAGR during 2026-2031.

- By flavor, seasoned variants captured 85.33% of 2025 sales and unflavored options are predicted to grow at an 8.77% CAGR to 2031.

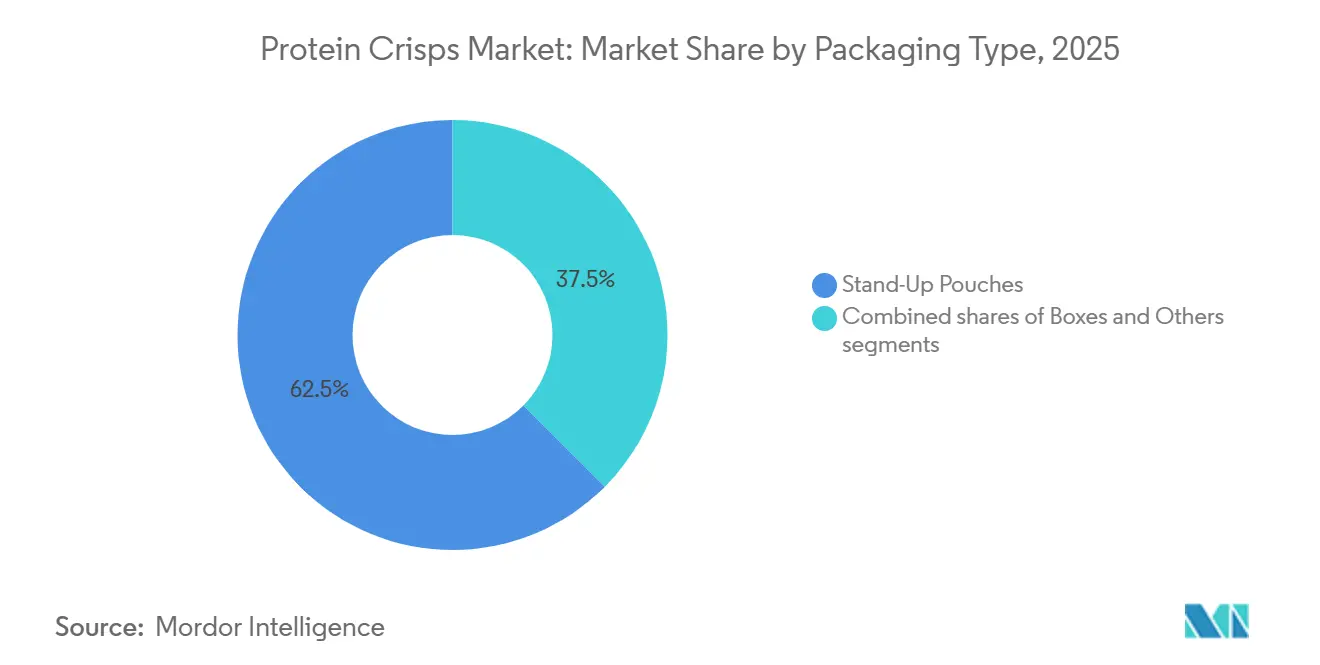

- By packaging, stand-up pouches dominated with 62.54% in 2025 and boxes exhibit the fastest growth at a 10.04% CAGR over the forecast horizon.

- By distribution channel, supermarkets and hypermarkets retained 50.05% share in 2025, but online retail is projected to climb at a 9.45% CAGR through 2031.

- Geographically, North America represented 35.07% of global revenue in 2025, whereas Asia-Pacific is poised to post the highest regional CAGR at 9.05% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Protein Crisps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for High-Protein Convenient Snacks | +1.8% | Global, peak in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rising Popularity of Plant-Based Proteins | +1.5% | North America, Europe, Australia; emerging in China and India | Long term (≥ 4 years) |

| Fitness and Lifestyle Trends Among Millennials and Gen Z | +1.2% | Global, led by North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of Retail and E-Commerce Channels | +1.0% | Global, strongest in North America, China, Southeast Asia | Short term (≤ 2 years) |

| Upcycling of Food-Industry By-Products | +0.6% | North America and Europe; pilots in Asia-Pacific | Long term (≥ 4 years) |

| Integration of Extrusion 4.0 | +0.5% | North America and Europe; adoption spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Protein Convenient Snacks

Snack foods now routinely feature 10-20 g of protein per serving, a standard expectation among mainstream shoppers. The 2025-2030 Dietary Guidelines for Americans advocate for increased protein consumption. Notably, 12% of U.S. adults on GLP-1 medication are gravitating towards protein-rich options that boost feelings of fullness. This shift highlights the growing consumer focus on functional benefits in everyday food choices. As a result, brands are innovating to meet these evolving preferences with products that combine convenience and nutrition. In response, PepsiCo launched Doritos Protein in 2026, aiming to capture this demand for protein-dense snacks. Additionally, the introduction of “better-for-you” end-caps in convenience stores reflects a broader industry effort to align with health-conscious consumer trends. Furthermore, convenience-store chains are introducing dedicated “better-for-you” end-caps, underscoring a sustained demand rather than a fleeting trend.

Rising popularity of plant-based proteins

Global revenue sees a boost from plant-based crisps, thanks to their allergy-friendly appeal and sustainability claims. By 2026, pea protein isolate is projected to command prices between USD 4.00 and 5.50 per kg. Notably, non-GMO variants are expected to fetch a premium of 15-20%. In contrast, soy isolate prices hover between USD 2,800 and 4,200 per metric ton, presenting a challenge for formulators to strike a balance between cost and flavor. The rising demand for plant-based ingredients is driven by increasing consumer awareness of health and environmental benefits.U.S. consumers, as reported by the International Food Information Council (IFIC), frequently chose food and beverages based on label claims: 40% opted for 'natural', 30% for 'organic', 29% for 'locally sourced and clean ingredients', and 28% for 'non-GMO'[2]Source: International Food Information Council (IFIC), "Consumer Food and Beverage Purchasing Behavior Based on Product Labels", ific.org. Additionally, manufacturers are investing in innovative formulations to enhance taste and texture, further fueling market growth. Meanwhile, hybrid blends that combine dairy with plant inputs are broadening their audience reach without complicating production lines.

Fitness and lifestyle trends among millennials and Gen Z

Half of Gen Z snackers prioritize high protein as their top nutrient. Glanbia's "Optimum Advantage" campaign, set for 2026 and featuring Formula 1 champion Lando Norris, brings performance nutrition imagery into the mainstream. Fifty percent of Gen Z respondents ranked high protein as the most important nutrient in snack selection in 2024, surpassing fiber, vitamins, and low sugar[3]Source: international Food Information Council (IFIC), "2024 Food and Health Survey", ific.org. By co-branding with iconic confectionery flavors, Glanbia effectively lowers trial barriers and broadens household penetration. This strategy not only addresses the rising preference for functional and convenient nutrition but also positions the brand as a leader in the high-protein snack market. Additionally, the campaign highlights the growing trend of blending indulgence with health benefits, appealing to a wider consumer base. The use of a high-profile athlete like Norris also reinforces the brand's association with performance and aspirational lifestyles. By leveraging Norris's global fanbase, the campaign is likely to enhance consumer engagement and drive brand loyalty. Furthermore, the inclusion of familiar confectionery flavors ensures accessibility, making the product more appealing to first-time buyers.

Expansion of retail and e-commerce distribution channels

Direct-to-consumer brands account for about 40% of global protein snack sales, benefiting significantly from subscription bundles and auto-replenishment. These brands have disrupted traditional retail models by offering convenience and personalized experiences to consumers. Their innovative strategies, such as leveraging e-commerce platforms and data-driven insights, have allowed them to capture a significant share of the market. In Q1 2026, THG's Myprotein saw a remarkable 200% year-on-year surge in units sold and has made its way into 1,200 Kroger stores, highlighting the trend of digital success translating into physical retail presence. This expansion into Kroger stores demonstrates how direct-to-consumer brands are increasingly bridging the gap between online and offline channels. Additionally, it reflects the growing consumer demand for protein snacks and the ability of such brands to adapt to evolving retail landscapes by securing partnerships with major retailers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenges in Taste and Texture Optimization | -0.9% | Global; most acute in North America and Europe | Short term (≤ 2 years) |

| Intense Competition from Alternative Protein Snacks | -0.7% | Global; led by North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Volatility in Specialty Isolate Tolling Capacity | -0.5% | Global; supply clusters in China, U.S., Europe | Short term (≤ 2 years) |

| Emerging Clean-Label Rules Limiting Binding-Agent Use | -0.4% | North America, Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Challenges in taste and texture optimization

High protein levels draw moisture from starch, limiting puffiness and resulting in dense, gritty textures. While plant isolates can impart bitterness, formulators turn to flavor-masking systems and micro-particle milling to cater to mainstream tastes. This approach ensures that the final product aligns with consumer expectations for taste and texture. Additionally, advancements in ingredient processing techniques are helping to minimize sensory challenges. By addressing these issues, brands can create products that not only meet functional requirements but also deliver a pleasant eating experience. Successfully overcoming these sensory barriers will enable brands to capture a larger share of the growing plant-based market. Furthermore, the ability to innovate in this space will differentiate brands in an increasingly competitive landscape. As consumer demand for plant-based options continues to rise, solving these sensory challenges will be critical for long-term success. Brands that bridge this sensory divide stand poised for expansion in supermarket center aisles.

Intense competition from alternative protein snacks

Bars, jerky, roasted chickpeas, and ready-to-drink (RTD) shakes vie for the same consumption moments, making it easier for consumers to switch between them and putting pressure on shelf space. This overlap in consumption occasions intensifies competition among these products, compelling brands to innovate and differentiate. Furthermore, the growing consumer demand for convenient and protein-rich snacks has expanded the market, increasing the need for brands to cater to diverse preferences. Additionally, the limited shelf space in retail outlets forces companies to strategically position their products to capture consumer attention. Major players like Ferrero, with its 2025 acquisition of Power Crunch, and Mars, which bought Kevin's Natural Foods in 2024, are diversifying their bets across various formats, rather than focusing exclusively on crisps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Source: Hybrids Outpace Single-Source Formulations

In 2025, plant-based variants dominate the protein crisps market, capturing 55.34% of total revenue. This leadership stems from a robust consumer appetite for sustainable, vegan, and allergen-friendly protein options. These offerings resonate with the clean-label movement and the growing trend of moving away from animal-derived ingredients. Furthermore, plant-based crisps enjoy widespread retail endorsement and a broadening product range in global markets. Even with rising competition from new formats, plant-based crisps maintain their lead, bolstered by a strong emphasis on health and sustainability.

Hybrid protein crisps are emerging as the market's fastest-growing segment, with projections indicating a CAGR of 9.82% during the forecast period. These hybrids meld the complete amino acid profile and neutral flavor of whey with the eco-friendly benefits of plant proteins like pea and soy. Their growth trajectory is buoyed by heightened production capabilities, notably in whey fractionation and surging investments in plant protein isolates, especially in North America and Asia. Brands report that hybrid SKUs enjoy a sales velocity that's approximately 17% higher than their single-source counterparts, a trend especially pronounced in club store channels. This momentum positions hybrids as a favored choice, bolstered by regulatory leniency, shifting consumer tastes, and a more pragmatic approach to protein sourcing.

By Category: Organic Captures Premium Shelf Real Estate

In 2025, conventional protein crisps are set to command a dominant 80.34% share of total sales. Their market leadership stems from lower production costs, widespread availability, and deep penetration in mass retail channels. These crisps cater to price-sensitive consumers, bolstered by established supply chains and scalable manufacturing. Moreover, conventional SKUs enjoy a robust foothold in both gym and mainstream snack segments, where affordability and accessibility reign supreme. While there's a burgeoning interest in premium alternatives, conventional crisps remain the bedrock of the market's overall volume.

Organic protein crisps are emerging as the market's fastest-growing segment, with projections of a 10.32% CAGR, outpacing the broader market by a notable margin. This growth surge is fueled by a rising consumer inclination towards clean-label, non-GMO, and pesticide-free products, especially in North America and Europe. Despite the 15–20% uptick in input costs due to organic certification, brands successfully leverage this to secure retail price premiums of 25–30%. With projections indicating the segment will eclipse USD 500 million by 2031, it's bolstered by stringent regulations like the EU Regulation COM(2025)780, which tightens labeling standards. Brands are also enhancing in-store visibility and diversifying their portfolios, allowing them to appeal to both value-driven and premium consumers.

By Flavor: Neutral Base Expands B2B Integrations

In 2025, seasoned protein crisps command a dominant 85.33% share of the market. Their popularity stems from consumer affinity for bold flavors like barbecue, ranch, and nacho. These flavors not only enjoy heightened visibility in retail snack aisles but also benefit from impulse buys. The strong appeal of these seasoned variants is further reinforced by their ability to cater to diverse consumer palates, offering a sense of familiarity and indulgence. Their established profiles foster brand loyalty and repeat purchases, even in competitive landscapes. Additionally, the widespread availability of seasoned crisps across various retail channels, including supermarkets, convenience stores, and online platforms, ensures consistent consumer access. Consequently, seasoned crisps remain a staple in the consumer snack segment, anchoring demand and driving growth.

Unflavored protein crisps are emerging as the fastest-growing segment, with projections indicating a CAGR of 8.77% during the forecast period. This surge is largely attributed to food manufacturers' increasing appetite for neutral inclusions, especially in protein bars, cereals, and meal replacements. Such a trend underscores the evolving role of protein crisps, transitioning from mere snacks to essential ingredients. Moreover, with advancements in flavor technology and strategic acquisitions like Glanbia’s takeover of Flavor Producers, customization capabilities for both flavored and neutral formats are on the rise. This momentum is propelling unflavored crisps into new B2B revenue streams, expanding the market's horizons.

By Packaging Type: Boxes Meet Retail Logistics Mandates

In 2025, stand-up pouches will dominate the protein crisps market, capturing 62.54% of the total share. Their lead stems from features like resealability and lightweight design, making them ideal for e-commerce. These attributes not only enhance consumer convenience but also reduce shipping costs, as their lightweight nature minimizes transportation expenses. Additionally, their compact design optimizes storage space, benefiting both manufacturers and retailers. Beyond convenience, these pouches streamline logistics and storage, appealing to both manufacturers and retailers. Their widespread acceptance across snack categories solidifies their market stance. Yet, concerns over the sustainability of multi-layer materials pose challenges, especially in markets with stringent environmental regulations. Manufacturers are increasingly exploring recyclable or biodegradable alternatives to address these concerns and maintain their competitive edge in environmentally conscious markets.

Boxes are rapidly emerging as the packaging segment with the highest growth rate, forecasted to surge at a CAGR of 10.04%. Their ascent is bolstered by benefits like stackability and enhanced shelf organization, resonating with retailer planogram strategies. Boxed multipacks are finding favor in office pantries and foodservice channels, broadening their consumption occasions. Regions like Europe are tightening regulations, imposing extended producer responsibility fees on non-recyclable materials. This push is steering the industry towards paper-based packaging. Consequently, boxes are rising as a sustainable, retail-friendly choice, all while maintaining healthy profit margins.

By Distribution Channel: Digital-First Brands Convert to Omnipresence

In 2025, supermarkets are set to dominate the protein crisps market, raking in nearly half of the total revenue. Their stronghold is bolstered by high foot traffic, prominent product visibility, and ingrained consumer buying habits. Supermarkets not only offer brands a robust shelf presence but also grant them access to a diverse customer base across various regions. Furthermore, these outlets leverage well-established supply chains and promotional strategies, driving significant volume sales. Even with rising competition from alternative channels, supermarkets steadfastly anchor the market's distribution landscape.

Online retail is emerging as the fastest-growing channel, with projections indicating a CAGR of 9.45% during the forecast period. This surge is largely attributed to direct-to-consumer models. Notably, subscription services boast impressive repeat purchase rates of 60–70%, which in turn slashes long-term customer acquisition costs. Moreover, a robust digital presence amplifies a brand's negotiating power with traditional retailers. This is exemplified by the swift offline expansions of brands like Myprotein into major chains such as Kroger and Tesco. E-commerce not only facilitates targeted marketing and a wider reach but also accelerates product adoption cycles. Consequently, online channels are evolving into a pivotal growth engine, working in tandem with traditional retail and redefining distribution strategies.

Geography Analysis

In 2025, North America is projected to account for 35.07% of the turnover, bolstered by established sports-nutrition channels and widespread supermarket reach. The launch of Doritos Protein by PepsiCo highlights a shift towards mainstream acceptance, while Glanbia's expansion in Idaho signals a strong belief in the ongoing demand for ingredients. Retail sales of plant-based snacks in Canada reached CAD 269.4 million in 2024 (equivalent to USD 200 million), pointing to a promising future for flexitarian products.

Asia-Pacific is emerging as the fastest-growing region, with a projected CAGR of 9.05%. Urban consumers in China, India, and Southeast Asia are gravitating towards Western-style high-protein snacks. However, local flavor adaptations, such as chili-lime or masala, are proving essential. South Korea showcases the success of single-serve, on-the-go snacks, while pricing trends of soy isolates in China are shaping global cost structures. In Southeast Asia, where price sensitivity is paramount, local co-manufacturing partnerships are proving beneficial by reducing tariffs and expediting replenishment cycles.

Europe finds itself at a crossroads of opportunity and regulatory challenges. The EU's stringent organic regulations, emphasizing traceability, are raising compliance costs. Yet, these regulations also enable premium pricing in markets like Germany, France, and the Netherlands. The U.K. stands out as a hub for flavor innovation, with "protein aisles" in retailers enhancing product visibility. Meanwhile, regions like South America and the Middle East and Africa are witnessing growth, driven by urbanization and heightened health consciousness. However, challenges like currency fluctuations and logistical issues are moderating the pace of expansion.

Competitive Landscape

The Market exhibits moderate consolidation, leaving headroom for challenger brands. Legacy confectioners, like Ferrero and Mars, are pivoting: Ferrero's 2025 acquisition of Power Crunch and Mars' 2024 buyout of Kevin's Natural Foods signal a shift towards protein-forward assets, countering traditional sugar declines. This strategic move highlights their efforts to diversify portfolios and align with evolving consumer preferences for healthier, protein-rich options. Glanbia ensures supply security through vertical integration, moving seamlessly from ingredient isolation to finished snacks, which not only strengthens its supply chain but also enhances operational efficiency. Meanwhile, THG capitalizes on its digital-first approach, leveraging e-commerce platforms to reach a broader audience and adapt quickly to market trends.

Technology emerges as a key differentiator. Firms adopting Extrusion 4.0 technology slash research and development lead times by 30-40%, enabling faster product innovation and reducing time-to-market. Additionally, this technology supports the production of smaller, yet profitable, batch sizes, catering to niche consumer demands. The ability to upcycle not only enhances ESG narratives by promoting sustainability but also offers potential margin boosts, helping companies balance profitability with environmental responsibility. Investors are backing omnichannel newcomers: Wilde Brands' Series C funding fuels flavor research and development and a rollout in Costco, underscoring confidence in niche scalability within the expansive protein crisps market. This funding also reflects the growing interest in brands that can effectively combine innovation with scalability.

As bars, jerky, and ready-to-drink shakes vie for prime shelf space, competitive pressures mount. Brands adept in both e-commerce strategies and traditional merchandising stand to gain, as mastering these channels ensures visibility and accessibility to a diverse consumer base. By securing multi-year contracts for isolates, companies can stabilize raw material costs, while exploring hybrid protein recipes allows them to innovate and cater to varied dietary preferences. These strategies help mitigate input volatility, safeguarding their gross margins as the protein crisps market evolves and matures.

Protein Crisps Industry Leaders

-

The Simply Good Foods Company

-

PepsiCo

-

General Mills Inc.

-

1440 Foods (Pure Protein)

-

THG PLC (Myprotein)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Quaker has unveiled its latest rice crisps, boasting 6 grams of protein and 9 grams of whole grains in each serving. These crisps are designed to cater to health-conscious consumers seeking nutritious snack options. They are available in two enticing flavors: chocolate caramel, which offers a sweet and indulgent taste, and tangy barbecue, providing a savory and bold flavor profile.

- January 2026: Optimum Nutrition launched "The Optimum Advantage," a global campaign featuring elite athletes, as part of its product launch to enhance the desirability of protein snacking. The campaign aims to highlight the benefits of protein-rich snacks while leveraging the credibility and influence of renowned athletes to connect with health-conscious consumers worldwide.

- January 2026: PepsiCo launched Doritos Protein, packing 10g of protein per ounce, catering to flavor-focused consumers prioritizing functional macros. This product aligns with the growing demand for snacks that combine taste with nutritional benefits.

Global Protein Crisps Market Report Scope

Protein crisps, crafted from protein-rich sources, offer a crunchy snack experience, boasting both a high-protein profile and a delightful crisp texture. Based on the protein source, the market is segmented into dairy-based protein crisps, plant-based protein crisps, and hybrid/other protein crisps. By category, the market is segmented into organic and conventional. Based on the flavor, the market is segmented into flavored and unflavored. By Packaging type, the market is segmented into stand-up pouches, boxes, and others. By Distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The report also offers a detailed analysis on major economies across North America, Europe, Asia-Pacific, South America and Middle East, and Africa regions.

| Dairy-Based Protein Crisps |

| Plant-Based Protein Crisps |

| Hybrid/Other Protein Crisps |

| Organic |

| Conventional |

| Flavored |

| Unflavored |

| Stand-Up Pouches |

| Boxes |

| Others |

| Supermarkets/Hypermarkets |

| Convinience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Protein Source | Dairy-Based Protein Crisps | |

| Plant-Based Protein Crisps | ||

| Hybrid/Other Protein Crisps | ||

| By Category | Organic | |

| Conventional | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | Stand-Up Pouches | |

| Boxes | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convinience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the protein crisps market?

The global protein crisps market size reached USD 1.66 billion in 2026 and is projected to hit USD 2.47 billion by 2031, growing at an 8.31% CAGR

Which protein source is gaining the most share?

Hybrid formulations that combine dairy and plant proteins are expanding at the fastest 9.82% CAGR, bridging taste and sustainability gaps

How fast is online retail growing for protein crisps?

Online retail is expected to post a 9.45% CAGR through 2031 as direct-to-consumer subscriptions and omnichannel launches accelerate

Which region will contribute the highest incremental revenue?

Asia-Pacific will deliver the largest incremental gains, advancing at a 9.05% CAGR on the back of urbanization and rising health awareness

Page last updated on: