Protein Chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

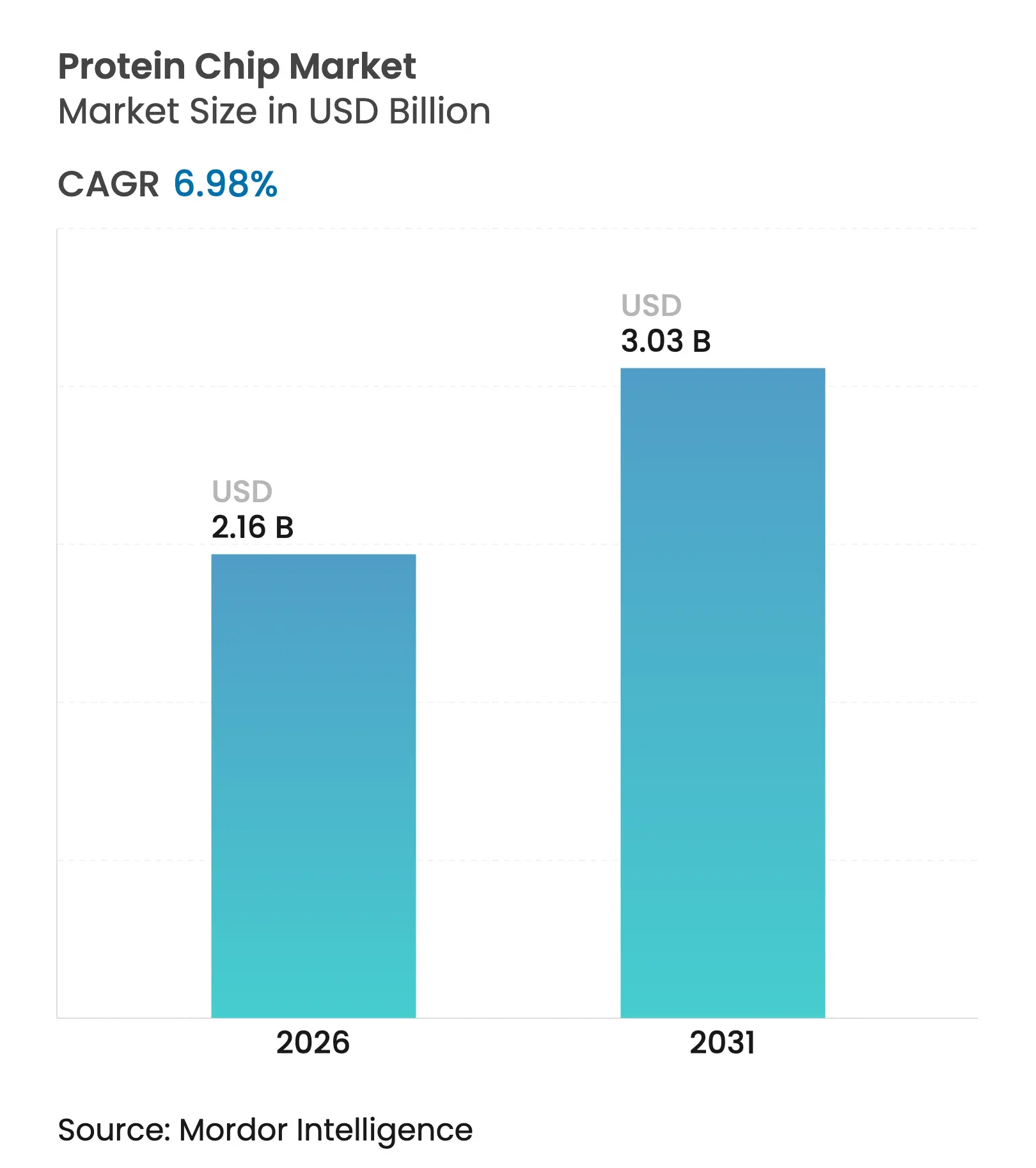

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 6.98 % CAGR |

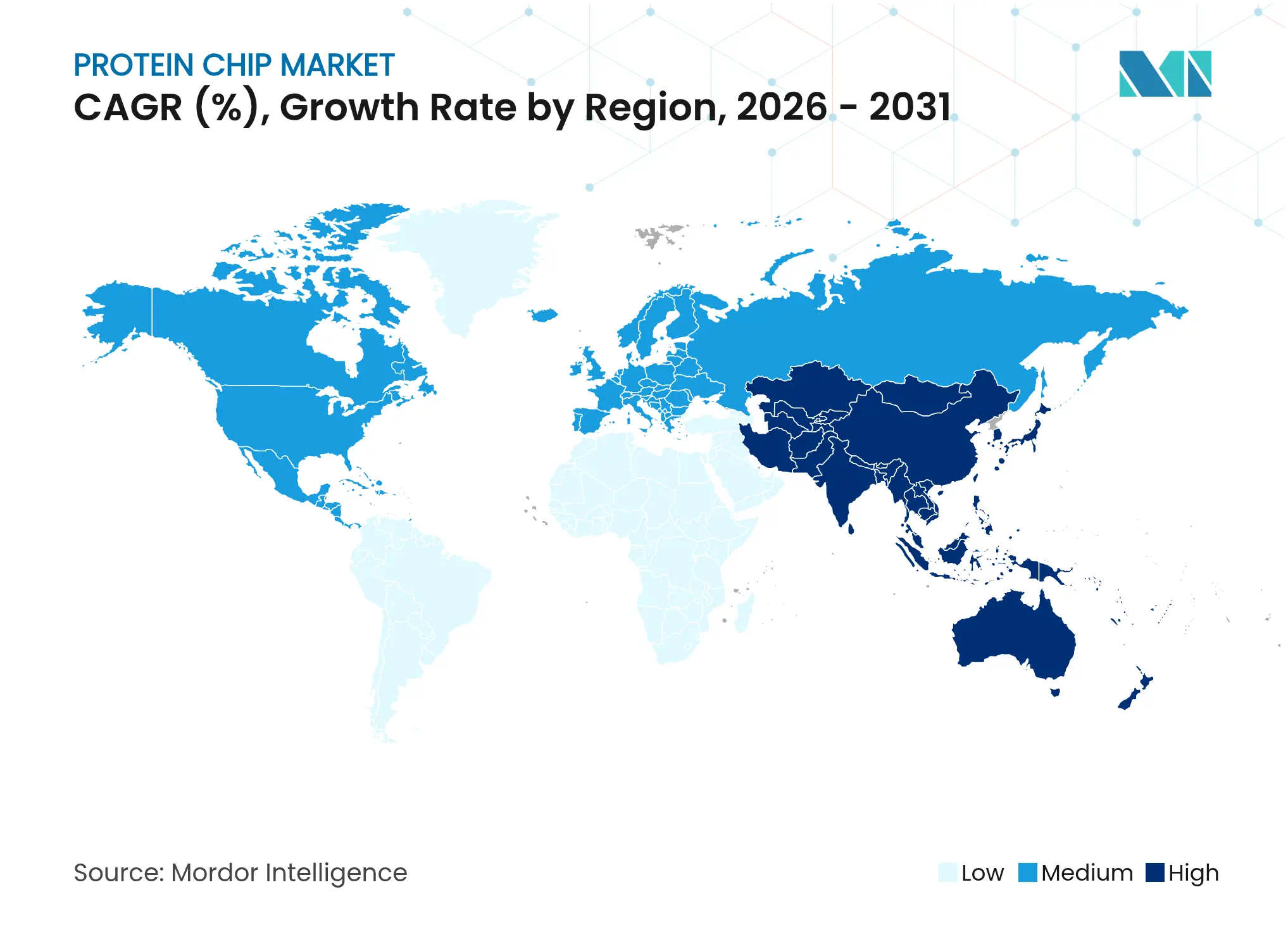

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Protein Chip Market Analysis by Mordor Intelligence

Protein chip market size in 2026 is estimated at USD 2.16 billion, growing from 2025 value of USD 2.02 billion with 2031 projections showing USD 3.03 billion, growing at 6.98% CAGR over 2026-2031. This expansion stems from rising precision oncology adoption, broader chronic-disease screening strategies, and AI-enabled data interpretation tools that shorten the time from sample to insight. Clinical laboratories now integrate high-throughput microarrays to generate comprehensive biomarker panels, thereby improving therapy selection while curbing downstream care costs. Increasing pharma–diagnostics alliances, exemplified by FDA-cleared pancancer companion tests, create mutual incentives to standardize protein chip workflows. Meanwhile, miniaturized micro-fluidic formats reduce reagent use and allow decentralized testing, positioning the protein chip market for sustained uptake in public-health programs worldwide.

Key Report Takeaways

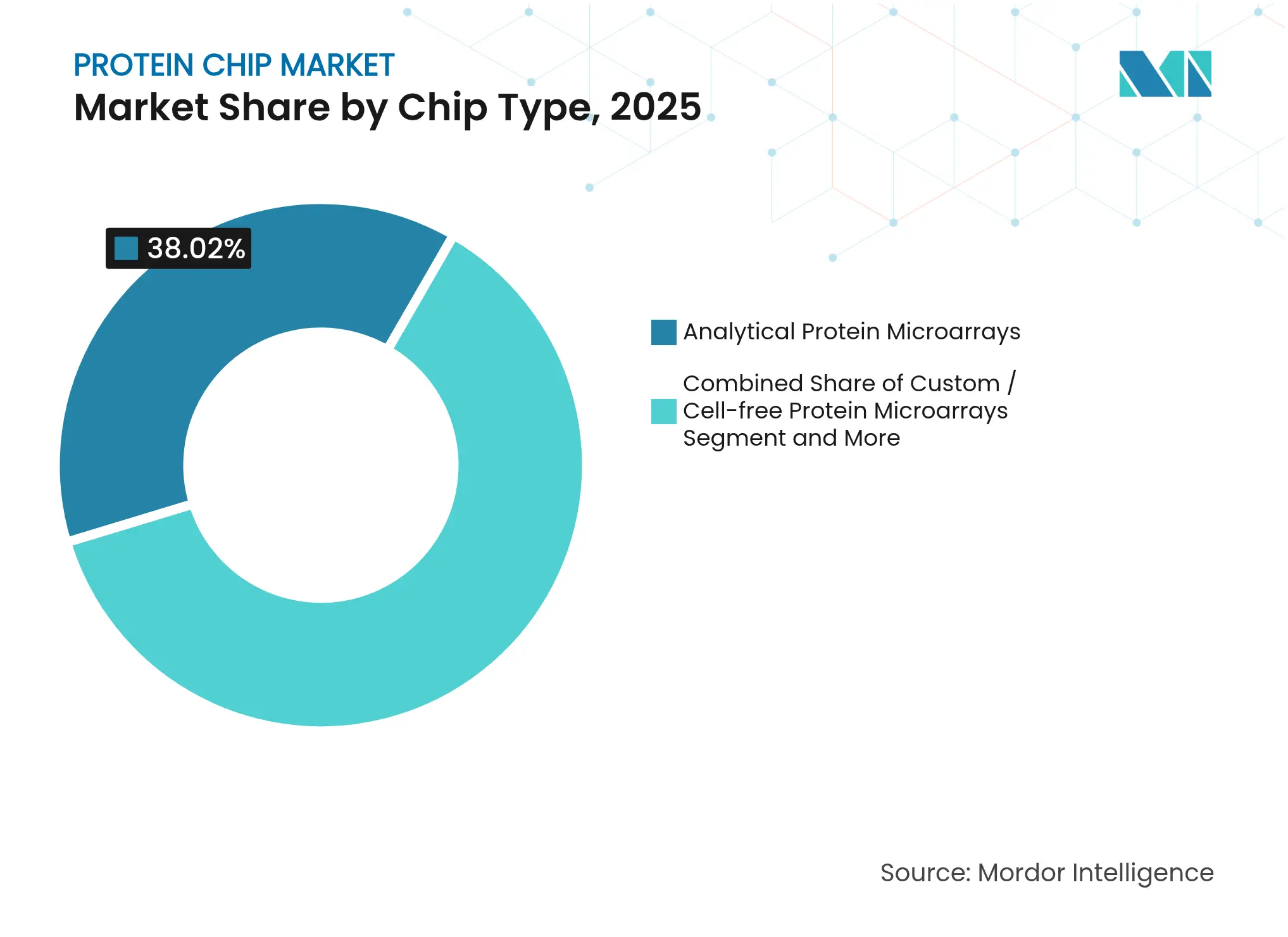

- By chip type, analytical microarrays captured 38.02% of protein chip market share in 2025, whereas custom/cell-free formats are projected to grow at 15.76% CAGR through 2031.

- By application, clinical diagnostics led with 35.05% revenue share in 2025; personalized medicine is set to advance at 16.28% CAGR to 2031.

- By surface chemistry, nitrocellulose-coated slides led with 39.94% revenue share in 2025; 3-D polymer coatings are forecast to expand at a 15.31% CAGR to 2031.

- By detection technology, fluorescence methods held 61.65% share of the protein chip market size in 2025 while label-free SPR is expected to post an 17.52% CAGR over the same horizon.

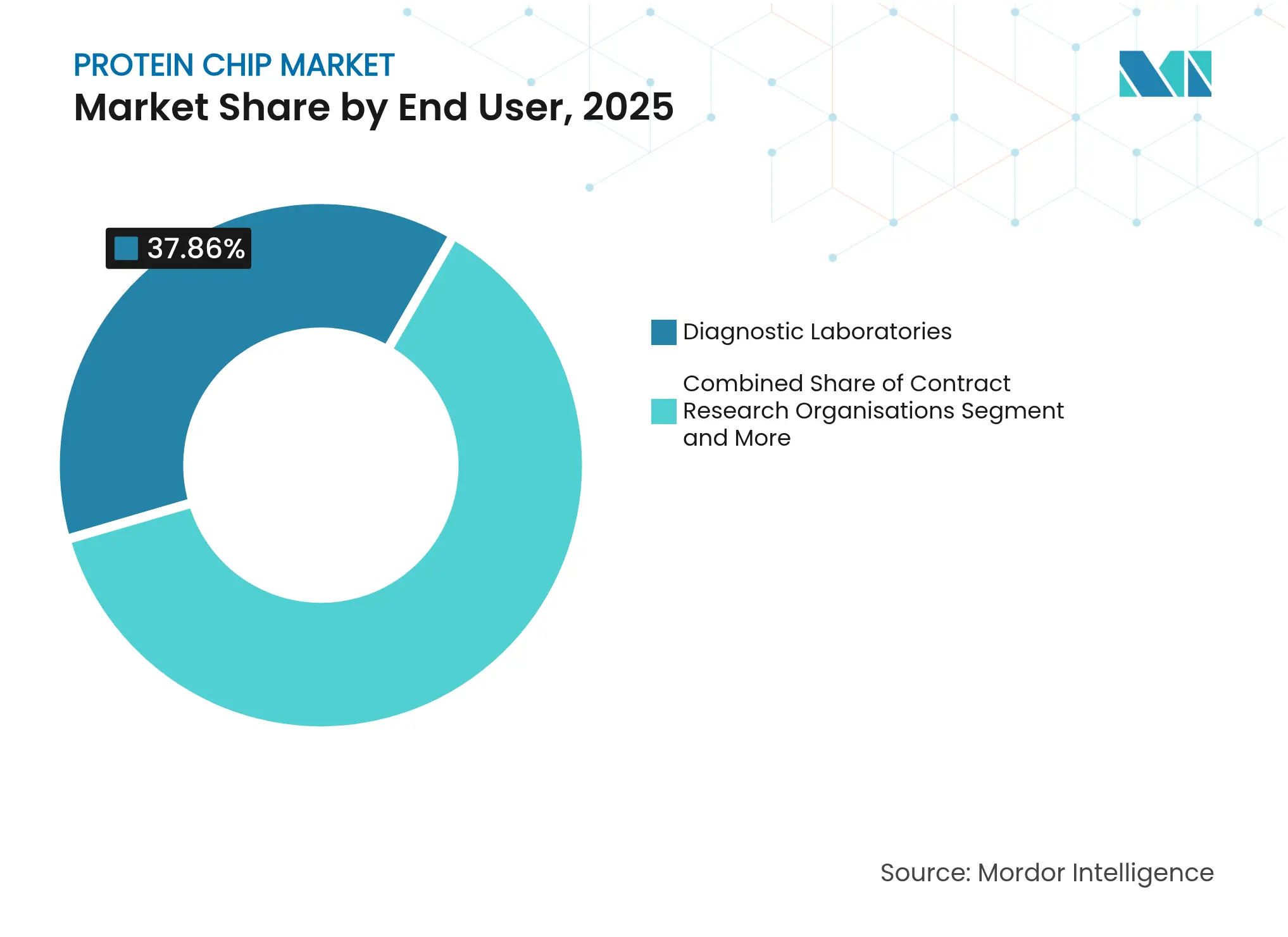

- By end user, diagnostic laboratories accounted for 37.86% of the protein chip market size in 2025, whereas contract research organizations are forecast to expand at 13.89% CAGR until 2031.

- By geography, North America commanded 44.78% share of the protein chip market in 2025, while Asia-Pacific is poised for a 13.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Chip Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising burden of chronic & complex diseases

Rising burden of chronic & complex diseases

| +1.8% | Global with focus on North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

Global with focus on North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Precision oncology adoption in clinical labs

Precision oncology adoption in clinical labs

| +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Expansion of pharma–microarray CDx partnerships

Expansion of pharma–microarray CDx partnerships

| +1.2% | Global, led by North America | Medium term (2-4 years) | |||

Micro-fluidic, high-throughput chip miniaturization

Micro-fluidic, high-throughput chip miniaturization

| +0.9% | APAC manufacturing hubs, global deployment | Long term (≥ 4 years) | |||

AI-driven analysis platforms lower data barriers

AI-driven analysis platforms lower data barriers

| +1.1% | Global, early uptake in developed markets | Short term (≤ 2 years) | |||

Pandemic-driven multiplex serology infrastructure

Pandemic-driven multiplex serology infrastructure

| +0.6% | Global, sustained in public-health systems | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Burden of Chronic & Complex Diseases

Growing prevalence of diabetes, cancer, and kidney disorders increases reliance on multiplex serum and urinary protein signatures that predict complications well before clinical onset[1]Devang Sheth, “Biomarkers in Diabetes Mellitus,” IP International Journal of Comprehensive and Advanced Pharmacology, ijcap.in. Health systems invest in analytical microarrays to discover early-stage markers that reduce downstream expenditure on late-stage interventions. Simultaneous analysis of hundreds of proteins accelerates therapeutic-target validation and enables longitudinal monitoring programs. The economic drag of chronic illnesses, measured in trillions of health-care dollars, pushes payers toward preventative diagnostics built on protein chips. Consequently, demand rises for high-capacity arrays able to process population-scale cohorts within routine laboratory turn-around times.

Precision Oncology Adoption in Clinical Labs

Laboratories shift from single-analyte assays to multiplex platforms that stratify tumor samples by protein expression, ensuring precise therapy alignment. New FDA LDT rules mandate quality-system rigor, prompting labs to implement validated protein chip kits to maintain compliance[2]U.S. FDA, “FDA Takes Action to Ensure Safety and Effectiveness of Laboratory Developed Tests,” fda.gov. Early adopters report improved diagnostic accuracy and reduced repeat testing, offsetting capital outlays for instrumentation. Implementation hurdles—staff training and workflow redesign—are mitigated by vendor-provided automation modules. As reimbursement frameworks begin to recognize multi-protein panels, precision oncology use cases transition from niche centers to broader hospital networks.

Expansion of Pharma–Microarray CDx Partnerships

Drug developers increasingly collaborate with microarray suppliers to build companion diagnostics that identify responders in oncology trials. Regulatory precedents, such as FDA clearance of TruSight Oncology Comprehensive, validate this co-development model and shorten approval cycles. Sponsors benefit from enriched trial populations that raise success probabilities, while array vendors lock in long-term reagent supply contracts. The protein chip market therefore grows through dual revenue streams: test-kit sales and royalty-bearing CDx agreements. International regulators adopt similar frameworks, expanding addressable markets across APAC and Europe.

Micro-Fluidic, High-Throughput Chip Miniaturization

Manufacturing advances in APAC enable cost-effective production of micro-fluidic arrays that require minimal sample volumes while supporting automated wash cycles. Miniaturized formats slash reagent consumption and align with point-of-care analyzers, opening public-health screening opportunities. OEMs integrate disposable cartridges with optical readers, delivering turnkey kits compatible with low-resource settings. These innovations broaden the protein chip market beyond tertiary centers to outpatient clinics and vaccination sites.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost & complexity of data analysis

High cost & complexity of data analysis

| –1.4% | Global with acute effect in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

–1.4%

| Geographic Relevance:

Global with acute effect in emerging markets

| Impact Timeline:

Medium term (2-4 years)

|

Limited availability of high-quality proteins/Abs

Limited availability of high-quality proteins/Abs

| –0.8% | Global supply chains | Long term (≥ 4 years) | |||

Lack of reimbursement for multiplex protein tests

Lack of reimbursement for multiplex protein tests

| –1.1% | North America & Europe | Medium term (2-4 years) | |||

Biosecurity & data-privacy concerns

Biosecurity & data-privacy concerns

| –0.5% | Global, heightened regulation in rich markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost & Complexity of Data Analysis

Protein chip workflows demand advanced mass-spectrometry or high-density imaging platforms that exceed the capital budgets of small labs. Skilled bioinformaticians command premium wages, adding recurrent costs. Cloud solutions lower upfront expenditure yet raise privacy worries when handling identifiable patient data. Continuous software upgrades and algorithm tuning stretch operating budgets and complicate procurement cycles. Education investments to keep staff current further restrain uptake among resource-constrained institutions.

Lack of Reimbursement for Multiplex Protein Tests

Average list prices of multiplex panels reach USD 585, contrasting sharply with USD 8 for legacy single-analyte assays. Payers often require extensive health-economics evidence, which manufacturers must finance before codes and coverage are issued. Novel biomarkers, especially in multi-cancer early detection, face skepticism over population-level cost-effectiveness. Consequently, laboratories hesitate to adopt assays without predictable payment pathways, slowing the protein chip market in payor-driven regions.

Segment Analysis

By Chip Type: Custom Platforms Drive Innovation

Analytical arrays held 38.02% of the protein chip market in 2025, underscoring their central role in regulated diagnostics where reproducibility is paramount. The protein chip market size for custom/cell-free arrays is projected to register 15.76% CAGR to 2031 as demand rises for personalized panels that mirror patient-specific mutations. NAPPA technology synthesizes proteins in situ, reducing degradation risk, and boosting capture efficiency.

Tailored arrays support rare-disease research, enabling investigators to screen patient-derived neoantigens rapidly. Reverse-phase and functional formats occupy specialized niches in oncology drug discovery, offering quantitative pathway mapping. Emerging SPOC chips pack thousands of folded proteins on 1.5-cm² sensors, raising throughput while shrinking sample volume requirements.

The protein chip market benefits as pharmaceutical sponsors outsource validation studies that require bespoke antigen sets. Glycan microarrays gain visibility in infectious-disease surveillance because they differentiate closely related viral strains. Peptide arrays mapping phospho-signatures inform kinase-inhibitor development. Sustained analytical demand plus accelerating custom adoption maintain robust order pipelines for manufacturers, cementing healthy revenue diversification across chip categories.

Note: Segment shares of all individual segments available upon report purchase

By Surface Chemistry: 3D Polymer Coatings Gain Momentum

Nitrocellulose substrates commanded 39.94% share in 2025 due to manufacturing familiarity and assay protocol compatibility. Yet 3D polymer coatings are forecast for 15.31% CAGR as improved binding sites elevate sensitivity. Hydrogels deliver soft, aqueous microenvironments that preserve protein conformation, enhancing assay fidelity.

Developers engineer anti-swelling aramid-reinforced hydrogels that resist mechanical stress and stabilize signals under high-throughput wash cycles. Surface hydrophobization achieved via interface-network reconfiguration permits selective wetting, optimizing low-abundance target capture. These advances broaden applicability from standard serum testing to cell-lysate and tissue-lysate analyses, thereby expanding the addressable protein chip market.

Demand also rises for coated slides compatible with label-free optics, where surface roughness and refractive-index homogeneity are critical. Suppliers bundle slide chemistries with validated blocking buffers, minimizing variability across lab sites. Strategic sourcing partnerships secure polymer supply chains, mitigating the restraint of limited high-quality reagents.

By Application: Personalized Medicine Accelerates Growth

Clinical diagnostics contributed 35.05% of revenue in 2025, reflecting entrenched use in autoimmune panels and infectious-disease serology. The protein chip market size allocated to personalized medicine segments is headed for 16.28% CAGR, propelled by integrative multi-omics programs that merge proteomic and genomic information for risk stratification.

Protein scoring systems measuring as few as 20 analytes surpass traditional vitals for predicting 52 incident diseases, prompting insurers to pilot preventive-screening reimbursements. Drug-discovery stakeholders deploy arrays to confirm target engagement in early clinical phases, lowering attrition rates. Epitope-mapping chips guide therapeutic-antibody engineering by pinpointing antigenic hotspots.

Laboratories engaged in mass population health studies adopt high-density arrays for cohort biomarker surveys. Multiplex disease-risk panels shift testing paradigms from confirmatory diagnostics to early-intervention gatekeepers, widening market scope. Continuous data-feedback loops refine protein-risk algorithms, driving repeat consumable purchases that underpin recurring revenue.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Contract Research Organizations Expand Services

Diagnostic labs were responsible for 37.86% of 2025 revenues, anchored by routine infectious-disease and oncology panels that run daily across core labs. CROs, however, are forecast to grow at 13.89% CAGR, leveraging flexible capacity to support pharma clinical trials requiring complex biomarker endpoints.

Hospitals extend point-of-care footprint by integrating portable fluorescence readers that deliver near-patient results within an hour. Academic centers remain innovation engines, using grant funding to test emerging chip chemistries before commercial hand-off. Biotechnology firms incorporate internal arrays for lead-compound screening but increasingly outsource high-volume sample processing to specialized CROs, reinforcing the service-led growth segment.

The protein chip industry bolsters CRO scalability through modular automation platforms that allow seamless expansion from pilot to pivotal trials. Single-cell screening interoperability enhances contract value propositions, driving multi-year strategic alliances.

Note: Segment shares of all individual segments available upon report purchase

By Detection Technology: Label-Free Methods Advance

Fluorescence detection dominated 61.65% revenue in 2025, a testament to mature reagent ecosystems and legacy instrumentation in hospital labs. Yet the protein chip market anticipates fastest growth in label-free SPR at 17.52% CAGR, driven by real-time kinetic profiling devoid of signal-quenching dyes.

Plasmonic surface-lattice resonators amplify signals by two orders of magnitude, lowering detection thresholds for low-abundance biomarkers. Machine-learning-augmented dual-band sensors provide simultaneous qualitative identification and quantitative affinity metrics. Colorimetric and chemiluminescent formats persist in low-resource settings where optical-excitation modules raise capital barriers but throughput demands remain moderate.

Emerging enhanced-angular configurations with silver nanoparticles embedded in MoS₂ films push sensitivity to 452.57°/RIU, widening dynamic range for early pathogen detection. Vendors supply application-specific kits pre-optimized for chosen optics, simplifying adoption across diverse laboratory infrastructures.

Geography Analysis

North America held 44.78% of the protein chip market in 2025, supported by precision-medicine consortia, NIH grant funding, and FDA frameworks that expedite companion diagnostic approvals. US hospital networks integrate protein chips into oncology tumor boards, while Canada’s national genomics initiatives drive proteomic add-ons in multi-omics studies. Mexico expands public-health screening via cross-border partnerships that transfer multiplex serology protocols into national labs.

Asia-Pacific is the fastest-growing region at 13.74% CAGR to 2031, propelled by China’s biopharmaceutical capacity expansion and Japan’s SCRUM-Japan nationwide precision-oncology initiative. Government subsidies for domestic instrumentation manufacturers lower acquisition costs, letting regional hospitals leapfrog legacy immunoassay platforms. India’s contract-research hub adds proteomics to existing genomics offerings, attracting multinational sponsors. South Korea embeds protein chip modules within its digital-hospital program, while Australia funds translational research that pairs chips with next-generation sequencing for pathogen surveillance.

Europe maintains steady demand underpinned by Germany’s strong biotech manufacturing base and the UK’s NHS investments in early-detection pilots. France leverages pharmaceutical sector collaborations to refine protein-based drug screening workflows. Italy and Spain adopt chips in academic cardio-metabolic studies funded by EU Horizon grants. The GCC countries invest in proteomics infrastructure to diversify oil economies through health-tech, setting up reference labs that source chips from global vendors. South Africa leads African uptake via infectious-disease monitoring projects, and Brazil anchors South American growth through public-private clinical-research networks.

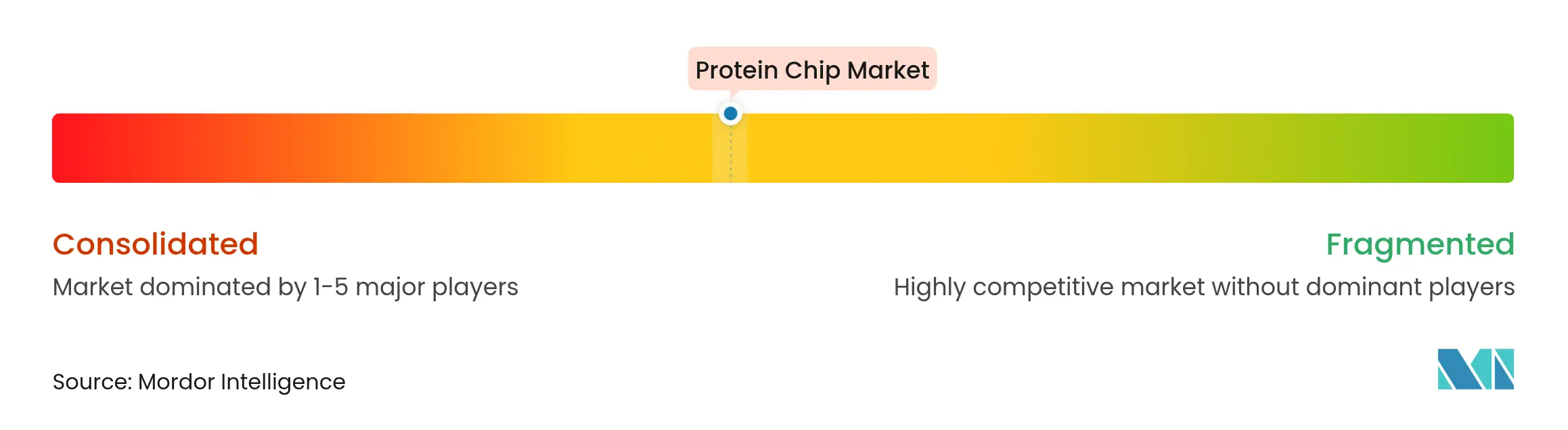

Competitive Landscape

Market Concentration

The market remains moderately fragmented yet shows signs of consolidation. Thermo Fisher’s USD 3.1 billion acquisition of Olink brought 5,300 validated PEA targets into an integrated life-science portfolio. Illumina finalized its USD 350 million SomaLogic purchase, pairing next-generation sequencing with high-plex protein quantification to enable seamless multi-omics workflows. These deals illustrate vertical-integration strategies that lock in consumables, software, and analytics under single brands.

Price competition is intense in standard analytical arrays as multiple suppliers offer near-commoditized nitrocellulose slides. Conversely, custom high-plex and spatial proteomic chips command premium margins due to limited IP ownership and specialized chemistries. Vendors differentiate through AI-enhanced analytics packages that reduce user interpretation barriers. Hardware progress, such as acoustic-ejection mass spectrometry capable of 1.5-second peptide sampling, further raises performance thresholds, favoring firms with deep R&D budgets.

White-space opportunity persists in spatial-proteomics, where emerging SPOT technology labels tissue sections in situ to map protein gradients with subcellular resolution. Companies that secure first-mover advantage in this segment may capture a disproportionate revenue share. Partnerships with contract research organizations broaden distribution reach, especially in APAC where domestic regulatory familiarity accelerates kit approvals.

Protein Chip Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina completed its acquisition of SomaLogic for USD 350 million, integrating proteomics with sequencing to drive next-generation multi-omics assay offerings.

- July 2024: Thermo Fisher Scientific finalized its USD 3.1 billion acquisition of Olink Holding, adding PEA technology and 5,300 biomarkers to its life-science solutions segment.

Table of Contents for Protein Chip Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Burden Of Chronic & Complex Diseases

- 4.2.2Precision Oncology Adoption In Clinical Labs

- 4.2.3Expansion Of Pharma-Microarray CDx Partnerships

- 4.2.4Micro-Fluidic, High-Throughput Chip Miniaturisation

- 4.2.5AI-Driven Analysis Platforms Lower Data Barriers

- 4.2.6Pandemic-Driven Multiplex Serology Infrastructure

- 4.3Market Restraints

- 4.3.1High Cost & Complexity Of Data Analysis

- 4.3.2Limited Availability Of High-Quality Proteins/Abs

- 4.3.3Lack Of Reimbursement For Multiplex Protein Tests

- 4.3.4Biosecurity & Data-Privacy Concerns

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers/Consumers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitute Products

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Chip Type

- 5.1.1Analytical Protein Microarrays

- 5.1.2Functional Protein Microarrays

- 5.1.3Reverse-Phase Protein Microarrays

- 5.1.4Glycan Microarrays

- 5.1.5Peptide / Phospho-specific Microarrays

- 5.1.6Custom / Cell-free Protein Microarrays

- 5.2By Surface Chemistry

- 5.2.1Nitrocellulose-coated Slides

- 5.2.2Hydrogel-coated Slides

- 5.2.33-D Polymer Coatings

- 5.2.4Other Chemistries

- 5.3By Application

- 5.3.1Antibody Characterisation & Epitope Mapping

- 5.3.2Clinical Diagnostics

- 5.3.3Drug Discovery & Development

- 5.3.4Proteomics & Biomarker Discovery

- 5.3.5Auto-immune & Infectious-disease Profiling

- 5.3.6Personalised / Precision Medicine

- 5.4By End User

- 5.4.1Hospitals & Clinics

- 5.4.2Diagnostic Laboratories

- 5.4.3Academic & Research Institutes

- 5.4.4Pharmaceutical & Biotechnology Companies

- 5.4.5Contract Research Organisations

- 5.5By Detection Technology

- 5.5.1Fluorescence-based

- 5.5.2Label-free (SPR)

- 5.5.3Chemiluminescence / Colorimetric

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Agilent Technologies Inc.

- 6.3.2Thermo Fisher Scientific Inc.

- 6.3.3Bio-Rad Laboratories Inc.

- 6.3.4PerkinElmer Inc.

- 6.3.5Illumina Inc.

- 6.3.6Roche Diagnostics (F. Hoffmann-La Roche Ltd.)

- 6.3.7Danaher Corp. (Molecular Devices)

- 6.3.8Merck KGaA (Sigma-Aldrich)

- 6.3.9Schott AG (Applied Microarrays Inc.)

- 6.3.10Shimadzu Corp.

- 6.3.11RayBiotech Inc.

- 6.3.12Arrayit Corporation

- 6.3.13Quanterix Corporation

- 6.3.14Abcam plc

- 6.3.15Creative Biolabs

- 6.3.16Creative Proteomics

- 6.3.17Luminex Corp. (DiaSorin Group)

- 6.3.18JPT Peptide Technologies GmbH

- 6.3.19Sengenics Corp.

- 6.3.20Z Biotech LLC

- 6.3.21Quansys Biosciences

- 6.3.22IntelliCyt (Sartorius)

- 6.3.23Innopsys

- 6.3.24FullMoon BioSystems Inc.

- 6.3.25CDI Laboratories Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Protein Chip Market Report Scope

As per the scope of the report, protein chips, commonly known as protein microarrays, serve as a high-throughput method to monitor protein interactions and activities and to ascertain their functions on a large scale. Typically, these arrays are created by depositing molecular probes onto a solid support. These probes are meticulously designed to capture specific proteins at designated sites. Protein arrays find applications in five primary domains: diagnostics, proteomics, protein functional analysis, antibody characterization, and treatment development.

The protein chip market is segmented by type, application, end-user, and geography. By type, the market is segmented by analytical microarrays, functional protein microarrays, and reverse phase protein microarrays. By application, the market is segmented by Antibody Characterization, clinical diagnostics, and proteomics. By end user, the market is segmented by hospitals & clinics, diagnostic laboratories, academic & research institutes, and pharmaceutical & biotechnology companies. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.