Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 33.47 Billion |

| Market Size (2031) | USD 58.66 Billion |

| Growth Rate (2026 - 2031) | 11.87% CAGR |

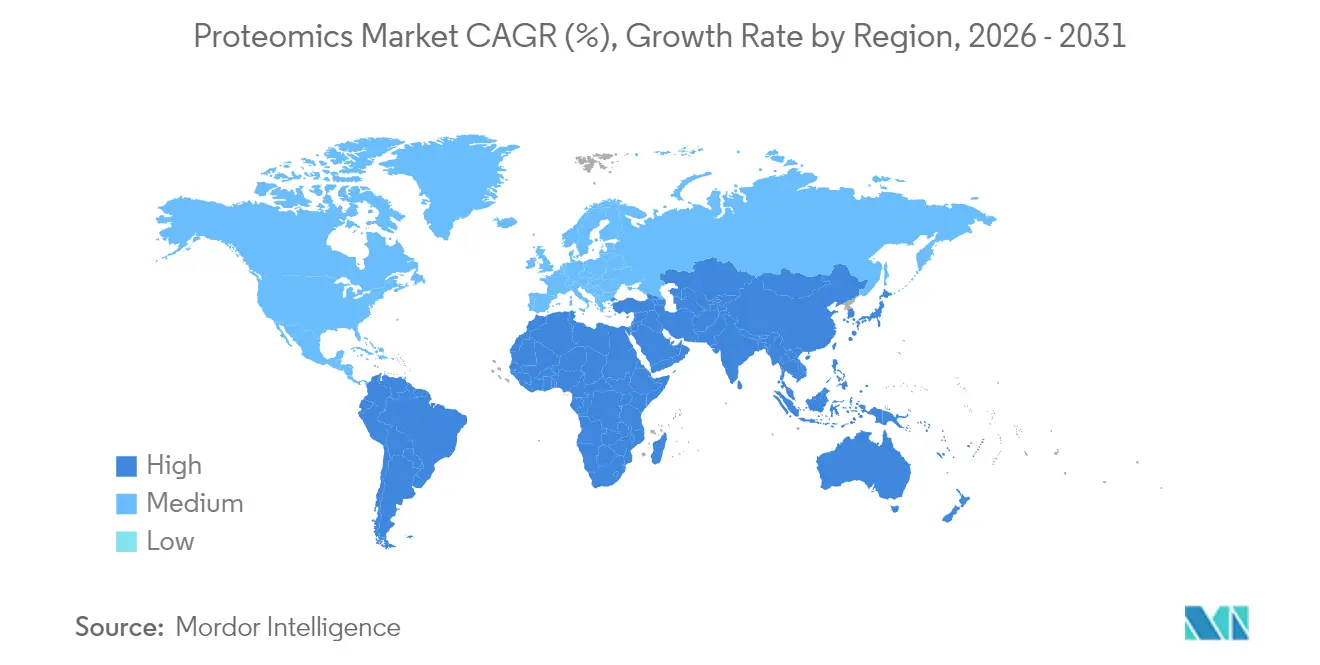

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

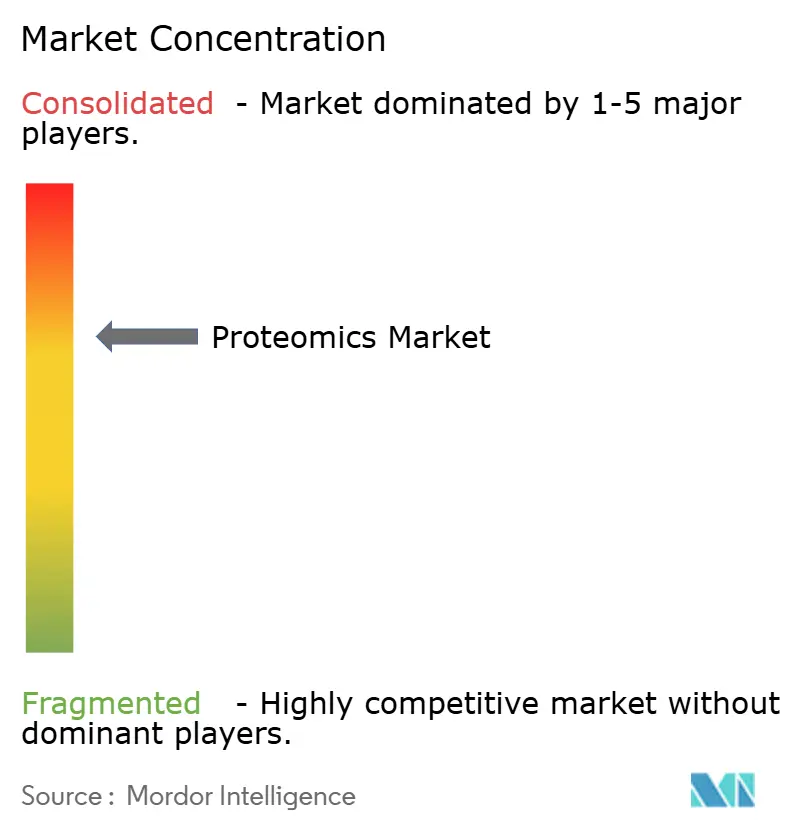

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Proteomics Market Analysis by Mordor Intelligence

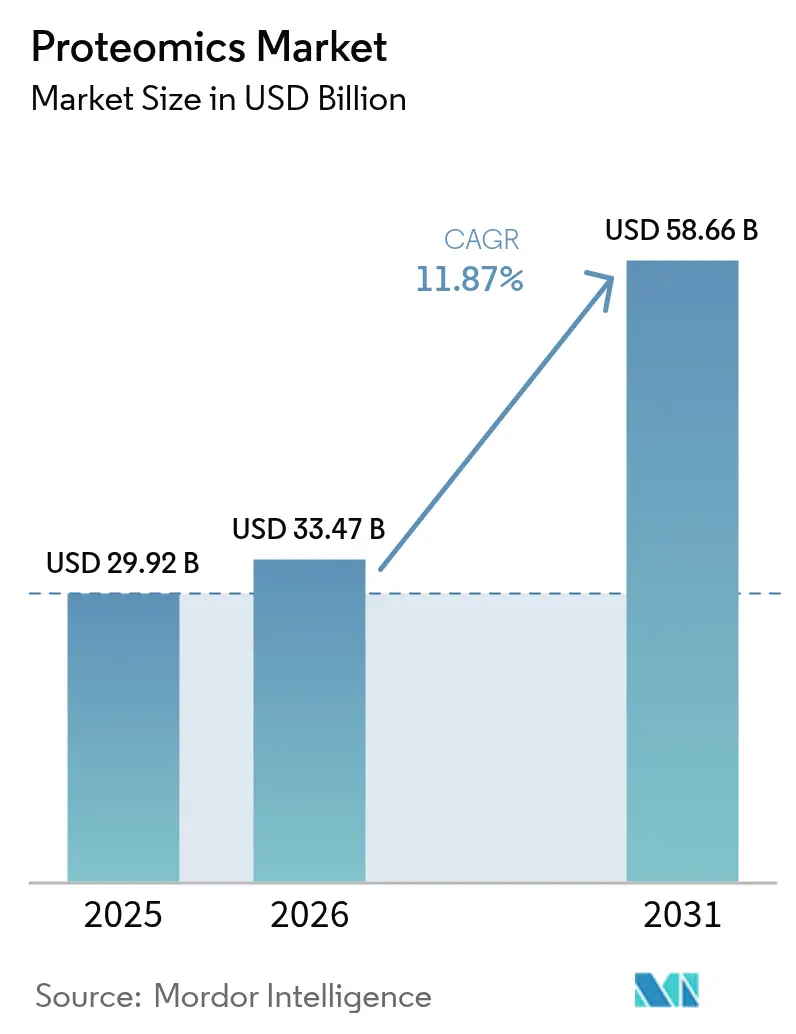

The proteomics market size was valued at USD 29.92 billion in 2025 and estimated to grow from USD 33.47 billion in 2026 to reach USD 58.66 billion by 2031, at a CAGR of 11.87% during the forecast period (2026-2031). Expansion is propelled by rapid adoption of high-throughput mass-spectrometry systems, AI-enabled single-cell workflows, and growing integration of proteomic readouts into precision-medicine programs. Pharmaceutical firms are embedding proteomics across target discovery, lead optimization, and biomarker validation, while contract research organizations (CROs) scale specialized services. Regionally, continued R&D funding and entrenched biopharma infrastructure anchor North American leadership, whereas vigorous investment across China, India, Japan, and South Korea positions Asia-Pacific as the fastest-growing arena. Competitive dynamics centre on platform consolidation: large vendors acquire niche innovators to deliver end-to-end reagent, instrument, and analytics solutions that shorten project timelines for drug-development customers.

Key Report Takeaways

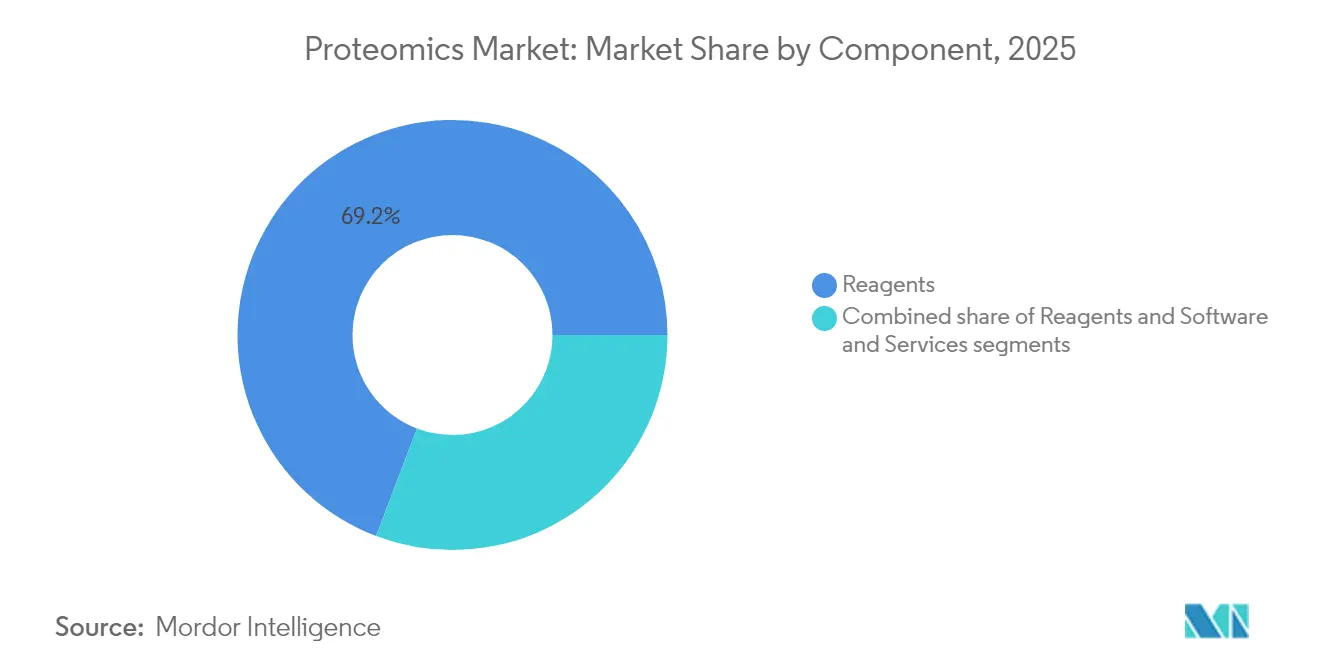

- By component, reagents led with 69.22% proteomics market revenue share in 2025; software and services are forecast to expand at a 13.31% CAGR through 2031.

- By technology, mass spectrometry commanded 30.28% of the proteomics market revenue share in 2025, while next-generation sequencing is projected to grow at 13.55% CAGR to 2031.

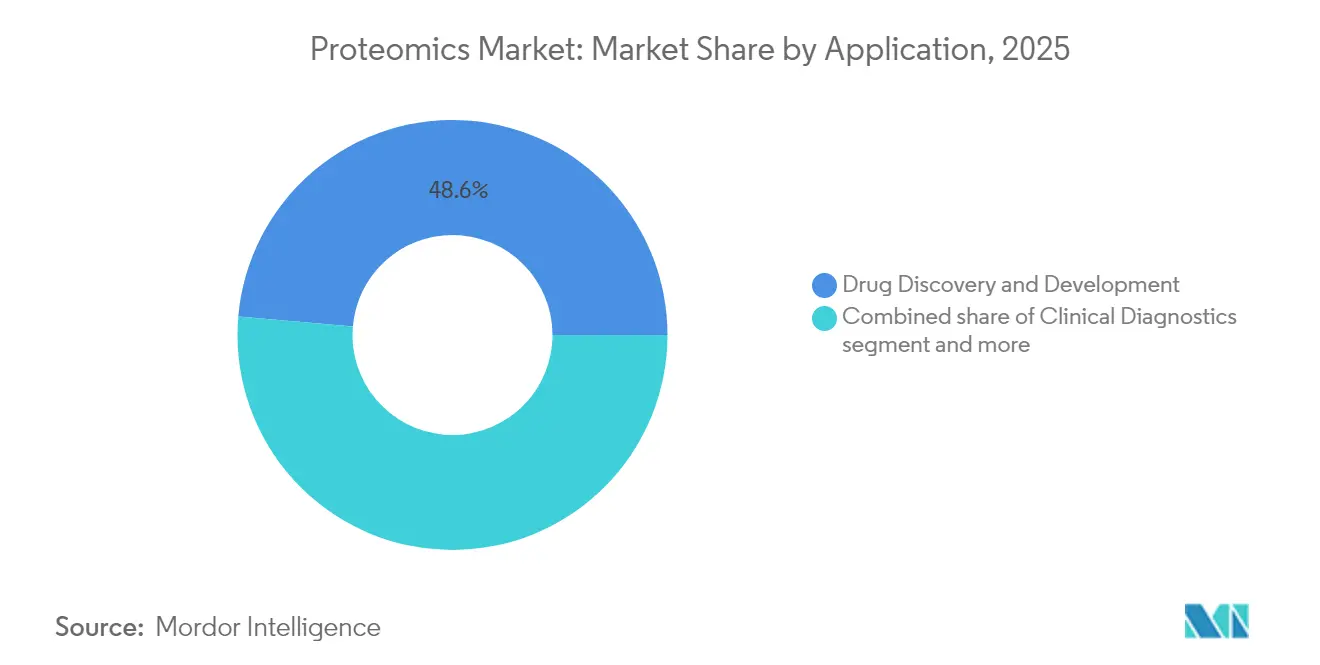

- By application, drug discovery and development captured 48.63% of the proteomics market size in 2025; precision and personalized medicine is advancing at a 13.95% CAGR to 2031.

- By end-user, pharmaceutical and biotechnology companies accounted for 73.06% demand in 2025; the CRO segment is rising at a 12.71% CAGR through 2031.

- By geography, North America contributed 44.02% of revenue in 2025, whereas Asia-Pacific is set to post a 13.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Proteomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for personalized & precision medicine | +2.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Increasing R&D expenditure and public funding | +2.1% | North America & EU, APAC core | Long term (≥ 4 years) |

| Rapid advances in high-throughput MS & LC-MS platforms | +1.9% | Global | Short term (≤ 2 years) |

| Growing adoption of proteomics in drug discovery pipelines | +1.7% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| AI-enabled single-cell proteomics breakthroughs | +1.4% | Global, concentrated in research hubs | Short term (≤ 2 years) |

| Expanding use of proteomics in agri-genomics & food safety | +0.8% | APAC core, emerging in MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Personalized & Precision Medicine

Growing clinical evidence links protein-based biomarkers with disease stratification, fostering routine inclusion of proteomic panels in large cohort studies. Thermo Fisher Scientific's Olink platform’s selection[1]Thermo Fisher Scientific, “Olink Platform Selected for World’s Largest Human Proteome Study,” thermofisher.com for the UK Biobank’s programme to profile 5,400 proteins across 600,000 samples exemplifies this shift, creating multidimensional datasets that guide therapeutic selection. Proteomic fitness scores now complement genetic risk metrics and have demonstrated responsiveness to lifestyle interventions, underscoring value for preventive-care planning. Organ-specific ageing clocks derived from circulating protein signatures are informing early intervention strategies. Pharma stakeholders view these insights as pivotal for companion-diagnostic development, reinforcing sustained demand for next-generation assay platforms.

Increasing R&D Expenditure and Public Funding

Consortia funding models that pool biopharma and public financing are scaling infrastructure once limited to elite academic centres. The UK Biobank's proteomics initiative, funded by 14 biopharmaceutical companies[2]UK Biobank, “UK Biobank Pharma Proteomics Project,” ukbiobank.ac.uk, represents a paradigm shift where industry collaboration drives large-scale proteomic studies that were previously unfeasible. Government grants across China, Japan, and Korea subsidize high-resolution mass-spectrometry installations and cloud-based data hubs, lowering barriers for start-up laboratories. Venture capital flows toward AI-native proteomic software firms, accelerating automated pattern-recognition tools that cut analysis times from days to minutes and broaden user access.

Rapid Advances in High-Throughput MS & LC-MS Platforms

Instrument suppliers introduced successive flagship releases in 2024-25 that multiply scan speed and sensitivity. Thermo Fisher’s Stellar Mass Spectrometer reports 10-fold higher quantitative sensitivity, while Bruker’s timsTOF Ultra 2 boosts ion-capture efficiency toward 100%, enabling deeper proteome coverage per run. SCIEX’s ZT Scan DIA achieves tenfold acceleration over earlier data-independent workflows, supporting population-scale studies without sacrificing data quality. These gains collectively shorten acquisition windows, increase sample throughout, and make deep-profiling economically viable for translational projects.

Growing Adoption in Drug-Discovery Pipelines

Proteomics underpins every linkage from target validation to clinical-trial biomarker readouts. Bristol Myers Squibb allocated USD 400 million to collaborate with AI Proteins on miniprotein-based therapeutics. Pfizer’s engagement with Edelris brings proteomics-driven molecular-glue discovery into its small-molecule portfolio. Such deals illustrate how in-house discovery teams partner with specialist platforms to tackle previously undruggable proteins, expanding total addressable markets for precision treatments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & operating cost of instruments | -1.8% | Global, particularly impacting smaller labs | Long term (≥ 4 years) |

| Shortage of skilled bioinformaticians & proteomics experts | -1.2% | Global, acute in emerging markets | Medium term (2-4 years) |

| Data-analysis complexity & lack of workflow standards | -0.9% | Global | Short term (≤ 2 years) |

| Limited throughput for native membrane-protein studies | -0.6% | Global, research-focused impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost of Instruments

Top-tier Orbitrap or trapped-ion-mobility platforms routinely exceed USD 1 million per system, and annual service contracts may add 10% of purchase price. Labs must also budget for consumables, vacuum infrastructure, and environmental controls. Although university-level initiatives such as the E3 method reduce sample-prep costs, hardware outlays remain a hurdle for mid-tier institutions. Shared-facility models and CRO outsourcing mitigate entry costs yet can constrain experimental flexibility.

Shortage of Skilled Bioinformaticians & Proteomics Experts

Analysis pipelines demand expertise spanning chemistry, statistics, and machine learning. Global demand for cross-trained scientists outpaces university graduates, creating wage inflation and hiring bottlenecks. Regulatory-grade workflows further require knowledge of CLIA-like validation standards, extending training timelines. Industry groups have responded with micro-credential programmes, but a structural talent gap persists, especially in fast-growing Asia-Pacific markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Dominance of Reagents and Momentum in Software

Reagents accounted for 69.22% of the proteomics market share in 2025, reflecting their consumable nature and indispensability across sample lysis, enrichment, labelling, and quantitation steps. High adoption of bioorthogonal tags that improve detection specificity sustains robust reorder volumes. The instruments sub-segment benefits from premium pricing on ultrahigh-resolution spectrometers designed for single-cell assays. Software and services are growing at a 13.31% CAGR as laboratories confront rising data volumes and seek AI-driven analytics platforms that remove bioinformatics bottlenecks. Cloud-native pipelines that integrate quality-control dashboards with automated annotation broaden accessibility for non-specialists, supporting overall proteomics market expansion.

Adoption of subscription licensing accelerates vendor revenue, while managed-service contracts bundle instrument monitoring, data storage, and compliance reporting into predictable fees. CROs leverage modular software to offer rapid-turnaround studies, allowing smaller biotech companies to conduct discovery without installing costly hardware. As multi-omics integration becomes routine, hybrid workflows that co-analyze transcriptomic and proteomic layers rely on middleware capable of harmonizing heterogeneous datasets, further fueling demand for specialized analytics solutions within the proteomics market.

By Technology: Mass Spectrometry Leadership and NGS Upswing

Mass-spectrometry platforms captured 30.28% of the proteomics market share in 2025, owing to continuous innovation in ion-optics and detector design that extends resolving power past 200,000 for proteins up to 80 kDa. Time-of-flight-Orbitrap hybrids deliver sub-ppm mass accuracy at scan speeds supporting population-scale cohort studies. The proteomics market size tied to next-generation sequencing is forecast to expand at 13.55% CAGR, reflecting the converging utility of DNA-encoded libraries and ribosome-display systems in mapping protein-interaction networks. Sequencing-based readouts provide orthogonal validation of post-translational modifications and support high-multiplex quantitation.

Complementary methods such as microfluidic-based separation and spatially resolved protein arrays gain traction for tissue-context analysis. Integration of chromatography upgrades, including ultra-high-pressure variants, enhances front-end separation and reduces sample carry-over, boosting confidence in low-abundance peptide identification. Vendors now package cross-platform kits that streamline transfer between LC-MS, capillary electrophoresis, and imaging-based workflows, ensuring method continuity for longitudinal studies within the proteomics market.

By Application: Drug-Discovery Scale and Precision-Medicine Acceleration

Drug discovery and development represented 48.63% proteomics market size in 2025 through its deep reliance on proteomic profiling for target validation, mode-of-action elucidation, and pharmacodynamic biomarker tracking. Adaptive trial designs incorporate real-time proteomic endpoints to expedite go/no-go decisions, thereby lowering attrition costs. Precision-medicine initiatives are projected to grow at 13.95% CAGR as health systems adopt multi-omic diagnostics to guide therapeutic selection. The proteomics market size associated with companion-diagnostic assays is expected to climb sharply as regulators endorse protein-signature panels for oncology and metabolic diseases.

Clinical-diagnostic laboratories deploy multiplexed protein panels for early detection of neurodegeneration and cardiovascular risk. Agricultural and food-safety groups adopt targeted proteomics to verify allergen content and monitor crop pathogen resistance. Environmental agencies monitor emerging contaminants via protein bioindicators in sentinel species, extending commercial opportunities beyond healthcare. Academic consortia leverage shared repositories to cross-validate biomarker signatures, underscoring collaborative momentum inside the proteomics market.

By End-User: Pharma-Biotech Pre-eminence and CRO Surge

Pharmaceutical and biotechnology companies generated 73.06% of the proteomics market share in 2025 by embedding high-depth proteome profiling across discovery pipelines. Integration of label-free quantitation and structural proteomics accelerates time-to-candidate selection and informs rational combination therapies. CROs are advancing at a 12.71% CAGR as outsourcing mitigates capital burden and supplies specialized analytical depth. The proteomics market share accruing to CROs rises alongside their capacity to manage regulatory documentation and to deliver clinical-grade datasets.

Academic institutions continue to spearhead fundamental technology advances, often in partnership with large instrumentation vendors that provide demonstration units in exchange for method-development insights. Government laboratories invest in biosurveillance and biodefence programmes, applying proteomic assays for pathogen fingerprinting. Food-testing facilities deploy targeted panels for quality-assurance programmes, adding non-pharma revenue streams that stabilize the overall growth of the proteomics market.

Geography Analysis

North America retained 44.02% of global revenue in 2025 due to an entrenched biopharma enterprise, sustained National Institutes of Health funding, and large-scale precision-medicine cohorts. The United States hosts leading vendors such as Thermo Fisher Scientific, which has closed 54 strategic acquisitions, averaging USD 3.09 billion, to deepen technology breadth. Canada expands through public-private genomics initiatives, while Mexico builds niche CRO capabilities serving regional generics manufacturers.

Europe recorded 11.72% CAGR with Germany, the United Kingdom, and France as principal contributors. The UK Biobank’s proteome programme exemplifies pan-European collaboration and underpins an ecosystem of contract-analysis providers that interpret multi-omic datasets for pharma sponsors. Germany leverages domestic precision-instrument engineering to export high-performance LC-MS systems, whereas France and Italy scale clinical trial networks that integrate proteomics endpoints, strengthening the proteomics market across the continent.

Asia-Pacific is positioned as the fastest-growing region at 13.62% CAGR through 2031. China’s Five-Year Plan earmarks biotechnology as a strategic pillar, and patent grants for novel diagnostic panels validate domestic innovation capacity. India draws investment into cost-effective CRO hubs and establishes joint-degree programmes in proteogenomics to alleviate talent shortages. Japan pioneers robotics-enabled sample preparation, while South Korea subsidizes AI-native bio-informatics start-ups. Australia’s translational research alliances focus on agrigenomics and rare-disease diagnostics, broadening the addressable proteomics market. Middle East and Africa show progressive adoption in tertiary hospitals, and Brazil leads South American uptake through vaccine-related proteome studies.

Regulatory Landscape

Proteomics used for regulated bioanalysis and clinical decision-making increasingly tracks harmonized validation expectations for mass spectrometry-based biomarker measurement. ICH M10 (effective January 2023) and EMA implementation guidance establish a common bar for bioanalytical method validation, shaping how quantitative proteomics assays are designed, validated, and documented for medicinal product development, especially when the resulting data support marketing authorization dossiers.

For proteomics-enabled companion diagnostics in Europe, Regulation (EU) 2017/746 (IVDR) requires conformity assessment and triggers EMA consultation with notified bodies for centrally authorized medicines. In the United States, FDA regulatory science collaboration with NIH through CPTAC provides a structured path for best-practice guidance on targeted, quantitative proteomic assays, while NIH Data Management and Sharing (DMS) Policy requirements (effective January 2023) formalize data planning, governance, and sharing obligations for many publicly funded proteomics programs.

Value Chain Analysis

The proteomics value chain covers instrument OEMs (mass spectrometers, LC systems, and automation), consumables and reagents (sample preparation, labeling, immunoaffinity enrichment, columns), and software and services (identification and quantitation pipelines, QC, data management, and interpretation). Biopharma discovery and regulated QC workflows increasingly pull demand through the chain, and CROs and clinical labs act as scale amplifiers by bundling method development, run execution, and compliance-grade reporting.

Partnerships also show tighter coupling across stages to reduce workflow complexity and improve throughput. Thermo Fisher Scientific's April 2026 collaboration with Singapores PRECISE-SG100K biobank connects Olink PEA and Orbitrap Astral systems into a population-scale pipeline, while IonOpticks June 2026 reseller and co-marketing arrangement with SCIEX packages chromatography (Aurora Series XS columns and HeatSync temperature control) through an OEM channel. In translational and emerging-modality work, Nomic Bios April 2026 partnership with Broad Clinical Labs integrates Omni 1000 into discovery and translational workflows, and Quantum-Si and Cell Signaling Technology are validating PTM workflows by pairing single-molecule protein sequencing with established immunoaffinity enrichment capabilities.

Competitive Landscape

Competition is marked by consolidation among instrument suppliers pursuing vertically integrated solutions. Thermo Fisher’s USD 3.1 billion acquisition of Olink in July 2024 unites proximity-extension assays with Orbitrap mass-spectrometry, creating a broad sample-to-insight workflow. Bruker completed an EUR 870 million purchase of ELITech[4]Bruker Corporation, “Bruker Completes Acquisition of ELITech,” bruker.com to reinforce diagnostic-kit offerings that feed downstream mass-spectrometry confirmation. Quanterix integrated Akoya Biosciences’ spatial-omics portfolio to deliver both blood-based and tissue-context protein biomarker detection.

Strategic partnerships escalate discovery pipelines: Bristol Myers Squibb signed a USD 400 million deal with AI Proteins to co-develop miniprotein therapeutics. Orionis Biosciences secured USD 105 million upfront from Genentech for molecular-glue drug discovery. Vendors differentiate through proprietary AI algorithms that automate peptide-spectra matching, reduce false-positive identifications, and enable real-time feedback during chromatographic runs. Smaller disruptors focus on cloud-native lab-in-a-box solutions that shrink hardware footprints and appeal to decentralized research teams.

Market entrants specializing in single-cell proteomics incorporate acoustic droplet-ejection and nanoflow LC to boost sensitivity at sub-picogram levels. Integration of rapid-sample tag chemistries with ultra-high-resolution mass analyzers delivers cell-to-cell heterogeneity insights critical for immuno-oncology programmes. Established players respond by launching upgrade pathways that plug next-gen front-end modules into installed bases, protecting share within the proteomics market.

Proteomics Industry Leaders

Agilent Technologies, Inc.

Bio-Rad Laboratories, Inc.

Bruker Corporation

Danaher Corporation

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is standardization and regulatory-grade translation of proteomics, where cross-platform comparability and validated workflows become expected procurement requirements rather than optional enhancements. The Charite Open Peptide Standard for Plasma Proteomics (OSPP), published in December 2025, offers a reference-material approach designed to support reproducibility across plasma and serum studies, targeting a key barrier for multi-site clinical programs and CRO-delivered datasets.

Another opportunity is scaling population and national infrastructure programs that lock in long-term demand for instruments, reagents, and analytics. In the Netherlands, the Oncode Accelerator second-round funding (EUR 123 million, July 2025) and the NWO-funded BioBeyond_NL roadmap award (EUR 17 million, September 2025) explicitly target mass spectrometry, glycoscience, and computational facilities, which expands the installed base and the surrounding service ecosystems. On the platform side, ultra-high-throughput MS performance disclosures such as Orbitrap Astral Zoom data (January 2026) and major vendor launches at ASMS 2026 (Thermo Fisher Scientific, May 2026) sustain procurement interest around faster scan rates and integrated analytics, while fit-for-purpose validation work aligned to ICH Q2(R2) for untargeted proteomics in biotherapeutic host cell protein quantification (March 2026) points to a commercial lane for compliant methods, software traceability, and QC-ready assay packages.

Recent Industry Developments

- June 2026: Bruker launched the timsMRMS system at ASMS, combining trapped ion mobility separation with magnetic resonance mass spectrometry. The introduction extends 4D proteomics workflows toward higher selectivity and richer proteoform and PTM readouts, raising the performance bar for premium instrument purchases and downstream software upgrades.

- May 2026: Agilent launched a multi-attribute method (MAM) solution built around LC high-resolution mass spectrometry for pharma and biopharma quality control use cases. Positioning HRMS as a more routine QC workflow supports recurring demand for standardized consumables, method packages, and compliance-oriented software.

- July 2024: Thermo Fisher Scientific completed its acquisition of Olink for USD 3.1 billion, combining proximity extension assay capabilities with Thermo Fishers mass spectrometry ecosystem. The deal strengthened end-to-end offerings from sample to protein readout and intensified platform consolidation across reagents, instruments, and analytics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the global revenue generated from tools, reagents, software, and services used to study proteins, including protein identification, quantification, structure, and related biological functions in research and applied settings.

Scope exclusions: genomics-only workflows, protein production and expression products, and general lab consumables that cannot be tied back to proteomics use are excluded.

Segmentation Overview

- By Component

- Instruments

- Reagents

- Software and Services

- By Technology

- Mass Spectrometry

- Spectroscopy

- Chromatography

- Next-Generation Sequencing

- Protein Microarrays

- Microfluidics

- X-ray Crystallography

- Other Technologies

- By Application

- Drug Discovery & Development

- Clinical Diagnostics

- Biomarker Discovery

- Precision and Personalized Medicine

- Agricultural & Environmental Proteomics

- Other Applications

- By End-User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting a clear boundary for what counts as proteomics revenue and mapping it to measurable signals. We relied on public sources such as the National Institutes of Health (NIH) funding databases, the World Health Organization (WHO) disease and health statistics, OECD health indicators, and US FDA databases where regulated diagnostics context was relevant. We also reviewed World Bank macro indicators and international trade statistics to sanity check regional demand direction for instruments and reagents.

To make the dataset usable, we reviewed company filings, investor presentations, product catalogs, and peer-reviewed journals to understand workflow adoption and product mix. Patent database screening was also used to detect technology intensity shifts (for example, mass spectrometry and data analysis advances). In parallel, we used paid subscriptions for company financials and shipment-level import and export records to cross-check supplier footprint and trade flows. These examples are not exhaustive, and other public and paid sources were also referenced to collect, validate, and clarify specific data points.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with instrument suppliers, reagent providers, software and service specialists, clinical lab stakeholders, and large research users. We included APAC, EMEA, and the Americas so pricing practices, procurement cycles, and adoption differences could be reconciled before finalizing assumptions for volumes and average selling prices.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 47% |

| Mid tier: 40% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 22% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where spending pools are reconstructed from proteomics workflow adoption across research, biopharma, and clinical use, then split into instruments, reagents, and software and services. After shaping the demand pool, we corroborate it with selective bottom-up approximations, such as rolling up sampled supplier revenues, applying sampled ASP times unit volumes, and validating channel feedback. This helps adjust totals when the top-down picture appears stretched.

Key inputs used in the model include mass spectrometry installation trends, reagent and consumable pull-through per active instrument, software and services attach rates, the split between discovery and clinical or applied use, and funding and budget direction in major research markets. Where an input is not consistently observable by country, we bridge gaps using proxy indicators like lab density and research intensity, and then pressure test the output with expert feedback. For forecasting, scenario analysis is used around adoption speed and ASP progression, and the year-by-year path is aligned to variable-level expectations shared by industry respondents so the forward curve stays realistic.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as instrument shipment direction, reported reagent revenue mix, and regional research spending trends, and then variances are investigated before sign-off. When a large mismatch appears, we revisit assumptions, re-check conversions and time alignment, and re-contact relevant respondents to confirm whether there was a pricing shift, a product mix change, or a demand shock.

Each study goes through multi-step analyst reviews where calculations, scope boundaries, and year mapping are verified. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, technology shifts, or sharp macro moves affecting lab budgets. Before delivery, a final pass is completed so the published view reflects the latest information available.

Mordor Intelligence's Global Proteomics Market Market Size Measured Against Other Published Estimates

Published market values for proteomics often diverge because researchers do not always count the same revenue streams, and they also pick different base years and update timing. Differences can also come from how instruments, reagents, and services are bundled, and how currency conversion is handled across regions.

The table makes the gap visible, and it usually traces back to what is included as proteomics revenue and how fast adoption is assumed to expand across research and clinical demand. Some sources exclude workflow areas like software and services or treat them as a smaller add-on, while others may include adjacent categories that are not strictly proteomics. Base-year choice matters too because pricing and product mix have been moving, so a 2024 base can land lower than a 2026 base even before forecasting assumptions are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.47 B (2026) | |

| Industry Publisher A | USD 31.00 B (2025) | Uses an earlier base year and applies a different product boundary that can exclude selected proteomics software and services, which reduces the starting value before growth is applied. |

| Global Consultancy B | USD 27.80 B (2024) | Anchors sizing to a 2024 base with heavier weight on reagents and consumables, and it can understate later-year instrument cycle effects and ASP uplift when converting across regions. |

The table points to a base-year and scope spread, and in Mordor Intelligence's model the 2026 value is built by counting instruments, reagents, and software and services only when they are tied to proteomics workflows, and then aligning regional currency timing to the same year. When those choices are made consistently, the outcome is easier to trace back to clear demand indicators, and the forecast steps are simpler to replicate and review.

Key Questions Answered in the Report

Why are reagents the most purchased products in the proteomics industry?

Every laboratory run requires fresh reagents for sample preparation, labeling, and quantification, so repeat purchasing drives constant revenue and keeps this category ahead of instruments and software.

How is artificial intelligence changing single-cell proteomics?

AI algorithms now automate peptide-spectra matching and pattern recognition, allowing researchers to extract meaningful insights from thousands of individual cells in hours instead of days.

What factors make Asia-Pacific the fastest-expanding proteomics hub?

Governments across China, India, Japan, and South Korea fund new biotech parks, subsidize high-resolution mass-spectrometry installations, and foster academic–industry partnerships that accelerate technology adoption.

Which end-user group is outsourcing proteomics services the most and why?

Mid-size pharmaceutical and biotechnology firms increasingly rely on contract research organizations to access advanced instrumentation and regulatory-grade workflows without making large capital investments.

How are mergers and acquisitions influencing market competition?

Large instrument vendors are buying niche assay and software developers to offer end-to-end platforms, giving customers seamless workflows from sample to insight and consolidating supplier options.

What is the biggest operational challenge facing labs that adopt next-generation proteomics hardware?

The shortage of cross-trained scientists who can operate complex instruments and interpret data sets slows project timelines and limits the pace at which new systems can be deployed.

Page last updated on: