Cosmetic Peptide Synthesis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 259.63 Million |

| Market Size (2031) | USD 337.09 Million |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic Peptide Synthesis Market Analysis by Mordor Intelligence

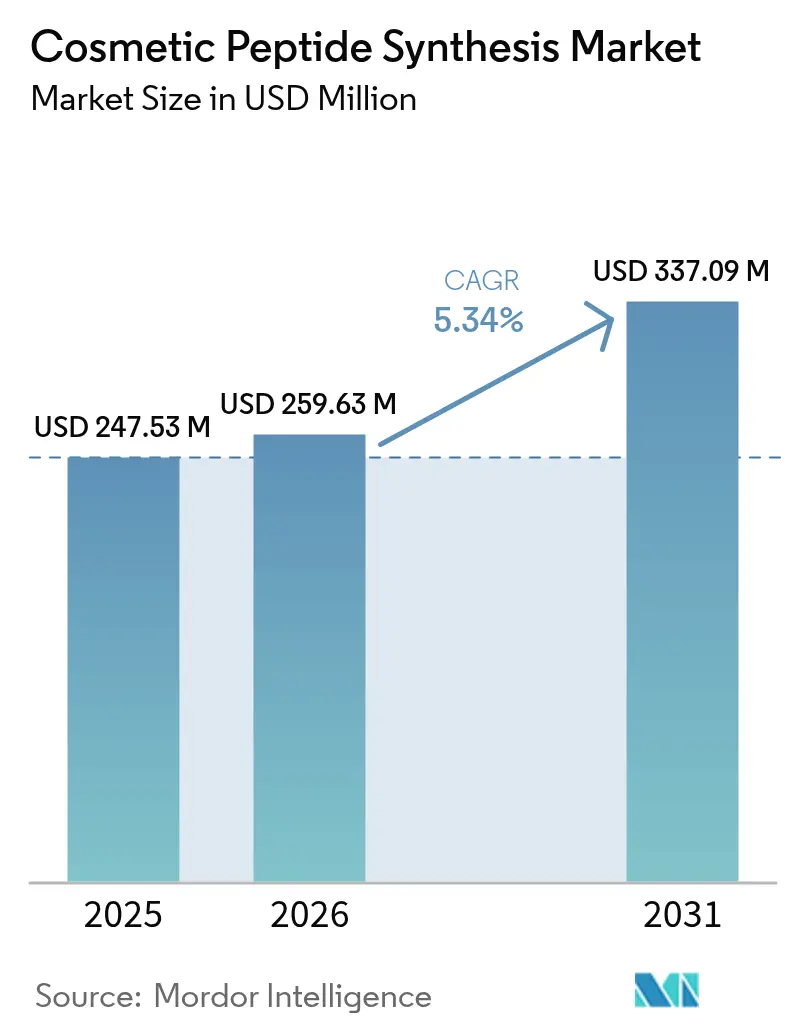

The Cosmetic Peptide Synthesis Market size was valued at USD 247.53 million in 2025 and is estimated to grow from USD 259.63 million in 2026 to reach USD 337.09 million by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

Advances in microwave-assisted solid-phase systems have trimmed synthesis cycles from weeks to days, while machine-learning models now predict peptide stability and skin permeability with better than 85% accuracy, giving formulators confidence to replace legacy actives. Demand is also migrating from single-function to multi-stack formulations, prompting brands to co-develop proprietary sequences with suppliers to secure exclusivity and higher price points. Regulatory fast-track pathways in the United States and South Korea shorten review times for functional cosmetics, enabling quicker commercialization of novel peptides. Finally, recombinant biosynthesis is reducing solvent use and production costs, helping the cosmetic peptide synthesis market adopt “clean-beauty” positioning without compromising purity.

Key Report Takeaways

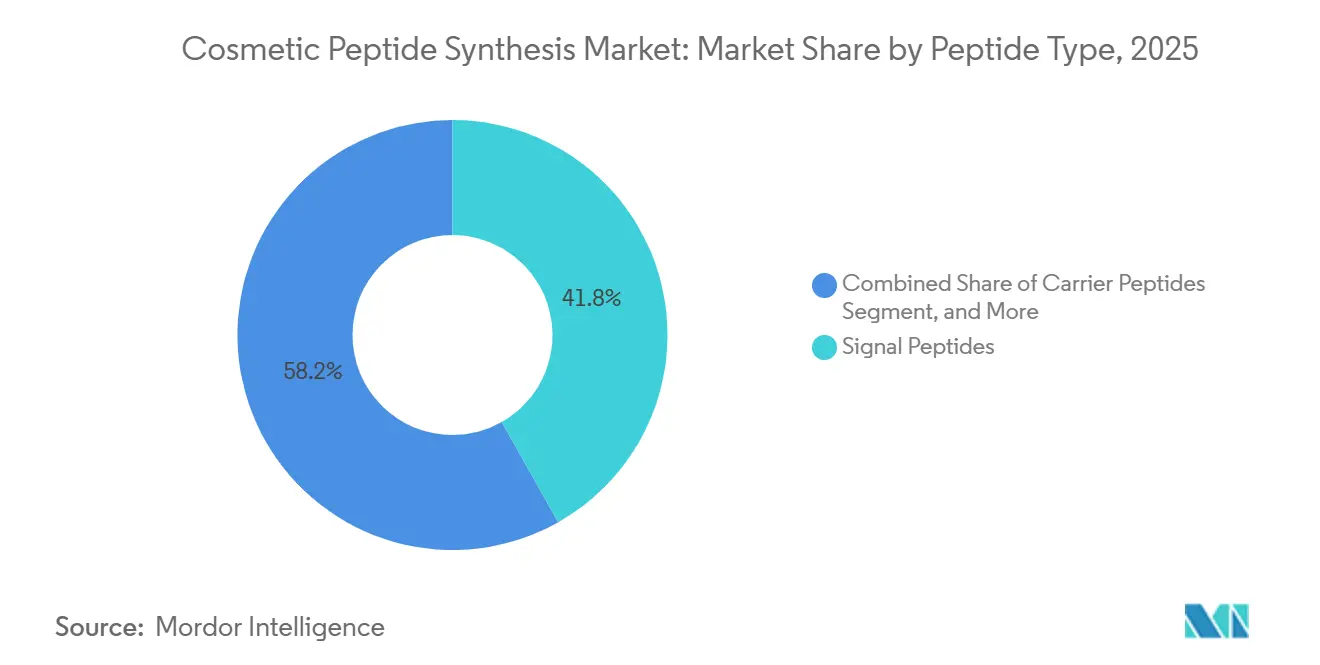

- By peptide type, signal peptides led with 41.82% of the cosmetic peptide synthesis market share in 2025, while carrier peptides are projected to expand at a 6.43% CAGR through 2031.

- By application, anti-aging accounted for 48.27% of the cosmetic peptide synthesis market size in 2025, whereas hair-care and scalp products are expected to post the fastest 8.72% CAGR to 2031.

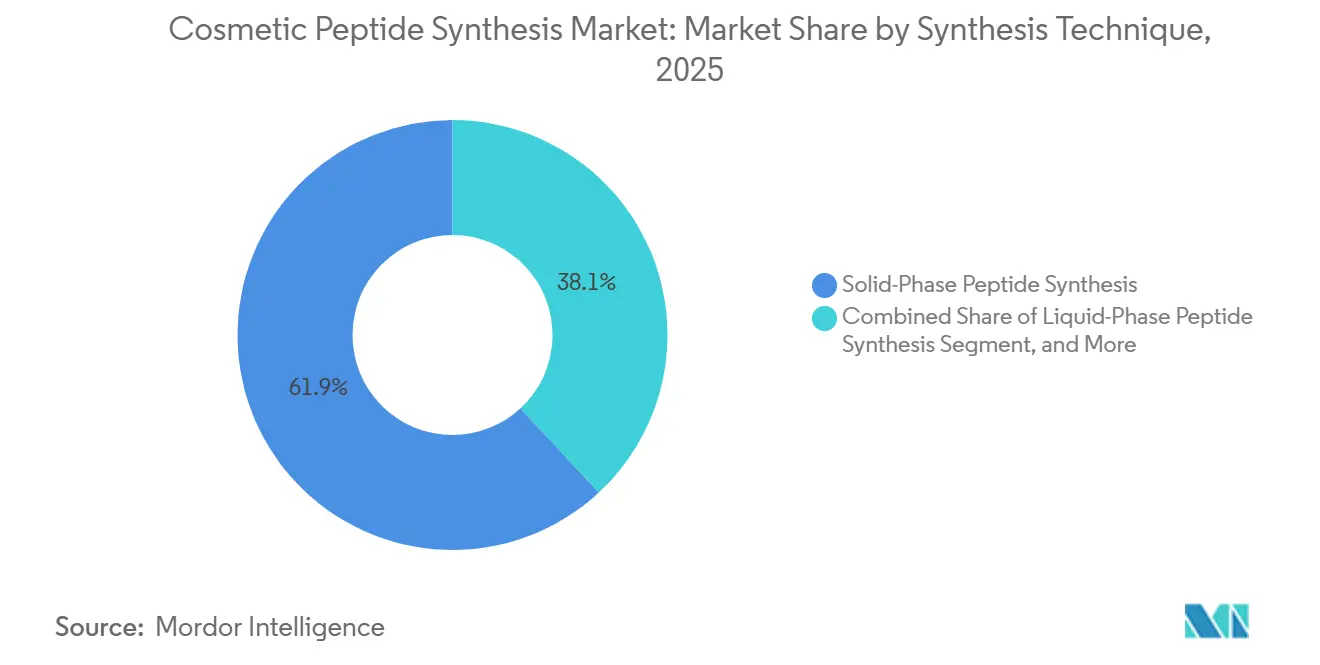

- By synthesis technique, solid-phase peptide synthesis held a 61.91% share in 2025, and recombinant or cell-free biosynthesis is advancing at a 7.45% CAGR between 2026 and 2031.

- By purity grade, ≥98% cosmetic grade accounted for 51.78% of the market in 2025 and is projected to grow at a 7.66% CAGR through 2031.

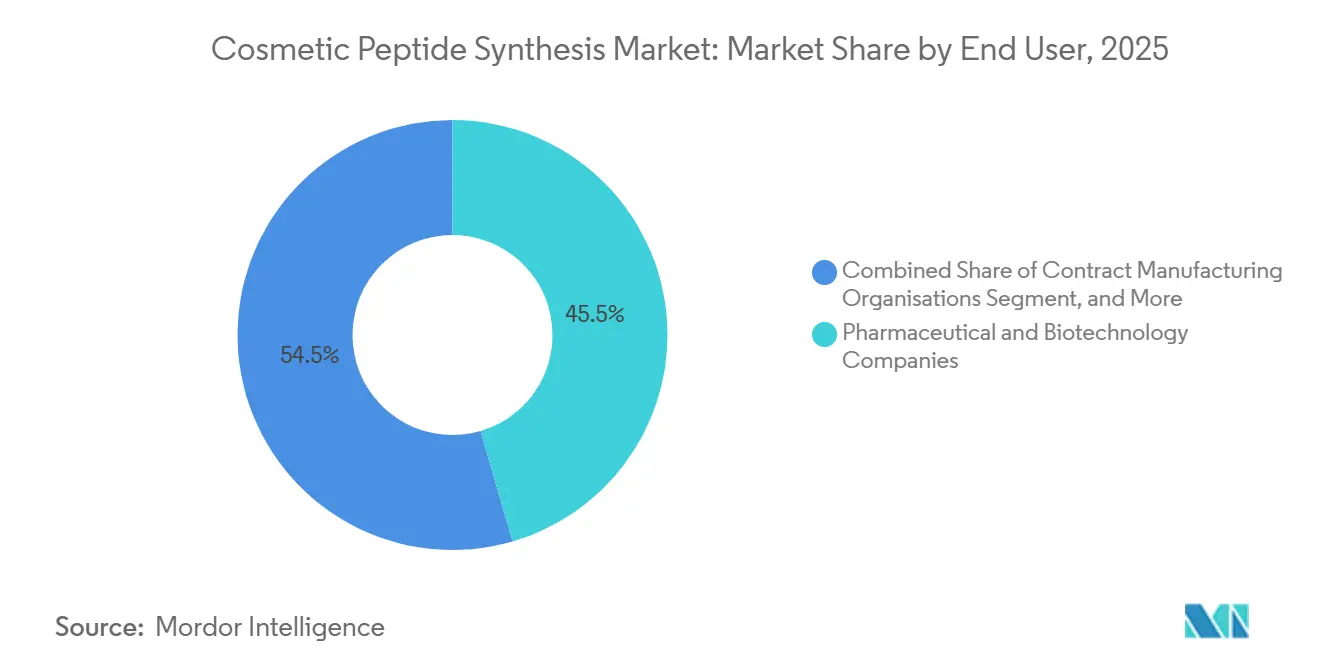

- By end user, pharmaceutical and biotechnology companies commanded 45.48% share in 2025, but contract manufacturing organizations are projected to register the highest 8.06% CAGR to 2031.

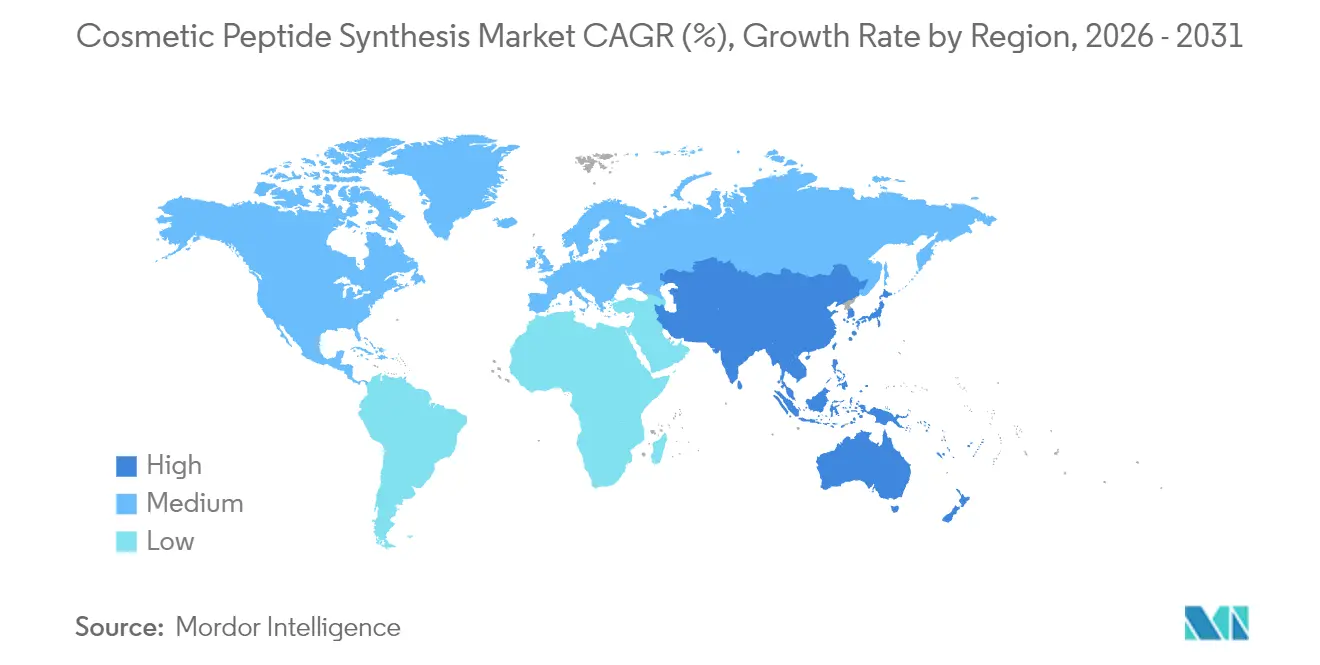

- By geography, North America retained a 42.84% share in 2025, whereas the Asia-Pacific is forecast to expand at a 9.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cosmetic Peptide Synthesis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Biomimetic Anti-Aging Actives | +1.8% | Global, early uptake in North America & Europe | Medium term (2-4 years) |

| Lower-Cost High-Throughput SPPS Automation | +1.5% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Premiumization of South-Korean Peptide Serums | +0.9% | South Korea & Japan, diffusing into Southeast Asia | Medium term (2-4 years) |

| Brand-Supplier Co-Development of Signature Peptides | +0.7% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| AI-Driven Sequence Design Shortening R&D Cycles | +1.2% | North America & Europe, South Korea | Medium term (2-4 years) |

| Fast-Track Functional-Cosmetic Regulations | +0.6% | South Korea, Japan, selective EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biomimetic Anti-Aging Actives

Clinical evidence shows palmitoyl pentapeptide-4 can reduce wrinkle depth by up to 20% within twelve weeks without the irritation seen with topical retinoids. Acetyl hexapeptide-8 attenuates muscle contraction by blocking the SNARE complex, delivering visible smoothing comparable to low-dose botulinum toxin. Copper-GHK peptides further remodel extracellular matrix by activating metalloproteinases, improving dermal density by 18% after four months. Brands increasingly layer signal, carrier, and enzyme-inhibitor peptides into a single product, though this strategy increases the complexity of stability testing. Regulators still treat peptides as cosmetic ingredients unless explicit structure-function claims cross the drug threshold.[1]U.S. Food and Drug Administration, “Cosmetics Regulatory Guidance,” fda.gov

Lower-Cost High-Throughput SPPS Automation

Microwave-assisted reactors have cut coupling times from hours to minutes, halving labor costs and solvent use.[2]Rui Zhou et al., “Advances in Solid-Phase Peptide Synthesis and Automation,” Nature Communications, nature.com Continuous-flow SPPS eliminates manual resin transfers and lowers solvent demand by about 40%. Contract manufacturers equipped with these platforms can supply sub-kilogram batches inside four weeks, matching the agility of small-molecule suppliers. As a result, custom peptides now reach mid-tier products priced under USD 50, a price band historically out of reach for peptide actives. ISO 22716 guidelines ensure that higher throughput does not compromise traceability or contamination control.

AI-Driven Peptide Sequence Design Shortening R&D Cycles

Protein language models and diffusion-based generators evaluate thousands of candidate sequences weekly, predicting bioactivity and skin permeation with close to 90% accuracy. Evonik’s collaboration with GenScript identified a tetrapeptide that outperformed palmitoyl pentapeptide-4 by 22% in fibroblast assays within six weeks of screening.[3]Evonik Industries, “AI-Enabled Peptide Discovery Platform,” evonik.com Reduced discovery time allows niche brands to commission proprietary actives without building in-house wet labs. Regulators have not issued peptide-specific AI guidance, so AI-generated sequences follow existing cosmetic-ingredient frameworks in the EU and U.S.

Premiumization of South-Korean Peptide Serums

South-Korean labels have popularized serums that combine PDRN with multi-functional peptides, often retailing above USD 80 per 30 mL. These products pitch peptides as “skin’s native language” and favor fermentation-derived sequences that align with clean-beauty narratives. Rising export volumes to North America and Europe show that premium peptide positioning is resonating outside Asia. South-Korean regulation classifies peptides under 50 amino acids as cosmetic ingredients, avoiding therapeutic review burdens and hastening launch timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Purification Costs Curb Mass-Market Pricing | -1.1% | Global, acute in cost-sensitive APAC & South America | Long term (≥ 4 years) |

| Batch-to-Batch Variability in Liquid-Phase Synthesis | -0.7% | APAC contract labs, less in EU & North America | Medium term (2-4 years) |

| Scrutiny of Micro-Plastic Carriers in Formulas | -0.3% | EU core, expanding to North America | Medium term (2-4 years) |

| Consumer Sensitivity to “Synthetic-Sounding” INCI Names | -0.4% | Global, most acute in clean-beauty segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Purification Costs Curb Mass-Market Pricing

Preparative HPLC can represent up to 40% of final peptide cost, mainly due to acetonitrile consumption and solvent disposal fee. Membrane-based and continuous chromatography can shave 25-35% off purification expense, but fewer than 15% of global lines have adopted them because of validation complexity. Brands aiming for mass-market price points often reduce peptide load below 0.5%, which compromises efficacy and reinforces the “luxury-only” perception around peptides.

Liquid-phase peptide synthesis (LPPS) leaves 2-8% unreacted amino acids in hydrophobic sequences, creating impurity swings of up to 12% between batches. Chinese and Indian facilities that favor LPPS report rejection rates near 10%, versus 3% for SPPS sites. Each rejected lot triggers re-formulation or inventory write-offs, adding USD 500-800 per batch in extra analytical testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Peptide Type: Signal Peptides Retain Lead as Carrier Peptides Gain Momentum

Signal peptides represented 41.82% of the cosmetic peptide synthesis market share in 2025. Continued use of palmitoyl pentapeptide-4 and palmitoyl tripeptide-1 in anti-aging creams sustains demand, while brands favor these sequences for their predictable stability profiles. Multi-vendor supply chains also support pricing discipline, limiting shortages.

Carrier peptides are forecast to post the fastest 6.43% CAGR through 2031. Copper-GHK complexes now shuttle trace elements that catalyze extracellular matrix remodeling without depending on synthetic polymers, which are now under environmental review. Formulators view carrier peptides as a route to differentiate textures and improve delivery efficiency.

Neurotransmitter-inhibitor peptides, such as acetyl hexapeptide-8, held a 23.1% share in 2025 and remain popular in expression-line serums, offering consumers a topical alternative to botulinum toxin injections. Enzyme-inhibitor peptides that block elastase and collagenase reached a significant share, with the highest uptake in urban regions where particulate pollution accelerates skin aging. Other functional peptides, including antimicrobial and pigment-modulating sequences and their use is widening into acne and hyperpigmentation products.

By Application: Anti-Aging Dominates while Hair-Care Accelerates

Anti-aging maintained 48.27% of the cosmetic peptide synthesis market size in 2025. Although growth moderates in mature regions, the segment still benefits from multi-peptide stacking strategies that promise synergistic collagen stimulation.

Hair-care and scalp treatments are projected to grow at an 8.72% CAGR between 2026 and 2031. Evidence that copper-GHK can keep follicles in the anagen phase up to 22% longer is encouraging formulators to extend peptides beyond facial care. Whitening and brightening products held a 16.8% share, driven by oligopeptide-68 and nonapeptide-1, which offer tyrosinase inhibition without the regulatory baggage of hydroquinone. Barrier-repair creams and moisturizers captured 14.3% share, helped by peptides that lower trans-epidermal water loss. Eye-care and sun-care collectively make up a modest but rising slice, with DNA-repair peptides under investigation for after-sun recovery.

By Synthesis Technique: SPPS Dominates, Recombinant Platforms Surge

Solid-phase peptide synthesis accounted for 61.91% of 2025 revenue and remains the default for sequences under 30 amino acids, thanks to automated platforms that deliver ≥98% purity in 4 weeks. The cosmetic peptide synthesis market size for SPPS is projected to keep expanding, though its overall share will gradually erode.

Recombinant and cell-free biosynthesis, growing at a 7.45% CAGR, benefits from lower solvent use and alignment with “green chemistry” targets. Liquid-phase peptide synthesis retains relevance for very short sequences, but its share is constrained by batch-quality issues. Hybrid or fragment-condensation routes remain a niche for cyclic or highly hydrophobic peptides that challenge standard SPPS.

By Purity Grade: ≥98% Specifications Gain Retail Preference

The ≥98% cosmetic-grade tier held 51.78% share in 2025 and is forecast to expand at a 7.66% CAGR as premium brands highlight analytical certificates on product pages. Retailers increasingly require proof of high purity to minimize contamination risk, pushing mid-tier brands toward the 95-98% band. Industrial and R&D grades below 95% cover pilot studies and cost-sensitive formulations but are unlikely to grow beyond a 15% share because efficacy claims weaken at low inclusion rates.

By End User: Pharma & Biotech Lead, CMOs Outpace on Growth

Pharmaceutical and biotechnology firms leveraged existing peptide drug know-how to hold a 45.48% share in 2025. However, contract manufacturing organizations will post the fastest CAGR of 8.06%, reflecting brand reluctance to invest in cGMP infrastructure. CMOs equipped with microwave-assisted SPPS and continuous-flow lines deliver sub-kilogram lots in under a month, attracting indie and prestige brands alike. Academic labs and formulation houses form the balance, using web-based configurators to order sample quantities for proof-of-concept studies.

Geography Analysis

North America held 42.84% market share of the cosmetic peptide synthesis market in 2025, anchored by cGMP facilities in New Jersey, California, and Massachusetts. Regional growth of 4.8% CAGR will be underpinned by AI-driven design tools, which are disproportionately headquartered in the United States. Canada mirrors U.S. regulatory frameworks, smoothing cross-border supply, while Mexico’s growth is strongest in premium department stores that favor high-purity imports.

Germany leads consumption thanks to in-house peptide units at BASF and Evonik, while France benefits from luxury-brand demand. The United Kingdom, Italy, and Spain follow, each showing mid-single-digit growth as peptides replace retinoids in sensitive-skin regimens.

Asia-Pacific is the fastest-growing region, with a 9.36% CAGR through 2031. China hosts expanding recombinant-biosynthesis hubs in Shenzhen and Shanghai, while South Korean brands collaborate with local suppliers to launch signature hexapeptides. Japan’s regulatory designation of “functional cosmetics” allows structure-function claims once ingredients pass safety review, helping local brands market efficacy data. India and Southeast Asia show double-digit growth driven by rising discretionary incomes, though price sensitivity still favors lower inclusion rates.

High per-capita spending and tourism retail bolster demand, but limited local manufacturing means most peptides enter as finished products. South Africa represents the region’s secondary growth node, focused on remedies for hyperpigmentation and sun damage.

Brazil dominates, supported by local brands adding peptides to anti-aging creams designed for sun-exposed climates. Argentina and Chile follow, though currency volatility can disrupt import pipelines. Regional regulators such as ANVISA require safety dossiers but no pre-market efficacy approval, enabling relatively swift launches.

Competitive Landscape

The cosmetic peptide synthesis market is moderately fragmented. Players compete on purity guarantees, sequence customization, and speed. Bachem’s 2026 Swiss plant expansion added microwave reactors that trim production timelines by 35%. PolyPeptide’s continuous-flow installation in Sweden reduces solvent use by 40%. BASF has commercialized fermentation-derived palmitoyl tripeptide-1, lowering per-gram costs by 38% while meeting clean-beauty claims.

AI partnerships are reshaping the landscape. Evonik’s alliance with GenScript screens 10,000 sequences weekly, bringing bespoke actives to market in under a year. Smaller firms such as Creative Peptides use automated configurators to quote and ship sub-kilogram lots within three weeks, attracting indie brands. Ingredient majors Givaudan and Croda are vertically integrating synthesis capacity to offer turnkey solutions from sequence ideation to finished formula testing.

Compliance remains non-negotiable. ISO 22716 certification and cosmetic GMP audits are routine, but leading brands now also request Ecocert or COSMOS validation. Consequently, suppliers are investing in recombinant platforms that minimize acetonitrile discharge and meet environmental audit requirements. The pivot to greener production is likely to tighten supply among firms still reliant on solvent-intensive chromatography.

Cosmetic Peptide Synthesis Industry Leaders

BASF SE

Croda International plc (Sederma)

Symrise AG

Givaudan SA (Active Beauty)

DSM-Firmenich (Pentapharm)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: L’Oréal and IBM entered an AI-powered formulation partnership to develop sustainable, skin-type-specific peptide actives, cementing digital innovation as a pillar of ingredient R&D.

- September 2024: SK Pharmteco confirmed a USD 260 million, eight-line peptide facility in Sejong City, South Korea, to serve rising cosmetic-grade demand and create 300+ jobs.

- August 2024: Kenvue unveiled the Neutrogena Collagen Bank serum featuring micro-peptide technology claimed to be half the size of conventional anti-aging peptides, positioning the brand at the forefront of molecular efficacy storytelling.

- July 2024: CordenPharma announced a EUR 900 million expansion across US and European peptide platforms, adding capacity flexible enough for both commercial and clinical volumes, thereby reinforcing global supply security.

- July 2024: Givaudan finalized the purchase of b.kolormakeup & skincare, enriching its active beauty peptide lines with enhanced formulation and sensory capabilities.

Global Cosmetic Peptide Synthesis Market Report Scope

As per the scope of the report, cosmetic peptides are a unique class of highly active and specific pharmaceutical compounds, molecularly poised between small molecules and proteins yet biochemically and therapeutically diverse from both. Bioactive peptides have been widely used in cosmetics to provide whitening, anti-aging, and skin repair effects.

The Cosmetic Peptide Synthesis Market Report is Segmented by Peptide Type (Signal Peptides, Neurotransmitter Inhibitor Peptides, Carrier Peptides, Enzyme Inhibitor Peptides, Other Functional Peptides), Application (Anti-aging, Whitening & Brightening, Barrier Repair & Moisturising, Hair-care & Scalp Treatments, Eye-care Products, Sun-care & After-sun), Synthesis Technique (Solid-Phase Peptide Synthesis, Liquid-Phase Peptide Synthesis, Hybrid/Fragment Condensation, Recombinant/Cell-free Biosynthesis), Purity Grade (≥98% Cosmetic Grade, 95-98% Cosmetic Grade, <95% Industrial/R&D Grade), End User (Pharmaceutical & Biotechnology Companies, Contract Manufacturing Organisations, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Signal Peptides |

| Neurotransmitter Inhibitor Peptides |

| Carrier Peptides |

| Enzyme Inhibitor Peptides |

| Other Functional Peptides |

| Anti-aging |

| Whitening & Brightening |

| Barrier Repair & Moisturising |

| Hair-care & Scalp Treatments |

| Eye-care Products |

| Sun-care & After-sun |

| Solid-Phase Peptide Synthesis (SPPS) |

| Liquid-Phase Peptide Synthesis (LPPS) |

| Hybrid / Fragment Condensation |

| Recombinant / Cell-free Biosynthesis |

| ≥ 98 % Cosmetic Grade |

| 95 – 98 % Cosmetic Grade |

| < 95 % Industrial / R&D Grade |

| Pharmaceutical & Biotechnology Companies |

| Contract Manufacturing Organisations (CMOs) |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Peptide Type | Signal Peptides | |

| Neurotransmitter Inhibitor Peptides | ||

| Carrier Peptides | ||

| Enzyme Inhibitor Peptides | ||

| Other Functional Peptides | ||

| By Application | Anti-aging | |

| Whitening & Brightening | ||

| Barrier Repair & Moisturising | ||

| Hair-care & Scalp Treatments | ||

| Eye-care Products | ||

| Sun-care & After-sun | ||

| By Synthesis Technique | Solid-Phase Peptide Synthesis (SPPS) | |

| Liquid-Phase Peptide Synthesis (LPPS) | ||

| Hybrid / Fragment Condensation | ||

| Recombinant / Cell-free Biosynthesis | ||

| By Purity Grade | ≥ 98 % Cosmetic Grade | |

| 95 – 98 % Cosmetic Grade | ||

| < 95 % Industrial / R&D Grade | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Manufacturing Organisations (CMOs) | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the cosmetic peptide synthesis market by 2031?

What is the forecast value of the cosmetic peptide synthesis market by 2031?

Which peptide category is expected to grow the fastest through 2031?

Carrier peptides are projected to register the highest 6.43% CAGR.

Why are contract manufacturing organizations gaining share?

Brands prefer outsourcing to CMOs that offer four-week turnaround times, validated GMP suites, and cost flexibility.

How is recombinant biosynthesis impacting peptide production?

Fermentation-based methods cut solvent use and lower per-gram costs by about 40%, aligning with clean-beauty goals.

Which region will experience the quickest growth?

Asia-Pacific is forecast to expand at a 9.36% CAGR through 2031, led by China and South Korea.

Page last updated on: