High Protein Bakery Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

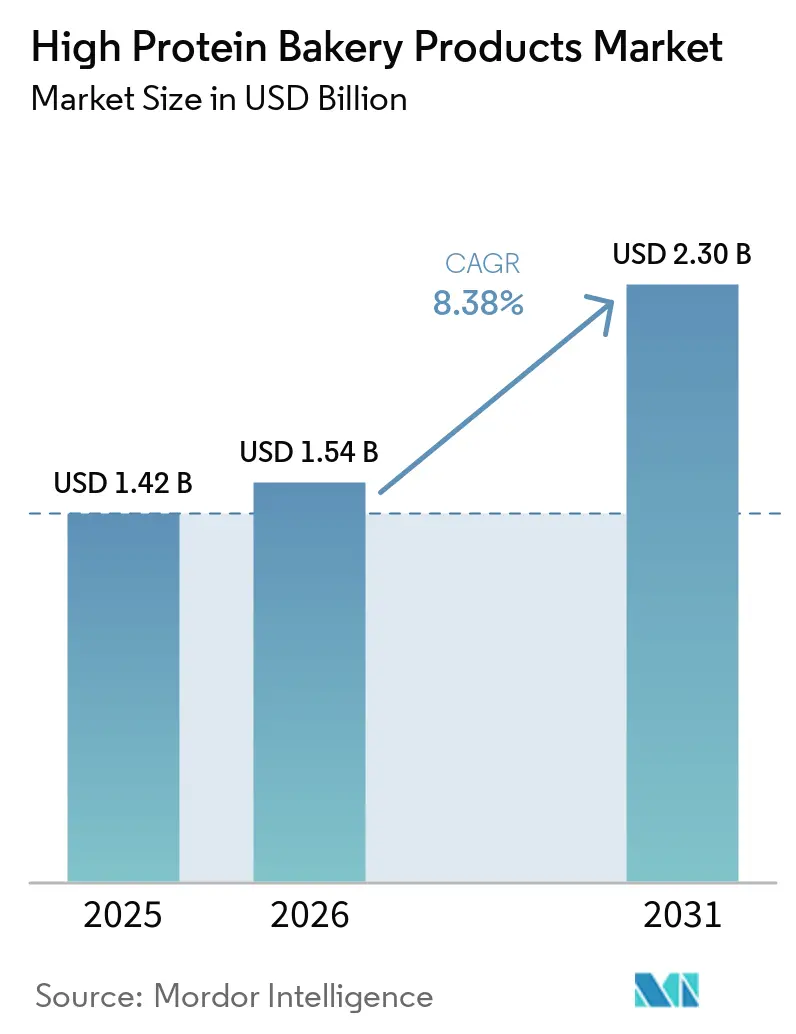

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 2.30 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Protein Bakery Products Market Analysis by Mordor Intelligence

The high protein bakery products market size was valued at USD 1.42 billion in 2025 and estimated to grow from USD 1.54 billion in 2026 to reach USD 2.30 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031). The high-protein bakery products market is expanding because protein fortification is no longer limited to sports nutrition shelves, and it is now treated as a core value cue in mainstream bread, cookies, and breakfast bakery products. AMF Bakery Systems stated in 2026 that 67% of consumers choose food based on health benefits, and it also identified protein as the most sought-after attribute in better-for-you bakery products, which helps explain why protein claims are moving closer to a baseline requirement in the category. The high-protein bakery products market is also benefiting from stronger demand for satiety-led and weight-management-oriented foods, which is pushing bakery makers to treat protein as a daily nutrition feature rather than an occasional indulgence. Regulatory support is also improving the backdrop for reformulation, as the FDA’s updated healthy nutrient content claim has increased the incentive to add more protein, fiber, and whole grains to bakery products, aiming for stronger health positioning. The high-protein bakery products market is creating space for both branded bakers and ingredient suppliers, as newer protein systems from companies such as Burcon and Glanbia are expanding formulation options, even as cost pressure and texture performance remain the main barriers to faster adoption.

Key Report Takeaways

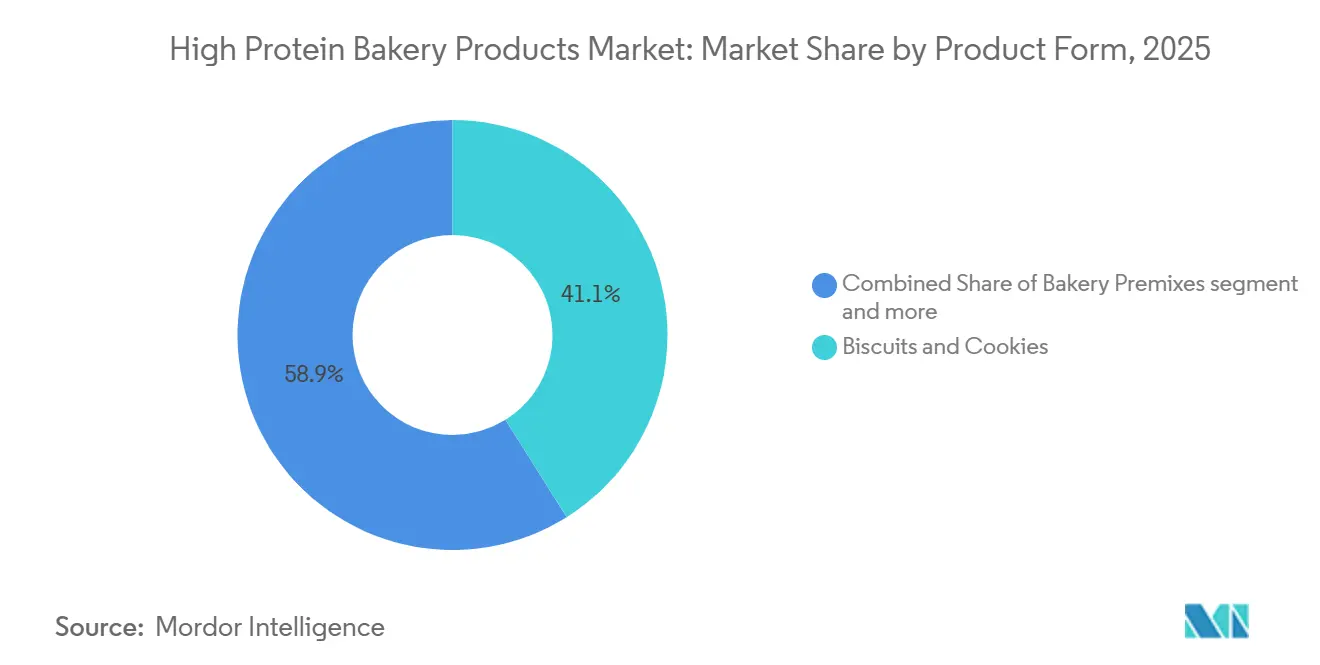

- By product form, cookies and biscuits accounted for 41.09% of the high protein bakery products market size in 2025, while bakery premixes are projected to grow at a 9.58% CAGR through 2031.

- By protein source, animal-derived proteins held 57.96% of the high-protein bakery products market share in 2025, while plant-derived proteins are expected to grow at a 10.74% CAGR through 2031.

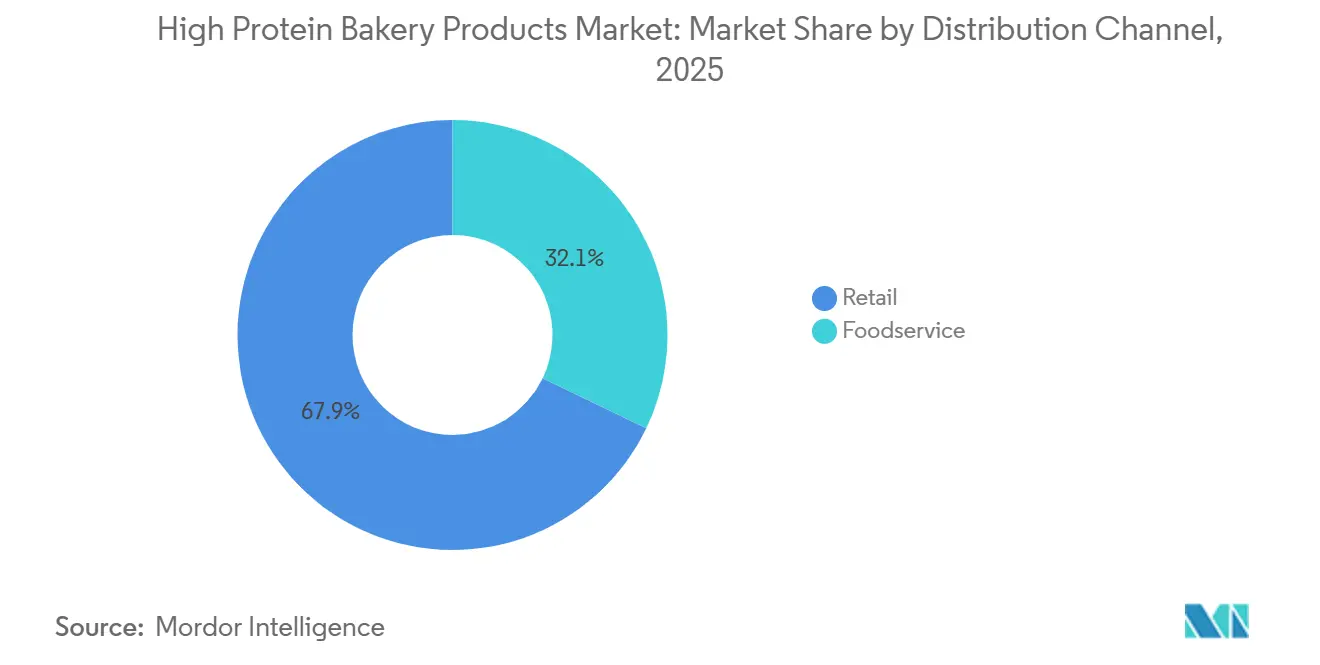

- By distribution channel, retail accounted for 67.87% of revenue in 2025, while foodservice is expected to grow at a 11.38% CAGR over 2026-2031.

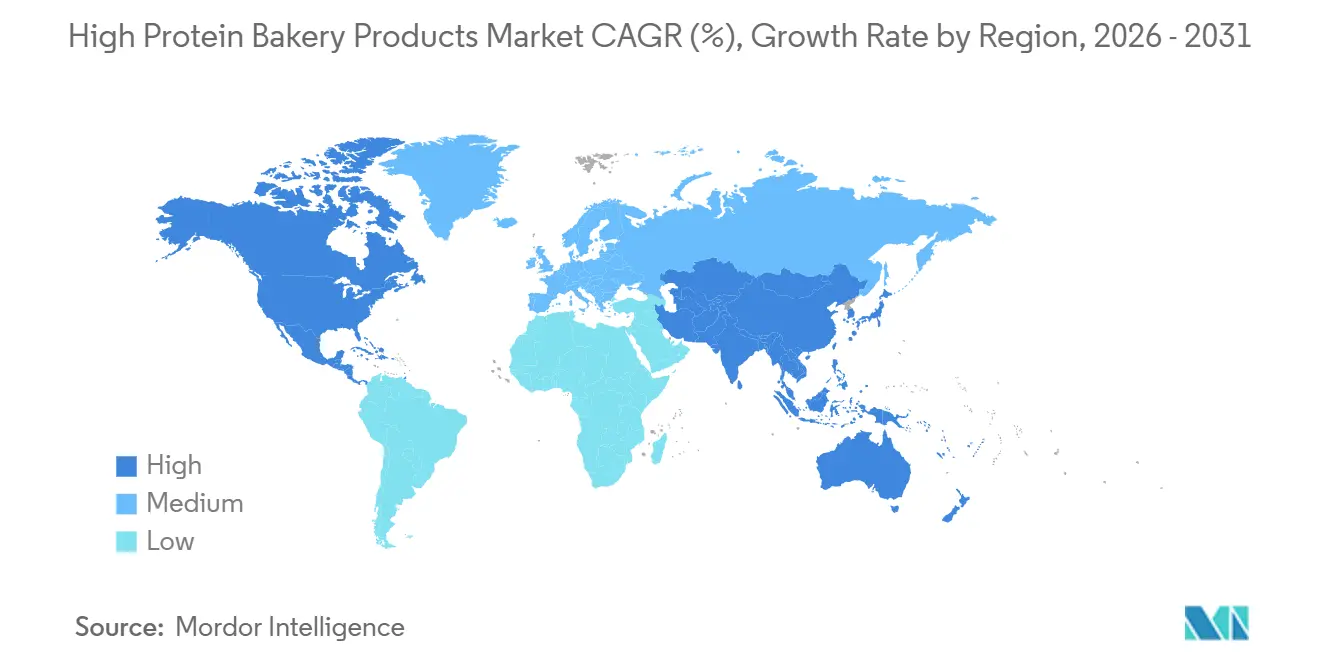

- By geography, North America held 34.64% share in 2025, while Asia-Pacific is set to grow at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Protein Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference For Protein-Enriched Diets | +2.0% | Global | Short term (≤ 2 years) |

| Product Innovation Using Whey, Soy, Pea, Wheat, Chickpea, And Fava Bean Proteins | +1.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing Demand From Cafés, QSRs, and Foodservice Chains For High-Protein Buns and Bread Bases | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Rising Demand For Weight Management and Satiety-Focused Bakery Products | +1.5% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Increasing Launch Of Clean-Label and Functional Bakery Products by Food Manufacturers | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Advances In Functional Wheat Protein Isolates Enable Scale | +0.8% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for protein-enriched diets

Nearly 3 in 10 US shoppers actively check packaging for protein content as of 2026, with online searches for "protein bread" and "high protein dessert" forecast to grow 17% through the year, according to AMF Bakery Systems' 2026 industry report[1]Source: AMF Bakery Systems, “The Bakery Trends That Will Define 2026,” AMF Bakery, amfbakery.com. The demographic profile of the protein bakery consumer has broadened materially, with consumers aged 15-29 as the strongest growth cohort, while GLP-1 medication users represent a high-value segment that specifically requires nutrient-dense bakery formats to protect muscle mass during medically induced caloric restriction. A structural shift with long-term implications is that protein content is functioning as a proxy for ingredient quality in consumers' minds: buyers of high-protein bakery are increasingly correlating protein grams with cleaner formulations, a second-order dynamic that expands the addressable market beyond dedicated fitness users into general wellness purchasers. Glanbia Nutritionals' 2026 bakery trends research confirms that protein is the most sought-after attribute in better-for-you sweet snacking and bakery, outranking fiber and reduced sugar as a purchase driver. Products without a credible protein claim are losing shelf space in health-focused retail channels, regardless of flavor quality.

Product innovation using whey, soy, pea, wheat, chickpea, and fava bean proteins

The diversity of commercially viable protein platforms is shifting competitive strategy from formulation capability toward ingredient sourcing networks. Burcon NutraScience commercially launched FavaPro™, a 90%+ purity fava protein isolate, in August 2025, adding a near-neutral-flavored option to a category long dominated by pea and soy proteins with documented off-note challenges[2]Source: Burcon NutraScience Corporation, “Burcon Achieves First Commercial Production of Fava Protein and Officially Launches FavaPro,” Burcon NutraScience Corporation, burcon.ca. AB Mauri and Nutris entered a technical and supply agreement in 2025 specifically targeting fava bean applications for industrial bakery in the UK and Ireland, with pilot trials scheduled across bread, morning goods, and snack formats throughout the year. Lasenor's VP-100 texturizing pea protein, co-developed with Meala FoodTech and launched at Fi Europe 2025, achieves 50–100% egg reduction in muffins while maintaining structural performance, a dual benefit that gains particular relevance given the 180%+ rise in US egg prices since early 2024 caused by avian influenza. Chickpea protein is emerging as a lower-allergen, clean-label alternative with US growth forecasts in the high-single to low-double-digit range, while pea protein retains the broadest application versatility given strong supply pipelines, including into China.

Growing demand from cafés, QSRs, and foodservice chains for high-protein buns and bread bases

QSR operators are incorporating high-protein baked bases as a menu-differentiation lever, not merely as a health statement. McDonald's India (operated by Westlife Foodworld) launched a "Protein Plus Range" in collaboration with CSIR-CFTRI, including a plant-based Protein Slice that allows customers to add 5 grams of protein to any burger, and a modular customization format that shifts protein delivery from the bun itself to a configurable element. In Australia, Daniel's Donuts launched a 30-gram protein beef and cheese pie for the 2025 footy season, validating that protein-fortified pastry is transitioning from gym-adjacent specialty to core QSR menu item. Grupo Bimbo's QSR business unit within its Europe, Asia, and Africa segment recorded double-digit net sales growth in full-year 2025, driven in part by protein-enhanced bread supply contracts across the region, per the company's Q4 2025 earnings release. The structural implication is that foodservice procurement standards are setting upstream formulation requirements: suppliers targeting QSR contracts must simultaneously hit protein thresholds, texture consistency specifications, and clean-label ingredient lists, raising the effective barrier to entry for all market participants. Circana data cited in QSR Media Australia identifies high-protein, low-calorie, and portion-controlled options as the primary innovation opportunities in the foodservice industry, with GLP-1-driven consumption habit changes amplifying this directional pull.

Rising demand for weight management and satiety-focused bakery products

Ardent Mills' consumer research positions "benefit-stacking", combining fiber, plant protein, and whole grains, as the primary formulation strategy to capture GLP-1-influenced consumers, noting that these users specifically prioritize satiety, muscle maintenance, and digestive health with formulation implications that are consistent across life stages and demographics. GLP-1 adoption is likely to lead to "increased demand for high-protein, high-fiber, and nutrient-dense, portion-controlled options and greater scrutiny of ingredient formulations in food and drinks", a behavioral profile that aligns closely with the high-protein bakery products segment's core proposition. Flowers Foods' CEO framed protein bread and buns as one of the most important drivers of future growth in the company's 2025 earnings commentary, confirming this consumer behavior shift is being explicitly translated into corporate revenue strategy. A less-discussed opportunity is the portion-control sub-format, half loaves and individually wrapped high-protein items, which are growing disproportionately fast as GLP-1 users eat less per sitting but more frequently, a consumption pattern that standard shelf-space metrics have not yet fully captured.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Protein Ingredients Increasing Final Product Prices | -1.2% | Global | Short term (≤ 2 years) |

| Sensory Challenges Such As Dryness, Bitterness, Graininess, And Dense Texture | -0.8% | Global | Medium term (2-4 years) |

| Higher Processing Complexity And Need For Specialized Bakery Formulation Expertise | -0.6% | APAC, MEA, South America | Medium term (2-4 years) |

| Regulatory Differences In Protein Claims, Health Claims, And Labeling Across Regions | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sensory challenges such as dryness, bitterness, graininess, and dense texture

Persistent sensory performance gaps remain the most consequential technical barrier to mainstream category penetration. Springer Nature's 2025 peer-reviewed analysis in Food and Bioprocess Technology identified bitterness, astringency, and dryness as the primary off-note mechanisms in plant protein systems, with polyphenols and tannins binding salivary proteins to produce mouth-drying effects and lingering off-flavors that directly impact consumer reacceptance rates. Glanbia Nutritionals' own consumer data indicates that 52% of US consumers report dissatisfaction with the texture of sweet protein snacks, characterizing them as grainy or hard, a finding that informs its OvenPro® functional bakery solution, which demonstrated textural parity with non-fortified controls across firmness, gumminess, and chewiness metrics in muffin trials. A study published in Applied Sciences (Multidisciplinary Digital Publishing Institute (MPDI), 2025) found that pea or rice protein substitution above 10% significantly reduced cookie sensory acceptance, with P15% and R15% formulations receiving substantially lower overall scores than control samples, indicating that loading rate, not protein source alone, determines acceptable ceilings. Sensory failure rates in protein bakery NPD are disproportionately high precisely at the 15g+ per-serving threshold that health-focused consumers now specifically seek, making formulation expertise a genuine competitive moat rather than a replicable commodity capability.

High cost of protein ingredients increasing final product prices

Whey protein isolate pricing climbed from approximately USD 6.70/lb in January 2024 to USD 10.50/lb by September 2025, a 57% increase in 20 months, driven by GLP-1-induced demand growth and US-China trade tariff dislocations that rerouted supply chains and created historically wide bid–ask spreads, according to Glanbia Nutritionals' market update[3]Source: Glanbia Nutritionals, “Top Trends in Bakery for Food and Beverage Manufacturers,” Glanbia Nutritionals, glanbianutrition.com. By early 2026, WPI prices were approaching USD 12.30/lb, with major suppliers sold forward well into the year, leaving smaller bakery manufacturers with limited spot procurement options. Over a two-year period, WPC80 costs jumped approximately 108%, and WPI costs approximately 139%, cost escalations structurally incompatible with the mid-market retail price ceilings at which most packaged high-protein bread products compete. In India, where nearly 90% of whey used by domestic brands is imported predominantly from Europe, a kilogram of whey isolate rose to approximately INR 4,500 (approximately USD 54), with brands anticipating further near-term increases, per a May 2026 Economic Times report. This cost overhang is most acute for products formulated to meet the 10g-per-serving high-protein threshold, since these require higher ingredient loading rates and less flexibility to substitute lower-cost protein concentrates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Cookies and biscuits lead on volume, premixes accelerate on flexibility

Cookies and biscuits accounted for 41.09% of the high-protein bakery products market in 2025, while bakery premixes are projected to grow at a 9.58% CAGR through 2031. The lead position of cookies and biscuits is tied to their dense structure, portion convenience, and longer shelf life, all of which make protein fortification easier than it is in many yeast-leavened formats. The high-protein bakery products market has favored this product form because consumers already accept cookies and biscuits as snack items, making it easier to add protein without changing the usage occasion. Premixes are rising faster because home bakers, cafés, and smaller QSR operators want ready-to-use protein-enhanced flour systems that reduce development time and lower the risk of batch inconsistency. The high protein bakery products market is therefore seeing a clear split between high-volume finished goods and high-growth formulation platforms. That split reflects how demand is broadening across both branded retail products and business-to-business baking inputs.

Bread and rolls remain central to the high-protein bakery products market because they are still the most visible daily-use bakery format in many countries, even though fortification is more difficult than in low-moisture products. Flowers Foods used its 2025 product pipeline to push higher-protein offerings under Nature’s Own, showing that mainstream bread brands now see protein as a direct route to defend premium shelf space and capture nutrition-led households. Bimbo Bakeries USA also launched Thomas’ High Protein Bagels nationwide in October 2025 with 21g of protein per bagel, which shows how heritage bakery brands are adapting familiar carriers instead of relying only on entirely new products. Morning goods, including waffles, pancake mixes, and muffins, are also gaining attention because breakfast is a natural setting for protein intake and portion-managed eating. The high protein bakery products market continues to reward product forms that can hold texture, flavor, and shelf stability together, and a 2025 scientific review reinforced that each bakery format needs its own protein strategy rather than a single formula applied across the category.

By Protein Source: Animal proteins anchor revenue, plant proteins lead innovation

Plant-derived proteins are forecast to grow at a 10.74% CAGR from 2026 to 2031, which makes them the fastest-growing source in the high-protein bakery products market. This growth reflects rising demand for cleaner labels, broader allergen management, and less dependence on dairy-heavy cost structures. The high-protein bakery products market is also benefiting from improved ingredient performance, as newer plant-based proteins, such as fava, pea, chickpea, and wheat, are giving formulators more flexibility to balance flavor neutrality and dough functionality. Burcon’s commercial launch of FavaPro in August 2025 is one example of how the plant-protein base is expanding, with more bakery-relevant options. The high-protein bakery products market is seeing plant proteins move from a niche substitution role to a more active growth engine that can support both retail and foodservice product development.

Animal-derived proteins still held 57.96% of the high-protein bakery products market share in 2025, which shows that whey, milk protein concentrate, and egg white remain important for functionality, familiarity, and strong protein quality. The American Society of Baking has noted that protein claims must reflect the FDA’s PDCAAS-corrected value under 21 CFR 101.9(c)(7)(ii), which is one reason animal proteins continue to hold a practical advantage in many commercial bakery formulations. The high protein bakery products market is not moving away from animal proteins all at once, because those proteins still perform well in dough systems and are easier to use when a product must hit clear on-pack protein thresholds. At the same time, Glanbia’s bakery-focused work shows why blend systems are gaining value, since manufacturers want to combine the performance of dairy proteins with the cost and label benefits of plant ingredients. The high protein bakery products market will likely keep both source groups relevant, but future share shifts will depend on whether plant systems can narrow the remaining gap in taste, texture, and claim efficiency.

By Distribution Channel: Retail anchors revenue, foodservice scales through menu integration

Foodservice is expected to grow at an 11.38% CAGR from 2026 to 2031, making it the fastest-growing channel in the high-protein bakery products market. This reflects stronger demand from cafés, QSRs, and contract bakery partners for protein-enriched bread bases, rolls, and related carriers built into standard menu offerings. The high-protein bakery products market benefits from this channel because foodservice can turn a nutritional proposition into a repeat-order cycle rather than a one-time retail trial. Grupo Bimbo’s Europe, Asia, and Africa business reported double-digit QSR sales growth in 2025, which supports the view that commercial demand for protein bakery supply is becoming more established across markets. The high-protein bakery products market is therefore seeing foodservice as a scale channel for suppliers that can combine nutrition claims with consistent operating performance.

Retail accounted for 67.87% of revenue in 2025, indicating that the high-protein bakery products market still relies heavily on supermarkets and hypermarkets for mass visibility and consumer education. Retail remains the main point where shoppers compare protein grams, price, ingredients, and familiarity across brands, so shelf presence still matters even as online and direct channels grow. The high protein bakery products market also uses retail to test new subformats, including bagels, snack cookies, breakfast items, and premium breads that can justify higher price points through added protein and cleaner labels. Flowers Foods and Bimbo Bakeries USA have both used established retail brands to bring protein-focused bakery products into mainstream aisles, which shows how incumbents are using familiar distribution power to normalize the category. The high protein bakery products market will keep retail in the lead, but channel growth is likely to come faster where foodservice and specialty direct models can shorten the path from product claim to repeat use.

Geography Analysis

North America held 34.64% of the high-protein bakery products market share in 2025, which makes it the largest regional base for the category. The region benefits from a mature health-and-wellness retail system, high familiarity with protein claims, and a strong set of branded bakery companies that can launch at a national scale. The U.S. remains the core demand center in the high-protein bakery products market because large packaged bakery players are now treating protein bread and buns as a meaningful growth lane rather than a side project. Flowers Foods said in 2025 that more than 40% of consumers want to add a good source of protein to their diets, and the company has used that direction to expand better-for-you bakery development across its portfolio. Regulatory support also matters in North America, because the FDA’s updated healthy claim has increased the incentive to build bakery products around stronger nutrient profiles, including higher protein content, where it fits the product.

Europe is the second-largest regional cluster in the high-protein bakery products market, supported by strong clean-label demand and a bakery culture that is open to functional reformulation when taste remains acceptable. Germany stands out as the most important national market in the region, while France, the UK, Italy, and Benelux contribute to demand through premium bread, snack bakery, and health-led retail formats. The regional pattern is shaped by a stronger push toward ingredient transparency, which is helping plant proteins, functional blends, and premium bread concepts gain traction across industrial and artisan-adjacent channels. The high protein bakery products market in Europe is therefore expanding through a mix of nutritional positioning, reformulation pressure, and gradual migration away from traditional high-sugar bakery formats in more regulated retail settings.

Asia-Pacific is forecast to grow at a 9.25% CAGR through 2031, making it the fastest-growing region in the high protein bakery products market. This regional momentum is tied to rising disposable incomes, urban fitness culture, QSR expansion, and growing familiarity with protein as an everyday food attribute across India, China, Japan, and Southeast Asia. Grupo Bimbo reported double-digit growth in India in 2025 within its Europe, Asia, and Africa operations, which supports the view that organized bakery demand is expanding alongside modern retail and foodservice development. South America is anchored by Brazil, where Grupo Bimbo’s acquisition of Wickbold in 2025 strengthened its packaged bakery platform and created a broader base for nutrition-led product rollouts. Middle East and Africa remains the smallest region in the high protein bakery products market, but urbanization, QSR growth, and rising fitness awareness are widening demand for protein-enriched bakery in markets such as Saudi Arabia, the UAE, and South Africa.

Competitive Landscape

The high-protein bakery products market remains moderately fragmented, as large packaged bakers, protein-led specialty brands, and ingredient suppliers compete across different parts of the value chain. Grupo Bimbo is the largest bakery company in the broader sector, and its 2025 results showed a strategy built around nutritional reformulation, QSR expansion, and acquisition-led regional strengthening. The company stated that 98% of its daily consumption portfolio met its Positive Nutrition standard by 2025, which shows how large incumbents are aligning product development with stronger nutrition expectations across the bakery. Flowers Foods is also repositioning around premium health demand, and its 2025 innovation commentary made clear that higher-protein bread is now part of its wider growth agenda across established brands. The high-protein bakery products market, therefore, combines scale players with niche specialists, keeping the competitive field active across both finished goods and supporting ingredients.

Ingredient platforms are increasingly important in the high-protein bakery products market because finished product success depends heavily on how proteins behave in dough, batter, and baked textures. Glanbia Nutritionals has positioned its OvenPro system around bakery fortification that aims to improve texture outcomes, which highlights how ingredient suppliers are becoming strategic partners rather than simple raw material vendors. The American Society of Baking has also emphasized the role of PDCAAS-corrected protein values in label claims, which means compliance knowledge now matters alongside flavor and texture expertise. The high protein bakery products market is rewarding companies that can combine formulation science, regulatory accuracy, and scalable sourcing instead of competing on protein grams alone.

Several recent moves show how competition is evolving in the high protein bakery products market. Grupo Bimbo used acquisitions such as Wickbold in Brazil and Don Don in the Balkans during 2025 to strengthen regional bakery platforms while also expanding its nutrition-oriented operating base. Flowers Foods expanded its product pipeline in 2025 and 2026 around higher-protein and better-for-you bakery offers, which shows how incumbent scale is being applied to a more targeted nutrition message. Burcon’s commercial launch of FavaPro in August 2025 shows that ingredient-side innovation is also shaping the field, because better plant protein options can change who is able to compete in finished bakery products. The high protein bakery products market is likely to remain open to new entrants, but the winners will be the players that manage protein quality, eating experience, pricing discipline, and channel fit at the same time.

High Protein Bakery Products Industry Leaders

Grupo Bimbo

Aryzta AG

Kodiak Cakes

General Mills Inc

Flower Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bimbo Bakeries USA launched Oroweat Protein Breads nationwide, offering 20 grams of complete protein per two slices in Protein White and Protein Honey Oat varieties at a USD 7.69 SRP; the launch marks a direct entry into the functional nutrition bread tier by a mass-market incumbent, intensifying competition against specialist brands.

- February 2026: Kodiak launched No Sugar Added Homestyle Power Waffles with 16 grams of protein and 100% whole grains, available at Target, Kroger, and Walmart, completing an NPD cycle that introduced Overnight Oats (January 2026), frozen breakfast sandwiches (June 2025), and Trail Bars (June 2025) within a nine-month window.

- January 2026: Flowers Foods' Nature's Own brand launched Life Wheat + Protein bread with 22 grams of protein per two-slice serving, a keto-friendly formulation, 9 grams of fiber, and no artificial preservatives or colors, the brand's highest-protein commercial offering and its first explicit protein-quantity leadership product.

- October 2025: Flowers Foods announced Nature's Own Life's higher-protein loaf and Dave's Killer Bread Supreme Sourdough as part of a broader innovation rollout, citing data that more than 40% of consumers want to add a good source of protein to their diet, directly informing the company's portfolio investment priorities.

Global High Protein Bakery Products Market Report Scope

High-protein bakery products are baked goods formulated with elevated protein content by adding animal- or plant-based protein ingredients to support nutritional and functional dietary needs. The high-protein bakery products market is segmented by product form, protein source, distribution channel, and geography. By product form, the market includes bread and rolls, morning goods, cookies and biscuits, bakery premixes, and other high-protein bakery products. Based on protein source, the market is segmented into animal- and plant-derived proteins. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further divided into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Bread and Rolls |

| Morning Goods |

| Cookies and Biscuits |

| Bakery Premixes |

| Other High-Protein Bakery |

| Animal-Derived Proteins |

| Plant-Derived Proteins |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Form | Bread and Rolls | |

| Morning Goods | ||

| Cookies and Biscuits | ||

| Bakery Premixes | ||

| Other High-Protein Bakery | ||

| By Protein Source | Animal-Derived Proteins | |

| Plant-Derived Proteins | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving demand for high protein bakery products in 2026?

Demand is being supported by broader health-focused food choices, stronger interest in satiety-led eating, and a shift toward protein as a core purchase criterion in everyday bakery.

How large is the global high protein bakery products space by 2031?

The high protein bakery products market size is expected to reach USD 2.30 billion by 2031, up from USD 1.54 billion in 2026, at an 8.38% CAGR over 2026-2031.

Which product form leads revenue today?

Cookies and biscuits led with 41.09% share in 2025 because they are easier to fortify, convenient for snacking, and more stable in texture than many bread formats.

Which protein source is growing the fastest?

Plant-derived proteins are projected to grow at a 10.74% CAGR through 2031 as manufacturers look for cleaner labels, lower allergen exposure, and more diversified sourcing.

Page last updated on: