Protein Sequencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Protein Sequencing Market Analysis by Mordor Intelligence

The Protein Sequencing market size is expected to grow from USD 1.67 billion in 2025 to USD 1.74 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 4.35% CAGR over 2026-2031.

Demand growth reflects an ecosystem shift from classical mass-spectrometry workflows toward single-molecule approaches that reveal protein variants and post-translational modifications in real time. Pharmaceutical companies deepen adoption to accelerate target validation, while Contract Research Organizations (CROs) capture incremental outsourcing budgets. Platform developers bundle instruments with consumables and analytics software, turning reagent sales into recurring revenue streams that cushion price pressure on hardware. North America retains spending leadership through entrenched R&D infrastructure, yet Asia-Pacific outpaces all regions in growth as local biopharma investment rises and regulatory pathways align with global norms.

Key Report Takeaways

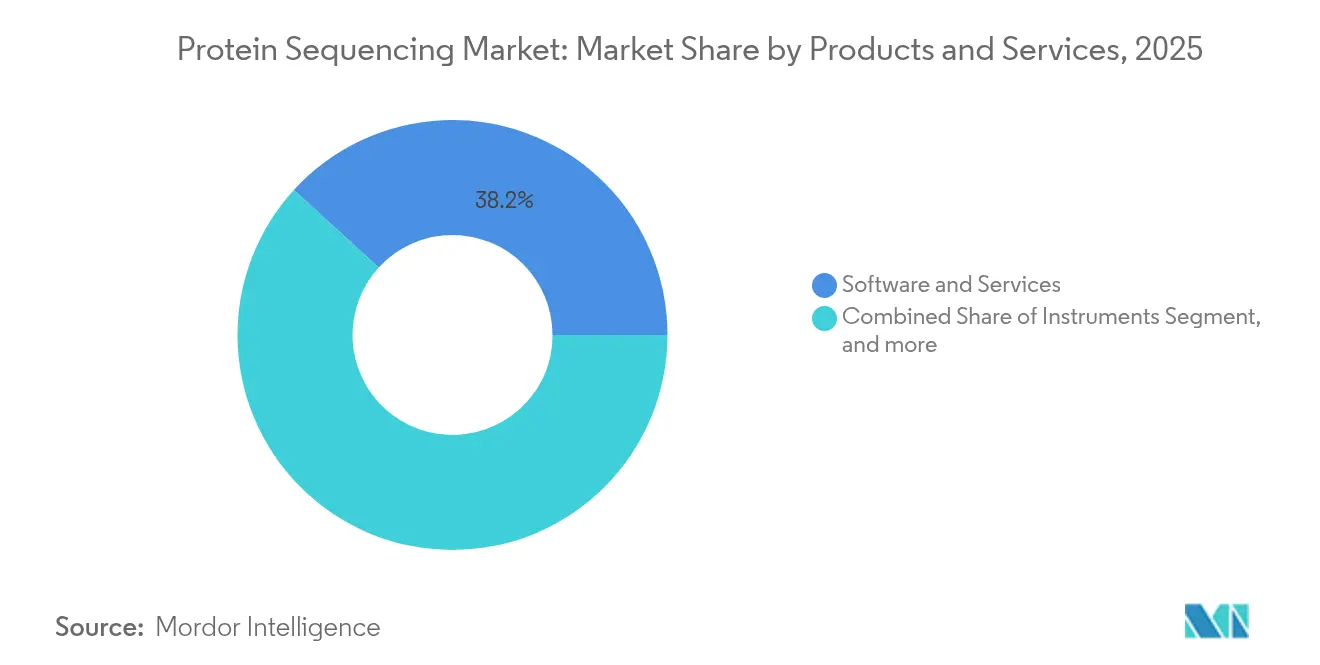

- By products & services, software & services held 38.21% revenue share in 2025; reagents & consumables is expanding at a 7.50% CAGR through 2031.

- By application, biotherapeutics quality control & discovery captured 36.05% of protein sequencing market share in 2025, while synthetic biology & cell-free systems is projected to climb at a 12.08% CAGR to 2031.

- By end user, pharmaceutical companies commanded 53.05% share of the protein sequencing market size in 2025, whereas CROs record the fastest 8.45% CAGR during the forecast period.

- By geography, North America led with a 43.12% share in 2025; Asia-Pacific is set to advance at an 8.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Sequencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Advancements in sequencing technologies | +1.8% | Global, led by North America & Asia-Pacific | Short term (≤ 2 years) |

| Growing focus on target-based drug development | +1.1% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increased R&D funding in proteomics | +0.9% | Global, particularly North America & China | Long term (≥ 4 years) |

| Expanding applications in biotherapeutics | +1.3% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Decreasing cost of sequencing services | +0.7% | Global, faster uptake in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Escalating burdens of cancer, cardiovascular disorders, and neurodegeneration push healthcare systems to augment genomic data with proteomic insight. The UK Biobank initiated a 2025 study profiling 5,400 proteins across 600,000 samples, laying the groundwork for large-scale correlation between circulating proteins and clinical outcomes.[1]UK Biobank, “UK Biobank proteomics study transforms population health research,” ukbiobank.ac.uk Early-stage cancer screening shows pronounced benefit: plasma-based multi-cancer tests reached 93% sensitivity in men and 84% in women, eclipsing many current modalities. Combining proteome, genome, and imaging layers fuels AI models that sharpen risk prediction and drive demand within the protein sequencing market. Pharmaceutical companies, already holding 53.78% share, integrate these datasets to prioritise therapeutic targets and stratify trial populations.

Advancements in Sequencing Technologies

Single-molecule innovations are redefining technical limits. Oxford Nanopore Technologies reported >98% accuracy in identifying protein variants with a prototype pore-based system.[2]Oxford Nanopore Technologies, “Advances in protein sequencing accuracy,” nanoporetech.comQuantum-Si commercialised this vision through the Platinum Pro benchtop sequencer launched in 2025, coupling semiconductor chips with machine-learning-guided base-calling. On the software side, deep-learning models such as InstaNovo now deliver 90.5% peptide sequencing accuracy from sparse amino-acid reads, dramatically shortening analysis cycles. Increased analytic power underpins the 7.63% CAGR rise in reagent demand as users run larger sample volumes to exploit newfound resolution.

Growing Focus on Target-Based Drug Development

Strategic pipelines prioritise protein structure and function rather than gene expression alone. Generate Biomedicines raised USD 700 million to design therapeutic proteins with generative AI, advancing two molecules to clinical testing by 2025. The US FDA refined guidance on recombinant biologics, clarifying requirements for sequence validation and comparability studies.[3]Food and Drug Administration, “Guidance for industry: recombinant therapeutic proteins,” fda.gov Cell-free protein synthesis accelerates optimisation loops and sustains a 12.32% CAGR within synthetic-biology applications. Researchers also deploy computational design to craft enzymes showing 100-fold efficiency gains over previous AI efforts, broadening the protein sequencing market scope beyond analytics into engineering.

Increased R&D Funding in Proteomics

Cross-sector funding has multiplied. Fourteen biopharma companies bankroll the UK Biobank proteomics project, underscoring shared interest in population-scale protein data. Glyphic Biotechnologies secured USD 39.2 million to advance a single-molecule platform, illustrating investor confidence in next-generation approaches. Academic-industry partnerships flourish; Northwestern Proteomics Center adopted Quantum-Si’s chip-based system to interrogate proteoforms in neurodegenerative disease. Sustained capital flows enable technology maturation and expand the protein sequencing market user base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of instruments and services | -1.4% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Complexity of data interpretation | -0.8% | Global, steeper in regions with limited expertise | Medium term (2-4 years) |

| Regulatory hurdles | -0.6% | Primarily North America & Europe | Medium term (2-4 years) |

| Limited standardisation across platforms | -0.5% | Global, affects interoperability | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Instruments and Services

Front-end capital remains a gating factor. Flagship single-molecule sequencers list upwards of USD 500,000 per unit, while consumables can add USD 50 per sample for deep proteome coverage. The FDA’s 2024 staff reductions inflated review timelines, indirectly raising compliance costs for newcomers. These economics motivate drug developers to engage CROs, whose 8.59% CAGR reflects an outsourcing preference that tempers direct instrument sales. Vendors counter by offering subscription financing and reagent rental plans, yet affordability gaps persist in price-sensitive markets.

Complexity of Data Interpretation

Proteome data sets dwarf genomic counterparts in scale and heterogeneity. While protein language models improve annotation fidelity, limited labelled data and model explainability impede adoption. Organisations lacking bioinformatics talent face bottlenecks even after hardware acquisition, propelling Software & Services to 38.83% market share. Platform suppliers now deliver turnkey pipelines that integrate sample prep, sequencing, and AI analytics, though mastering downstream biological context still demands expert oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Software Integration Drives Platform Adoption

The segment generated the largest contribution to the protein sequencing market in 2025, with Software & Services accounting for 38.21% of revenue. Instruments remain essential, but value increasingly migrates to cloud analytics subscriptions that translate complex spectra into actionable readouts. Growth accelerates in Reagents & Consumables, which expand at a 7.50% CAGR as single-molecule workflows rely on branded chips and chemistry kits. Integrated ecosystems create vendor lock-in that stabilises recurring turnover and underpins predictable cash flows for suppliers.

Customers now prioritise end-to-end solutions that bundle assay kits, AI algorithms, and workflow automation. Developers embed real-time quality metrics and adaptive chemistries, shortening run times and reducing failed experiments. Over the forecast window, instrument margins may compress as competition rises, while software-as-a-service models and reagent volumes sustain profitability. As a result, the protein sequencing market is expected to experience a broader shift toward service-centred revenue without diluting ongoing hardware innovation.

By Application: Synthetic Biology Emerges as Growth Engine

Synthetic Biology & Cell-free Systems is the fastest-expanding use case, growing at 12.08% CAGR and steadily enlarging its share within the protein sequencing market. Demand is driven by rapid prototyping of therapeutic enzymes and vaccine antigens, which benefit from cell-free platforms that bypass cloning cycles and expedite functional testing. Biotherapeutics Quality Control & Discovery preserved the leading 36.05% share due to regulatory mandates for sequence confirmation and impurity profiling across monoclonal antibodies, fusion proteins, and bispecific formats.

Breakthroughs in enzyme engineering demonstrate why single-molecule accuracy matters: computational redesign achieved 100-fold catalytic gains relative to earlier AI-guided efforts, validating proteome sequencing as a critical feedback tool. Growing sensitivity further enables biomarker discovery in oncology and neurodegeneration, extending the technology’s impact into clinical diagnostics. Overall, the protein sequencing market size for application segments exhibits a characteristic barbell pattern, pairing steady demand in quality control with outsized growth from synthetic biology.

By End User: CROs Capitalize on Outsourcing Trends

Pharmaceutical companies retained a dominant 53.05% share of the protein sequencing market in 2025, underpinned by pipeline breadth and budget size. Yet CROs register the quickest 8.45% CAGR as they absorb tasks that require specialised personnel and high-capex instruments. This shift reflects internal cost-containment priorities and the desire for variable rather than fixed R&D expenditure.

Academic institutes extend capabilities through shared core facilities but frequently partner with CROs for large-scale studies, mirroring biopharma’s outsourcing behaviour. Biotechnology startups leverage CRO-led services to access proteomics early without spending scarce venture capital on equipment. Over time, the market may bifurcate between integrated R&D giants with in-house platforms and a services layer that blankets smaller innovators. Both cohorts, however, will continue to drive reagent consumption and software utilisation, sustaining expansion of the overall protein sequencing market.

Geography Analysis

North America generated 43.12% of revenue in 2025, benefiting from deep venture capital pools, corporate R&D clustering, and established regulatory pathways. Leading suppliers such as Thermo Fisher Scientific and Quantum-Si operate extensive manufacturing and support networks that reinforce regional dominance. Nevertheless, high labour and operational costs temper incremental growth, resulting in a mid-single-digit CAGR across the outlook period.

Asia-Pacific is the fastest mover with an 8.68% CAGR, propelled by government initiatives that underwrite local biomanufacturing capacity and streamline ethics review for multi-centre studies. China finances large-scale biotechnology parks, while Japan, South Korea, and India expand academic-industry collaborations. The influx of multinational clinical trials stimulates demand for high-throughput proteomics, enlarging the regional protein sequencing market.

Europe exhibits steady progress, anchored by long-standing proteomics centres and pan-EU funding mechanisms such as Horizon Europe. Harmonised documentation standards facilitate cross-border sample exchange, which enables consortium-driven discovery efforts. Markets in South America, the Middle East, and Africa remain emergent but show promise as diagnostics programmes expand and public health agencies recognise the value of protein-level surveillance. Collectively, geographic diversification cushions suppliers against cyclical spending patterns and broadens the global protein sequencing market footprint.

Regulatory Landscape

Regulatory oversight for protein and peptide sequencing is anchored in biotherapeutic quality frameworks that require robust identity confirmation, impurity profiling, and characterization of post-translational modifications. Global development and CMC packages align to ICH Q6B specifications and test procedures for biologics, while the US FDA maintains product-specific guidance that shapes documentation for recombinant constructs.

In Europe, the EMA Guideline on the Development and Manufacture of Synthetic Peptides (EMA/CHMP/CVMP/QWP/367182/2025) entered into force in June 2026, elevating analytic characterization and impurity-control requirements for peptide medicines. Across major agencies there is convergence toward high-resolution readouts, including LC-MS/MS for structural confirmation and PTM mapping, driving demand for validated workflows, traceable data handling, and cross-platform assay standardization used in quality control and comparability exercises.

Competitive Landscape

The competitive field features a mix of diversified instrument vendors and venture-backed specialists. Thermo Fisher’s USD 3.1 billion purchase of Olink in 2024 extended its reach into proximity-based protein assays and signalled rising consolidation among incumbents. Agilent, Waters, and Bruker defend share through incremental mass-spectrometry upgrades and bundled informatics. Emerging entrants including Quantum-Si, Encodia, and Erisyon focus on semiconductor chips, fluorescent barcodes, or time-of-flight nanopore readouts that promise single-molecule precision.

Strategic alliances proliferate: Quantum-Si signed distribution pacts with Avantor to widen laboratory access across North America. Meanwhile, AI platform providers court hardware makers to embed predictive algorithms directly within run control software, sharpening competitive differentiation. Price competition intensifies in mid-throughput instruments where multiple players now offer comparable specifications. Yet high-end single-molecule systems remain differentiated by chemistry fidelity, throughput, and ecosystem maturity, giving first movers a defensible moat.

Going forward, success will hinge on integrated value propositions that knit instruments, reagents, and cloud analytics into cohesive user experiences. Suppliers able to flatten learning curves and lower total cost of ownership are poised to capture incremental share. Venture funding momentum and technological breakthroughs suggest additional mergers or strategic partnerships as companies seek scale and complementary capabilities within the protein sequencing market.

Protein Sequencing Industry Leaders

Agilent Technologies, Inc.

SGS SA

Shimadzu Corporation

Thermo Fisher Scientific Inc.

Selvita SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity arises from multiomics-scale proteomics programs that convert protein readouts into routine, high-throughput data streams, expanding demand for standardized sample preparation, sequencing reagents, and analysis software. Illumina’s 2025 global availability of Illumina Protein Prep, paired with the UK Biobank pilot program to analyze 50,000 samples on NovaSeq X Plus, demonstrates a population-scale protein measurement template that complements established genomics infrastructure.

De novo and antibody sequencing capacity expands through continued innovation. XA-Novo work in 2026 with MS-based antibody reconstruction and multi-enzymatic digestion demonstrates growing demand for software, spectral libraries, and tailored informatics that reduce interpretation burden. Platform upgrades in single-molecule ecosystems, such as Quantum-Si’s V4 Sequencing Kit launched in 2025 adding glycine recognition and 24-plex barcoding, point to ongoing expansion in proteome coverage and multiplexing, strengthening the business case for recurring consumables and outsourced sequencing services where instrument costs constrain adoption.

Recent Industry Developments

- July 2026: Agilent expanded its Altura chromatography portfolio with inert size exclusion and PLRP-S column options designed for biotherapeutic analysis. The additions support higher-confidence separations for complex biologics, strengthening end-to-end workflows that connect upstream sample preparation to downstream protein characterization and sequencing-adjacent analytics.

- September 2025: Quantum-Si launched the V4 Sequencing Kit for its Platinum and Platinum Pro instruments, adding glycine recognition and enabling 24-plex barcoding. The kit expands proteome coverage per run and improves throughput economics for labs adopting single-molecule protein sequencing workflows.

- April 2024: Thermo Fisher Scientific completed its acquisition of Olink, extending its protein-analysis portfolio into proximity extension assay-based proteomics. The deal broadened Thermo Fisher's position across complementary protein measurement modalities that feed discovery and translational workflows and can increase cross-selling into pharma and academic proteomics users.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue earned from protein sequencing solutions used to determine amino acid sequences of proteins or peptides. It includes instruments, reagents and consumables, and software and services that support sample prep, sequencing runs, and interpretation across research and applied settings.

Scope exclusions: We exclude routine peptide mapping done only as a secondary quality control step when it is not sold or priced as a protein sequencing workflow.

Segmentation Overview

- By Products & Services

- Instruments

- Mass Spectrometry

- Edman Degradation Systems

- Single-Molecule Sequencers

- Reagents & Consumables

- Software & Services

- Instruments

- By Application

- Biomarker Discovery

- Protein Engineering Studies

- Biotherapeutics QC & Discovery

- Synthetic Biology & Cell-free Systems

- Others

- By End User

- Pharmaceutical Companies

- Biotechnology Firms

- Contract Research Organizations

- Academic & Research Institutes

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and supply signals that can be checked in public data, then narrowing them to what is actually used for protein sequencing. We typically review sources such as NIH and other public research-funding award databases, FDA and ClinicalTrials.gov activity for biologics and related R&D, and OECD or World Bank indicators that help explain lab spending capacity across regions.

To keep the model aligned with real commercial behavior, we also use company annual reports, investor presentations, and product documentation to understand portfolio boundaries and revenue drivers. Patent databases are reviewed to see where sequencing workflows are being developed and adopted, and trade statistics plus shipment-level import-export subscriptions are used selectively to sanity check instrument movement and pricing ranges. These desk sources are not exhaustive, and many other public references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to convert desk signals into usable assumptions, especially around what buyers actually purchase as sequencing, how often workflows repeat, and where spending is shifting between kits, instruments, and services. We speak with a mix of lab decision makers, procurement teams, and technical experts across biopharma, academic centers, and service providers, with coverage balanced across major regions so regional demand and pricing differences are not averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 16% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

The sizing build starts with a top-down reconstruction of addressable spend by linking proteomics and sequencing related lab activity to what is specifically purchased for protein sequencing workflows, then allocating it using region-level adoption signals. Once that structure is set, totals are cross-checked with selective bottom-up approximations such as sampled average selling price ranges for key consumables, instrument placement logic, and service throughput assumptions from interviews, which are then used to adjust any over- or under-statements.

Inputs used in the model include the pace of biologics and protein engineering programs, public funding trends for proteomics research, instrument replacement and upgrade cycles, the mix shift between reagents and consumables versus services, and typical workflow run volumes by end user type. Where direct volume data is missing, gaps are handled by using proxy indicators that can be validated in interviews, followed by conservative range setting until consistency is reached.

For forecasting, scenario analysis is used with a central case built from expert consensus on adoption and pricing progression, then stress-tested for faster automation uptake or slower capital spending years. Assumptions are kept traceable so a client can follow how each driver moves the final number.

Data Validation & Update Cycle

Outputs are checked against independent signals like funding direction, instrument shipment patterns, and the observed split of spend between consumables and services, before figures are finalized. If a region shows an unusual jump, the drivers are re-reviewed and we re-contact relevant experts when the desk evidence is not strong enough.

A second analyst reviews the logic, inputs, and calculations, and then variances are discussed until the model behaves consistently across regions and years. Reports are refreshed annually, and interim updates are made when material events affect demand, pricing, or availability. Before delivery, a final pass is done so the client receives the latest updated view.

Mordor Intelligence's Protein Sequencing Market Sizing Compared With Other Published Estimates

Published market sizes for protein sequencing can look far apart because the boundary of what counts as sequencing is not consistent, and because different studies use different base years and price assumptions. Differences also show up when one estimate leans more on long-range projections, and another stays closer to near-term purchasing signals.

Instrument shipment direction, consumables pull-through expectations, and the services share seen in interviews are the checks that keep Mordor Intelligence's 2025 market size tied to sequencing-specific workflows rather than broader proteomics activity. The remaining spread usually comes from whether routine peptide mapping is counted as sequencing revenue, how quickly average prices are assumed to decline, and how often models are refreshed when workflow automation changes the mix.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.67 B (2025) | |

| Global Consultancy A | USD 1.43 B (2024) | Uses an earlier base year and a shorter forecast window, and the boundary is often interpreted more tightly around recognized product and service categories, which can undercount emerging software and workflow related services in some regions. |

| Industry Publisher B | USD 2.12 B (2025) | The higher value is consistent with a broader revenue boundary that can pull in adjacent proteomics activities and more aggressive assumptions on product dominance and end-use expansion, which increases the starting year total. |

Across the three figures, the main driver of the gap is not math complexity, it is scope control and how pricing and adoption are anchored to observable signals. By keeping inclusions clear, validating run-rate and spend mix with interviews, and then rechecking against external activity indicators, the estimate stays practical to replicate and easier to track over time.

Key Questions Answered in the Report

What is the current value of the protein sequencing market?

The protein sequencing market size is USD 1.74 billion in 2026 and is projected to reach USD 2.16 billion by 2031.

Which segment is expanding fastest within the market?

Synthetic Biology & Cell-free Systems leads growth with a 12.08% CAGR through 2031.

Why are Contract Research Organizations gaining ground?

CROs grow at 8.45% CAGR because they offer specialised expertise and eliminate the need for drug developers to invest in high-cost instruments.

Which region holds the largest market share?

North America accounts for 43.12% of 2025 revenue owing to entrenched R&D infrastructure and a dense supplier base.

What technology trends are reshaping the competitive landscape?

Single-molecule sequencing, AI-powered data interpretation, and integrated instrument-software ecosystems drive differentiation and vendor consolidation.

How are high instrument costs being addressed?

Vendors introduce subscription financing, reagent rental models, and cloud-based analytics bundles to lower upfront capital and operational barriers.

Page last updated on: